group results presentation - tiger brands procurement savings of r211 million ... r12.8bn 13%...

TRANSCRIPT

Group Results Presentation

for the year ended 30 September 2016

2Group Results Presentation for the year ended 30 September 2016

Index

Overview

Financial & operating performance

Strategic review

3Group Results Presentation for the year ended 30 September 2016

Disclaimer

Forward-looking statement

This document contains forward looking statements that, unless otherwise indicated, reflect the company’s expectations as at

23 November 2016. Actual results may differ materially from the company’s expectations if known and unknown risks or

uncertainties affect the business, or if estimates or assumptions prove to be inaccurate. The company cannot guarantee that any

forward looking statement will materialise and, accordingly, readers are cautioned not to place undue reliance on these forward

looking statements. The company disclaims any intention and assumes no obligation to update or revise any forward looking

statement even if new information becomes available as a result of future events or for any other reason, save as required to do

so by legislation and/or regulation.

Lawrence Mac DougallChief Executive Officer

Please replace this pic

5Group Results Presentation for the year ended 30 September 2016

A year characterised by a volatile external environment

Including socio-political turbulence

-18

-15

-12

-9

-6

-3

0

Consumer confidence

80

100

120

140

160

180

Maize price index

12

13

14

15

16

17

18

US$/ZAR

Weak consumer confidence Abnormal raw material inflation Unpredictable forex markets

13.84

13.78

13.63

13.59

13.36

13.42

13.30

13.27

13.41

13.32

13.08

13.11

13.25

13.26

13.48

13.44

13.59

13.60

13.66

13.56

13.85

13.81

13.79

13.85

13.94

13.93

14.19

14.32

14.28

14.19

14.29

14.40

14.37

14.27

14.22

14.03

13.93

14.08

13.99

14.16

14.27

14.34

14.42

14.43

14.39

14.39

14.31

14.56

14.61

14.56

15.20

16.02

15.28

14.99

15.04

15.21

15.06

15.05

15.21

15.19

15.29

15.29

15.27

15.29

15.56

15.50

15.50

15.64

15.62

15.81

15.95

16.17

16.67

16.57

16.43

16.46

16.78

16.75

16.73

16.94

16.62

16.50

16.49

16.39

16.38

16.21

15.90

16.00

16.17

16.21

15.83

15.99

16.14

16.05

15.85

15.71

15.86

15.78

15.76

15.50

15.31

15.42

15.18

15.24

15.68

15.61

16.11

15.78

15.66

15.58

15.55

15.39

15.30

15.44

15.25

15.40

15.24

15.56

15.94

16.13

15.19

15.27

15.16

15.20

15.33

15.53

15.53

15.57

15.40

14.83

14.71

14.83

14.73

15.00

15.21

15.23

14.93

14.71

14.68

14.57

14.51

14.61

14.48

14.28

14.26

14.28

14.40

14.50

14.43

14.53

14.26

14.18

14.29

14.61

14.90

14.97

14.94

15.15

15.10

15.03

15.02

15.30

15.65

15.56

15.74

15.90

15.71

15.77

15.67

15.70

15.63

15.66

15.84

15.73

15.58

15.59

15.31

14.91

14.90

14.71

14.83

15.10

15.06

15.33

15.24

15.50

15.19

14.78

14.73

14.67

14.49

14.91

15.52

15.23

14.81

14.65

14.56

14.54

14.79

14.86

14.72

14.59

14.44

14.34

14.46

14.21

14.34

14.29

14.39

14.27

14.18

14.32

14.39

14.41

14.28

14.24

13.86

13.90

13.96

13.99

13.78

13.78

13.63

13.43

13.30

13.26

13.44

13.26

13.34

13.44

13.33

13.47

13.56

13.47

14.14

14.25

14.06

14.41

14.48

14.71

14.67

14.47

14.38

14.05

14.05

13.96

14.37

14.42

14.44

14.30

14.19

14.30

14.02

13.86

13.72

13.59

13.68

13.66

13.53

13.66

13.87

13.75

13.65

13.67

13.75

13.90

13.83

13.77

14.35

14.27

Source: Bloomberg, Factset

Oct 15 Nov 16 Oct 15 Nov 16Dec 15 Sep 16Mar 16 Jun 16

6Group Results Presentation for the year ended 30 September 2016

Solid results from continuing operations

Group performance*

Group volumes up

1%

Group turnover up

11%

to R31.7 billion

Group operating income up

5%

to R4.2 billion

Total dividends up

12%

to 1 065 cents

* From continuing operations | Group operating income from continuing operations before abnormal items, impairments & IFRS 2 charges

1 786

2 127

1 600

1 700

1 800

1 900

2 000

2 100

2 200

FY 15 FY 16

Total HEPS up 19%Cents

7Group Results Presentation for the year ended 30 September 2016

Strong overall performance in tough environment

Domestic

o Volumes up 2%

o Power brands maintain leading positions

o Continued cost savings & investments

o Disciplined price/volume management

International

(including Exports)

o Deciduous Fruit (LAF) delivers exceptional earnings growth

o Seventh consecutive year of growth from Central Africa

o Exports & West Africa impacted by macro-economic challenges

8Group Results Presentation for the year ended 30 September 2016

Sustained market leadership in power brands

#1 #1 #1 #1 #1

#1 #1 #1 #1 #2

#1 #1 #2 #1 #1Source: Nielsen package share, 12 month moving average to September 2016

TOP

9Group Results Presentation for the year ended 30 September 2016

Building on operational excellence

Moving to a high performance culture

Operational

excellence

o Excellent in-store execution

o On-shelf availability at 96% up from 89%

o Achieved further savings of R380 million, including

o Procurement savings of R211 million

o Innovation rate improves to 4.5% of turnover from 3.5%

People & culture

o Improved engagement

o Achieved Top Employer status

Social

responsibility

o Food programmes feed 100,000 children daily

o Sustainable socio-economic development gaining momentum

Financial & operating

performanceNoel DoyleChief Financial Officer

11Group Results Presentation for the year ended 30 September 2016

Credible operating performance*

Boosted by forex gains & associate growth but offset by higher tax rate

* From continuing operations | Effective tax rate before abnormals, impairments & associate income

Rm 2016 2015 % change

Turnover 31 698 28 660 11%

Cost of sales (21 499) (18 981) 13%

Operating income before IFRS 2 charges 4 243 4 055 5%

IFRS 2 charges (89) (29) 207%

Operating income before impairments & abnormal items 4 154 4 026 3%

Impairments & abnormals (324) (339) 4%

Net finance costs (297) (224) (33%)

Foreign exchange gains 121 21 476%

Income from associated companies 861 603 43%

Profit before taxation 4 515 4 087 10%

Taxation (1 221) (977) (25%)

Profit for the year 3 294 3 110 6%

Operating margin before IFRS 2 charges 13.4% 14.1% (0.7%)

Effective tax rate 30.9% 25.6%

EPS (cents per share) 2 007 1 930 4%

HEPS (cents per share) 2 130 2 091 2%

12Group Results Presentation for the year ended 30 September 2016

Income from associates up 43%

Associates contribution driven by once-off items

* Excludes capital profits of R69m in Carozzi, R47m in Oceana & R1m in National Foods Holdings

303234 207

449

402

309

29

29

33

80

79

54

FY16 FY16 excl. capital profits* FY15

Empresas Carozzi Oceana Group UAC of Nigeria National Food Holdings

Total income from

associates (Rm)603861 744

13Group Results Presentation for the year ended 30 September 2016

Cost awareness – a key contributor to performance

Achieved continuous improvement savings of R380 million

R91m

R36m

R42m

R211m

Manufacturing efficiencies

IT platform

Financial shared service centre

Procurement savings

245

481

692

0

100

200

300

400

500

600

700

800

FY 14 FY 15 FY 16

3 year cumulative procurement savings

Total

savings

R380m

Rm

14Group Results Presentation for the year ended 30 September 2016

Continue to invest in growth, efficiency & flexibility

983

882945

679 662

559

1.45 1.33

1.69

0

200

400

600

800

1 000

1 200

FY 14 FY 15 FY 16

Rm

Capex (Rm) Depreciation (Rm)

Capex / Depreciation

R376m

R639m

Capex & acquisition spend for FY16 (Rm)

Expansion Replacement

Capex up

7% to

R945m

15Group Results Presentation for the year ended 30 September 2016

Cash flow improves

Debt reduction impacted by TBCG disposal

Rm 2016 2015

Cash operating profit 4 837 4 396

Working capital changes (604) (812)

Cash generated from operations 4 233 3 584

Finance costs net of dividends received 109 (71)

Taxation paid (1 107) (1 159)

Dividends paid (1 661) (1 643)

Capex & acquisition (1 015) (882)

Exercise of share options held in BMT & other 59 397

Disposal of TBCG debt 1 142 -

Investments - (525)

Opening Balance – Net cash/(debt) (3 788) (3 489)

Closing Balance – Net cash/(debt) (2 028) (3 788)

16Group Results Presentation for the year ended 30 September 2016

Balance sheet strength provides capacity for investment

in future growth

* From continuing operations

2016* 2015

Cash generated from operations (Rm) 4 233 3 584

Net (debt) / cash (Rm) (2 028) (3 788)

Net debt / equity (%) 13 28

Net debt / EBITDA 0.4x 0.8x

RONA (%) 31 26

Net interest cover (times) 14 18*

17Group Results Presentation for the year ended 30 September 2016

Group turnover up 11% to R32 billion

Group volumes up 1%, domestic volumes up 2%

FY 2015 FY 2016

R28.7bn

8%

inflationR31.7bn

1%

volume

2%

forex

Total

growth

Price

inflation

Total

volumeForex

Domestic operations 11% 9% 2% -

International (including Exports) 7% 2% (5%) 10%

Total continuing operations 11% 8% 1% 2%

18Group Results Presentation for the year ended 30 September 2016

Group achieves double-digit turnover growth

Strong performances from Groceries, Beverages & Home Care

Grains

Consumer

Brands Food HPCB

International

(incl. Exports) Group*

Volume - ▲ 3% ▲ 6% ▼ 5% ▲ 1%

TurnoverR12.8bn

▲ 13%

R11.0bn

▲ 9%

R2.4bn

▲ 13%

R5.4bn

▲ 7%

R31.7bn

▲ 11%

Operating

income**

R2.0bn

▼ 3%

R1.2bn

▲ 9%

R0.5bn

▲ 20%

R0.5bn

▲ 19%

R4.2bn

▲ 5%

Operating

margin**▼15.6% 10.8% ▲ 21.9% ▲10.2% ▼13.4%

* From continuing operations ** Before abnormal items, impairments & IFRS 2 charges

19Group Results Presentation for the year ended 30 September 2016

Grains

o Solid performance from core business (Millbake)

• Offset by Maize & Sorghum

o Albany volumes grow despite challenges in Western Cape

• Leading position in bread maintained

• Western Cape bakery online end FY17

o Other Grains driven by Jungle & Fatti’s & Moni’s

• Strong volume growth in Fatti’s & Moni’s

• Launch of instant noodles

• Single-serving Jungle cups

11 37512 845

2 061 2 002

0

4 000

8 000

12 000

16 000

FY 15 FY 16

Resilient in tough environment – margin distorted by abnormal inflation

Turnover Operating income

Rm

Raw material costs

▲ 22%

Marketing investment

▲ 13%

20Group Results Presentation for the year ended 30 September 2016

Groceries

o Strong growth in volumes

o Revenue up 10%

o Operating income up 13%

o Input costs impacted by drought and currency volatility

• Appropriate pricing strategy implemented

o Improved manufacturing performance

o KOO retains South Africa’s favourite brand status

• Ahead of leading international brands

4 2654 701

411 466

0

1 000

2 000

3 000

4 000

5 000

FY 15 FY 16

Benefits from successful price/volume management in H2

Rm

Turnover Operating income

21Group Results Presentation for the year ended 30 September 2016

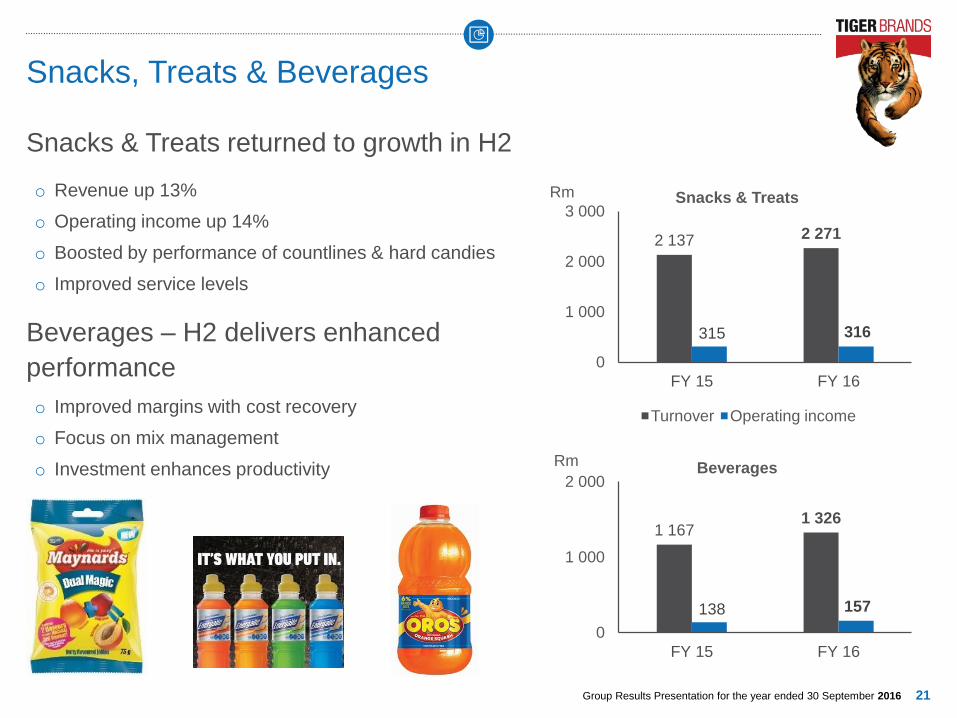

Snacks, Treats & Beverages

o Revenue up 13%

o Operating income up 14%

o Boosted by performance of countlines & hard candies

o Improved service levels

Beverages – H2 delivers enhanced

performance

o Improved margins with cost recovery

o Focus on mix management

o Investment enhances productivity

2 137 2 271

315 316

0

1 000

2 000

3 000

FY 15 FY 16

Snacks & Treats

Snacks & Treats returned to growth in H2

Rm

Turnover Operating income

1 1671 326

138 157

0

1 000

2 000

FY 15 FY 16

BeveragesRm

22Group Results Presentation for the year ended 30 September 2016

Home, Personal & Baby Care (HPCB)

o Outstanding performance from Home Care

o Personal Care delivers growth in competitive environment

o Baby Care impacted by consumer down-trading

o Turnover up 13%

o Operating income up 20%

o Margins improve to 21.9%

o Performance underpinned by

• Innovation

• Operational efficiencies

• In-store execution

2 1472 437

444 534

0

1 000

2 000

3 000

FY 15 FY 16

Exceptional performance repeated

Rm

Turnover Operating income

23Group Results Presentation for the year ended 30 September 2016

International (including Exports)

o Deciduous Fruit (LAF) benefits from favourable

exchange rates, improved yields & cost containment

o Central Africa delivers 7th year of consecutive growth

• Volumes driven by chocolate bars & spreads

• Innovation up to 7.2% of turnover

o East Africa driven by recovery at Haco

• Announced disposal of EATBI

o Exports impacted by macro-economic challenges

• Demand for brands remains robust

o West Africa impacted by delayed recovery in cost push

driven by currency devaluation

• Power shortages

• Value Added Tax

5 0295 386

462 547

0

2 000

4 000

6 000

FY 15 FY 16

Strong growth with mixed performances

Rm

Turnover Operating income

24Group Results Presentation for the year ended 30 September 2016

Outlook

o Difficult trading environment to persist

o Inflation to remain high

o Forex & commodity prices remain volatile

Focus areas

o Leverage power brands to grow market share

o Optimise margin

o Accretive innovation & targeted investment

o Aggressive focus on cost savings

o Drive high performance culture

Strategic reviewLawrence Mac DougallChief Executive Officer

26Group Results Presentation for the year ended 30 September 2016

Strategic review in progress

Developing a strategy for sustainable profitable growth

Portfolio growth

& strategy

o Rejuvenate domestic

operations to profitable

growth

o International strategy

accretive to domestic

performance

o Build a capable & cost

conscious culture with

the capacity to grow

o Winning through a high

performance culture

=

Cost & investment

strategy

Operating model &

organisational design

Growth

CapabilityCost

27Group Results Presentation for the year ended 30 September 2016

Leadership

Board and Executive Committee appointments

o Khotso Mokhele to be appointed chairman at upcoming AGM

o Kevin Hedderwick & Emma Mashilwane join the board as non-executive directors

o Mary-Jane Morifi joins as Corporate Affairs Executive in December

o Neil Brimacombe resigned as Business Executive effective 31 January 2017

Investor RelationsNikki Catrakilis-WagnerGroup Investor Relations Executive

T: +27 11 840 4841

Appendices

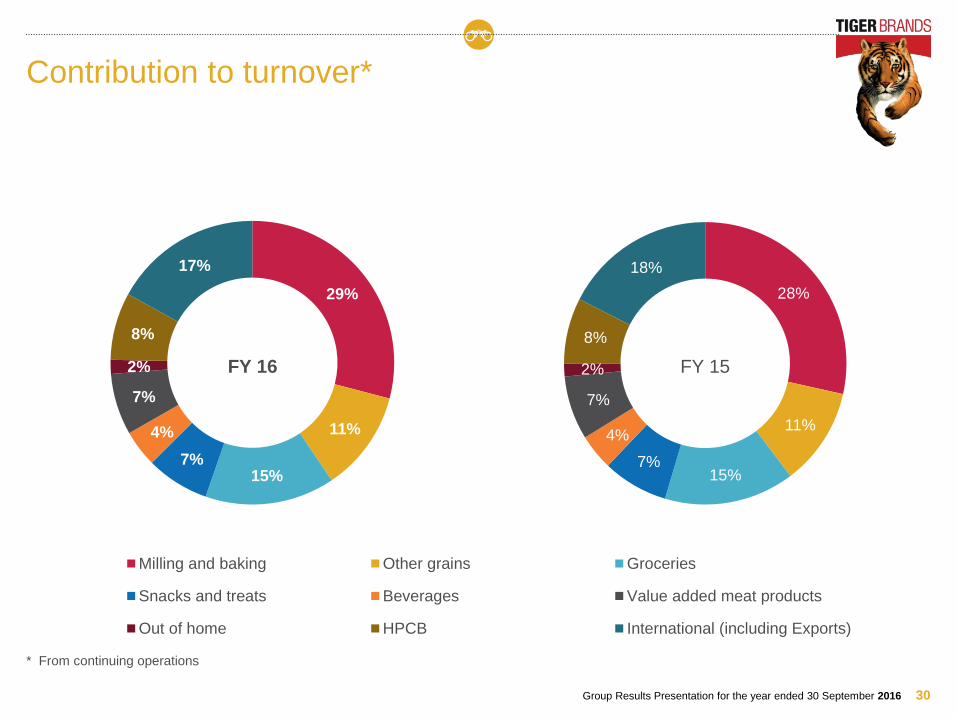

30Group Results Presentation for the year ended 30 September 2016

29%

11%

15%7%

4%

7%

2%

8%

17%

Milling and baking Other grains Groceries

Snacks and treats Beverages Value added meat products

Out of home HPCB International (including Exports)

Contribution to turnover*

* From continuing operations

FY 16 FY 15

28%

11%

15%7%

4%

7%

2%

8%

18%

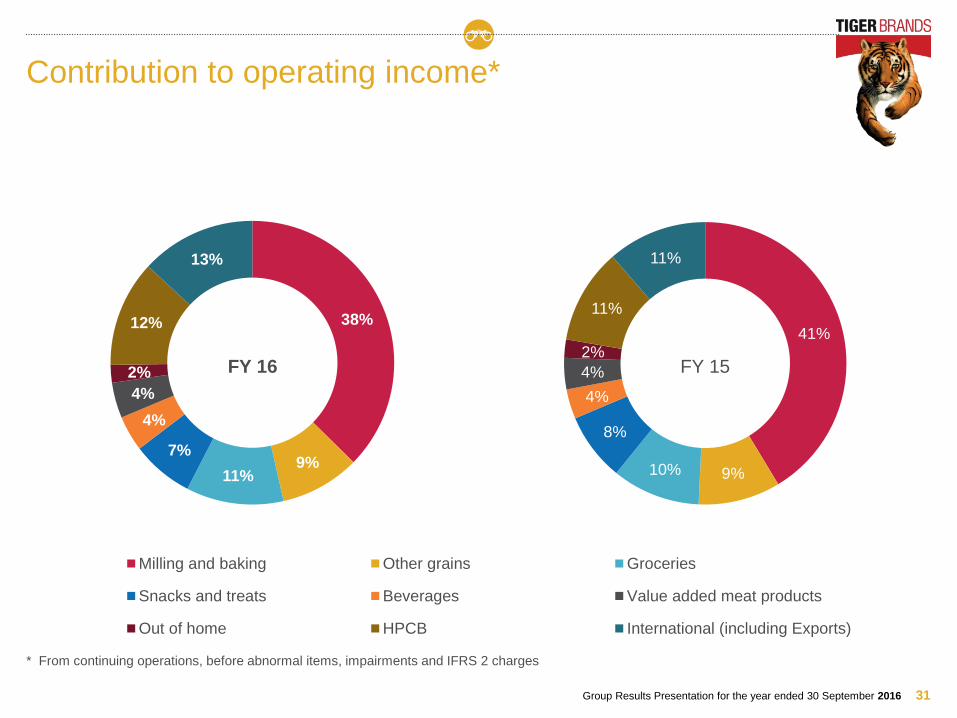

31Group Results Presentation for the year ended 30 September 2016

38%

9%11%

7%

4%

4%

2%

12%

13%

Milling and baking Other grains Groceries

Snacks and treats Beverages Value added meat products

Out of home HPCB International (including Exports)

Contribution to operating income*

* From continuing operations, before abnormal items, impairments and IFRS 2 charges

FY 16 FY 15

41%

9%10%

8%

4%

4%

2%

11%

11%

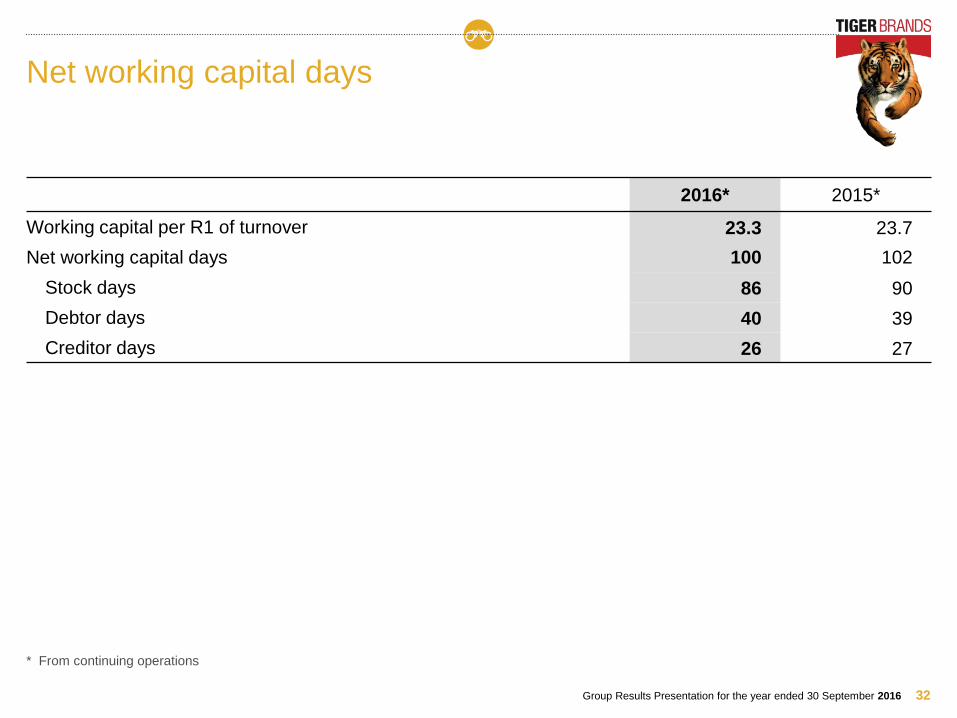

32Group Results Presentation for the year ended 30 September 2016

Net working capital days

2016* 2015*

Working capital per R1 of turnover 23.3 23.7

Net working capital days 100 102

Stock days 86 90

Debtor days 40 39

Creditor days 26 27

* From continuing operations

Investor RelationsNikki Catrakilis-WagnerGroup Investor Relations Executive

T: +27 11 840 4841