global demand for lithium-ion batteries

TRANSCRIPT

2020 Vision: Global Lithium-ion Battery Market Changing Utility Regulation is Helping to Pave the Way For

Grid Storage

Vishal Sapru

Research Manager

Energy and Power Systems

Frost & Sullivan

2

Executive Summary

3

Executive Summary

Source: Frost & Sullivan

• Demand for lithium-ion batteries is expected to continue to grow from 2013 to 2020.

• Key end-users driving growth in demand for lithium-ion batteries include consumer

device vendors, industrial goods manufacturers, the grid and renewable energy storage

segment, and automobile manufacturers.

• The automotive segment is slated to exhibit higher growth beyond 2015, largely because

of the increase in electric vehicle (EV) production and the continuing demand for hybrid

electric vehicles (HEVs) and plug-in hybrid vehicles (PHEVs).

• The grid and renewable energy storage energy segment will likely provide lithium-ion

battery manufacturers with solid revenue growth opportunities over the next 5 to 7 years.

• Within the industrial segment, healthcare, power tools and equipment, and military

applications constitute the leading user-base for lithium-ion batteries.

• Regulatory factors such as a push toward alternative and green energy sources,

increasing emphasis on boosting fuel efficiency, and emissions standards will likely

stimulate market demand.

4

Executive Summary (continued)

• Continuing investments in research and development (R&D) will likely improve

lithium-ion battery capabilities and pricing.

• The competitive structure within the lithium-ion battery market remains fragmented,

including providers such as cell manufacturers and battery-pack integrators.

• Market consolidation is expected as fewer smaller participants will likely sustain rising

R&D costs, combined with a push toward declining prices.

• North America and Asia-Pacific (APAC) are expected to lead in market demand;

however, many European countries also continue to seek alternative energy sources for

the automotive and the grid and renewable energy storage segments.

Source: Frost & Sullivan

5

Market Overview

6

Market Segmentation by Application

Automotive 18.3%

Grid and Renewable

Energy Storage

6.9%

Consumer 60.3%

Industrial 14.5%

Key Takeaway: The consumer segment

dominates the global lithium-ion battery

market with increased use in laptops, smart

phones, power tools, and other applications.

Total Lithium-ion Battery Market: Percent

Revenue Breakdown by Application, Global,

2013

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

Key Takeaway: The utility segment dominates the

market as utilities are seeking smart grid solutions

that utilize lithium-ion batteries to improve

operational efficiency and effectiveness.

Total Lithium-ion Battery Market: Percent

Revenue Breakdown by Application, Global,

2020

Automotive 30.0%

Grid and Renewable

Energy Storage 37.6%

Consumer 23.9%

Industrial 8.5%

7

Market Segmentation by Application (Continued)

• While still showing revenue growth, the consumer segment is expected to see its share of the overall

industry revenues decline throughout the forecast period. The consumer segment, which accounted

for 60.3% of total lithium-ion battery revenues in 2013, is expected to see its market share reduced to

23.9% in 2020.

• This reduction in total market share will likely be from declining prices, significant growth in lithium-ion

battery demand in other segments such as grid and renewable energy storage, and lower demand

expectations for certain consumer products such as laptops, and standalone audio and video devices

such as MP3 players.

• In addition, continuing device convergence will likely further limit the ability of the consumer market to

garner stronger revenue growth throughout the forecast period. For instance, smartphones and

tablets are increasingly taking on MP3 player functionality, thereby reducing the need for consumers

to buy devices such as Apple’s iPods. A decline is also expected in demand for hand-held video

gaming consoles.

• Despite revenue growth, market share in the industrial segment is expected to decline because of the

explosive growth in the grid and renewable energy storage segment and the automotive segment.

• Furthermore, longer replacement cycles for certain industrial products such as power tools will also

likely be a factor responsible for the reduction in revenues contributed by the industrial segment.

Source: Frost & Sullivan

8

External Challenges: Drivers and Restraints

9

Drivers 1–2 Years 3–4 Years 5–7 Years

Growth in mobile communications and

computing devices drives demand for lithium-ion

batteries

H H M

The industrial segment continues to grow because

of greater utilization of lithium-ion batteries in power

tools and other sectors such as telecommunications

H H M

Developing applications within the energy sector

help fuel interest in lithium-ion batteries L M H

The automotive segment continues to present

growth opportunities for lithium-ion batteries L M M

Impact Ratings: H = High, M = Medium, L = Low

Total Lithium-ion Battery Market: Key Market Drivers, Global, 2014–2020

Market Drivers

Source: Frost & Sullivan

10

Restraints 1–2 Years 3–4 Years 5–7 Years

Product safety concerns continue to affect lithium-

ion battery utilization across certain industrial

applications

H M L

The lack of a recharging infrastructure for EVs

further impedes demand within the automotive

segment

H H M

Higher prices continue to stifle production and

sales of pure EVs H H M

Total Lithium-ion Battery Market: Key Market Restraints, Global, 2014–2020

Market Restraints

Impact Ratings: H = High, M = Medium, L = Low

Source: Frost & Sullivan

11

Market Forecast

12

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0.0

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

90,000.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Gro

wth

Ra

te (

%)

Re

ve

nu

e (

$ M

illi

on

)

Year

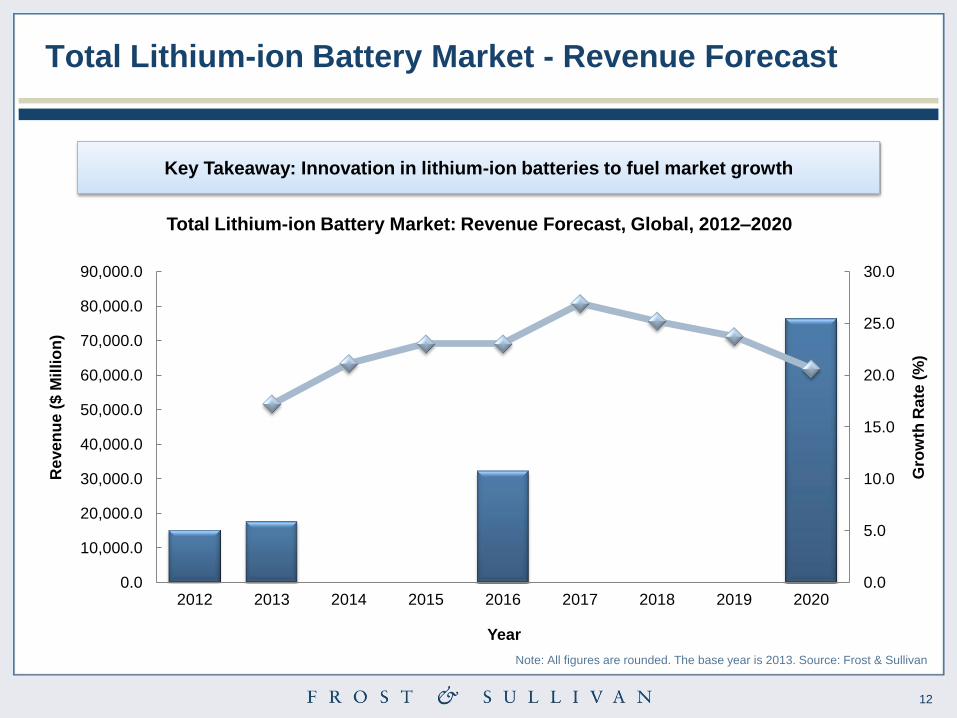

Total Lithium-ion Battery Market - Revenue Forecast

Key Takeaway: Innovation in lithium-ion batteries to fuel market growth

Total Lithium-ion Battery Market: Revenue Forecast, Global, 2012–2020

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

13

Revenue Forecast Discussion

• Overall demand for lithium-ion batteries will continue to increase throughout the forecast period

because of anticipated high growth within the automotive and grid and renewable energy storage

segments.

• Within the automotive segment, the pure EV market is expected to face a longer mass adoption cycle;

therefore, the continuing push toward marketing hybrid vehicles is expected to provide lithium-ion

battery vendors with growth opportunities.

• In addition, the trend toward incorporating lithium-ion batteries for start-stop applications within the

automotive segment is also expected to drive demand.

• Several manufacturers are planning to launch additional hybrid models and pure EVs in the 2014 to

2015 time period, including BMW (i3), Tesla (Model X), and Volkswagen (e-Golf). Within emerging

markets such as India, Mahindra launched the e2o lithium-ion vehicle.

• Price reductions for existing EVs (Nissan Leaf) and PHEVs (Chevy Volt) within the North American

market are further expected to have some positive impact on demand.

• Within the industrial segment, increasing utilization of battery back up for healthcare, military,

telecommunications, and other applications will likely drive demand.

• The grid and renewable energy storage segment is expected to show strong growth throughout the

forecast period. Source: Frost & Sullivan

14

Total Lithium-ion Battery Market - Percent Revenue

Forecast by Region

Key Takeaway: North America and APAC will remain at the forefront of growth.

0.0

20.0

40.0

60.0

80.0

100.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Reve

nu

e (

%)

Year

Total Lithium-ion Battery Market: Percent Revenue Forecast by Region, Global, 2012–2020

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

NA

EU

APAC

LATAM ROW

15

Revenue Forecast Discussion by Region

• The APAC market accounted for the largest share of revenue at 43.6% in 2013 because of its large

demand base for lithium-ion batteries used in manufacturing a range of consumer devices such as

smartphones, laptops, and tablets.

• The North American market, which accounted for 34.7% of the total revenue generated by lithium-ion

battery manufacturers in 2013, is expected to become the leading revenue generating source in 2020

because of the rising interest in alternative energy sources within the region.

• In addition, increasing demand for lithium-ion batteries within the automotive and industrial segments

is further expected to drive revenue growth in North America. The US market remains a prime target

for EVs, HEVs, and PHEVs among domestic and global auto manufacturers.

• The European market, which accounted for nearly 16% of the revenue in 2013, is expected to show

stable revenue growth because of continuing increased investments in renewable energy storage

across countries such as Germany.

• The European market is also showing some signs of growth within the EV market as companies such

as Tesla are gaining greater traction across certain countries such as Norway.

Source: Frost & Sullivan

16

Technology Trends

17

Technology Trends - Battery Chemistries, Costs, and

Safety

• Given the temperature constraints faced by traditional lithium-ion batteries, manufacturers are

increasingly seeking materials that enable lithium-ion batteries to operate effectively and safely in

extreme temperatures.

• For instance, Leyden Energy has developed lithium imide-based electrolytes that minimize the

incidence of thermal expansion when operated in extremely hot temperatures. Leyden is also at the

forefront of developing silicon-based anodes that enable higher energy density compared to

carbon-based anodes.

• Similarly, Electrovaya Inc. has launched SuperPolymer 2.0 lithium-ion batteries that improve battery

efficiency and effectiveness across a range of applications and also exclude non-toxic material

N-Methyl Pyrrolidone (NMP), which is known to be hazardous to human health.

• SuperPolymer 2.0 is expected to have greater fire resistance and wider operating temperature

ranges, both hot and cold.

• While greater power and energy density remain the focus in new product development initiatives,

stronger emphasis is also being placed on reducing overall costs, including cells, battery-pack

materials, and battery management systems.

Source: Frost & Sullivan

18

Technology Trends - Role of Support Infrastructure

• While the availability of an effective and cost-efficient support infrastructure such as charging stations

and solar panels is on the rise, the overall number of deployments remains low.

• Despite the increase in charging stations within the automotive segment, their geographic

concentration is limited to major cities, hence failing to address range anxiety concerns of potential EV

buyers. The overall figure remains limited to a few thousand worldwide compared to the presence of

traditional fueling stations.

• For instance, Tesla, a leading marketer of EVs, reported 94 charging stations in the United States, 17

across Europe, and 3 in APAC. While there are other charging mechanisms besides Tesla’s

Supercharger stations, their number remains rather low compared to the over 130,000 gas stations

that exist in the United States alone.

• While most of the existing automotive charging facilities were built using government subsidies,

private sector investment in infrastructure is essential in fostering EV demand.

• Lacking short-term battery technology improvements that address driver range anxiety concerns, the

limited availability of effective (low charging time) and cost-efficient (installation and maintenance

costs) charging stations will continue to influence demand for EVs.

Source: Tesla Motors, Inc., ”Road Trips Made Easy: Charge in minutes, for free.” (May 2014); Frost & Sullivan

19

Market Trends

20

Automotive Segment - Outstanding Question

In the absence of significant charging infrastructure and the rather lengthier charging times, what

improvements need to be made to EVs to address range anxiety issues?

• A short-term answer to the above question may reside in convincing automotive OEMs to utilize larger

battery packs. For instance, unlike Nissan’s 24 kWh battery pack for Leaf, Tesla offers 2 battery size

options of 60 kWh and 85 kWh for its Model S EV. While a larger battery size increases production

costs and retail prices, Tesla’s recent success alludes to the fact that larger battery packs may be the

answer to range anxiety concerns in the short term. Tesla touts a driving range of 244 to 300 miles, at

55 miles per hour (mph) average speed, for its Model S, compared to the 75 to 125 miles for other

EVs.

• While using smaller battery packs leads to lower EV prices, an argument can be made that a car that

is not deemed functional because of a limited driving range may be unappealing to consumers at any

price. This scenario is essentially akin to what is taking place in the smartphone industry. For

example, while most carriers offer non-smartphones for free, consumer migration to smartphones

continues to grow despite higher prices as these phones deliver greater functionality.

• Lithium-ion battery vendors must work to reduce overall prices, hence allowing auto manufacturers to

consider using larger battery packs.

• The idea of battery-pack swapping, while helpful, will likely remain in an evolutionary stage, at least

during the first half of the forecast period. Source: Frost & Sullivan

21

Automotive Segment - Outstanding Question (continued)

• While expansion of charging stations is expected to occur over the forecast period, the mere presence

of such stations is less likely to convince consumers to purchase costlier EVs that offer a lower driving

range.

• Moreover, the reduction in charging time is also expected to have a limited impact on influencing

demand for EVs unless accompanied by improvements in the driving range for such vehicles.

• For instance, within the traditional (gasoline powered) vehicle market, the mere presence of

thousands of fueling stations does not translate into greater consumer interest in purchasing vehicles

with a lower driving range, regardless of the attractiveness of the sticker price of such vehicles. This

specifically holds true for markets such as the United States, where driving habits vary significantly

compared to other regions worldwide and where the need for instant gratification often affects

consumer behavior, which translates to shorter charging times, increased access to charging

infrastructure, and a higher driving range.

• In the near term, extending the driving range of EVs will likely remain a function of improvements in

battery technology or utilization of a larger battery pack, which is akin to Tesla’s approach for its

Model S vehicle that comes with much larger battery pack options compared to other EVs currently on

the market.

Source: Frost & Sullivan

22

Grid and Renewable Energy Storage Segment - Global

Projects

• The DOE’s global energy storage database shows a range of projects that are employing various

lithium-ion chemistries for grid storage applications.

• From a global perspective, the United States leads in the overall number of lithium-ion-based grid

storage projects. Most of these 41 projects, however, are concentrated in the East and West coast

states because of the greater regulatory push for grid and renewable energy storage in these

markets.

• As of December 2013, 16 projects across Europe were reported as active by the DOE. These projects

are scattered across Germany, Italy, the United Kingdom, and Spain.

• Within the APAC market, the DOE identified China, South Korea, and Japan as active participants in

the grid and renewable energy storage segment.

• From a capacity perspective, the sizes of these projects vary widely as some are currently in an

exploratory or trial stage, whereas others are actual commercial deployments.

Source: Frost & Sullivan

23

Grid and Renewable Energy Storage Segment - Trends

Within the grid and renewable energy storage segment, the following key trends are driving demand for

lithium-ion batteries:

• A changing regulatory environment requires utility companies to improve operational efficiency and

effectiveness through energy storage. Within the US market alone, utility regulators such as CPUC

are setting guidelines for utilities and other load-serving entities (LSEs) for energy storage

procurement mechanisms and goals. For instance, in October 2013, CPUC established an energy

storage target of 1,325 megawatts by 2020 for Pacific Gas & Electric Company, Southern California

Edison, and San Diego Gas & Electric. CPUC’s decision was guided by the need to optimize the grid

performance, including peak reduction, and to improve power distribution reliability.

• Alternative energy generation sources reduce greenhouse emissions. In this regard, greater

investments in renewable energy resources are being considered to help both the consumer and

commercial markets, including the grid and renewable energy storage segment, while also achieving

environmental sustainability goals.

Outside North America, organizations such as the European Association for Storage of Energy (EASE)

are making efforts to increase energy storage deployments that are designed to boost energy distribution

efficiency while also supporting climate goals.

Source: Frost & Sullivan

24

Consumer Segment - Trends

• The consumer segment continues to provide lithium-ion battery vendors with a stable source of

revenue growth.

• The continuing increase in the adoption of mobile computing and communications devices such as

smartphones and tablets is a major driver behind growth in the consumer segment. Expanding

product lines for these devices, such as various screen sizes and functionality, will likely keep the

consumer segment as a large source of revenue for lithium-ion battery vendors.

• Greater use of battery-draining and battery-hungry applications such as mobile video will likely force

OEMs to continue to incorporate higher-end and higher-priced batteries in smartphones and tablets.

• In addition, the development of wearable technology such as smart watches will likely continue to

provide a new avenue of growth for lithium-ion battery vendors.

Source: Frost & Sullivan

25

Industrial Segment - Market Trends

• Within the telecommunications and IT sectors, lithium-ion battery use for cell towers and datacenter

back-up powering is on the rise.

• In addition, lithium-ion batteries are increasingly being used in a variety of healthcare-related

applications such as back-up powering and implantable devices.

• Growth in demand across various industrial sectors and growth in other consumer, automotive, and

grid and renewable energy storage applications will likely result in demand outstripping supply,

thereby leading to a slightly higher average price per unit toward the end of the forecast.

Source: Frost & Sullivan

26

Contact Us To Find Out More

Source: Frost & Sullivan

Vishal Sapru Research Manager & Growth Consultant

Energy and Power Systems

210-348-1016 (O), 732-429-2252 (C)