globalization in historical perspective · this pdf is a selection from a published volume from the...

TRANSCRIPT

This PDF is a selection from a published volume from theNational Bureau of Economic Research

Volume Title: Globalization in Historical Perspective

Volume Author/Editor: Michael D. Bordo, Alan M. Taylorand Jeffrey G. Williamson, editors

Volume Publisher: University of Chicago Press

Volume ISBN: 0-226-06598-7

Volume URL: http://www.nber.org/books/bord03-1

Conference Date: May 3-6, 2001

Publication Date: January 2003

Title: Core, Periphery, Exchange Rate Regimes, and Globalization

Author: Michael D. Bordo, Marc Flandreau

URL: http://www.nber.org/chapters/c9595

9.1 Introduction

Historians know the crucial importance played by the boundary that sep-arated the core of the Roman Empire from its periphery—a boundaryknown as the Limes. In addition to being a line of military defense, it was alocus of cross-influences. While the core contributed to shaping the “bar-barous” lands located beyond its walls, the periphery shaped the inner ar-eas, since protection from the dangers of military conflict involved provid-ing for such outcomes. And for reasons that are hard to understand, thelong survival of this frontier extended long after the fall of the Roman Em-pire: More than ten centuries after its collapse, the former Limes surpris-ingly coincided with the line that separated Christians during the religiouswars, into Protestants and Roman Catholics.

In comparison with this very long-run phenomenon, the experience ofthe international monetary system is that of a toddler. And yet the recentturmoil in international financial markets has forced economists and poli-cymakers to come to grips with something similar. The recent discussionson the exchange rate regimes that are advisable in order to cope with finan-

417

Michael D. Bordo is professor of economics at Rutgers University and a research associateof the National Bureau of Economic Research. Marc Flandreau is professor of economics atthe Institut d’Etudes Politiques de Paris.

We are grateful to Ignacio Briones, Dhiman Das, Sonal Dhingra, Juan Flores, and DavidKhoudour-Casteras for excellent research assistance. They thank Larry Neal, Marc Weiden-meir, Antu Murshid, Ugo Pannizza, and Anne Jansen for providing data. Comments from ourdiscussants Anna Schwartz, Charlie Calomiris, Angela Redish, Chris Meissner, and especiallyAlan Taylor, and conference participants are gratefully acknowledged. Discussions withFrédéric Zumer proved very useful to foster thinking on the Feldstein-Horioka regressions.Bordo gratefully acknowledges the financial support of the NBER and the National ScienceFoundation.

9Core, Periphery, Exchange RateRegimes, and Globalization

Michael D. Bordo and Marc Flandreau

cial instability rest on the observation that the challenges of globalizationare not quite the same depending on whether we focus on developing coun-tries and emerging markets or developed ones. Whereas the latter are freeto go their exchange rate way, the former are said to face the dilemma of ei-ther anchoring themselves to core countries with extra strong glue, or re-maining out of the Limes of modern integration with a volatile exchangerate.

As a recent literature has argued, there is a certain “fear of floating”among modern developing countries. But this is obviously nihil novi sub solefor economic historians familiar with that other major experience of glob-alization, namely that of the late nineteenth century. For then, already, therewas a core that followed the high road of more or less complete gold con-vertibility, and an infamous periphery that had trouble pegging but re-sented floating. And it is striking that the list of “peripheral” nations hasnot changed that much over the course of the century: Today, like yesterday,it includes Latin American countries, Central Europe, Russia, and to someextent Asia—among the latter, Japan was already standing out as an ex-ception.1

This persistence nonetheless conceals a profound transformation of theinternational monetary system—a transformation that has occurred at thecore of the global exchange rate system. Today, flexible exchange rates havesuperseded, in advanced countries (with the notable exception of Europe)the nineteenth-century system of fixed exchange rates known as the goldstandard. In other words, “globalization” appears to mean surprisinglyconsistent things in the periphery, but radically opposite things in the core.This may in fact sound somewhat paradoxical: In the late nineteenth cen-tury globalization was in the popular mind associated with the gold stan-dard, and most academics concurred (Kemmerer 1916). Yet after the col-lapse of the Bretton Woods system in the early 1970s the heart of the globalmonetary system is based on floating exchange rates. How do we interpretthis? On the surface, this would seem to suggest that the exchange rate sys-tem is quite irrelevant to the process of globalization: Nature finds its ways.At the same time, how do we make sense of the serious concerns that aca-demics and policymakers have over the problem of the appropriate ex-change rate system for the emerging countries? Why should there be differ-ent recipes for the advanced and the emergers?

The theoretical literature pertaining to the links between integration and

418 Michael D. Bordo and Marc Flandreau

1. We use the distinction core versus periphery for the pre-1914 period following a well-established tradition in economic history. For the recent period we use the terminology ad-vanced versus emerging countries. The difference between the two demarcations is largely geo-graphical (the core before 1914 meant Western Europe and after 1900 the United States,whereas the periphery was everyone else). Today advanced countries are in every region. Thekey unifying theme for both demarcations, as pointed out by our discussant Anna Schwartz,is that (core) advanced countries are generally capital rich and the (periphery) emerging coun-tries are generally capital poor.

exchange rate regimes generally overlooks this problem. Two oppositeviews may be identified. Both assume some kind of market imperfection,because in a perfectly rational and frictionless world, fixed and flexible sys-tems should deliver identical outcomes and the question of the links be-tween exchange rate regimes and integration would be irrelevant (Helpman1981).

The “transaction costs” view on the one hand assumes that floating ex-change rates are a risk that cannot be diversified away and thus tantamountto a distortion preventing full specialization. From this perspective a fixedexchange rate may deliver both a higher level of integration and superioreconomic performance. This view is very old and originates in nineteenth-century classical economics.

On the other hand, the “policy view” rests on the notion that, due to theexistence of nominal rigidities and factor immobility, flexible exchangerates might be advisable to smooth out the international adjustment pro-cess: Exchange rate flexibility, from this perspective, is not an enemy to in-ternational integration. This view is traditionally associated with RobertMundell, and Padoa-Schioppa’s trilemma. It has been put to work by BarryEichengreen to explain the (according to the recent literature, partial) trendtoward fluctuating exchange rates. The expansion of democracy, by callingfor an increase in income smoothing, has led more and more countries tofloat their way into globalization—again with the notable exception of Eu-rope.

None of these views, however, takes seriously into account the dichotomybetween core and peripheral countries. And yet the quite distinct dynamicsof exchange rate regimes depending on whether we focus on the center oron the periphery suggests that different stories may have to be told for each.At the same time, as the comparison with the Roman Empire suggests, therecord of the center cannot be understood without reference to the periph-ery, and vice versa. Systems are tested on their margins.

In this paper we seek to provide an interpretation of both the presence of“fear of floating” in the periphery and the transition to flexible exchangerates in the center. Our argument rests on the role of technological progressin money and finance. In the nineteenth century, adherence to gold pro-vided a stable environment that contributed to the development of deep andliquid money markets. At the same time, gold convertibility was a con-straint on monetary policies because it implied currency bands withinwhich core nations sought to obtain as much room to maneuver as theycould. By the 1970s, financial maturity allowed the core countries to float.In a sense in the current floating regime countries, by learning to follow adomestic nominal anchor, have been able to eliminate the credibility bandsof the classical gold standard, which in its time granted the core countriesonly a modicum of the policy independence they have today.

By contrast to the core, many peripheral countries in the pre-1914 period

Core, Periphery, Exchange Rate Regimes, and Globalization 419

lacked what we suggest calling the “financial maturity” to successfully ad-here to gold. The alternative of floating was fraught with danger becausethey were forced to obtain the foreign capital crucial to their developmentby borrowing in terms of sterling (or other core-country currencies) or elsehaving gold clauses.

In times of financial crises, then as now, devaluations led to debt crises.Thus, we argue that peripheral countries then, as now, were forced to adoptsuper-hard fixed exchange rates (currency boards or close to 100 percentgold reserves then, currency boards or dollarization now) because they hadnot developed the financial maturity to float, or else they had to restrict for-eign borrowing. Thus, the link between globalization and the exchange rateregime turns out to depend on financial maturity:2 That is, “Tell us how fi-nancially mature you are, and we will tell you what exchange rate regimeyou’ll end up with through globalization!”

The remainder of the paper is organized as follows. In section 9.2, we setthe stage by considering the evidence on global financial integration from1880 to 1997, using the well-known Feldstein-Horioka approach. The con-tribution of our work is that it combines both cross-section and time seriesdimensions with an extended sample of emerging countries to show a num-ber of disturbing facts that suggest that financial globalization varies a lotdepending on the type of country—core (advanced) or periphery (emerg-ing)—and the type of regime (floating, fixed) we consider. This leads to theconclusion that financial integration today is primarily an advanced countryphenomenon, while the link with the exchange rate regime is a complex one.

Section 9.3 lays out the financial maturity hypothesis and presents nar-rative evidence for the pre-1914 period of the different experiences of thecore and peripheral countries in adhering to the gold standard.

Section 9.4 presents some empirical evidence on the link between finan-cial depth and the exchange rate regime for core (advanced) and peripheral(emerging) countries 1880–1913 and today.

Section 9.5 summarizes our findings and suggests some lessons from his-tory.

9.2 Financial Integration, Exchange Rate Regimes, and Hollowing Out

In this section, we use saving-investment correlation tests (Feldstein andHorioka 1980). Saving-investment (S-I) tests seek to measure the degree of

420 Michael D. Bordo and Marc Flandreau

2. The main focus of our study is the exchange rate arrangements of the two periods of glob-alization (i.e., of open capital markets and relatively open trade). We do not take a stand onwhy the global system collapsed after 1918 (or, more correctly, after 1931) and was not reat-tained until the 1980s. We are sympathetic to the view that the deglobalization of the middletwo quarters of the twentieth century had a lot to do with the disruptive “second thirty years’war” that began in 1914 and only really ended with the end of the cold war. We are agnostic onthe views of those who see the breakdown of the global system as related to flaws of the goldstandard and to those who see it as a backlash to the excesses of the earlier age of globalization.

financial integration by examining the relationship between saving and in-vestment. Integration is high if the correlation of a regression of investmenton saving is low and vice versa: In the latter case investment is constrainedby domestic savings, whereas it is not in the former case. Feldstein-Horioka’s analysis sparked a considerable research effort. One importantarea of research was the analysis of the historical behavior of correlationcoefficients in order to document the historical progress of international fi-nancial integration. Standard references in this field are Bayoumi (1990),Tesar (1991), Zevin (1992), Eichengreen (1992), Obstfeld (1995), Jones andObstfeld (1997), Bayoumi (1997), and Obstfeld and Taylor (1998).3 Theseworks outline the now famous inverted U-shaped pattern of financial inte-gration, which is obtained when one plots the results from a series of annualcross-section regressions for the period 1880–1995 (fig. 9.1).4 The message

Core, Periphery, Exchange Rate Regimes, and Globalization 421

3. See Flandreau and Rivière (1999) for a survey.4. The countries were Argentina, Australia, Austria, Belgium, Canada, Denmark, Finland,

France, Germany, Greece, Ireland, Iceland, Italy, Japan, Luxembourg, Norway, New Zealand,the Netherlands, Portugal, Russia, Spain, Sweden, Switzerland, the United Kingdom, and theUnited States. For data sources see appendix to Flandreau and Rivière (1999), available on re-quest.

Fig. 9.1 The inverted U-shaped pattern of financial integrationSource: Flandreau and Rivière (1999).

seems to be that, after the interruption of the interwar years, the world isheading toward reglobalization that recalls nineteenth-century patterns.We refer to this as the “folk view.”

9.2.1 Taking Panel Econometrics Seriously

We seek to show that this wisdom is too simple and conceals a number offiner phenomena. This is done by extending existing analyses in two criticaldirections. First, we supplement the traditional cross-section regressions bypanel estimates. Second, when this can be done (i.e., for the post-1973 period)we supplement the traditional group, of primarily advanced countries thatresearchers have been looking at, with a large sample of emerging countries.

The importance of panel econometrics for analyzing S-I correlation wasemphasized by Krol (1996), Coiteux and Simon (2000), and Flandreau andRivière (1999). Panel data such as those used in Feldstein-Horioka (FH) re-gressions have two dimensions. Research on the long-run behavior of S-Iregressions has focused on the interindividual dimension, computing cross-section regressions either on annual data on or individual averages for givenperiods. These latter estimates are known as between-estimates. They maybe thought of as generalizations of pointwise cross-section regressions.

One problem with between-estimates, though, is that they introduce anumber of biases in the estimation technique. For instance, they tend tooverestimate “true” disintegration when current accounts experience fre-quent reversals, because averaging wipes out those reversals. This is why“within”-estimates are in our view a much sounder measure, because theyhighlight an essential dynamic dimension of financial integration by focus-ing on the ability of countries to finance changes in their current account po-sition. Indeed, within estimates measure whether increases in investmentabove average can occur without running into an investment constraint. Athird possible estimate, known as “pooling,” gives equal weight to the timeand individual dimensions.

Figure 9.2 shows the results of computing triplets of estimates (pooling,within, between) for the standard subperiods people have focused on andfor the typical group of countries for which such estimates have been com-puted before. As can be seen, while the popular inverted U-shaped patternis discernible, the precise picture depends on the estimator used.

Although the three estimates give a similar picture for the pre-1914 pe-riod, within-estimates suggest that the interwar was less closed than hasbeen assumed, probably because the frequency of current account reversalsduring those years tends to average out the countries’ short-term ability touse foreign capital. Moreover, we observe huge discrepancies among thevarious estimates for the period after 1973. This suggests that althoughsome countries have dramatically increased their ability to use the foreigncapital market, the sample’s ability at financing current account imbalanceshas increased much less. In what follows we shall accordingly give special

422 Michael D. Bordo and Marc Flandreau

weight to the within-estimates, which might sound as a better measure,5 al-though for the sake of completeness, we will report all three measures.

9.2.2 Regimes of Financial Integration

Having emphasized the importance of panel estimates, our strategy is thefollowing: Using a sample similar to the one previous scholars have workedwith, we replicate benchmark estimates of S-I correlation by subperiodsand compare these with the estimates one obtains for subgroupings that wethink may be relevant, because they were characterized by arrangementsimplying exchange rate stability.6

In this fashion, we identify (a) gold countries before 1914; (b) gold coun-tries, gold bloc members, and sterling area members in the interwar; (c)countries that pegged to the dollar under the fixed Bretton Woods era;7 and(d) members of the European exchange rate mechanism (ERM) after 1979.8

Core, Periphery, Exchange Rate Regimes, and Globalization 423

Fig. 9.2 Integration coefficients: Folk sample

5. As will be seen, the standard errors of between-estimates are always larger than those ofthe two alternative estimators.

6. Our sample only differs from the existing one in that some corrections were made. For in-stance, the sample used by Eichengreen, Taylor, and others has France importing capital be-fore 1914; whereas Lévy-Leboyer shows that it was exporting. See Flandreau and Rivière(1999) for a discussion of alternative samples.

7. We identified the arrangements using data from Bordo and Schwartz (1996), Bordo(1993), and Ghosh et al. (1995).

8. We compute this restriction rather than a restriction to fixed exchange rate regimes be-cause of problems with identifying these regimes to which we return to below.

Our goal is to see whether these groupings succeeded in achieving signifi-cantly higher levels of integration than the sample at large. The intuition isthat, if exchange rate stability is an instrument meant to unlock participat-ing countries’ current account constraints, then we should observe lowerbetas for subgroupings than for the sample at large (see fig. 9.2).

Table 9.1 displays the results.9 They show that for the pre–World War Iperiod, countries that strictly adhered to gold do not seem to have been ableto achieve a significantly greater degree of financial openness than thosewho did not. The estimated beta for both the entire population and the re-stricted sample shows figures that are very close to each other so that it isimpossible to reject the null that they are the same.

The interwar years reveal an interesting pattern: We see that countriesthat adhered to gold, as well as members of the sterling zone, actuallyachieved less integration than the international average reported in table9.3. The straightforward interpretation of this is probably that members ofthe interwar gold standard could only retain membership through capitalcontrols, thus actually achieving less integration than the sample at large. Asimilar result is in fact obtained for the Bretton Woods period, probably forthe very same reason.

Finally, moving to the recent experience, we see that ERM membershipdid succeed in reducing the beta parameters compared to the entiresample.10 At the same time, since we know that the making of the euro wasaccompanied by a companion capital movement liberalization within Eu-ropean countries, it is not clear whether the greater integration is due to ex-change rate stability or to lower controls.

At this stage, one forceful conclusion that emerges is that fixed exchangerate regimes were not in the nineteenth century an instrument for financialintegration. Financial integration has been directly related to the presenceor absence of capital controls, and these controls have been used in periodsof both fixed and flexible exchange rates. The pre-1914 period stands out asone that was exceptionally free from these controls rather than one whoseglobalization was related to exchange rate stability since, as observed, therestriction of the integration coefficient to those countries that did not floatis not higher than the one obtained by the entire sample. In fact, it is quitestriking to see that even with fixed exchange rates, even with no capital con-trols at all, the degree of integration achieved was not perfect. We think thatthese findings are consistent with the notion that globalization in the nine-teenth century caused the adoption of the gold standard, rather than the

424 Michael D. Bordo and Marc Flandreau

9. Similar results can be found in Flandreau and Rivière. The only difference comes fromminor updates in the database.

10. In this part, we use the folk sample. The very low pooling and between-estimates comefrom the inclusion of Luxembourg. Results without Luxembourg are respectively P: 0.700, W:0.521, B: 0.819, and for the restriction to Europe P: 0.551, W: 0.502, B: 0.664. As can be seen,the within-estimates are much more robust than the between and pooling.

Tab

le 9

.1F

inan

cial

Int

egra

tion

: Ben

chm

ark

Est

imat

es a

nd F

ixed

Exc

hang

e R

ates

Res

tric

tion

s (f

olk

sam

ple)

Cla

ssic

al G

old

Bre

tton

Woo

ds 1

:B

rett

on W

oods

2:

Stan

dard

Inte

rwar

Gol

d D

olla

rF

loat

(188

0–19

13)

(191

8–19

39)

(194

5–19

73)

(197

4–19

96)

Ben

chm

ark

esti

mat

esP

: 0.4

60 (0

.030

)P

: 0.7

68 (0

.027

)P

: 0.8

63 (0

.019

)P

: 0.3

39 (0

.026

)W

:0.4

37 (

0.03

0)W

: 0.6

41 (

0.03

0)W

: 0.7

84 (

0.02

2)W

: 0.6

81 (

0.10

6)B

: 0.4

82 (0

.184

)B

: 0.9

71 (0

.082

)B

: 0.9

44 (0

.090

)B

: 0.2

24 (0

.035

)R

estr

icti

on to

gol

d st

anda

rdP

: 0.4

45 (0

.038

)P

: 1.0

15 (0

.066

)W

: 0.4

75 (

0.03

7)W

: 0.8

76 (

0.08

2)B

: 0.4

59 (0

.211

)B

: 1.0

82 (0

.096

)N

= 4

33 (1

5 co

untr

ies)

N=

59

(10

coun

trie

s)R

estr

icti

on to

ste

rlin

g zo

neP

: 0.8

08 (0

.048

)W

:0.8

04 (

0.08

8)B

: 0.8

54 (0

.110

)N

= 6

3 (8

cou

ntri

es)

Res

tric

tion

to g

old

stan

dard

+ g

old

bloc

P: 0

.943

(0.0

49)

W: 0

.864

(0.

056)

B: 1

.002

(0.1

06)

N=

82

(11

coun

trie

s)R

estr

icti

on to

gol

d bl

ocP

: 0.6

93 (0

.055

)W

: 0.6

76 (

0.06

0)B

: 0.6

77 (0

.216

)N

= 1

9 (3

cou

ntri

es)

Res

tric

tion

to d

olla

r st

anda

rd (I

MF

dat

a)P

: 0.9

32 (0

.025

)W

: 0.8

09 (

0.03

0)B

: 1.0

42 (0

.088

)N

= 3

72 (1

7 co

untr

ies)

Res

tric

tion

to e

xcha

nge

rate

mec

hani

smP

: 0.0

89 (0

.028

)W

: 0.3

16 (

0.05

7)B

: 0.0

944

(0.0

99)

N=

196

(13

coun

trie

s)

Sou

rce:

Aut

hors

’ com

puta

tion

s (s

ee te

xt).

other way round, and the remainder of the paper shall seek to develop thisintuition.

9.2.3 Expanding the Horizon: Developedand Emerging Integration since 1973

In order to go beyond these findings, we extend existing analyses in a sec-ond direction. We seek to expand the folk sample used in the literature(essentially, developed countries plus Argentina) to include for the morerecent period a large number of emerging countries in Asia and LatinAmerica. Although data availability limits the number of emerging coun-tries that can be identified during the late nineteenth century (and thus thesignificance of tests conducted on more limited samples), such is not thecase for the more recent period. This enables us to make systematic com-parisons between performances in the core (advanced) and in the periphery(emerging).11 For this purpose we constructed an expanded database com-prising forty-six countries and spanning the period 1973–98. The folk data-base is embedded in this broader set.12 To document the properties of the ex-panded sample, we run cross-section regressions for the period after 1973.As can be seen in figure 9.3, the trend toward greater financial integrationafter 1973 captured by estimates based on the folk sample (the right part ofthe inverted U) mostly reflects the properties of the sample itself. In otherwords, it shows that there was indeed a process of financial integration, butthis process varied a lot along the individual dimension, as illustrated by theincrease in the cross-section correlation for emerging countries in the sec-ond half of the 1980s. Moreover, extracting from the sample countries be-longing to the European Union shows that the trend toward greater inte-gration that many authors have emphasized is truly a story about Europeanintegration. The disproportionate share of European nations in the samplehas led scholars—unknowingly—to eurocentric conclusions.

In line with the previous discussion, however, it is obvious that one can-not restrict one’s attention to these cross-section estimates, as telling as theyare. In a second stage, we thus use our new sample to compute benchmarkestimates and test in a second stage whether restrictions to given exchangerate regimes are associated with higher or lower levels of integration.

The identification of exchange rate regimes is more complex today than itwas one century ago when the choice was between paper and gold. We de-cided to rely on the Masson and Levy-Yeyati and Sturzenegger (LYS) clas-

426 Michael D. Bordo and Marc Flandreau

11. Earlier exercises in Flandreau and Rivière (1999) based on the Folk’s sample plus fiveemergers suggested that the record of peripheral countries might be different from that of de-veloped ones.

12. The additional countries are Brazil, Chile, China, Colombia, Egypt, Hong Kong, Hun-gary, India, Indonesia, Israel, Malaysia, Mexico, Peru, the Philippines, Poland, the Czech Re-public, Russia, Singapore, South Africa, South Korea, Thailand, Turkey, Uruguay, and Vene-zuela. For data sources, see data appendix to Flandreau and Rivière (1999), available onrequest, and the IMF’s International Financial Statistics.

sifications of countries by type of exchange rate regime (Masson 2001; LYS2001). Both provide country classifications that recognize that modern ex-change rate regimes can be of the fixed, floating, or intermediary category.Since one needs to cross the information available in our sample and thatavailable in either the Masson or LYS databases, one is bound to lose somecountries or observations in the process. We end up with two restricted data-bases of forty-two (Masson) or thirty-five (LYS) countries, whose properties,when one considers both samples in their entirety, are almost identical.13

The Masson classification works with the International Monetary Fund(IMF) categories but follows an earlier IMF study by Ghosh et al. (1995)which demarcated the IMF’s twenty-six categories into just three (flexible,intermediate, and floating).14 Masson rearranges the Ghosh categories bydefining flexible as strictly independent floats and fixed as hard pegs (cur-rency boards and announced pegs with no change in parity), with the re-mainder classified as intermediate. As a result Masson has a much smaller

Core, Periphery, Exchange Rate Regimes, and Globalization 427

13. We checked this by running pooling-within-, and between-estimates. Results (availableupon request) are virtually identical, a result of the broad overlap between the two samples.

14. Flexible arrangements included crawling pegs, target zones, managed floats, and inde-pendent floats. Pegged arrangements include single currencies, special drawing rights (SDR)pegs, other official basket pegs, and secret pegs.

Fig. 9.3 Financial integration 1973–97: Difference between advanced and emergingcountries

number of truly fixed or truly flexible regimes, with the bulk of the samplebeing made of intermediate regimes.

The LYS indicators use measures of the volatility of exchange rates andinternational reserves and cluster analysis to classify countries into fourgroups (floating, dirty floating, crawling pegs, and fixed).15 The classifica-tion is based on the theoretical prior that countries that really float shouldhave greater exchange rate volatility and smaller international reservemovements than those that do not. We further classified the LYS classifica-tion into three by combining dirty floats and crawling arrangements into anintermediate category. Thus, our rearrangement of the LYS classificationgives much weight to the tails.

The results we get from these exercises are documented in table 9.2. First,it appears that there are several patterns of financial integration. We find im-portant distinctions among emergers, and also among regimes. In practice,whereas Asian countries are less financially open than the average, LatinAmerican nations are more open for both the Masson and LYS databases.

The effects of alternative exchange rate regimes on financial integrationare also interesting. Developed countries are more integrated when they fix,but to a certain extent also when they float, at least according to LYS. Thisis interesting because floating developed countries are typically made oflarge mature economies with sophisticated financial systems, such as GreatBritain or the United States, whereas fixing developed countries typicallyinclude small open economies such as Austria.

We take these results as illustrating how financially deep economies,while floating, can nonetheless achieve high levels of financial integrationthat can compare with nineteenth-century gold standard records. On theother hand, smaller countries may find themselves opting for a fixed ex-change rate regime because they are very open rather than being open be-cause they have a fixed exchange rate system.

Emerging countries face varied experiences: As can be seen from theMasson database, emerging Latin countries are highly integrated at bothends of the exchange rate regime spectrum, with intermediate regimes be-ing less integrated. Something similar is also perceptible in the LYS data-base, especially if we recall the greater significance we attach to the within-estimates. For Asian countries, by contrast, the opposite is obtained: There,intermediary regimes correspond to comparatively higher, not lower, levelsof integration than extreme floats or fixed regimes. However, even for the in-termediate category the degree of integration achieved is very low.

This certainly gives support to Fischer’s view that developing countries,which are not very exposed to international capital flows, have the oppor-tunity to adopt intermediate exchange rate options (Fischer 2001). To us,

428 Michael D. Bordo and Marc Flandreau

15. They also have another category, called “inconclusive,” which results from the statisticaltechnique employed, and which we omit in our classification scheme.

Tab

le 9

.2T

he W

orld

Acc

ordi

ng to

Mas

son

and

Lev

y-Y

eyat

i and

Stu

rzen

egge

r

Tota

lF

ixed

Inte

rmed

iate

Flo

atin

g

A. M

asso

n (1

973–

97)

Tota

l sam

ple

P: 0

.703

(0.0

18)

P: 0

.441

(0.1

28)

P: 0

.747

(0.0

21)

P: 0

.625

(0.0

34)

W: 0

.527

(0.0

25)

W: –

0.10

2 (0

.220

)W

: 0.5

11 (0

.029

)W

: 0.5

84 (0

.057

)B

: 0.8

12 (0

.053

)B

: 0.6

72 (0

.164

)B

: 0.8

66 (0

.056

)B

: 0.6

54 (0

.117

)N

= 1

017

(42

coun

trie

s)N

= 4

2 (5

cou

ntri

es)

N=

774

(39

coun

trie

s)N

= 1

98 (c

ount

ries

)D

evel

oped

P: 0

.718

(0.0

27)

P: –

0.25

1 (0

.202

)P

: 0.7

36 (0

.038

)P

: 0.6

61 (0

.031

)W

: 0.7

37 (0

.036

)W

: 0.2

95 (0

.228

)W

: 0.6

54 (0

.045

)W

: 0.6

48 (0

.059

)B

: 0.7

04 (0

.101

)B

: n.a

.B

: 0.8

37 (0

.104

)B

: 0.7

11 (0

.110

)N

= 5

50N

= 2

1 (2

cou

ntri

es: 3

et1

3)N

= 3

77 (1

9 co

untr

ies)

N=

150

Tota

l em

ergi

ngP

: 0.7

93 (0

.032

)P

: 0.4

46 (0

.198

)P

: 0.8

38 (0

.031

)P

: 0.2

94 (0

.149

)W

: 0.6

15 (0

.044

)W

: –0.

153

(0.3

44)

W: 0

.615

(0.0

46)

W: 0

.454

(0.1

41)

B: 0

.911

(0.0

95)

B: 0

.676

(0.2

37)

B: 0

.929

(0.0

96)

B: –

0.14

6 (0

.404

)N

= 3

41N

= 1

9 (3

cou

ntri

es: 2

5.36

.46)

N=

278

(16

coun

trie

s)N

= 4

3 (5

cou

ntri

es)

Em

ergi

ng A

sia

P: 0

.833

(0.0

60)

P: 0

.757

(0.0

79)

P: 1

.621

(0.0

37)

W: 0

.850

(0.0

80)

n.a.

W: 0

.826

(0.0

85)

W: 1

.621

(0.3

70)

B: 0

.814

(0.1

46)

B: 0

.610

(0.1

28)

B: i

mpo

ssib

leN

= 1

07N

= 8

7 (5

cou

ntri

es)

N=

18

(1 c

ount

ry)

Em

ergi

ng L

atin

Am

eric

aP

: 0.5

21 (0

.046

)P

: 0.4

55 (0

.209

)P

: 0.5

73 (0

.049

)P

: –0.

277

(0.0

97)

W: 0

.478

(0.0

57)

W: –

0.31

1 (0

.357

)W

: 0.5

16 (0

.052

)W

: –0.

411

(0.1

07)

B: 0

.603

(0.1

59)

B: n

.a.

B: 0

.623

(0.2

10)

B: –

0.06

1 (0

.152

)N

= 1

76N

= 1

5 (2

cou

ntri

es: 2

5, 4

6)N

= 1

50 (8

cou

ntri

es)

N=

10

(3 c

ount

ries

)(c

onti

nued

)

Tab

le 9

.2(c

onti

nued

)

Tota

lF

ixed

Inte

rmed

iate

Flo

atin

g

B. L

evy-

Yey

ati a

nd S

turz

eneg

ger

(197

3–97

)To

tal s

ampl

eP

: 0.7

27 (0

.021

)P

: 0.5

42 (0

.069

)P

: 0.7

66 (0

.037

)P

: 0.6

25 (0

.035

)W

: 0.6

17 (0

.028

)W

: 0.1

96 (0

.091

)W

: 0.4

81 (0

.058

)W

: 0.3

95 (0

.058

)B

: 0.8

08 (0

.071

)B

: 0.7

66 (0

.137

)B

: 0.8

10 (0

.080

)B

: 0.6

52 (0

.091

)N

= 8

48 (3

5 co

untr

ies)

N=

129

(16

coun

trie

s)N

= 3

86 (2

9 co

untr

ies)

N=

393

(31

coun

trie

s)D

evel

oped

P: 0

.685

(0.0

29)

P: 0

.487

(0.1

13)

P: 0

.526

(0.0

57)

P: 0

.636

(0.0

40)

W: 0

.699

(0.0

38)

W: 0

.164

(0.1

19)

W: 0

.615

(0.0

97)

W: 0

.413

(0.0

74)

B: 0

.676

(0.1

19)

B: 0

.743

(0.2

83)

B: 0

.578

(0.0

96)

B: 0

.583

(0.1

19)

N=

467

(18

coun

trie

s)N

= 8

4 (9

cou

ntri

es)

N=

83

(10

coun

trie

s)N

= 2

38 (1

6 co

untr

ies)

Tota

l em

ergi

ngP

: 0.7

56 (0

.031

)P

: 0.4

76 (0

.097

)P

: 0.7

94 (0

.043

)P

: 0.8

01 (0

.055

)W

: 0.5

62 (0

.043

)W

: 0.2

24 (0

.148

)W

: 0.4

63 (0

.071

)W

: 0.5

52 (0

.078

)B

: 0.8

84 (0

.086

)B

: 0.6

58 (0

.128

)B

: 0.8

69 (0

.100

)B

: 0.9

58 (0

.128

)N

= 3

57 (1

6 co

untr

ies)

N=

45

(7 c

ount

ries

)N

= 1

68 (1

6 co

untr

ies)

N=

135

(14

coun

trie

s)E

mer

ging

Asi

aP

: 0.7

23 (0

.065

)P

: 0.7

04 (0

.072

)P

: 0.6

98 (0

.087

)P

: 0.8

56 (0

.192

)W

: 0.8

50 (0

.080

)W

: 0.8

95 (0

.128

)W

: 0.5

07 (0

.123

)W

: 0.9

32 (0

.255

)B

: 0.7

91 (0

.130

)B

: 0.6

30 (0

.099

)B

: 0.8

77 (0

.161

)B

: 0.7

74 (0

.096

)N

= 1

12 (5

cou

ntri

es)

N=

17

(3 c

ount

ries

)N

= 6

9 (5

cou

ntri

es)

N=

23

(3 c

ount

ries

)E

mer

ging

Lat

in A

mer

ica

P: 0

.523

(0.0

46)

P: 0

.440

(0.1

49)

P: 0

.339

(0.0

64)

P: 0

.603

(0.0

79)

W: 0

.480

(0.0

55)

W: 0

.168

(0.2

17)

W: 0

.454

(0.0

81)

W: 0

.406

(0.0

74)

B: 0

.611

(0.1

68)

B: 0

.652

(0.0

49)

B: 0

.376

(0.1

59)

B: 0

.917

(0.2

79)

N=

184

(8 c

ount

ries

)N

= 2

2 (3

cou

ntri

es)

N=

77

(8 c

ount

ries

)N

= 8

2 (8

cou

ntri

es)

Sou

rce:

Aut

hors

’ com

puta

tion

s.N

ote:

n.a.

= n

ot a

vaila

ble.

these results clearly support the notion that more open countries will endup either in a fixed exchange rate system or in a flexible one.

To sum up, we found that a large part of the extensive integration that theadvanced countries have achieved has to do with European integration thathas been able to drive Europe over and beyond what has been achievedelsewhere under both fixed and flexible exchange rates. We think that thisshould be seen as a result of the liberalization of financial services, whichEurope has implemented, rather than as a result of the exchange rate regimeper se. A number of advanced floaters have in effect been quite good at im-plementing financial openness: Although a fixed exchange rate regime inadvanced countries often goes with higher integration, a flexible one mightdo quite well too.

Moreover, our results support the hollowing-out hypothesis for emergingcountries, since they show that the trend toward greater integration has splitLatin America into two groups, where financial integration has in turnforced the adoption of either floating or fixed exchange rate regimes. Bycontrast, Asia has been able to retain intermediate and both fixed and float-ing exchange rate regimes because it has remained on average more finan-cially closed than the rest of the world.

In other words, the exchange rate regime is a product of globalization,and globalization has caused a polarization between floating and fixed ex-change rates—a process known as hollowing out. Only those who havemaintained a degree of financial insulation have been able to postpone thechoice. Again, globalization appears to have been the driving force.

9.3 Brave New World: Is Financial Vulnerability a Discovery of the 1990s?

The previous section has suggested that causality goes from globalizationto the exchange rate regime.16 In this section, we carry on with this line ofanalysis. We survey the recent literature on exchange rate regimes and fi-nancial crises and argue that it has a lot to say about nineteenth-centurymacroeconomic problems.

9.3.1 Exchange Rate Regimes and Financial Crises:The Modern Literature

The experience of both advanced and emerging countries on financialcrises teaches us that pegged exchange rates invariably succumb to specula-tive attacks. From a theoretical point of view, this can be explained as a re-

Core, Periphery, Exchange Rate Regimes, and Globalization 431

16. In a previous draft of this paper we used gravity equations to analyze the relationship be-tween trade integration and the exchange rate regime. Our results for the 1880–1919 periodcomplement those presented above for financial integration and the exchange rate regime. Wefound, among other things, that exchange rate volatility did not significantly hinder bilateraltrade, and although adhering to gold was associated with greater trade, it seems as if this is ex-plained by deeper institutional forces at work.

sult of growing tensions between the peg and domestic economic conditions(Krugman 1979; Obstfeld 1984). The general lesson seems to be that theonly alternatives in the face of mobile capital are floating or a hard fix suchas a currency board, dollarization, or membership in a monetary union.

Thus, the “corner solutions” literature has developed on the notion thatemerging countries (and to a certain extent developed ones as well) mustchoose between fixed and floating regimes, but cannot durably remain inany intermediary system. More fundamentally, the flexible corner has comeunder further attack in the “fear of floating” literature—according to whichseemingly flexible countries do not truly float, because in effect, such a pol-icy is for them both inefficient and dangerous. The argument runs as fol-lows: In principle, a country that experiences a shock can adjust by lower-ing the exchange rate. This is supposed to enable that country to enjoytransitorily lower interest rates so that output may recover. But accordingto Hausmann et al., (1999), this aspirin, although it may have been goodmedicine for European nations in the 1990s, in effect gives headaches toLatin American countries. According to this view, the record for LatinAmerican countries is that letting the exchange rate go forces an increase ininterest rates and causes a major decline of output.

This is because exchange rate depreciation in turn triggers a capital flight,perhaps because that country relies heavily on foreign capital (so that ex-change rate depreciation signals serious problems ahead). Another mecha-nism goes through the share of external debt that is denominated in aforeign currency. Today, only a very limited number of about twenty-fivecountries can issue debt in their own currency. As a result, exchange crisesmay cause a debt crisis. In such a setting, emerging markets would be betteroff pegging, even if rampant “peso” problems imply for them that pegging,whatever the amount of glue they use, does not automatically buy lower in-terest rates. At least, the argument goes, countries doing so would be pro-tected from short-term external disturbances, which they would not have toshore up against.

9.3.2 Credibility, Interest Rates, and Monetary Policy

For students of the gold standard, it is striking how familiar the modernview sounds, if only we look carefully at the record. The European aspirin,on the one hand, closely resembles what a large body of literature has de-scribed as the normal state of affairs for core members of the gold standard.Because exchange depreciation (be it the result of suspended convertibilityor a widening of the gold bands through the well-known “gold devices”)was not expected to last,17 these nations, often also the more developedones, enjoyed a measure of short-term policy flexibility that enabled them

432 Michael D. Bordo and Marc Flandreau

17. This is the logic of what Bordo and Kydland (1995) refer to as the gold standard as a con-tingent rule.

to buffer transitory shocks, very much in the same fashion modern devel-oped floaters can: Exchange rate depreciation did not induce capital flight.

Recent tests have suggested that in effect, support was provided by themarket itself, which took bets on the eventual reappreciation of the cur-rency, thus enabling monetary authorities to lower interest rates and thuscompensate for declining output; in other words, the gold points served asa credible target zone (Hallwood, MacDonald, and Marsh 1996; Bordo andMacDonald 1997). Working with data from the Vienna forward market,Flandreau and Komlos (2001) have shown that modern target zone theorywas in fact invented and successfully applied in Austria-Hungary in theearly twentieth century, once it had stabilized its currency. In the case oflarge foreign shocks (such as during the crisis of 1907) Austria-Hungarywould let its exchange rate go. This triggered stabilizing expectations thatenabled the monetary authorities to keep a lower interest rate than abroad,with speculators taking bets on an eventual reappreciation.

Thus, to a certain extent, the current trend toward floating in advancedcountries has some resemblance to a classical gold standard in which thefluctuation margins have been, in line with Keynes’ (1931, 314–31) pro-posal, widened to give more flexibility. The key difference between then andnow is that the nominal anchor—gold parity, around which the target zoneoperated—has been jettisoned and a domestic nominal anchor has beensubstituted in its place, which allows exchange rate flexibility without theconstraints of a target zone. Thus if the degree of flexibility compared to thegold standard is greater, the spirit is the same, a point to which we will comeback later.18

This possibility for the core countries of the classical gold standard era toactually manage the money supply despite the gold constraints is in sharpcontrast with what countries in the European periphery, in Asia, or in Latinand Central America could do.

On the one hand, floating did not create much room for them to conductactive monetary policies. Exchange depreciation often triggered expecta-tions of further depreciation rather than expectations of eventual stabiliza-tion. For instance, Flandreau and Komlos (2001) show that, intriguinglyenough, it was the stabilization of the Austro-Hungarian currency thatopened the door to active monetary policies. During the infamous periodof exchange rate gyrations that extended until the mid-1890s, exchange de-preciation was not usually followed by expectations of an eventual recov-

Core, Periphery, Exchange Rate Regimes, and Globalization 433

18. Thus, we are not arguing that monetary authorities are following a target zone approach,as advocated by (for example) Bergsten and Williamson (1983). Rather, we are arguing that thecredibility of adhering to gold convertibility gave the core countries before 1914 the flexibilityto conduct discretionary policy within the gold points as if they were operating in a target zoneà la Krugman (1991) and Svennson (1994), whereas today the credibility attached to followingmonetary rules such as inflation targeting gives the monetary authorities the freedom to oper-ate with much greater flexibility without the bands of a target zone.

ery—unlike what would happen when the country regained credibility af-ter joining the gold standard in 1896.

On the other hand, going onto gold did not buy immediate credibility, asillustrated by the levels of short-term interest rates in a number of typicalmembers of the periphery. Figure 9.4 shows that the weaker members of thegold club faced higher short-term interest rates even when on gold than is

434 Michael D. Bordo and Marc Flandreau

A

B

Fig. 9.4 Short-term interest rates (bank rates), 1880–1913, compared to UnitedKingdom: A, Chile; B, Greece; C, Portugal; D, Russia; E, ItalySource: See appendix.Note: Shaded areas represent periods when each country was on the gold standard.

C

D

E

Fig. 9.4 (continued)

consistent with their actual exchange rate record. This suggests some kindof peso problem. The high short-term rates faced by Chile, Greece, Portu-gal, Italy, or Russia during their more or less extended flirt with gold sug-gest that the problems that the modern periphery has with pegging havenineteenth-century precedents. The fact that even when on gold these coun-tries could face high short-term interest rates might explain why some ofthem ended up floating. An interesting case from that perspective is Chile,whose attempt at returning onto gold in 1895–98 involved both a sharp in-crease in interest rates—because that decision was not credible—and asubstantial fall in the rate of inflation, with the result that the stabilizationwas associated with huge real interest rates, recession, and a quick reversalto floating exchange rates (Subercaseaux 1926). Plus ça change . . .

9.3.3 Fear of Floating, Nineteenth-Century Style:A New View of the Gold Standard

If going on gold was so costly for the periphery, one may wonder why anumber of countries nonetheless sought to stick to gold. We argue that thischoice rested on something quite similar to the current fear-of-floatingdilemma. If fixing was quite painful under the gold standard for many of theperipheral countries, floating could be just as deadly as today. This was dueto pervasive problems of currency mismatch arising from the inability, forunderdeveloped borrowing countries, to issue foreign debts in their owncurrency.

It is well known from the works of historians that the financial markets ofthe less developed countries were very backward.19 This led governments ofthe European or Latin American periphery to issue their debts in the large fi-nancial markets of the core countries, such as London, Amsterdam, Paris, orlater Berlin, which by contrast had developed early on (Neal 1990). In effect,the investors in peripheral countries developed the habit of holding that partof their wealth which they invested in domestic bonds in the large markets ofthe core countries (Broder 1975; Lévy-Leboyer 1976; De Cecco 1990).

Borrowing abroad also implied borrowing in foreign currencies. Today,many emerging countries find it impossible to borrow abroad in their owncurrency. Ricardo Hausmann and various co-authors20 refer to these na-tions as suffering from “original sin.” Something similar existed one centuryago. According to John Francis (1859), exchange rate guarantees in inter-national bond issues were an innovation that had been pioneered by theLondon Rothschilds.21 The guarantees were widely used during the boom

436 Michael D. Bordo and Marc Flandreau

19. See Rousseau and Sylla (ch. 8 in this volume).20. See Hausmann et al. (1999), Hausmann, Pannizza and Stein (2000), Fernandez-Arias

and Hausmann (2000), and Eichengreen and Hausmann (1999).21. Previous to the advent of Mr. Rothschild, foreign loans were somewhat unpopular in

England, as the interest receivable abroad, subject to the rate of exchange, liable to foreigncaprice, and payable in foreign coin. He introduced the payment of the dividends in England,and fixed it in sterling money, one great cause of the success of these loans in 1825” (298–99).See also Ferguson (1998, 132–34).

of Latin American bond issues of the 1820s (Fodor 2000). As foreign in-vestment soared, this practice became widespread. Prior to the advent ofthe gold standard, countries were alternatively tied to gold, silver, or bi-metallic currencies depending on the market they were tapping. With thespread of the gold standard in Western Europe, gold clauses generalized.22

Fully comprehending the logic of these gold clauses is a theoretical chal-lenge that is beyond the scope of this paper. It is not clear, for instance, whyinvestors should have preferred a lower exchange rate risk—but with agreater default risk when exchange rate crises occurred—to a higher ex-change rate risk but a lower risk of default.

One possible answer is that, in a system where instruments to hedgeagainst long-run exchange rate risks were not available, the clauses enabledforeign investors to pass on the costs of exchange risk to issuing govern-ments or corporations.23 This was one way contemporaries rationalized thispractice, emphasizing that it was motivated by the risk aversion of foreigninvestors.24 But this would imply that contemporaries were more willing torun default risk than exchange rate risks.

Second, this practice might be understood as the solution to a commit-ment problem. While local issues could be easily inflated away, foreign is-sues with gold clauses provided safeguards, precisely because they in turninduced governments to be on their guard (Missale and Blanchard 1990).

Core, Periphery, Exchange Rate Regimes, and Globalization 437

22. Flandreau (2002) argues that this contributed to tying countries to the monetary systemof the financial center on which they depended, thus contributing to the emergence of regionalgroupings such as the Latin Union.

23. There were forward exchange markets, but only for a small number of currencies, andonly for short horizons (Einzig 1937). We are not aware of swap contracts that would have in-volved long-term cover against exchange rate risk. The only kind of protection against ex-change rate volatility would have been diversification, which by definition does not provide fullinsurance.

24. On Russia see de Block, (1889, 214): “Pour décider ces capitalistes à engager leurs fondsdans une entreprise dont l’avenir pour eux état incertain, il fallut leur garantir un minimumnormal de revenu annuel sur les actions et obligations de chemins de fer russes, en fixant ceminimum sur l’étalon métallique” (In order to convince capitalists to put their money in proj-ects whose success was for them uncertain, it was necessary to provide them with a guaranteedminimum revenue on their railway bonds and stocks and to index this minimum on a metallicstandard). On Spain, Austria, and Hungary see Lévy (1901, 6): “Chez nous surtout où les ren-tiers quelque peu timorés et mal au courant des questions de change ont marqué de tout tempsune grande répugnance à admettre dans leur portefeuille des titres don’t le revenu ne fût passtable; la première condition de cette fixité du coupon étant celle de la monnaie la conséquencenaturelle de cette exigence légitime de notre public a été la création de monbreaux titresétrangers stipulés payables en francs ou en or. L’un des premiers a été la rente espagnole ex-térieure 3% depuis transformée en 4%; puis sont venues les rentes autrichiennes 4% or, la rentehongroise 6% or” (In our country where rentiers are risk averse and not very conversant in ex-change matters and have always been reluctant to take in their portfolio bonds whose incomeis variable [and a necessary condition for revenue stability is the stability of the currency],francs or gold clauses emerged as a natural requirement in many bond issues. One of the firstwas the Spanish rente 3 percent, then came the Austrian 4 percent, the Hungarian 6 percent).On the United States, see Wilkins (1989, 619): “Often sovereign investors insisted on goldclauses in railroad bonds. They wanted ‘sound money’ in America and worldwide. The US ad-herence to a gold standard (after 1879) was in part a consequence of America’s desire to at-tract such investment.”

Figure 9.5 gives some support to this view because it shows that the shareof gold debt was an increasing function of total indebtedness for a numberof peripheral countries. On the other hand, it is hard to determine the ex-tent to which markets and governments were in a position to internalize theconsequences of gold clauses plus exchange depreciation: In the politicallyunstable, revolution-driven Latin America, could precommitment actuallywork? Moreover, although commitment might explain why some debtwould have been issued with gold clauses, it is not clear why all debt issuedabroad should have included such clauses.

A final possibility rests in the motivations of international bankers whosesyndicates arranged the loans. Because the bankers offered a number of ser-vices to cash-strapped government in periods of crisis, lending into arrearsand helping them to muddle through financial trouble, they were also in aposition to impose a lot of conditionality (Flandreau 2002). This asymme-try was often emphasized by contemporary observers: According to Lévy,“The creation of debts denominated in the currency of the lending countrycan be understood as resulting from the fact that it is the lending countrythat dictates its conditions to the borrowing part” (1901, 6). It must be thatthe bankers expected that the bonds they were prepared to guarantee wouldface a deeper and more willing demand as a result of the gold clauses, andthey thus persuaded borrowers to issue their securities with fixed exchangerate clauses that tied the coupon to the unit of the market where the bonds

438 Michael D. Bordo and Marc Flandreau

Fig. 9.5 Total indebtedness and currency mismatch: Austria, Hungary, Portugal,Greece, 1880–1913Source: Crédit Lyonnais Archives as adapted by the authors.

were sold.25 But then we are back to the question, why shouldn’t the regularinvestor be willing to hold paper debts, provided he gets a return for it?

In any case, given the situation, the fixed exchange rate clauses drew asharp line between those members of the core where there had been a longrecord of adherence to a convertible standard and those who did not. Asone leading financial economist of the time explained, robust gold convert-ibility was an acceptable substitute for the gold clauses: “When it comes tothe bonds of countries where the gold standard prevails, such as GreatBritain, Sweden, Norway, Denmark or Canada, special clauses are not nec-essary, since the obligation to pay in gold results from the fact that bondsare denominated in the currency of that country” (Lévy 1901, 6).

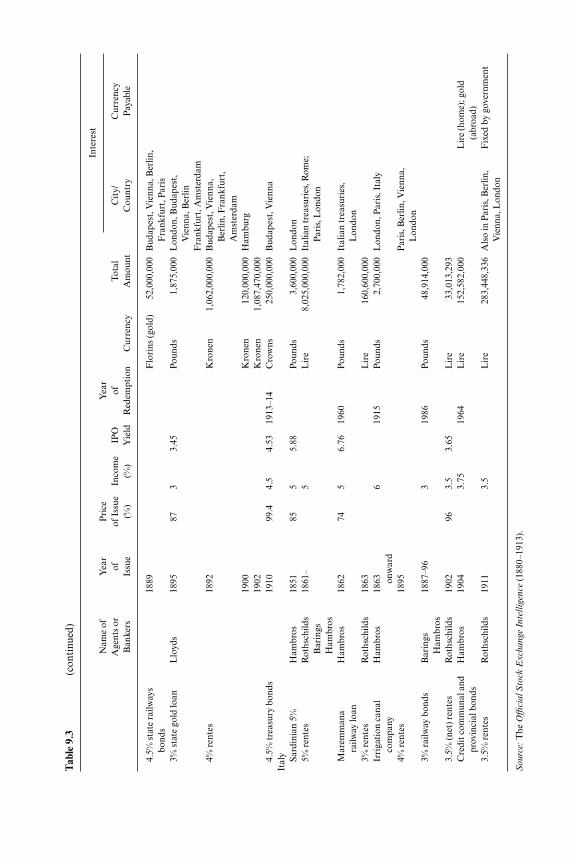

This was certainly a reason why a number of countries became quite in-terested in trying to find ways to stabilize their currency in terms of gold.Yet the gold standard was definitely not a perfect substitute for gold clauses,since the club of countries that could issue abroad debts denominated intheir own currency was much more selective than the gold club (as illus-trated later, in table 9.5, which shows the list of “senior” sovereigns in Lon-don.26 These data come from Burdett’s Official Stock Exchange Intelli-gence.) Table 9.3 lists the bonds with various characteristics, including thecurrency in which it was issued and the currency in which the coupon waspayable for ten major countries, eight of which issued bonds in their owncurrencies without fixed exchange rate clauses.27 Other countries listed onlyshowed bonds issued in some gold-tied unit.28

The borderline members of the list (i.e., those for which the currency de-nomination was ambiguous) provide interesting evidence that the mere sta-bilization of the currency in terms of gold was not enough. As can be seen,Austria-Hungary’s position is ambiguous. And as a matter of fact, we foundin separate French sources an interpretation of this problem: In the early1890s, this country sought to stabilize its currency and defined a new unit,the crown, with a fixed gold parity. At first, market participants understood

Core, Periphery, Exchange Rate Regimes, and Globalization 439

25. The fixed exchange rate clause could come in various ways: either by denominating thecurrency in the foreign currency, by denominating it in a gold or silver domestic unit that thushad a fixed exchange rate with foreign gold or silver units, or by stating the fixed exchange rateat which the coupon would be paid to foreigners regardless of the actual exchange rate againstpaper money. From an economic point of view all these are equivalent.

26. The countries that could issue sovereign bonds in terms of their own currencies duringthe period 1880–1914 were the United States, the United Kingdom, France, Germany, theNetherlands, Belgium, Denmark, and Switzerland. Two additional countries included in thetable that listed sovereign debt in their own currency were Austria, Hungary and Italy. How-ever, there is ample evidence to suggest that these bonds bore gold clauses. See Tattara (1999)and Flandreau (2002).

27. For the United States, table 9.3 shows three bonds listed as payable in gold coin for theyears 1895, 1898, and 1900. The previous bonds shown are listed as “payable in the coin stan-dard of the United States.” The changed status was a response to the silver uncertainty of the1890s, to remove any ambiguity over which metallic coin was the standard. See Wilkins (1989)and Laughlin (1903).

28. These data are available on request.

Tab

le 9

.3In

tern

atio

nal S

over

eign

Sec

urit

ies

Lis

ted

on th

e L

ondo

n S

tock

Exc

hang

e, 1

880–

1913

, Sel

ecte

d C

ount

ries

Inte

rest

Nam

e of

Yea

rP

rice

Yea

rA

gent

s or

ofof

Iss

ueIn

com

e IP

Oof

Tota

lC

ity/

Cur

renc

yB

anke

rsIs

sue

(%)

(%)

Yie

ldR

edem

ptio

nC

urre

ncy

Am

ount

Cou

ntry

Pay

able

Fra

nce

3% r

ente

s18

86–9

1F

ranc

s15

,304

,231

,433

Par

isN

o fix

ed e

xcha

nge

or p

ound

s61

2,16

9,25

64%

ren

tes

Fra

ncs

11,1

52,4

004.

5% r

ente

s, o

ldF

ranc

s83

1,85

5,66

64.

5% r

ente

s of

188

318

83F

ranc

s6,

789,

783,

906

or p

ound

s27

1,46

6,39

73%

red

eem

able

ren

tes

1878

1953

Fra

ncs

4,00

4,34

6,10

0P

aris

1881

or p

ound

s16

0,17

3,84

418

84G

erm

any

3.5%

con

sols

Mar

ks45

0,00

0,00

0G

erm

any

3% im

peri

al lo

anB

erlin

, 18

9087

33.

45M

arks

170,

000,

000

Ger

man

y, L

ondo

nM

arks

; pou

nds:

L

ondo

nex

chan

ge o

f the

day

1891

84.4

33.

55M

arks

200,

000,

000

1892

83.6

33.

59M

arks

160,

000,

000

1893

86.8

33.

46M

arks

160,

000,

000

1905

101.

23.

53.

46M

arks

300,

000,

000

3.5%

bon

ds19

0610

0.1

3.5

3.50

Mar

ks26

0,00

0,00

019

0995

.63.

53.

66M

arks

160,

000,

000

4% b

onds

1909

4B

avar

iaM

arks

940,

000,

000

Ber

lin, F

rank

furt

Pru

ssia

Pru

ssia

n co

nsol

s M

arks

3,59

2,66

7,85

0B

erlin

, chi

ef

(now

3.5

%)

Pru

ssia

n to

wns

4% c

onso

lsPo

unds

84,5

00,0

00B

erlin

, chi

ef

Pru

ssia

n to

wns

3% c

onso

lidat

ed

1890

–190

5M

arks

1,50

1,29

6,15

0L

ondo

n, G

erm

any

stat

e lo

an4%

bon

ds19

094

Mar

ks1,

260,

000,

000

3.5%

bon

ds19

0610

0.1

3.5

3.50

Mar

ks6,

090,

675,

900

The

Net

herl

ands

2.5%

1814

Flo

rins

626,

008,

900

Hol

land

Flo

rins

3.5%

of 1

830

1830

Flo

rins

3,35

6,00

0H

olla

ndF

lori

ns4%

Flo

rins

182,

075,

900

Hol

land

Flo

rins

; tw

elve

gui

lder

s to

the

poun

d3%

Bar

ings

1844

,189

6,18

98F

lori

ns46

8,17

5,30

0H

olla

ndF

lori

nsSt

ate

railw

ay s

tock

1870

Flo

rins

2,71

9,69

3St

ate

railw

ay s

tock

1876

Flo

rins

294,

000

3.5%

1886

Flo

rins

11,2

50,0

00A

mst

erda

m,

Lon

don,

Par

isF

rank

furt

, Ber

lin4%

1878

98.3

754

4.07

1936

Flo

rins

43,0

00,0

00H

olla

ndF

lori

nsPo

unds

3,58

3,33

34%

of 1

883

1883

98.7

54

4.05

1939

Flo

rins

609,

000,

000

Am

ster

dam

Flo

rins

Poun

ds5,

075,

000

3.5%

of 1

891

1892

100.

53.

53.

48F

lori

ns44

,700

,000

Am

ster

dam

3.5%

loan

, 191

119

113.

5A

mst

erda

m;

Flo

rins

; at t

he e

xcha

nge

Lon

don,

Par

is,

of th

e da

yB

erlin

H

ambu

rg,

Fra

nkfu

rtU

nite

d St

ates

4.5%

fund

ed18

7618

91D

olla

rs30

0,00

0,00

0A

mer

ica

4% fu

nded

1877

1907

Dol

lars

1,00

0,00

0,00

0A

mer

ica

3%18

82D

olla

rs27

4,93

7,25

0A

mer

ica

4.5%

loan

of 1

891

Dol

lars

25,3

64,5

00G

old

coin

4% lo

an18

9519

25D

olla

rs16

2,31

5,40

0U

nite

d St

ates

Gol

d co

in3%

loan

1898

1908

Dol

lars

198,

792,

660

2% th

irty

-yea

r bo

nds

1900

1930

Dol

lars

646,

250,

150

Uni

ted

Stat

esG

old

coin

Bel

gium

2.5%

Rot

hsch

ilds

1842

Fra

ncs

389,

271,

000

Bel

gium

Par

is4%

Fra

ncs

731,

287,

900

Fra

ncs

134,

719,

000

4% lo

an o

f 188

318

8310

4.28

43.

84F

ranc

s16

4,79

6,00

0B

elgi

um, P

aris

3.5%

deb

t18

86F

ranc

s1,

296,

935,

757

Bel

gium

, Par

is(c

onti

nued

)

Tab

le 9

.3(c

onti

nued

)

Inte

rest

Nam

e of

Yea

rP

rice

Yea

rA

gent

s or

ofof

Iss

ueIn

com

e IP

Oof

Tota

lC

ity/

Cur

renc

yB

anke

rsIs

sue

(%)

(%)

Yie

ldR

edem

ptio

nC

urre

ncy

Am

ount

Cou

ntry

Pay

able

3% b

onds

18

95F

ranc

s54

4,95

6,27

5(fi

rst s

erie

s)18

97F

ranc

s20

8,04

6,50

018

98F

ranc

s19

5,99

3,80

03%

bon

ds (s

econ

d B

arin

gs18

73–1

912

Fra

ncs

1,91

2,52

0,80

0B

elgi

um, P

aris

, F

ranc

s po

und:

25

fran

cs

seri

es)

Lon

don

25 c

ents

(fixe

d)C

ashi

er o

f sta

te18

95F

ranc

s96

0,48

9,88

2R

oths

child

s3%

bon

ds (t

hird

Cas

hier

of s

tate

1895

Fra

ncs

200,

040,

000

Bel

gium

Fra

ncs;

pou

nd: 2

5 fr

ancs

se

ries

)25

cen

ts (fi

xed)

Rot

hsch

ilds

3F

ranc

s59

,856

,600

Par

is3%

con

vers

ion

loan

1895

Fra

ncs

1,30

1,44

6,05

7B

elgi

um, P

aris

Den

mar

k4%

185

0H

ambr

os18

50–6

190

44.

44Po

unds

400,

000

4% 1

862

Ham

bros

1862

914

4.40

Poun

ds66

0,00

04%

sta

te lo

anH

ambr

os18

80K

rone

n26

,339

,700

Lon

don

Poun

d93

,525

3.5%

inte

rnal

H

ambr

os18

8798

.53.

53.

55K

rone

n15

5,00

0,00

0C

open

hage

n,C

urre

nt e

xcha

nge

rate

de

bt lo

anL

ondo

n

3.5%

am

orti

sabl

eC

rédi

t Lyo

nnai

s19

0094

.75

3.5

3.69

Cop

enha

gen,

lo

anL

ondo

n, P

aris

, B

erlin

Ham

burg

, Bru

ssel

s3%

gol

d lo

an o

f 189

4H

ambr

os18

9496

.375

33.

1119

14K

rone

n66

,306

,000

Lon

don,

Par

isE

xcha

nge

of th

e da

y;

10.5

0 fr

ancs

per

500

kr

onen

or p

ound

s3,

684,

777

Cop

enha

gen,

3% g

old

loan

of 1

897

Ham

bros

1897

99.1

253

3.03

Lon

don,

Par

is

4% lo

an o

f 191

2H

ambr

os19

1297

44.

12Po

unds

2,50

0,00

0L

ondo

n, P

aris

, St

erlin

g; 2

5.20

fran

cs;

Cop

enha

gen

1816

kro

nen

Ham

burg

, 20

.43

reic

hsm

arks

, A

mst

erda

m12

.10

flori

nsSw

itze

rlan

d3.

5% lo

an19

03–0

7F

ranc

s50

0,00

0,00

0Sw

itze

rlan

dL

ondo

nA

ustr

iaA

ustr

ian

5% s

ilver

18

68–

Flo

rins

1,00

5,75

7,89

5V

ienn

aSi

lver

rent

esA

ustr

ian

5% p

aper

18

68–

Flo

rins

1,48

3,38

7,48

7V

ienn

aP

aper

rent

esA

ustr

ian

4% g

old

1876

–F

lori

ns49

0,85

0,20

0V

ienn

a; B

erlin

, G

old;

mar

ks, 2

0.25

re

ntes

Stut

tgar

t,

mar

ks p

er 1

0 flo

rins

Fra

nkfo

rtB

russ

els,

F

ranc

s, 2

5 fr

ancs

per

10

Am

ster

dam

, Par

isflo

rins

Pap

er r

ente

s18

81F

lori

ns23

8,87

7,10

0P

aper

Aus

tria

n 4%

con

vert

ed

1903

Kro

nen

3,61

4,48

6,82

0V

ienn

are

ntes

Bru

ssel

s, A

mst

er-

25 fr

ancs

per

10

flori

nsda

m, P

aris

, Bal

e, Z

urig

Aus

tria

n 4%

kro

nen

1901

–12

Kro

nen

2,26

5,84

4,50

0V

ienn

a, A

mst

erda

m,

rent

esG

erm

any

Aus

tria

n 3.

5% r

ente

s18

97K

rone

n or

116,

901,

000

flori

ns58

,450

,500

Hun

gary

Hun

gari

an lo

anL

ondo

n &

18

6871

.66

56.

9819

17Po

unds

8,51

2,56

0C

ount

yP

aris

, Fra

nkfo

rt-o

n-th

e-M

ain,

Am

ster

dam

Vie

nna,

Bud

apes

t5%

187

1R

apha

els

1872

815

6.17

1904

Poun

ds30

0,00

05%

of 1

873

Rap

hael

s18

7380

56.

2519

04Po

unds

5,40

0,00

0P

aris

, Fra

nkfo

rt-o

n-th

e-M

ain,

Am

ster

dam

Vie

nna,

Bud

apes

t4%

gol

d re

ntes

Rot

hsch

ilds

1881

–88