globe specialty metals - the global investment banking firm · 750,000 tons consumed by silicones...

TRANSCRIPT

Globe Specialty Metals

August 2014

1

Silicon – Product Line & End Markets

Silicon

99% Si content 75% Si alloyed with Fe 50% Si alloyed with

Fe, Mg & rare earths

New product development & expanding uses driven by R&D (e.g. electric cars, semiconductors)

Silicon Metal

53% of Revenue

Silicon Alloys

47% of Revenue

Note: Revenue percentages exclude 49% of the joint ventures owned by Dow Corning

2

GSM: The Leader in Silicon – Well Positioned for Further Growth

The lowest cost silicon producer and one of the world’s largest

• Owner of 100% of merchant capacity in North America (6 N.A. smelters). Other producer is Dow Corning, producing for internal consumption

• Leading global silicon alloys producer

Global reach with 13 facilities in 6 countries – U.S., Canada, Argentina, Poland, China, and South Africa

Strong, flexible balance sheet – designed for growth

Built and run by entrepreneurs with strong and proven M&A and operational backgrounds and unique investment approach

3

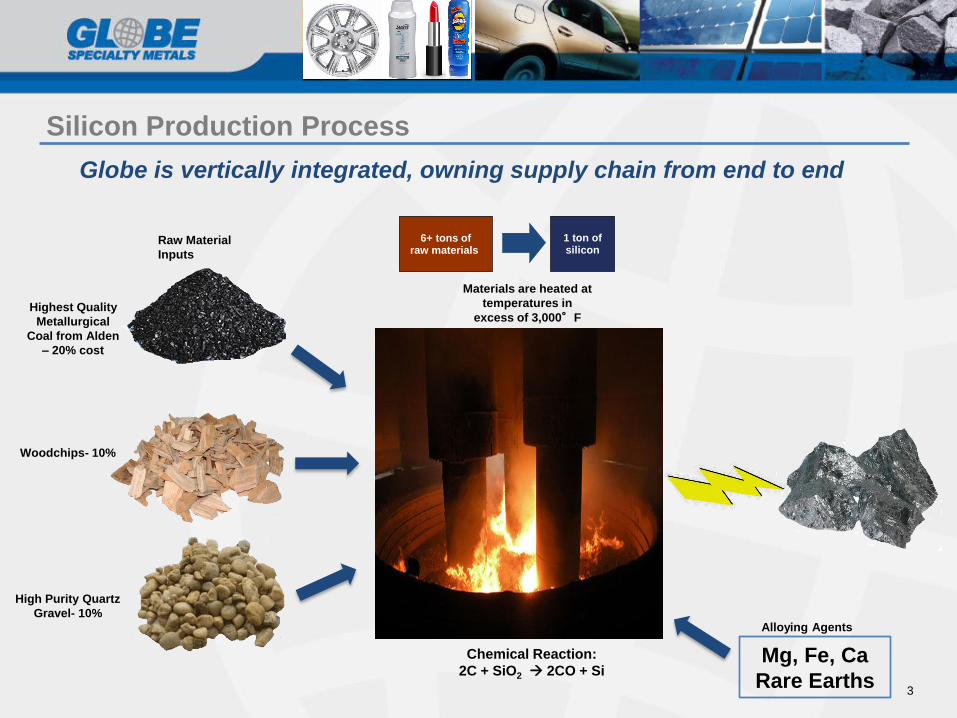

Silicon Production Process

Raw Material

Inputs

Highest Quality

Metallurgical

Coal from Alden

– 20% cost

Woodchips- 10%

High Purity Quartz

Gravel- 10%

Materials are heated at

temperatures in

excess of 3,000°F

6+ tons of raw materials

1 ton of silicon

Chemical Reaction:

2C + SiO2 2CO + Si

Globe is vertically integrated, owning supply chain from end to end

Alloying Agents

Mg, Fe, Ca

Rare Earths

4

North America81%

Asia/Other4%

Europe11%

South America4%

Well-Diversified Business in Growing Markets

Revenue Mix End-markets

Customers – Minimal Concentration

Note: All data exclude the 49% of the joint ventures owned by Dow Corning Data represents fiscal year 2013 results

Revenue by region

Silicon, 53%

Silicon Alloys, 47%

11%

6%

4%

3% 2% 2%

2% 2%

2% 2%

Other 58%

Aluminum20%

Silicones15%

Polysilicon10%

Other16%

Steel16%

Foundry Alloys21%

5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Acquisition of Selma, AL Alloy, WV Mendoza, Camargo, Yonvey, Core Metals, Alden, KY Becancour, Siltech,

Assets Niagara, NY AS&G, AL Argentina Brazil China AL Canada South Africa

Beverly, OH Alloy Power San Luis, MPM, IN

Argentina

Divestiture of Alloy Power Camargo

Assets Alloy - 49%

Estimated

Replacement Cost $2,275

Acquisition Price $404

Divestiture Price (295)

Total Net Investment $109

Multiple of

Net Investment

Total Replacement Cost less Divestitures: $1,980 18.2x

Total Enterprise Value Today: $1,541 14.1x

Continuing Growth through Key, Strategic, Timely & Accretive Acquisitions

$ in millions

Note: Management estimates using replacement value of $90M for a standard sized furnace

6

Global Production Footprint

7

Silicon End Markets: Silicones (50% of Silicon metal market)

750,000 tons consumed by silicones industry

GDP + 4% growth – NA silicones facilities running at full capacity

Note: % of sales figures represent industry estimates of western world consumption For additional detail on silicones end markets, visit www.silicones.eu

Paint

Grout Sealants

Cables

Tires

Weather stripping

Coatings

Dashboard

Caulking Shampoo Cosmetics

8

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E

2.0% 2.1%

3.9%

4.5%

7.1%

6.4%6.9%

7.8%

8.8%

10.4%

13.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015E 2020E

Silicon End Markets: Aluminum (40% of Silicon metal market) Silicon metal is required in aluminum as a strengthener and alloying agent to improve

castability and minimize shrinking and cracking

Significant growth expected in silicon-intensive aluminum wheels to meet EPA regulations for the trucking industry (aluminum wheels average 7.5% silicon content by weight)

Aluminum provides a lighter weight alternative to steel

Aluminum demand has increased at a 5%+ CAGR for the past 20 years

North American light vehicle aluminum content as a percent of curb weight

Source: Ducker Worldwide Note: Based on 3,600 lbs of curb weight

Global primary aluminum demand (000s tons)

Source: Bloomberg and Street research

343 pounds

77 pounds

Approx. 10kg of silicon metal per car

~500 pounds

9

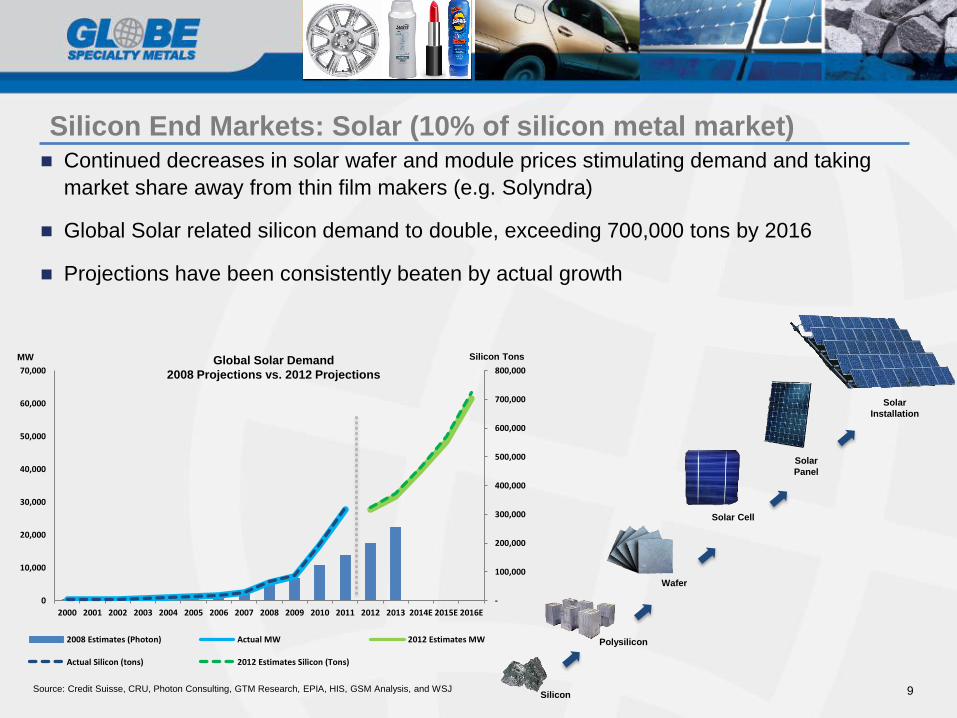

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E 2016E

2008 Estimates (Photon) Actual MW 2012 Estimates MW

Actual Silicon (tons) 2012 Estimates Silicon (Tons)

Silicon End Markets: Solar (10% of silicon metal market) Continued decreases in solar wafer and module prices stimulating demand and taking

market share away from thin film makers (e.g. Solyndra)

Global Solar related silicon demand to double, exceeding 700,000 tons by 2016

Projections have been consistently beaten by actual growth

Source: Credit Suisse, CRU, Photon Consulting, GTM Research, EPIA, HIS, GSM Analysis, and WSJ

Global Solar Demand

2008 Projections vs. 2012 Projections

MW Silicon Tons

Silicon

Polysilicon

Wafer

Solar Cell

Solar

Panel

Solar

Installation

10

Silicon End Markets: Semiconductors

Silane gas is an essential material used in the production of semi-conductors and LCD display panels

The three strongest demand areas for semiconductors will be NAND flash, logic application specific integrated circuits, and microprocessors

NAND and ASIC demand will be driven by media tablets and smartphones

Microprocessor growth will be driven by demand for computers, tablets, and smart phone devices

$200

$250

$300

$350

$400

2011 2012 2013 2014 2015 2016

Semiconductor Revenue ($ in Bn)

Source: IHS

11

Silicon Alloys End Markets: Steel (electrical steel)

Ferrosilicon (FeSi)

Calcium Silicon (CaSi)

Steel

Only 6 producers in Western World

~18% global market share and ~50% U.S. share

High grade specifications

Requires technical know-how

Used in production of carbon steels, stainless steels and other steel alloys

Technical expertise

Just-in-time delivery

1 of 2 U.S. producers

~50% U.S. capacity and ~40% North American capacity

Commodity Specialty

12

Ductile Iron Castings Ductile Iron Pipe

Magnesium Ferrosilicon (MgFeSi)

Foundry

Used in applications where strength and formability are required

− Automotive components

Often sole supplier

Water transmission

~50% share of the magnesium ferrosilicon market in the Americas and 20% in the Western World

Silicon Alloys End Markets: Foundry Products

13

Silicon End Markets: New Applications & Products

Example: Silicon anode Lithium-ion battery

Greater energy storage capabilities

Allows for smaller sizes batteries for electronic devices and electric cars

Energy storage for renewable energy sources

14

Silica Fume End Markets: Construction, Oil & Gas, Refractory

Collected in bag houses – sold to concrete, oil well and refractory end markets

Key benefits of silica fume:

• Physical strength of concrete up to 20,000 psi

• Very low permeability to water and chloride intrusion of cement

• Extremely high electrical resistivity (up to 100x greater than ordinary concrete)

• Increased resistance to chemical attack from acids, nitrates and sulfates

New applications have significantly added to demand and increases in price

GSM’s Silica Fume Used in:

Key Component in Hydraulic Fracturing Process Construction

(One World Trade Center-NYC)

Infrastructure/public works

(Panama Canal Expansion)

Oil Wells Refractory

15

New Capacity Pre-requisites

1. Capital cost, lead time, and permitting obstacles of green field construction

2. Technology and operational expertise

3. Power (35% of cost) – requires stable, long-term supply of low cost electricity.

4. Raw materials (40% of cost) – requires access to high purity, low cost raw materials

6+ tons of

raw materials 1 ton of silicon

Raw materials are emerging as the most critical differentiator – Globe owns its entire supply chain

The gas/energy revolution in the US should, in the near term, reduce energy costs & increase demand for its products

16

Globe’s Supply Chain has Key Logistical Advantages

Globe is vertically integrated--Owns its supply chain from end to end

17

Substantial Leverage to Price

Costs are stable and facilities are some of the most efficient in the world

Each 1¢/lb ($22/mt) increase in silicon & silicon alloys price leads to ~$5.3

million more in EBITDA at full capacity

0

50

100

150

200

250

300

350

400

450

500

$1.25$1.00

$1.35$1.10

$1.45$1.20

$1.55$1.30

$1.65$1.40

$1.75$1.50

$1.85$1.60

$1.95$1.70

EBITDA, $m

Incremental EBITDA

Silicon Metal PricingSilicon-Based Alloys Pricing

18

0

500

1,000

1,500

2,000

2,500

3,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E

Western World China & CIS

Global Silicon Consumption to Grow ~6% by 2018

Source: CRU

kMT

19

Third Party Low Ash Coal Sales

Only significant North American supplier of specialty low ash

metallurgical coal used in the production of SiM and specialty FeSi

Leverage coal assets to supply ultra special low ash coal to other silicon metal producers at a premium price

Best quality low ash coal in the world for silicon production — management estimates coal improves furnace efficiency up to 10%

Other currently available alternatives are Charcoal & Colombian coal

• Charcoal – more expensive and supply constrained

• Colombian coal – not as reactive with quartz - lower efficiency

20

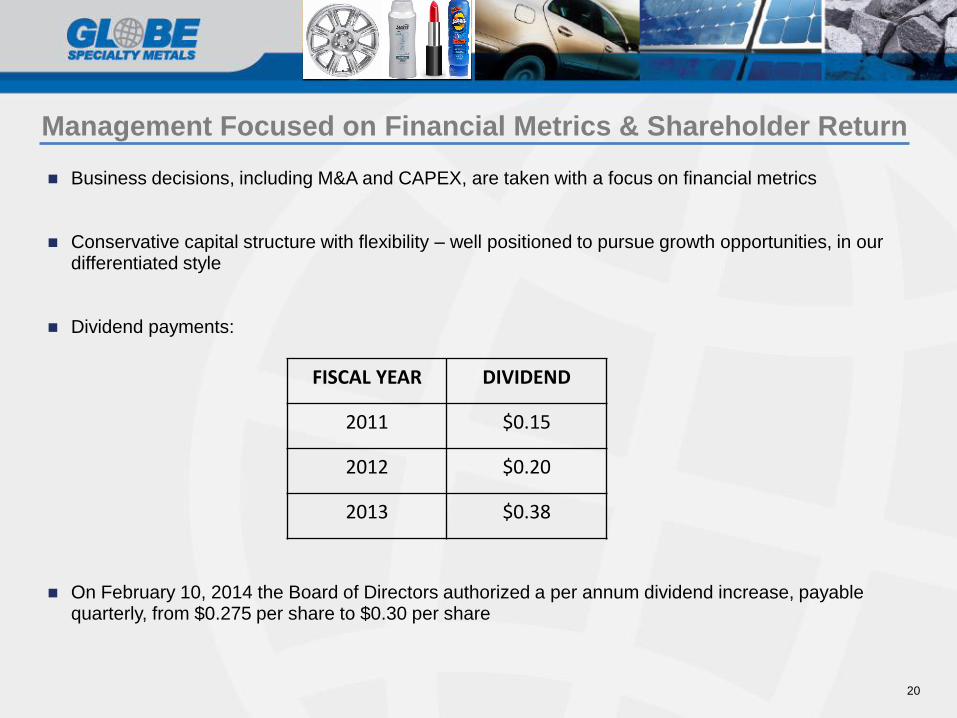

Management Focused on Financial Metrics & Shareholder Return

Business decisions, including M&A and CAPEX, are taken with a focus on financial metrics

Conservative capital structure with flexibility – well positioned to pursue growth opportunities, in our differentiated style

Dividend payments:

On February 10, 2014 the Board of Directors authorized a per annum dividend increase, payable quarterly, from $0.275 per share to $0.30 per share

FISCAL YEAR DIVIDEND

2011 $0.15

2012 $0.20

2013 $0.38

21

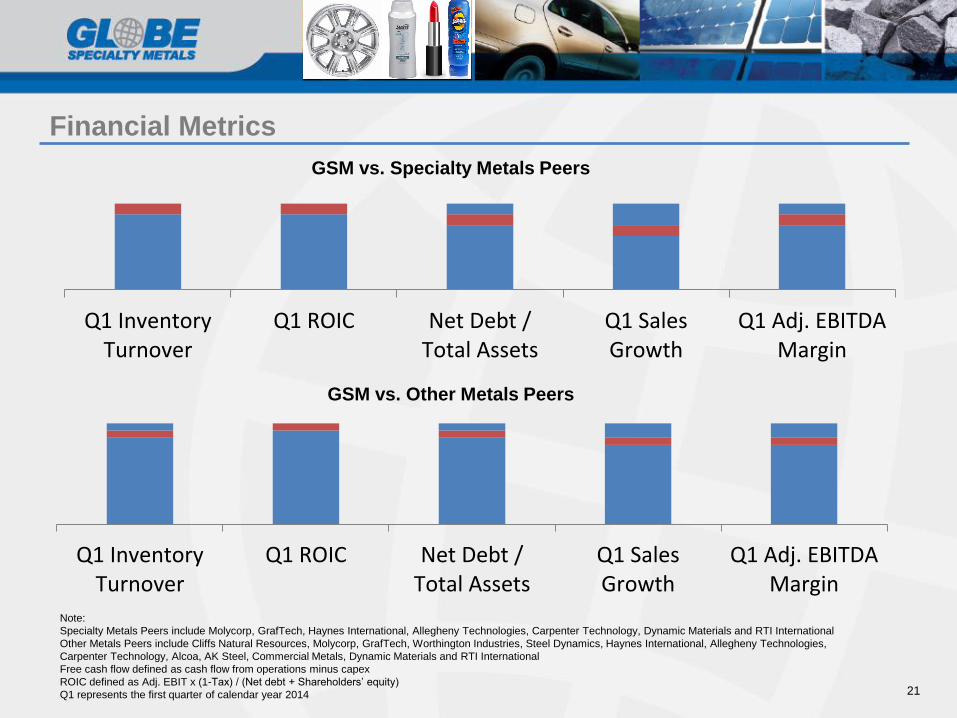

Financial Metrics

Q1 InventoryTurnover

Q1 ROIC Net Debt /Total Assets

Q1 SalesGrowth

Q1 Adj. EBITDAMargin

GSM vs. Specialty Metals Peers

Q1 InventoryTurnover

Q1 ROIC Net Debt /Total Assets

Q1 SalesGrowth

Q1 Adj. EBITDAMargin

GSM vs. Other Metals Peers

Note:

Specialty Metals Peers include Molycorp, GrafTech, Haynes International, Allegheny Technologies, Carpenter Technology, Dynamic Materials and RTI International

Other Metals Peers include Cliffs Natural Resources, Molycorp, GrafTech, Worthington Industries, Steel Dynamics, Haynes International, Allegheny Technologies,

Carpenter Technology, Alcoa, AK Steel, Commercial Metals, Dynamic Materials and RTI International

Free cash flow defined as cash flow from operations minus capex

ROIC defined as Adj. EBIT x (1-Tax) / (Net debt + Shareholders’ equity)

Q1 represents the first quarter of calendar year 2014

22

Globe’s Strategy & Roadmap

Global uncertainty

Shorter Cycles

Less forward visibility

Necessity of discipline

Increased risk of mis-timing and over paying for investments

Environment

Continue cyclical trough acquisitions at low costs

Patience

Discipline

High return investments

Globe’s Strategy

Faster Growth & Higher Returns

23

Highlights

Diverse and strong end markets

Leading cost position—with room for further improvements

• Vertical integration

• New capacity pre-requisites

Strong balance sheet

Significant access to deal flow at opportune time

Substantial leverage to price

Shareholder friendly

Strong entrepreneurial management team with:

• Strong M&A and operational track record

• Focus on financial metrics which drives decision making

• Significant investment in company

APPENDIX

25

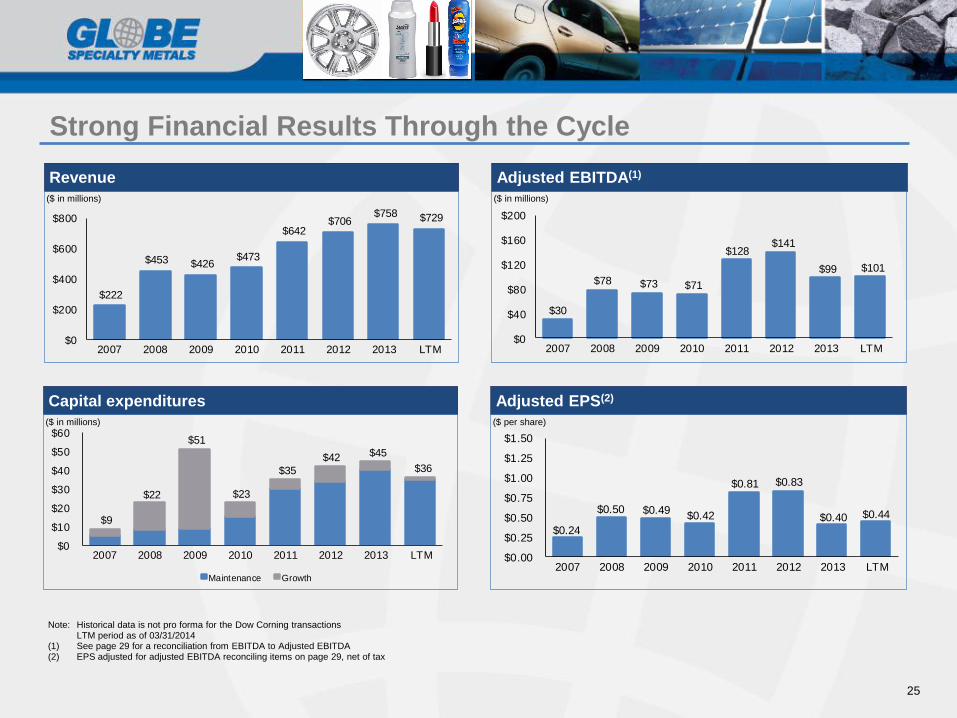

Strong Financial Results Through the Cycle

Adjusted EBITDA(1)

($ in millions)

Revenue

($ in millions)

Note: Historical data is not pro forma for the Dow Corning transactions LTM period as of 03/31/2014 (1) See page 29 for a reconciliation from EBITDA to Adjusted EBITDA (2) EPS adjusted for adjusted EBITDA reconciling items on page 29, net of tax

Adjusted EPS(2)

($ per share)

Capital expenditures

($ in millions)

$222

$453 $426 $473

$642 $706

$758 $729

$0

$200

$400

$600

$800

2007 2008 2009 2010 2011 2012 2013 LTM

$30

$78 $73 $71

$128 $141

$99 $101

$0

$40

$80

$120

$160

$200

2007 2008 2009 2010 2011 2012 2013 LTM

$9

$22

$51

$23

$35

$42 $45

$36

$0

$10

$20

$30

$40

$50

$60

2007 2008 2009 2010 2011 2012 2013 LTM

Maintenance Growth

$0.24

$0.50 $0.49 $0.42

$0.81 $0.83

$0.40 $0.44

$0.00

$0.25

$0.50

$0.75

$1.00

$1.25

$1.50

2007 2008 2009 2010 2011 2012 2013 LTM

26

Management Team

Alan Kestenbaum, Executive Chairman

Founded GSM through the roll-up of global silicon assets and subsequently led GSM through it’s IPO on NASDAQ and several key acquisition

and divestitures

Over 20 years' experience in metals trading, distribution, finance and manufacturing

Founded leading international metals trader, Marco International, in 1985 and led its expansion into China and former Soviet Union

Managed a series of successful metals private equity transactions

Began his career in metals with Glencore and Philip Brothers in New York

Joseph Ragan, Chief Financial Officer

Joined GSM in 2013

CFO of Boart Longyear 2008-2013

Prior roles include: CFO, GTSI Corp; Interim CFO for several underperforming companies; CFO, US Operations of Winstar Communications;

Vice President, PSEG Global; Subsidiary CFO, The AES Corporation; Consultant, Deloitte & Touche; Military Intelligence Officer, US Army

Jeff Bradley, Chief Executive Officer

30 years experience in the metals industry

Joined GSM in 2008

Prior roles include: CEO – Claymont Steel (former public company); Vice President and General Manager – Worthington Industries

27

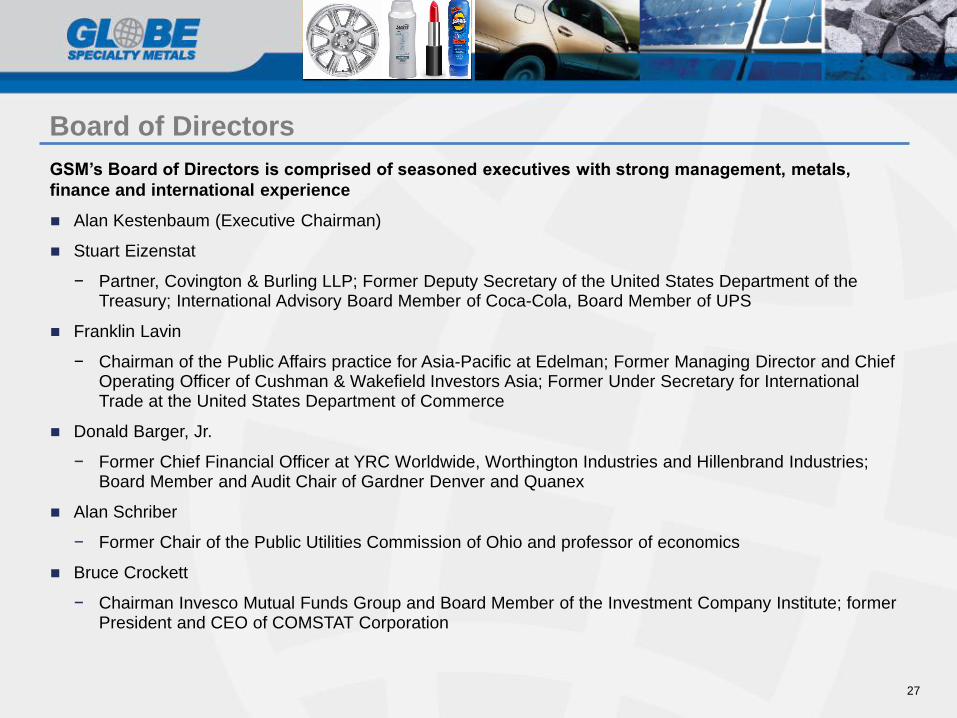

Board of Directors

GSM’s Board of Directors is comprised of seasoned executives with strong management, metals,

finance and international experience

Alan Kestenbaum (Executive Chairman)

Stuart Eizenstat

− Partner, Covington & Burling LLP; Former Deputy Secretary of the United States Department of the Treasury; International Advisory Board Member of Coca-Cola, Board Member of UPS

Franklin Lavin

− Chairman of the Public Affairs practice for Asia-Pacific at Edelman; Former Managing Director and Chief Operating Officer of Cushman & Wakefield Investors Asia; Former Under Secretary for International Trade at the United States Department of Commerce

Donald Barger, Jr.

− Former Chief Financial Officer at YRC Worldwide, Worthington Industries and Hillenbrand Industries; Board Member and Audit Chair of Gardner Denver and Quanex

Alan Schriber

− Former Chair of the Public Utilities Commission of Ohio and professor of economics

Bruce Crockett

− Chairman Invesco Mutual Funds Group and Board Member of the Investment Company Institute; former President and CEO of COMSTAT Corporation

28

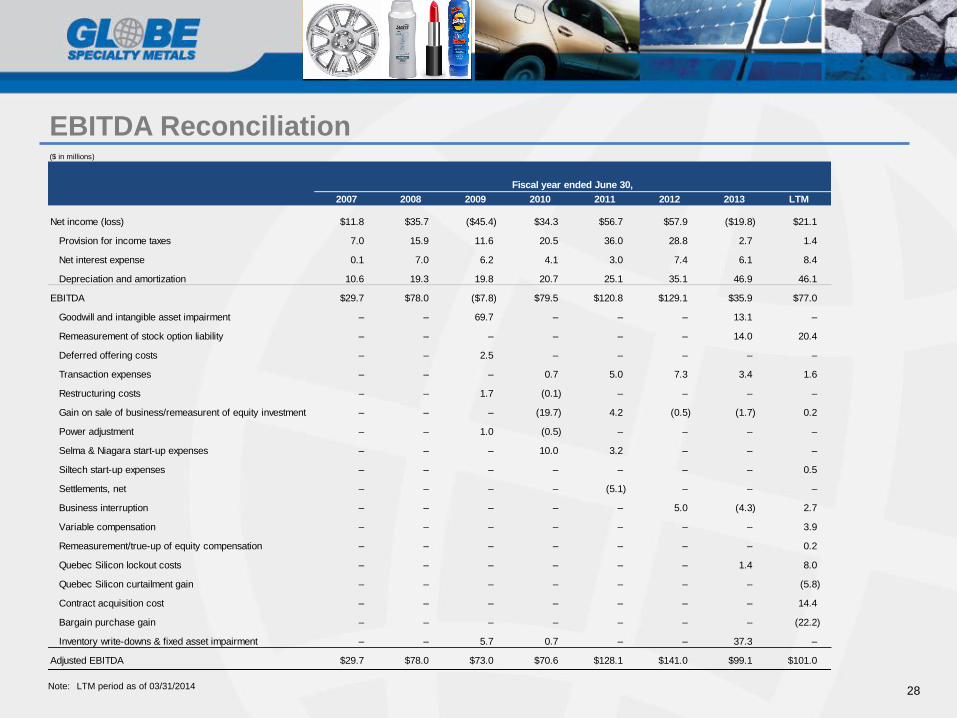

EBITDA Reconciliation

($ in millions)

Fiscal year ended June 30,

2007 2008 2009 2010 2011 2012 2013 LTM

Net income (loss) $11.8 $35.7 ($45.4) $34.3 $56.7 $57.9 ($19.8) $21.1

Provision for income taxes 7.0 15.9 11.6 20.5 36.0 28.8 2.7 1.4

Net interest expense 0.1 7.0 6.2 4.1 3.0 7.4 6.1 8.4

Depreciation and amortization 10.6 19.3 19.8 20.7 25.1 35.1 46.9 46.1

EBITDA $29.7 $78.0 ($7.8) $79.5 $120.8 $129.1 $35.9 $77.0

Goodwill and intangible asset impairment – – 69.7 – – – 13.1 –

Remeasurement of stock option liability – – – – – – 14.0 20.4

Deferred offering costs – – 2.5 – – – – –

Transaction expenses – – – 0.7 5.0 7.3 3.4 1.6

Restructuring costs – – 1.7 (0.1) – – – –

Gain on sale of business/remeasurent of equity investment – – – (19.7) 4.2 (0.5) (1.7) 0.2

Power adjustment – – 1.0 (0.5) – – – –

Selma & Niagara start-up expenses – – – 10.0 3.2 – – –

Siltech start-up expenses – – – – – – – 0.5

Settlements, net – – – – (5.1) – – –

Business interruption – – – – – 5.0 (4.3) 2.7

Variable compensation – – – – – – – 3.9

Remeasurement/true-up of equity compensation – – – – – – – 0.2

Quebec Silicon lockout costs – – – – – – 1.4 8.0

Quebec Silicon curtailment gain – – – – – – – (5.8)

Contract acquisition cost – – – – – – – 14.4

Bargain purchase gain – – – – – – – (22.2)

Inventory write-downs & fixed asset impairment – – 5.7 0.7 – – 37.3 –

Adjusted EBITDA $29.7 $78.0 $73.0 $70.6 $128.1 $141.0 $99.1 $101.0

Note: LTM period as of 03/31/2014