global fuel oil market overview - platts · global fuel oil market overview ... the american shale...

TRANSCRIPT

© 2013 Platts, McGraw Hill Financial. All rights reserved.

Global Fuel Oil Market Overview

Sharmilpal Kaur, Associate Editorial Director June 11, 2013

Global fuel oil market overview: Is the market bottoming out?

• Broad-based oil outlook • Changing crude oil flows – what do shifting

heavy/light crude oil dynamics mean for the residual fuel oil market?

• Shifting refining dynamics globally and how they affect demand and supply fundamentals

• Key emerging concerns in 2013 and beyond

2

New crude trade flows govern markets

3

Source:IEA

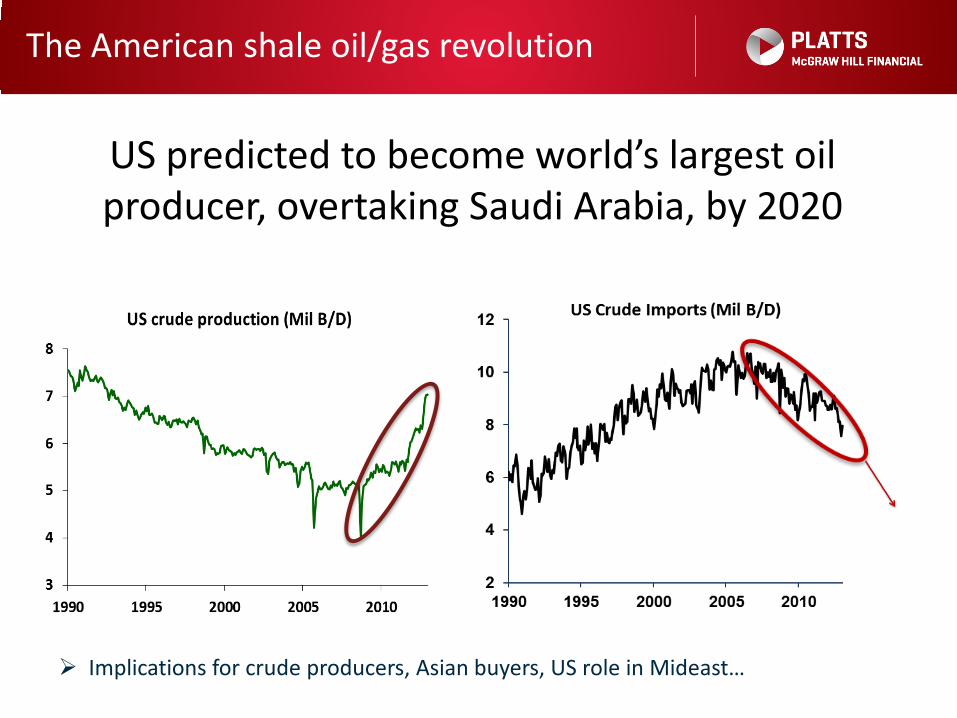

The American shale oil/gas revolution

US predicted to become world’s largest oil producer, overtaking Saudi Arabia, by 2020

Implications for crude producers, Asian buyers, US role in Mideast…

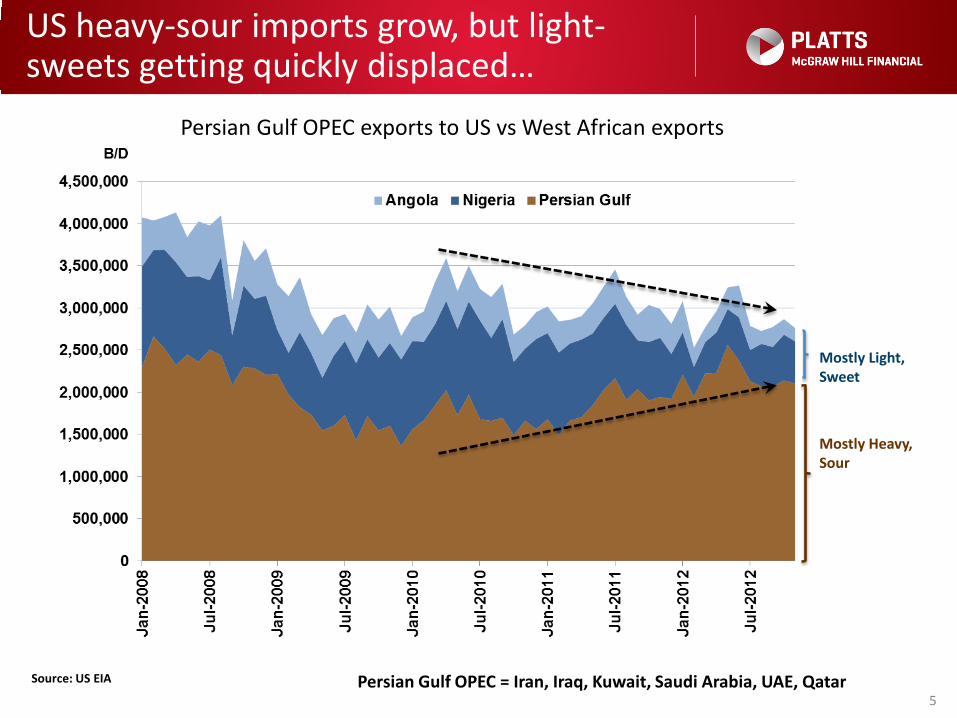

US heavy-sour imports grow, but light-sweets getting quickly displaced…

5

Mostly Heavy, Sour

Mostly Light, Sweet

Persian Gulf OPEC = Iran, Iraq, Kuwait, Saudi Arabia, UAE, Qatar Source: US EIA

Persian Gulf OPEC exports to US vs West African exports

6

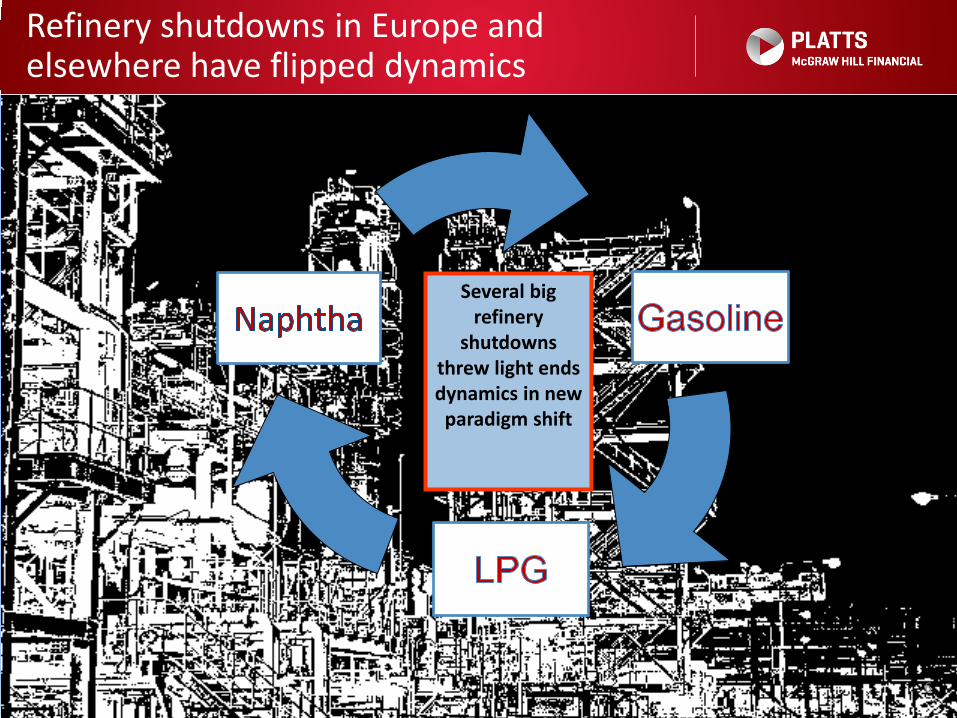

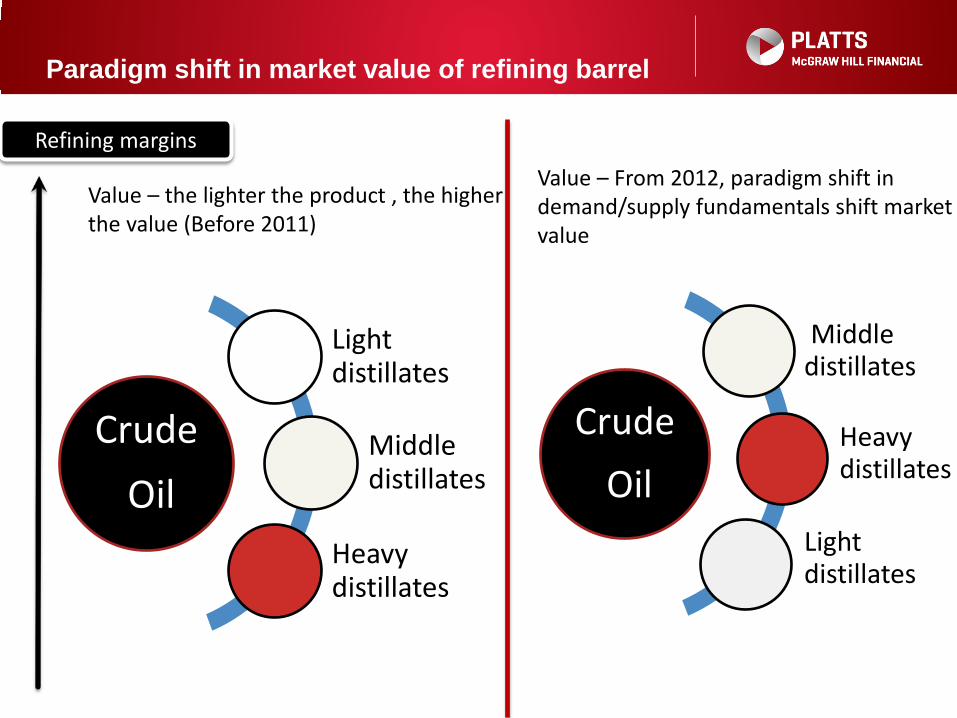

Several big refinery

shutdowns threw light ends dynamics in new

paradigm shift

Refinery shutdowns in Europe and elsewhere have flipped dynamics

Crude Oil

Light distillates

Middle distillates

Heavy distillates

Value – the lighter the product , the higher the value (Before 2011)

Crude Oil

Middle distillates

Heavy distillates

Light distillates

Value – From 2012, paradigm shift in demand/supply fundamentals shift market value

Paradigm shift in market value of refining barrel

Refining margins

Shifting fundamentals as gasoil demand rises

Light ends

Gasoil

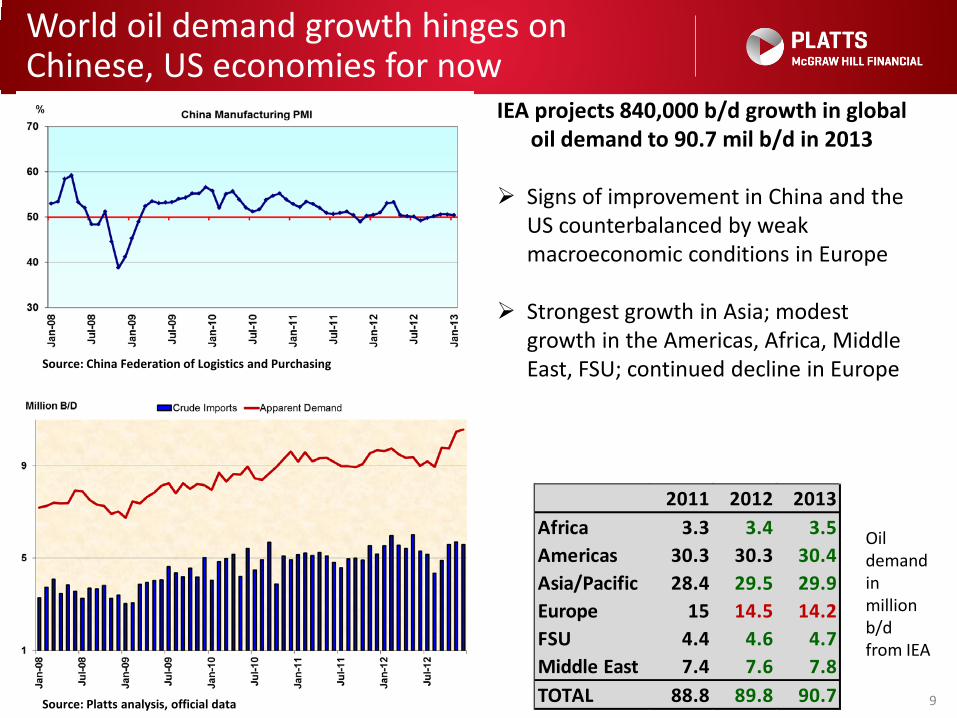

World oil demand growth hinges on Chinese, US economies for now

9

IEA projects 840,000 b/d growth in global oil demand to 90.7 mil b/d in 2013

Signs of improvement in China and the

US counterbalanced by weak macroeconomic conditions in Europe

Strongest growth in Asia; modest growth in the Americas, Africa, Middle East, FSU; continued decline in Europe

Source: China Federation of Logistics and Purchasing

Source: Platts analysis, official data

2011 2012 2013Africa 3.3 3.4 3.5Americas 30.3 30.3 30.4Asia/Pacific 28.4 29.5 29.9Europe 15 14.5 14.2FSU 4.4 4.6 4.7Middle East 7.4 7.6 7.8TOTAL 88.8 89.8 90.7

Oil demand in million b/d from IEA

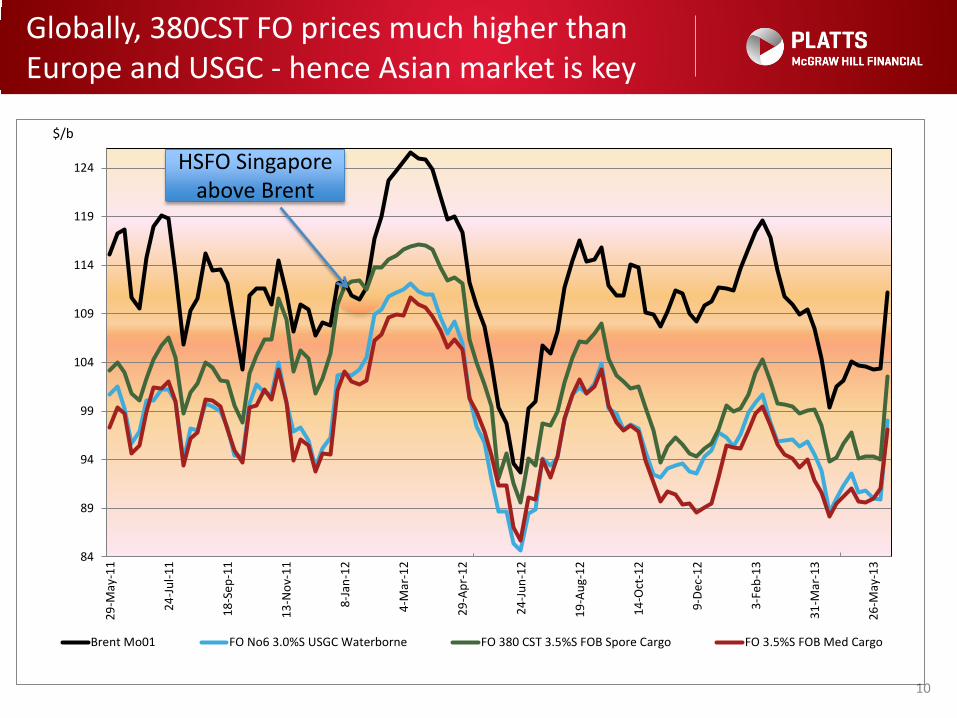

Globally, 380CST FO prices much higher than Europe and USGC - hence Asian market is key

10

84

89

94

99

104

109

114

119

124

29-M

ay-1

1

24-Ju

l-11

18-S

ep-1

1

13-N

ov-1

1

8-Ja

n-12

4-M

ar-1

2

29-A

pr-1

2

24-Ju

n-12

19-A

ug-1

2

14-O

ct-1

2

9-De

c-12

3-Fe

b-13

31-M

ar-1

3

26-M

ay-1

3

Brent Mo01 FO No6 3.0%S USGC Waterborne FO 380 CST 3.5%S FOB Spore Cargo FO 3.5%S FOB Med Cargo

$/b

HSFO Singapore above Brent

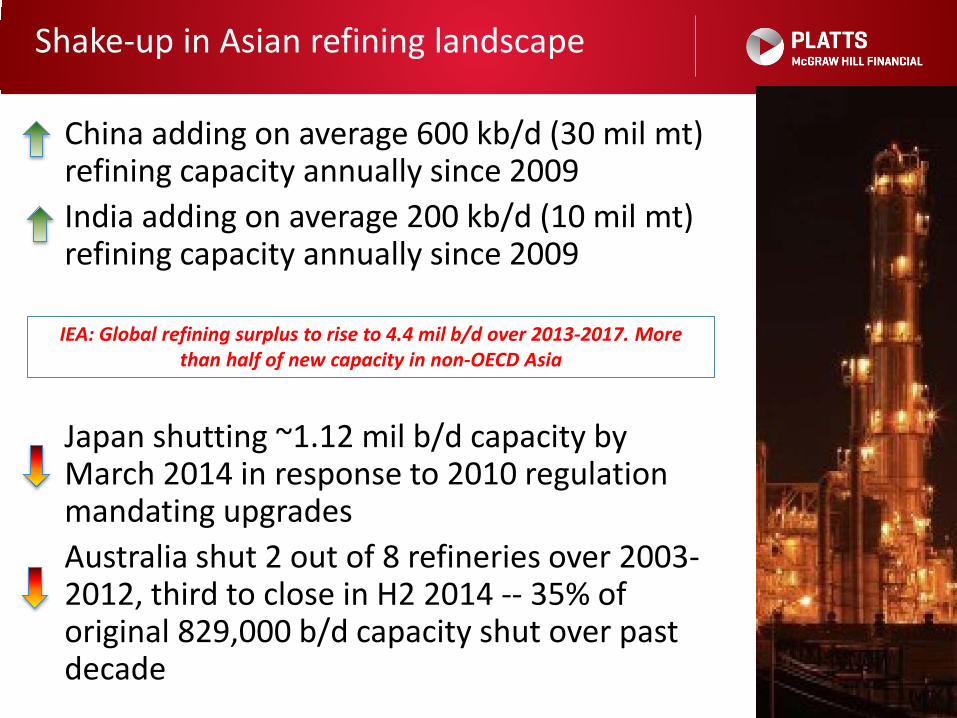

China adding on average 600 kb/d (30 mil mt) refining capacity annually since 2009 India adding on average 200 kb/d (10 mil mt) refining capacity annually since 2009

Japan shutting ~1.12 mil b/d capacity by March 2014 in response to 2010 regulation mandating upgrades Australia shut 2 out of 8 refineries over 2003- 2012, third to close in H2 2014 -- 35% of original 829,000 b/d capacity shut over past decade

11

Shake-up in Asian refining landscape

IEA: Global refining surplus to rise to 4.4 mil b/d over 2013-2017. More than half of new capacity in non-OECD Asia

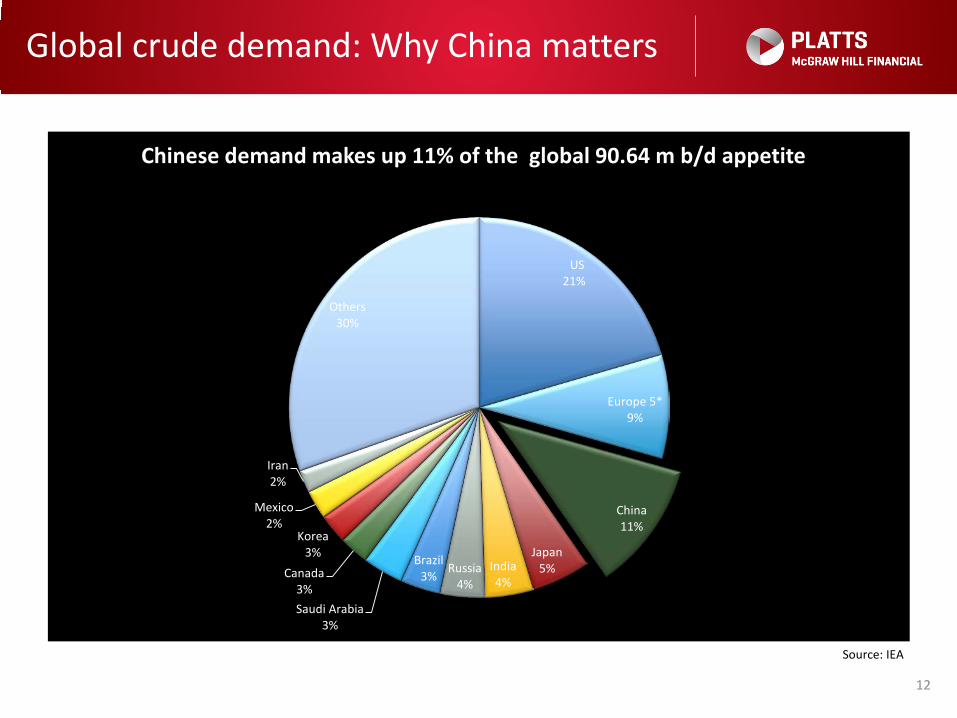

Global crude demand: Why China matters

12

US 21%

Europe 5* 9%

China 11%

Japan 5% India

4% Russia

4%

Brazil 3%

Saudi Arabia 3%

Canada 3%

Korea 3%

Mexico 2%

Iran 2%

Others 30%

Chinese demand makes up 11% of the global 90.64 m b/d appetite

Source: IEA

China has been slightly shifting its crude oil buying patterns

13

Saudi Arabia 20.25%

Angola 14%

Iraq 9%

Russia 9%

Oman 8%

Iran 7%

Venezuela 5%

Kazakhstan 4%

UAE 4%

Kuwait 3%

Other countries 17%

China crude imports Jan-Mar 2013 Jan-Mar 2013 (mt)

Saudi Arabia 13,971,171 Angola 9,705,699 Iraq 6,231,675 Russia 6,011,360 Oman 5,563,428 Iran 5,048,482 Venezuela 3,516,708 Kazakhstan 2,908,518 UAE 2,389,060 Kuwait 2,229,957 Other countries 11,401,510 Total 68,977,568

China is now importing more Latin American grades: Vasconia, Castille Blend, Napo, Oriente, Maya, Mesa 30, Marlim, Escalante, Santa Barbara grades

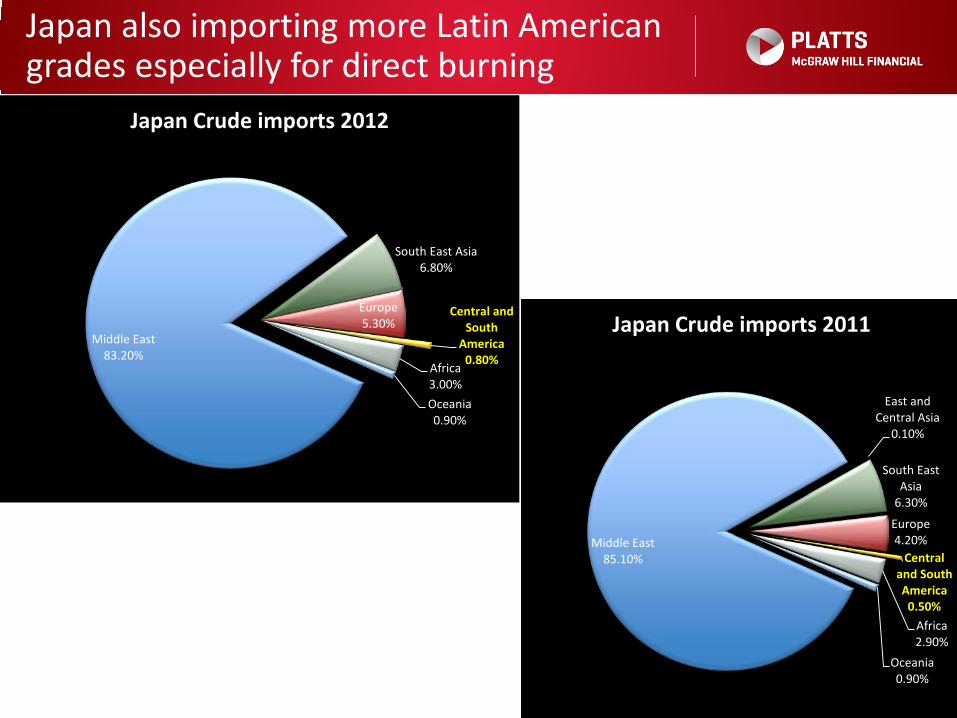

Japan also importing more Latin American grades especially for direct burning

14

Middle East 85.10%

East and Central Asia

0.10%

South East Asia

6.30%

Europe 4.20%

Central and South America

0.50% Africa 2.90%

Oceania 0.90%

Japan Crude imports 2011 Middle East

83.20%

South East Asia 6.80%

Europe 5.30%

Central and South

America 0.80% Africa

3.00% Oceania 0.90%

Japan Crude imports 2012

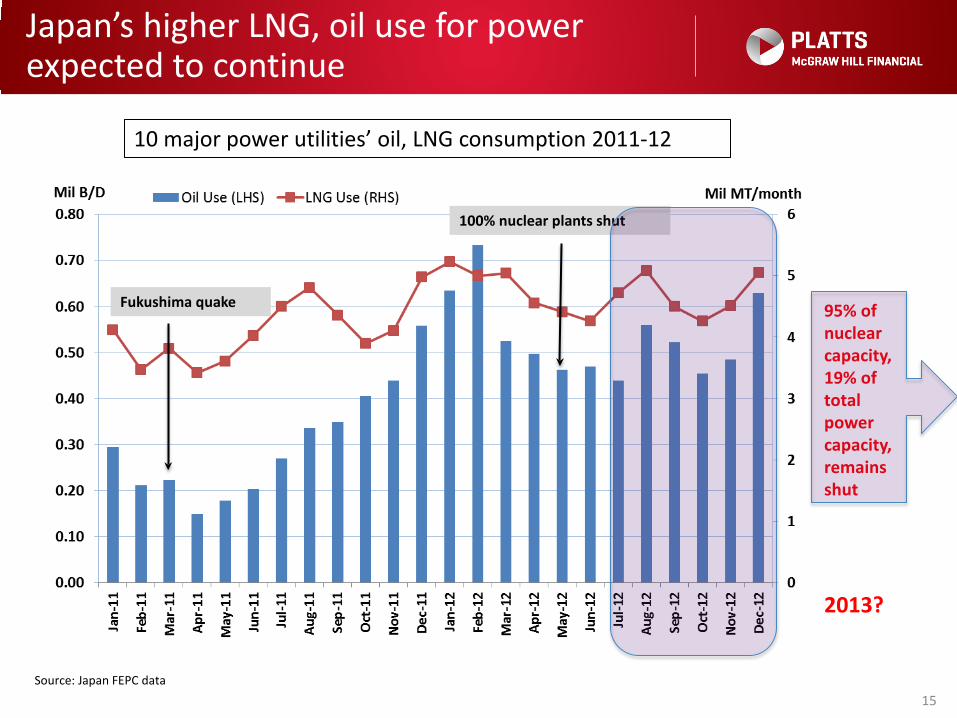

Japan’s higher LNG, oil use for power expected to continue

15

10 major power utilities’ oil, LNG consumption 2011-12

Source: Japan FEPC data

Fukushima quake

100% nuclear plants shut

95% of nuclear capacity, 19% of total power capacity, remains shut

2013?

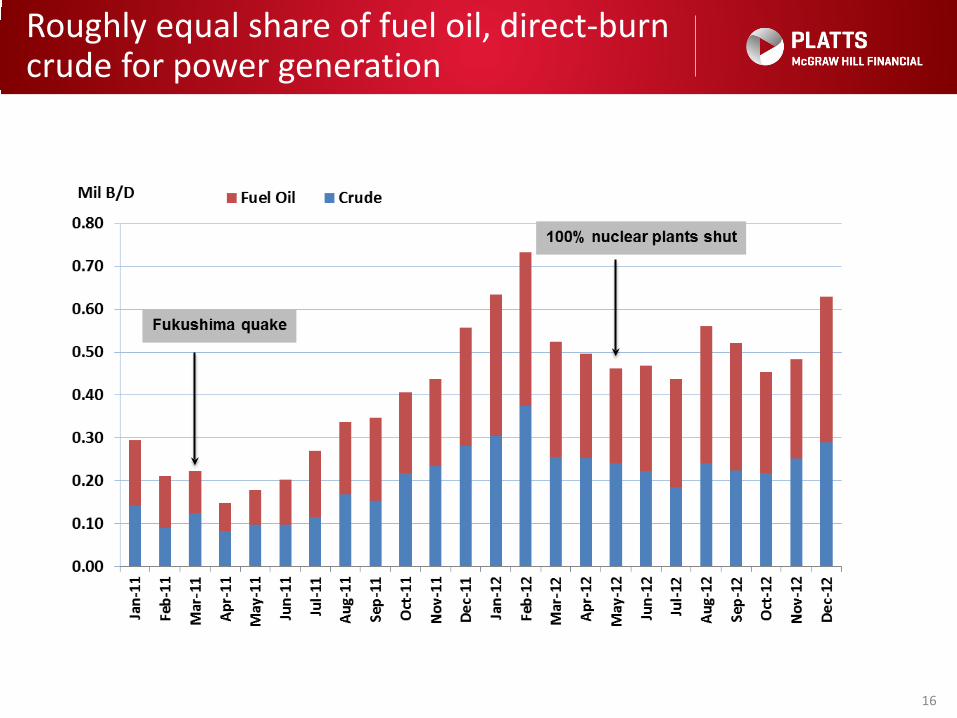

Roughly equal share of fuel oil, direct-burn crude for power generation

16

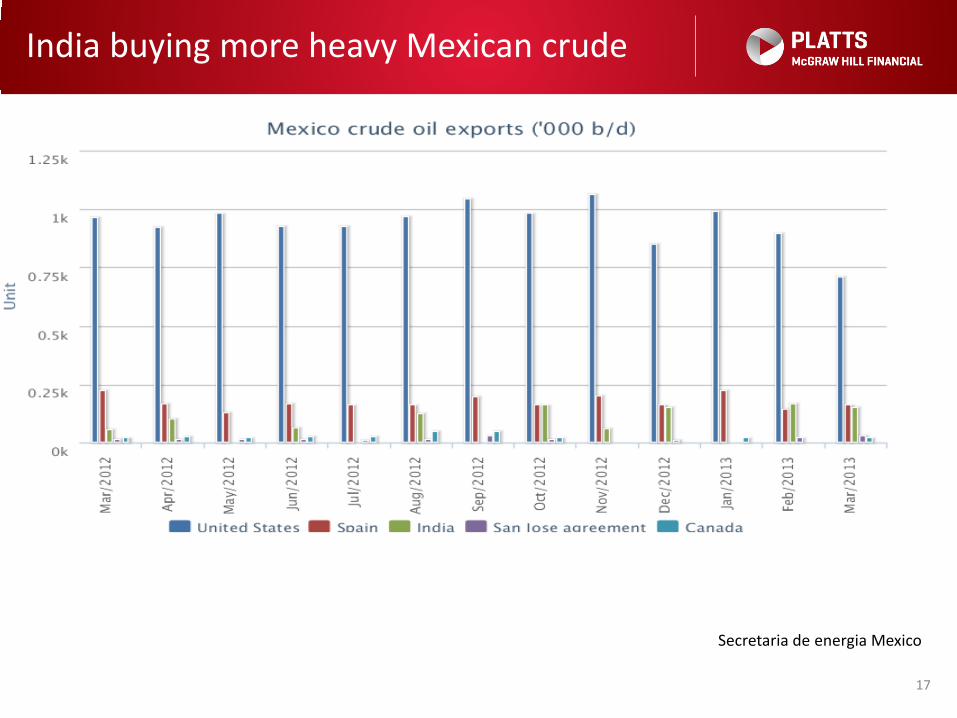

India buying more heavy Mexican crude

Secretaria de energia Mexico

17

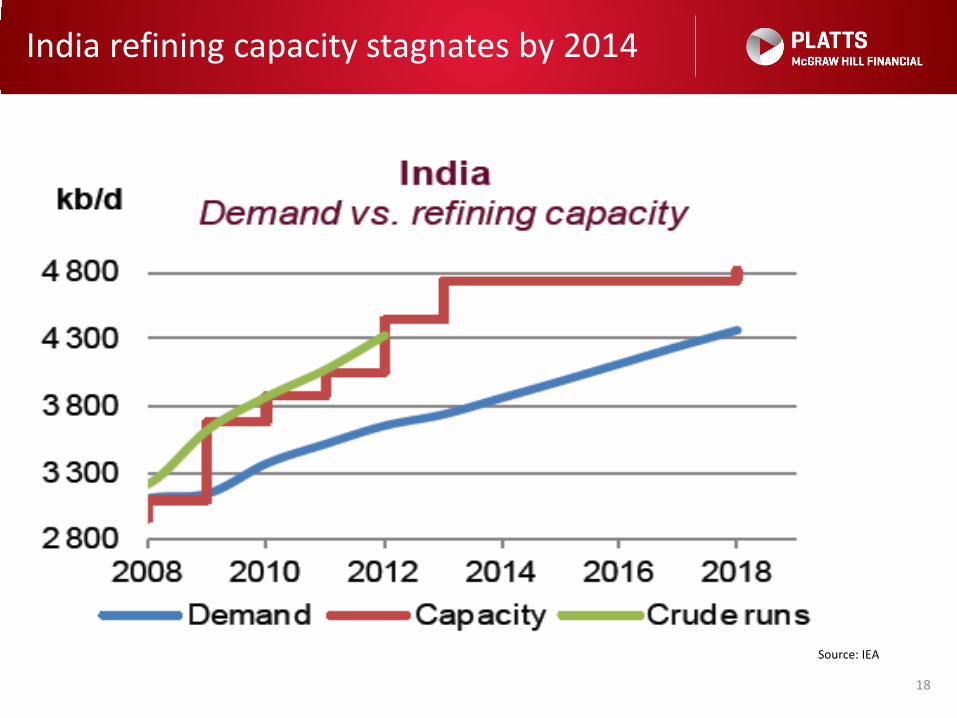

India refining capacity stagnates by 2014

18

Source: IEA

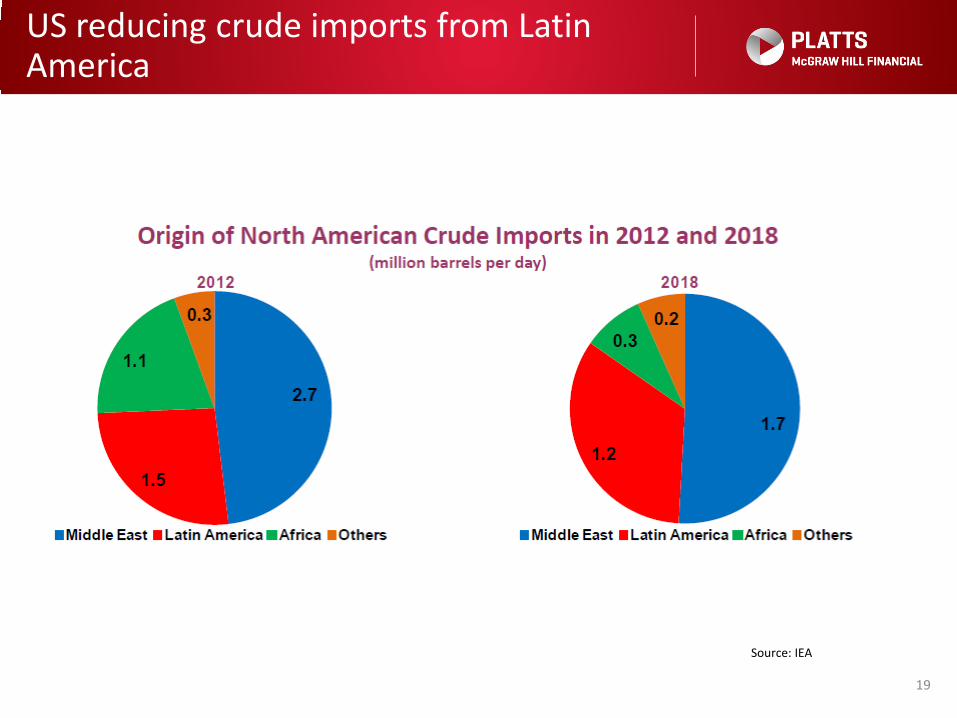

US reducing crude imports from Latin America

19

Source: IEA

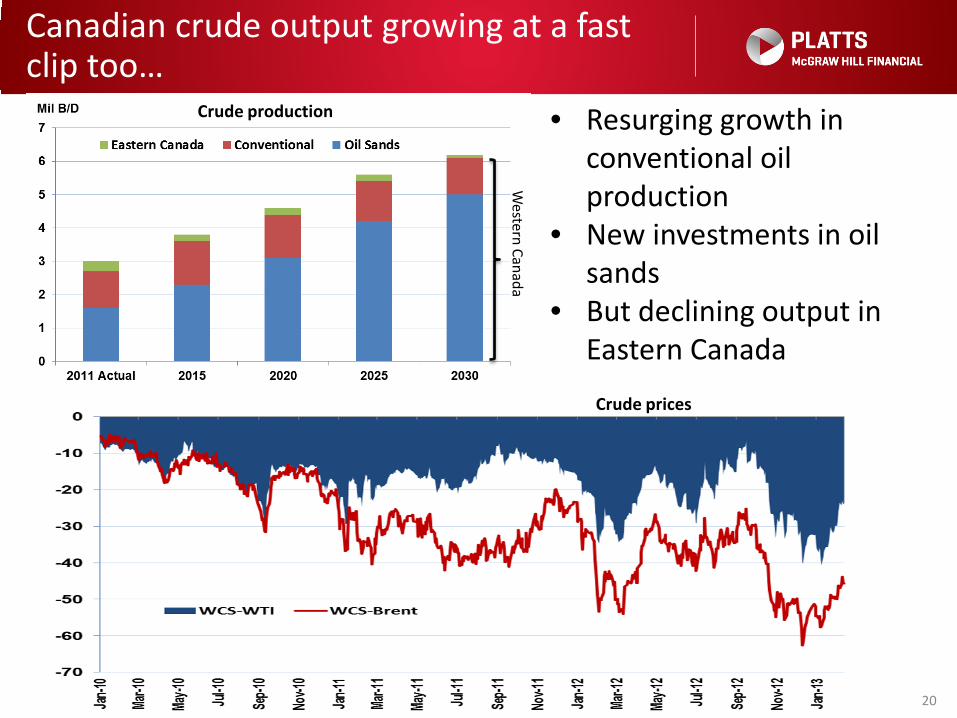

Canadian crude output growing at a fast clip too…

20

Source: Canadian Association of Petroleum Producers

• Resurging growth in conventional oil production

• New investments in oil sands

• But declining output in Eastern Canada

Western Canada

Crude production

Crude prices

Canadian, Colombian exports to US gain in recent years; Mexico and Venezuela down

21

Between 2008-2012: Imports from Canada UP 18% to ~2.9 mil b/d Imports from Colombia UP 118% to ~ 440 kb/d

Imports from Mexico DOWN 21% to ~ 1 mil b/d Imports from Venezuela DOWN 22% to ~ 930 kb/d

Source: EIA

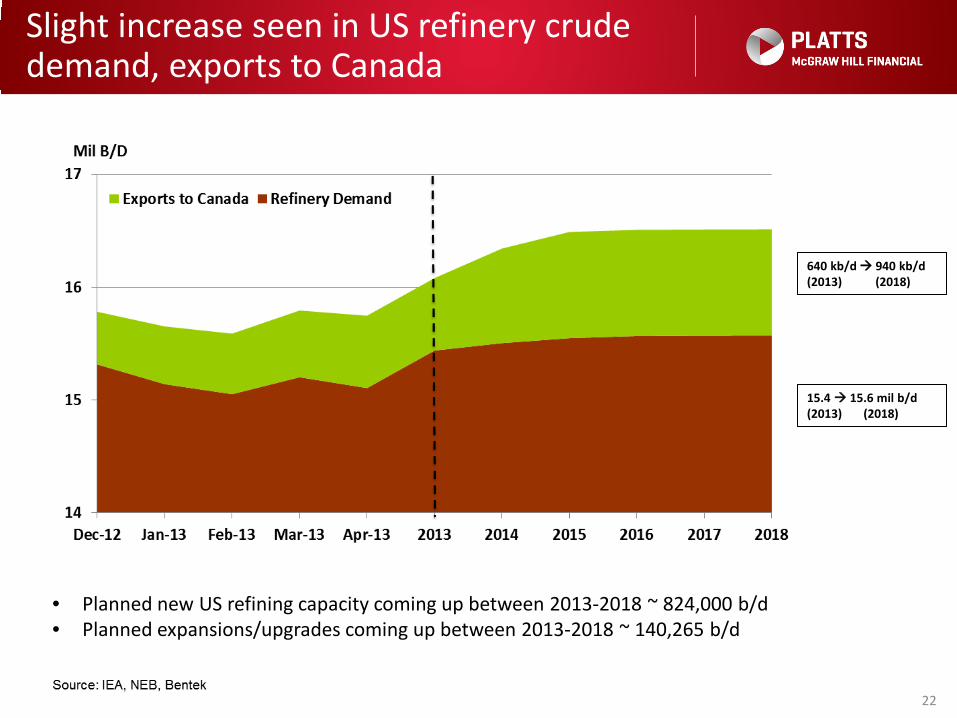

Slight increase seen in US refinery crude demand, exports to Canada

22

15.4 15.6 mil b/d (2013) (2018)

640 kb/d 940 kb/d (2013) (2018)

• Planned new US refining capacity coming up between 2013-2018 ~ 824,000 b/d • Planned expansions/upgrades coming up between 2013-2018 ~ 140,265 b/d

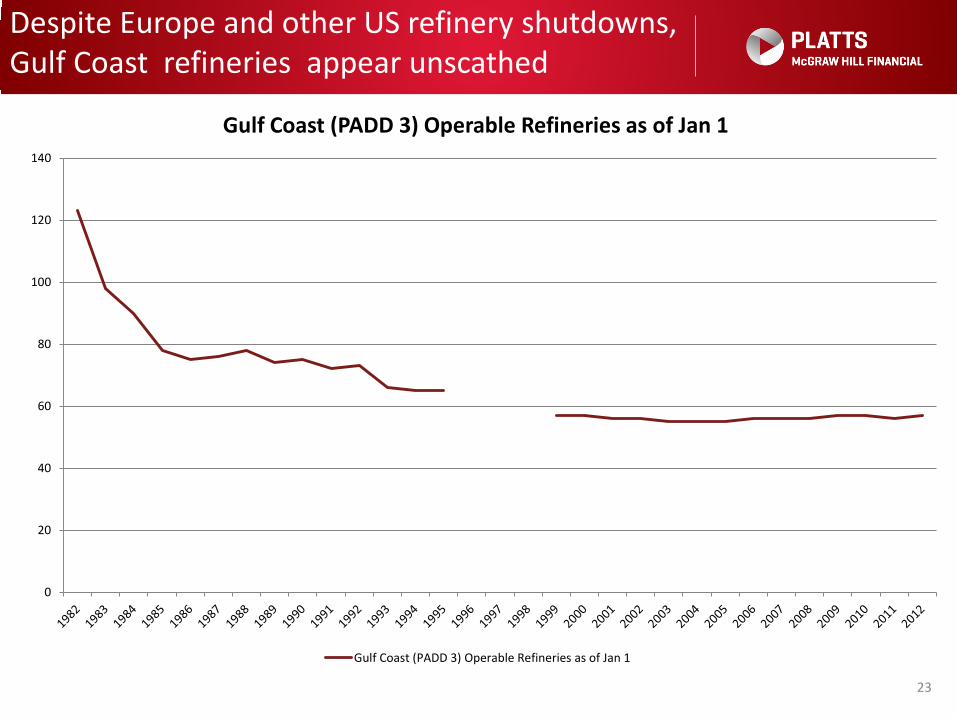

Despite Europe and other US refinery shutdowns, Gulf Coast refineries appear unscathed

23

0

20

40

60

80

100

120

140

Gulf Coast (PADD 3) Operable Refineries as of Jan 1

Gulf Coast (PADD 3) Operable Refineries as of Jan 1

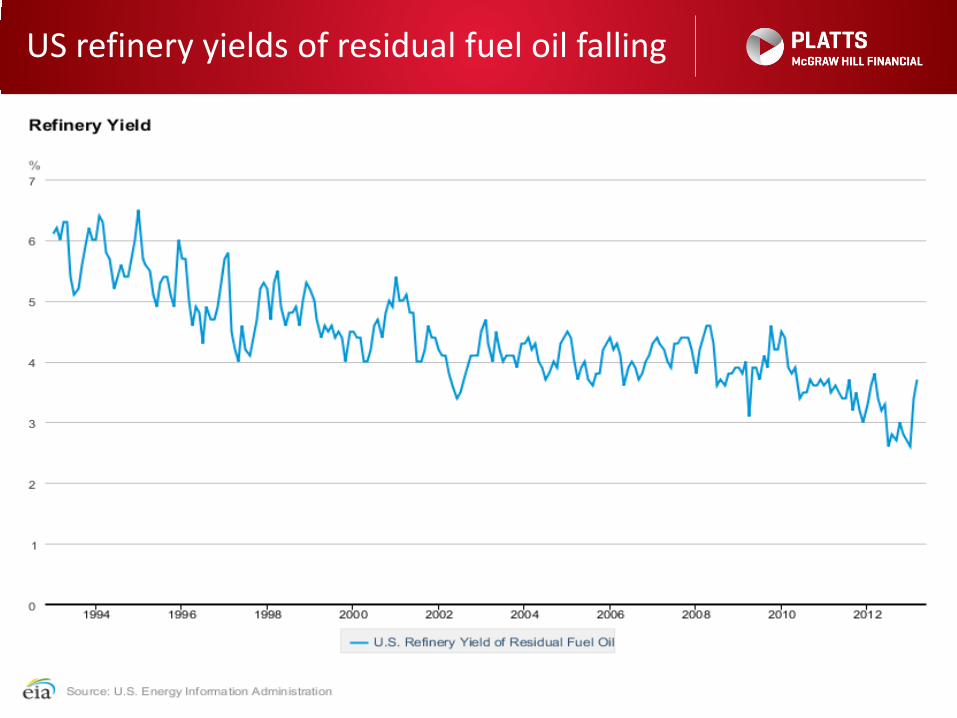

US refinery yields of residual fuel oil falling

24

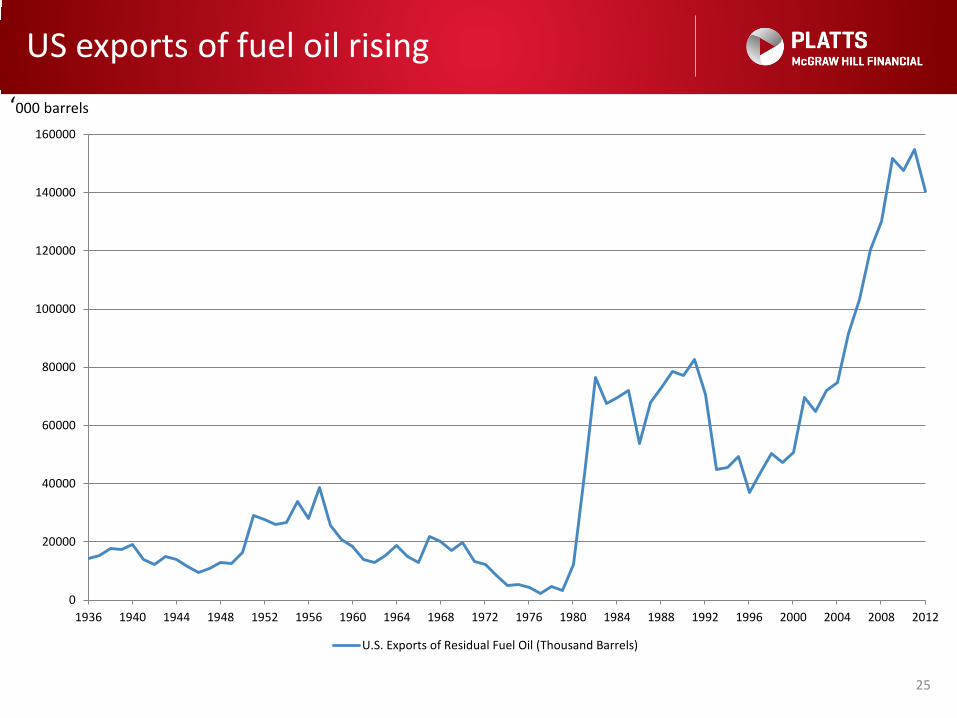

US exports of fuel oil rising

25

0

20000

40000

60000

80000

100000

120000

140000

160000

1936 1940 1944 1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012

U.S. Exports of Residual Fuel Oil (Thousand Barrels)

‘000 barrels

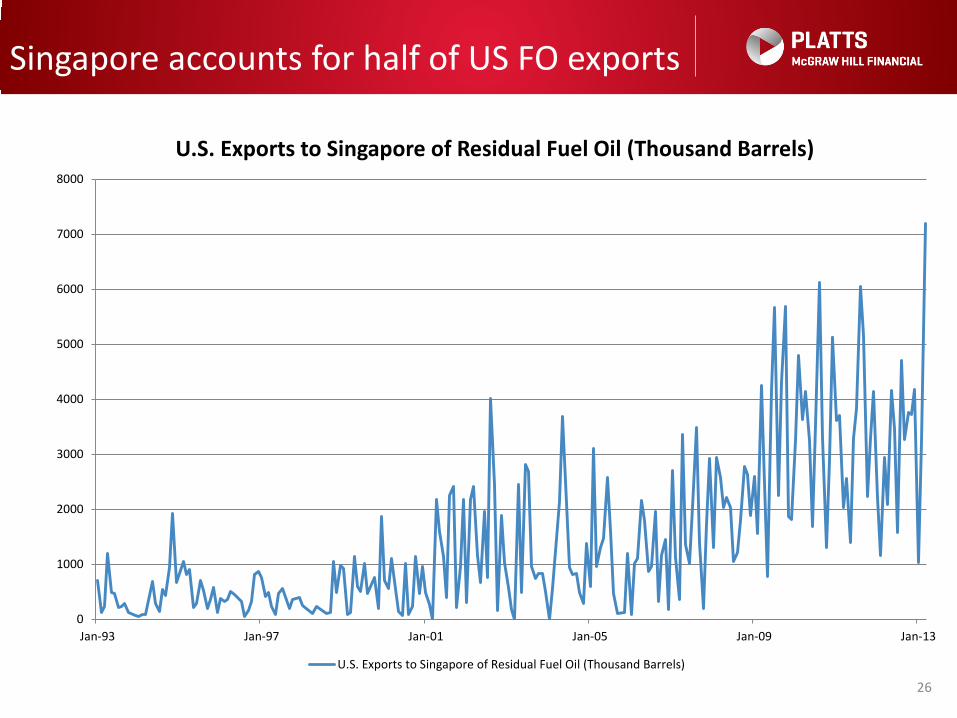

Singapore accounts for half of US FO exports

26

0

1000

2000

3000

4000

5000

6000

7000

8000

Jan-93 Jan-97 Jan-01 Jan-05 Jan-09 Jan-13

U.S. Exports to Singapore of Residual Fuel Oil (Thousand Barrels)

U.S. Exports to Singapore of Residual Fuel Oil (Thousand Barrels)

Tightening sulfur limits – supply concerns

27