global tax accounting services newsletter … · the global tax accounting services newsletter is a...

TRANSCRIPT

Global tax accounting services newsletter

Focusing on tax accounting issues affecting businesses today

April—June 2014

SubscriptionPrintHome

The Global tax accounting services newsletter is a quarterly publication from PwC’s Global Tax Accounting Services Group. It highlights issues that may be of interest to tax executives, finance directors, and financial controllers.

In this issue, we provide an update on country-by-country reporting, the OECD’s project on hybrid mismatch arrangements, and the new converged standard on revenue recognition recently issued by the Financial Accounting Standards Board and International Accounting Standards Board.

We also draw your attention to some significant tax law and tax rate changes that occurred around the globe during the quarter ended 30 June 2014.

Finally, we discuss the importance of technology in tax function effectiveness.

If you would like to discuss any items in this newsletter, tax accounting issues affecting businesses today, or general tax accounting matters, please contact your local PwC team or the relevant Tax Accounting Services network member listed at the end of this document.

Readers should not rely on the information contained within this newsletter without seeking professional advice. For a thorough summary of developments, please consult with your local PwC team.

Andrew WigginsGlobal and UK Tax Accounting Services Leader+44 (0) 121 232 [email protected]

Introduction

Global tax accounting services newsletter

SubscriptionPrintHome

In this issue

Accounting and reporting updatesu Country-by-country reporting

u Hybrid mismatch arrangements

u New standard on revenue recognition

Recent and upcoming major tax law changesu Notable tax rate changes

u Other important tax law changes

Tax accounting refresheru Importance of technology for tax function effectiveness

Contacts and primary authorsu Global and regional tax accounting leaders

u Tax accounting leaders in major countries

u Primary authors

Global tax accounting services newsletter

SubscriptionPrintHome

4

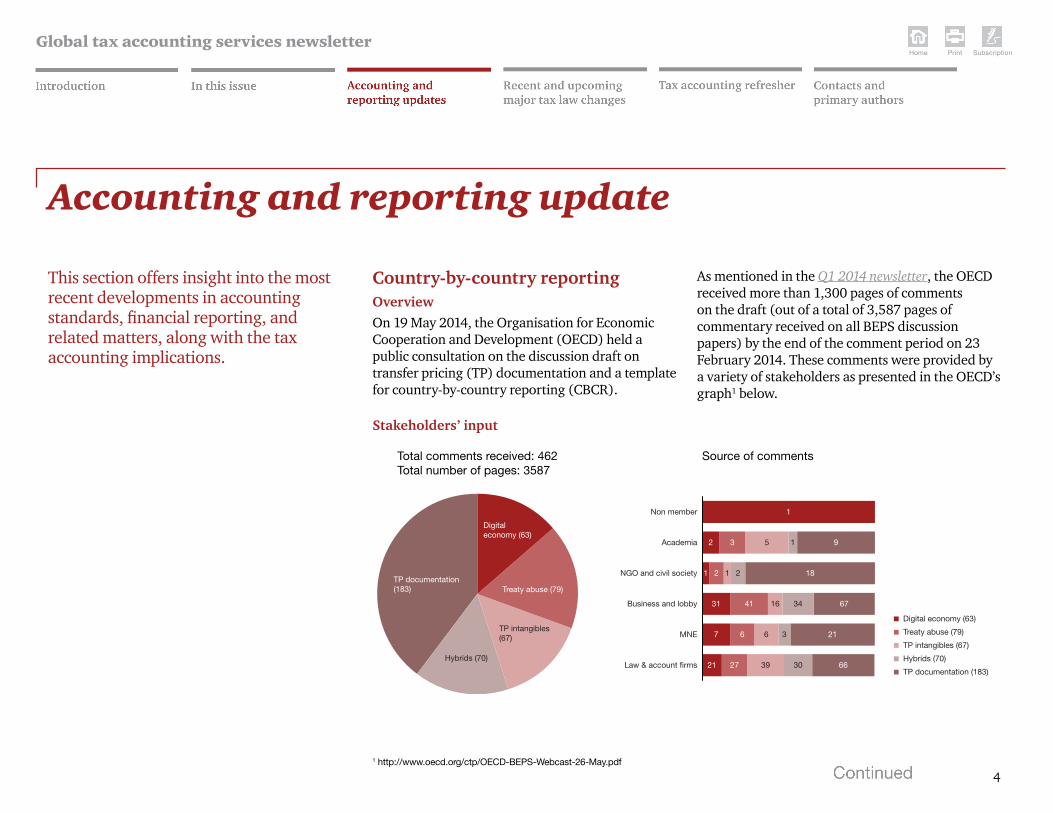

Country-by-country reporting Overview On 19 May 2014, the Organisation for Economic Cooperation and Development (OECD) held a public consultation on the discussion draft on transfer pricing (TP) documentation and a template for country-by-country reporting (CBCR).

As mentioned in the Q1 2014 newsletter, the OECD received more than 1,300 pages of comments on the draft (out of a total of 3,587 pages of commentary received on all BEPS discussion papers) by the end of the comment period on 23 February 2014. These comments were provided by a variety of stakeholders as presented in the OECD’s graph1 below.

This section offers insight into the most recent developments in accounting standards, financial reporting, and related matters, along with the tax accounting implications.

Accounting and reporting update

1 http://www.oecd.org/ctp/OECD-BEPS-Webcast-26-May.pdf

Stakeholders’ input

Total comments received: 462Total number of pages: 3587

Source of comments

TP documentation (183)

Digital economy (63)

Treaty abuse (79)

TP intangibles (67)

Hybrids (70)

Non member 1

2 3 5

18

6734164131

7

21 27 39 30 66

6 6 3 21

2121

1 9Academia

NGO and civil society

Business and lobby

MNE

Law & account firms

Digital economy (63)

Treaty abuse (79)

TP intangibles (67)

Hybrids (70)

TP documentation (183)

Global tax accounting services newsletter

SubscriptionPrintHome

5

– stated capital and accumulated earnings

– number of employees, and

– tangible assets other than cash and cash equivalents.

• The OECD tentatively decided not to include a materiality threshold for the CBCR template so no country is precluded from receiving information.

• Representatives from multinationals encouraged flexibility with respect to the source of data, limiting required data points to those that are ‘useful, relevant, non-duplicative, and cost-effective’, and limiting the use of the CBCR template to a high-level risk assessment. It was further advocated that tax authorities be required to maintain confidentiality of the information received on the CBCR template.

• The BEPS Monitoring Group, a non-governmental organisation (NGO), stated that the information to be included in the CBCR template was not commercially sensitive, that the information should be made public, that requiring disclosure by country might provide an incentive for multinationals to use less complex structures, and that the cost of compliance should not be considered in determining the content of the CBCR template.

• There was also extensive discussion regarding the need and burden associated with providing intra-group payment information and the importance of confidentiality.

Mechanism for filing and sharing of the CBCR template• The OECD stated that it is still considering the

best way for the CBCR template to be filed and shared. It is also concerned that options which increase confidentiality may create obstacles to information sharing and slow the process. As such, the OECD is trying to arrive at a system that will work for all countries.

• Different views were expressed during the consultation regarding filing of the CBCR template. While some stakeholders expressed a view that the template should be filed where the business is taking place, multinationals advocated the option of filing the template with the tax authority of the ultimate parent, which can then be shared through treaty networks.

• The OECD questioned the need for a treaty-based sharing mechanism, noting that many countries do not have an extensive treaty network, and such a system would limit access to information by developing countries.

The OECD also provided an update on the Transfer Pricing (TP) documentation and the CBCR template during its third Base Erosion and Profit Shifting (BEPS) public webcast on 26 May 2014 and the 2014 OECD International Tax Conference in Washington, DC on 2 and 3 June 2014.

Key topics discussed during the public consultationDiscussion during the OECD’s public consultation on 19 May 2014 was predominantly focused on the content of the CBCR template and the mechanism for filing and sharing of the CBCR template. A few key items are summarised below.

Content of the CBCR template• The OECD’s tentative changes made to the

original CBCR template were consistent with those reported earlier (see the Q1 2014 newsletter). Information in the revised draft CBCR template will be reported by country and include the following:

– revenue (broken down by unrelated party and related party)

– profit (loss) before income tax

– income tax paid (on a cash basis)

– income tax accrued – current year

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

6

OECD’s updateDuring its third public BEPS webcast and the International Tax Conference, the OECD provided an update on the CBCR template, highlighting the following:

• The CBCR template will be a separate document.

• Options for sharing the CBCR template with local tax authorities are still being considered.

• A monitoring mechanism needs to be developed to assess the effectiveness and efficiency of the template.

• A structured and careful implementation will be necessary to guarantee the following:

– consistency in the approaches by governments

– availability of the relevant information to governments on a timely basis

– confidentiality of commercially sensitive information

– balanced cost for taxpayers and tax administrators, and

– use of the information as intended.

What’s next?The CBCR template will be presented to the G20 Finance Ministers at the September meeting in Cairns and the G20 Leaders meeting in Brisbane in November 2014.

Given the need for careful implementation, however, the OECD will continue to work on implementation and filing issues and report on these matters in January 2015.

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

7

Accounting and reporting update

Hybrid mismatch arrangementsOverviewOn 19 March 2014, the OECD released two draft reports calling for the introduction of domestic rules and amendments to the OECD Model Tax Convention to neutralise the effect of hybrid mismatch arrangements. The recommendations of the OECD on hybrids mismatch arrangements result from Action 2 of the BEPS Action Plan.

The OECD received more than 400 pages of comments on the draft reports, including a response from PwC, by the end of the comment period that expired on 2 May 2014 (see stakeholders involved in the consultation process in the OECD graph on page 4).

The OECD also held a public consultation on 15 May 2014 to discuss the reports, and provided an update on their status during the third BEPS webcast on 26 May 2014 and the 2014 OECD International Tax Conference in Washington, DC on 2 and 3 June 2014.

OECD’s draft reports on hybridsThe OECD draft reports on hybrid mismatch

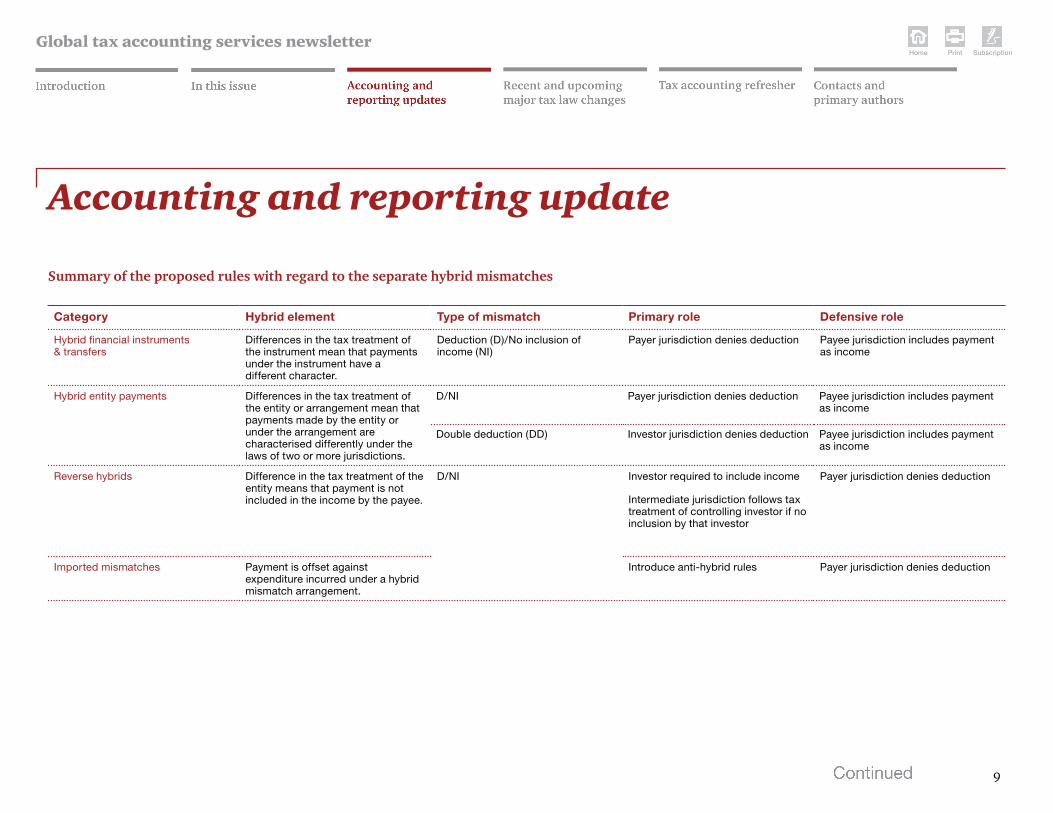

arrangements have a strong focus on intra-group financing, although other arrangements are not excluded. The reports focus on the incidence of double non-taxation and measures to combat such occurrences (see a summary of the proposed rules with regard to separate hybrid mismatches in the table on page 9).

To ensure appropriate balance, it will be important that the OECD address the potential for double taxation which could, inadvertently or otherwise, arise as a consequence of the proposed changes.

The draft reports describe ‘hybrid mismatch arrangements’ as being the result of a difference in the characterisation of an entity or arrangement under the laws of two or more tax jurisdictions that result in a mismatch in tax outcomes. The hybrid mismatch arrangements targeted in the reports are those that result in a lower aggregated tax burden for the parties involved. The OECD considers these arrangements to harm competition, economic efficiency, transparency, and fairness.

The first report (which is both lengthy and complex) recommends amendments to domestic laws to negate the tax consequences identified by the OECD. The tax consequences targeted are categorised in

three different hybrid mismatch arrangements that produce what the OECD has identified as profit shifting or base erosion consequences. The first draft report contains detailed rules designed to address these outcomes.

The second draft report examines treaty issues relating to dual-resident entities and transparent entities. It also points out that the report (Preventing the Granting of Treaty Benefits in Inappropriate Circumstances), recently released by the OECD in the context of Action 6 (Treaty abuse) of the BEPS action plan, already addresses some concerns in relation to the issues of dual-resident entities and ‘hybrid mismatch arrangements’ with the proposed changes to the OECD Model Tax Convention. Where no treaty is involved, solutions for these concerns need to be found in domestic law.

Challenges for multinationalsIf the recommendations in the reports are adopted without appropriate safeguards for scope and application, they are likely to create significant challenges for multinationals. Such challenges may include the following:

• requirement to comply with widely varying provisions across multiple tax jurisdictions

Global tax accounting services newsletter

SubscriptionPrintHome

8

• increased uncertainty (e.g., in situations where deductions in one jurisdiction are claimed on the accrual basis and the inclusion in the payee’s jurisdiction may not arise for some time)

• the clear risk of double taxation, and

• materially increased levels of complexity regarding intra-group cash flow and treasury management.

Issues highlighted in PwC’s responsePwC’s response to the OECD’s discussion drafts on ‘hybrid mismatch arrangements’ included a number of recommendations in relation to the above issues:

• Due to the existence of many related-party arrangements where there is no abuse, the proposed approach could have disproportionate consequences and could negatively impact global trade and investment in an unforeseen manner. As such, a purpose or motive test should be included to cover all instances.

• Sufficient time should be dedicated to allow for modifications to the design of the recommendations. These modifications should ensure that the recommendations with regard to hybrid mismatches are focused only on abusive outcomes; do not result in situations which give rise to double taxation; and are

coordinated with the work of the other key working groups on controlled foreign companies, interest deductibility, treaty abuse, and harmful tax practices.

• If a delay in publishing the final report on hybrids beyond the scheduled date is considered unacceptable, the report should adopt an interim solution, pending the outcome of the other relevant work streams. This interim solution should include a purpose or motive test.

• It should be clarified that countries are urged to not unilaterally enact legislation on hybrid outcomes until conclusions have been reached on the other key interrelated work streams, and consensus is reached on a final set of uniform principles to be applied.

OECD’s update As mentioned above, the OECD provided a brief update on the hybrid mismatch arrangement project during its third BEPS webcast on 26 May 2014 and the 2014 OECD International Tax Conference held in Washington, DC on 2 and 3 June 2014.

The OECD highlighted that the recommendations for changes to domestic law (and to a lesser extent treaty rules) are progressing largely as intended. They also suggested that several issues (e.g., how

much should be left to the domestic legislations to address, whether timing differences should be considered hybrid mismatches, whether the rules should apply outside the related party and controlled group context) are still being considered. More work is required by the OECD before final guidance on hybrid mismatch arrangements can be finalised.

Tax accounting considerationsMultinationals will need to consider possible tax accounting implications of the above proposals and their timing. In particular, tax accounting considerations may include foreign exchange issues associated with the proposed changes in the tax treatment of the above hybrid instruments and uncertain tax positions.

Multinationals will also need to consider what financial disclosures in relation to the above proposals should look like, and at what point in time they should be included in financial statements.

What’s next?Similar to the CBCR template mentioned above, the report will be presented to the G20 Finance Ministers at the September 2014 meeting in Cairns and the G20 Leaders meeting in Brisbane in November 2014.

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

9

Category Hybrid element Type of mismatch Primary role Defensive role

Hybrid financial instruments & transfers

Differences in the tax treatment of the instrument mean that payments under the instrument have a different character.

Deduction (D)/No inclusion of income (NI)

Payer jurisdiction denies deduction Payee jurisdiction includes payment as income

Hybrid entity payments Differences in the tax treatment of the entity or arrangement mean that payments made by the entity or under the arrangement are characterised differently under the laws of two or more jurisdictions.

D/NI

Double deduction (DD)

Payer jurisdiction denies deduction

Investor jurisdiction denies deduction

Payee jurisdiction includes payment as income

Payee jurisdiction includes payment as income

Reverse hybrids Difference in the tax treatment of the entity means that payment is not included in the income by the payee.

D/NI Investor required to include income

Intermediate jurisdiction follows tax treatment of controlling investor if no inclusion by that investor

Payer jurisdiction denies deduction

Imported mismatches Payment is offset against expenditure incurred under a hybrid mismatch arrangement.

Introduce anti-hybrid rules Payer jurisdiction denies deduction

Summary of the proposed rules with regard to the separate hybrid mismatches

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

10

New standard on revenue recognitionOverviewOn 28 May 2014, the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) issued their long-awaited converged standard on revenue recognition titled Revenue from Contracts with Customers (Topic 606 and IFRS 15).

The largely principles-based standard addresses revenue recognition issues comprehensively for all contracts with customers for both US Generally Accepted Accounting Principles (US GAAP) and International Financial Reporting Standards (IFRS), with certain limited exceptions. The new standard supersedes the industry-specific standards that currently exist under US GAAP, including those for software, entertainment and media, telecommunication, and construction industries. Entities in these industries should expect a potentially significant impact with adoption of the new standard.

Many observers believe that the impact of the new standard will be widespread, affecting the financial reporting practices of almost every company.

Summarised below are some of the areas that could create significant challenges for entities as they transition to the new standard:

• changes to the timing of revenue recognition

• inclusion of variable consideration in revenue prior to resolution of contingencies

• allocation of revenue for bundled contracts based on standalone selling price

• determination of timing of revenue recognition for licenses of intellectual property

• consideration of time value of money

• capitalisation of certain contract costs, and

• enhanced and additional disclosure requirements.

For US tax and tax accounting implications that need to be considered in relation to the new standard, please refer to our publication New FASB, IASB revenue recognition rules could have significant US tax implications.

Challenging areas of the new standardTiming of revenue recognition Revenue is recognised when a customer obtains control of a good or service. A customer obtains control when it has the ability to direct the use of and obtain the benefits from the good or service. Transfer of control is not the same as transfer of risks and rewards, nor is it necessarily the same as the culmination of an earnings process as it is considered today. Entities will also need to apply new guidance to determine whether revenue should be recognised over time or at a point in time.

Variable consideration Entities may agree to provide goods or services for consideration that varies upon certain future events occurring or not occurring. Examples include refund rights, performance bonuses, and penalties.

Under the prior standard, these amounts are often not recognised as revenue until the contingency is resolved. Now, an estimate of variable consideration is included in the transaction price if it is probable (US GAAP) or highly probable (IFRS) that the amount will not result in a significant revenue reversal if estimates change. Even if the entire amount of variable consideration fails to meet this threshold, management will need to consider

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

whether a portion (a minimum amount) does meet the criterion. This amount is recognised as revenue when goods or services are transferred to the customer. This could affect entities in multiple industries where variable consideration is currently not recorded until all contingencies are resolved. Management will need to reassess estimates each reporting period, and adjust revenue accordingly.

There is a narrow exception for licenses of intellectual property (IP) where the variable consideration is a sales- or usage-based royalty.

Bundled contractsEntities that sell multiple goods or services in a single arrangement must allocate the consideration to each of those goods or services. This allocation is based on the price an entity would charge a customer on a standalone basis for each good or service. Management should first consider observable data to estimate the standalone selling price. An entity will need to estimate the standalone selling price if such data does not exist. Some entities will need to determine the standalone selling price of goods or services that have not previously required this assessment, such as entities that report under US GAAP and issue customer loyalty points.

LicensesEntities that license their IP to customers will need to determine whether the license transfers to the customer over time or at a point in time. A license that is transferred over time allows a customer access to the entity’s IP as it exists during the license period. Licenses that are transferred at a point in time allow the customer the right to use the entity’s IP as it exists when the license is granted. The customer must be able to direct the use of and obtain substantially all of the remaining benefits from the licensed IP to recognise revenue when the license is granted. The standard includes several examples to assist entities in making this assessment.

Time value of moneySome contracts provide the customer or the entity with a significant financing benefit (explicitly or implicitly). This is because performance by an entity and payment by its customer may occur at significantly different times. An entity should adjust the transaction price for the time value of money if the contract includes a significant financing component. The standard provides certain exceptions to applying this guidance, and a practical expedient which allows entities to ignore time value of money if the time between the transfer of goods or services and payment is less than one year.

Contract costsEntities sometimes incur costs (such as sales commissions or mobilisation activities) to obtain or fulfil a contract. Contract costs that meet certain criteria are capitalised as an asset and amortised as revenue is recognised. More costs are expected to be capitalised in some situations. Management will also need to consider how to account for contract costs incurred for contracts that are not completed upon the adoption of the standard.

DisclosuresExtensive disclosures are required to provide greater insight into revenue that has been recognised and revenue that is expected to be recognised in the future from existing contracts. Quantitative and qualitative information will be provided about the significant judgments and changes in those judgments that management made to determine revenue that is recorded.

Tax accounting considerationsBecause tax law generally prescribes special rules for recognition of revenue for tax purposes, most changes introduced by the new revenue standard will likely affect computation of book-to-tax differences and the related deferred taxes. This becomes even more challenging for multinational

11

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

companies where the impact can vary by country. We strongly recommend that companies consider the tax implications in advance of the effective dates of the new standard mentioned below, and address issues before the standard’s implementation.

Companies will also need to consider an impact of the new standard (if any) on their cash tax profile.

What’s next?The standard will be effective for US GAAP reporters for annual reporting periods beginning after 15 December 2016 for public entities and after 15 December 2017 for non-public entities, with no early adoption permitted.

The standard will be effective for IFRS reporters for the annual reporting periods beginning on or after 1 January 2017, and will allow early adoption, with no delay in effective date for non-public entities.

Companies must apply the new standards (1) retroactively to each prior reporting period presented, or (2) retroactively with the cumulative effect of initially applying the standard recognised at the date of initial application.

12

Accounting and reporting update

Global tax accounting services newsletter

SubscriptionPrintHome

13

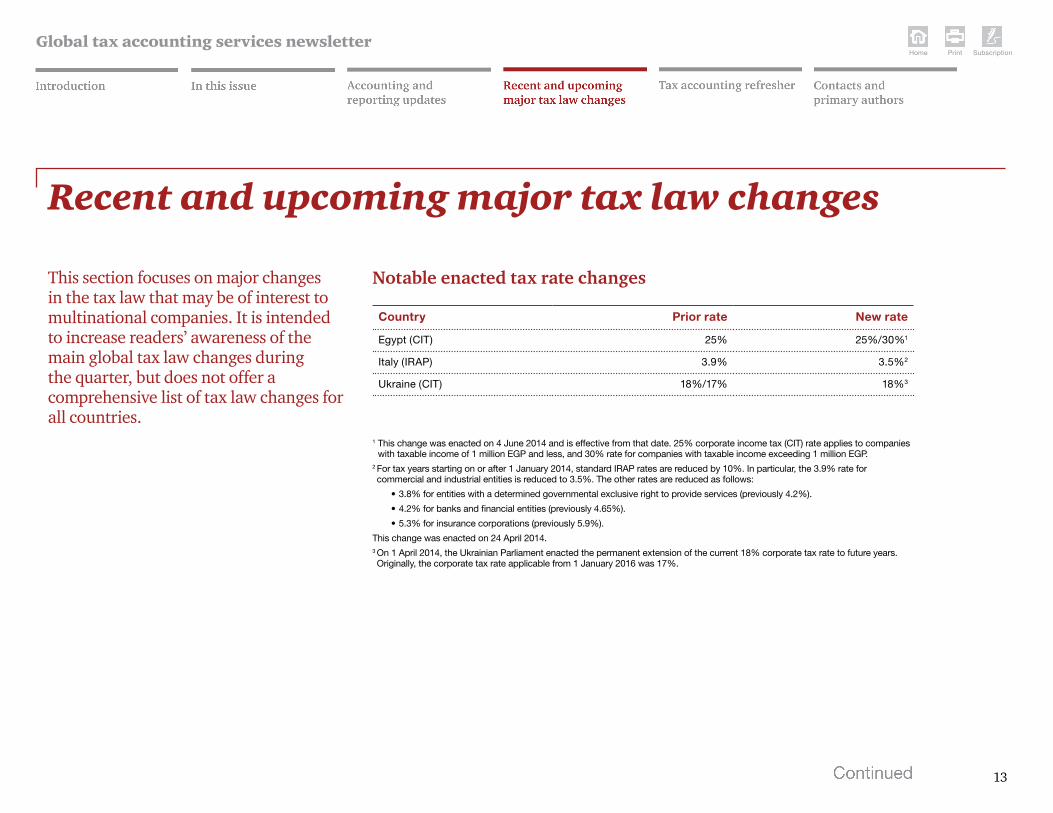

This section focuses on major changes in the tax law that may be of interest to multinational companies. It is intended to increase readers’ awareness of the main global tax law changes during the quarter, but does not offer a comprehensive list of tax law changes for all countries.

Country Prior rate New rate

Egypt (CIT) 25% 25%/30%1

Italy (IRAP) 3.9% 3.5%2

Ukraine (CIT) 18%/17% 18%3

Notable enacted tax rate changes

1 This change was enacted on 4 June 2014 and is effective from that date. 25% corporate income tax (CIT) rate applies to companies with taxable income of 1 million EGP and less, and 30% rate for companies with taxable income exceeding 1 million EGP.

2 For tax years starting on or after 1 January 2014, standard IRAP rates are reduced by 10%. In particular, the 3.9% rate for commercial and industrial entities is reduced to 3.5%. The other rates are reduced as follows:

• 3.8% for entities with a determined governmental exclusive right to provide services (previously 4.2%).

• 4.2% for banks and financial entities (previously 4.65%).

• 5.3% for insurance corporations (previously 5.9%).

This change was enacted on 24 April 2014.3 On 1 April 2014, the Ukrainian Parliament enacted the permanent extension of the current 18% corporate tax rate to future years. Originally, the corporate tax rate applicable from 1 January 2016 was 17%.

Recent and upcoming major tax law changes

Global tax accounting services newsletter

SubscriptionPrintHome

14

Other important tax law changes

Click each circle to review

Recent and upcoming major tax law changes

Global tax accounting services newsletter

SubscriptionPrintHome

15

AustraliaDuring the second quarter of 2014, the Australian government released the 2014/2015 Federal Budget (Budget) containing a number of measures designed to increase tax revenue and reduce the projected Budget deficit. The proposed measures included the following:

• The scope of Australia’s foreign resident capital gains tax (CGT) will be increased by removing the ability to use inter-group transactions that generate non-land assets in determining whether an entity sold is Australian ‘land-rich’ and therefore subject to Australian CGT.

• The Australian corporate tax rate will be reduced from 30% to 28.5% effective for tax years beginning on or after 1 July 2015. However, any expected benefits from the rate cut will be largely offset for companies with taxable income in excess of AUD 5 million by the imposition of a levy on such companies to pay for a proposed Paid Parental Leave scheme.

• Certain changes to the tax consolidation regime announced by the previous government in the 2013/2014 Budget will be implemented.

• The start date for the new Management Investment Trust (MIT) regime will be deferred to 1 July 2015.

• In conjunction with the cut in the company tax rate, the relative value of the Research and Development (R&D) tax incentive will be preserved by reducing the rates of the refundable and non-refundable R&D offsets by 1.5%, effective 1 July 2014.

Following the Budget release, the Australian Treasury released exposure draft legislation to reform Australia’s thin capitalisation and dividend exemption rules. The proposed measures include:

• The proposed thin capitalisation amendments would tighten the deductible debt limits from a debt-to-equity ratio of 3:1 to 1.5:1, increase the de minimis threshold exemption from AUD 250,000 to AUD 2,000,000, and make the worldwide leverage ratio test available to Australian inbound and outbound groups. The new thin capitalisation rules are expected to apply for income tax years that begin on or after 1 July 2014 (e.g., for companies with a 31 December year-end the rules would apply from 1 January 2015).

• The proposed dividend exemption amendments would reform the exemption for non-Australian, non-portfolio dividends received by an Australian company. They are designed to address perceived integrity issues by excluding the exemption for shares that are debt interests for Australian tax purposes and allowing the exemption to apply when distributions flow through trusts and partnerships. The Treasury also proposes to eliminate the taxpayers’ ability to pool portfolio dividends in a foreign company to qualify for the non-portfolio dividend exemption.

During the second quarter of 2014, the Australian Taxation Office also released final Tax Determination TD 2014/14 outlining its views on whether certain payments described in the determination as capital support payments made by an Australian parent company to its subsidiary are deductible.

BrazilDuring the second quarter of 2014, application of tax on financial operations (IOF in Portuguese) to foreign loans was modified to narrow the definition of a short-term regular loan from a loan with a term of 360 days or less to a loan with a term of 180 days or less. The 6% IOF rate now applies only to foreign loans and bonds with terms of 180 days or

Recent and upcoming major tax law changes

Map view

Global tax accounting services newsletter

SubscriptionPrintHome

16

less. The 0% IOF rate will apply to foreign loans and bonds with terms of over 180 days. The new rules are intended to encourage Brazilian companies to obtain loans from abroad and to mitigate the effects of foreign exchange swings between the Brazilian real and the US dollar.

During the second quarter of 2014, the Brazilian Federal Revenue Authorities issued Interpretative Declaratory Act No. 5/2014 (ADI 5/2014), which clarifies the tax treatment of payments made by Brazilian entities for technical assistance and services (with or without transfer of technology) to a company located in a country with which Brazil has a signed double-tax treaty. In accordance with ADI 5/2014, such service fees may be characterised as royalties, independent personal services, business profits, or other income.

ColombiaDuring the second quarter of 2014, the Colombian tax authorities issued Tax Ruling No 607 specifying that payments made to individuals or companies based, incorporated, or carrying out activities in countries qualified as tax havens cannot be deductible for income tax purposes unless specific conditions are satisfied.

Czech RepublicDuring the second quarter of 2014, a proposal was introduced in the Czech Republic with respect to the taxation of investment funds. Under the proposal, funds are divided into ‘basic’ and ‘other’. Basic investment funds would be taxed at a reduced corporate income tax rate of 5% and income of the investors would be subject to withholding tax of 15%. Other investment funds would be taxed at the standard corporate income tax rate of 19% and income of the investors would be tax exempt.

FinlandDuring the second quarter of 2014, a proposal was introduced in Finland to re-establish from 1 January 2015 a deduction for 50% of entertainment expenses. Such a deduction was available in prior years but was disallowed in the 2014 income year.

FranceDuring the second quarter of 2014, the French tax authorities released draft guidelines regarding the legislation enacted on 30 December 2013, targeting hybrid mismatch arrangements. Under that legislation, interest deductions are allowed only if the French borrower demonstrates that the lender is, for the current tax year, subject to a corporate tax

rate on the interest income that equals 25% or more of the corporate tax that would be due under French tax rules.

A proposal was also issued in France to extend the temporary 10.7% exceptional surcharge on corporate income tax (leading to a maximum corporate income tax rate of 38%) until 30 December 2016. This would mean that December year-end companies will be subject to the increased surtax until 31 December 2015.

GermanyThe following measures that were substantively enacted for IFRS purposes in the fourth quarter of 2013 (see the Q4 2013 newsletter) were enacted during the second quarter of 2014 in Germany:

• Losses from the transfer of certain accruals subject to special tax valuation rules (e.g., pensions, early retirement, contingent liabilities) are deductible by the seller over a period of 15 years.

• The buyer has to adjust the fair value of the transferred accruals and consider the special tax valuation rules. Any arising profit can be spread over 15 years.

Recent and upcoming major tax law changes

Map view

Global tax accounting services newsletter

SubscriptionPrintHome

17

During the second quarter of 2014, the German Ministry of Finance also issued a revised draft decree dealing with corporate loss forfeiture rules. These rules limit the availability of losses when there is a material direct or indirect change in ownership of a German company. The new draft decree, issued on 15 April 2014, also includes the tax authorities’ view on the interpretation of exceptions to the rules that have been implemented since the previous decree’s release. Even though a Ministry of Finance decree does not have the force of statutory law, the decree is binding on the tax authorities applying the rules.

GreeceThe following measures were enacted during the second quarter of 2014 in Greece:

• Fees paid for the provision of certain services (e.g., to freelancers, contractors) not exceeding 300 euros are exempt from withholding tax, provided the recipient of the fee is a Greek tax resident.

• No withholding tax is imposed on royalties received by individuals or legal entities that are residents in Greece or have a permanent establishment in Greece.

• It is clarified that fees to contractors are subject to a withholding tax of 3% regardless of whether the recipient of the fee is an individual or legal entity.

• No withholding tax is imposed on the interest income arising from Greek State bonds and Treasury bills for legal entities that are not tax residents of Greece and do not have a permanent establishment in the Greek Territory. In addition, no tax is imposed on the goodwill arising from the transfer of Greek State bonds and Treasury bills acquired from the above legal entities.

• It is clarified that the exemption from withholding tax on intercompany dividends received by legal entities that are tax residents in Greece (or permanent establishments in Greece of EU tax resident entities) is provided only for dividends distributed by subsidiaries that are tax residents in an EU member state or in the European Economic Area (EEA).

During the second quarter of 2014, the Greek Ministry of Finance issued Circular (POL.1120/2014) specifying categories of income that are subject to withholding tax (e.g., technical management, advisory, and other similar services).

ItalyThe following measures were enacted during the second quarter of 2014 in Italy:

• The asset step-up substitution tax is payable in three instalments during the 2014 income year.

• Starting 1 July 2014, withholding tax payable on interest and other financial payments from Italian resident entities to Italian and non-Italian resident investors is increased from 20% to 26%. The increase does not apply to governmental bonds.

LuxemburgThe following measures were enacted during the second quarter of 2014 in Luxemburg:

• Taxpayers migrating their statutory seat and place of central administration from Luxemburg to another European Economic Area (EEA) member state now have an option to defer the exit tax arising on the migration without incurring interest on the outstanding tax liability.

Recent and upcoming major tax law changes

Map view

Global tax accounting services newsletter

SubscriptionPrintHome

18

• A ‘roll over’ is now available for capital gains realised on the disposal of certain qualifying assets (e.g., immovable property) if the sale proceeds are reinvested in an asset allocated to a permanent establishment of the company in any other EEA member state and certain other conditions are satisfied.

During the second quarter of 2014, the Luxemburg tax authorities released Circular L.G.-A no60 formalising the use of a functional currency other than euros for tax purposes. Prior to this guidance, Luxemburg taxpayers were required to file their tax returns in euros, regardless of whether they opted to use other functional currency to draw up their financial statements.

MacedoniaDuring the second quarter of 2014 the following measures were proposed in Macedonia:

• Current-year profit determined in accordance with the applicable accounting standards and adjusted by the value of prescribed taxable expenses would be taxed. Currently (since 2009), profit is subject to tax only upon its distribution.

• Tax exemption would be introduced for the previous-year profit reinvested in tangible and intangible assets.

• Losses could be carried forward for the maximum period of three years from the year in which they were realised.

MexicoDuring the second quarter of 2014, the Mexican tax authorities issued a resolution that exempts gains derived by foreign investors from the sale of American Depositary Receipts (ADRs) of Mexican listed securities. The exemption is available only if the seller is resident in a country with which Mexico has an active double-tax treaty.

NetherlandsDuring the second quarter of 2014, the European Court of Justice found that the Dutch fiscal unity rules breach EU law. This is because they do not allow a fiscal unity between a Dutch parent company and a Dutch subsidiary held through an EU/EEA intermediate subsidiary or a fiscal unity between two Dutch ‘sister’ companies held through a joint EU/EEA parent company. For more information see PwC’s news alert.

PeruDuring the second quarter of 2014, the Peruvian government issued long-awaited guidance (Resolution No. 169-2014) on the requirement to

report the direct or indirect transfer, and issuance or cancellation of shares and participations in Peruvian entities.

The resolution took effect 5 June 2014 and imposed a retroactive reporting requirement for transactions that took place between 6 February 2011 and 31 May 2014. The deadline for reporting these transactions is 30 June 2014 or 31 July 2014, depending on when the transaction took place.

Transactions that take place after 31 May 2014 must be reported in the month following the transaction. Failure to do so could result in penalties equal to 30% of a Peruvian ‘UIT’ (tax unit) or approximately USD 500.

Transactions involving Peruvian American Depository Receipts (ADRs) are not subject to the new reporting requirements.

SpainDuring the second quarter of 2014, the Spanish Basque region (the territories of Bizkaia, Alava, and Gipuzkoa) enacted changes to the special tax regime for holding companies that will apply to tax years starting on or after 1 January 2014. In particular:

Recent and upcoming major tax law changes

Map view

Global tax accounting services newsletter

SubscriptionPrintHome

19

Recent and upcoming major tax law changes

Map view

• The special tax regime for holding companies (the ETVE regime) is replaced by a new tax regime (the ETDV regime). The ETDV regime retains the benefits of the ETVE regime, but also includes a special 0.5% minimum tax on the book value of non-Spanish subsidiaries.

• There is a five-year transition period (until 2019) for companies under the ETVE regime.

During the second quarter of 2014, the Spanish government also proposed that, as part of the general tax reform in Spain, the corporate income tax rate is reduced from 30% to 25% progressively over 2015 and 2016 (except for financial institutions), and losses arising as a result of certain intra-group transactions are limited.

Global tax accounting services newsletter

SubscriptionPrintHome

20

In this section we will step away from our usual refresher on technical tax accounting matters and focus on tax technology that has become increasingly important to the effectiveness of multinational companies’ tax function.

Importance of technology for tax function effectivenessIssueTax departments around the world are facing growing demands to do more with fewer resources. The constant demand to increase productivity, escalating regulatory burdens, unprecedented demands for information from tax authorities, and high pressure to consistently produce timely and accurate tax compliance and financial accounting reports – all are factors contributing to a difficult operating environment for tax departments around the world.

In addition to the above hurdles, tax departments often face internal barriers. Access to quality data, heavy reliance on complex spreadsheets, inefficient data collection processes, and sometimes less than ideal collaboration with other parts of the business all contribute to today’s challenging landscape for tax executives.

While other portions of the business are continually enhancing access to real-time, high-quality information through the use of technology and knowledge management systems, tax departments are often technologically overlooked, which could lead to inefficiency, and, at times, costly errors

and missed opportunities. This ‘technological deficiency’ may become an even bigger issue for tax departments due to the additional reporting requirements arising as a result of the OECD’s proposed CBCR template (see above) and other similar reporting frameworks, e.g., EU Capital Requirements Directive IV (CRD IV).

The inability to meet today’s challenges can result in internal control deficiencies, financial restatements, and, in some extreme instances, a general loss of confidence in the tax function and the company itself. Plus, to the extent that resources are stretched to deal with compliance and other mandatory risk management activities, it limits efforts to focus on more discretionary activities, such as planning and advocacy, resulting in the loss of potential upside benefits. In spite of this, over recent years many tax executives have experienced mounting pressure to rationalise headcount and operating budgets.

Technological solutionsThe search for solutions has led many tax professionals to realise that technology can significantly aid in the effort to maintain or improve their effectiveness.

Tax accounting refresher

Global tax accounting services newsletter

SubscriptionPrintHome

21

However, as mentioned above, the use of technology, especially in the compliance and financial accounting areas, is less prevalent than might be anticipated. Tax executives globally have encountered significant resistance when seeking budgets for tax technology investments sufficient to make a meaningful impact on tax function effectiveness.

One approach to leveraging technology is to more effectively use the infrastructure already embedded in the broader finance organisation. Automating tax operations by integrating well-established tax tools, such as compliance and tax accounting systems, with financial reporting source systems can substantially reduce the effort to collect, manipulate, and validate data. However, due to often disjointed systems and solutions, it can be difficult to obtain information necessary for the tax function.

The above results in an email- and spreadsheet-based environment, with mission-critical, complex spreadsheets typically dependent on a single user and lacking an audit trail, as well as quality and version control.

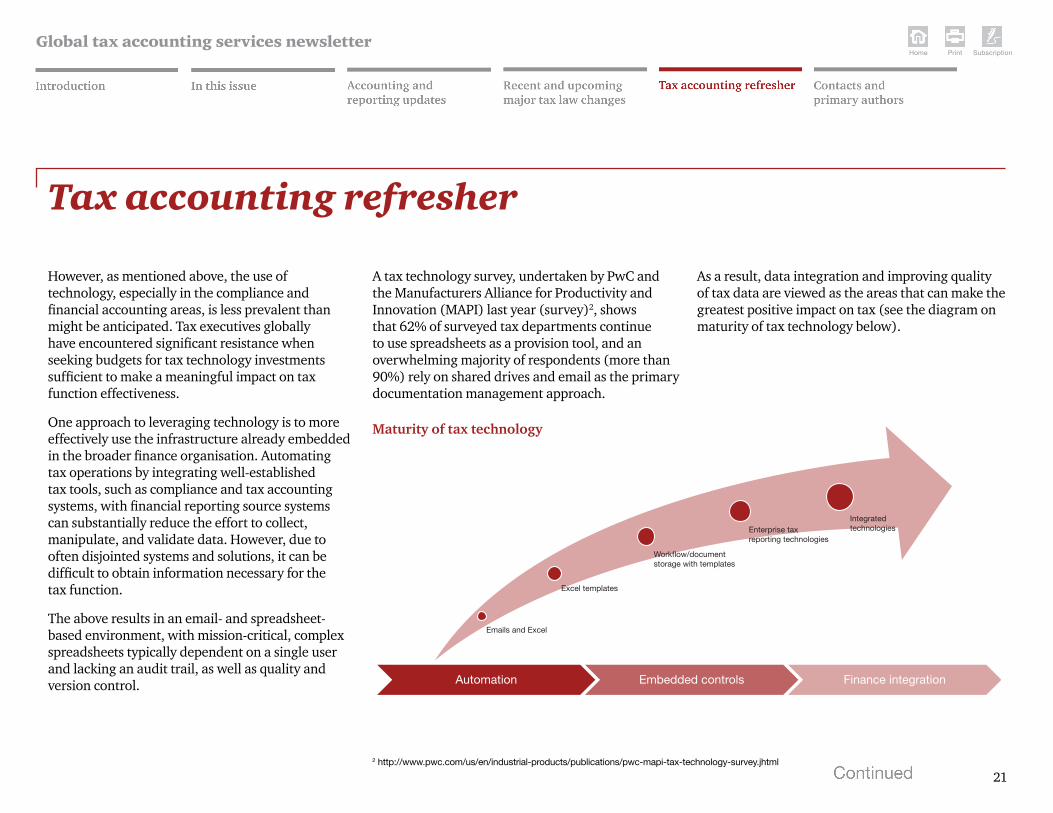

A tax technology survey, undertaken by PwC and the Manufacturers Alliance for Productivity and Innovation (MAPI) last year (survey)2, shows that 62% of surveyed tax departments continue to use spreadsheets as a provision tool, and an overwhelming majority of respondents (more than 90%) rely on shared drives and email as the primary documentation management approach.

As a result, data integration and improving quality of tax data are viewed as the areas that can make the greatest positive impact on tax (see the diagram on maturity of tax technology below).

Tax accounting refresher

2 http://www.pwc.com/us/en/industrial-products/publications/pwc-mapi-tax-technology-survey.jhtml

Maturity of tax technology

Emails and Excel

Excel templates

Workflow/document storage with templates

Enterprise tax reporting technologies

Integratedtechnologies

Automation Embedded controls Finance integration

Global tax accounting services newsletter

SubscriptionPrintHome

22

Tax accounting refresher

When looking for existing technology assets within the broader organisation, a good place to begin is within the company’s enterprise resource planning (ERP) system and related modules. Most finance departments have invested heavily in their ERP systems but with little input from the tax side. The difficulty is that existing ERP or related modules often are not configured to automate extraction of information needed for tax reporting and planning. While 85% of survey respondents said they use an ERP solution, those solutions frequently are not leveraged to the fullest extent for tax.

In addition to data integration, integrated workflow and document management solutions can provide even more efficiencies, connecting standardised processes with a common access point for the tax work papers and documentation needed to perform each task.

While more than 25% of the survey respondents said they have workflow tools, only 9% use them. As a result, substantial opportunity exists for tax departments to improve their process and workflow management and potentially shorten process execution time.

Similarly, opportunities exist to shift from data gathering to data analysis, using reporting and

forecasting tools in a common, integrated tax data environment. In migrating to tax-specific data warehouse solutions, companies can integrate data required by tax in a standard platform which can be accessed via a common centralised portal or reporting environment.

Efficiencies that could be brought by tax technologyThe above technological solutions could bring the following efficiencies to the tax function.

Freed-up staffEfficiency gains via technology can reduce the hours required to complete tasks by 10% to 20%. Most tax functions redeploy that newly created capacity to high-value tasks such as risk management, planning, financial reporting, and controls. This can also contribute to staff satisfaction and retention.

Improved quality of informationUsing technology enables a higher level of accuracy and faster access to book data directly from source systems worldwide.

Increased analyticsHaving more time available to perform analytics rather than data collection provides significant value to the business.

Connected tax personnel globallyMany material weaknesses attributed to the tax function relate to matters originating from outside the home country. Technology is becoming increasingly important to close this gap.

Strengthened internal controlsWhen done correctly, implementation of new technology includes the design and introduction of new processes. The result can be a much improved control environment evidenced by new processes and supported by enabling technology.

Improved forecasting capabilityAccurate forecasts of the effective tax rate and cash taxes are critical to the effective management of tax. The emergence of more advanced tax accounting software, as well as sophisticated modelling and analytic software, now makes it much easier to report, model, and forecast the effective tax rate. In addition, closing the gap between the tax accounting system and the ERP system in an effort to collect the most current data is another critical technology element enabling better tax forecasting.

Global tax accounting services newsletter

SubscriptionPrintHome

23

Tax accounting refresher

The way forwardInvestment in tax technology will allow companies to be better prepared to deal with tax reporting and tax risk management going forward. Additional reporting requirements imposed by CBCR and other reporting frameworks may help tax departments shape their case for further investment in system changes to be better positioned to cope with the increased compliance burden, reconcile the group reporting numbers and gain confidence in the reported data.

The technology challenge represents an opportunity for tax functions to reduce time spent on data collection and manipulation, as well as achieve technology and process improvements, including leveraging existing investments in enterprise systems.

Further, there can be no doubt that most tax departments can gain significant financial benefit by embarking on a well thought-out tax data management plan and create value by realising the above efficiencies.

Global tax accounting services newsletter

SubscriptionPrintHome

24

For more information on the topics discussed in this newsletter or for other tax accounting questions, including how to obtain copies of the PwC publications referenced, contact your local PwC engagement team or your Tax Accounting Services network member listed here.

Global and regional tax accounting leaders

Global and United KingdomAndrew Wiggins Global and UK Tax Accounting Services Leader +44 (0) 121 232 2065 [email protected]

EMEAKenneth Shives EMEA Tax Accounting Services Leader +32 (2) 710 4812 [email protected]

Contacts

Asia PacificTerry SY Tam Asia Pacific Tax Accounting Services Leader +86 (21) 2323 1555 [email protected]

Latin AmericaMarjorie Dhunjishah Latin America Tax Accounting Services Leader +1 (703) 918 3608 [email protected]

Global tax accounting services newsletter

SubscriptionPrintHome

25

Contacts

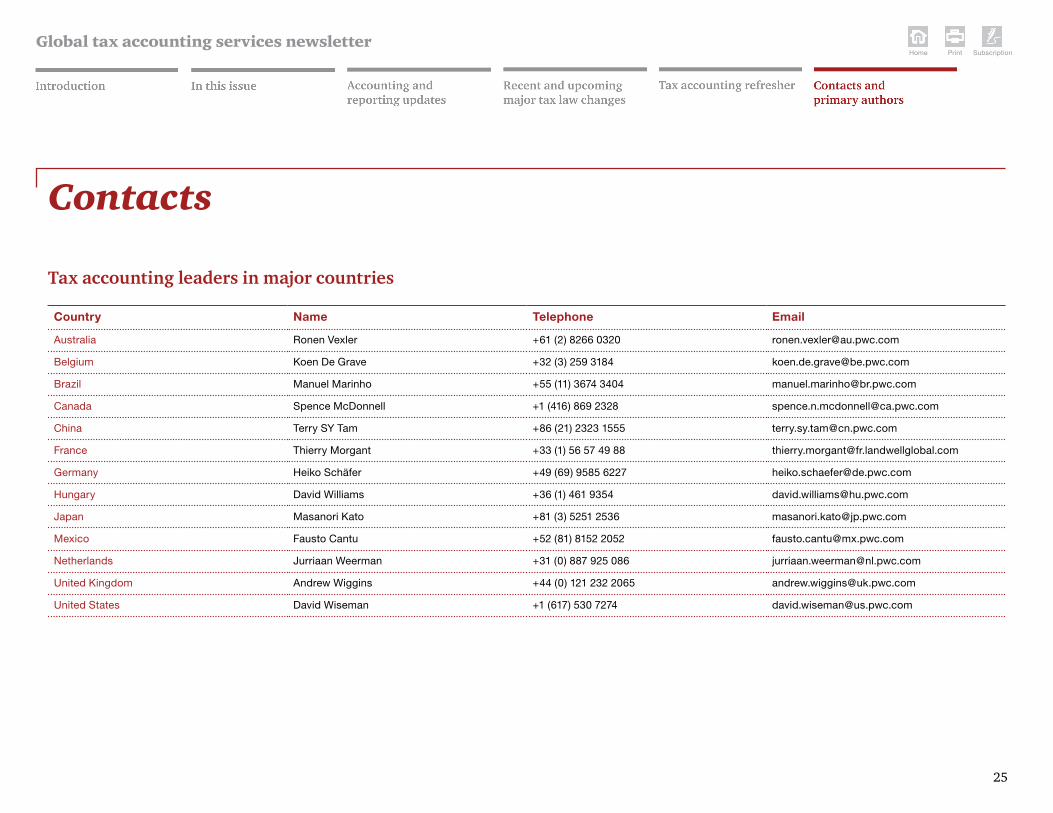

Country Name Telephone Email

Australia Ronen Vexler +61 (2) 8266 0320 [email protected]

Belgium Koen De Grave +32 (3) 259 3184 [email protected]

Brazil Manuel Marinho +55 (11) 3674 3404 [email protected]

Canada Spence McDonnell +1 (416) 869 2328 [email protected]

China Terry SY Tam +86 (21) 2323 1555 [email protected]

France Thierry Morgant +33 (1) 56 57 49 88 [email protected]

Germany Heiko Schäfer +49 (69) 9585 6227 [email protected]

Hungary David Williams +36 (1) 461 9354 [email protected]

Japan Masanori Kato +81 (3) 5251 2536 [email protected]

Mexico Fausto Cantu +52 (81) 8152 2052 [email protected]

Netherlands Jurriaan Weerman +31 (0) 887 925 086 [email protected]

United Kingdom Andrew Wiggins +44 (0) 121 232 2065 [email protected]

United States David Wiseman +1 (617) 530 7274 [email protected]

Tax accounting leaders in major countries

Global tax accounting services newsletter

SubscriptionPrintHome

26

Andrew WigginsGlobal and UK Tax Accounting Services Leader +44 (0) 121 232 2065 [email protected]

Katya UmanskayaGlobal and US Tax Accounting Services Director +1 (312) 298 3013 [email protected]

Steven SchaeferNational Professional Services Group Partner +1 (973) 236 7064 [email protected]

Primary authors

Global tax accounting services newsletter

www.pwc.com

SOlICITATIONThis document is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. This document was not intended or written to be used, and it cannot be used, for the purpose of avoiding US, federal, state or local tax penalties.

© 2014 PricewaterhouseCoopers llP. All rights reserved. PwC refers to the United States member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.