gsi 101 all you need to get started selling gsi for producer use only. not for use with clients. di...

TRANSCRIPT

GSI 101All You Need to Get Started Selling GSI

For Producer use only. Not for use with clients.DI 1355 1-14

disclosures

• In approved states, DInamic Foundation (forms 4501NC, 4502GR and 4503BOE) and DInamic FundamentalSM (form 4504LS) are issued by Ameritas Life Insurance Corp. located at 5900 O Street, Lincoln, NE 68510. In New York, DInamic Foundation (forms 5501-NC, 5502-GR and 5503-BOE) and DInamic FundamentalSM (form 5504-LS) are issued by Ameritas Life Insurance Corp. of New York located at 1350 Broadway, Suite 2201, New York, NY 10018. Policy and riders may vary and may not be available in all states.

• This information is provided by Ameritas®, which is a marketing name for subsidiaries of Ameritas Mutual Holding Company, including, but not limited to, Ameritas Life Insurance Corp., Ameritas Life Insurance Corp. of New York and Ameritas Investment Corp., member FINRA/SIPC. Ameritas Life Insurance Corp. is not licensed in New York. Each company is solely responsible for its own financial condition and contractual obligations. For more information about Ameritas®, visit ameritas.com.

• When implementing a GSI program, you should always advise your clients to speak with an attorney to determine if there are ERISA issues.

Ameritas® and the bison design are registered service marks of Ameritas Life Insurance Corp. Fulfilling life® is a registered service mark of affiliate Ameritas Holding Company. © 2014 Ameritas Mutual Holding Company

For Producer use only. Not for use with clients.DI 1355 1-14

For Producer use only. Not for use with clients.

agenda

• What is Guaranteed Standard Issue (GSI)?

• Why sell GSI?

• Who is a good GSI prospect?

• GSI highlights – DInamic Foundation and Fundamental

• Plan Design

• Guidelines

• Product

• How to submit a request for proposal (RFP)

• GSI sales support team services

• Q & A

DI 1355 1-14

For Producer use only. Not for use with clients.

what is GSI?

• Not a product, but a streamlined underwriting process

• Applicants who pass the gatekeeper questions will be issued a standard policy with no medical exclusions or ratings

• Gatekeeper questions:

• Missed work due to injury or illness in past 6 months?

• Ever experienced specified losses (sight, hearing, speech, two limbs)?

• Employer-employee relationship – 1099 possible

• Individual policies are discounted

DI 1355 1-14

For Producer use only. Not for use with clients.

what is GSI?

• GSI can be written on most occupation classes

• Medical professionals not eligible, except for small animal veternarians and any approved residency programs

• GSI plan can supplement Group LTD or stand alone

• Plan design at the group level – can vary by well defined eligible classes

DI 1355 1-14

For Producer use only. Not for use with clients.

why GSI?

• Your clients need it

• Threat of disability is real

• Group LTD may not be adequate

• Everyone wins: employer-employee-you

• “Multiple policies – minimal underwriting” means more premium with less time invested

• Writing agent commissions are vested for 10 years – no agent of record take-over

• Cross-selling opportunities with valuable employees

DI 1355 1-14

For Producer use only. Not for use with clients.

objections to selling individual DI insurance

• Expensive

• Detailed financial documentation

• Extensive medical underwriting

• Too many choices - confusing

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI answers objections

•Expensive

•Detailed financial documentation

•Extensive medical underwriting

•Too many choices

•Permanently discounted premiums*

•Census-only financial documentation

•Gatekeeper questions

•Plan design done at the group level

DI 1355 1-14

* Variation applies in Ohio on DInamic Fundamental.

For Producer use only. Not for use with clients.

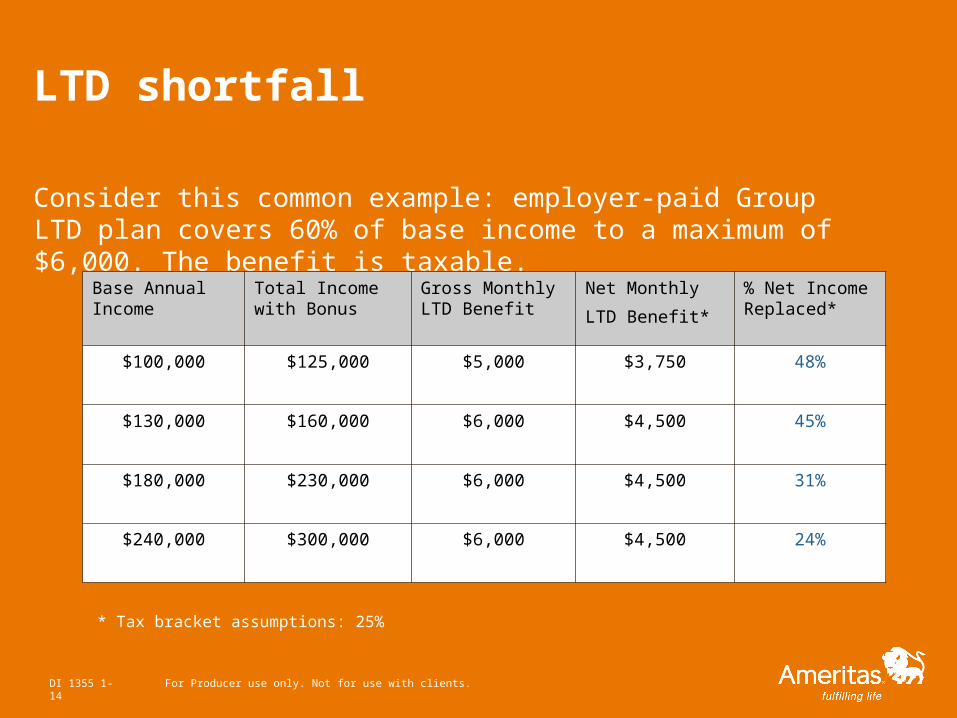

LTD shortfall

Base Annual Income

Total Income with Bonus

Gross Monthly LTD Benefit

Net Monthly

LTD Benefit*

% Net Income Replaced*

$100,000 $125,000 $5,000 $3,750 48%

$130,000 $160,000 $6,000 $4,500 45%

$180,000 $230,000 $6,000 $4,500 31%

$240,000 $300,000 $6,000 $4,500 24%

Consider this common example: employer-paid Group LTD plan covers 60% of base income to a maximum of $6,000. The benefit is taxable.

* Tax bracket assumptions: 25%

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI is beneficial for employers

• Important perk for employees• Attract/retain talent, increase employee job satisfaction and

productivity

• Great flexibility:• Paid by company, employee or both (cost-share)• Different levels of coverage by class

• Deductible business expense for employer-paid premiums (applies to non-owner premiums)

• Fixed expense – Noncancelable policy option guarantees level premium to age 65

• Voluntary plan - additional benefit offered with no additional cost to the employer

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI is beneficial for employees

• GSI underwriting means:• No exams or labs

• Short-form application

• Gatekeeper questions: actively at work, presumptive loss of use

• Applicants who satisfactorily answer gatekeeper questions will be issued a standard policy

• Streamlined financial underwriting – census from employer for GSI amount and up to $5,000 of monthly benefit above GSI level

DI 1355 1-14

For Producer use only. Not for use with clients.

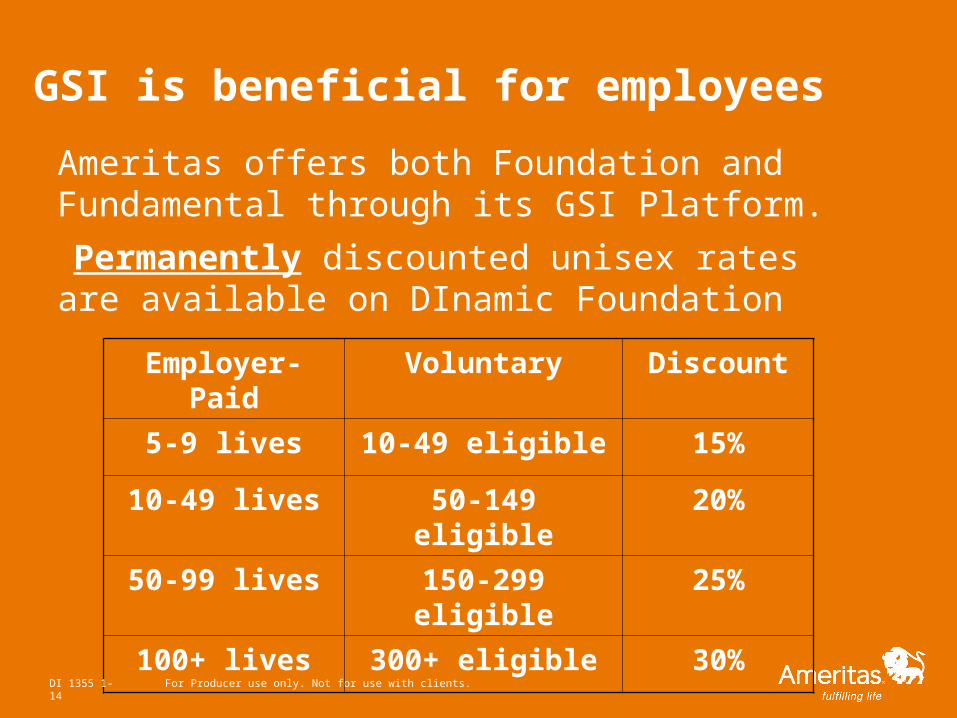

GSI is beneficial for employees

Employer-Paid Voluntary Discount

5-9 lives 10-49 eligible 15%

10-49 lives 50-149 eligible 20%

50-99 lives 150-299 eligible 25%

100+ lives 300+ eligible 30%

Permanently discounted unisex rates are available on DInamic Foundation

DI 1355 1-14

Ameritas offers both Foundation and Fundamental through its GSI Platform.

For Producer use only. Not for use with clients.

GSI is beneficial for employees

Employer-Paid Voluntary Discount

5-9 lives under 75 eligible 5%

10+ lives 75+ eligible 10%

Permanently discounted, sex –distinct rates* DInamic Fundamental

DI 1355 1-14

* In Ohio, the discount will be removed.

For Producer use only. Not for use with clients.

GSI is beneficial for employees

• Better disability income insurance policy compared to group LTD• Stronger provisions• No offsets• Individually owned• Fully portable

• Higher income protection with GSI• LTD maximum benefit for highly compensated often not

enough – reverse discrimination • GSI covers total comp vs. base salary only (most LTD plans)• Most LTD plans employer paid – benefits taxable

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI is beneficial for the producer

• GSI makes your life easier…multiple contracts with minimal underwriting

• Great cross-selling opportunities

• Effective use of your time - favorable rate of return on time invested

• Strong commissions

• 50% to 30% FYC - based on case size and premium payor

• 10% renewals

• 2 - 5% renewal bonus – based on in-force premium and persistency

• You are 100% vested – no threat of losing commissions to agent of record letter

DI 1355 1-14

For Producer use only. Not for use with clients.

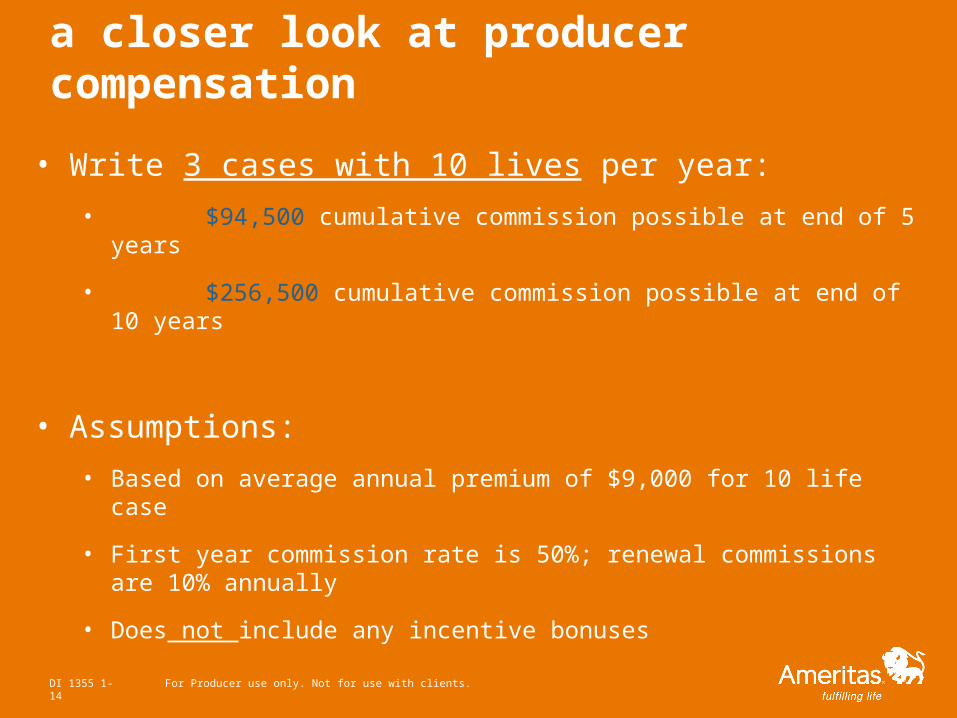

a closer look at producer compensation

• Write 3 cases with 10 lives per year:

• $94,500 cumulative commission possible at end of 5 years

• $256,500 cumulative commission possible at end of 10 years

• Assumptions:

• Based on average annual premium of $9,000 for 10 life case

• First year commission rate is 50%; renewal commissions are 10% annually

• Does not include any incentive bonuses

DI 1355 1-14

For Producer use only. Not for use with clients.

marketing opportunity

0

10

20

30

40

50

60

70

80

90

Physicians Dentists Attorneys Corp. Execs Prof. Managers MiddleIncome

Pe

rce

nt

of

Pe

ne

tra

tio

n

Individual DI Insurance Market Penetration by Profession

Source: 2012 Munich American Reassurance Company

DI 1355 1-14

For Producer use only. Not for use with clients.

how to identify a good GSI prospect DInamic Foundation• 6A-3A occupational classes• Executive carve-outs in blue/grey-collar industries• $75,000+ incomes• LTD plan does not fully cover highly compensated • Financially stable company/industry• Average age less than 50• Male/female ratio – 60/40 • Employer

• Offers other employee benefits

• Supportive of marketing plan/endorses GSI plan

• Group meetings and access to contact employees

DI 1355 1-14

For Producer use only. Not for use with clients.

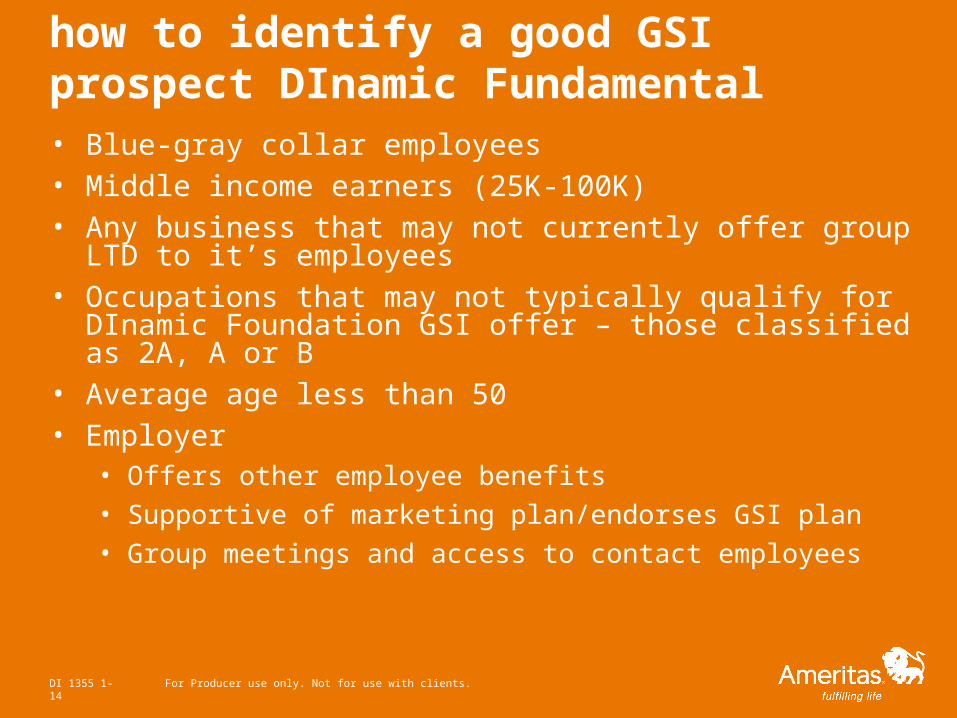

how to identify a good GSI prospect DInamic Fundamental• Blue-gray collar employees• Middle income earners (25K-100K)• Any business that may not currently offer group LTD to it’s

employees• Occupations that may not typically qualify for DInamic

Foundation GSI offer – those classified as 2A, A or B• Average age less than 50• Employer

• Offers other employee benefits

• Supportive of marketing plan/endorses GSI plan

• Group meetings and access to contact employees

DI 1355 1-14

For Producer use only. Not for use with clients.

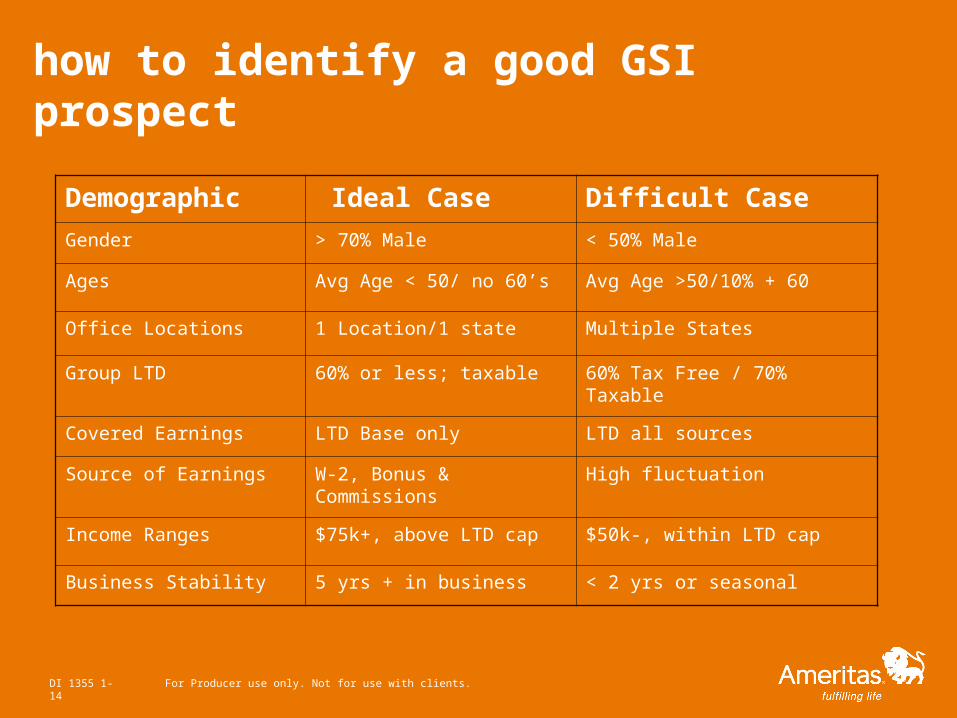

how to identify a good GSI prospect

Demographic Ideal Case Difficult Case

Gender > 70% Male < 50% Male

Ages Avg Age < 50/ no 60’s Avg Age >50/10% + 60

Office Locations 1 Location/1 state Multiple States

Group LTD 60% or less; taxable 60% Tax Free / 70% Taxable

Covered Earnings LTD Base only LTD all sources

Source of Earnings W-2, Bonus & Commissions High fluctuation

Income Ranges $75k+, above LTD cap $50k-, within LTD cap

Business Stability 5 yrs + in business < 2 yrs or seasonal

DI 1355 1-14

For Producer use only. Not for use with clients.

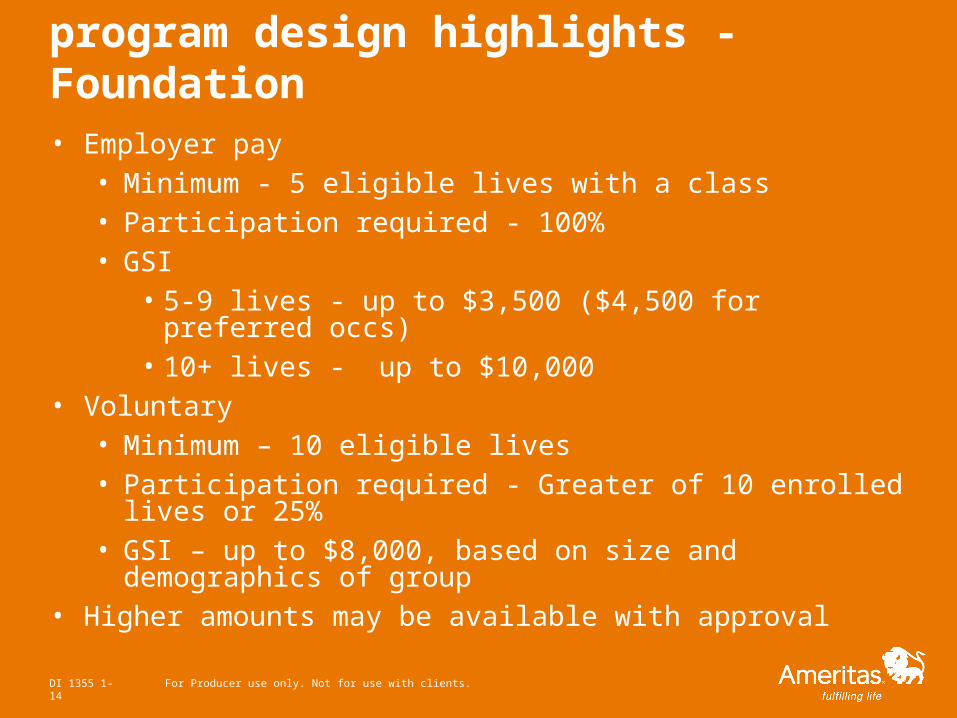

program design highlights - Foundation

• Employer pay • Minimum - 5 eligible lives with a class• Participation required - 100%• GSI

• 5-9 lives - up to $3,500 ($4,500 for preferred occs) • 10+ lives - up to $10,000

• Voluntary• Minimum – 10 eligible lives• Participation required - Greater of 10 enrolled lives or 25% • GSI – up to $8,000, based on size and demographics of

group• Higher amounts may be available with approval

DI 1355 1-14

For Producer use only. Not for use with clients.

program design highlights - Foundation

• Core/Buy-up• Employer pay core – 100% participation• Voluntary buy-up – participation is greater of 10 lives or 25%

of eligible employees

DI 1355 1-14

For Producer use only. Not for use with clients.

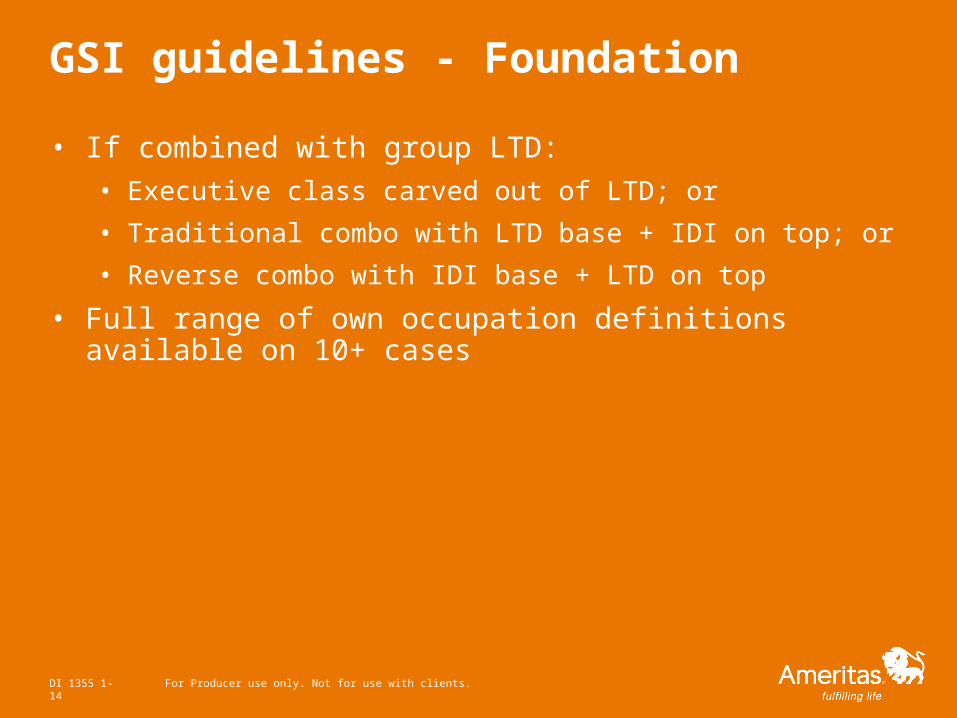

GSI guidelines - Foundation

• If combined with group LTD:

• Executive class carved out of LTD; or

• Traditional combo with LTD base + IDI on top; or

• Reverse combo with IDI base + LTD on top

• Full range of own occupation definitions available on 10+ cases

DI 1355 1-14

For Producer use only. Not for use with clients.

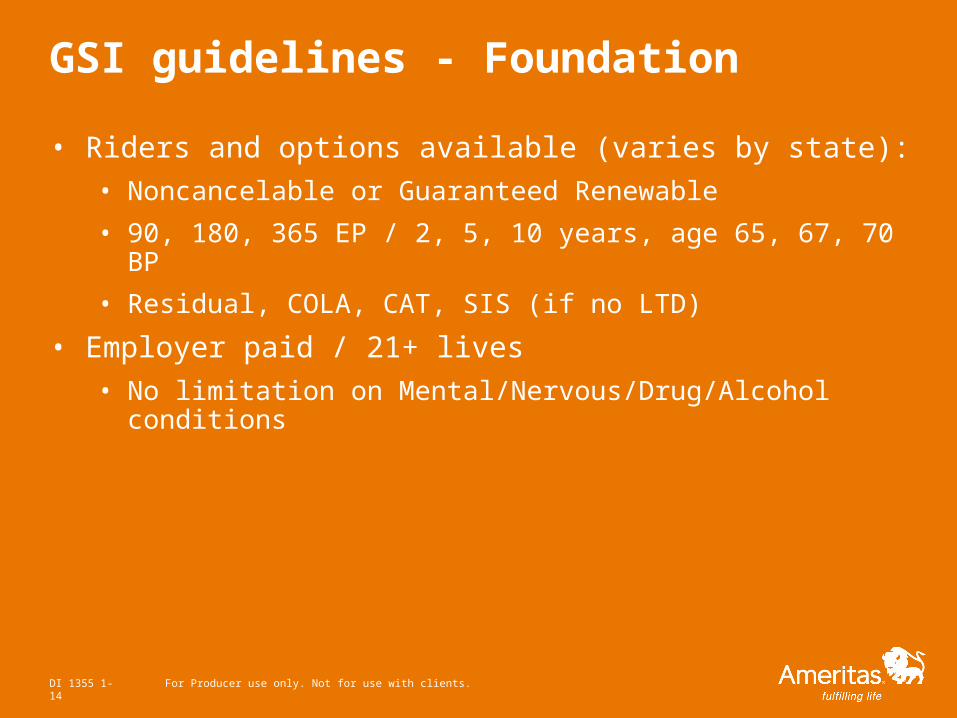

GSI guidelines - Foundation

• Riders and options available (varies by state):

• Noncancelable or Guaranteed Renewable

• 90, 180, 365 EP / 2, 5, 10 years, age 65, 67, 70 BP

• Residual, COLA, CAT, SIS (if no LTD)

• Employer paid / 21+ lives

• No limitation on Mental/Nervous/Drug/Alcohol conditions

DI 1355 1-14

For Producer use only. Not for use with clients.

product highlights

• Noncancelable (NC) or Guaranteed Renewable (GR) options• 3 Definitions of Total Disability* (including True Own

Occupation)• Unlimited MNDA – Employer pay 21+ lives• Basic Residual or Enhanced Residual• Good Health* • Nondisabling Injury*• COBRA Premium*

*Subject to state variations

DI 1355 1-14

For Producer use only. Not for use with clients.

product highlights

• Presumptive Total Disability• Survivor* • Rehabilitation• Catastrophic Disability Rider*• COLA Rider - 3% Simple or 6% Compounded• No FIO (except appropved Medical Residency program)

*Subject to state variations

DI 1355 1-14

For Producer use only. Not for use with clients.

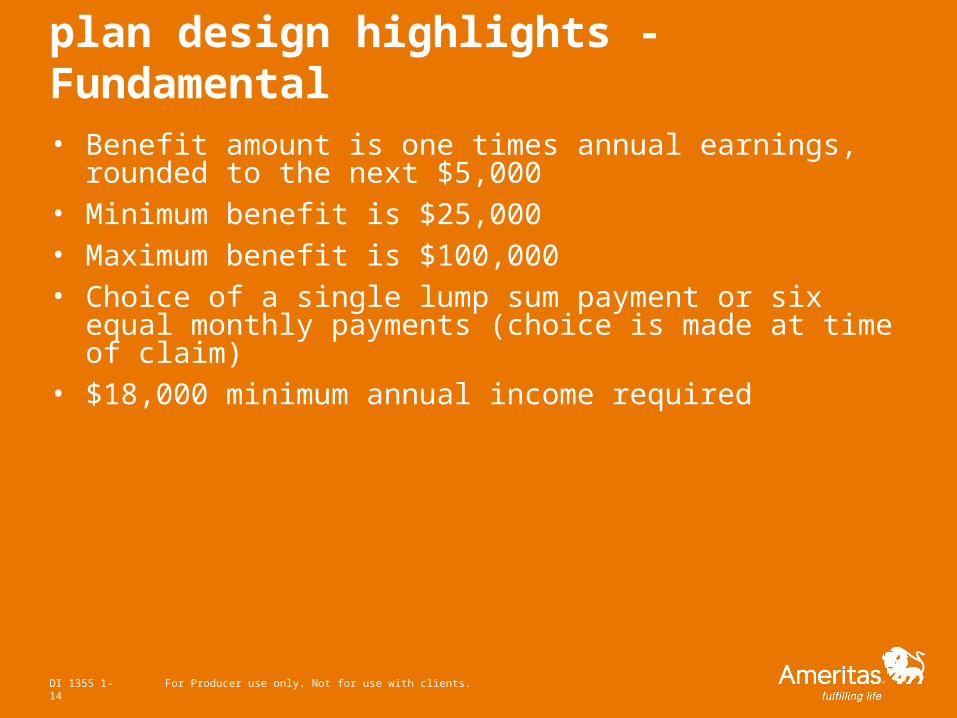

plan design highlights - Fundamental

• Benefit amount is one times annual earnings, rounded to the next $5,000

• Minimum benefit is $25,000• Maximum benefit is $100,000• Choice of a single lump sum payment or six equal monthly

payments (choice is made at time of claim)• $18,000 minimum annual income required

DI 1355 1-14

For Producer use only. Not for use with clients.

plan design highlights - Fundamental

• Guaranteed Renewable to age 65• Issue ages 18-64• Benefits are payable for total disability only – no residual or

partial benefit• No additional benefit riders• Covers actual duties performed in occupation, including manual

duties• Minimum number of 5 lives required for employer paid cases

DI 1355 1-14

For Producer use only. Not for use with clients.

plan design highlights - Fundamental

• Benefits are payable when disability prevents insured from perform material/substantial duties of any occupation for which he/she is reasonably suited based on education, training and experience

• Total disability must be expected to last at least 365 days• There is no elimination period, but insured must survive the

disability by 30 days• 6/12 pre-existing condition limitation

DI 1355 1-14

For Producer use only. Not for use with clients.

plan design highlights - Fundamental

• Policy exclusions include war or acts of war, self-inflicted injury, criminal activity and termination/suspension of license

• Benefits for mental/nervous disorders, alcoholism and/or drug abuse are limited to one-half of the total disability benefit, unless insured is expected to be confined to a hospital for at least 365 days due to the condition

• Some restricted occupations, such as seasonal occs, professional athletes, occs with duties that include severe environmental, chemical or radioactive exposure, hazardous duties, etc.

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI guidelines - Fundamental

Employer paid

• 100% participation (with minimum of 5 lives)• Maximum offer is 1x annual earnings

• Up to $50,000 for 5-9 lives• Up to $100,000 for 10+ lives

• Occupational classes are 1L and 2L• Determined by % of manual duties performed in occupation

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI guidelines - Fundamental

Employer paid

• Medical occupations are ineligible• Family content less than 50% of group• All full-time W-2 employees working at least 30 hours per week

are eligible; 1099 employees may be eligible• Business must have 2 years of stability

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI guidelines - Fundamental

Employee paid

• Groups must have a minimum of 10 eligible employees• Requires greater of 10 lives or 25% participation of all eligible

employees

• Maximum offer is 1x annual earnings, up to $100,000• Occupational classes are 1L and 2L

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI guidelines - Fundamental

Employee paid

• Medical occupations are ineligible• Family content less than 50% of group• All full-time W-2 employees working at least 30 hours per week

are eligible; 1099 employees may be eligible• Some restricted occupations (as previously mentioned)• Business must have 2 years of stability

DI 1355 1-14

For Producer use only. Not for use with clients.

how to request a proposal

• Complete one page RFP form

• Includes all the information we need to consider a GSI offer

• Submit complete census from employer (if able to obtain) in Excel format

• Employee name & address

• Gender

• DOB

• Occupation or job title – duties if known

• Income (base and bonus separated)

• Location

DI 1355 1-14

For Producer use only. Not for use with clients.

regional DI-GSI wholesale directors

• Extension of the DI product management department

• Our combined individual DI insurance and group LTD expertise is extensive

• We are committed and ready to support and equip producers to sell GSI business

DI 1355 1-14

For Producer use only. Not for use with clients.

GSI sales support and expertise

• We make it easy for you!

• Prepare proposals

• Formal offer letter

• Detailed premium and benefit summary

• Competitive analysis

• Consultation on plan design

• Pre-filled applications

• Personalized enrollment packets

• Employer and employee meetings with PowerPoint presentations

• We walk you through GSI process step-by-step

DI 1355 1-14

questions?

For Producer use only. Not for use with clients.DI 1355 1-14

key contacts

• Your agency or brokerage manager

• Your regional DI wholesale office

• Your Ameritas® sales development team

• The DI product management team

For Producer use only. Not for use with clients.DI 1355 1-14