growth, poverty and agriculture in africa: linkages and policy

DESCRIPTION

Growth, Poverty and Agriculture in Africa: Linkages and Policy. Joachim von Braun Director General International Food Policy Research Institute Accra, Nov. 2007. IFPRI’s Strategic Framework. Research. Partners, stakeholders, donors, IFPRI Board and Staff. Influence on policies - PowerPoint PPT PresentationTRANSCRIPT

Growth, Poverty and Agriculture Growth, Poverty and Agriculture in Africa: Linkages and Policyin Africa: Linkages and Policy

Joachim von BraunJoachim von BraunDirector GeneralDirector General

International Food Policy Research InstituteInternational Food Policy Research Institute

Accra, Nov. 2007Accra, Nov. 2007

Influence on policies

Impact on poor people

IFPRI’s Strategic FrameworkIFPRI’s Strategic Framework

Research

Capacity strengthening

Policy communication

Partners, stakeholders,

donors, IFPRI Board and Staff

Policymakers, media, opinion

leaders, and IFPRI

ECOWASCORAF

COMESA

ASARECA

IFPRI Offices

SAKSS Nodes

IFPRI in Africa

NEPAD

AU

Africa on the move: OverviewAfrica on the move: Overview

1.1. Growth for poverty reductionGrowth for poverty reduction

2.2. Africa’s new growth and development Africa’s new growth and development initiatives (NEPAD and CAADP)initiatives (NEPAD and CAADP)

3.3. Supporting implementation of Africa’s Supporting implementation of Africa’s growth agendagrowth agenda

AFRICA IS GROWING AGAINAFRICA IS GROWING AGAIN

-3

0

3

6

9

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Per

cen

t (%

)

Agriculture, value added (annual % grow th)

GDP grow th (annual %)

GROWTH IS SPREADING

Agriculture GROWTH IS SPREADING

95

100

105

110

115

120

125

2001 2002 2003 2004 2005

World Africa

Index of Ag. Export Value (2000 =100)

TRADE PERFORMANCE IS PICKING UP

95

100

105

110

115

120

125

130

135

140

145

150

155

160

2001 2002 2003 2004 2005

World Africa

Index of Ag. Export Volume (2000 =100)

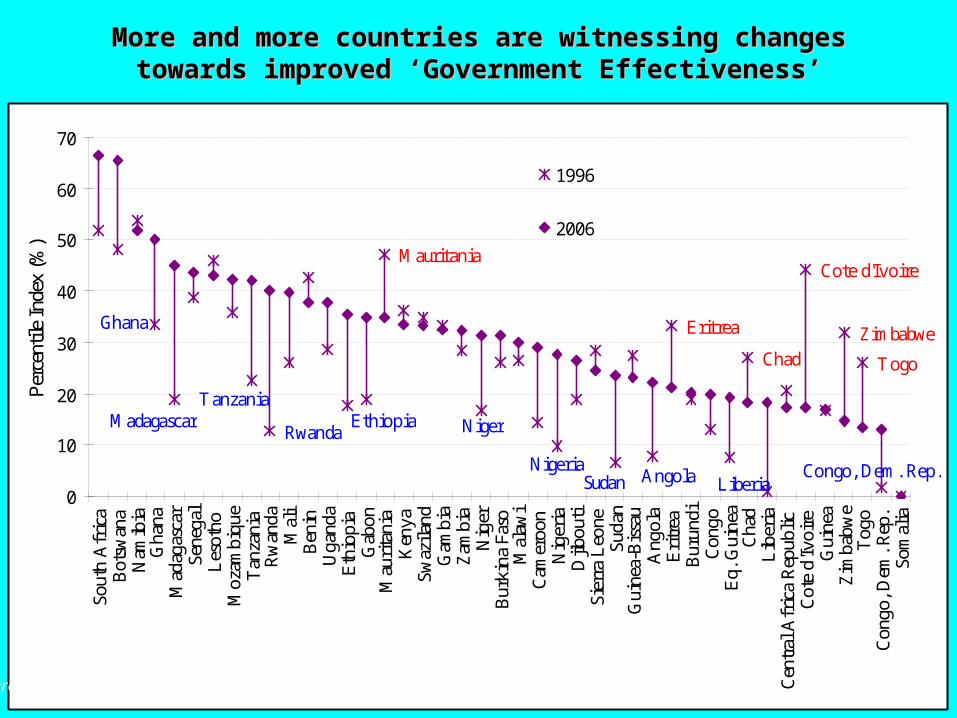

More and more countries are witnessing changes towards More and more countries are witnessing changes towards improved ‘Government Effectiveness’improved ‘Government Effectiveness’

Ghana

TanzaniaEthiopia

Nigeria

Cote d'Ivoire

Zimbabwe

Togo

Mauritania

Eritrea

MadagascarRwanda

Chad

Niger

Congo, Dem. Rep.LiberiaAngolaSudan

0

10

20

30

40

50

60

70

Sout

h A

fric

aB

otsw

ana

Nam

ibia

Gha

naM

adag

asca

rSe

nega

lL

esot

hoM

ozam

biqu

eT

anza

nia

Rw

anda

Mal

iB

enin

Uga

nda

Eth

iopi

aG

abon

Mau

rita

nia

Ken

yaSw

azila

ndG

ambi

aZ

ambi

aN

iger

Bur

kina

Fas

oM

alaw

iC

amer

oon

Nig

eria

Djib

outi

Sier

ra L

eone

Suda

nG

uine

a-B

issa

uA

ngol

aE

ritr

eaB

urun

diC

ongo

Eq.

Gui

nea

Cha

dL

iber

iaC

entr

al A

fric

a R

epub

licC

ote

d'Iv

oire

Gui

nea

Zim

babw

eT

ogo

Con

go, D

em. R

ep.

Som

alia

Per

cent

ile I

ndex

(%

)

1996

2006

Source: 2006 Worldwide Governance Indicators, The World Bank, 2007

Food retailers

top 10:$777bln • Wal-Mart • Carrefour • Royal Ahold • Metro AG • Tesco

C o

n s u

m e r s $4,000 b

illion

The world food system globalizesThe world food system globalizes

Food processors and traders

top 10: $363 bln

• Nestle • Cargill • Unilever • ADM • Kraft Foods

Agricultural input

industry

top 10: $37 bln

• Syngenta • Bayer • BASF • Monsanto • DuPont

Farms

Agricultural value added:

$1,315 bln

450 million>100 ha: 0.5%

< 2 ha: 85%

Source: von Braun, 2005

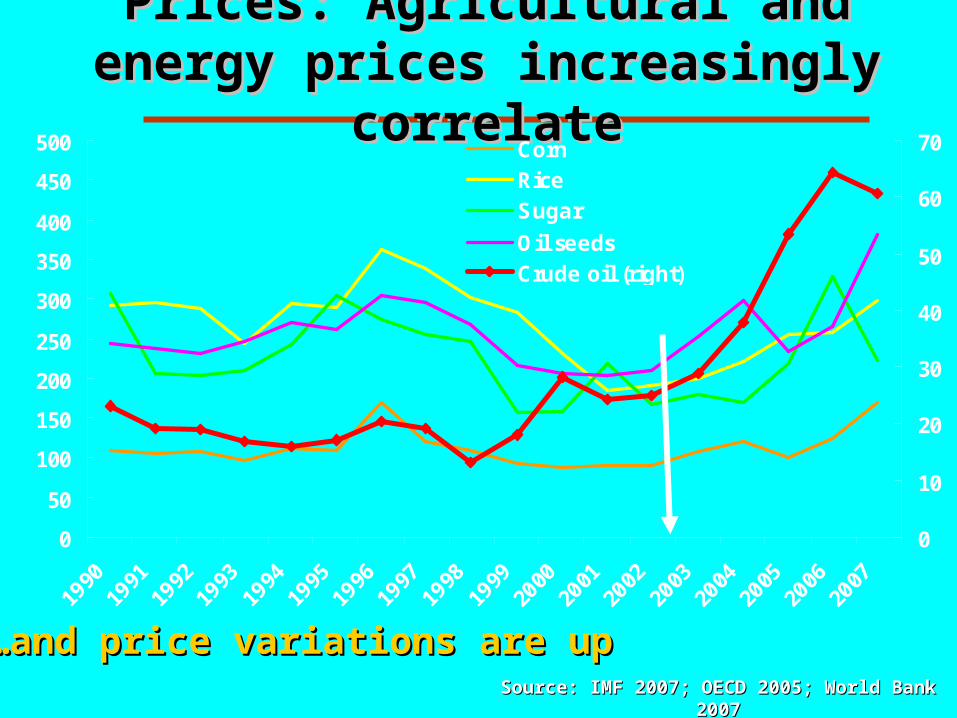

Prices: Agricultural and energy Prices: Agricultural and energy prices increasingly correlateprices increasingly correlate

Source: IMF 2007;Source: IMF 2007; OECD 2005; World Bank 2007OECD 2005; World Bank 2007

0

50

100

150

200

250

300

350

400

450

500

0

10

20

30

40

50

60

70CornRiceSugar

Oil seedsCrude oil (right)

……and price variations are upand price variations are up

Climate change & energy threatsClimate change & energy threats

• By 2020, 75-250 million people expected to be By 2020, 75-250 million people expected to be exposed to drought (mainly in Africa)exposed to drought (mainly in Africa)

- Adverse effect on livelihoods & food Adverse effect on livelihoods & food securitysecurity

- Exacerbate malnutrition & water-related Exacerbate malnutrition & water-related problemsproblems

- By 2020, yields could be reduced by up to By 2020, yields could be reduced by up to 50% (rain-fed agriculture)50% (rain-fed agriculture)

Energy: biofuels - food / biomass competitionEnergy: biofuels - food / biomass competition

Higher food prices (scenarios: 30 to 80% + prices)Higher food prices (scenarios: 30 to 80% + prices)

Instabilities increase (new risks for Africa’s poor)Instabilities increase (new risks for Africa’s poor)

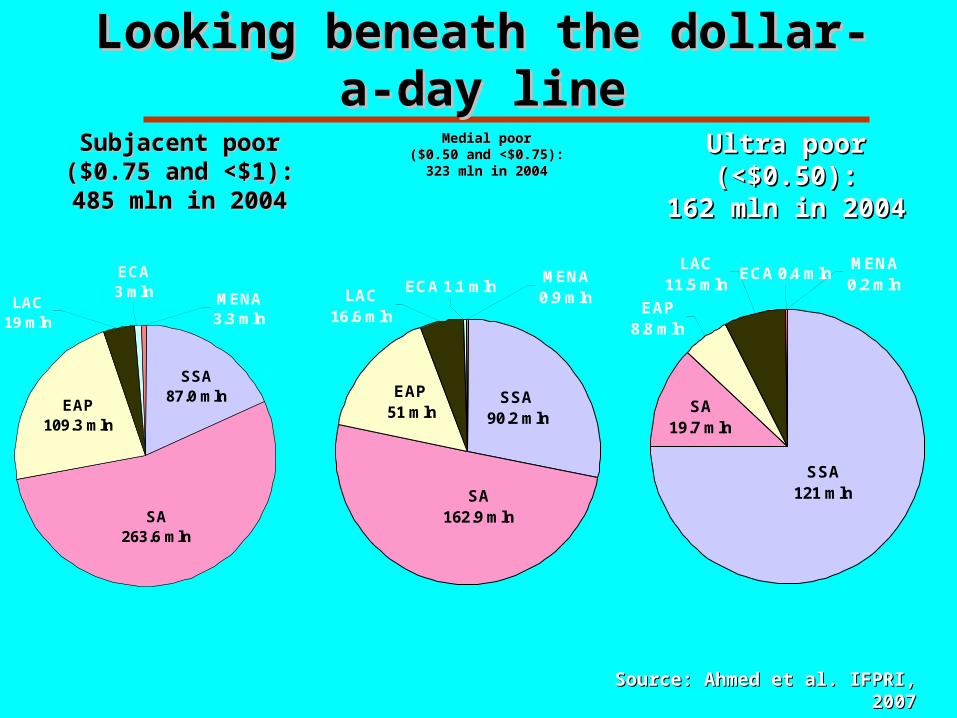

Looking beneath the dollar-a-day Looking beneath the dollar-a-day lineline

Subjacent poorSubjacent poor($0.75 and <$1):($0.75 and <$1):485 mln in 2004485 mln in 2004

Ultra poorUltra poor(<$0.50):(<$0.50):

162 mln in 2004162 mln in 2004

Medial poorMedial poor($0.50 and <$0.75):($0.50 and <$0.75):

323 mln in 2004323 mln in 2004

ECA 1.1 mlnMENA0.9 mlnLAC

16.6 mln

EAP 51 mln

SSA 90.2 mln

SA162.9 mln

MENA0.2 mln

ECA 0.4 mlnLAC

11.5 mln

EAP8.8 mln

SA19.7 mln

SSA121 mln

LAC19 mln

ECA3 mln MENA

3.3 mln

EAP109.3 mln

SSA87.0 mln

SA263.6 mln

Source: Ahmed et al. IFPRI, 2007Source: Ahmed et al. IFPRI, 2007

The share of the poorest in SSA is The share of the poorest in SSA is growinggrowing

-1.4

-0.9

-0.7

0.06 0.14

-2

-1.5

-1

-0.5

0

0.5

Developing World

East Asia & Pacific

South Asia

L America & Caribb.

Sub-Saharan Africa

% p

oin

t c

ha

ng

e

Source: Ahmed et al. 2007Source: Ahmed et al. 2007

Change in the share of poor living below .50$/day 1990-2004Change in the share of poor living below .50$/day 1990-2004

MDG progress (GHI), growth & MDG progress (GHI), growth & governancegovernance

-1.00

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

-10 -5 0 5 10

low government effectiveness (1998) higher governnment effectiveness (1998)

Annual growth rate in GNI per capita, 1990-2004 (in %)

GH

I pro

gre

ss

ind

ica

tor

Congo DR

Ethiopia India China

Brazil

Nigeria

Ghana

Kenya Tanzania

Uganda

Source: Wiesmann 2007.

Low gov. effectiveness is assigned to countries in the lowest quartile of Worldwide Governance Indicators.

What explains the high poverty and What explains the high poverty and hunger incidences in Africa?hunger incidences in Africa?

1.1. Low agricultural productivity and output growthLow agricultural productivity and output growth

2.2. Poor access to infrastructure, production inputs Poor access to infrastructure, production inputs and rural services (e.g. health and education) and rural services (e.g. health and education)

3.3. Loss of competitiveness in domestic, regional and Loss of competitiveness in domestic, regional and world marketsworld markets

4.4. Years of neglect of food staples and livestock Years of neglect of food staples and livestock sectors sectors

5.5. Inadequate public and private sector investments, Inadequate public and private sector investments, especially in rural areasespecially in rural areas

6.6. Weak enabling environment: governance, Weak enabling environment: governance, institutions, standards and regulationsinstitutions, standards and regulations

7.7. Low capacity to deal with vulnerabilities to political Low capacity to deal with vulnerabilities to political instability and natural shocks (droughts, disease instability and natural shocks (droughts, disease and pests, health, such as HIV/AIDS and Malaria)and pests, health, such as HIV/AIDS and Malaria)

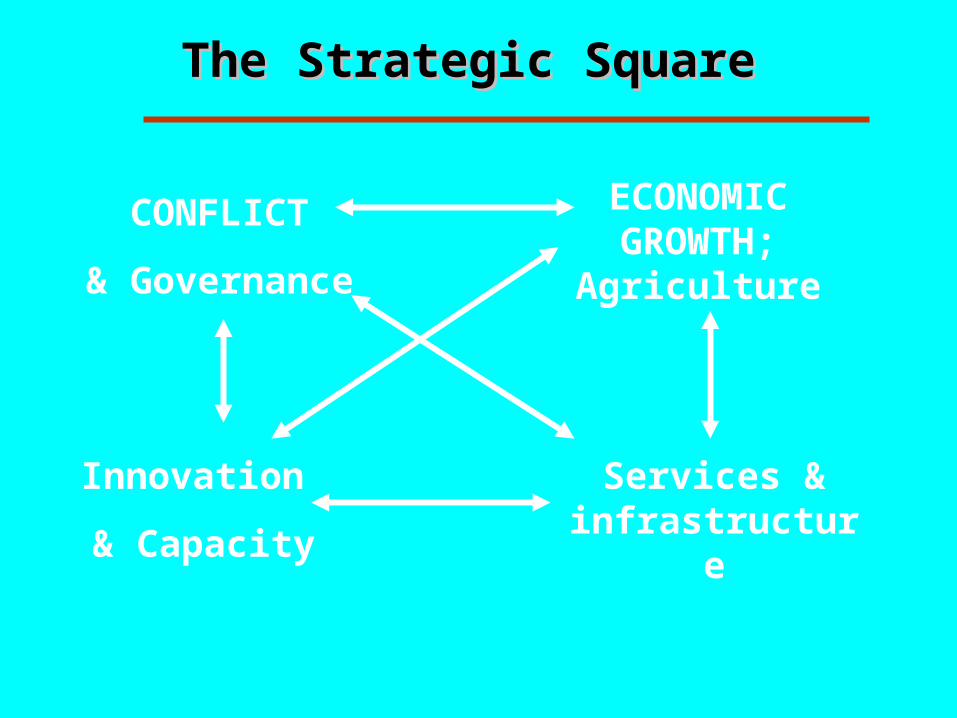

The Strategic Square The Strategic Square

Innovation

& Capacity

ECONOMIC GROWTH; Agriculture

CONFLICT

& Governance

Services & infrastructure

AGRICULTURE-LED GROWTH TO REACH MDG1AGRICULTURE-LED GROWTH TO REACH MDG1

TARGET GOAL OF 6% SECTOR GROWTH RATETARGET GOAL OF 6% SECTOR GROWTH RATE

INCREASED PUBLIC INVESTMENT (10% BUDGET SHARE)INCREASED PUBLIC INVESTMENT (10% BUDGET SHARE)

FOUR MAIN PILLARS TO GUIDE INVESTMENTFOUR MAIN PILLARS TO GUIDE INVESTMENT Land and water managementLand and water management Agribusiness and InfrastructureAgribusiness and Infrastructure Hunger and social safety netsHunger and social safety nets Science and TechnologyScience and Technology

POLICY EFFICIENCY, PEER REVIEW, ACCOUNTABILITYPOLICY EFFICIENCY, PEER REVIEW, ACCOUNTABILITY

EXPLOITATION OF REGIONAL COMPLEMENTARITIESEXPLOITATION OF REGIONAL COMPLEMENTARITIES

INCLUSIVENESS: FARMERS, AGRIBUSINESS, CIVIL SOCIETYINCLUSIVENESS: FARMERS, AGRIBUSINESS, CIVIL SOCIETY

MAIN FEATURES & PRINCIPLES

THE COMPREHENSIVE AFRICA AGRICULTURE THE COMPREHENSIVE AFRICA AGRICULTURE DEVELOPMENT PROGRAMME DEVELOPMENT PROGRAMME

Supporting implementation of Supporting implementation of Africa’s growth agendaAfrica’s growth agenda

• Analytical Agenda and M&E of CAADPAnalytical Agenda and M&E of CAADP

• Piloting Country Strategy SupportPiloting Country Strategy Support

• Establishment of ReSAKSSEstablishment of ReSAKSS

• Providing Roundtable Support to Implement Providing Roundtable Support to Implement CADDP at the National LevelCADDP at the National Level

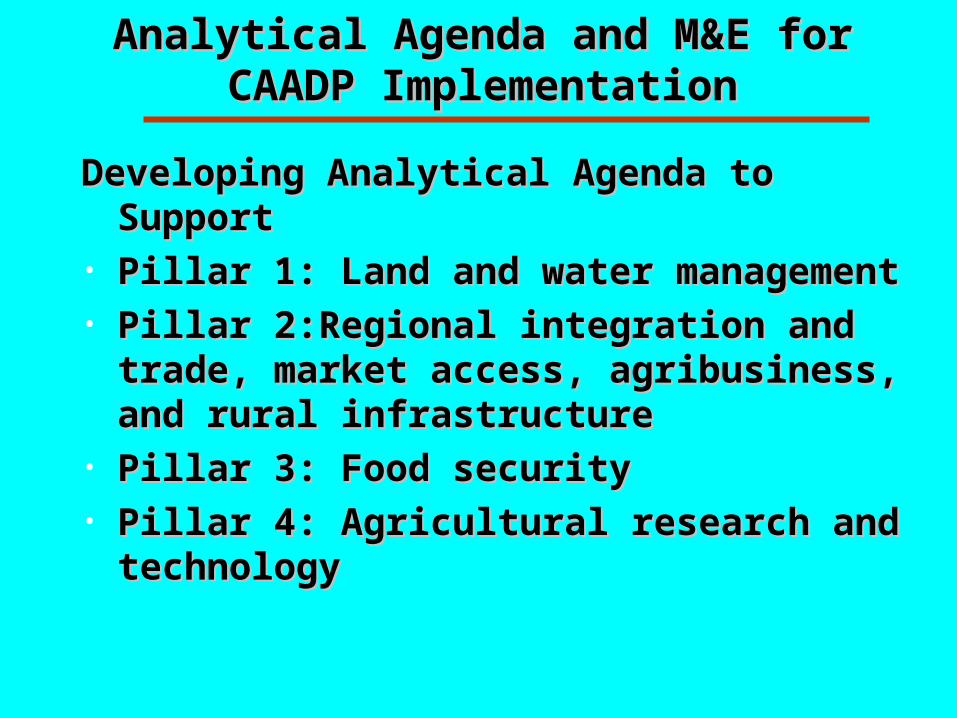

Analytical Agenda and M&E for CAADP Analytical Agenda and M&E for CAADP ImplementationImplementation

Developing Analytical Agenda to Support Developing Analytical Agenda to Support • Pillar 1:Pillar 1: Land and water management Land and water management • Pillar 2:Regional integration and trade, Pillar 2:Regional integration and trade,

market access, agribusiness, and rural market access, agribusiness, and rural infrastructure infrastructure

• Pillar 3: Food security Pillar 3: Food security • Pillar 4: Agricultural research and Pillar 4: Agricultural research and

technologytechnology

PROGRESS TOWARDS CAADP GROWTH TARGETPROGRESS TOWARDS CAADP GROWTH TARGET

-12

-9

-6

-3

0

3

6

9

12

15

18

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37

Sample of countries (Total =37)

Gro

wth

Rat

e (%

)

2000-2003

2003-2005

CAADP 6% target

Progress against CAADP 10% goal (2004)Progress against CAADP 10% goal (2004)

0

5

10

15

20

25G

uine

a

Mad

agas

car

Nam

ibia

Mal

i

Cha

dG

ambi

a

Leso

tho

Zim

babw

eC

ote

d'Iv

oire

Mau

ritan

iaU

gand

a

Ken

yaE

thio

pia

Mal

awi

Cam

eroo

nM

ozam

biqu

e

Ben

inN

iger

iaS

eneg

al

Cen

tral

Afri

can

Rep

ublic

Zam

bia

Sw

azila

ndB

urki

na F

aso

Tan

zani

a

Tog

oB

urun

di

Nig

erG

hana

Gui

nea-

Bis

sau

Rw

anda

Per

cent

of

Ag

to T

otal

Sp

end

ing

(%)

Source: Fan et al., IFPRI (forthcoming)

Analysis SupportAnalysis Support

• 1. How agricultural growth vs. non 1. How agricultural growth vs. non agricultural growth contributes to national agricultural growth contributes to national development goalsdevelopment goals

• 2. How much investment is needed to 2. How much investment is needed to support needed agricultural growthsupport needed agricultural growth

• 3. How to allocate agricultural investment 3. How to allocate agricultural investment • 4. What are other complementary polices 4. What are other complementary polices

are needed to help the poor who will not are needed to help the poor who will not benefit from agricultural growthbenefit from agricultural growth

• 5. How to reform the governance structure 5. How to reform the governance structure

GhanaGhana

Source: IFPRI work in Progress

Ghana

50

75

100

125

15019

92

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Inde

x (1

985=

100)

AgricultureProducivity

HouseholdIncome

Poverty

Hunger

GHI Trends in Africa 1981 - 2003GHI Trends in Africa 1981 - 2003

Sub-Saharan Africa, Trends 1981-2003

0

5

10

15

20

25

30

35

40

45

50

0 500 1,000 1,500 2,000 2,500

Gross National Income per capita

Glo

ba

l Hu

ng

er

Ind

ex

Ghana

Mozambique

Ethiopia

Malawi

Zambia

SenegalUganda

Kenya

•African economic growth accelerates•Agriculture is essential element of growth •Institutional reforms for markets & infrastructure

Strategic support at National and regional level

Facilitating learning across countries

Conclusions: New partnering with Africa