gesch.ftsber versag engl 03 - ruv.de r+v versicherung ag r+v komposit holding gmbh r+v personen...

TRANSCRIPT

R+V Versicherung AGAnnual Report

Taunusstrasse 1, 65193 Wiesbaden, Germany, Tel. +49 (0) 611 533-0

Registered at the Wiesbaden Local Court, HRB 7934

Presented to the Ordinary General Meeting on May 6, 2004

20032003

2

R+VVersicherung

AG

R+VKompositHoldingGmbH

R+VPersonenHoldingGmbH

KRAVAG-LOGISTIC

Versicherungs-AG

R+VKranken-

versicherungAG

R+VLuxembourg

Lebensversiche-rung S.A.

Assimoco VitaS.p.A.,Italy

AssimocoS.p.A.,Italy

R+VPensions-

fondsAG

KRAVAG-ALLGEMEINE

Versicherungs-AG

R+VAllgemeine

VersicherungAG

KU FilarS.A.,

Poland

R+VPoistóvna

a.s.,Slovakia

R+VRechtsschutz-versicherung

AG

R+VLebens-

versicherungAG

DomesticCompanies

InternationalCompanies

R+VPensions-

versicherunga. G.

R+VLebens-

versicherunga. G.

VereinigteTier-

versicherunga. G.

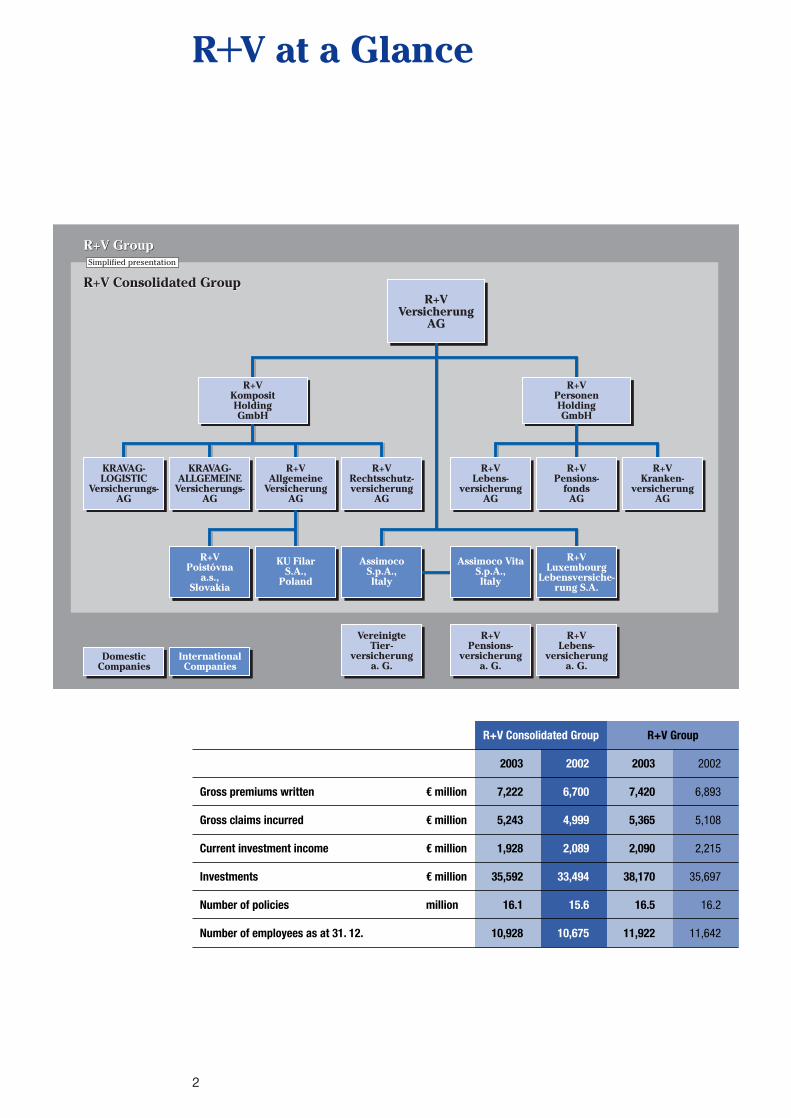

R+V Group

R+V Consolidated Group

Simplified presentation

R+V Consolidated Group

R+V Group

R+V Consolidated Group R+V Group

2003 2002 2003 2002

Gross premiums written € million 7,222 6,700 7,420 6,893

Gross claims incurred € million 5,243 4,999 5,365 5,108

Current investment income € million 1,928 2,089 2,090 2,215

Investments € million 35,592 33,494 38,170 35,697

Number of policies million 16.1 15.6 16.5 16.2

Number of employees as at 31. 12. 10,928 10,675 11,922 11,642

R+V at a Glance

3

Management Report 4

Proposal on the Appropriation of Profits 27

Annual Financial Statements 2003Balance Sheet 30Income Statement 34Notes

Accounting policies 37List of Shareholdings 40Notes to the Balance Sheet 42Notes to the Income Statement 46Other Information 47

Auditors’ Report 50

Report of the Supervisory Board 51

Content

Management Report

R+V Versicherung AG acts as both the parent company of the R+V Group and thereinsurer for the Group’s direct insurancecompanies. R+V Versicherung AG also operates independently on the internationalreinsurance market. The reinsurance busi-ness is primarily run from the head office inWiesbaden, Germany. The Group’s interestsin Southeast Asia are managed by its Singa-pore branch, which was established in1997.

R+V Versicherung AG’s 2003 annual finan-cial statements include all reinsurance business assumed from the R+V Groupcompanies in the 2003 calendar year. In contrast, reporting of the majority of business assumed from other domestic andforeign cedents is deferred by one year andtherefore relates to calendar year 2002.

Investment income as well as all other income and expenses relate to calendaryear 2003.

General economic situation

2003 dominated by slump in consumerspending and high unemployment –slight recovery in the fall

After a long period of stagnation, the lastquarter of 2003 showed signs of a tentativerecovery in the German economy. Grossdomestic product increased by 0.5%. Both incoming orders – especially from foreign businesses – and German industrialproduction picked up towards the end ofthe year.

However, until the fall neither the changesin incoming orders and production nor theemployment figures in the Federal Republicof Germany gave grounds for assuming aneconomic recovery – whereas in the otherwestern industrial nations a slight improve-ment got underway at the beginning of theyear. Investment levels were low, unemploy-ment rates rose even higher despite wide-ranging reform measures and the number of insolvencies reached record levels.Reduced incomes, high tax burdens anduncertainty over the future shape of thesocial security and taxation systems wereunsettling for businesses and consumersalike, who continued to invest and consumewith extreme caution.

The leading economic research institutesare viewing 2004 with guarded optimism.They anticipate a growth in gross domesticproduct of between 1.5% and 1.8%,although this is likely to come primarily fromforeign business. In the opinion of manystock market and economic analysts, neither the billions of euros in tax reliefresulting from bringing forward part of thefinal stage of tax reform, nor the labor market reforms will bring the hoped-foreconomic revival. In their opinion thereforms have not been nearly ambitiousenough.

4

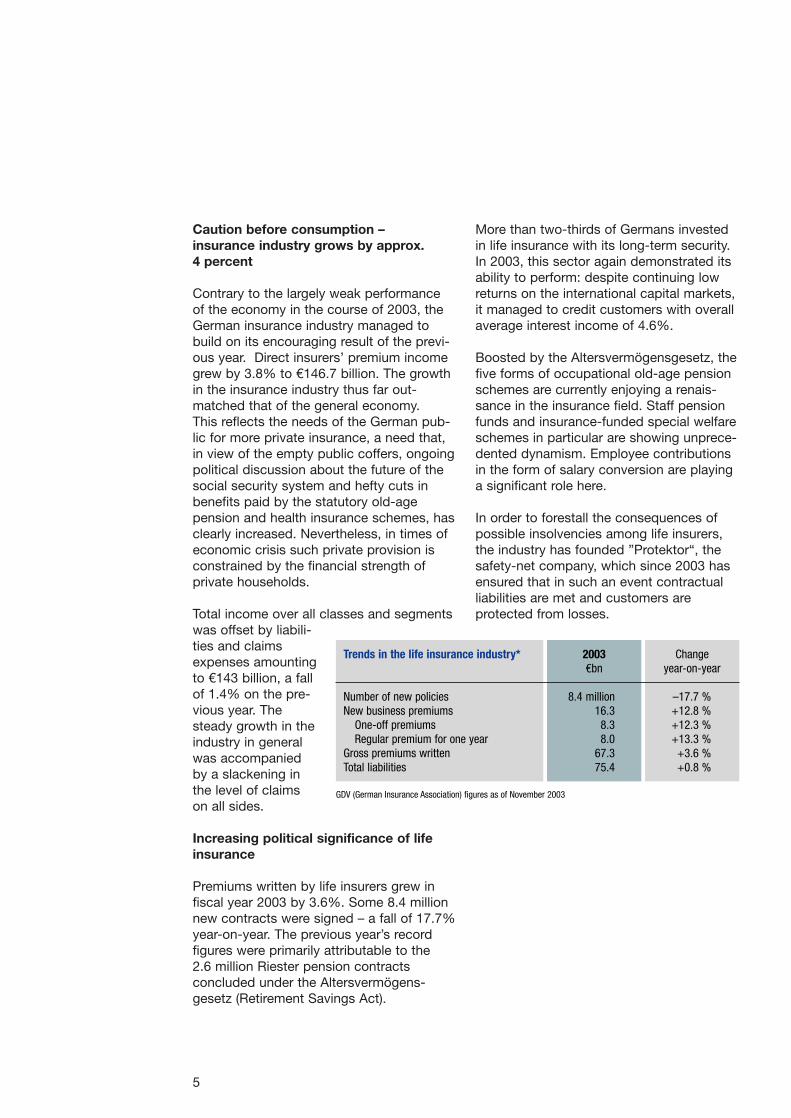

Caution before consumption – insurance industry grows by approx. 4 percent

Contrary to the largely weak performance of the economy in the course of 2003, theGerman insurance industry managed tobuild on its encouraging result of the previ-ous year. Direct insurers’ premium incomegrew by 3.8% to €146.7 billion. The growthin the insurance industry thus far out-matched that of the general economy. This reflects the needs of the German pub-lic for more private insurance, a need that,in view of the empty public coffers, ongoingpolitical discussion about the future of thesocial security system and hefty cuts inbenefits paid by the statutory old-age pension and health insurance schemes, hasclearly increased. Nevertheless, in times ofeconomic crisis such private provision isconstrained by the financial strength of private households.

Total income over all classes and segmentswas offset by liabili-ties and claimsexpenses amountingto €143 billion, a fallof 1.4% on the pre-vious year. Thesteady growth in theindustry in generalwas accompaniedby a slackening inthe level of claimson all sides.

Increasing political significance of lifeinsurance

Premiums written by life insurers grew infiscal year 2003 by 3.6%. Some 8.4 millionnew contracts were signed – a fall of 17.7%year-on-year. The previous year’s record figures were primarily attributable to the 2.6 million Riester pension contracts concluded under the Altersvermögens-gesetz (Retirement Savings Act).

More than two-thirds of Germans investedin life insurance with its long-term security.In 2003, this sector again demonstrated itsability to perform: despite continuing lowreturns on the international capital markets,it managed to credit customers with overallaverage interest income of 4.6%.

Boosted by the Altersvermögensgesetz, thefive forms of occupational old-age pensionschemes are currently enjoying a renais-sance in the insurance field. Staff pensionfunds and insurance-funded special welfareschemes in particular are showing unprece-dented dynamism. Employee contributionsin the form of salary conversion are playinga significant role here.

In order to forestall the consequences ofpossible insolvencies among life insurers,the industry has founded ”Protektor“, thesafety-net company, which since 2003 hasensured that in such an event contractualliabilities are met and customers are protected from losses.

5

Trends in the life insurance industry* 2003 Change€bn year-on-year

Number of new policies 8.4 million –17.7 %New business premiums 16.3 +12.8 %

One-off premiums 8.3 +12.3 %Regular premium for one year 8.0 +13.3 %

Gross premiums written 67.3 +3.6 %Total liabilities 75.4 +0.8 %

GDV (German Insurance Association) figures as of November 2003

Strong private health insurance growthcontinues

As in 2002, private health insurance wasanother growth driver for the insuranceindustry. Indeed, growth in premium incomeincreased from last year’s extremelyencouraging 6.3% to 7.0%. This growthwas partly due to rising numbers of insuredpersons, both for comprehensive healthinsurance and supplementary insurance. Inthe health insurance field too, it is clear thatthe public are increasingly taking mattersinto their own hands.

Motor vehicle insurance class boostsresults significantly

The encouraging performance of the prop-erty and casualty sector was primarilyattributable to the motor vehicle insurers.For the first time since 1996 they achieveda technical profit which amounted to almost€450 million.

The pleasing technical result is due to thegreatly improved earnings situation in themotor vehicle liability sector, where easingclaims pressure – both in value and in number – plus successful restructuringmeasures are expected to produce strongtechnical income. Comprehensive insur-ance, on the other hand, will show losseson final account.

Overall claims expenses for motor insur-ance fell by 3.3% to €19.7 billion. Premiumincome continued to rise, but did not matchthe growth rates of the previous year sincesignificantly fewer vehicles were registeredor reregistered in 2003.

Non-life sectors break even thanks tofewer claims and restructuring measures

Non-life insurance also did well in 2003.Claims expenses fell substantially: by18.4% to €10.1 billion after increasing by39.9% in 2002. This positive result was dueto the absence of storms, floods and hail.The restructuring measures embarked onseveral years ago also began to take effect.

6

Trends in the health insurance sector* 2003 Change€bn year-on-year

Gross premiums writtenTotal 24.7 +7.0 %

of which health insurance 22.8 +8.1 %of which long-term care insurance 1.9 –4.3 %

Benefit payments 16.1 +5.8 %

GDV (German Insurance Association) figures as of November 2003

Good weather is good news for propertyand casualty insurers

After a year of exceptionally severe lossesin 2002, property and casualty insurers suffered no major losses from natural disasters in fiscal year 2003 and the situa-tion has eased noticeably as a result.Claims expenses dropped by 6.1% to €40.7 billion. The combined ratio fell to encouraging 97.0%. Thanks to the lesscapricious behavior of the weather, propertyand casualty insurers, who lost €2.1 billionthe previous year, are now expected to record a technical profit of around €1.5 billion.

On the income side, premium growthslipped slightly due to the effect of theeconomy. Gross premiums written grew by 2.8% to €52.9 billion.

As a result, claims expenses in all sub-classes were lower than premium incomefor the first time for many years. The com-bined ratios for the individual classes ofnon-life business also declined year-on-yearand are now around the hundred percentmark. Thanks to successful restructuringmeasure and appropriate premium prices,industrial business achieved a positivetechnical result with a combined ratio of100%.

The general liability, accident, legal andmarine sectors saw few changes from theprevious year.

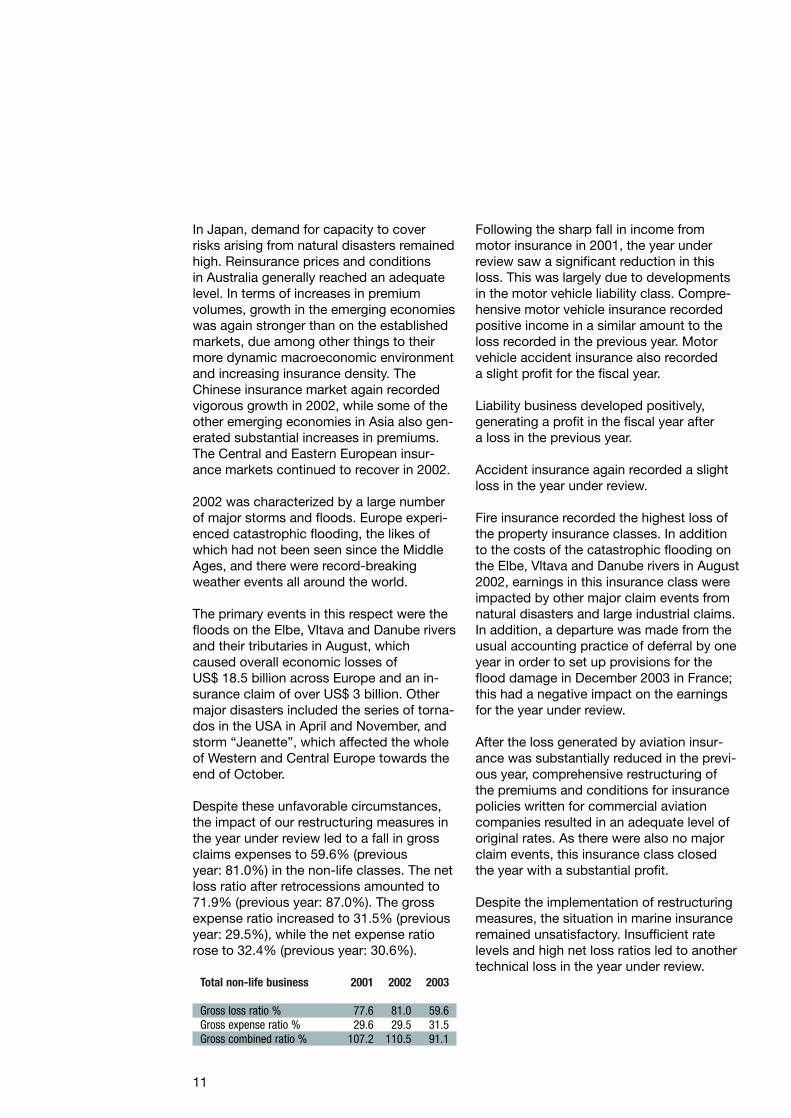

Developments on the international directinsurance and reinsurance markets

Business assumed from cedents outside theR+V Group was affected by developmentson the international reinsurance markets.Because most property and casualty insur-ance business is deferred by one year, thefollowing paragraphs primarily present thesituation on the key reinsurance markets asit was in calendar year 2002.

Developments on the direct insurance andreinsurance markets in 2002 were dominat-ed in particular by the terrorist attacks in the USA on September 11, 2001. On theone hand, this claim event led to a marketshakeout, with some direct insurers andreinsurers – including a number of bignames – forced to scale back their businessor even close down altogether. On the otherhand, rates increased significantly, resultingin profitable growth for reinsurers. However,the slump on the capital markets had a sub-stantial impact on earnings.

Fiscal year 2002 also saw a large number ofnatural disasters. Although overall economiclosses increased considerably year-on-year,claims for insured losses rose only slightlyto US$ 13.0 billion. At around 700, the num-ber of natural disasters recorded remainedat the same level as the previous year; ofthis figure, around 500 related to storms andfloods alone. The major event in this respectwas the catastrophic flooding in Europe inAugust, which resulted in an estimated in-surance claim of US$ 3 billion. Other signifi-cant claim events included floods in Indone-sia, storm “Jeanette” in Western and CentralEurope, and the fire at a Kuwaiti oil refinery.

7

Gross premiums written in the 2003 Changeproperty/casualty insurance €bn year-on-year (direct business)*

Total property/casualty 52.9 +2.8 %Motor 22.4 +2.0 %General liability 6.3 +3.0 %Accident 5.7 +2.0 %Non-life 13.7 +4.5 %Legal protection 2.8 +3.0 %

GDV (German Insurance Association) figures as of November 2003

In the United Kingdom and Ireland, the direct insurance and reinsurance marketshardened significantly across almost all sectors, leading to improvements in premi-ums and conditions. In addition, there weremajor changes in the structure of the market: a large German reinsurer stoppedwriting new policies, a Lloyd’s syndicatediscontinued its liability insurance coverage,and other competitors had difficulties inwriting long-term business due to currentbusiness developments. This led to a reduc-tion in capacity in the liability insurance sector and increased demand at reinsurerswith good ratings, particularly for long-termcontracts.

In France and the Benelux countries, too,rates and conditions in the insurance sectorimproved significantly in the year under review. This applied in particular to industrialfire insurance. The situation for reinsurerswas even more positive than for direct insurers. Furthermore market withdrawalsand lower underwriting volumes of some competitors lead to reductions in capacity.

As the regulatory authorities are no longerresponsible for monitoring the calculation of motor vehicle liability tariffs, Italian directinsurers were able to extensively restructurethis segment. Property and liability insur-ance business with private customers remained profitable on the whole. Underpressure from the reinsurance sector, directinsurers also succeeded in bringing their exposure to natural disasters in their industrial business under better control. Liability for natural disasters was restricted,while liability for terrorist activities – particularly for higher-exposure risks – was generally excluded.

In recent years, the direct insurance marketin Northern Europe has been characterizedby stiff competition, particularly in the area of commercial and industrial insurance.However, rates began to increase percep-tibly in the second half of 2002.

In Central and Eastern Europe, the direct insurance market was characterized byheightened competition, increasingly reflect-ing conditions in the rest of Europe. Themain claim event in this region was the flooddisaster in the Czech Republic in August2002, which led to improvements in originalconditions in both the direct insurance andthe reinsurance markets.

Direct insurance in North America experi-enced a year of mixed fortunes, with a lowlevel of catastrophic losses and consider-able falls in investment income. The mainproblem was the excessively low loss provi-sions at a large number of direct insurersduring the soft market phase, as well as the costs of asbestos claims. This situationmeant that, in some cases, extensive additional provisions had to be recognized,impacting the earnings of the companiesconcerned. Developments in terms of premiums were varied, although a clearoverall recovery was recorded. There wasabove-average growth in premiums forcommercial and private property, while developments in the liability sector leftsome room for improvement.

The recovery of the direct insurance marketwas not fully reflected in the reinsurancesector. The reported combined ratio of allAmerican reinsurers, which also had to recognize additional reserves, amounted to121.3% at year-end.

Most Latin American countries continued tosuffer from the ongoing economic crisis in2002. This in turn impacted the direct insur-ance and reinsurance markets, which saw asignificant fall in premiums for both privateand commercial insurance. These effectsare primarily attributable to developments inArgentina and Venezuela, while the marketsin the other Latin American countriesshowed signs of hardening in a manner similar to the rest of the world.

8

In Japan, the concentration on the direct insurance market continued; the five largestproviders now account for 86% of all premiums. Market conditions for reinsurershardened substantially, and reinsurancecontract prices increased.

The Chinese insurance market also record-ed strong growth in 2002. In 1991, it wasranked 25th among the global insurancemarkets; by 2001, its dynamic developmenthad propelled it into 13th place. The otheremerging Asian insurance markets also generated substantial premium growth insome cases.

The insolvency of a major player on theAustralian direct insurance market led to a considerable increase in competitive pressure, thus further exacerbating the lia-bility insurance crisis which began in 2001.This meant dramatic increases in liabilitypremiums and heavily restricted coverage.

The reinsurance sector was also able tobenefit from this development, enjoying aparticularly strong year in 2002 with a per-ceptible improvement in the market situa-tion. The winners were primarily the largeproviders with good ratings. The insolvencyled to greater quality awareness in the service sector as a whole, with market participants’ ratings and financial stabilitybecoming more important across the board.In addition, the Australian regulatory author-ities tightened the reporting duties and capital requirements of insurance compa-nies.

The South African insurance market is dominated by two large direct insurancecompanies which, between them, have amarket share of over 52%. Premiums in thedirect insurance sector increased substan-tially, particularly for commercial and indus-trial insurance. Prices and conditions on thereinsurance market also hardened consider-ably.

Business development and position ofthe Company

Premium income

Fall in premium volume in Germany morethan offset by foreign business

R+V Versicherung AG’s gross premium in-come increased by 1.0% to €967.4 millionin the fiscal year. After adjustment for ex-change rate effects, premium income in-creased by 5.0% to €1,006.0 million.

Increases in the retentions of direct insurerswithin the R+V Group resulted in domesticpremiums being reduced in the marine, live-stock, credit (provision for doubtful debts),fidelity and legal insurance classes. In con-trast, premiums increased in the life insur-ance, motor vehicle liability, comprehensivemotor vehicle and aviation insurance class-es due to portfolio growth. The premiumvolume generated by business assumedfrom domestic cedents outside the R+VGroup fell by €16.3 million or 11.2%. Over-all, domestic business saw a 9.4% decreasein premiums.

Premium income from foreign business roseby €54.7 million or 11.5%. This meant thatforeign business accounted for 54.8% (pre-vious year: 49.6%) of the total. The maincontributors to the premium volume werethe traditional reinsurance markets of Italy,Spain, France, United Kingdom and NorthAmerica, along with the Singapore branch.

The total net premium volume increasedyear-on-year by €5.3 million, or 0.8%, to€628.2 million. Retention remained essen-tially unchanged at 64.9% (previous year:65.0%).

9

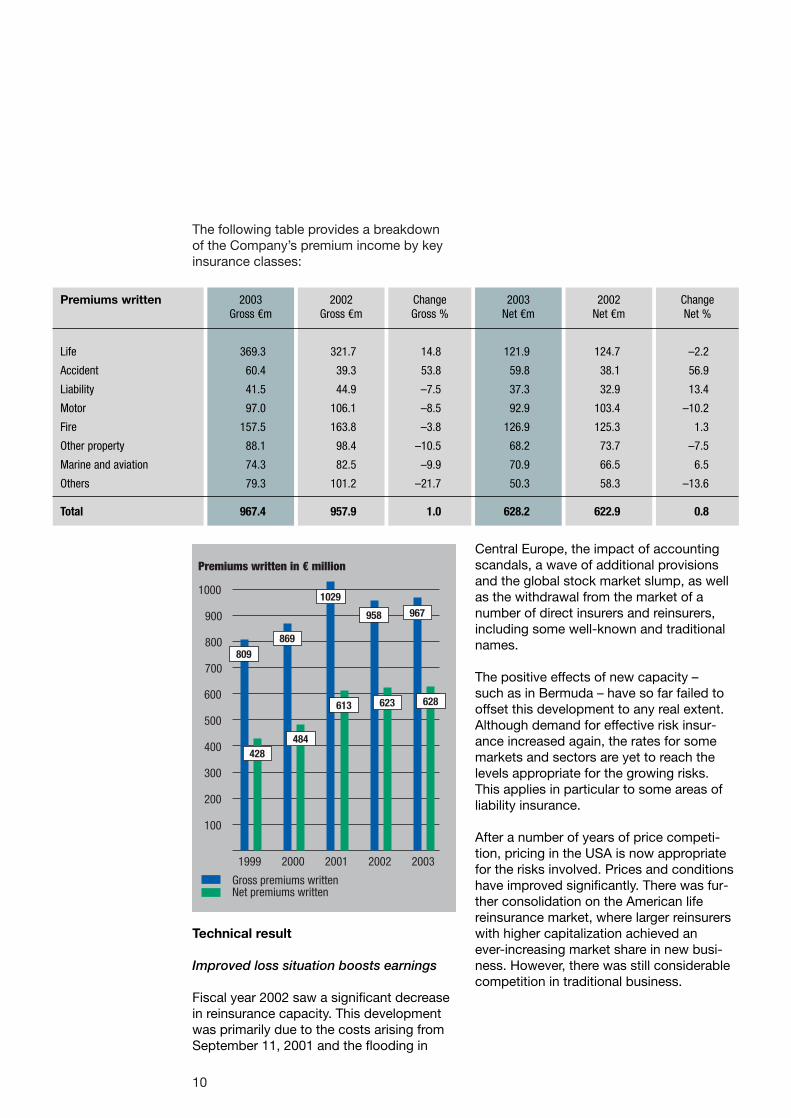

The following table provides a breakdown of the Company’s premium income by keyinsurance classes:

10

Premiums written 2003 2002 Change 2003 2002 ChangeGross €m Gross €m Gross % Net €m Net €m Net %

Life 369.3 321.7 14.8 121.9 124.7 –2.2

Accident 60.4 39.3 53.8 59.8 38.1 56.9

Liability 41.5 44.9 –7.5 37.3 32.9 13.4

Motor 97.0 106.1 –8.5 92.9 103.4 –10.2

Fire 157.5 163.8 –3.8 126.9 125.3 1.3

Other property 88.1 98.4 –10.5 68.2 73.7 –7.5

Marine and aviation 74.3 82.5 –9.9 70.9 66.5 6.5

Others 79.3 101.2 –21.7 50.3 58.3 –13.6

Total 967.4 957.9 1.0 628.2 622.9 0.8

Central Europe, the impact of accountingscandals, a wave of additional provisionsand the global stock market slump, as wellas the withdrawal from the market of a number of direct insurers and reinsurers, including some well-known and traditionalnames.

The positive effects of new capacity – such as in Bermuda – have so far failed tooffset this development to any real extent.Although demand for effective risk insur-ance increased again, the rates for somemarkets and sectors are yet to reach thelevels appropriate for the growing risks. This applies in particular to some areas of liability insurance.

After a number of years of price competi-tion, pricing in the USA is now appropriatefor the risks involved. Prices and conditionshave improved significantly. There was fur-ther consolidation on the American life reinsurance market, where larger reinsurerswith higher capitalization achieved an ever-increasing market share in new busi-ness. However, there was still considerablecompetition in traditional business.

Technical result

Improved loss situation boosts earnings

Fiscal year 2002 saw a significant decreasein reinsurance capacity. This developmentwas primarily due to the costs arising fromSeptember 11, 2001 and the flooding in

800

900

700

600

400

100

1000

20032001

Gross premiums writtenNet premiums written

Premiums written in € million

1999

500

300

200

2000 2002

428

809

628

967

484

869

613

1029

623

958

Total non-life business 2001 2002 2003

Gross loss ratio % 77.6 81.0 59.6Gross expense ratio % 29.6 29.5 31.5Gross combined ratio % 107.2 110.5 91.1

In Japan, demand for capacity to coverrisks arising from natural disasters remainedhigh. Reinsurance prices and conditions in Australia generally reached an adequatelevel. In terms of increases in premium volumes, growth in the emerging economieswas again stronger than on the establishedmarkets, due among other things to theirmore dynamic macroeconomic environmentand increasing insurance density. The Chinese insurance market again recordedvigorous growth in 2002, while some of theother emerging economies in Asia also gen-erated substantial increases in premiums.The Central and Eastern European insur-ance markets continued to recover in 2002.

2002 was characterized by a large numberof major storms and floods. Europe experi-enced catastrophic flooding, the likes ofwhich had not been seen since the MiddleAges, and there were record-breakingweather events all around the world.

The primary events in this respect were thefloods on the Elbe, Vltava and Danube riversand their tributaries in August, whichcaused overall economic losses ofUS$ 18.5 billion across Europe and an in-surance claim of over US$ 3 billion. Othermajor disasters included the series of torna-dos in the USA in April and November, andstorm “Jeanette”, which affected the wholeof Western and Central Europe towards theend of October.

Despite these unfavorable circumstances,the impact of our restructuring measures inthe year under review led to a fall in grossclaims expenses to 59.6% (previousyear: 81.0%) in the non-life classes. The netloss ratio after retrocessions amounted to71.9% (previous year: 87.0%). The grossexpense ratio increased to 31.5% (previousyear: 29.5%), while the net expense ratiorose to 32.4% (previous year: 30.6%).

Following the sharp fall in income from motor insurance in 2001, the year under review saw a significant reduction in thisloss. This was largely due to developmentsin the motor vehicle liability class. Compre-hensive motor vehicle insurance recordedpositive income in a similar amount to theloss recorded in the previous year. Motorvehicle accident insurance also recorded a slight profit for the fiscal year.

Liability business developed positively, generating a profit in the fiscal year after a loss in the previous year.

Accident insurance again recorded a slightloss in the year under review.

Fire insurance recorded the highest loss ofthe property insurance classes. In additionto the costs of the catastrophic flooding onthe Elbe, Vltava and Danube rivers in August2002, earnings in this insurance class wereimpacted by other major claim events fromnatural disasters and large industrial claims.In addition, a departure was made from theusual accounting practice of deferral by oneyear in order to set up provisions for theflood damage in December 2003 in France;this had a negative impact on the earningsfor the year under review.

After the loss generated by aviation insur-ance was substantially reduced in the previ-ous year, comprehensive restructuring ofthe premiums and conditions for insurancepolicies written for commercial aviationcompanies resulted in an adequate level oforiginal rates. As there were also no majorclaim events, this insurance class closedthe year with a substantial profit.

Despite the implementation of restructuringmeasures, the situation in marine insuranceremained unsatisfactory. Insufficient ratelevels and high net loss ratios led to anothertechnical loss in the year under review.

11

Overall, the other insurance classes gener-ated a profit in the year under review. Thisdevelopment was driven by the storm andlivestock classes, which recorded a clearprofit after losses in the previous year.

In contrast, the technical surplus in the lifeinsurance class was slightly down year-on-year. Health insurance recorded a loss atthe previous year’s level.

Overall, reinsurance business ended the fiscal year with a loss of €19.0 million (previous year: loss of €81.6 million) beforeallocations to the equalization provision andsimilar provisions.

As a result of improved net loss ratios in the year under review, allocations weremade to the equalization provision in the liability, comprehensive motor vehicle, fire,comprehensive home contents, storm, engineering, livestock and aviation classes,whereas the earnings situation in the otherclasses led to withdrawals. All in all, alloca-tions of €24.9 million were made to theequalization provision and similar provisions(previous year: withdrawals of €17.4 million).

After allocations to the equalization provi-sion and similar provisions, the technicalloss amounted to €43.9 million (previousyear: loss of €64.2 million).

Investment portfolio

R+V Versicherung AG’s investment portfolioamounted to €2,090.8 million in the past fiscal year – a decrease of €54.5 million or 2.5% year-on-year. Shares in affiliatedcompanies still accounted for a majority ofholdings, increasing slightly again year-on-year from 67.6% to 69.3%.

The valuation reserves in the investmentscarried at cost amounted to €1,716.9 mil-lion. The reserve ratio for the entire invest-ment portfolio thus amounts to 82.1% (pre-vious year: 80.4%).

12

500

1000

1500

2003

2500

1999

Development of investments in € million

2000

2000 2001 2002

1125

2091

1219

1369

2145

Investment result

Current investment income (excluding inter-est on deposits) returned to a normal levelof €111.4 million in 2003 after €321.1 millionin the previous year, which was due toGroup restructuring. After adjustment forcurrent expenses of €4.8 million, an ordinaryresult of €106.6 million was generated.

Overall result

Including the technical result (€-43.9 mil-lion), the investment result (€107.4 million),other income (€23.5 million) and other expenses (€42.0 million), R+V VersicherungAG generated earnings before tax of €44.9 million in 2003, compared with€702.5 million in the previous year.

After deduction of taxes on income and other taxes, net income for the year totaled€43.9 million (previous year: €701.4 mil-lion).

A proposal will be made to the GeneralMeeting to distribute €43.8 million of thenet retained profits to shareholders by distributing a regular dividend of €3.50 anda bonus of €0.40 per no-par value share.

Guarantee funds

Based on net premiums written, the guaran-tee ratio remained at a high level of 406.7%(previous year: 422.5%). The equity ratiocontained within this figure remained un-changed year-on-year at 230.1%, and thereserve ratio amounted to 176.6% (previousyear: 192.4%).

13

Remeasurements at R+V Versicherung AG’sItalian subsidiaries led to write-downs total-ing €2.9 million.

The net investment result also stabilized at€106.3 million, after the extraordinary€784.3 million recorded in the previous year.

Including interest on deposits and after de-duction of the allocated investment return,the Company recorded an investment resultof €107.4 million, compared with €786.6million in the previous year.

Other income and expenses

A large proportion of other income, which totaled €23.5 million (previous year:€19.8 million), resulted from services per-formed for other companies within the R+VGroup. However, this increase was offset byexpenses in the same amount. In addition,other income includes foreign currencygains of €6.5 million. Other expenses in the amount of €42.0 million contain interestexpenses of €15.5 million. On balance, netother income and expenses amounted to€-18.6 million (previous year: €-19.9 mil-lion).

Guarantee funds 2003 2002

€m €m

Share capital 292.0 226.0

Capital reserves 1,001.4 429.6

Revenue reserves 107.6 107.6

Net retained profits 43.9 669.9

Shareholders’ equity 1,444.9 1,433.1

Unearned premiums 67.1 88.2

Aggregate reserve 363.9 491.0

Reserve for loss and loss adjustment expenses 564.7 526.1

Policyholders’ reserves 0.6 0.3

Equalization provision and similar provisions 112.6 87.7

Other insurance reserves 0.4 5.4

Total insurance reserves 1,109.3 1,198.7

Guarantee funds 2,554.2 2,631.9

Business developments in the individualinsurance classes

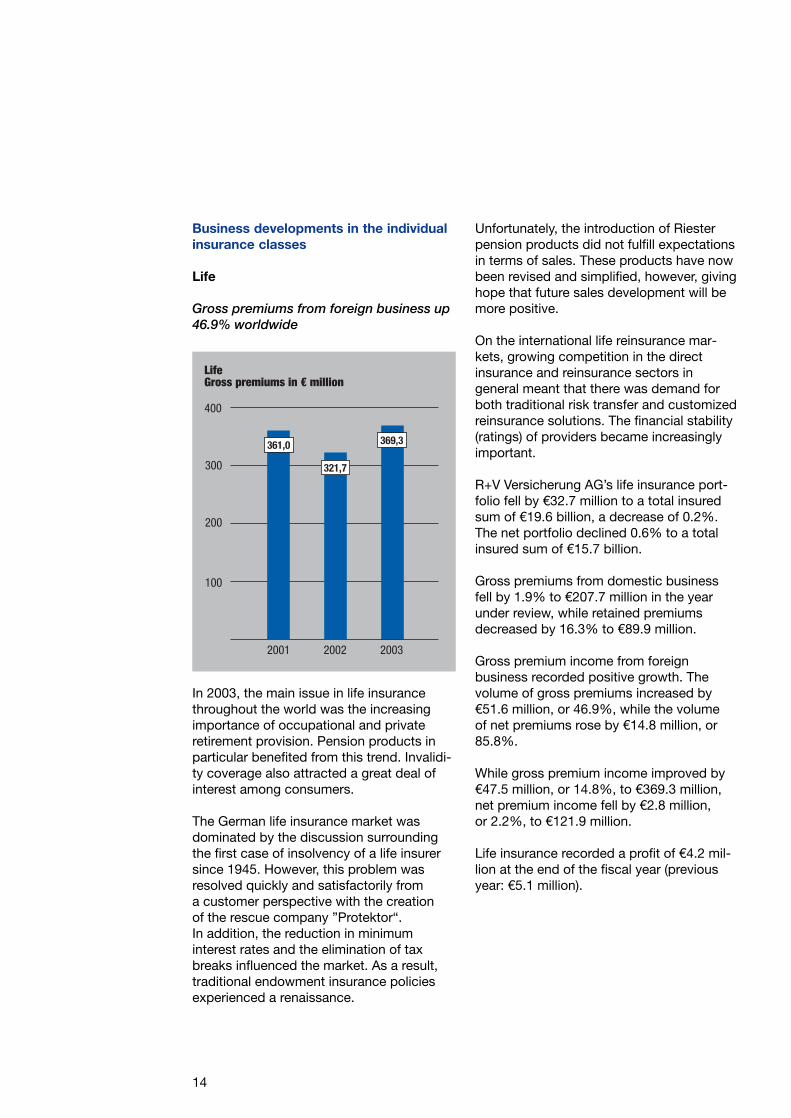

Life

Gross premiums from foreign business up46.9% worldwide

14

Unfortunately, the introduction of Riesterpension products did not fulfill expectationsin terms of sales. These products have nowbeen revised and simplified, however, givinghope that future sales development will bemore positive.

On the international life reinsurance mar-kets, growing competition in the direct insurance and reinsurance sectors in general meant that there was demand forboth traditional risk transfer and customizedreinsurance solutions. The financial stability(ratings) of providers became increasinglyimportant.

R+V Versicherung AG’s life insurance port-folio fell by €32.7 million to a total insuredsum of €19.6 billion, a decrease of 0.2%.The net portfolio declined 0.6% to a total insured sum of €15.7 billion.

Gross premiums from domestic businessfell by 1.9% to €207.7 million in the year under review, while retained premiums decreased by 16.3% to €89.9 million.

Gross premium income from foreign business recorded positive growth. The volume of gross premiums increased by€51.6 million, or 46.9%, while the volume of net premiums rose by €14.8 million, or85.8%.

While gross premium income improved by€47.5 million, or 14.8%, to €369.3 million,net premium income fell by €2.8 million, or 2.2%, to €121.9 million.

Life insurance recorded a profit of €4.2 mil-lion at the end of the fiscal year (previousyear: €5.1 million).

300

200

100

400

2003

LifeGross premiums in € million

2001 2002

369,3361,0

321,7

In 2003, the main issue in life insurancethroughout the world was the increasing importance of occupational and private retirement provision. Pension products inparticular benefited from this trend. Invalidi-ty coverage also attracted a great deal of interest among consumers.

The German life insurance market wasdominated by the discussion surroundingthe first case of insolvency of a life insurersince 1945. However, this problem was resolved quickly and satisfactorily from a customer perspective with the creation of the rescue company ”Protektor“. In addition, the reduction in minimum interest rates and the elimination of taxbreaks influenced the market. As a result,traditional endowment insurance policiesexperienced a renaissance.

2001 2002 2003

Gross loss ratio % 49.8 49.0 54.2Gross expense ratio % 48.8 52.3 46.2Gross combined ratio % 98.6 101.3 100.4

2003 2002€m €m

Reinsurance business assumedSum insured Capital 14,315.2 14,404.3

Annuity 5,317.8 5,261.4

Business cededSum insured Capital 2,685.8 2,696.3

Annuity 1,204.9 1,132.4

Retained for own accountSum insured Capital 11,629.4 11,708.0

Annuity 4,112.9 4,129.0

40

20

10

60

2003

AccidentGross premiums in € million

2001 2002

30

50

60,4

36,539,3

In terms of sums insured, the portfolio developed as follows:

Accident insurance saw a slight decrease inboth the gross and the net premium volumefrom domestic business. The low level ofretrocessions meant that gross and net domestic premiums alike fell slightly by €1.2 million, or 5.2%, from €24.0 million to€22.8 million.

New underwritings and increased marketshare led to above-average growth in for-eign business. The gross premium volumegrew by €22.3 million, or 146.8%, risingfrom €15.3 million to €37.6 million, while net premiums improved by €22.9 million, or162.7%, from €14.1 million to €37.0 million.

Overall, gross premium income grew by53.8% to €60.4 million, while net premiumincome rose 56.9% to €59.8 million.

General accident ended the year with a netloss of €0.3 million (previous year: €-0.7 mil-lion). After withdrawals from the equalizationprovision, this insurance class generated aprofit of €1.8 million (previous year: a loss of€1.2 million).

The premium volume from motor vehicle accident insurance remained at the prior-year level and was due almost exclusively to domestic business. This class broke evenfor the year as a whole.

15

Accident

Strong premium growth in foreign business

After the markets in the United Kingdomand Australia hardened substantially in theprevious year, the year under review alsosaw restructuring efforts in other direct insurance markets. Significant premium increases and restrictions on conditionscould be seen in pharmaceutical product liability and D&O insurance in particular.Original premiums in Australia rose espe-cially sharply in the year under review due to the insolvency of a major direct insurer –a market leader in terms of pricing in partic-ular.

Restructuring measures led to a decline ingross premium income from both domesticand foreign business. Gross premiums fromdomestic business fell slightly by €0.2 mil-lion, or 0.8%, from €28.2 million to €28.0million, while the decrease for foreign busi-ness was €3.2 million, or 19.1%, from €16.6 million to €13.4 million. By contrast,retained premiums increased both domesti-cally and in foreign business; this was due to retrocession agreements expiring.Retained domestic premiums increased by€3.0 million, or 13.6%, from €22.0 million to €25.0 million, while foreign business rose€1.4 million, or 12.8%, from €10.9 million to €12.3 million.

Overall, gross premium income declined by €3.4 million, or 7.5%, from €44.8 millionto €41.4 million. In contrast, the net premium grew by €4.4 million, or 13.4%,from €32.9 million to €37.3 million.

The reported net loss ratio fell by 16.4%,from 79.0% to 62.6%, while the net ex-pense ratio decreased by 0.8%, from 30.9%to 30.1%. Taken together, these factors ledto a profit of €2.7 million (previous year: lossof €3.3 million) in the balance on technicalaccount. This resulted in a loss of €3.0 mil-lion (previous year: loss of €3.6 million) afterallocation to the equalization provision.

16

In the year under review, premiums in thegeneral liability business in Germany in-creased slightly year-on-year by 3.0% to€6.3 billion. A significant fall in the numberof large claims as against the previous yearled to a reduction in losses for the market asa whole.

In the industrial and large-scale commercialliability sector, insurance providers respond-ed by hardening original conditions and adjusting premiums. For the first time, therewas a fundamental examination of policyconditions for particularly highly exposedrisks in the pharmaceutical industry, with afocus on the definition of the term “insur-ance claim” and the inclusion of sites in theUS. Directors & Officers’ (D&O) insurance also saw substantial increases in premiumsand restrictions on conditions. By contrast,competition on the market for commercialand private customers remained stiff.

Liability

Fall in loss and expense ratios lifts income

2001 2002 2003

Gross loss ratio % 33.7 72.2 45.4Gross expense ratio % 30.5 31.6 37.6Gross combined ratio % 64.2 103.7 83.0

40

30

20

10

50

2003

LiabilityGross premiums in € million

2001 2002

50,050,0

41,544,944,9

200

150

100

50

250

2003

MotorGross premiums in € million

2001 2002

97,0

211,6

106,1

2001 2002 2003

Gross loss ratio % 79.4 92.8 74.8Gross expense ratio % 20.0 19.1 17.6Gross combined ratio % 99.4 111.9 92.4

The necessary rate adjustments on themass German motor insurance market weremuted. By contrast, there were signs of arecovery in technical income in the fleetbusiness. Comprehensive insurance classeswere hit by a large number of Acts of God.These included localized hailstorms in thesummer months, various severe rainstormsand the flooding in eastern Germany in August.

Foreign motor insurance business againsuffered from inadequate rate levels. The re-sult for the year under review was impactedby various natural disaster claims resultingfrom the floods in Central Europe and theneed to set up additional provisions in thenon-proportional business, among otherthings.

Growth in the portfolio of R+V AllgemeineVersicherung AG led to an increase in bothgross and net premiums in the domesticbusiness. While gross premium income roseby €6.5 million, or 12.5%, from €51.9 millionto €58.4 million, retained premiums in-creased by €3.7 million, or 7.1%, from €52.3 million to €56.0 million. Foreign busi-ness developed in the opposite direction,with restructuring measures resulting in areduction in gross premium income. It fell by€15.6 million, or 28.7%, from €54.2 millionto €38.6 million, while net premium incomedeclined by €14.2 million, or 27.9%, from€51.1 million to €36.9 million.

Overall, gross premium income declined by€9.1 million, or 8.5%, from €106.1 million to€97.0 million. Net income after retroces-sions amounted to €92.9 million, comparedwith €103.4 million in the previous year (-10.2%).

Domestic business performed more or lessidentically across all the individual classesof motor insurance. The gross premium vol-ume in the motor vehicle liability insuranceclass increased by €4.1 million, or 11.9%,from €34.4 million to €38.5 million, while thenet amount rose by €1.7 million, or 4.9%,from €34.9 million to €36.6 million. Develop-ments in the motor vehicle class were similar, with gross premium volumes of€19.9 million in the year under review asagainst €17.5 million in the previous year(+13.7%). Retained premiums amounted to €19.4 million, after €17.4 million in theprevious year (+11.6%).

Foreign business performed differentlyacross the various classes. Premiums in the motor vehicle liability insurance classdeclined by €15.9 million, or 36.1%, to€28.2 million (gross) and by €15.1 million, or35.9%, to €27.0 million (net). In contrast,gross premiums in the motor vehicle classincreased by €0.4 million, or 3.7%, from€10.1 million to €10.5 million, while net premiums rose by €0.9 million, or 9.6%,from €9.0 million to €9.9 million.

17

Motor

Fall in premiums in foreign businessUnsatisfactory earnings development

Motor vehicle liability insurance recorded aloss in both domestic and foreign business;however, the figure of €9.6 million was €8.5million less than in the previous year. Afterwithdrawals from the equalization provision,the loss fell to €8.2 million (previous year:loss of €10.3 million).

Motor vehicle cover generated a profit indomestic business and a slight loss in for-eign business. This resulted in a profit of€2.0 million (previous year: loss of €2.3 mil-lion) in the balance on technical account, or€0.1 million (previous year: €0.1 million) afterallocations to the equalization provision.

The overall balance on technical account inthe motor insurance class was once againnegative at €-7.5 million (previous year:€-20.4 million). After allocations to theequalization provision, the loss increased to€-8.1 million (previous year: €-10.2 million).

Fire

Decline in premium volume in domestic businessUnsatisfactory earnings development

The restructuring of industrial and large-scale commercial fire insurance showed thefirst signs of success, particularly followingthe reduction in coverage levels, which hadbecome excessive over time, and the intro-duction of appropriate retention premiums.However, the commercial business still suffered from high levels of competition interms of price and conditions.

Gross premium income from fire insurancefell slightly during the fiscal year. The premium volume declined by €6.3 million, or 3.8%, from €163.8 million to €157.5 mil-lion. This development was solely attribut-able to domestic business. While foreignbusiness rose by €2.0 million, or 1.5%, from€133.7 million to €135.7 million, domesticpremiums fell by €8.3 million, or 27.7%, to€21.8 million.

After retrocessions, retained premiums fromforeign business rose by €10.4 million, or9.8%, to €116.4 million, while a premiumvolume of €10.5 million was retained fromdomestic business. This corresponded to areduction of 45.4%. The share of gross pre-mium income attributable to foreign busi-ness increased to 86.2%, up from 81.6% inthe previous year.

The technical result in the year under reviewwas impacted by a high number of basicclaims. By contrast, claims for large individ-ual risks decreased substantially year-on-year. Taken together, these factors led to anet loss of €16.9 million (previous year: lossof €33.0 million). Following allocations to theequalization provision, the loss increased to€19.3 million (previous year: loss of €26.7million).

18

50

200

2003

FireGross premiums in € million

2001 2002

150

100

157,5

123,7

163,8

2001 2002 2003

Gross loss ratio % 103.1 90.5 66.1Gross expense ratio % 35.4 29.6 30.3Gross combined ratio % 138.5 120.1 96.5

50

70

40

30

20

10

90

2003

Marine and aviationGross premiums in € million

2001

60

80

2002

74,3

62,0

82,5

2001 2002 2003

Gross loss ratio % 124.5 93.0 83.7Gross expense ratio % 25.2 23.8 21.3Gross combined ratio % 149.7 116.8 105.0

Following premium growth in previousyears, restructuring measures in the yearunder review led to a reduction in the grossand net premium volumes in the marinebusiness. Gross premium income fell by€17.7 million, or 26.9%, to €48.4 million,with retained premiums declining by €4.6 million, or 8.9%, to €47.2 million.

Gross premiums from domestic businessfell by €6.6 million, or 29.7%, to €15.7 mil-lion. By contrast, net premiums written increased by €2.7 million, or 18.7%, to€16.8 million.

Gross and net premiums from foreign busi-ness developed in a similar manner. Thegross premium volume fell by €11.1 million,or 25.4%, to €32.7 million, while the net figure declined by €7.3 million, or 19.3%, to €30.4 million.

After the first three quarters of 2002 hadbeen largely free of major incidents in the international comprehensive marine insur-ance business, there was a wave of largeclaims in the last three months of the year,including the fire on board the cruise shipDiamond Princess during its construction,the terrorist attack on the Limburg and thefire on board the Hanjin Pennsylvania.These events had a negative impact onearnings. The net technical loss totaled €9.6 million (previous year: loss of €13.3million). As there was no change in the cal-culation of the equalization provision duringthe year under review, the technical loss also amounted to €9.6 million (previousyear: loss of €13.3 million).

The terrorist attacks on September 11, 2001led to fundamental changes in aviation in-surance. Comprehensive restructuring ofthe prices and conditions for insurance poli-cies written for commercial aviation compa-nies led to an adequate level of originalrates for the first time in many years.

This development improved both the premium volume and the earnings situation.The gross premium volume in aviation andaerospace insurance increased by €9.6 mil-lion, or 58.5%, to €25.9 million. In parallelwith this development, retained premiumsrose by €9.0 million, or 61.1%, to €23.7 mil-lion.

This growth was mainly due to foreign busi-ness. In this segment, the gross premiumvolume climbed by €5.8 million, or 47.1%,to €18.2 million, while the net premium vol-ume rose €6.1 million, or 51.8%, to €17.9million.

Gross domestic business grew by €3.7 mil-lion, or 94.1%, to €7.7 million. The net figurewas up €2.9 million, or 98.8%, to €5.8 mil-lion.

19

Marine and aviation

Unsatisfactory earnings in marine business– encouraging income development in aviation

At the end of the fiscal year, this insuranceclass posted a profit of €5.0 million (previ-ous year: loss of €0.4 million), producing aloss of €1.4 million (previous year: loss of€1.3 million) after allocations to the equal-ization provision.

Other insurance classes

Decline in premiums from domestic businessImproved net loss ratio

20

Both the gross and net premiums from domestic business decreased, with thegross premium volume falling €35.0 million,or 31.7%, to €75.3 million, while retainedpremiums declined €19.4 million, or 36.5%,to €33.7 million.

Foreign business developed positively in both gross and net terms. The gross premium volume increased by €2.7 million,or 3.0%, from €89.4 million to €92.1 million,while net premiums written improved by€5.9 million, or 7.5%, from €78.8 million to€84.7 million.

Key contributions to the premium volumecame from the credit and bonds, storm,health, hail/crop, comprehensive home contents, legal, engineering and livestockinsurance classes.

Loss ratios developed differently to the pre-vious year. While there were improvementsin the reported net loss ratios for compre-hensive home contents, comprehensivehomeowners, storm, engineering, livestock,credit, fidelity, legal and health insurance,the opposite was true for the burglary andtheft, water damage, hail/crop and bondsinsurance classes.

Profits were generated in comprehensivehome contents, storm, engineering, live-stock and legal insurance, while technicallosses were recorded in the credit andbonds, hail/crop, health, burglary and theftand comprehensive homeowners insuranceclasses.

Overall, the other insurance classes gener-ated a net profit of €3.3 million in the yearunder review (previous year: net loss of€15.7 million), producing a loss of €8.5 mil-lion (previous year: loss of €13.1 million) after allocations to the equalization provi-sion.

150

100

50

200

2003

Other classesGross premiums in € million

2001 2002

167,4

183,7

199,6

2001 2002 2003

Gross loss ratio % 61.0 70.4 39.4Gross expense ratio % 34.0 32.5 38.9Gross combined ratio % 95.0 102.9 78.3

The premium growth recorded in recentyears did not continue in the year under review. Gross premium income fell by €32.3 million, or 16.2%, to €167.4 million;the net figure declined by €13.4 million, or10.2%, to €118.5 million.

2003 2002

Total number of employees 244 232 of whom:

Full-time 214 204 Part-time 26 23 Employees with fixed-term contracts 4 5

Staff development

As of December 31, 2003, the number ofpeople employed in comparison to the pre-vious year was as follows:

Shareholder structure

As of the balance sheet date, shares in R+V Versicherung AG were held indirectly or directly by the following shareholders be-longing to the union of cooperative banks:

– DZ BANK AG Deutsche Zentral-Genossenschaftsbank, Frankfurt/Main

– WGZ-Bank Westdeutsche Genossen-schafts-Zentralbank eG, Düsseldorf

– Projekt 7 GmbH, Hamm– Bayerische Raiffeisen Beteiligungs-AG,

Munich– Beteiligungs-AG der

Bayerischen Volksbanken, Munich– Genossenschaftliche Beteiligungs-

gesellschaft Kurhessen AG, Kassel– Norddeutsche Genossenschaftliche

Beteiligungs-AG, Hanover– DZ PB-Beteiligungsgesellschaft mbH,

Frankfurt/Main – KRAVAG-Holding AG, Hamburg– Raiffeisen Zentralbank Österreich AG,

Vienna – 846 branches of Volksbank and

Raiffeisenbank throughout Germany– Seven interests in free float

Dependent company report

In the dependent company report preparedin accordance with section 312 of the Aktiengesetz (AktG – German Public Com-panies Act), the Board of Management de-clared that, according to the circumstancesknown to it at the time the transactionsmentioned in the report were performed, theCompany received adequate considerationfor each transaction, and that it did not takeor fail to take any other measures subject todisclosure.

21

235 people were employed at the head office in Wiesbaden (previous year: 223) andnine people were employed at the branchoffice in Singapore, as in the previous year.

Contractual relations within the R+V Group

Members of the Boards of Management of anumber of R+V Group companies also holdsimilar positions at other R+V Group com-panies. R+V companies have concludedservice agreements within the Group. In linewith these agreements, certain intragroupservices are performed by one of the follow-ing companies – R+V Versicherung AG, R+V Allgemeine Versicherung AG, R+VLebensversicherung AG or Rhein-Main Assistance GmbH – in each case.

The services performed for the other com-panies primarily extend to the following ar-eas: sales, investments, asset management,accounting, financial control, legal, premiumcollection, auditing, communications, per-sonnel management, general administrationand IT.

The companies receiving these services arecharged after these have been provided;they have rights of instruction and controlover the outsourced areas.

In addition, the companies of the R+VGroup have concluded an agreement oncentral cash management and a central financial clearing system.

Risks of future development

Risk management process

The Gesetz zur Kontrolle und Transparenzim Unternehmensbereich (KonTraG – Ger-man Act on Control and Transparency inBusiness) that took effect on May 1, 1998details the duties of the Board of Manage-ment to report on the risks of future development and to provide appropriate risk management. In this context, risk management covers all systematic mea-sures involved in recognizing, evaluatingand controlling risks.

R+V Versicherung AG is integrated in theR+V Group’s risk management process. The organization of the latter – including therelevant risk officers – and the risk principlesare documented in a risk management man-ual. Risks are managed and analyzed withthe aid of an IT application.

The R+V Group has a number of systems atits disposal to document and control risks.These systems are further developed on anongoing basis and supplemented by a top-down risk approach as part of a permanentearly warning system. In 2003, an index rat-ing for all of the R+V Group’s major riskswas introduced in the IT database as an additional early warning instrument. It is up-dated quarterly and draws on the bindingfixed indicators relevant to each risk and thethresholds they are based on. In the eventthat a specific index value is exceeded,obligatory measures are instituted and theindividuals responsible for them appointed.

The regular risk conferences and central risk reporting to the Board of Managementguarantee that risks to future developmentthat could impact the Company as a goingconcern are identified, analyzed and con-trolled in a timely manner. In addition, in exceptional cases where changes to risksrepresent a threat to the Group’s continuedexistence, reports will be made to the member of the Board of Management responsible and the coordinator of the riskconference on an ad hoc basis. The risksmonitored are technical risks, default risksrelating to receivables from the insurancebusiness, investment risks, operating risks,and global and strategic risks. The latter relate to risks from changes in the marketand relationships with sales partners, aswell as risks involved in the core activities of planning and control.

Technical risks

The main technical risks for a reinsurer lie in an unbalanced portfolio, inappropriate lia-bility for catastrophic loss and fundamentalchanges in the basic trends on the mainmarkets.

R+V Versicherung AG counters these risks by continuously tracking the markets.Particular importance is attached to main-taining a balanced portfolio – in terms ofboth territorial diversification across theworld and different classes of insurance.Risks are assumed within prescribed under-writing boundaries that limit liability for bothindividual and cumulative losses. The leveland frequency of possible impacts from catastrophic losses are documented andtracked on an ongoing basis using estab-lished industry software, supplemented byadditional verification by the Company itself.Liabilities assumed, particularly in the areaof cumulative losses, are reinsured on national and international reinsurance markets with companies with first-classcredit ratings. Technical provisions aremaintained at appropriate levels. Based onnet premiums written, the Company has ahigh guarantee funds ratio and a high equityratio.

22

Default risks relating to receivables fromthe insurance business

The default risk relating to the billed reinsur-ance receivables from cedents and retro-cessionaries is limited by monitoring theStandard & Poor’s ratings on a regular basis.

Investment risks

In order to create „insurance coverage“products, insurance companies exposethemselves to market price, credit and liquidity risks as part of their investment activities. R+V Versicherung AG countersthese risks by observing the basic principleof achieving the greatest possible securityand profitability while maintaining the liquid-ity of the insurance company at all times. In particular, its investment policy aims tominimize risks by maintaining an appropri-ate mix and diversification of investments.The Anlageverordnung (AnlV – Regulationon the Investment of the Committed Assetsof Insurance Undertakings [Investment Reg-ulation]), which took effect on January 1,2002, explicitly describes qualitative super-vision elements for the first time. The Bun-desanstalt für Finanzdienstleistungsaufsicht(BaFin – the Federal Financial SupervisoryAuthority) issued several circulars, includingR 29/2002, on the concrete interpretation of the AnlV at the end of 2002. R+V Ver-sicherung AG ensures that it adheres to theresulting regulatory investment principlesand requirements by providing qualified in-vestment management, appropriate internalinvestment guidelines and controls, a farsighted investment policy and other organizational measures.

Derivative financial instruments, structuredproducts or asset backed securities are onlyused in accordance with the regulatory requirements set out in BAV (Federal Insur-ance Supervisory Office) circulars R 3/2000,R 3/99 and R 1/2002. Their use is explicitlyregulated by internal guidelines. These include volume and counterparty limits, inparticular.

Extensive, timely reporting ensures that thevarious risks are regularly monitored andpresented transparently. Extrapolating thecapital market situation at the end of 2003to December 31, 2004 and continuing the methods adopted in 2003 to calculatelasting impairments, the Company expectsinvestment income to make a positive contribution to the net income for the year.

At an organizational level, R+V VersicherungAG counters investment risks by ensuringthe strict functional separation of trading,settlement and financial control.

Currency risks

As far as possible, liabilities in foreign currencies arising from reinsurance busi-ness are matched with investments in theseforeign currencies. This allows exchangerate gains and losses to be generally offsetby the correlative effect.

Operating risks

Operating risks are risks from general business activities. They arise as a result ofhuman behavior, technical faults, weakness-es in process or project management, or external influences.

23

Risk provisioning using the internal control system

The main instrument used by the R+VGroup to limit operating risks is the internalcontrol system. The Group protects againstthe risk of errors and fraudulent activities inits administration through regulations andcontrols in force in its specialist depart-ments and by reviewing the application andeffectiveness of the internal control systemsin Group audits. As far as possible, paymentflows and undertakings are handled bycomputer. Additional security is provided by predefined powers of attorney and authorization rules stored in the user profile,as well as electronic submissions for releasemade by the stored random generator. Depending on the risk, manual processing is conducted according to the dual controlprinciple.

The internal monitoring of the regulationsgoverning the risk management system,particularly with regard to their effective-ness, was reviewed by the Group audit de-partment again in 2003. The implementationof the resulting measures is monitored bythe Group audit unit and as part of the riskconference.

Provision for IT risks

In the IT area, the security of programs anddata and the ability to ensure business continuity is guaranteed by comprehensiveaccess controls and safety precautions. A particular risk would be the partial orcomplete failure of the IT systems. The R+V Group has made provisions againstthis by establishing two separate data cen-ters, each with special access protection,sensitive fire protection measures and a secure power supply based on emergencypower generators. A defined restart proce-dure to be used in the event of a disaster istested for its effectiveness in exercises on a regular basis. Data is stored in differentR+V buildings in high security areas as well as at additional external locations.

The telecoms infrastructure has been designed with a high level of redundancy,both internally within buildings and with regard to external network access.

Quality assurance for the IT systems is pro-vided by way of established problem andchange management processes. All eventsof relevance to services are recorded andtracked in accordance with their signifi-cance. Current topics are dealt with in daily conferences and allocated processingpriority. Monthly service control meetingsattended by all IT division heads are held toescalate problems and agree and takecountermeasures when fixed thresholds forsystem availability and response times areexceeded.

Risk provisions for major projects and investments

The R+V Group has laid down binding pro-cedures for the planning and implementa-tion of projects and investments. In line with these specifications, an investmentcommittee regularly examines major pro-jects and investments, paying particular attention to events, problems and (counter)measures, as well as adherence to budgets.Necessary changes are implemented imme-diately. The investment committee also liaises with the risk conference committee.

Summary of the risk situation

The instruments and methods of analysisoutlined here show that R+V VersicherungAG has a comprehensive system that satis-fies the risk identification and analysis requirements needed for efficient risk management. To date, it has not identifiedany developments that could have a materi-al adverse effect on the Company’s net assets, financial position and results of operations in the long term.

24

25

Significant events and outlook

The current economic environment is char-acterized by a high level of uncertainty. The effects of the war in Iraq and the fear of further terrorist attacks are affecting sentiment, and the current downturn isseemingly here for the longer term. On thecapital markets, too, the mood is depressedand appears unlikely to improve in the shortterm.

The USA’s position as the growth driver ofthe global economy has weakened. Due tolow capacity utilization in manufacturing in-dustry, investment has declined perceptibly.Even cheap loans have been unable to pro-vide any relief in this regard. To date, privateconsumption and the real estate markethave shored up the US economy. In view of increasing unemployment, however, thereis a danger that these factors will also loseground.

In Japan, the world’s second-largest econ-omy, the first signs of recovery are nowemerging after a period of stagnation. Germany is still relying on its exports, butdomestic demand has declined notably anda recovery is not on the cards in the shortterm.

The insurance sector will inevitably continueto be affected by global economic develop-ments and the difficult conditions on thecapital markets. This means that the pres-sure to generate good technical results isparticularly great. Overall, property insur-ance is seeing higher rates and improvedconditions as well as lower reinsurance capacity. For reinsurers, it can therefore be assumed that the favorable market con-ditions in property reinsurance will continuein 2005. In the area of personal insurance,there is a general trend towards increasedpersonal provision for pensions and health-care. This should be a source of growth potential for the reinsurance sector.

The consolidation measures initiated in2001 for the 2002 underwriting year affectedthe balance sheet for the first time in theyear under review, due to the deferred reporting of third-party business. We sys-tematically pursued this consolidation strategy and are forecasting a further improvement in the technical result in thenext fiscal year on the back of a moderateincrease in premiums.

Wiesbaden, March 9, 2004

The Board of Management

26

Appendix to the Management Report

In the year under review, the Company was active in the following fields of domestic and foreign reinsurance:

Life

Health

Accident

Liability

Motor

Aviation

Legal

Fire and allied perils

Burglary and theft

Water damage

Glass

Storm

Comprehensive home contents

Comprehensive homeowners

Hail

Livestock

Engineering

Marine

Credit and bonds

Other

27

Net retained profits for the fiscal year amount to €43,938,702.We propose to the General Meeting that the net retained profits be used as follows:

€

€3.50 dividend 39,347,000 plus €0.40 bonus 4,496,800 per no-par value share for 11,242,000 shares Retained profits brought forward 94,902

43,938,702

Proposal on the Appropriation of Profits

R+V Versicherung AGAnnual Financial Statements 2003

R+V Versicherung AGAnnual Financial Statements 2003

30

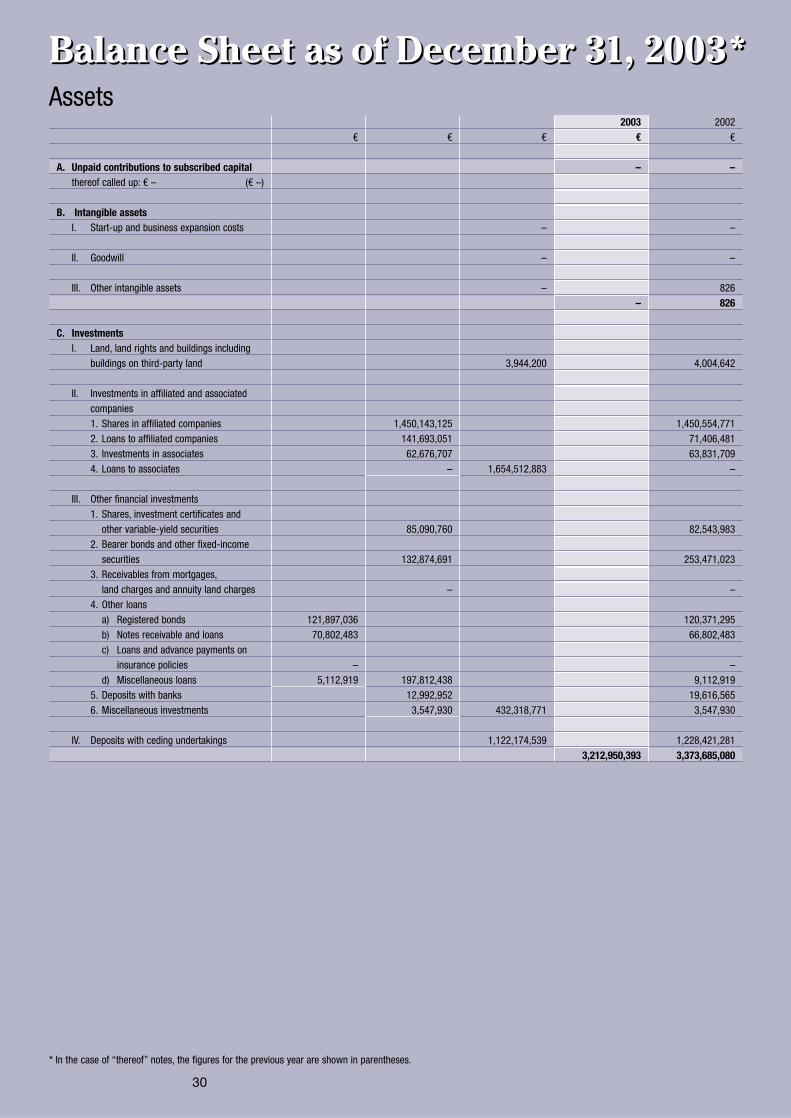

Balance Sheet as of December 31, 2003*Balance Sheet as of December 31, 2003*Assets

2003 2002€ € € € €

A. Unpaid contributions to subscribed capital – –thereof called up: € – (€ –)

B. Intangible assetsI. Start-up and business expansion costs – –

II. Goodwill – –

III. Other intangible assets – 826– 826

C. InvestmentsI. Land, land rights and buildings including

buildings on third-party land 3,944,200 4,004,642

II. Investments in affiliated and associated companies1. Shares in affiliated companies 1,450,143,125 1,450,554,7712. Loans to affiliated companies 141,693,051 71,406,4813. Investments in associates 62,676,707 63,831,7094. Loans to associates – 1,654,512,883 –

III. Other financial investments1. Shares, investment certificates and

other variable-yield securities 85,090,760 82,543,9832. Bearer bonds and other fixed-income

securities 132,874,691 253,471,0233. Receivables from mortgages,

land charges and annuity land charges – –4. Other loans

a) Registered bonds 121,897,036 120,371,295b) Notes receivable and loans 70,802,483 66,802,483c) Loans and advance payments on

insurance policies – –d) Miscellaneous loans 5,112,919 197,812,438 9,112,919

5. Deposits with banks 12,992,952 19,616,5656. Miscellaneous investments 3,547,930 432,318,771 3,547,930

IV. Deposits with ceding undertakings 1,122,174,539 1,228,421,2813,212,950,393 3,373,685,080

* In the case of “thereof” notes, the figures for the previous year are shown in parentheses.

31

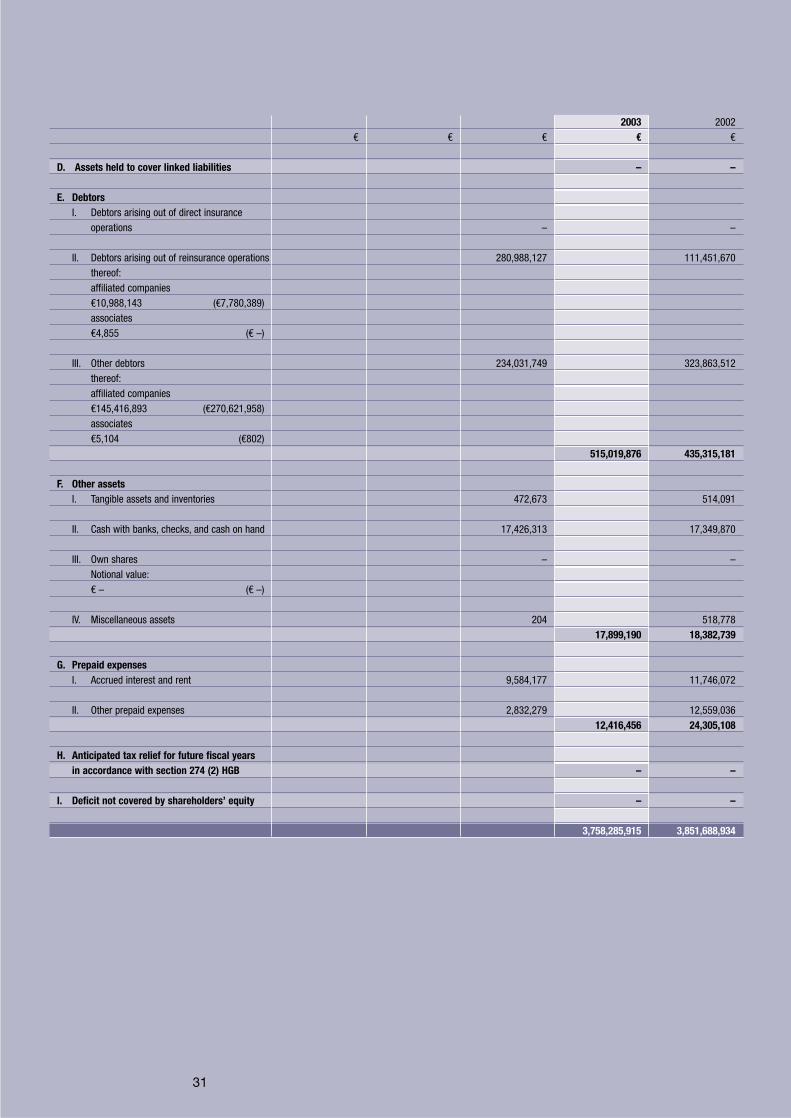

2003 2002€ € € € €

D. Assets held to cover linked liabilities – –

E. DebtorsI. Debtors arising out of direct insurance

operations – –

II. Debtors arising out of reinsurance operations 280,988,127 111,451,670thereof:affiliated companies€10,988,143 (€7,780,389)associates€4,855 (€ –)

III. Other debtors 234,031,749 323,863,512thereof:affiliated companies€145,416,893 (€270,621,958)associates€5,104 (€802)

515,019,876 435,315,181

F. Other assetsI. Tangible assets and inventories 472,673 514,091

II. Cash with banks, checks, and cash on hand 17,426,313 17,349,870

III. Own shares – –Notional value:€ – (€ –)

IV. Miscellaneous assets 204 518,77817,899,190 18,382,739

G. Prepaid expensesI. Accrued interest and rent 9,584,177 11,746,072

II. Other prepaid expenses 2,832,279 12,559,03612,416,456 24,305,108

H. Anticipated tax relief for future fiscal years in accordance with section 274 (2) HGB – –

I. Deficit not covered by shareholders’ equity – –

3,758,285,915 3,851,688,934

32

Equity and liabilities2003 2002

€ € € € €

A. Shareholders’ equityI. Subscribed capital 292,000,000 226,000,000

II. Capital reserves 1,001,381,228 429,590,228

III. Revenue reserves1. Legal reserve – –2. Reserve for own shares – –3. Statutory reserves – –4. Reserve in accordance with

section 58 (2a) AktG – –5. Other revenue reserves 107,558,087 107,558,087 107,558,087

IV. Net retained profits 43,938,702 669,989,823thereof profits brought forward:€12,823 (€24,476)

1,444,878,017 1,433,138,138

B. Participation certificates – –

C. Subordinated liabilities 76,693,782 76,693,782

D. Special tax-allowable reserves (in accordance with section 6b EStG) – 357,608

E. Technical provisionsI. Unearned premiums

1. Gross 96,348,694 119,882,3822. less:

Reinsurance amount 29,265,864 67,082,830 31,645,128

II. Mathematical reserve1. Gross 1,014,853,825 1,106,559,2932. less:

Reinsurance amount 650,923,928 363,929,897 615,531,444

III. Claims outstanding1. Gross 797,204,478 863,043,9052. less:

Reinsurance amount 232,468,709 564,735,769 336,925,214

IV. Provision for bonuses and rebates1. Gross 616,514 318,4542. less:

Reinsurance amount 2,923 613,591 –

V. Equalization provision and similar provisions 112,593,672 87,657,592

VI. Other technical provisions1. Gross 343,362 5,743,1212. less:

Reinsurance amount –50,000 393,362 355,5021,109,349,121 1,198,747,459

33

2003 2002€ € € € €

F. Technical provisions for linked liabilities – –

G. Other provisionsI. Provisions for pensions and similar

obligations 17,672,243 16,625,387

II. Tax provisions 3,866,710 3,867,943

III. Provisions for anticipated tax charges in future fiscal years in accordance with section 274 (1) HGB 539,585 1,100,000

IV. Other provisions 6,569,627 4,051,14328,648,165 25,644,472

H. Deposits received from reinsurers 676,222,630 642,823,871

I. Other liabilitiesI. Creditors arising out of direct insurance

operations – –

II. Creditors arising out of reinsurance operations 314,615,309 158,694,363thereof:affiliated companies€16,791,975 (€28,616,932)associates€ – (€4,823)

III. Bonds 19,623,532 19,576,050thereof convertible:€ – (€ –)

IV. Liabilities to banks – 50.035.103

V. Other creditors 87,924,922 245,816,191thereof:taxes€332,231 (€335,291)social security contributions€317,782 (€281,607)affiliated companies€81,192,999 (€239,162,489)associates€887,304 (€887,304)

422,163,763 474,121,707

K. Deferred income 330,437 161,897

3,758,285,915 3,851,688,934

34

Income Statement for the Period from January 1 to December 31, 2003*Income Statement for the Period from January 1 to December 31, 2003*

2003 2002€ € € €

I. Technical account

1. Premiums earned – net:a) Gross premiums written 967,352,061 957,885,754b) Reinsurance premiums ceded 339,171,705 628,180,356 334,996,177c) Change in provision for unearned premiums – gross 18,508,798 –41,541,313d) Change in provision for unearned premiums – reinsurers’ share 2,363,873 16,144,925 13,621,075

644,325,281 594,969,339

2. Allocated investment return – net 12,298,899 20,554,117

3. Other technical income – net 1,587,441 1,508,815

4. Claims incurred – neta) Claims paid

aa) Gross 570,487,002 606,640,514bb) Reinsurers’ share 221,211,360 349,275,642 239,179,762

b) Change in provision for claims outstandingaa) Gross –38,432,657 68,159,399bb) Reinsurers’ share –100,288,037 61,855,380 –46,900,593

411,131,022 482,520,744

5. Change in other technical provisions – neta) Mathematical provision – net –55,051,165 7,422,344b) Other technical provisions – net 4,837,172 –2,492,500

–50,213,993 4,929,844

6. Bonus and rebates – net 372,568 530,019

7. Operating expenses – neta) Operating expenses – gross 315,201,810 307,128,378b) less:

Reinsurance commissions and profit participations received 100,321,294 87,182,489214,880,516 219,945,889

8. Other technical expenses – net 583,066 520,259

9. Subtotal –18,969,544 –81,554,796

10. Change in the equalization provision and similar provisions –24,936,080 17,370,114

11. Balance on technical result – net –43,905,624 –64,184,681

* In the case of “thereof” notes, the figures for the previous year are shown in parentheses.

35

2003 2002€ € € € €

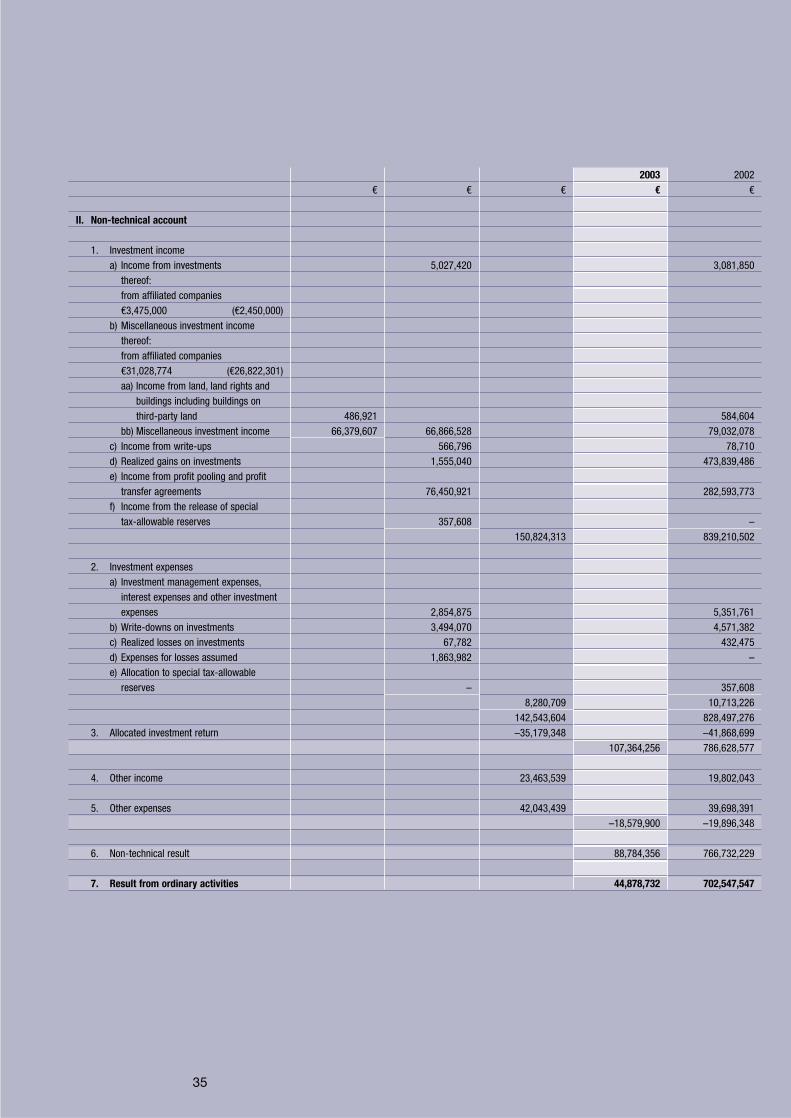

II. Non-technical account

1. Investment incomea) Income from investments 5,027,420 3,081,850

thereof:from affiliated companies€3,475,000 (€2,450,000)

b) Miscellaneous investment incomethereof:from affiliated companies€31,028,774 (€26,822,301)aa) Income from land, land rights and

buildings including buildings on third-party land 486,921 584,604

bb) Miscellaneous investment income 66,379,607 66,866,528 79,032,078c) Income from write-ups 566,796 78,710d) Realized gains on investments 1,555,040 473,839,486e) Income from profit pooling and profit

transfer agreements 76,450,921 282,593,773f) Income from the release of special

tax-allowable reserves 357,608 –150,824,313 839,210,502

2. Investment expensesa) Investment management expenses,

interest expenses and other investment expenses 2,854,875 5,351,761

b) Write-downs on investments 3,494,070 4,571,382c) Realized losses on investments 67,782 432,475d) Expenses for losses assumed 1,863,982 –e) Allocation to special tax-allowable

reserves – 357,6088,280,709 10,713,226

142,543,604 828,497,2763. Allocated investment return –35,179,348 –41,868,699

107,364,256 786,628,577

4. Other income 23,463,539 19,802,043

5. Other expenses 42,043,439 39,698,391–18,579,900 –19,896,348

6. Non-technical result 88,784,356 766,732,229

7. Result from ordinary activities 44,878,732 702,547,547

36

2003 2002€ € € €

8. Extraordinary income – –

9. Extraordinary expenses – –

10. Extraordinary result – –

11. Taxes on income 911,274 1,117,938thereof reallocation within fiscal entity:€13,368,229 (€ –)

12. Other taxes 41,579 47,721thereof reallocation within fiscal entity:€9,073 (€–520,939)

952,853 1,165,659

13. Income from losses assumed – –

14. Profit transferred as a result of profit pooling and profit transfer agreements – –

15. Net income for the year 43,925,879 701,381,889

16. Retained profits brought forward from the previous year 12,823 24,476

17. Withdrawals from capital reserves – –

18. Withdrawals from revenue reservesa) from legal reserve – –b) from reserve for own shares – 1,583,458c) from statutory reserves – –d) from other reserves – –

– 1,583,458

19. Transfers from participation certificates – –

20. Appropriations to other revenue reservesa) to legal reserve – –b) to reserve for own shares – –c) to statutory reserves – –d) to other revenue reserves – 33,000,000

– 33,000,000

21. Transfers to participation certificates – –

22. Net retained profits 43,938,702 669,989,823

NotesNotesAccounting policies

Basis of preparation

The annual financial statements of R+VVersicherung AG for 2003 were prepared inaccordance with the provisions of theHandelsgesetzbuch (HGB – GermanCommercial Code), the Aktiengesetz (AktG– German Public Companies Act) and theprovisions of the Versicherungsaufsichts-gesetz (VAG – German Act on PrivateInsurance Undertakings) as well as theVerordnung über Rechnungslegung vonVersicherungsunternehmen (RechVersV –German Federal Regulations on InsuranceAccounting) dated November 8, 1994.

Use of simplification procedures

The annual financial statements for 2003also cover all business assumed by R+VGroup companies in 2003, domestic andforeign third-party life insurance businessand the business of our branch office inSingapore.

As other non-life business underwritten onthe international reinsurance market is oftensettled with the cedents long after the bal-ance sheet date, we applied the approxima-tion and simplification procedures permittedunder section 27 (1) in conjunction withsection 3 of the RechVersV. In accordancewith this, business with a gross premiumvolume of €387.0 million or a 40.0% shareof total premiums written was included oneyear in arrears. Technical provisions wererecognized in a sufficient amount to meetcurrent and future obligations.

Intangible assets were measured at costand written down using the straight-linemethod over the useful life of the assetsallowed by tax law. Additions and disposalsin the fiscal year were written down prorata.

Land, land rights and buildings includingbuildings on third-party land were carriedat acquisition or manufacturing cost lesswrite-downs. Straight-line depreciation wasperformed using the rate allowed by taxlaw.

Shares in affiliated companies and asso-ciates and other investments were carriedat cost. Investments held in foreign curren-cies were translated using the exchangerate applicable at the time of acquisition.

Investments in associates were measuredaccording to the length of time they havebeen held by the Company, as were othervariable-yield securities, bearer bondsand other fixed-income securities, otherloans and deposits with banks. Depositswith banks in foreign currencies were translated using the exchange rate as of the balance sheet date.

With the exception of shares and invest-ment certificates, all securities were measured in line with the strict principle of the lower of cost or market. Where thereasons for write-downs charged in thepast no longer applied, write-ups weremade up to a maximum of the acquisitioncost in accordance with section 280 (1)HGB. These items also include derivativefinancial instruments; these were combinedwith existing securities in the portfolio toform microhedges for hedge accountingpurposes.

Shares and investment certificates werealso recognized at the lower of cost or market as of December 31, 2003. Anexception was made for long-term invest-ments whose price at the closing date wasdue only to temporary impairment. This wasdetermined by way of forecasting.

The ”sustainable value” of such invest-ments was calculated on the basis of theDCF model (annuity immediate) togetherwith IBES profit estimates (market consen-sus). The directly held portfolio and specialfunds were both measured at the level ofthe individual shares and investment certifi-cates.

37

38

If the DCF value (sustainable value calculat-ed on the basis of the DCF model) wasslightly higher than the market price, theDCF value at the balance sheet date wasrecognized. If the DCF value was lower than the market price, the market price wasrecognized.

Carrying amounts were written up to themarket price, up to a maximum of theacquisition cost.

The acquisition cost in euros of securitiesheld in foreign currencies was calculatedusing the price of the security and theexchange rate at the time of acquisition; thebook value in euros was calculated on thebasis of the price of the security and theexchange rate as of the balance sheet date.

Other loans and deposits with bankswere reported at their repayment value,insofar as specific valuation allowances didnot have to be performed. Deposits withbanks in foreign currencies were translatedusing the exchange rate as of the balancesheet date.

Premiums and discounts were amortizedover the maturity period. The proportionrelating to future years was reported as prepaid expenses.

Financial derivatives and structuredproducts were broken down into their individual components and measured usingrecognized actuarial methods based on theBlack-Scholes option pricing model.

Deposits with ceding undertakings and debtors arising out of reinsuranceoperations were carried at their nominalvalue. Doubtful debtors were written down directly.

Operating and office equipment was carried at cost and written down using thestraight-line method over the useful lifeallowed by tax law. Additions and disposalsin the fiscal year were written down prorata. Low-value assets were written off infull in their year of acquisition.

The remaining assets are carried at theirnominal value. Any necessary valuationallowances were performed and deductedfrom assets.

Technical provisions (unearned premiums,mathematical provisions, claims outstand-ing and other technical provisions) weregenerally reported in line with informationprovided by the cedents.