growing the bank with mobile - tennessee bankers … handoutgrowing the bank...growing the bank with...

TRANSCRIPT

1 | © 2014 Jack Henry & Associates, Inc.®

Growing the Bank

with Mobile

The Bottom Line on Risks & Rewards

Lee Wetherington, AAPDirector of Strategic InsightJack Henry & Associates, Inc.®

2 | © 2014 Jack Henry & Associates, Inc.®

Lee WetheringtonDirector of Strategic Insight

• Develops actionable insight and strategy

for the financial services industry

• Delivers keynotes nationwide

• Technology Faculty Chair and guest

lecturer for graduate banking schools

• Authors articles for industry trades

• Degrees in Economics and English

from Duke University

• Accredited ACH Professional (AAP)

Presenter

@leewetherington

4 | © 2014 Jack Henry & Associates, Inc.®

Mobile Banking Today: Fed Report

• Mobile phones are in widespread use.

– 87% of the U.S. adult population has a mobile phone,

consistent with 2013.

– 71% of mobile phones are smartphones (Internet-

enabled), up from 61% in 2013.

• 39% of all mobile phone owners with a bank

account used mobile banking in 2014

– Up from 33% in 2013 and 29% in 2012.

• 52% of smartphone owners with a bank account

used mobile banking in 2014

– Up only one percentage point from 51% in 2013

SOURCE: Federal Reserve’s 2015 Consumers and Mobile Financial Services Report

5 | © 2014 Jack Henry & Associates, Inc.®

Mobile Banking Today: Fed Report, 2

• 11% of mobile phone users with bank accounts

plan to use mobile banking within a year

– Down from 12% a year earlier

• Mobile banking usage

– 94% check account balances/recent activity

– 61% transfers between own accounts

– 57% receiving alerts (text, push notification, or e-mail)

• 51% of mobile bankers used mRDC in 2014

– Up from 38% in 2013.

• Frequency of mobile banking usage

– 5X per month in 2014 (same since 2012)

SOURCE: Federal Reserve’s 2015 Consumers and Mobile Financial Services Report

7 | © 2014 Jack Henry & Associates, Inc.®

Mobile Payments: Fed Report

• Smartphones are changing the way

people shop and make financial decisions.

– 47% of smartphone owners comparison

shopped with their phone while at a retail store

• 69% changed where they purchased as a result!!!

– 33% scanned a product’s barcode to find the

best price for the item.

– 42% of smartphone users browsed product

reviews while shopping at a retail store

• 79% of them changed item they purchased based on

this information!!!

SOURCE: Federal Reserve’s 2015 Consumers and Mobile Financial Services Report

9 | © 2014 Jack Henry & Associates, Inc.®

10 | © 2014 Jack Henry & Associates, Inc.®

Mobile Payments: Fed Report, 2

• 63% of mobile banking users have checked their

account balance on their phone before making

a large purchase

– 53% decided not to purchase an item as a

result of their account balance or credit limit.

• 29% of all mobile phone users and 38% of

smartphone users have used their phone to

track purchases and expenses.

SOURCE: Federal Reserve’s 2015 Consumers and Mobile Financial Services Report

11 | © 2014 Jack Henry & Associates, Inc.®

Reasons Not Using Mobile: Fed Report

• Why not using mobile banking?

– 86% say banking needs being met without

mobile banking

– 62% say security concerns

• Why not using mobile payments?

– 75% say easier to pay with cash or cards

– 59% say security concerns

SOURCE: Federal Reserve’s 2015 Consumers and Mobile Financial Services Report

12 | © 2014 Jack Henry & Associates, Inc.®

Biometrics have

boosted perception

of mobile payments

security.

13 | © 2014 Jack Henry & Associates, Inc.®

Fingerprint scan is 3-to-1

most preferred form of

biometric authentication

among consumers.

11

14 | © 2014 Jack Henry & Associates, Inc.®

Who Do Consumers Trust w/ Biometrics?

Businesses and Institutions That Consumers Trust With Biometric Information

15

16 | © 2014 Jack Henry & Associates, Inc.®7

17 | © 2014 Jack Henry & Associates, Inc.®

Why Apple Pay Matters

18 | © 2014 Jack Henry & Associates, Inc.®

• Good News

– Reinforces issuer’s card franchises

– Apple not going after issuers’ payments data

– Adds security and reduces card fraud risk/liability

• Bad News

– Additional compression of interchange rates

– New player in already crowded field of card stakeholders (from 4-party to 5-party)

– Increases urgency for community banks to remain relevant in the convergence of payments/banking/ shopping

Apple Pay: Good News and Bad

19 | © 2014 Jack Henry & Associates, Inc.®

State of Mobile Payments

Consumers Who Made a Purchase of Physical Goods

With a Mobile Phone (Past 12 Months)

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 2014

20 | © 2014 Jack Henry & Associates, Inc.®

Mobile Proximity Payments to Jump 60% CAGR

SO

UR

CE

: Javelin

Str

ate

gy &

Researc

h;

“Pre

paid

Card

s a

nd M

obile

Paym

ent R

eaders

Change t

he P

OS

Paym

ent S

tream

thro

ugh 2

018t”

; M

ay 2

014

Mobile Proximity Payment Purchase Dollar Volume and Share, 2012-2019

21 | © 2014 Jack Henry & Associates, Inc.®

Evolution of Mobile Payments

Mobile

Digital

Invisible

22 | © 2014 Jack Henry & Associates, Inc.®

From Mobile to Digital…

v. 1 v. 3

23 | © 2014 Jack Henry & Associates, Inc.®

…and from Digital to Invisible

v. 3

24 | © 2014 Jack Henry & Associates, Inc.®

Digital/Mobile Wallet Technologies

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 2014

20

26 | © 2014 Jack Henry & Associates, Inc.®

Consumers Prefer Primary FI to

Provide Mobile Wallets, But…

Consumers’ Likelihood to Select Company as Mobile Wallet Provider

27 | © 2014 Jack Henry & Associates, Inc.®

…Few FIs Provide One

• Launches late 2014

• Credit union controlled

• Issuer owns data

• 74 credit unions onboard

with 8M members

• Uses Paydiant’s barcode-

cloud system for now

• Supported by MCX

• Barcode-cloud & tokenization model

• Issuer owns data

• Partnerships with FIS, Pulse, Vantiv, BoA, Capital One, Barclaycard & Diebold

• White-label provider for MCX’s CurrentC

28 | © 2014 Jack Henry & Associates, Inc.®

“If banks can’t leverage their unique advantage as trusted entity for consumer mobile payments, they risk being… a utility that provides the transactions.”

FRBs of Boston & Atlanta (5/2/13)

“U.S. Mobile Payments Landscape –Two Years Later”

29 | © 2014 Jack Henry & Associates, Inc.®29 | © 2014 Jack Henry & Associates, Inc.®

“Google, PayPal, Amazon and

Apple…have recognized that being

first to enroll mobile wallet customers

provides them with a marketing

platform opportunity that will be far

more lucrative than interchange.”

--CU Wallet Blog, www.cuwallet.com

30 | © 2014 Jack Henry & Associates, Inc.®

PayPal Tops Branded Wallets

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 2014

Me

rch

ant

Scal

abili

ty

Consumer Preference- +

+Top 10 Branded Consumer Wallets

31 | © 2014 Jack Henry & Associates, Inc.®

Branded Wallet Rankings: Top 10

1. PayPal

2. Google Wallet

3. Apple Pay

4. MasterCard

MasterPass

5. Visa Checkout

6. AMEX Serve

7. Microsoft Wallet

8. Softcard (fka “Isis”)

9. Starbucks

10.MCX CurrentC

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 2014

32 | © 2014 Jack Henry & Associates, Inc.®

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 201435

33 | © 2014 Jack Henry & Associates, Inc.®

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 201433

34 | © 2014 Jack Henry & Associates, Inc.®

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 201437

35 | © 2014 Jack Henry & Associates, Inc.®

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 201441

36 | © 2014 Jack Henry & Associates, Inc.®

SOURCE: Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy:

How the Game Changes with Apple Pay”; October 201446

37 | © 2014 Jack Henry & Associates, Inc.®

Issuer Tokenization & Apple Pay

• Apple Pay is first to deploy “issuer tokenization”

– A token is a numeric substitute (DAN) used in

place of the card’s primary account number (PAN)

• Payment networks provision a specific token (on

behalf of issuers) not only for the PAN but also for the

platform for which it was requested in a process

called identification and verification (ID&V), which

is performed each time a payment token is requested,

subsequently locking that payment data into that

specific use case.

• Standards set by EMVCo in March 2014

SOURCE: Aite Group; “How Tokenization and Encryption

Can Take the Wind Out of a Hacker's Sails”; October 2014

38 | © 2014 Jack Henry & Associates, Inc.®

Issuer Economics: Apple Pay

• Apple Fees

– Transaction Fees

• Debit: $.005 per transaction

• Credit: 15 basis points

• Processor Onboarding Fees

– Implementation; card art; token transmission

• Network Fees

– Tokenization

• Token provisioning

• Monthly management/maintenance

• Token/PAN mapping to/from alternate networks

39 | © 2014 Jack Henry & Associates, Inc.®

MasterCard Issuer Tokenization Fees

Description Frequency Fee

MasterCard Digital

Enablement Service

Lifecycle Management

(MasterCard)

Monthly 10 cents per primary

account number

MasterCard Digital

Enablement Service

Lifecycle Management

(Maestro/Cirrus)

Monthly 10 cents per primary

account number

MasterCard Digital

Enablement Service

Digitization

Per Successful

Provision

50 cents per device

token

MasterCard Digital

Enablement Service

Alternate Network Call Out

Monthly 2.5 cents per call from/to

alternate network’s API

SOURCE: MasterCard U.S. Region Pricing Bulletin No.,6; August 6, 2014; Clarification of New Fees for MasterCard Digital Enablement Services

40 | © 2014 Jack Henry & Associates, Inc.®

Visa Issuer Tokenization Fees

Description Frequency Fee

Token Provisioning Per token created 7 cents

Per token declined 2 cents

Residency & Maintenance

(to maintain token)

Monthly $.0025 per active1 token(Capped at 15 cents per primary

account number per month)

Lifecycle Management Per token update 2 cents

SOURCE: Visa Business News; Systems & Operations | Interchange & Pricing; September 16, 2014; Visa Token Service Pricing for U.S. Issuers & Processors

1 With at least one transaction in the past 12 months.

NOTE: Issuers may also be assessed a one-time set-up fee for custom implementation.

41 | © 2014 Jack Henry & Associates, Inc.®

Big Questions for Small Issuers

• Will lower fraud rates/liability/losses offset

higher issuer costs (tokenization and Apple fees)?

• Will Apple Pay actually convert more cash

transactions to card transactions?

• Will Apple Pay create bias for credit cards over

debit cards?

• When will participation (or not) in Apple Pay really

begin to matter for issuers?

• What about Android customers?

42 | © 2014 Jack Henry & Associates, Inc.®

Issuers: Apply Pay Pros & Cons

PROS

• Reduced fraud rates

(tokenization and

biometric authentication)

• Increased card

transaction volumes due

to cash displacement???

• Rise in share of card

transactions

• Retained ownership

transaction data

• Progressive brand image

CONS

• Apple transaction fees

• Tokenization fees

• No access to credentials

from your mobile banking

app

• Negative brand impact?

• Default card is crucial;

how to get and stay

there?

SOURCE: Celent: “Apple Enters Payments: Is Apple Pay the Answer for Mobile Payments?”

Celent Webinar; 20 October 2014

43 | © 2014 Jack Henry & Associates, Inc.®

Apple Pay: Shift from Debit to Credit?

SOURCE: Celent: “Apple Enters Payments: Is Apple Pay the Answer for Mobile Payments?”

Celent Webinar; 20 October 2014

44 | © 2014 Jack Henry & Associates, Inc.®

Over Half of U.S. POS Terminals

Will Be EMV Compliant by EOY 2015

Percentage and Number of Total U.S. EMV POS Terminals, 2014–2018

SOURCE: Javelin Strategy & Research; “Mobile Wallets 2014:

How Apple Pay Changes Everything”; Webinar; 10/22/14

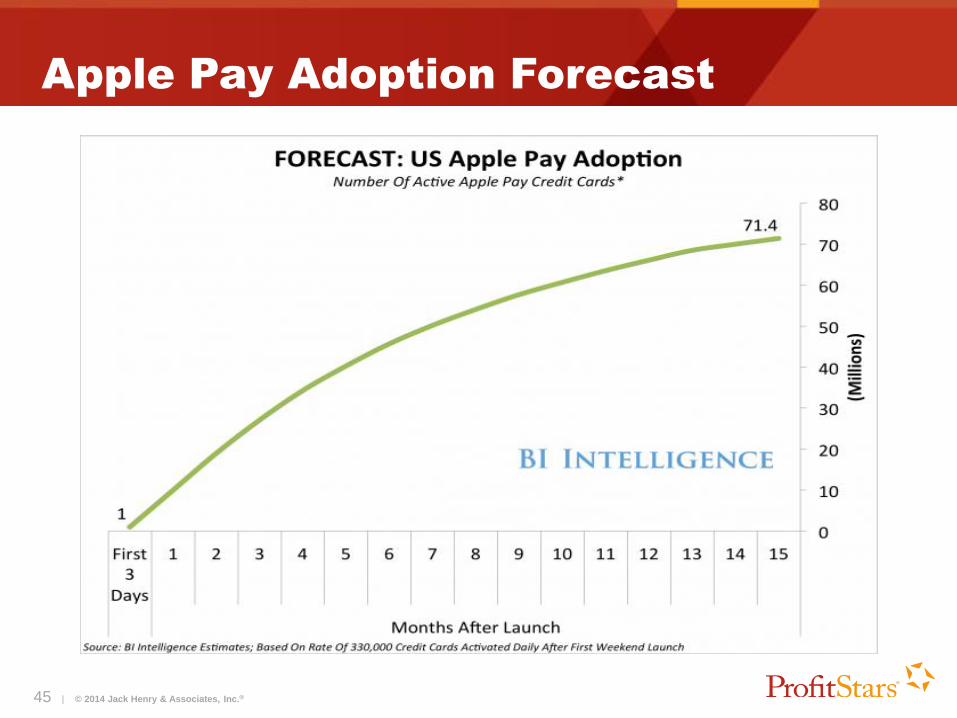

45 | © 2014 Jack Henry & Associates, Inc.®

Apple Pay Adoption Forecast

46 | © 2014 Jack Henry & Associates, Inc.®

Perspective: 70M Cards Still Small %

Cards Users Locations $ Volume

Visa 685M 280M 9.4M $2.27T

MasterCard 336M 148M 9.4M $1.05T

AMEX 53M 37M 6.4M $633B

Discover 64M 46.6M 9.2M $127B

SOURCE: Nilson #1034; February 2014

47 | © 2014 Jack Henry & Associates, Inc.®

When Will Apple Pay Impact Small

Issuers?

Timeline

• 2014: ZERO

• 2015: ZERO

• 2016: ZERO

• 2017: Uncertain

Reasons

1. Apple Pay can only be used on NFC

terminals…there aren’t many.

– 2.5% of existing POS terminals

2. It requires consumer setup

– Buy iPhone 6, set up card(s) in

Passbook, authorize card(s), enable

TouchID, etc.

3. Low opportunity cost for not

supporting Apple Pay short term

– Few if any consumers will defect

because they can’t put your debit

card in Passbook for Apple Pay

SOURCE: “Why (Most) Banks Need Not Worry About Apple Pay (Yet)”; By Jim Bruene; 9/15/14; www.netbanker.com

48 | © 2014 Jack Henry & Associates, Inc.®

Adoption Wildcards: Apple Pay

• Growth in NFC terminals at merchants

– Will merchants “turn on NFC” when they deploy

their EMV-enabled POS terminals?

• Growth in number, quality, and popularity of apps

that leverage Apple Pay

• Will Apple Pay migrate from NFC to Cloud?

– iBeacons (Bluetooth LE) and integrated cloud

payments that iPhone 5s devices could do?

SOURCE: “Apple Pay, Now That We’ve Sobered Up”; By David S. Evans; www.pymnts.com; 09/25/14

49 | © 2014 Jack Henry & Associates, Inc.®

Issuer Decisions

• Participate? Enroll now or later?

• Enroll debit cards, credit cards, or both?

– Only consumer credit and debit BINs eligible.

– Debit BINs subject to Durbin

• Which unaffiliated debit networks to add to your debit token BIN(s)

• Is debit network(s) ready for token support?

• Do you have card art?

• Do you have cardholder Terms & Conditions?

• Which employees may access token management admin tools?

50 | © 2014 Jack Henry & Associates, Inc.®

The future is

more about data

than payments…

51 | © 2014 Jack Henry & Associates, Inc.®

SOURCE: Ron Shevlin’s Snarketing 2.0; “The Mobile Moments Of Opportunity

(Or Why Mobile Wallets Haven’t Caught On)”; http://snarketing2dot0.com/57

53 | © 2014 Jack Henry & Associates, Inc.®

Before the Payment…

1. Is this the right product for me?

– 40% of smartphone owners scan labels and UPC

codes in the store while shopping. (Aite Group)

2. Is this the best price I can get?

– One third of smartphones store coupons on their

mobile device. (Aite Group)

3. How can/should I pay for this? Can I afford it?

– Would putting this on my Amex credit card be

better than paying for it with my debit card? Do I

have rewards points I can apply to the purchase?

SOURCE: Ron Shevlin’s Snarketing 2.0; “The Mobile Moments Of Opportunity

(Or Why Mobile Wallets Haven’t Caught On)”; http://snarketing2dot0.com/

54 | © 2014 Jack Henry & Associates, Inc.®

Activity Based Marketing Marketing within the context

of an activity being performedby a customer or prospect.

56 | © 2014 Jack Henry & Associates, Inc.®

After the Payment…

1. How much did I spend on a particular category of

product so far this month?

– Traditional online PFM made it inconvenient to

answer this simple question. As mobile PFM

evolves, we’ll see more interest in this

question.

2. Where are the receipts for what I purchased?

– A quarter of smartphone owners scan paper

receipts into their smartphone. (Aite Group)

SOURCE: Ron Shevlin’s Snarketing 2.0; “The Mobile Moments Of Opportunity

(Or Why Mobile Wallets Haven’t Caught On)”; http://snarketing2dot0.com/

57 | © 2014 Jack Henry & Associates, Inc.®

Future Mobile Revenue

The revenue upside for banks and

merchants from the mobile-marketing

transformation will be a trillion dollars

or more—if the first generation of wallet

providers doesn’t lay claim to it first.

Steve MottBetterBuyDesign

58 | © 2014 Jack Henry & Associates, Inc.®

Why will consumers

choose banks for

mobile payments?

A: Context

59

60 | © 2014 Jack Henry & Associates, Inc.®

Mobile PFM is the

segue from mobile

banking to mobile

shopping/payments.

65

62 | © 2014 Jack Henry & Associates, Inc.®

Mobile PFM is the

segue from mobile

banking to mobile

finance and loans.

63 | © 2014 Jack Henry & Associates, Inc.®67

64 | © 2014 Jack Henry & Associates, Inc.®

MB’ers Want PFM (Can Get It Elsewhere)

SO

UR

CE

: Javelin

Str

ate

gy &

Researc

h;

“Levera

gin

g a

n O

mnic

hannel

Appro

ach t

o D

rive $

1.5

B in

Mobile

Bankin

g C

ost

Savin

gs”;

July

2013

Preferred Source for PFM for Online Bankers (Past 90 Days) vs. Mobile

Bankers (Past 90 Days) vs. All Consumers

65 | © 2014 Jack Henry & Associates, Inc.®

So, who wants

mobile PFM?

66 | © 2014 Jack Henry & Associates, Inc.®

Who Wants Mobile PFM?

• The Young

– Typical PFM user is 40 years old, while

non‐users are 49.

• The Wealthy

– Household income for the typical PFM user is

$92K (18% higher than the $78K for non‐users).

• The Digitally Intensive

– Dubbed “Moneyhawks” by Javelin, they use

online banking, billpay, and mobile banking

intensively…and they’re the most highly

coveted/profitable consumer segment.

SO

UR

CE

: Javelin

Str

ate

gy &

Researc

h;

“Managin

g M

oney in

the ‘M

obile

-First’ E

ra:

A B

lueprin

t fo

r O

n-t

he-G

o P

ers

onal F

inance M

anagem

ent”

; June 2

014

67 | © 2014 Jack Henry & Associates, Inc.®

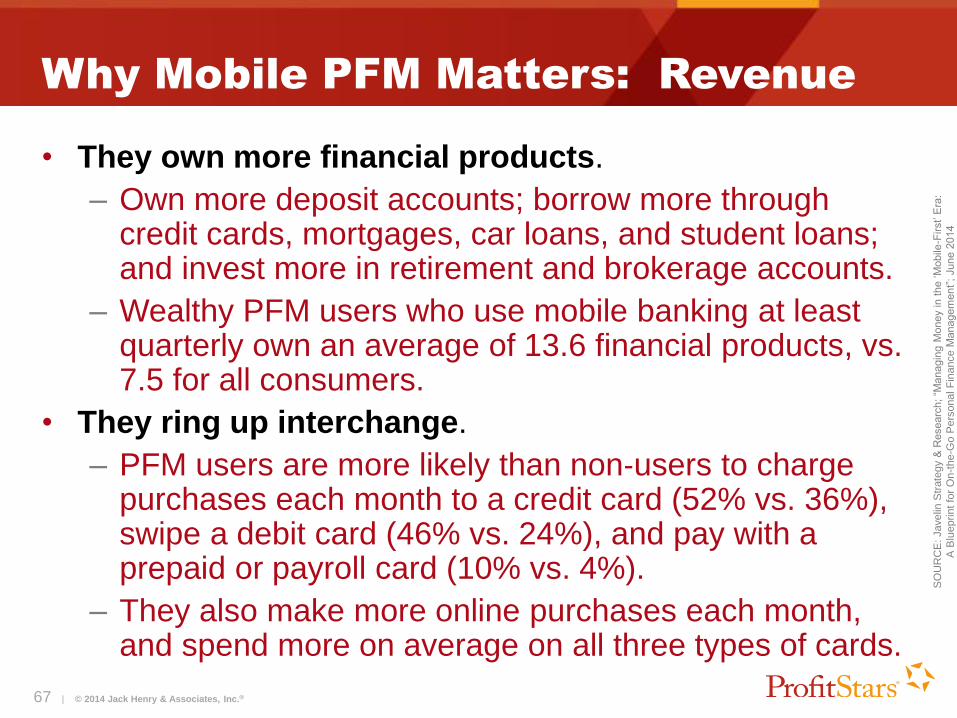

Why Mobile PFM Matters: Revenue

• They own more financial products.

– Own more deposit accounts; borrow more through credit cards, mortgages, car loans, and student loans; and invest more in retirement and brokerage accounts.

– Wealthy PFM users who use mobile banking at least quarterly own an average of 13.6 financial products, vs. 7.5 for all consumers.

• They ring up interchange.

– PFM users are more likely than non‐users to charge purchases each month to a credit card (52% vs. 36%), swipe a debit card (46% vs. 24%), and pay with a prepaid or payroll card (10% vs. 4%).

– They also make more online purchases each month, and spend more on average on all three types of cards.

SO

UR

CE

: Javelin

Str

ate

gy &

Researc

h;

“Managin

g M

oney in

the ‘M

obile

-First’ E

ra:

A B

lueprin

t fo

r O

n-t

he-G

o P

ers

onal F

inance M

anagem

ent”

; June 2

014

68 | © 2014 Jack Henry & Associates, Inc.®

Moneyhawks: Primary Wallet Target

Used a Mobile Wallet (Past 90 Days)

SO

UR

CE

: Javelin

Str

ate

gy &

Researc

h;

“Mobile

Walle

ts A

naly

sis

and S

trate

gy:

How

the G

am

e C

hanges w

ith A

pple

Pay”;

Octo

ber

2014

69 | © 2014 Jack Henry & Associates, Inc.®

Moneyhawks

• Who they are

– Profitable, demanding, mobile-oriented, digitally intensive

• What they want

– Simplicity; one-stop oversight; practical bill pay

• How to give it to them

– Easy-to-use mobile apps with account aggregation

– Overdraft and credit limit alerts

– Spend tracking, analysis, and recommendations

– Easy online and mobile account opening

• Start application in one channel and finish in another

– Prove data-mining for their benefit only (not shared)

69

SO

UR

CE

: Javelin

Str

ate

gy &

Researc

h;

“Managin

g M

oney in

the ‘M

obile

-First’ E

ra:

A B

lueprin

t fo

r O

n-t

he-G

o P

ers

onal F

inance M

anagem

ent”

; June 2

014

71 | © 2014 Jack Henry & Associates, Inc.®

Let Strategy Drive Optimal Channel Mix

Ph

ysic

al

Dig

ital

Digital Focus

Digital Mainstream

Balanced

Trust Advisor

Physical Focus

72 | © 2014 Jack Henry & Associates, Inc.®

Physical Focus Channel Strategy

73 | © 2014 Jack Henry & Associates, Inc.®

Digital Focus Channel Strategy

74 | © 2014 Jack Henry & Associates, Inc.®

75 | © 2014 Jack Henry & Associates, Inc.®

Non-Customer Access to Channels

76 | © 2014 Jack Henry & Associates, Inc.®

Marching Orders for Banks

• Monitor evolution of digital/mobile wallets/payments

– No rush, but protect your data!!!

• Ensure cards are available with the wallets most likely to

win in the market.

– Apple Pay is a relatively safe bet short-mid term

– Visa Checkout, MC’s MasterPass (no brainers)

– Isis, PayPal & Google Wallet (beware your data)

• Ensure your cards are “top of [digital] wallet”

– Apple Pay timing; card-linked offers; mobile PFM

• Enhance mobile banking with MDC, PFM, P2P, best-

price shopping, and, ultimately, your own mobile wallet.

77 | © 2014 Jack Henry & Associates, Inc.®

Sources

• Javelin Strategy & Research; “Mobile Wallets Analysis and Strategy: How the

Game Changes with Apple Pay”; October 2014

• Celent; “Apple Enters Payments: Is Apple Pay the Answer for Mobile

Payments?”; October 2014

• Aite Group; “How Tokenization and Encryption Can Take the Wind Out of a

Hacker's Sails”; October 2014

• EMVCo, LLC; “EMV®* Payment Tokenization Specification Technical

Framework, Version 1.0”; March 2014

• MasterCard Digital Enablement Service; Pricing Bulletin No. 6, August 6, 2014

• Visa Token Service Pricing; Visa Business News on September 16, 2014; Visa

Online

• Apple Pay Developers Kit

• American Bankers Association: Apple Pay FAQs; September 2014

• Javelin Strategy & Research; “Managing Money in the ‘Mobile-First’ Era: A

Blueprint for On-the-Go Personal Finance Management”; June 2014

78 | © 2014 Jack Henry & Associates, Inc.®

Lee Wetherington, [email protected]://discover.profitstars.com/leewetherington

@leewetherington

/in/leewetherington

Thanks for Attending!