global development finance 2001 building coalitions for effective development finance

TRANSCRIPT

Global Development Finance 2001

Building Coalitions for Effective Development Finance

The context

• Global uncertainties in the short-term- deceleration of growth- emerging market crises- heightened interaction between financial markets and

real economy• Strong medium-term prospects

- technology- policy flexibility- greater commitment to global challenges

This presentation covers

• The macro outlook• Private capital flows

- Trends- Implications for developing country growth

• Concessional resource transfers- Trends and effectiveness- Debt relief- International public goods

Macro outlook

• Sharp slowdown

• Early recovery

• Important risks

Sharp slowdown in world GDP growth(percent change)

0

1

2

3

4

5

6

1997 1998 1999 2000 2001 2002 2003

Source: World Bank data and projections.

Developing

Industrial

World

Cycle should be short-lived

• Interest rate reductions

• Anticipation of tax cut in U.S. and Europe

• Technology helps shorten inventory cycle

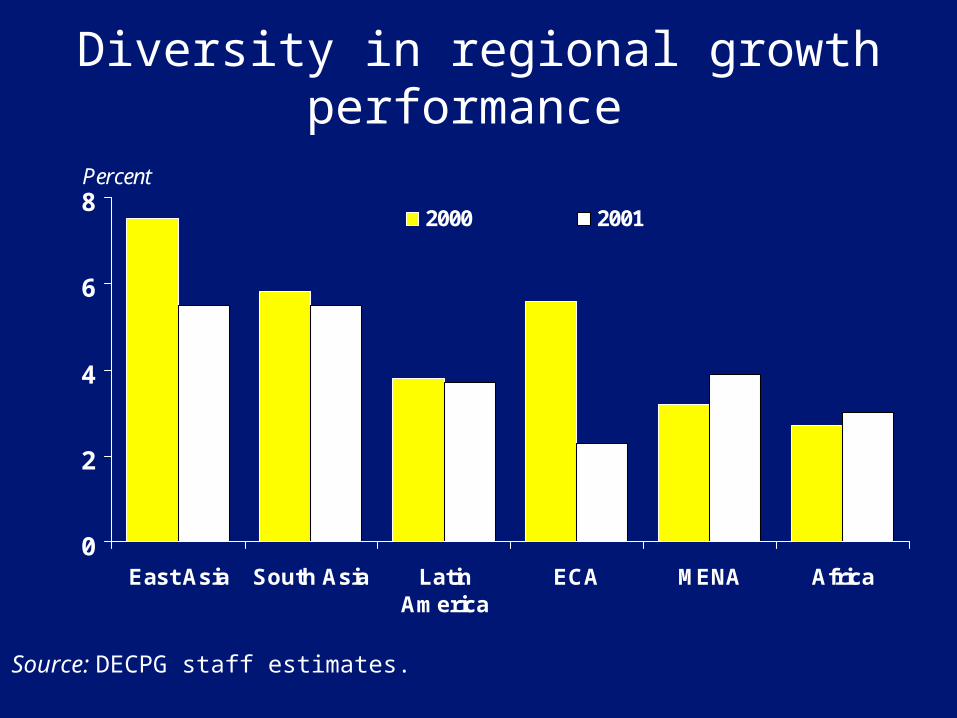

Diversity in regional growth performance

0

2

4

6

8

East Asia South Asia LatinAmerica

ECA MENA Africa

2000 2001

Percent

Source: DECPG staff estimates.

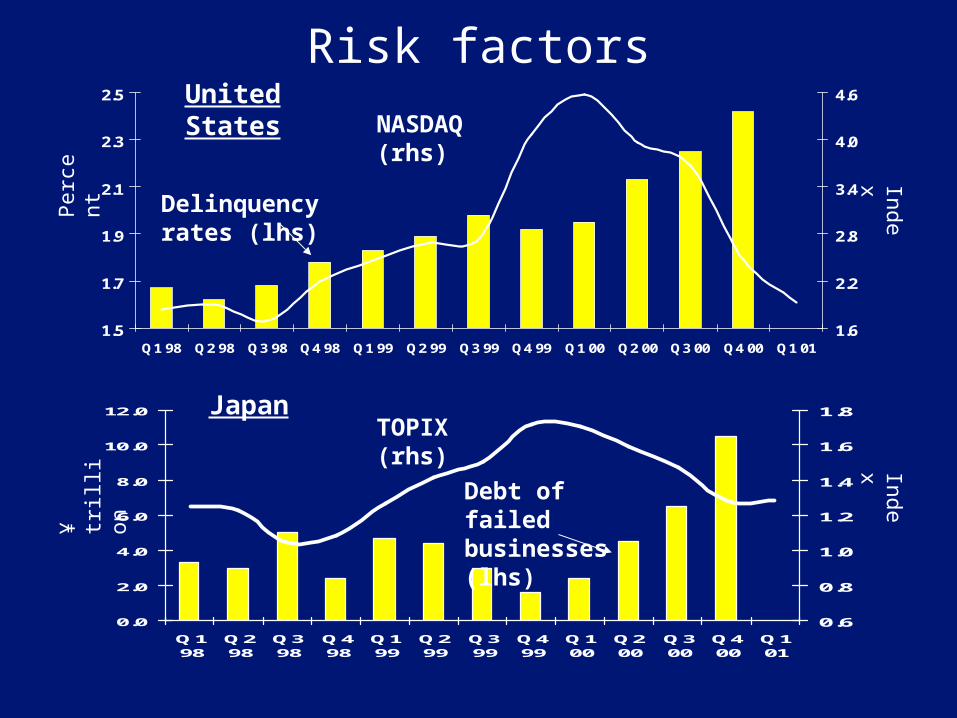

1.5

1.7

1.9

2.1

2.3

2.5

Q1 98 Q2 98 Q3 98 Q4 98 Q1 99 Q2 99 Q3 99 Q4 99 Q1 00 Q2 00 Q3 00 Q4 00 Q1 011.6

2.2

2.8

3.4

4.0

4.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q198

Q298

Q398

Q498

Q199

Q299

Q399

Q499

Q100

Q200

Q300

Q400

Q101

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Per

cent

Index¥

tril

lion

Delinquency rates (lhs)

NASDAQ (rhs)

TOPIX (rhs)

Debt of failed businesses (lhs)

United States

Japan

Risk factorsIndex

Trends in capital flows

• Capital flows down relative to GDP

• Developing countries improve creditworthiness

• But lose share of global flows

0

5

10

15

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Per

cent

Russia BrazilCrises

Private capital flows/ Recipients’ exports

Private capital flows/Recipients’ GDP

Private capital flows in relation to

GDP and trade

ThailandMexico

Note: Private capital flows are net of amortization.

Reduced external vulnerability

a. Short-term debt and total debt are as of September 2000.Source: Bank for International Settlements, Global Development Finance Country Tables and sources cited therein, IMF International Financial Statistics and World Bank staff estimates.

Region and indicator (ratio) 1996 1997 1998 1999 2000a

All developing countries

Short-term debt to total debt 54.3 52.2 46.9 45.3 46.5

Reserves to short-term debt 138.4 130.8 164.2 184.2 204.3

East Asia and Pacific

Short-term debt to total debt 61.1 53.4 45.2 43.1 44.3

Reserves to short-term debt 127.0 126.7 233.2 325.3 377.9

Latin America and Caribbean

Short-term debt to total debt 52.4 53.2 49.4 46.8 47.1

Reserves to short-term debt 116.4 106.4 104.4 105.3 104.4

Developing countries lose share in international FDI

0

200

400

600

800

1000

1200

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

1991

1992

1993

1994

1995

1996

1997

1998

1999

Global Developing countries Top 10 LDCs

FDI Mergers and acquisitions

Note: Top 10 refers to the developing countries with the largest FDI (or M&A) flows.

Private flows and growth

• Private capital flows reinforce growth

• Volatility has high costs

• No “race to the bottom”

Capital flows to GDP ratio (percent)

0

1

2

3

4

5

6

7

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998

Top 10*

Middle income

Low income

* Refers to the ten developing countries with the largest net capital flows.Note: Capital flows are net of amortization.

Growing divergence between middle and low income

countries(annual GDP growth rates)

0

1

2

3

4

5

6

7

1970s 1980s 1990s

Low Income Middle Income Top 10*

* Refers to the ten developing countries with the largest net capital flows.

-6

-4

-2

0

2

4

6

8

-3 -2 -1 0 1 2 3 4

Volatility

Per

cap

ita

grow

th r

ate,

un

exp

lain

ed

par

t

percent

Capital flows volatility reduces growth

Note: The regression line controls for other determinants of growth

Pollution levels have fallen, while FDI has increased: Sao Paulo State,

Brazil

0

1

2

3

4

5

6

7

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

FD

I (1

998

US

$ b

illi

ons)

0

20

40

60

80

100

120

140

160

Par

ticu

late

air

pol

luti

on (

SP

M+

ug/

m3)

Pollution index (rhs)

FDI (lhs)

FDI

More aid and more effective aid

• Slight rise in aid flows since 1997

• Better policy performance

• Better aid allocation

Aid has risen modestly since 1997

35.0

37.5

40.0

42.5

45.0

47.5

50.0

0.20

0.22

0.24

0.26

0.28

0.30

0.32

0.34

0.36US$ billion % of donor GNP

Aid as a percentage of donor GNP (rhs)

Aid in US$ billions (lhs)*

* Net of technical cooperation grants.

Improved policy performanceover the 1990s

0

1

2

3

4

5

IDA onlycountries

Low incomecountries excl.

IDA

Lower middleincome countries

Upper middleincome countries

1991 1999

Index (1-6)

Source: DECPG staff estimates.

Poor performers received less aid

Highpolicy

Middlepolicy

Lowpolicy

Lowest third

Middle third

Top third0

0.1

0.2

0.3

Aid

/GD

P

Developing countryincome groups

Countryperformance

Source: OECD and World Bank.

Between 1992 and 1994, on average, poor performers received more aid than better performers...

Lowpolicy

Middlepolicy

Highpolicy

Lowest third

Middle third

Top third0

0.1

0.2

0.3

Aid

/GD

P

Developing countryincome groups

Countryperformance

...In 1998 poor performers are receiving less aid than better performers.

The increasing coordination challenge

0

5

10

15

20

1960s 1970s 1980s 1990s

Num

ber o

f don

ors

Note: The Theil index in Panel C is a statistical measure of the extent of concentration of aidby sector. Higher values of the index indicate that aid is spread over a greater number of sectors.Source: OECD Development Assistance Committee.

0.7

0.8

0.9

1

1.1

Thei

l's in

dex

0

10

20

30

40

50

60

70

80

90

100

Num

ber o

f rec

ipie

nt c

ount

ries

The Heavily Indebted Poor Countries initiative

• A new start: quicker pace, more relief

• Tie to policy reform: key for success.

• Eventual cost of initiative: $28.6 billion (net

present value).

The declining HIPC debt burden

0

5

10

15

20

25

1998 1999 2000 2001-05

Debt service/exportsDebt service/fiscal revenue

percent

Note: Ratios for 1998 and 1999 are debt service paid to exports or revenue: ratios for 2000 onwards are debt service due after HIPC assistance to exports or revenue. Data refers to the22 HIPCs that reached decision points by end-December.Source: Country authorities and World Bank/IMF staff estimates.

International public goods

• $5 billion a year of aid flows

• Growing trend

• But incentives more important than

finance

Growing share of development assistance to international public

goods

0

5

10

15

20

1970s 1980s Early 1990s Late 1990s

Per

cen

t of

tot

al O

DA

0

10000

20000

30000

40000

50000

US

$ m

illio

n

Core expenditure (lhs) Complementary expenditure (lhs) Total Aid expenditure (rhs)

Principles for public goods

• Complementarity

• Leverage

• Incentives for responsible action

The agenda

• Investment climate

• Volatility safeguards

• More aid: better performers & the poor

• More donor specialization & coordination

• High leverage in public goods provision

• IFIs: specialization, subsidiarity, convening

role.