grade 12 accounting september 2018 memorandum trial 2018.pdf · credit balance according to the...

TRANSCRIPT

MARKS: 300

MARKING PRINCIPLES: 1. Penalties for foreign items are applied only if the candidate is not losing marks elsewhere in the

question for that item (no penalty for misplaced item). No double penalty applied. 2. Penalties for placement or poor presentation (e.g. details) are applied only if the candidate is earning

marks on the figures for that item. 3. Full marks for correct answer. If answer incorrect, mark the workings provided. 4. If a pre-adjustment figure is shown as a final figure, allocate the part-mark for the working for that

figure (not the method mark for the answer). Note: if figures are stipulated in memo for components of workings, these do not carry the method mark for final answer as well.

5. Unless otherwise indicated, the positive or negative effect of any figure must be considered to award the mark. If no + or – sign or bracket is provided, assume that the figure is positive.

6. Where indicated, part-marks may be awarded to differentiate between differing qualities of answers from candidates.

7. This memorandum is not for public distribution, as certain items might imply incorrect treatment. The adjustments made are due to nuances in certain questions.

8. Where penalties are applied, the marks for that section of the question cannot be a final negative. 9. Where method marks are awarded for operation, the marker must inspect the reasonableness of the

answer and at least one part must be correct before awarding the mark. 10. Operation means 'check operation'. 'One part correct' means operation and one part correct. Note;

check operation must be +, -, x, ÷, or per memo. 11. In awarding method marks, ensure that candidates do not get full marks for any item that is incorrect

at least in part. Indicate with a . 12. Be aware of candidates who provide valid alternatives beyond the marking guideline. 13. Codes: f = foreign item; p = placement/presentation.

This memorandum consists of 22 pages.

NATIONAL

SENIOR CERTIFICATE

GRADE 12

ACCOUNTING

SEPTEMBER 2018

MEMORANDUM

Accounting 2 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

QUESTION 1 RECONCILIATIONS 1.1 BANK RECONCILIATION

1.1.1

Calculate the correct balance of the Bank Account on 28 February 2018. 12 500 + 34 360 ‒ 37 480 + 540 + 2 700 ‒ 180 ‒ 780 + 250 ‒ 1 750 + 2 500 ‒ 3 100 = 9 560 one part correct

Foreign entries: ‒ 1 (max 1) Be aware of foreign entries incorrectly duplicated in journals and/or reconciliation.

1.1.2 Prepare the Bank Reconciliation Statement on 28 February 2018.

Bank reconciliation statement on 28 February 2018

Debit Credit

Credit balance according to the bank statement 6 790 Balancing figure, one part correct

Credit outstanding deposits (3 400 + 2 050 ) 5 450

Debit outstanding cheques:

Nr. 928 500

Nr. 1010 780

Nr. 1013 1 400

Debit balance according to bank account 9 560

Both columns equal 12 240 12 240

Foreign entries: ‒ 1 (max 1) Be aware of foreign entries incorrectly duplicated in journals and/or reconciliation.

12

8

Accounting 3 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

1.1.3

Refer to information A. The owner asked the bookkeeper, Ray Duncan, why the deposit of R2 050 was not yet deposited. Ray said that she was very busy at that time and could not deposit the money. She kept it in her drawer and forgot about it. She brought it to the owner and said that she will deposit it as soon as possible. What control measures can the owner put in place to avoid this situation in the future? Provide TWO measures.

Separation of duties – deposits must be recorded by one person and deposited by another

Use a drop safe which is picked up by the bank

Check outstanding deposits weekly

Any acceptable answer

1.1.4

Refer to Information E. When the financial statements will be drawn up on 28 February 2018, an adjustment has to be made for cheque no. 1010 where R780 has to be added to Bank and to Creditors control. Explain why this adjustment has to be made and why the R780 has to be added to Trade and other Payables.

The cheque is post dated for the coming year . The cheque will not be paid this year, therefore the entry in the cash payments journal did actually not decrease the bank balance

It is shown as a creditor because the business must be aware that this payment must be provided for as the recipient of the cheque can bank the cheque any given time from the date on the cheque.

2

4

Accounting 4 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

1.2 CREDITORS RECONCILIATION

1.2.1

No.

Creditor’s Ledger of

Tyrone Suppliers

Statement from Richard

Traders

Balance 9 330 11 800

1. ‒ 2 400

2. + 350

3. ‒ 50

4. + 6 300

5. + 5 400 (or + 2 700 one mark, +

2 700 one mark)

6. ‒ 670

Total 15 030 15 030

column totals added, including the opening balances

.

TOTAL MARKS

35

9

Accounting 5 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

QUESTION 2 COST ACCOUNTING 2.1 SEW NEW CURTAINS

2.1.1 Production cost statement for the year ended 31 March 2018

Direct material 2 270 000

Direct labour 34 500 (2 marks)

(780 000 ‒ 260 000 ‒ 175 000) + 34 500 379 500

Prime cost 2 649 500

Factory overhead cost Transfer from note 609 500

Total cost of production 3 259 000

Work in process (beginning of the year) 69 500

3 328 500

Work in process (end of the year) Balancing figure, must be deducted

(72 000)

Total cost of production of complete products 2 605 200 x 100/80

3 256 500

Factory overhead cost

Indirect labour (260 000 + 26 000 ) * 286 000

Indirect material (3 800 + 31 300 ‒ 4 300 ) * 30 800

Insurance (62 400 ‒ 14 400 ) * 48 000

Rent (77 000 + 7 700) 84 700

Depreciation 160 000

* 609 500

* one part correct

16

10

Accounting 6 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

2.1.2 Provide a calculation to prove how the Direct Material Cost were calculated as R2 270 000. 36 000 x 60%

224 000 + 2 500 200 ‒ 140 000 ‒ (292 600 + 21 600 ) = 2 270 000

2.2 GLASS AND CO.

2.2.1 Explain why it is important to calculate the Breakeven Point.

Any acceptable, relevant answer. So that the owner/manager knows how much products must be produced in order to cover all costs.

2.2.2 Why is the production staff’s wages seen as a variable cost, but the factory cleaner’s wages is a fixed cost? Production staff is paid per unit/hour, so their labour cost would change as production levels change. The factory cleaner is paid a salary regardless of the amount of units produced. (Any acceptable answer)

2.2.3 Calculate the following:

(a)

Factory overhead per unit 114 000 = R7,60 15 000

(b)

Total Fixed Cost 114 000 + 70 400 = 184 400

6

1

2

2

2

Accounting 7 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

(c)

Variable cost per unit 142 400 ‒ 70 400 = 72 000 / 15 000 = R4,80

34 (20,00 + 14,00) + 11,20 + 4,80 = 50 one part correct

2.2.4 Calculate the Breakeven Point. 184 400 (See b)

70 ‒ 50 (See c)

= 9 220 Should Glass and Co. be satisfied with their current production of 15 000 units? Explain. Compare BEF with level of production Figure They produce 5 800 more units than what is required to break even.

TOTAL MARKS

50

5

6

Accounting 8 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

QUESTION 3 COMPANIES FIXED ASSETS, BALANCE SHEET AND NOTES

3.1 COMPANY CONCEPTS

3.1.1 Directors

3.1.2 Internal auditor

3.1.3 External auditor

3.1.4 Shareholder

3.2 FIXED ASSETS – GIANTS LTD.

3.2.1 Vehicles: One of the two vehicles was sold for R245 000 on 31 December 2017. Calculate the profit or loss made from selling this asset. Calculation: 500 000 ‒ 220 000

500 000 ‒ 280 000 (2 or nothing)_ ‒ 245 000 = 25 000 Or

Asset disposal

Vehicles 500 000 Acc depr 2 0 000 Profit on AD *25 000 Bank 245 000

3.2.2 Equipment:

(a)

Calculate the cost price of equipment purchased. 260 000

155 000 + 105 000 ‒ 200 000 = 60 000

(b)

Calculate the depreciation on equipment for the year 30 June 2018. (Do not use the 10% mentioned in no c.)

120 000 + 60 000 ‒ 155 000 = 25 000

4

5

2

4

Accounting 9 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

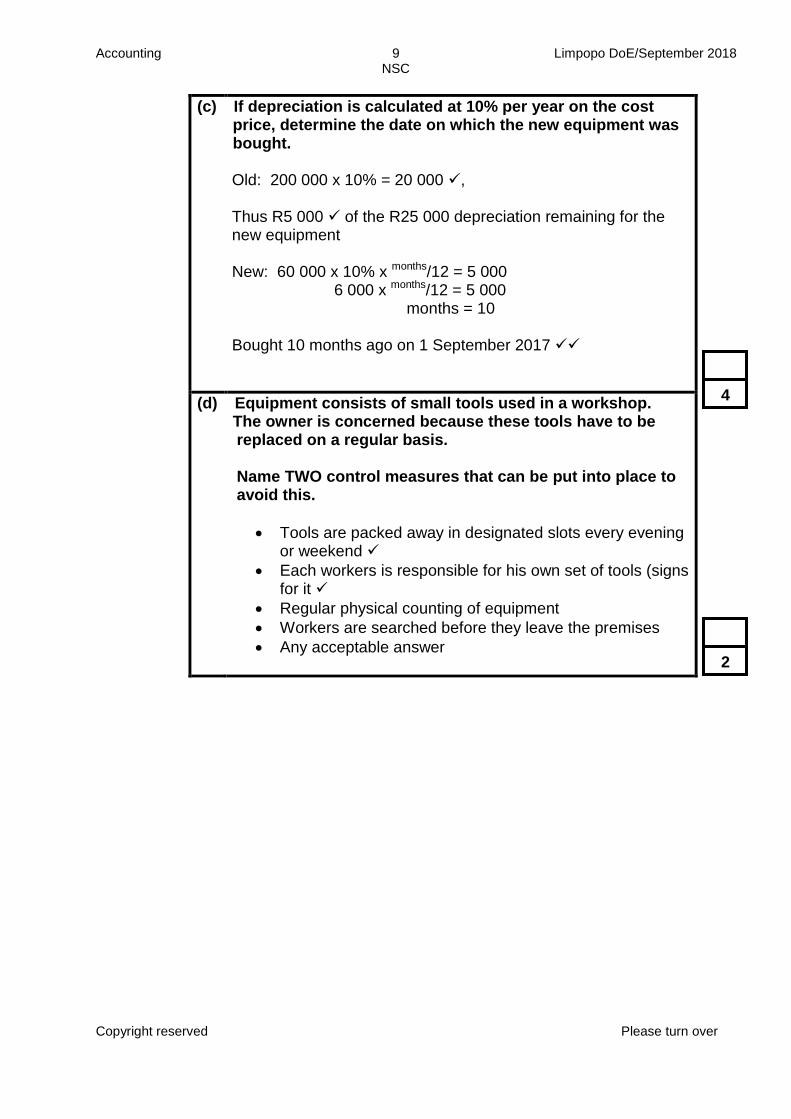

(c)

If depreciation is calculated at 10% per year on the cost price, determine the date on which the new equipment was bought. Old: 200 000 x 10% = 20 000 , Thus R5 000 of the R25 000 depreciation remaining for the new equipment New: 60 000 x 10% x months/12 = 5 000 6 000 x months/12 = 5 000 months = 10 Bought 10 months ago on 1 September 2017

(d)

Equipment consists of small tools used in a workshop. The owner is concerned because these tools have to be replaced on a regular basis.

Name TWO control measures that can be put into place to avoid this.

Tools are packed away in designated slots every evening or weekend

Each workers is responsible for his own set of tools (signs for it

Regular physical counting of equipment

Workers are searched before they leave the premises

Any acceptable answer

4

2

Accounting 10 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

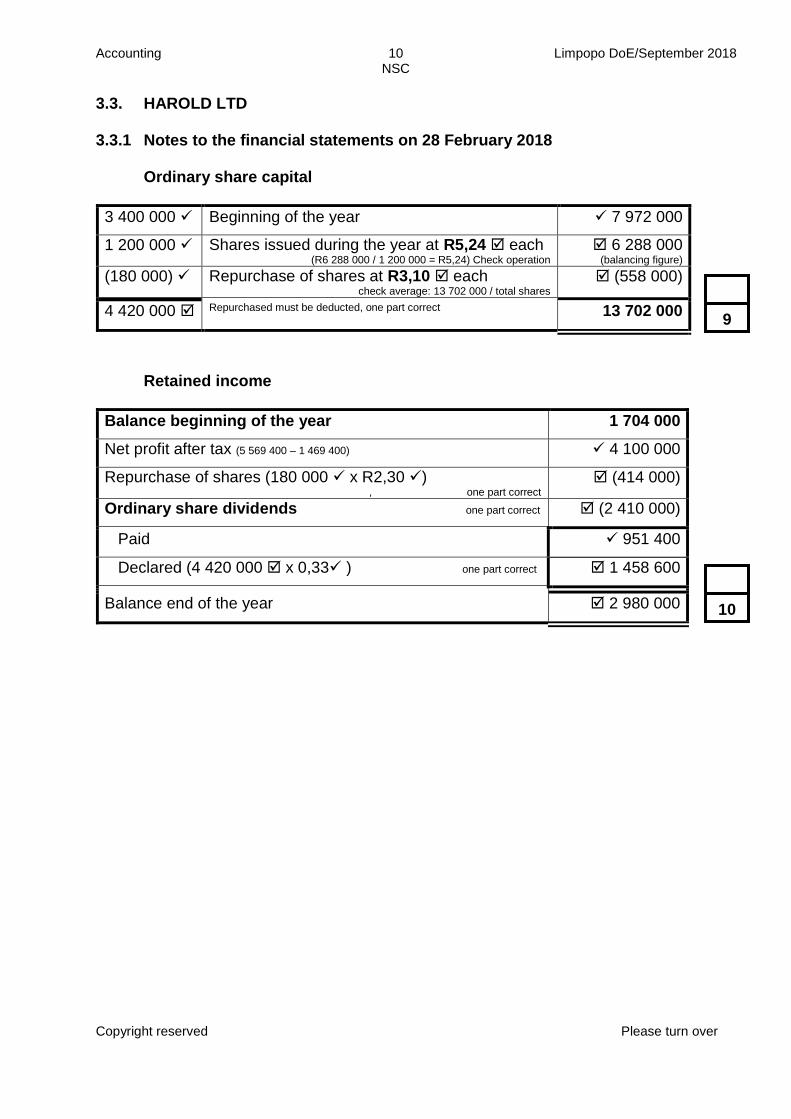

3.3. HAROLD LTD 3.3.1 Notes to the financial statements on 28 February 2018 Ordinary share capital

3 400 000 Beginning of the year 7 972 000

1 200 000 Shares issued during the year at R5,24 each (R6 288 000 / 1 200 000 = R5,24) Check operation

6 288 000 (balancing figure)

(180 000) Repurchase of shares at R3,10 each check average: 13 702 000 / total shares

(558 000)

4 420 000 Repurchased must be deducted, one part correct 13 702 000

Retained income

Balance beginning of the year 1 704 000

Net profit after tax (5 569 400 ‒ 1 469 400) 4 100 000

Repurchase of shares (180 000 x R2,30 ) , one part correct

(414 000)

Ordinary share dividends one part correct (2 410 000)

Paid 951 400

Declared (4 420 000 x 0,33 ) one part correct 1 458 600

Balance end of the year 2 980 000

9

10

Accounting 11 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

3.3.2 BALANCE SHEET ON 28 FEBRUARY 2018

ASSETS

Non-Current Assets balancing figure 1 15 014 600

Fixed assets (11 428 400 ‒ 990 000) 10 438 400

Fixed deposit: Rush Bank balancing figure 2 4 576 200

Current Assets CL x 2 5 613 400

Trading stock CL x 0,5 or CA ‒ (CL x 1,5) 1 403 350

Trade and other debtors one part correct (289 000 ‒ 1 100 + 6 400)

294 300

Cash and cash equivalents balancing figure 3 1 670 446

TOTAL ASSETS transfer from TE&L 20 628 000

EQUITY AND LIABILITIES

Ordinary shareholder’s equity check operation 16 682 000

Ordinary share capital 13 702 000

Retained income from the note 2 980 000

Non-Current Liabilities 1 139 300

Loan from director one part correct (1 346 000 + 154 000 ‒ 360 700 )

1 139 300

Current Liabilities If the candidate has the correct total CL, award full

marks for the whole section

2 806 700

Trade and other payables (495 000 + 12 000) 507 000

Shareholders for dividends transfer from Ret Inc 1 458 600

SARS (Income Tax) (1 469 400 ‒ 989 000) 480 400

Shortterm portion of loan transfer from NCL 360 700

TOTAL EQUITY AND LIABILITIES 20 628 000

4

11

2

5 8

‒ 1 for misplaced items, no maximum, award marks for the item, then ‒ 1 ‒ 1 for foreign items, max 2

TOTAL MARKS

70

30

Accounting 12 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

QUESTION 4 CASH FLOW STATEMENT, RATIO ANALYSIS 4.1 CONCEPTS

4.1.1 What does the acronym IFRS stand for and why should financial statements adhere to its stipulations? International Financial Reporting Standards Reason

So that financial statements provide the same information in the same format internationally

To indicate that the financial statements adhere to specified standards and procedures determined by international bodies.

4.1.2 Give the name or acronym for any professional body (except IFRS from 4.1.1) within the accounting sector and provide TWO reasons what the purpose of such a professional body is. Body Reasons (part marks for partial answers) SAIPA/SAICA/SAIPA, etc.

They set the qualification standards

Provides/manages internships/articles

Gives advice to accountants

They set up the code of conduct and disciplinary procedures for accounts

Take disciplinary action against accountants when necessary

Any other acceptable answer

4.1.3 Why is it important for a company to have a Code of Conduct?

By using a code of conduct, guidance is given on how to handle clients, colleagues and other partakers in the business.

It develops/organises the business’ operations by developing the participants’ behaviour etc.

It guides the ethical standards and internal control measurements that will be in place during the activities of the company

Any acceptable answer

3

5

2

Accounting 13 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

4.2.1 Note for Reconciliation of net profit before tax and cash generated from operations on 28 February 2018

Net profit before tax 943 000

Adjustments for:

Depreciation 85 000

Interest expense 228 400

Operating profit before changes in working capital one part correct

1 256 400

Changes in working capital one part correct 18 600

Increase in stock (80 000 ‒ 73 000)

(7 000)

Increase in debtors (117 500 + 8 600) ‒ (102 000 + 11 700)

(12 400)

Decrease in creditors (165 000 - 127 000)

38 000

Cash generated from operating activities one part correct 1 275 000

4.2.2

Cash flow statement for the year ended 28 February 2018.

Cash flow from operating activities * 174 700

Cash generated from operating activities * 1 275 000

Dividends paid (582 400)

Interest paid (11 300 + 228 000 ‒ 9 800 ) #* (229 500)

Tax paid (24 000 + 283 000 ‒ 18 600 ) #* (288 400)

Cash flow from investing activities (1 100 000)

Purchase of fixed assets (1 150 000)

Earnings from non-current assets sold 50 000

Cash flow from financing activities * 802 000

Repayment of loan (98 000

Proceeds from shares issued

900 000)

Net change in cash and cash equivalents * (123 300)

Cash and cash equivalents beginning of the year 131 500

Cash and cash equivalents end of the year * 8 200

* One part correct, correct use of brackets to earn the mark on final answer

# Signs may be reversed; apply consistently, mark one line only to benefit candidate If a working is shown as a final answer, award working mark only if brackets correctly applied for this item. If workings not shown but figure is correct without brackets, award marks to cover workings and penalise on answer. If item is incorrectly placed, award no marks for details or figures.

12 6

11

Accounting 14 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

4.2.3 Calculate the following:

(a)

Price of new shares issued on 1 March 2017 900 000 = R11,25 80 000

(b)

Dividends per share (DPS) on 28 February 2018 314 000+ 284 400 x 100 = 88 c answer must be in c, 680 000 one part correct

(c)

Return on shareholder’s equity (ROSHE) on 28 February 2018 660 000 x 100 ½ (6 211 800 + 5 160 000 ) = 660 000__ x 100 5 685 900 = 11,61% must be a % sign, one part correct

4.2.4 Explain whether Kefilwe, a shareholder in Vericon Ltd, should be satisfied with the return on his investment? Quote TWO financial indicators with figures to support your answer. Explanation The percentage received in investing in the company is more than the interest on fixed deposit ratio named trend and figure ratio named trend and figure DPS improved, was 75c per share, now 88c per share ROSHE improved, was 9,3%, now 11,61% EPS improved, was 125c per share, now 150c per share

2

4

5

5

Accounting 15 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

4.2.5 Kefilwe is interested in purchasing more shares in Vericon Ltd. He contacts you and seeks advice. Do you think it is a wise decision? Explain your answer and quote two ratios/figures (other than those mentioned in 4.2.4.) Explanation: Must compare NAV and market price Ratio figure Ratio figure NAV increased from R8,60 to R9,14 Market value decreased from R21,50 to R20, it is the right time to buy OR No Ratio figure Ratio figure NAV is R9,14 but is sold for R20 Market value is decreasing, R21,50 to R20. Wait for it to decrease more

4.2.6 Vericon Ltd. wants to expand their business and buy a warehouse situated close to their current property. This warehouse will cost them R1,8 million. According to your opinion, what is the best way to finance this transaction? Quote TWO financial indicators with figures to motivate your answer. Loan Explanation figure Explanation figure Debt/equity including new loan: 807 000 + 1 800 000 : 6 211 800 0,42 : 1 ROTCE increased from 15,3% to 19,6%. Current loan is 15% whilst earning 19,6%. Dividends are already 88c per share, more shares will lead to a decrease in DPS / Market value already decreasing.

TOTAL MARKS

65

5

5

Accounting 16 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

QUESTION 5 VAT & INVENTORY VALUATIONS

5.1. VAT CONCEPTS

5.1.1 Exempt

5.1.2 Zero

5.1.3 Exempt

5.2 WINSTON TRADERS

5.2.1 Calculate the amount that would be entered next to Debtors Control on the credit side of the VAT Output account. Total sales = 120 000 x 25/75 = 40 000 x 15% = 6 000

5.2.2 Calculate the VAT amount owed to SARS on 28 February 2018 after the VAT Input and VAT Output accounts were closed off. (18 000 + 6 000 see 5.2.1) 24 000 ‒ (276 + 350) + 150 ‒ (8 600 + 6 000) = 8 924

5.2.3 In which section of the Balance Sheet will you record the amount calculated in 5.2.3? Trade and other payables

3

3

5

1

Accounting 17 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

5.3 INVENTORY VALUATION

5.3.1 Explain to the owner the difference between the First In First Out method and the Weighted average method. Also provide ONE reason why the weighted average method would be better suited for his product. Difference: With FIFO items are priced are kept separate With weighted average an average price is calculated with each purpose Reason: The crates are small items which does not differ greatly in price

5.3.2 Calculate the value of closing stock by using the FIFO method. 10 units x R0 240 units x R14,60 = R3 504 30 units x R14,50 = R 435 280 R3 939 one part correct

5.3.3 Calculate the value of closing stock by using the weighted average method. 5 880 + (8 742 ‒ 846) + (4 350 + 3 504) 370 + (620 ‒ 60) + (300 + 240) + 10 = 21 630 1 480 = 14,61 x 280 = R4 090,80

5.3.4 The owner suspects that some of the stock was stolen, but there is no proof.

(a)

Calculate the number of units that cannot be accounted for. (370 + 1 110 ‒ 1 190)

290 ‒ 280 = 10

3

10

4

4

Accounting 18 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

(b)

Provide any TWO internal control measures that can be implemented in order to prevent this loss in the future. Part marks for incomplete answers

Check all stock receipts against the invoice confirming the transaction

Limit the access to the stock room

The person collecting the stock from the storeroom should not be the person who handles the sale

Any acceptable internal control measure of stock

5.3.5 The owner wants to charge an additional fee of R4,00 per crate for delivering the crates to his customers. Do you agree with his decision? Motivate your answer by providing ONE point. Comparison of the competitor’s price and the new price after increase with figures

R4,00 per crate would increase his sales price to R22, which would then be higher that his competitor’s price. (part marks for an incomplete answer)

TOTAL MARKS

40

4

3

Accounting 19 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

QUESTION 6 PROBLEM SOLVING AND BUDGET 6.1 PROBLEM SOLVING

6.1.1 Franco Traders increased both the salaries of directors and other employees in March. Do you think that the increases were reasonable? Explain your answer and provide supporting figures. Explanation: Compare the increase of workers and directors with the inflation rate The workers will receive an increase of R420 per worker/R8 400 for 20 workers (4% increase) The directors will receive an increase of R33 000 per director/R66 000 for 2 directors (30% increase)

6.1.2 The worker’s union representative has scheduled a meeting with the directors and management staff. They want to discuss the given figures with the directors and management staff. They are grateful for certain aspects but others raise concern. Apart from salaries, provide TWO points which they could see as positive points and TWO points of concern. Quote figures in all of your explanations. Positive:

Improved security (R2 000 increased to R25 000)

Training for workers (R6 000 increased to R26 000) Negative:

Transport costs were cut from R12 000 to R7 000

Training is in addition to normal week hours, and over weekends, without payment (any one reason)

8

5

Accounting 20 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

6.2 BUDGET

6.2.1 Explain the importance of comparing the actual figures to the budgeted figures in the cash budget. To determine of the items/costs were managed well and within the set limits (Any acceptable answer)

6.2.2 Calculate the values marked (A) ‒ (F).

Calculati ns

A

1 080 000 x 95% = 1 026 000

B

1 800 000 x 100/160 = 1 125 000

C

360 000 / 2 = 180 000

D

51 200

E

675 400 + 51 200 (see D) = 624 200

F

49 680 x 100/115 = 43 200

8

1

Accounting 21 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

6.2.3 Refer to the figures for “Cash received from debtors”. Are the debtors adhering to the credit terms of the business? Provide figures to support your answer. . Explanation: Comparison of budgeted e and actual Figures They should have paid R864 000 and only paid R624 000

6.2.4 The workers are receiving a salary increase in November 2018. Considering this, as well as the fact that no new workers were employed during July and August 2018, what could possibly be a reason for the change in each of the actual figures for those two months?

Reason

July

Workers worked overtime

August

Less workers came to work / Workers were on a strike

(Any acceptable answers for both scenarios)

6.2.5 The owner feels that the business pays less money by renting equipment than purchasing the equipment. Do you agree with her opinion? Provide TWO points to support your answer. Yes/No Explanation Yes

Only hires equipment when necessary

Does not have to pay maintenance on equipment

Any other reasonable answer No

By purchasing their own equipment they will save money as the equipment will last longer than what the repayment period

The equipment can be rented out to earn an additional income (if it is not in use in the business at that time)

Any other reasonable answer

3

2

5

Accounting 22 Limpopo DoE/September 2018 NSC

Copyright reserved Please turn over

6.2.6 The business still faces a cash flow problem in August, even though a loan was obtained in July and the receipts from debtors improved. Excluding these two items, identify TWO other items, (other than the renting of equipment in 6.2.5), with figures, that needs attention. Also provide advice how these items can be managed. Item Figure Advice

Item Figure Advice

Creditors

960 000 or (b) 1 125 000 Or 1 200 000

Buy less on credit, attempt more cash sales in order to qualify for a cash discount.

Drawings

150 000 or 210 000 or 168 000

Urge owner to decrease drawings so that the business can recover the cash flow

Salaries and wages

144 000 to 180 000 or 144 000 to 108 000

Pay workers a fixed salary; employ workers for a fixed term.

6.2.7 The owner bought the vehicle from the business for her son. The usual driver and the finance officer were unhappy with this. Prove each person’s point by explaining ONE reason for each.

Concern

Driver

He was supposed to have first option to buy the vehicle and now he can’t go against the owner of the business.

Finance officer

The business received R60 000 less (R180 000 ‒ R120 000) than what they would have received if the vehicle was sold to the driver.

TOTAL MARKS

40

TOTAL: 300 marks

6

2