h. l 2004 - 2008 annual report 08 · annual report 08 the specialist in psychiatry and pioneer in...

TRANSCRIPT

AnnuAlREPORT

08

The specialist in psychiatryand pioneer in neurology

Photos

Patient photos: Joachim Ladefoged and Simon Ladefoged.All patients have had their photos taken after preceding agreement. The patients have no connection to Lundbeckor to pharmaceuticals marketed by Lundbeck. Other photos: Joachim Ladefoged, Simon Ladefoged and Ricky John Molloy.

H. Lundbeck A/S

Ottiliavej 9

2500 Copenhagen - Valby

Denmark

Corporate Reporting

Tel. +45 36 30 13 11

Fax +45 36 30 19 40

www.lundbeck.com

CVR nr. 56759913

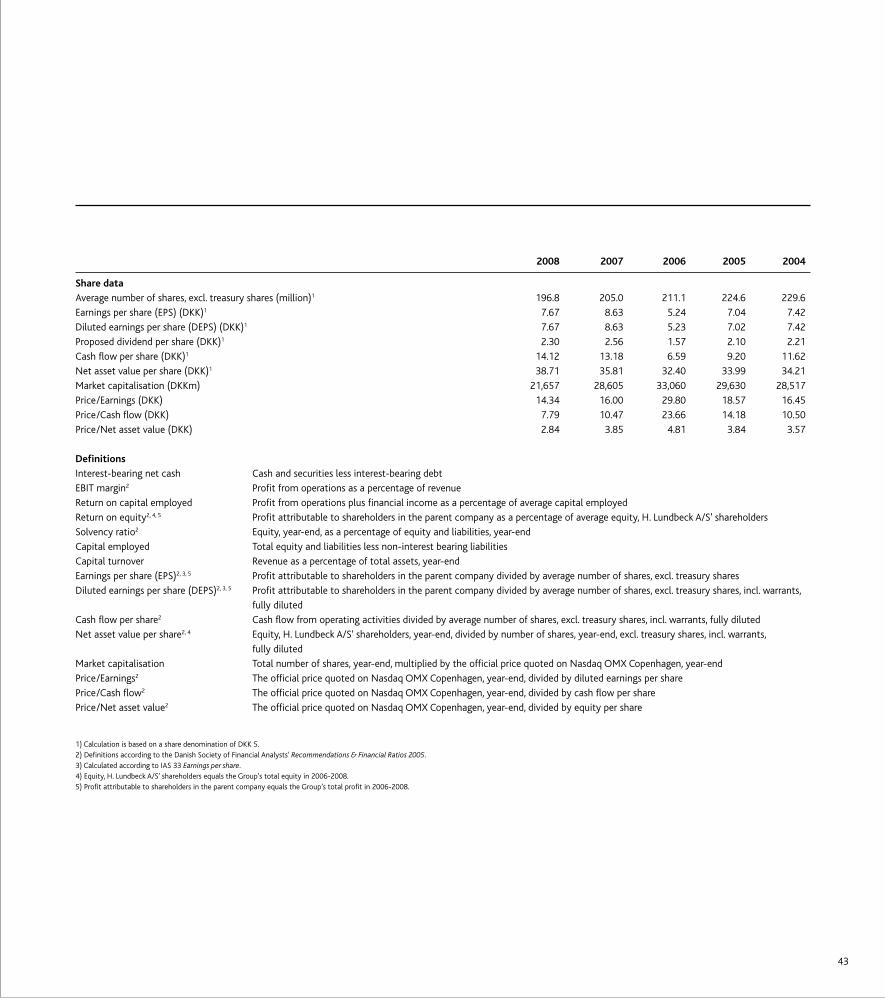

2008 2007 2006 2005 2004 2008 2008 DKKm DKKm DKKm DKKm DKKm EURm1 USDm2

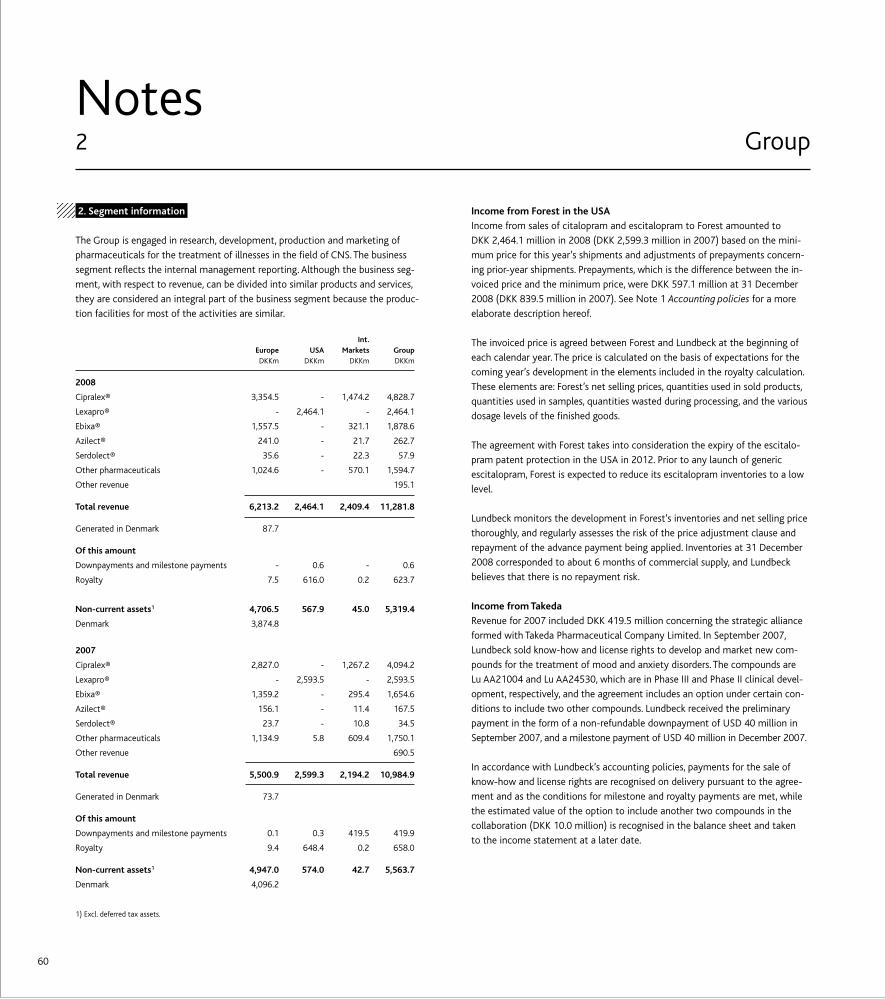

Revenue 11,282 10,985 9,221 9,070 9,733 1,513 2,219

Research and development costs 2,992 2,187 1,958 1,782 1,776 401 589

Profit from operations 2,352 2,695 1,784 2,170 2,554 315 463

Net financials (185) (50) (64) 108 16 (25) (36)

Profit for the year 1,510 1,770 1,107 1,574 1,689 202 297

Total assets 12,607 12,326 11,631 11,628 11,509 1,692 2,385

Equity 7,592 7,185 6,765 7,492 7,839 1,019 1,437

Cash flows from operating and investing activities 2,193 1,610 1,633 1,587 884 294 431

Property, plant and equipment investments, gross 229 474 567 447 305 31 43

% % % % % % %

EBIT margin 20.8 24.5 19.3 23.9 26.2 20.8 20.8

Return on capital employed 29.8 34.9 25.2 32.0 37.0 29.8 29.8

Return on equity 20.4 25.3 15.6 20.7 23.2 20.4 20.4

Research and development costs as a percentage of revenue 26.5 19.9 21.2 19.6 18.2 26.5 26.5

Solvency ratio 60.2 58.3 58.2 64.4 68.1 60.2 60.2

Capital turnover 89.5 89.1 79.3 78.0 84.6 89.5 89.5

DKK DKK DKK DKK DKK EUR1 USD2

Earnings per share (EPS)3, 4 7.67 8.63 5.24 7.04 7.42 1.03 1.51

Diluted earnings per share (DEPS)3, 4 7.67 8.63 5.23 7.02 7.42 1.03 1.51

Proposed dividend per share3 2.30 2.56 1.57 2.10 2.21 0.31 0.45

Cash flow per share3 14.12 13.18 6.59 9.20 11.62 1.89 2.78

Net asset value per share3 38.71 35.81 32.40 33.99 34.21 5.20 7.32

Market capitalisation (million) 21,657 28,605 33,060 29,630 28,517 2,907 4,098

Average number of employees 5,208 5,134 5,111 5,022 5,155

1) Income statement items are translated using the average EUR exchange rate for the year (745.58). Balance sheet items are translated at the EUR exchange

rate on 31 December 2008 (745.06). 2) Income statement items are translated using the average USD exchange rate for the year (508.38). Balance sheet items are translated at the USD exchange

rate on 31 December 2008 (528.49). 3) The calculation is based on a share denomination of DKK 5. 4) Calculated according to IAS 33 Earnings per share.

Financial highlights 2004 - 2008

H. LU

ND

BECK A

/S AN

NU

AL REPO

RT 2008

Frontpage

Denmark (depression)

Tove is out for a walk in a

park in inner Copenhagen.

Page 7

Mexico (depression)

Javier with his wife

on a cold winter day

in Mexico City.

Page 17

Malaysia (schizophrenia)

Rajesh in his room in

a treatment center in

Kuala Lumpur.

Page 21

Denmark (Alzheimer's

disease)

Ry in a quiet moment

in the day centre, where

he meets with other

patients.

Page 25

Malaysia (schizophrenia)

Seniwati sweeps the floor

in her room in a hospital

in Johor Bahru.

Page 31

Malaysia (depression)

Chia works as a tailor in

a hospital in Johor Bahru.

Page 1

Denmark (Parkinson's

disease)

Just makes gymnastic

exercises in a hot water

basin to relieve his

symptoms.

Page 35

Mexico (depression)

Yolanda looks over

Mexico City from a tall

office building.

Page 36

Mexico (depression)

Javier in a coffee shop

in Mexico City.

Page 40

China (Alzheimer's

disease)

Zhongying enjoys a

cup of coffee in a cafe

in Beijing.

AnnuAlREPORT

08

Depression and anxiety • Depression is a common and partly hereditary

disease with symptoms such as melancholy, loss of energy, difficulty concentrating and sui-cidal thoughts. Patients have trouble holding onto their job, keeping up with their studies and/or maintaining their family life and social contacts.

• The neurotransmitter serotonin transmits nerve impulses from one nerve ending to an-other. Too little serotonin can trigger a depres-sive episode.

• The disorder is categorised as either mild, moderate or severe, which refers to the inten-sity of the symptoms. Depression can strike anyone, but certain social and biological fac-tors make some people more predisposed to this disorder than others.

• There is a close correlation between depres-sion and anxiety disorders such as generalised anxiety, panic disorder and social anxiety symptoms. Nearly all patients suffering from depression also suffer from anxiety, and more than half of those who suffer from anxiety also suffer from another psychiatric disorder, pri-marily depression.

Psychotic disorders • Schizophrenia is the most common psychotic

disorder and may lead to pronounced changes in the patient's way of thinking and perception of the outside world. Affecting about 1% of the population, the disorder often starts in late adolescence. Suicide is a major cause of pre-mature deaths.

• Patients with schizophrenia may suffer acute psychotic episodes of hallucinations and delu-sions. Many patients also have some cognitive dysfunction that makes it difficult to think straight and convert thought into action. Pa-tients often also suffer from isolation and lack of initiative.

• Bipolar disorder (manic depression) is another form of psychotic disorder that is difficult to diagnose. The mood of the patients can cycle between depression and mania.

• People with uncontrolled bipolar disorder of-ten experience an impaired level of function-ing and ruined personal relationships.

Parkinson’s disease • Parkinson’s disease is a chronic and progres-

sive brain disorder that usually affects people over the age of 60.

• Parkinson’s is caused by the lack of dopamine, which is one of several chemical neurotrans-mitters responsible for transmitting signals within the brain. Loss of dopamine causes an imbalance in nerve cell activity, leaving pa-tients unable to direct or control their move-ments in a normal manner.

• Typical symptoms are tremors, stiffness, slow movements and impaired balance. The precise cause of the disease is unknown, but genes, environmental factors and age are believed to be some of the factors involved.

• As the disease progresses, the symptoms grow worse, and the patient will most likely experi-ence motor function problems. Ultimately, Parkinson’s impairs the patient's ability to function in daily life situations.

Alzheimer’s disease • Alzheimer’s disease is a neurological disorder

and is the most common form of dementia. The disease is caused by the destruction of nerve cells, causing a gradual functional de-terioration in the affected areas of the brain.

• The disease primarily affects those in middle and old age, starting with a mild stage of for-getfulness, changes in personality and confu-sion.

• At the moderate stage, patients lose the abil-ity to perform everyday activities; they suffer disorientation, delusion and language prob-lems and fail to recognise their loved ones.

• The severe stage involves a period of time with the patient in an almost vegetative state, gradually losing the ability to communicate, eat and drink. Eventually, the patient dies.

Insomnia • Insomnia is the most common form of sleep

disorder. The term "primary insomnia" refers to the fact that the disorder is not caused by other factors such as depression or pain.

• Melatonin is a naturally occurring hormone produced by the pineal gland, and it has a pivotal role in the regulation of circadian

rhythms and sleep. Endogenous melatonin levels decrease with age and may contribute to the complaint of poor sleep quality seen amongst those of middle and old age.

• Insomnia is more common among women than men. It reduces the ability to perform everyday activities and contributes to an overall deterioration in the patient's health.

• Affecting one-fourth of the population, pri-mary insomnia is characterised by symptoms such as difficulty falling asleep or sleeping without interruption, waking up frequently or very early, and experiencing non-refreshing sleep.

Stroke • Stroke is a primary reason for serious disabil-

ity in the industrialised world and one of the leading causes of death.

• A stroke occurs when the blood supply to a part of the brain is suddenly interrupted (is-chaemic) or when a blood vessel in the brain bursts, bleeding into the spaces surrounding the brain cells (haemorrhagic).

• Some of the damaged brain cells can be saved only if treatment is given within a few hours after the stroke.

• Symptoms of a stroke include sudden numb-ness or weakness, especially on one side of the body, confusion, and loss of balance or coordination skills.

Alcohol abuse • Alcohol is toxic to most body organs, espe-

cially in large amounts. • Excessive consumption of alcohol is a com-

mon problem in many parts of the world and involves huge social consequences, whilst also increasing the risk of developing a number of diseases such as cancer, cardiovascular dis-ease, cerebral atrophy, stomach ulcer and liver cirrhosis.

• The extent of injury depends on how much and for how long a time a person drinks alcohol.

• In the Western world, one in ten deaths is alcohol-related.

Mechanism First Approvedno.Compound ofaction Indication Trademark registration ofcountries Melatonin Regulation of Primary insomnia Circadin® 2007 29 circadian rhythm

Escitalopram ASRI Depression, generalised Cipralex®, Lexapro®, Sipralexa®, 2001 94 anxiety disorder, panic Sipralex® disorder, social anxiety disorder, OCD Citalopram SSRI Depression, panic disorder, Cipramil®, Seropram®, Cipram®, 1989 77 OCD Celexa® Memantine NMDA-antagonist Moderate to severe Ebixa®, Ebix® 2002 66 Alzheimer’s disease

Rasagiline MAO-B inhibitor Parkinson’s disease Azilect® 2005 33

Sertindole Atypical antipsychotic Schizophrenia Serdolect®, Serlect® 1996 45

Flupentixol Typical antipsychotic Mild depression Deanxit® 1971 28+melitracene + TCA Nortriptyline TCA Depression Noritren®, Nortrilen®, Sensaval® 1963 22 Amitriptyline TCA Depression Saroten®, Sarotex®, Redomex® 1961 31 Zuclopenthixol Typical antipsychotic Schizophrenia and other Cisordinol®, Clopixol® 1982 72 psychotic disorders, anxiety, restlessness, insomnia

Zuclopenthixol- Depot antipsychotic Maintenance treatment Cisordinol Depot®, 1976 74 decanoate of chronic psychotic Clopixol Depot®, disorders Ciatyl-Z Depot®

Zuclopenthixol- Typical antipsychotic Acute psychotic episodes, Cisordinol-Acutard®, 1986 73 acetate exacerbation of psychotic Clopixol-Acutard®, disorders Clopixol-Acuphase®, Ciatyl-Z-Acuphase®

Flupentixol Typical antipsychotic Schizophrenia and other Fluanxol®, Fluanxol Mite®, 1965 66 psychotic disorders and Depixol® mild depression

Cis(Z)- Depot antipsychotic Maintenance treatment Fluanxol Depot®, Depixol® 1970 73 flupentixol- of chronic psychoticdecanoate disorders

Chlorprothixene Typical antipsychotic Schizophrenia and other Truxal®, Truxaletten® 1959 23 psychotic disorders, anxiety, restlessness, withdrawal symptoms in drug addicts

Facts about brain disorders Launched pharmaceuticals

Design: Bysted ASPrint: Quickly Tryk A/SMarch 2009

Parent company Denmark

Production DenmarkItalyMexico

Research DenmarkUSA

Sales EuropeAustriaBelgiumBulgariaCroatiaCzech RepublicDenmarkEstoniaFinlandFranceGermanyGreeceHungary

IcelandIrelandItalyLatviaLithuaniaNetherlandsNorwayPoland PortugalRomaniaSerbia and MontenegroSlovakiaSloveniaSpainSwedenSwitzerlandUK

Int. Markets ArgentinaAustraliaBelarusBrazilCanadaChileChina (incl. Hong Kong)

EgyptIndiaIndonesiaIsraelJapanMalaysiaMexicoPakistanPhilippinesRussiaSaudi ArabiaSingaporeSouth AfricaSouth KoreaTurkeyUkraineUnited Arab EmiratesVenezuela

USA

Institutes Lundbeck Institute

Countries are listed in accordance with Lundbeck’s market regions.

Lundbeck at a glanceSpecialtypharmaceuticalcompanyengagedinthedevelopmentofpharma-ceuticalsforthetreatmentofbraindisordersonthebasisofin-houseresearch.

Foundedin1915byHanslundbeck,thecompanywaslistedonthenasdaqOMXCopenhagenstockexchangein1999.

ThelundbeckFoundationisthelargestshareholder,own-ingabout70%oftheshares.In2008,thefoundationpaidoutDKK328millioninfundsforscientificresearch.

5,511employeesin55countries.

Approved for: Depression and anxietyRevenue in 2008: DKK 7,293m (+9%) Partner: Forest Laboratories, Inc. (Lexapro®)

Approved for: Alzheimer’s diseaseRevenue in 2008: DKK 1,879m (+14%)Partner: Merz Pharmaceuticals GmbH

Approved for: Parkinson’s diseaseRevenue in 2008: DKK 263m (+57%)Partner: Teva Pharmaceutical Industries Ltd.

Approved for: SchizophreniaRevenue in 2008: DKK 58m (+68%)

Approved for: InsomniaRevenue in 2008: Not reported Partner: Neurim Pharmaceuticals Ltd.

A total of ten products approved for the treatment of various brain disorders

Other pharmaceuticals

Products

Milestones

2008

Lu AA21004 In cooperation with our partner Takeda Pharmaceutical Company Ltd. the pivotal Phase III programme is expanded for Lu AA21004, which is Lundbecks most advanced compound in the field of depression and anxiety.

Circadin®The sleep agent Circadin® is launched in Germany and subsequently rolled out in a total of 12 markets during 2008.

New President and CEO Ulf Wiinberg is appointed as President and CEO from 1 June, after Claus Bræstrup. Ulf Wiinberg previously had strategic responsi-bility for biopharma activities in the US pharmaceutical company Wyeth and was overall responsible for Wyeth in Europe, Middle East, Africa and Canada.

Azilect®Lundbeck’s partner Teva Pharmaceutical Industries Ltd. announces results from the ADAGIO Phase III trial with Azilect®.

Michael J. Fox FoundationMichael J. Fox Foundation – established by US actor Michael J. Fox, who suffers from Parkinson’s disease – supports two of Lundbeck's early-stage research projects with a total amount of DKK 4.5 million.

Serdolect® in the USALundbeck submits a New Drug Application to the U.S. Food and Drug Administration (FDA) for Serdolect® for the treatment of schizophrenia. A reply from the authorities is expected in May 2009.

02 Towards new goals 04 Management’s review 08 The road ahead 10 Market

14 Products 18 Pipeline 22 Risk management 26 CSR

28 Share 32 Organisation 37 Executive Management

and Supervisory Board

41 Financial statements 103 Management statement

and Auditor’s report

COnTEnTS

PhotosThroughout this report we portray patients with brain disorders. See list of photos including descriptions on the back cover.

Lu AE58054Lundbeck initiates Phase II trials with Lu AE58054, which is being developed against schizophrenia and has shown an ability to improve patient’s cognition in preclinical trials.

DesmoteplaseLundbeck initiates a Phase III clinical trial with desmoteplase, which has the potential to improve treatment of patients with acute ischaemic stroke.

NalmefenePhase III clinical trials initiated with nalmefene, which can limit patient’s intake of alcohol.

Lu AA39959Lundbeck initiates Phase II trials with Lu AA39959, which is expected to demonstrate an effect in patients with bipolar disorder.

p8

p18

PipelineLundbeck is developing new and promising pharmaceuti-cals for the treatment of depression, anxiety and psychotic disorders and for new disease areas such as stroke and alcohol dependence.

The road ahead We have launched the project Decisions now and have defined five areas, where Lundbeck must develop in the years to come.

p2

Towards new goals ”The ambition for Lundbeck is to be the company that makes the biggest difference worldwide in the treatment of patients suffering from brain disorders”, says Ulf Wiinberg, President and CEO.

Udviklin

gssta

die

Registre

rings

Indik

ation

Stof

Virknin

gsmekanism

e

Fase

I

Fase

II

Fase

III

ansøgnin

g

Skizo

freni

Serd

olect

® USA

Dop

amin

/sero

tonin

Filed

Depres

sion/a

ngst

Lu A

A2100

4

Mon

oam

inerg

mod

ulato

r

2010

+

Skizo

freni

Bifep

runo

x

Dopam

in/se

roto

nin

2011

Alkoho

lafhæ

ngigh

ed

nalmefe

n

Spec

ifik opio

idrec

epto

ranta

gonis

t

2011

Slagt

ilfælde

Desm

otep

lase

Plasm

inoge

nakti

vato

r

2011

+

Psyk

ose

Lu 31

-130

Mon

oam

inerg

2011

+

Depres

sion

Lu A

A2453

0

Mult

iple t

arget

s

2011

+

Depres

sion/b

ipolar

lidels

e Lu

AA34

893

Mult

iple t

arget

s

2011

+

Psyk

ose

Lu A

E580

54

Selek

tiv 5-

HT 6 an

tago

nist

2011

+

Psyk

ose/

bipola

r lide

lse

Lu A

A3995

9

Ionka

nalm

odula

tor

2011

+

Slagt

ilfælde

/nerv

eska

de

Lu A

A2449

3

Vævsbe

skyt

tend

e cyt

okin

2011

+

neuro

logisk

e syg

dom

me

Lu A

A3846

6

Ionka

nalm

odula

tor

2011

+

PartnersPeople

ProductsPerformance

Pipeline

Selsk

abs-

Indbet

alt

Overfø

rt

kapita

l

overk

urs

resu

ltat

Egen

kapita

l1

DKK mio.

DKK mio.

DKK mio.

DKK mio.

Egen

kapita

l 01.0

1.2008

1.036,4

223,9

5.924,6

7.184,9

Årets

indre

gned

e indtæ

gter

og o

mko

stnin

ger

-

-

1.446,1

1.446,1

Udlodd

et ud

bytte

, bru

tto

-

-

(530

,6)

(530

,6)

Udlodd

et ud

bytte

, egn

e akti

er

-

-

26,6

26,6

Kapit

alned

sætte

lse og

annu

llerin

g af e

gne a

ktier

(52,0

)

-

52,0

-

Tilba

gekø

b af e

gne a

ktier

-

-

(538

,3)

(538

,3)

Incita

men

tspro

gram

mer

-

-

3,2

3,2

Øvrige

tran

sakt

ioner

(52,0

)

-

(987,1

)

(1.0

39,1)

Egen

kapita

l 31.1

2.2008

984,4

223,9

6.383,6

7.591,9

Egen

kapita

l 01.0

1.2007

1.060,8

121,6

5.582,4

6.764,8

Årets

indre

gned

e indtæ

gter

og o

mko

stnin

ger

-

-

1.808,9

1.808,9

Udlodd

et ud

bytte

, bru

tto

-

-

(333

,8)

(333

,8)

Udlodd

et ud

bytte

, egn

e akti

er

-

-

9,2

9,2

Kapit

alfor

højel

se ve

d udn

ytte

lse af

tegn

ingso

ption

er

5,0

102,3

-

107,3

Kapit

alned

sætte

lse og

annu

llerin

g af e

gne a

ktier

(29,4

)

-

29,4

-

Tilba

gekø

b af e

gne a

ktier

-

-

(1.19

1,3)

(1.19

1,3)

Incita

men

tspro

gram

mer

-

-

16,4

16,4

Skat

af øv

rige t

ransa

ktion

er i e

genk

apita

len

-

-

3,4

3,4

Øvrige

tran

sakt

ioner

(24,4

)

102,3

(1.4

66,7)

(1.3

88,8)

Egen

kapita

l 31.1

2.2007

1.036,4

223,9

5.924,6

7.184,9

Egen

kapita

l 01.0

1.2006

1.136,1

69,5

6.286,1

7.491,7

Årets

indre

gned

e indtæ

gter

og o

mko

stnin

ger

-

-

1.253,5

1.253,5

Udlodd

et ud

bytte

, bru

tto

-

-

(477

,2)

(477

,2)

Udlodd

et ud

bytte

, egn

e akti

er

-

-

32,7

32,7

Kapit

alfor

højel

se ve

d udn

ytte

lse af

tegn

ingso

ption

er

2,6

52,1

-

54,7

Kapit

alned

sætte

lse og

annu

llerin

g af e

gne a

ktier

(77,9

)

-

77,9

-

Tilba

gekø

b af e

gne a

ktier

-

-

(1.59

1,1)

(1.59

1,1)

Skat

af øv

rige t

ransa

ktion

er i e

genk

apita

len

-

-

0,5

0,5

Øvrige

tran

sakt

ioner

(75,3

)

52,1

(1.9

57,2)

(1.9

80,4)

Egen

kapita

l 31.1

2.2006

1.060,8

121,6

5.582,4

6.764,8

1) Eg

enka

pital

er lig

med

egen

kapit

al, H

. Lun

dbec

k A/S

’ akti

onærer

.

p41

Financial statements 2008Lundbeck’s financial

performance in detail.

2

Brain disorders such as depression, schizophre-nia and Alzheimer’s disease, to name but a few, inflict an immense amount of suffering on pa-tients, as well as sorrow and despair on their relatives.

Hundreds of millions of people in the world suffer from brain disorders. In spite of thera-peutic progress, unfortunately, we remain a long way from fully understanding these disor-ders. There are big unmet needs, not only for medication, but also for entire solutions in which therapy and updated information about the disorders are crucial factors.

Unfortunately, public awareness and the re-sources spent on curing and alleviating brain disorders are a long way from matching the severity and consequences of these disorders.

Brain disorders place an enormous economic burden on society, equal to the combined burden of cancer and cardiac disorders, in part because brain disorders reduce or eliminate the patient’s ability to work.

Thanks to the profound dedication and profes-sional capability of Lundbeck staff, the company currently enjoys worldwide respect for its efforts to combat some of these disabling diseases. I am therefore proud to have taken the helm at Lund-beck and to present my first annual report.

Biggest difference for patients The ambition for Lundbeck is to be the com-pany that makes the biggest difference world-wide in the treatment of patients suffering from brain disorders. We wish to be known as a growth company that attracts and retains the best employees.

We have launched the programme ‘Decisions now’ which will be the cornerstone in our

Towards new goals

3

next five years. At the same time, our presence in the USA will provide even greater opportu-nities for in-licensing new products.

With this acquisition and other decisions, the course for Lundbeck’s future is charted. There is still a great deal we need to achieve. But Lundbeck has previously proven its ability to develop some of the world’s best pharmaceu-ticals in our field. And we have the potential to do so again, for the benefit of patients, society, employees and shareholders.

Ulf WiinbergPresident and CEO

development over the next few years. The programme is incorporated throughout the company, while the responsibility for the activ-ities is placed in senior management. I will closely monitor the process to ensure that we accomplish our targeted progress.

Specifically, we aim to generate increased reve-nue through targeted investments in selected markets for instance by conducting new scien-tific investigations that can underline the strengths of our pharmaceuticals.

Concurrently, we will allocate extra resources to key projects in the pivotal development stage to maximise the return on the product launches we are facing.

We will source funding for the new activities partly by improving our organisation’s effi-ciency, including a close review of costs. Some of the changes will not materialise as fi-nancial improvements until after some time has passed. We can allow ourselves such initia-tives because our business is basically healthy and growing. But we have made the most im-portant decisions so that the changes will take full effect when we need them most.

New platform in the USA We have recently acquired Ovation Pharma-ceuticals, Inc. in the largest transaction in Lundbeck’s history. This deal fulfils one of our key strategic goals: to establish a commercial platform in the USA, the world’s largest phar-maceutical market.

This acquisition makes us a truly global player, and it brings us a number of new products and exciting pipeline projects that I look forward to pursuing. We may be able to launch several new products from our pipeline within the

Towards new goals

”The ambition for Lundbeck is to be the company that makes the biggest difference worldwide in the treatment of patients suffering from brain disorders.”

4

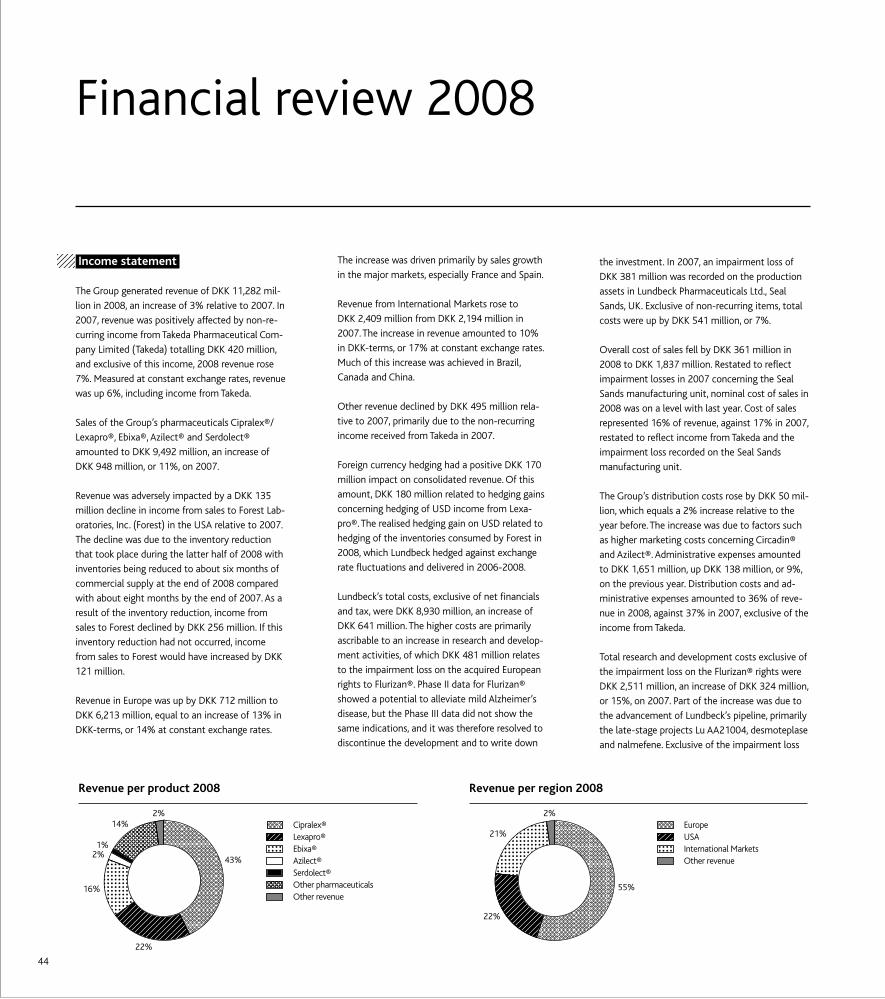

Lundbeck’s revenue continued to grow in 2008 to a record high of DKK 11,282 million. The improvement was primarily attributable to sales of Cipralex® and Ebixa® and was achieved in spite of our decision to reduce US inventories of Lexapro®, which decreased our sales income by DKK 256 million.

Profit from operations (EBIT) amounted to DKK 2,833 million, excluding non-recurring items, which translates into a growth of 7%.

The Supervisory Board finds the increase in revenue and profit from operations very satis-factory.

The income translates into an EBIT margin of 25%, excluding non-recurring items. We have been able to maintain the EBIT margin in spite of an increase in research and development costs from 21% of revenue in 2007 to 22% in 2008.

Including a DKK 481 million impairment loss on Flurizan®, profit from operations amounted to DKK 2,352 million in 2008, compared with DKK 2,695 million in 2007.

Group net investments amounted to DKK 439 million in 2008, excluding inlicensing and mile-stone payments, compared to DKK 630 million in 2007.

Cash flows from operating and investment ac-tivities amounted to DKK 2,193 million com-pared with DKK 1,610 million in 2007.

The Group’s financial performance was con-sistent with the guidance presented in the an-nual report for 2007.

The tax charge for 2008 was DKK 613 million, against DKK 792 million in 2007. The effective tax rate fell to 28.9% in 2008 from 30.9% in 2007.

Profit for the year amounted to DKK 1,510 million in 2008, compared with DKK 1,770 million in 2007.

The Supervisory Board will propose to the An-nual General Meeting that a dividend of 30% of net profit be paid for the year, correspond-ing to DKK 2.30 per share.

Pipeline progress Key pipeline projects are proceeding according to plan, and we initiated more Phase II and III clinical studies than ever before in Lundbeck’s history.

However, Phase III data with the in-licensed compound Flurizan®, developed by Myriad Ge-netics, Inc. for the treatment of Alzheimer’s disease, failed to live up to our expectations. The development of this compound was there-fore discontinued.

Lundbeck has submitted an application to the U.S. Food and Drug Administration (FDA) for the approval of Serdolect® for the treatment of schizophrenia, after having confirmed the efficacy, tolerability and safety of the com-pound through daily clinical practice in 40,000 patient years.

Lundbeck’s revenue rose to its highest-ever level in 2008. We have commenced more pivotal clinical trials than ever before, and continue to increase investments in research and development of new pharmaceuticals.

Management’s review

Revenue per product and region

Total Europe USA Int. MarketsDKKm 2008 2007 2008 2007 2008 2007 2008 2007

Total revenue 11,282 10,985 6,213 5,501 2,464 2,599 2,409 2,194 Growth 3% 13% -5% 10%

Cipralex® 4,829 4,094 3,355 2,827 - - 1,474 1,267 Growth 18% 19% - 16%

Lexapro® 2,464 2,594 - - 2,464 2,594 - - Growth -5% - -5% -

Ebixa® 1,879 1,655 1,557 1,359 - - 321 295 Growth 14% 15% - 9%

Azilect® 263 168 241 156 - - 22 11 Growth 57% 54% - 89%

Serdolect® 58 34 36 24 - - 22 11 Growth 68% 50% - 108%

Other pharmaceuticals 1,595 1,750 1,025 1,135 - 6 570 609 Growth -9% -10% - -6%

Other revenue 195 690 - - - - - - Growth -72% - - -

Forecast and profit 2008 (DKK)

Forecast Realised

Revenue 11-11.5 bn 11,282 m

Profit from operations (EBIT), excl non-recurring items 2.8-2.9 bn 2,833 m

Investments, excl. in-licensing and milestone payments Approx. 500 m 439 m

5

The FDA is expected to announce its decision in May 2009.

The compound nalmefene represents a novel regime for the treatment of alcohol depend-ence, and we have commenced the pivotal Phase III trials.

Correspondingly, we have initiated Phase III studies with desmoteplase, which holds new perspectives in the treatment of stroke.

The Phase III programme with Lu AA21004, our most advanced project in depression and anxiety, progressed as scheduled throughout 2008. By the end of the year, Lundbeck had tested Lu AA21004 in 14 clinical trials in de-pression and anxiety in cooperation with Takeda Pharmaceutical Company Ltd. (Takeda).

Furthermore, the recruitment of patients for the Phase II study with another compound, Lu AA24530, proceeded according to plan. This compound is also being co-developed with Takeda.

Lundbeck has decided to initiate Phase II stud-ies of the compounds Lu AA34893 and Lu AA39959 for the treatment of bipolar disorder

Lundbeck’s operations nor its financial position were adversely affected by the global eco-nomic crisis in 2008.

At present, however, we cannot rule out that Lundbeck may be affected. Our financial guid-ance for 2009 is presented with the reserva-tion that the future scope of the economic crisis remains unknown and that our expecta-tions are based exclusively on the knowledge we have today.

On 9 February 2009, Lundbeck announced that the company is acquiring the US com-pany Ovation Pharmaceuticals, Inc. (Ovation). The acquisition of Ovation is subject to the approval of the US competition authorities, which is expected to be granted in March 2009. Consequently, the financial guidance provided at this time only includes Lundbeck.

(manic depression), which is a complicated – and until now underserved – disease area.

The pipeline has been expanded by the Phase II compound Lu AE58054, which is being de-veloped for treatment of schizophrenia and has demonstrated an ability to improve cogni-tion in preclinical trials. The second pipeline addition is the Phase I compound Lu AA38466, which has shown a potential in the treatment of neurological disorders.

In 2008, we discontinued three Phase I projects: Lu AA44608 for the treatment of mood disorders, Lu AA47070 for the treatment of neurological disorders and Lu AA37096 for the treatment of mood and anxiety disorders.

Overall, Lundbeck’s pipeline now consists of 12 projects in psychiatric and neurological disor-ders. Four of these projects are in pivotal Phase III, five projects are in Phase II and two projects are in Phase I. A registration application for the last compound is currently being evaluated by the FDA.

Outlook for 2009 The pharmaceutical industry is inherently less cyclical than most other industries. neither

Disclaimer Forward-looking statements are sub-ject to risks, uncertainties and inaccu-rate assumptions. This may cause ac-tual results to differ materially from expectations.

Factors that may affect future results include interest rate and exchange rate fluctuations, delay or failure of

development projects, production problems, unexpected contract breaches or terminations, govern-ment-mandated or market-driven price decreases for Lundbeck’s prod-ucts, introduction of competing prod-ucts, Lundbeck’s ability to successfully market both new and existing prod-ucts, exposure to product liability and

other lawsuits, changes in reimburse-ment rules and governmental laws and related interpretation thereof and unexpected growth in expenses.

Pursuant to section 107a of the Dan-ish Financial Statements Act, listed companies are under an obligation to consider whether they wish to

disclose whether material agreements will be affected in the event of a change of control of the company. For reasons of competition, Lundbeck does not wish to disclose this.

Outlook 2009 (DKK)

Revenue 12-12.5 bn

Profit from operations (EBIT) 3.0-3.2 bn

Research and development 23-24% of revenue

6

The financial guidance for 2009 includes an in-come of DKK 124 million concerning the di-vestment of shares in LifeCycle Pharma A/S to LFI a/s (The Lundbeck Foundation) at the be-ginning of 2009.

Lundbeck expects that revenue for 2009 will rise to DKK 12-12.5 billion, and that profit from operations (EBIT) will amount to DKK 3.0-3.2 billion.

Lundbeck will increase spending on research and development, which is expected to ac-count for 23-24% of revenue in 2009.

Events reported after the end of the financial year On 9 February 2009, Lundbeck announced that the company will acquire Ovation for up to USD 900 million, or DKK 5.2 billion, through its wholly owned subsidiary Lundbeck, Inc.

The acquisition of Ovation fulfils Lundbeck’s strategic goal to build a commercial infrastruc-ture in the USA. Ovation is a profitable and fast-growing company, with a broad portfolio of marketed products and an attractive pipe-line of new, innovative products primarily fo-cused on brain disorders.

The pipeline is expected to drive growth signifi-cantly in the coming years through multiple new product launches.

Following the transaction, Lundbeck will have a diverse portfolio of marketed products and a broader pipeline primarily focused on brain disorders.

Pending final approvals and antitrust clear-ances, closing of the transaction is expected totake place in March 2009. A thorough discus-sion of the influence of Ovation on Lundbeckis not included in the annual report for 2008.

7

1. korrektur 9/2-09

8

Based on our long-standing experience and unique focus as a research-based company in the field of brain disorders, our goal is to help patients by being specialists and developing new and innovative pharmaceuticals. We aim to be a healthy and growing business, and an attractive place to work, to partner, and to in-vest in - for employees, for the surrounding community, and for our shareholders, respec-tively.

Focus on brain disorders Lundbeck believes there is a great potential in focusing on brain disorders. Valued at more than DKK 600 billion, the market for pharma-ceuticals to treat brain disorders is the world’s largest pharmaceutical therapy area. With its existing products or clinical development projects, Lundbeck currently has activities in about half the market. In other words, the market for pharmaceuticals for the treatment of brain disorders is huge and offers strong growth and promising potential.

Lundbeck remains open to expanding its focus to include other brain disorders, as opportuni-ties arise from new discoveries in our own re-search laboratories, or from the acquisition of new projects or pharmaceuticals.

With the acquisition of Ovation Pharmaceuti-cals, Inc. (Ovation), Lundbeck diversifies its treatment offers and obtains a commercial platform in the USA, which is the world’s larg-est pharmaceutical market by far. north Ame-rica represents 57% of the global market for pharmaceuticals for brain disorders, and Lund-beck has aimed to establish an independent commercial presence in this market for a number of years. With the acquisition, we be-lieve that the US market will offer good growth potential in the years ahead.

Five priority areas Lundbeck currently has leading pharmaceuti-cals that can continue to provide growth rates in the years ahead. Furthermore, we have inno-vative pharmaceutical candidates in our pipe-line that will represent growth drivers in the medium and long-term. In order to accomplish our ambition to become the company that makes the biggest difference worldwide for pa-tients with brain disorders, we have defined five strategic focus areas, each of which will contribute to Lundbeck’s progress.

The ‘Decisions now’ programme is incorpo-rated throughout the company. Progress in the

Representing 28% of the global market, Eu-rope has been Lundbeck’s domestic market for many years. In this region, Lundbeck has a fully developed sales infrastructure for marketing pharmaceuticals.

Over the past few years, Lundbeck has in-creased its presence in the International Mar-kets region, which accounts for 15% of the global market. We currently have a presence in most relevant countries in the International Markets region. We will continue to expand our presence in all markets in which we expect increasing proliferation of medication for the treatment of brain disorders.

Lundbeck’s road aheadLundbecks long term objective is to become the company that makes the biggest difference worldwide for patients with brain disorders. We have launched the project Decisions now and have defined five areas, where Lundbeck must develop in order to succeed.

Decisions now

People Performance

Partners

Pipeline

ProductsBest company

in the treatment of brain disorders

9

Performance – Increasing efficiency and reducing costs We aim to release resources for investments in other areas in Decisions now by making our organisation more efficient. The objective is to review processes, systems and procurement in the company.

People – Developing a high performance culture and ensuring consistent targets A prerequisite for accomplishing the above-mentioned ambitions, launching value-adding initiatives, and increasing earnings is that our organisation is geared towards these chal-lenges. Our company and employees must be characterised by a high performance mentality in which cooperation, willingness and ability to change, innovative skills and drive are the pro-pelling force.

underlying projects aimed at creating the im-provements will be monitored closely by senior management, who has the ultimate responsibility. Products – Achieving full potential of marketed pharmaceuticals Lundbeck’s existing pharmaceuticals offer a substantial growth potential. Management has identified measures to achieve this potential and increase revenue growth in the years to come. Moreover, the expected growth in Ova-tion sales will provide revenue that will more than offset the expected revenue decrease from Lexapro® following patent expiry in the US in 2012.

Pipeline – Maximising the value of new and innovative pharmaceuticals Lundbeck currently invests more than 20% of its revenue in research and development. Inno-vation and medical improvements represent the cornerstone of our strategy. Our high level of investment will continue to strengthen and broaden our pipeline, with the aim of generat-ing the major part of long-term growth. The latest investment increase target the compa-ny’s late-stage projects in order to accelerate development and maximise the value of the projects. Following the acquisition of Ovation, Lundbeck has the potential to launch several new pharmaceuticals over the next five years.

Partners – Intensifying growth through business development and partnerships In-licensing activities, acquisitions and part-nerships will continue to be a part of Lund-beck’s strategy. We have defined targets for business development, and having established a commercial platform in the USA we will also be seeking products and development projects in the US market. In addition, we will review our existing partnership agreements, seeking to maximise the opportunities.

The market for pharmaceuticals for the treatment of patients with brain disorders is growing, and there is a great need for improving the existing treatment options.

Lundbeck is engaged in a single therapeutic area: brain disorders, which are also referred to as dis-orders of the central nervous system (CNS). Lundbeck is the only company in the world that focuses exclusively on brain disorders and is fully integrated, which means that we cover the entire value chain, from research and develop-ment to production, marketing and sales.

Over the past few years, the market for phar-maceuticals for brain disorders has grown con-siderably, currently representing a value of just over DKK 600 billion. This makes it the world’s largest pharmaceutical therapy area, even larger than cardiovascular diseases. Lundbeck’s reve-nue accounts for about 2% of the total market for pharmaceuticals for brain disorders. This market therefore holds significant growth po-tential.

Depression and psychotic disorders represent the two largest markets within brain disorders. With the pharmaceuticals currently marketed by Lundbeck and the pharmaceutical candi-dates we are developing, Lundbeck is active in about 50% of the market for brain disorders.

The growth recorded in the market for phar-maceuticals for the treatment of brain disor-ders underlines the huge need for more effec-

tive medication with fewer side effects. Although we have come a long way, unmet needs – and thus growth potential – exist in the field of psychiatric disorders such as de-pression and psychotic disorders, as well as in neurological disorders such as Alzheimer’s and Parkinson’s diseases.

The shortcomings of the treatments currently available for patients with brain disorders can cause great suffering for patients and their relatives, resulting in huge costs for society.

The World Health Organization (WHO) has estimated which diseases cause the largest global losses in quality of life. The figures show that, next to cancer, depression/anxiety is the most burdensome illness.

Brain disorders are complex and difficult to understand, and although we can expect sub-stantial progress in treatments, brain disorders will continue to cause a great deal of societal loss and suffering.

Market

10

The world’s most burdensome illnesses

1. Cancer2. Depression and anxiety3. Ischaemic heart disease4. Cerebrovascular disease5. Chronic obstructive pulmonary disease6. Refractive errors in the eye7. Hearing loss8. Congenital anomalies9. Alcohol abuse10. Diabetes mellitus11. Cataracts12. Schizophrenia13. Asthma

14. Osteoarthritis15. Bipolar disorder16. Liver cirrhosis17. Dementia18. Endocrine disorders19. Macular degeneration 20. Nephritis and nephrosis21. Drug abuse22. Hypertensive heart disease23. Epilepsy24. Migraine25. Rheumatic heart disease

Note: DALY (disability adjusted life years), except infectious diseases.Source: Lundbeck and WHO World Health Report 2004.

1. korrektur 9/2-09

11

By 2030, depression, Alzheimer’s disease and alcohol-related disorders are expected to be among the five diseases that constitute the greatest burden on society in the world’s high-income countries.(1)

Depression and anxiety WHO estimates that about 150 million people around the world suffer from depression. The market for pharmaceuticals for the treatment of depression represents approximately DKK 107 billion. Measured in terms of value, the market is declining because a number of branded products have lost their patent pro-tection and cheaper generic versions have been launched. Measured in terms of volume, global usage is growing as more and more pa-tients are diagnosed. It is estimated that about half of the people suffering from depression currently receive treatment. It is also esti-mated that, until 2016, the number of people receiving treatment for depression will grow by 2-3% each year in the USA and Europe.(2)

Although treatments with antidepressants have improved significantly since the first generation of therapeutics was launched in the 1960s, substantial unmet needs persist.

The US market accounts for more than 60% of the global antipsychotics market. The reason is especially that more than 85% of patients in the USA receive the latest antipsychotics (the so-called atypical pharmaceuticals), which cause fewer side effects than older therapeu-tics. In Europe, only about 55% of patients re-ceive the latest generation of drugs; 45% are treated with older and cheaper pharmaceuti-cals developed as long as 50 years ago.

Although treatments for psychotic disorders have improved, a considerable need for better therapies persists. According to WHO, the greatest unmet treatment needs include the fact that only one-third of treated patients be-come symptom-free and capable of function-ing in daily life. This limited effect, combined with adverse effects, result in many patients changing antipsychotics or discontinuing their treatment. Thus, future treatments need to be more efficacious, especially in the treatment of the cognitive dysfunction and so-called nega-tive symptoms, such as isolation and lack of initiative. In addition, new pharmaceuticals should have fewer side effects, and patients would benefit greatly from a faster diagnosis and quicker treatment start.

The priority areas are improved efficacy, faster onset of action and fewer side effects.

Antidepressants represent an effective treat-ment for 50-70% of depressed patients, but it takes time for the effect of the treatment to set in – often up to three or four weeks. The delayed efficacy makes some patients discon-tinue their treatment prematurely. Further-more, it is not unusual for patients to have to try several different treatments before they ex-perience a beneficial effect.

Lundbeck expects to play a decisive role in the future treatment of depression. The launch of new and innovative pharmaceuticals can cre-ate substantial value for the company in the medium and long-term.

Psychotic disorders The market for pharmaceuticals for the treat-ment of patients with psychotic disorders is currently the largest CnS area in terms of value, representing DKK 113 billion. IMS esti-mates, that the value of the market for antip-sychotics will grow by about 2% per annum until 2013. Accordingly, there is a substantial market potential for Lundbeck to develop and launch new antipsychotic pharmaceuticals.

(1) Mathers & Loncar, 2006 (2) COGnOS Study #4 - Major depressive disorder, December 2007

12

Parkinson’s disease The global market for pharmaceuticals to treat patients with Parkinson’s disease represents a value of approximately DKK 20 billion. There is a large number of pharmaceuticals on the market, including many generics that offer symptomatic treatment in the various stages of the disease. The most commonly used com-pound is levodopa, which was developed more than 40 years ago. Since then, additional phar-maceuticals have been launched, aimed at op-timising the treatment at the various stages (some of these compounds are used in combi-nation with levodopa).

In a large clinical trial, Lundbeck’s partner Teva Pharmaceutical Industries, Ltd. has shown that Azilect® is the only pharmaceutical capable of slowing the progression of Parkinson’s disease.

The number of patients being treated is ex-pected to grow by about 3% per annum until 2017(3). Lundbeck believes that the Parkinson’s market will offer a great potential in the years ahead.

Alzheimer’s disease The market for pharmaceuticals for the treat-ment of patients with Alzheimer’s disease rep-resents a value of approximately DKK 31 bil-lion and is a market that continues to grow strongly. The 21% increase in 2007 was prima-rily due to the launch of new pharmaceuticals.

The probability of being afflicted by Alzheim-er’s disease increases sharply with age.

Whereas only 0.1% of those aged under 65 get the disease, 4% in the age between 65 and 90 and 25% of those over 90 years are affected.

The number of patients being treated for Alzheimer’s disease is expected to grow by about 5% per annum in the USA and 6% in Europe until 2017(4).

Lundbeck believes that the Alzheimer’s market is attractive both in the short and long-term.

Insomnia The market for pharmaceuticals to treat in-somnia and other related disorders is valued at approximately DKK 27 billion. Insomnia is an under-served area in which the major unmet needs are the ability to normalise sleep and reduce tiredness symptoms the following day.

Insomnia is estimated to affect about one-quarter of the population. Lundbeck believes that insomnia is an attractive market and will continue to assess new opportunities.

Stroke The current market for pharmaceuticals for the treatment of ischaemic stroke is relatively small. Today, medicine is only approved for use within the first three hours after a stroke has occurred. But because strokes typically occur during sleep and patients must be scanned prior to treatment to rule out a possible brain haemorrhage, about 80% of all ischaemic stroke patients are never treated.

In the USA alone, approximately 700,000 peo-ple suffer an ischaemic stroke each year, and 8-12% of them die within 30 days. In the USA, the American Heart Association estimates the financial burden of stroke from hospitalisation costs, long-term care programmes and produc-tivity losses to have reached approximately DKK 360 billion in 2008.

Consequently, new and better treatment op-tions that offer a longer time window after the stroke occurs would offer substantial benefits to patients compared with today. It could also expand the market significantly, making it very attractive for Lundbeck.

Alcohol abuse It is estimated that up to 60 million Europeans consume hazardous amounts of alcohol and that only 10% of all alcoholics receive treat-ment. Consequently, new treatment options that offer patients the possibility of reducing their alcohol consumption to a non-hazardous level would contribute to improving the treat-ment. In addition, new treatment options may reduce some of the huge losses to society caused by excess consumption of alcohol.

The market for the treatment of alcohol abuse is relatively small. Lundbeck believes there is substantial market potential if the company can successfully develop a new treatment con-cept dedicated to reducing excess consump-tion.

(3) COGnOS study #8 - Parkinson’s disease, June 2008. (4) COGnOS study #6 - Alzheimer’s disease, June 2008.

13

Disease Total North America Europe Rest of world DKK bn % of total DKK bn % of total DKK bn % of total DKK bn

Depression 2006 111.9 67% 75.3 22% 24.3 11% 12.3

(n6A) 2007 107.4 62% 66.5 25% 26.8 13% 14.2

Growth -4% -12% 10% 15%

Psychotic 2006 99.1 65% 64.4 24% 24.1 11% 10.6

disorders 2007 112.9 64% 71.9 26% 28.8 11% 12.2

(n5A) Growth 14% 12% 20% 15%

Parkinson’s 2006 17.1 35% 5.9 43% 7.3 23% 3.9

disease 2007 20.3 36% 7.3 44% 8.9 21% 4.2

(n4A) Growth 19% 23% 22% 7%

Alzheimer’s 2006 25.3 55% 14.0 30% 7.6 15% 3.8

disease 2007 30.7 54% 16.6 30% 9.3 16% 4.8

(n7D) Growth 21% 18% 23% 27%

Insomnia * 2006 29.6 67% 19.8 18% 5.3 15% 4.5

(n5B) 2007 27.2 61% 16.6 22% 5.9 17% 4.7

Growth -8% -16% 12% 4%

Alcohol abuse 2006 0.8 28% 0.2 55% 0.4 18% 0.1

(n7E) 2007 0.9 36% 0.3 53% 0.5 11% 0.1

Growth 22% 58% 19% -27%

Total CNS 2006 552.7 59% 326.1 27% 147.0 15% 80.1

(n) 2007 608.0 57% 345.3 28% 172.1 15% 90.6

Growth 10% 6% 17% 13%

Stroke 2006 n.a. n.a. n.a. n.a.

(B1D) 2007 4.0 49% 2.0 32% 1.3 19% 0.8

Growth - - - -

* Insomnia and related diseasesSource: IMS World Review 2007, 2008

Market values

14

In 2008, sales of Lundbeck’s pharmaceuticals continued to grow and exceeded DKK 11 billion for the first time.

In the Decisions now programme, we have identified a number of measures aimed at accelerating sales growth. Some of these

measures may have an impact already in 2009, whilst others will emerge over a longer period of time.

Lundbeck divides its markets into: Europe, USA and International Markets.

Cipralex®/Lexapro® (escitalopram) Depression and anxiety Cipralex®/Lexapro® for the treatment of de-pression and anxiety was launched in 2002 and is the most frequently prescribed branded antidepressant in Europe and the USA. Lund-beck is marketing Cipralex® in 93 countries. In the USA, Lexapro® is marketed by Forest Labo-ratories, Inc. (Forest), and Lundbeck receives royalties from the sales. To date, more than 160 million patients worldwide have been treated with escitalopram, the active pharma-ceutical ingredient.

Over the past few years, the Cipralex® profile has gradually been strengthened as additional clinical data have been published. A number of randomised clinical trials have demonstrated that Cipralex® is efficacious both in short-term and long-term treatment of depression, whilst also offering a good safety profile. Further-more, other clinical trials have demonstrated the therapeutic benefits of using Cipralex® in

comparison with other antidepressants in the treatment of both depression and anxiety.

By the end of 2008, Cipralex® commanded 16.8% of the European market for antidepres-sants (15.2% in 2007). Lexapros® market share in the US grew to 22.9% (22.7% in 2007). In the International Markets region, the market share of Cipralex® was 10.8% in Q3 2008, which is the most recent period for which figures are available (9.4% in Q3 2007).

In the years ahead, Lundbeck intends to step up its marketing efforts for Cipralex®, partly based on new knowledge that has come to light since the original launch, but also on the basis of the expected results of a number of new clinical trials. Lundbeck currently supports 16 ongoing trials.

Furthermore, Lundbeck wishes to maximise its combined sales and distribution capabilities. This may be achieved by optimising the size of the sales force relative to the market potential in the individual countries.

In the USA, Forest has filed a registration ap-plication for the use of Lexapro® for adoles-cents and expects to receive approval in the spring of 2009. Forest has indicated that the

Lundbeck continues to sell pharmaceuticals in new markets and to capitalise on the strength of the products to increase market shares in existing markets.

Products

Total revenue

DKKm 2008 2007 Growth Growth*

Europe 6,213 5,501 13% 14%

USA 2,464 2,599 -5% -2%

Int. Markets 2,409 2,194 10% 17%

Other** 195 690 -72% -72%

Total 11,282 10,985 3% 6%

* Local currency ** Other revenue

Revenue Cipralex®/Lexapro®

DKKm 2008 2007 Growth Growth*

Europe 3,355 2,827 19% 21%

USA** 2,464 2,594 -5% -2%

Int. Markets 1,474 1,267 16% 24%

Total 7,293 6,688 9% 13%

* Local currency ** Lundbeck’s income from sales of Lexapro®

“From 2009 onwards, we will dedicate extra resources to sales-promoting projects in the markets where we believe there is room for improvement.”

Stig Løkke Pedersen, Executive Vice President, Commercial Operations

1. korrektur 9/2-09

15

company expects additional sales of approxi-mately DKK 550 million from this new indication.

In Canada, we expect to see a continued posi-tive effect after Cipralex® became eligible for reimbursement in the Province of Ontario, and the product is expected to become eligible for reimbursement in other provinces as well.

Ebixa® (memantine) Alzheimer’s disease Ebixa®, Lundbeck’s second best-selling pharma-ceutical, was in-licensed from Merz Pharmaceu-ticals GmbH in Germany in 2002, and is now marketed by Lundbeck in 57 countries world-wide. Lundbeck is marketing Ebixa® in more or less all parts of the world, excluding the USA and Japan. Memantine, the active pharmaceuti-cal ingredient in Ebixa®, is the second most pre-scribed pharmaceutical in the world for treating patients with Alzheimer’s disease.

In a number of clinical trials, Ebixa® has shown to be efficacious and demonstrated a strong safety profile in patients with moderate to se-vere Alzheimer’s disease. Compared with pla-cebo, treatment with Ebixa® offers patients stabilisation or less marked worsening on three important domains: cognition, daily function-ing and behaviour.

In addition to being effective and easy to ad-minister, Azilect® is well-tolerated by patients and has only few adverse effects.

By the end of 2008, Azilect® represented 6.5% of total European sales of pharmaceuticals to treat patients with Parkinson’s disease (4.6% in 2007). Because Azilect® has only been launched in a single country in the International Markets region, revenue here is very modest.

In August 2008, Lundbeck’s partner Teva announced positive results from the Azilect® ADAGIO Phase IIIb study, one of the largest studies ever conducted for Parkinson’s disease with 1,176 patients. Azilect® met all three endpoints of the primary analysis, as well as the secondary endpoint - all with statistical significance.

The results demonstrate that early treatment with Azilect® slows the progression of Parkin-son’s disease and indicate that early treatment with Azilect® could modify the course of the disease. Delaying disease progression is one of the most important unmet needs in the treat-ment of patients with Parkinson’s disease.

One of Lundbeck’s key priorities is to ensure that the ADAGIO data is presented in all relevant

At the end of 2008, Ebixa® commanded 16.0% of the European market for anti-Alzheimer’s agents (15.9% in 2007). In the International Markets region, the market share of Ebixa® was 10.9% in Q3 2008 (10.8% in Q3 2007).

Lundbeck has also identified a number of measures to boost sales growth of Ebixa®. In a number of countries, the goal is to in-crease awareness among healthcare providers and to exploit Ebixa’s greater efficacy relative to competing products. In addition, Lundbeck is developing a promising dispenser, and our continuing focus on the medication being administered only once daily will promote its use, mainly among patients with moderate Alzheimer’s disease.

Finally, a number of trials due to be completed in 2009 and 2010 may create new market po-tential, depending on the results.

Azilect® (rasagiline) Parkinson’s diseaseAzilect® has been in-licensed from Teva Phar-maceutical Industries Ltd. (Teva), and is used both as monotherapy and in combination treatments of patients with Parkinson’s dis-ease. Azilect® was launched in the first Euro-pean market in 2005. Lundbeck is now market-ing Azilect® in 29 countries.

Revenue Ebixa®

DKKm 2008 2007 Growth Growth*

Europe 1,557 1,359 15% 15%

Int. Markets 321 295 9% 15%

Total 1,879 1,655 14% 15%

* Local currency

Revenue Azilect®

DKKm 2008 2007 Growth Growth*

Europe 241 156 54% 56%

Int. Markets 22 11 89% 103%

Total 263 168 57% 59%

* Local currency

1. korrektur 9/2-09

16

forums and make sure that healthcare provid-ers and other stakeholders become aware of the product’s qualities. The purpose is to pro-vide patients with a possibility of taking Azi-lect® at an earlier stage and increase its use as monotherapy.

Serdolect® (sertindole) Schizophrenia The result of Lundbeck’s in-house research, Serdolect® is an effective antipsychotic drug for the treatment of schizophrenia without sedative effect and with placebo-level extra pyramidal side effects (e.g. slow movements and tremors).

The clinical and pharmacological profile of Serdolect® shows that the pharmaceutical may increase the likelihood of patients re-maining on therapy, which will increase the quality of life for patients and relatives alike.

Lundbeck holds the global rights to Serdolect®, which has been on the market since the begin-ning of 2006. By the end of 2008 we had rolled out Serdolect® in 38 markets.

In 2008, Lundbeck submitted a new Drug Ap-plication to the U.S. Food and Drug Adminis-tration (FDA) for Serdolect® for the treatment

of schizophrenia. In September, the FDA com-pleted its initial check for completeness and accepted the application. Serdolect® may thus potentially become a new treatment option for patients with schizophrenia in the USA. On receiving feedback from the FDA, Lundbeck will decide finally on a launch of Serdolect®.

Circadin® (melatonin) Primary insomniaIn 2007, Lundbeck in-licensed Circadin® for the treatment of primary insomnia from neu-rim Pharmaceuticals Ltd. with rights to about 80% of the European market and to a number of other markets.

Circadin® was approved by the European Medi-cines Agency (EMEA) in June 2007 as mono-therapy for the short-term treatment of primary insomnia in patients aged 55 or over. Circadin® mimics the normal nocturnal profile of the hor-mone melatonin, which has a pivotal role in the regulation of circadian rhythms and sleep.

In 2008, Lundbeck launched Circadin® in 12 markets across Europe.

Lundbeck’s primary focus in respect of Circadin® is to continue the process of launching, market-ing and selling the product in Europe.

Revenue Serdolect®

DKKm 2008 2007 Growth Growth*

Europe 36 24 50% 47%

Int. Markets 22 11 108% 120%

Total 58 34 68% 70%

* Local currency

“In 2009, we will review all parts of our organisation with the aim of identifying areas in which we can release funds for securing long-term growth.”

Lars Bang, Executive Vice President, Supply Operations & Engineering

17

1. korrektur 9/2-09

18

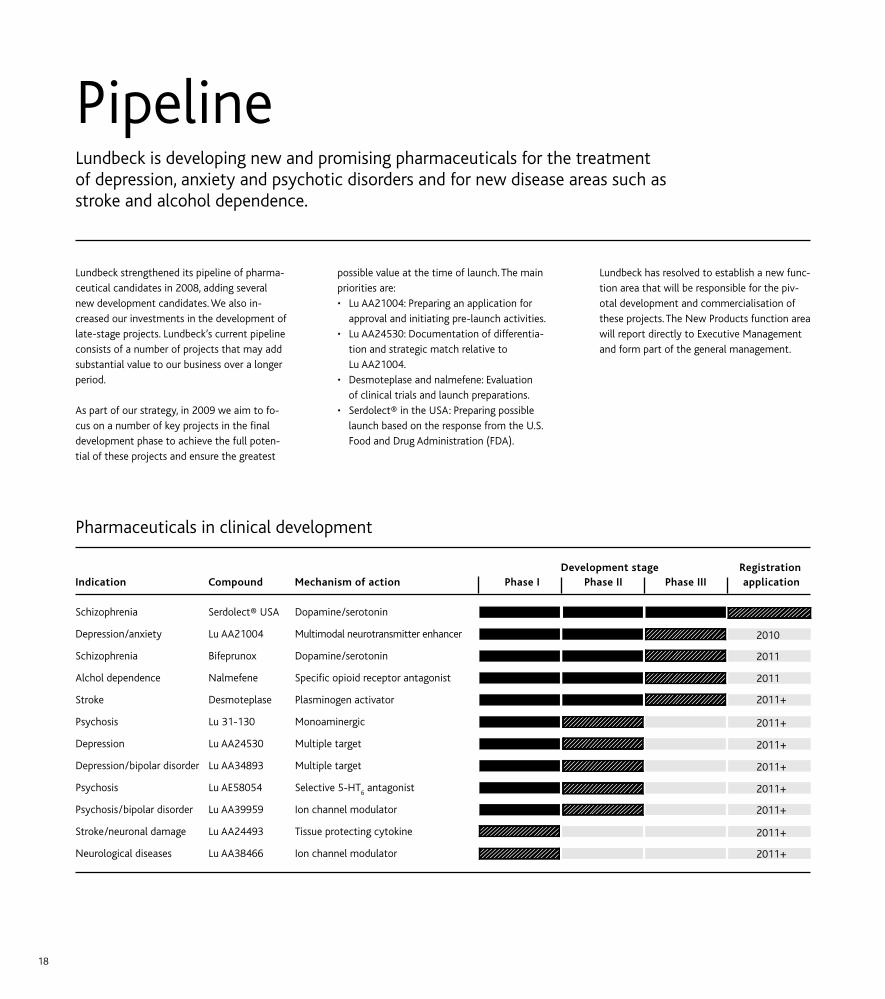

Lundbeck strengthened its pipeline of pharma-ceutical candidates in 2008, adding several new development candidates. We also in-creased our investments in the development of late-stage projects. Lundbeck’s current pipeline consists of a number of projects that may add substantial value to our business over a longer period.

As part of our strategy, in 2009 we aim to fo-cus on a number of key projects in the final development phase to achieve the full poten-tial of these projects and ensure the greatest

possible value at the time of launch. The main priorities are:• Lu AA21004: Preparing an application for

approval and initiating pre-launch activities. • Lu AA24530: Documentation of differentia-

tion and strategic match relative to Lu AA21004.

• Desmoteplase and nalmefene: Evaluation of clinical trials and launch preparations.

• Serdolect® in the USA: Preparing possible launch based on the response from the U.S. Food and Drug Administration (FDA).

Lundbeck has resolved to establish a new func-tion area that will be responsible for the piv-otal development and commercialisation of these projects. The new Products function area will report directly to Executive Management and form part of the general management.

Lundbeck is developing new and promising pharmaceuticals for the treatment of depression, anxiety and psychotic disorders and for new disease areas such as stroke and alcohol dependence.

Pipeline

Pharmaceuticals in clinical development

Development stage RegistrationIndication Compound Mechanism of action Phase I Phase II Phase III application

Schizophrenia Serdolect® USA Dopamine/serotonin

Depression/anxiety Lu AA21004 Multimodal neurotransmitter enhancer 2010

Schizophrenia Bifeprunox Dopamine/serotonin 2011

Alchol dependence nalmefene Specific opioid receptor antagonist 2011

Stroke Desmoteplase Plasminogen activator 2011+

Psychosis Lu 31-130 Monoaminergic 2011+

Depression Lu AA24530 Multiple target 2011+

Depression/bipolar disorder Lu AA34893 Multiple target 2011+

Psychosis Lu AE58054 Selective 5-HT6 antagonist 2011+

Psychosis/bipolar disorder Lu AA39959 Ion channel modulator 2011+

Stroke/neuronal damage Lu AA24493 Tissue protecting cytokine 2011+

neurological diseases Lu AA38466 Ion channel modulator 2011+

19

Depression and anxiety Lundbeck has been one of the world’s trend-setting companies in the field of depression and anxiety for more than 40 years and cur-rently has three new compounds in Phase II and Phase III development.

We aim to develop pharmaceuticals that ad-dress the medical needs – first and foremost better efficacy and faster onset of action – without causing more side effects. If our devel-opment programmes are successfully com-pleted, all three compounds could be approved and launched during 2011-2014.

Lu AE58054 improves the efficacy of other anti-psychotics. Consequently, Lundbeck ex-pects that Lu AE58054 will improve the daily functioning of patients with schizophrenia and, for example, will improve their ability to solve practical problems in their daily lives. The trial consists of 120 patients, and preliminary re-sults are expected by the end of 2009.

In an ongoing Phase IIa trial with Lu 31-130, preliminary clinical results are positive. Lu 31-130 is expected to show efficacy in both positive and negative symptoms in schizophre-nia combined with a low risk of extrapyramidal side effects (motor disturbances). In 2008, Lundbeck initiated a Phase IIb trial in which Lu 31-130 is compared with the compound olan-zapine. Lundbeck expects to report results from this trial in the second half of 2009.

Psychotic disorders/bipolar disorder Lundbeck has initiated Phase II clinical trials with the compound Lu AA39959, which is a first-in-class compound. Preclinical studies have shown anti-psychotic and anti-depres-sant-like effects. Lundbeck expects that Lu AA39959 will show clear and convincing effects in patients with bipolar disorder (manic depression) and is likely to have additional positive features such as a low switch rate to mania. The Phase II study is placebo-controlled and includes 180 patients with bipolar I or II disorder.

Lu AA34893 is being investigated in Phase II trials as a treatment for both bipolar disorder and depression.

Lu AA21004 is the most advanced compound in the development of a new class of pharma-ceutical candidates for the treatment of pa-tients with depression and anxiety. By the end of 2008, the Phase III programme included 14 trials. nine of these trials focus on the treat-ment of depression, while five focus on the treatment of generalised anxiety. Lundbeck ex-pects that the combined Phase III programme will include more than 5,000 patients.

Lu AA24530 also belongs to a new class of antidepressants. Development is progressing as planned, and the ongoing Phase II studies are expected to be completed during the first half of 2009.

The above two projects, which are being co-developed with Japanese Takeda Pharmaceuti-cal Company Ltd., and Lu AA34893 cover the entire differentiated range of mood disorders.

Psychotic disorders/schizophrenia Lundbeck and Solvay Pharmaceuticals, B.V. have initiated two Phase III clinical trials with bifeprunox for maintenance treatment of schizophrenia. Recruitment of patients for the two trials is progressing as planned. Each trial will enrol about 450 patients, who will be treated for 12 months. Results from the trials are expected to be announced in the second half of 2010.

In 2008, Lundbeck initiated Phase II trials with Lu AE58054, which was acquired through the acquisition of US biotech company Saegis Pharmaceuticals, Inc. in 2006. In preclinical trials, the compound has documented its abil-ity to improve cognition. Lu AE58054 affects other areas of the brain than other anti- psychotics. Animal trials have shown that

“We have never before initiated as many large clinical trials as we did in 2008. In 2009, our key challenge is to prepare the upcoming product launches.”

Anders Gersel Pedersen, Executive Vice President, Drug Development

20

Acute ischaemic stroke Lundbeck has initiated a Phase III trial with desmoteplase for the treatment of acute is-chaemic stroke, in which the blood supply to part of the brain is interrupted.

Desmoteplase is a modified version of a clot-dissolving protein used by the vampire bat Desmodus rotundus to prevent the blood of its prey from clotting. The compound has received fast-track designation from the U.S. Food and Drug Administration (FDA) for the indication of acute ischaemic stroke.

Today, approved medical treatment must be applied within a maximum of three hours after the stroke occurs. However, 80% of the pa-tients never make it to the hospital in time to be diagnosed within the treatment window.

The Phase III programme consists of two pla-cebo-controlled trials, each enrolling approxi-mately 320 patients. Lundbeck is recruiting pa-tients for the studies at sites in Europe, the USA, Canada, South America and Asia. Follow-ing consultations with health authorities, the trials have been designed with the aim of measuring efficacy of one dosage of desmoteplase administered in a window of be-tween three and nine hours after the stroke occurred. The efficacy of the treatment is as-sessed after 90 days.

The rights to desmoteplase are in-licensed from German PAIOn AG.

Alcohol dependence Nalmefene builds on a novel principle of treating alcohol dependence. Treatment with nalmefene is not aimed at keeping patients from drinking. Instead, the compound blocks

the mechanism in the brain that produces the desire to drink more, thereby controlling and limiting the patient’s intake of alcohol. In addi-tion, nalmefene is available as a tablet formu-lation to be taken only according to need, whereas existing pharmaceuticals must be taken continuously over a longer period of time.

A previous study documented nalmefene’s ability to significantly limit both the average alcohol intake and the number of days with an intake above five units of alcohol. This means a sharp reduction in the risk of developing dis-eases such as cardiovascular diseases, liver cir-rhosis and a number of cancers. Previous clini-cal trials have proven nalmefene to be safe and well-tolerated.

Lundbeck has launched three Phase III trials enrolling more than 1,800 patients receiving nalmefene or placebo. In the first two trials, the patients are treated over a period of six months, primarily to demonstrate efficacy, whilst patients in the third trial are treated for 12 months to confirm that the compound is well tolerated. The first data are expected in the first half of 2011. nalmefene was originally developed by BioTie of Finland. Lundbeck holds the global rights to the compound, with the exception of north America, Mexico, Turkey and South Korea.

“We consistently seek to improve our understanding of brain disorders and have promising projects in our pipeline, for example for the treatment of bipolar disorder, which is an area that is difficult to treat.”

Peter Høngaard Andersen, Executive Vice President, Research

21

1. korrektur 9/2-09

Lundbeck’s risk management systems are con-sistently updated and adapted to match exter-nal and intra-Group requirements and needs.Such revisions provide Group management with a solid basis for decisions regarding the company’s overall risk exposure and give them an overview of the activities and resources available.

Lundbeck pursues decentralised management of specific risks in those parts of the organisa-tion that have the most extensive knowledge of such risks and the best possibility of mini-mising such exposure. The individual business units take a systematic approach to monitor-ing, identifying, quantifying and responding to risks. Furthermore, we have defined reporting, decision-making and follow-up procedures and routines.

Based on reports received from its business entities every six months, Lundbeck manage-ment identifies the risks that are particularly critical for business targets. These risks are monitored in an ongoing process and, where possible, risk-reducing initiatives are taken.

The figure shows risks in the pharmaceutical value chain with accentuation of risks that Lundbeck considers particularly critical.

Research and development risks Lundbeck relies on its ability to protect its intellectual property rights in connection with new pharmaceuticals and to operate its business without infringing the rights of others. Patenting and the patent application process in pharmaceutical companies are legally and scientifically complicated processes and thus subject to a certain degree of uncertainty.

Lundbeck is taking major steps to develop and maintain competences in this area, and we consistently defend our intellectual property rights.

Throughout the research and development process, there is a risk that new pharmaceuti-cals will be delayed or have to be abandoned altogether. In 2008, Lundbeck avoided signifi-cant setbacks in late-stage projects in our own pipeline, although we did have to discontinue the development of the in-licensed anti-Alzhe-imer’s compound Flurizan® in Phase III.

In each of our late-stage projects, we thor-oughly assess whether factors such as the ini-tiation of new clinical trials or additional sup-port for patient recruitment for ongoing studies could increase the chances of a suc-cessful completion of the projects.

Lundbeck attempts to secure a reasonable balance between overall risk exposure and value-generation in a rapidly changing market.

Risk management

22

“As a pharmaceutical company, we auto-matically operate in a high-risk industry and for this reason take a systematic approach to balancing our combined business risks.”

Anders Götzsche, Executive Vice President, Finance, IT & Communication/IR

Risks in the pharmaceutical value chain

Sales and marketing risks• Price pressure and market access • Generic competition • Confidence in pharmaceuticals

• Marketing • Product liability

Research and development risks• Intellectual property rights• R&D process

• Trials and product approvals• In-licensing• Out-licensing • Tecnology

Production risks• Reliability of supply• Product recall

• Regulatory risk• Suppliers• Distribution• Intellectual property rights

Risks across the value chain • Finance • Partnerships, in-licensing and acquisitions

• Corporate governance, business ethics and public reputation• Employees and organisation

1. korrektur 9/2-09

Production risks Managing reliability of supply is crucial in en-suring that patients constantly have access to the pharmaceuticals they need. For this reason, Lundbeck carefully monitors the supply situa-tion and as a rule maintains an inventory level that will help it overcome a production break-down. In addition, Lundbeck has prepared plans for accessing alternative production facilities.

In rare cases, pharmaceutical companies are forced to recall a product from the market due to a problem with the safety or quality of the medicine. Lundbeck has systems and pro-cedures in place to ensure a swift and effective response if the need should arise.

Sales and marketing risks The pharmaceutical market is characterised by the aim of the authorities to reduce prices and regulate access to the market in order to cap increases in healthcare costs. Market changes such as price reductions may have a considerable impact on the earnings potential of pharmaceuticals.

We expect that additional healthcare reforms will be initiated in several markets and that such reforms will reduce prices and restrict ac-cess for pharmaceuticals.

The sale of counterfeit medicine in the phar-maceuticals market, also online, has become a growing problem in recent years. However, only a few cases of counterfeit Lundbeck medi-cations have been seen, with 14 cases in 2008 versus 11 in 2007. Lundbeck pursues all cases through its Anti-Counterfeit Task Force and is a member of the World Health Organisation’s (WHO) anti-counterfeit organisation IMPACT.

Risks across the value chain Lundbeck has a number of financial risks, such as currency, interest rate and credits risks.

The bulk of the Group’s commercial transac-tions are settled in foreign currency. Foreign currency exposure is reduced by hedging posi-tions in the most important foreign currencies through forward and option contracts and, to a minor extent, by raising foreign currency loans.

At the present time, the currency risk is prima-rily associated with movements in the US dol-lar and in a number of other currencies, includ-ing the UK pound.

By the end of 2008, Lundbeck had hedged in-come in these currencies for the majority of 2009. Accordingly, if the exchange rates

We are continuously working with the health authorities to document the value of our phar-maceuticals. Also, Lundbeck continuously seeks to adjust its organisation to accommo-date changes in market conditions.

Lundbeck monitors and analyses the Group’s intellectual property rights and the risks of generic competition in depth. We believe that the Group’s intellectual property rights are valid and enforceable, and it is our policy to defend intellectual property rights energeti-cally, wherever they may be infringed.

Lundbeck is involved in pending patent trials in Australia, Austria, Belgium, Canada, Denmark, France, Germany, the netherlands, norway, Portugal, the UK and the USA in respect of in-tellectual property rights concerning escitalo-pram.