gregory ford | dec. 2013 internal revenue service 2013 fsa training conference for financial aid...

TRANSCRIPT

Gregory Ford | Dec. 2013

Internal Revenue Service

2013 FSA Training Conference for Financial Aid Professionals

What You Need to Know About Education Tax Credits and Deductions

Session 34

Partnership is Key

• IRS and DOED are working together • FAFSA DRT • Reaching and serving low income and underserved • Communication and Outreach

• You are a trusted resource for the students and parents you serve

• Together we can reach and help more of them

2

3

The Tax Law is Complex

• Because of complexity, it is difficult for students to self-identify

• Result: each year money is left on the table

• You can help ensure all those who qualify receive the federal tax credits and deductions they deserve and need to pay for higher education

4

IRS Education Credits & Deductions

• A tax credit reduces the amount of income tax someone may have to pay on a dollar-for-dollar basis for qualified education expenses.– The American Opportunity Tax Credit– The Lifetime Learning Credit

• A deduction reduces the amount of income that is subject to tax, which generally reduces the amount of tax someone may have to pay. – The tuition and fees deduction

• There are criteria common to all three benefits

5

6

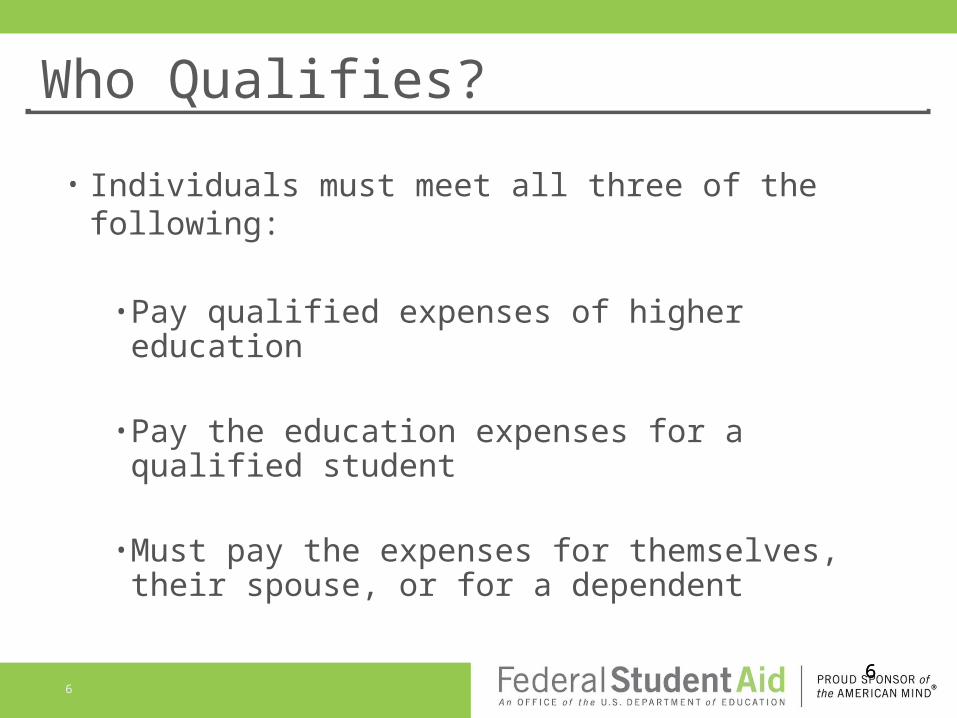

Who Qualifies?

• Individuals must meet all three of the following:

• Pay qualified expenses of higher education

• Pay the education expenses for a qualified student

• Must pay the expenses for themselves, their spouse, or for a dependent

66

7

Who Does Not Qualify?

• Individuals cannot claim the credit if any of the following are true:

• Files married filing separately

• Is listed as a dependent on another person’s return

• They or their spouse were a nonresident alien for any part of the year and did not choose to be treated as a resident alien

77

8

Funds that Qualify

• Individuals do not have to reduce the amount of expenses paid by the following:

• Payments for services, such as wages• A loan• A gift• An Inheritance, or• A withdrawal from student’s personal savings• Taxable scholarships or fellowships

88

9

Expenses that Do Not Qualify• Insurance

• Medical expenses (including student health fees)

• Room and Board

• Transportation

• Personal, Living, or Family Expenses

• Sports, games, hobbies, and noncredit courses unless included in course of instruction

99

10

No Double Credits

• One expense – One Student – One Education Credit

• If the funding for the expense is tax free – You can’t claim the credit

1010

AOTC Enhances the “Hope Credit”

• Added expenses for books, supplies and equipment need for a course of study to the list of qualifying expenses

• Allows the credit to be claimed for four post-secondary education years, instead of two

• The credit is available to individuals with a higher adjusted gross income

• Starts to phase out at $80,000 for individuals or $160,000 for married couples filing a joint return

• Completely phases out at $90,000 for individuals or $180,000 for married couples filing a joint return

• 40% of the credit is refundable, up to $1,000

11

AOTC – Who Qualifies?

• In addition to basic requirements, student must:

• Be pursuing an undergraduate degree or other recognized education credential

• Attend at least half time for one academic period starting during 2012

• Not have felony drug conviction on record

12

Overview of Lifetime Learning Credit

• Up to $2,000 per return

• Non-refundable

• Limit on MAGI• $62,000 single, head of household, or qualifying widow or widower• $124,000 married filing jointly

• Available for all years of postsecondary education and for courses taken to acquire or improve job skills

• Available for one or more courses

• No restriction for felony drug conviction

13

Overview of Tuition and Fees Deduction

• Maximum benefit—reduce your taxable income by up to $4,000

• Limit on MAGI• $80,000 single, head of household, or qualifying widow or

widower• $160,000 married filing jointly

• Student must:• Be enrolled in postsecondary education• Have high school diploma or GED• Take one or more courses

• No restriction for felony drug conviction

• No restriction on number of years

14

Which Credit or Benefit Is More Advantageous?

15

Compare the Benefits – Maximum

AOTCLifetime Learning

CreditTuition and Fee

Deduction

Up to $2,500 credit per student

40% of credit up to $1,000 may be

refundable

Up to $2,000 credit per tax return – Not Refundable

Deduct up to $4,000 from

taxable income – Not Refundable

16

Compare Qualifying Expense Besides Tuition and Fees

AOTCLifetime

Learning CreditTuition and Fee

Deduction

Course-related books, supplies, and equipment

None None

17

Compare Who Must Pay the Qualified Expenses?

AOTCLifetime

Learning CreditTuition and Fee

Deduction

You or your spouse

Student

Third partyˆ

You or your spouse

Student

Third partyˆ

You or your spouse

18

Compare the Education that Qualifies

AOTCLifetime

Learning CreditTuition and Fee

Deduction

• Four years of postsecondary education

• Undergraduate• Graduate• Courses to

acquire or improve job skills

• Undergraduate• Graduate

19

Compare Income Range and Phase out

AOTCLifetime Learning

CreditTuition and Fee

Deduction

• $80,000 to $90,000 for Single or Head Of Household

• $160,000 to $180,000 for Married Filing Jointly

• $52,000 to $62,000 for Single or Head Of Household

• $104,000 to $124,000 for Married Filing Jointly

• $65,000 to $80,000 for Single or Head Of Household

• $130,000 to $160,000 for Married Filing Jointly

20

Claiming the Tax Benefit

AOTCLifetime

Learning CreditTuition and Fee

Deduction

• Complete Form 8863 Parts I, III, and IV

• Complete Form 8863 Parts II and IV

• Complete Form 4917

21

Did You Get All That?

Not to worry – we have tools for you and the students and parents you help

22

Tools to Help Promote Education Benefits

http://www.eitc.irs.gov/Other-Refundable-Credits/main

23

24

Interactive Tax Assistant

25

Flyer and YouTube

26

Students Can Find Education Benefit Information at One Convenient Location on IRS.gov

27

You Can Help

• Use the tools on the Refundable Credit Toolkit

• Subscribe to the IRS Outreach Corner and place articles in your newsletters or LISTSERV

• Use our Social Media products

• Link to products and tools from your websites

28

Questions?

30