global retail & supply chain perspectives

TRANSCRIPT

1

Hozefa Saylawala

Director of Sales – Middle East

Global Retail & Supply Chain Perspectives

2

A new reality has arrived!

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2019 2020 2021 2022 2023 2024 2025

Global: Top level channel metrics, COVID-19 re-forecasts, year-on-year growth, 2019-2025 (%)

Hyper-Stores Supermarkets & Neighbourhood Stores Discount Convenience Consumer Electronics Fashion and Apparel Department Stores Ecommerce Pharma & Health

3Global COVID-19 Forecast Update, May 2020 Source: Edge by Ascential channel forecasts. Data sourced on 22 May 2020, variations may occur on data sourced after this time.

As consumers worry about leaving home and

physical stores are shut for months, we expect

ecommerce growth to accelerate by 8.2

percentage points in 2020, as we are revising

our growth outlook from +22.2% to +30.4%.

Grocery channels are benefitting

from stockpiling and increased

home eating in 2020. Meanwhile,

the pharma & health channel is

receiving a boost from rising

health and hygiene awareness.

Non-food channels will see sales take heavy

hits in 2020. Despite bouncing back in 2021,

most will not return to pre-COVID-19 sales

levels as part of revenue is permanently lost to

online.

Impact of Covid

The COVID-19 consumer

47%49%

"I am cutting back on my spending" "Given the economy and my personalfinances, I have to be very careful

how I spend my money"

% of consumers who strongly agree (Source: McKinsey, US only)

CAUTIOUS ABOUT SPENDING

Retailer/Supplier Action: Ensure product visibility across all

pricing brackets with an emphasis on value proposition, drive

price transparency

MOTIVATED BY GOOD HEALTH, HYGEINE & WELLNESS

Retailer/Supplier Action: Re-align product portfolio and

ingredients towards health-focused products, increase services

tailored towards healthcare and wellness.

COMMUNITY-CENTRIC

43% of people said they have felt closer to their neighbors and

local community since the lockdown began. (Source: Retail Week)

Retailer/Supplier Action: Implement more localized campaigns and

purpose-led initiatives e.g. charitable giving. Consider adapting

ranges and sourcing with a stronger emphasis on local.

VALUES TRANSPARENCY & TRUST

49% of consumers are willing to pay a premium for products of high-quality

assurances and safety standards (Source: WGSN, Nielsen)

Retailer/Supplier Action: Prioritize product quality

credentials, review sourcing practices, enhance supply

chain traceability

73% of consumers plan to eat and drink more healthily in response to

COVID-19 (Source: FMCG Guru)

ZEBRA TECHNOLOGIES 5

OmnichannelManaging a new Retail Mix

ZEBRA TECHNOLOGIES 6

Today’s Supply Chain is ComplexSatisfying customers is no simple matter

ZEBRA TECHNOLOGIES

Customer

StoreThird-PartyLogistics

ManufacturerPlant / Warehouse

Warehouse / Distribution Center / Fulfillment Center

Retail or Wholesale Customer Service and Corporate Operations

New shipping mandates

Suppliers

Raw Materials

Real timeInventory status

Ship direct to customer

Ship to store

Finished goods

Returns

Returns

Real timeitem status

Pallet shipping

Real timeInventory status

Real timeInventory status

Real timeInventory status

Returns

Real timeInventory status

Returns

Ship to store

Ground orders

Rush orders

Pick-up instore

Shipment fromclosest location

Zebra Warehouse Maturity ModelAn incremental and strategic modernization framework

7

Barcode

Wearable

& Voice

Optimize use

of mobility

Wide-spread

use of real-time

visibility

Targeted use of

real-time visibility

Sensors

Locationing

Intelligent

Automation

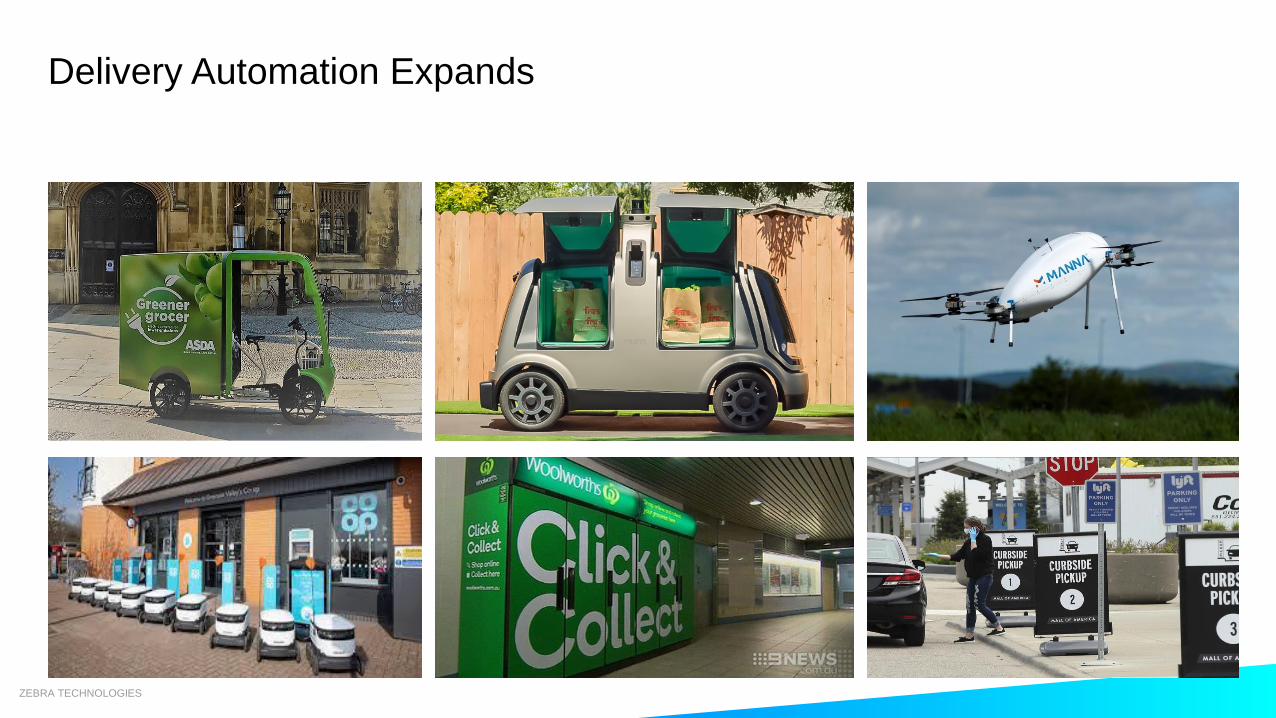

Delivery Automation Expands

ZEBRA TECHNOLOGIES

2015

Last Mile Delivery Ecosystem

Traditional Delivery Click and Collect Crowd-Sourced Delivery Autonomous Delivery

Amazon is touching all leading package delivery avenues

How will consumers decide?

Whichever option is faster and/or cheaper

• ~80% of goods can fit into the

automated system

• Manual pick section is dedicated

for oversized items

• SKU consolidation lanes have

strong potential for robotic arm

applications

Is Micro-Fulfilment

The Answer?

ZEBRA TECHNOLOGIES

Solution Provider Company Sites Solution Type Site Location

Alert Innovation Walmart 1 MFC US

Attabotics Canadian Tire 2 MFC Canada

Gordon Foods 1 MFC Canada

Nordstrom 2 CFC US

Autostore/Swisslog ASDA 1 CFC UK

Best Buy 3 CFC US

Best Buy 3 MFC US

Competec 1 CFC Switzerland

HEB 1 MFC US

Puma 1 CFC US

Dematic Amazon 1 CFC US

Big W 1 CFC Australia

Meijer 1 MFC US

Tesco 2 CFC UK

Ocado Casino 1 CFC France

Coles 2 CFC Australia

Kroger 20 CFC US

Sobeys 2 CFC Canada

Takeoff/Knapp Ahold/Stop&Shop 50 MFC US

Albertsons/Safeway 2 MFC US

Carrefour 1 MFC Middle East

Loblaw 1 MFC Canada

Sedano’s 1 MFC US

Wakefern/ ShopRite 1 MFC US

Woolworths 2 MFC Australia

Wincanton Waitrose 1 CFC UK

DEMATIC

Retail Customer Adoption of MFCs (as of Sept 2020)

Smarter Warehouses

Robots & Co-bots

• Increased automation to

support omnichannel picking

– Amazon

– Alibaba

– Fetch

– Ocado

– Walmart AlphaBot

12

Warehouse Automation Competitive Segments

Manual Carts Follow Bots Co-BotsShelf-to-Person Bots

• Rapid deployment

• Increased operational efficiency

for workforce

• Typically quickest ROI

• Shelf-movement bots

• Requires reconfiguration of warehouse

• Brings goods to the picker

• Improves efficiency, but requires high

degree of direct human interaction with

the robot (fixed worker-to-robot ratio)

• Current solution, which leverages

Zebra devices on every picker

ZEBRA TECHNOLOGIES

ZEBRA TECHNOLOGIES

Convenience Store of the Future

ReturnsPick Up Shop Simple

Hot Food Local SourcingSelf-Service

ZEBRA TECHNOLOGIES

The Big Retail Tech Plays

▪Customer Analytics

▪Customer Apps & Interaction

▪Augmented reality

▪Voice

▪AI & Automation

▪Smart Stores

▪Mobility - Digitally Connected Staff

16

Thank You

ZEBRA and the stylized Zebra head are trademarks of ZIH Corp, registered in many jurisdictions worldwide. All other trademarks are the property of their

respective owners. ©2018 ZIH Corp and/or its affiliates. All rights reserved.