half-yearly financial report at 30 june …. +39 0522 9433 fax +39 0522 944044 share capital: €...

TRANSCRIPT

Half-yearly financial report – H1 2012 ________________________________________________________________ 1

HALF-YEARLY FINANCIAL REPORT AT 30 JUNE 2012

(Translation of the Italian original which remains the definitive version)

Half-yearly financial report – H1 2012 ________________________________________________________________ 2

CONTENTS

1. GENERAL INFORMATION

1.1. Corporate officers and information 1.2. Group Structure 1.3. Landi Group Financial Highlights 1.4. Significant Events During the Six Months

2. INTERIM REPORT ON OPERATING PERFORMANCE

2.1. Macroeconomic context and reference market 2.2. Company development 2.3. Innovation, industrial research and development 2.4. Human Resources, training and safety at work 2.5. Operating performance 2.6. Landi Renzo and the financial markets 2.7. Policy for analyzing and managing risks connected with the activities of the Group 2.8. Other information 2.9. Significant events after closing the six-month period and forecast for operations.

3. ABBREVIATED SIX-MONTHLY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AS AT 30 JUNE

2012

3.1. CONSOLIDATED STATEMENT OF FINANCIAL POSITION 3.2. General consolidated Income Statement 3.3. Consolidated cash flow statement 3.4. Consolidated statement of changes in Equity

4. EXPLANATORY NOTES TO THE ABBREVIATED SIX-MONTHLY CONSOLIDATED FINANCIAL STATEMENTS AS AT 30 JUNE 2012

4.1. General information 4.2. General preparation criteria and Consolidation Principles 4.3. Consolidation scope 4.4. Explanatory notes to the consolidated financial statements

5. Declaration of the abbreviated consolidated half-yearly financial statements pursuant to art. 154-bis,

subsections 3 and 4, of Legislative Decree 58/1998 6. Auditors' Report

Half-yearly financial report – H1 2012 ________________________________________________________________ 3

1. GENERAL INFORMATION

1.1. CORPORATE OFFICERS AND INFORMATION

Board of directors

Chairperson of the board of directors Stefano Landi

Director - Honorary Chairperson Giovannina Domenichini

Chief Executive Officer Claudio Carnevale

Executive Director Carlo Alberto Pedroni

Director Carlo Coluccio

Independent Director Alessandro Ovi (*)

Independent Director Tomaso Tommasi di Vignano

Board of Statutory Auditors

Chairman of the Board of Statutory Auditors Luca Gaiani

Standing Auditor Massimiliano Folloni

Standing Auditor Marina Torelli

Alternate Auditor Filippo Nicola Fontanesi

Alternate Auditor Filomena Napolitano

Control and Risks Committee

Chairman Carlo Coluccio

Member of the Committee Alessandro Ovi

Member of the Committee Tomaso Tommasi di Vignano

Committee for Remuneration

Chairman Carlo Coluccio

Member of the Committee Alessandro Ovi

Member of the Committee Tomaso Tommasi di Vignano

Committee for Transactions with Related Parties

Member of the Committee Alessandro Ovi

Member of the Committee Tomaso Tommasi di Vignano

Surveillance Body pursuant to Legislative Decree 231/01

Chairman Daniele Ripamonti

Member of the Body Domenico Aiello

Member of the Body Enrico Gardani

Independent Auditors

KPMG S.p.A.

(*) The Director also holds the office of Lead Independent Director

Half-yearly financial report – H1 2012 ________________________________________________________________ 4

Registered office and parent details

Landi Renzo S.p.A.

Via Nobel 2/4

42025 Corte Tegge – Cavriago (RE) – Italy

Tel. +39 0522 9433

Fax +39 0522 944044

Share capital: € 11,250,000 Tax No. and VAT No. IT00523300358 This report is available on the website

www.landi.it

Half-yearly financial report – H1 2012 ________________________________________________________________ 5

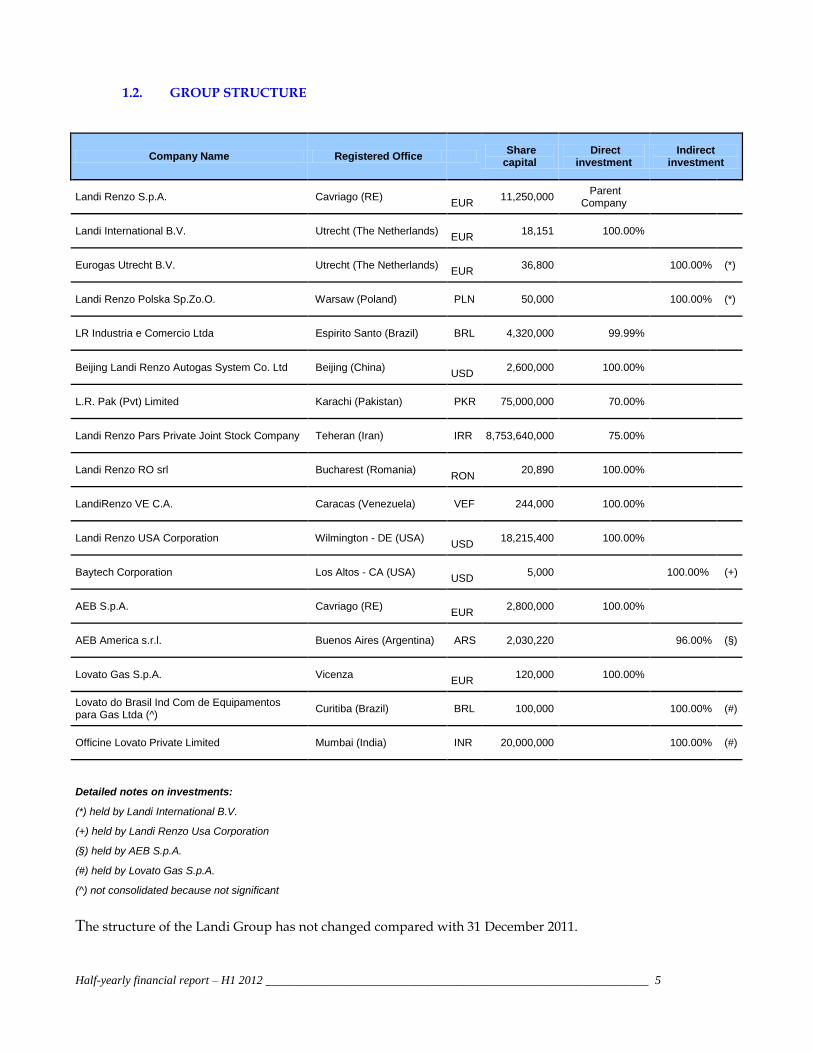

1.2. GROUP STRUCTURE

Company Name Registered Office Share capital

Direct investment

Indirect investment

Landi Renzo S.p.A. Cavriago (RE) EUR

11,250,000 Parent

Company

Landi International B.V. Utrecht (The Netherlands) EUR

18,151 100.00%

Eurogas Utrecht B.V. Utrecht (The Netherlands) EUR

36,800 100.00% (*)

Landi Renzo Polska Sp.Zo.O. Warsaw (Poland) PLN 50,000 100.00% (*)

LR Industria e Comercio Ltda Espirito Santo (Brazil) BRL 4,320,000 99.99%

Beijing Landi Renzo Autogas System Co. Ltd Beijing (China) USD

2,600,000 100.00%

L.R. Pak (Pvt) Limited Karachi (Pakistan) PKR 75,000,000 70.00%

Landi Renzo Pars Private Joint Stock Company Teheran (Iran) IRR 8,753,640,000 75.00%

Landi Renzo RO srl Bucharest (Romania) RON

20,890 100.00%

LandiRenzo VE C.A. Caracas (Venezuela) VEF 244,000 100.00%

Landi Renzo USA Corporation Wilmington - DE (USA) USD

18,215,400 100.00%

Baytech Corporation Los Altos - CA (USA) USD

5,000 100.00% (+)

AEB S.p.A. Cavriago (RE) EUR

2,800,000 100.00%

AEB America s.r.l. Buenos Aires (Argentina) ARS 2,030,220 96.00% (§)

Lovato Gas S.p.A. Vicenza EUR

120,000 100.00%

Lovato do Brasil Ind Com de Equipamentos para Gas Ltda (^)

Curitiba (Brazil) BRL 100,000 100.00% (#)

Officine Lovato Private Limited Mumbai (India) INR 20,000,000 100.00% (#)

Detailed notes on investments:

(*) held by Landi International B.V.

(+) held by Landi Renzo Usa Corporation

(§) held by AEB S.p.A.

(#) held by Lovato Gas S.p.A.

(^) not consolidated because not significant

The structure of the Landi Group has not changed compared with 31 December 2011.

Half-yearly financial report – H1 2012 ________________________________________________________________ 6

1.3. LANDI GROUP FINANCIAL HIGHLIGHTS

1.3. LANDI GROUP FINANCIAL HIGHLIGHTS

Half-yearly financial report – H1 2012 ________________________________________________________________ 7

Half-yearly financial report – H1 2012 ________________________________________________________________ 8

(Amounts in thousands of Euros) 6 MONTHS QUARTER

2011 2012 2011 Var. Diff. % Q2 2012 Q2 2011 Var. Diff. %

INCOME STATEMENT

253,529 Net Revenues 139,155 127,743 11,412 8.9% 79,557 80,575 -1,018 -1.3%

19,477 Gross Operating Profit 15,885 10,885 5,000 45.9% 10,267 11,996 -1,729 -14.4%

-3,260 Operating Profit 6,736 1,797 4,939 274.8% 5,661 6,789 -1,128 -16.6%

-8,213 Result Before Tax 4,902 -1,748 6,650 n.a. 5,594 4,634 960 20.7%

-9,138 Net Result for the Group 2,606 -2,397 5,003 n.a. 3,398 2,926 472 16.1%

7.7% Gross Operating Profit/Net Revenues 11.4% 8.5% 12.9% 14.9%

-1.3% Operating Profit/Net Revenues 4.8% 1.4% 7.1% 8.4%

-3.6% Net Group Result/Net Revenues 1.9% -1.9% 4.3% 3.6%

CONSOLIDATED BALANCE SHEET

INVESTED CAPITAL

143,974 Net tangible and other non-current assets 140,215 147,865

103,188 Working Capital (1) 90,487 95,190

-20,046 Non-current liabilities (2) -19,290 -20,410

227,116 NET CAPITAL EMPLOYED 211,412 222,645

SOURCES

90,112 Net financial position (opening cash) 71,565 80,394

137,004 Equity 139,848 142,251

227,116 BORROWINGS 211,412 222,645

MAIN INDICATORS

40.7% Working Capital/Turnover (rolling) 34.2% 36.9%

65.8% Net Financial Debt / Equity 51.2% 56.5%

11,992 Gross tangible and intangible investments 6,428 6,320

866 Personnel (peak) 860 884

(1) This is calculated as the difference between Trade Receivables, Inventories, Other Current Assets and Trade Payables, Tax liabilities, Other Current Liabilities;

(2) These are calculated by totaling Deferred Tax Liabilities, Defined Benefit Plans and Provisions for Risks and Charges;

Half-yearly financial report – H1 2012 ________________________________________________________________ 9

1.4. SIGNIFICANT EVENTS DURING THE SIX MONTHS

April On 24 April 2012 the Shareholders' Meeting resolved, amongst other things, the following:

Covering of the loss for the year posted by Landi Renzo S.p.A. equal to € 8,529,753.47 through

use of the Extraordinary Reserve.

renewal of authorization for the purchase and disposal of treasury shares;

April In April 2012 the subsidiary Landi Renzo USA obtained EPA approval for the conversion of

Ford F-series Medium Duty Vehicles including F-250/F-350 2WD /4WD pickup variants, which

use CNG systems.

May In May 2012 Landi Renzo S.p.A. proposed, with completion in the following July, rental - with

conditional purchase - of the former SAFE business unit from Agave S.r.l. in arrangement with

creditors.

The aim of this transaction, strategic for the expansion of the industrial offer and know-how, is to

relaunch the SAFE brand, known for more than 35 years in the gas treatment compressor

manufacturing sector and active in the main business areas related to compressed natural gas

(systems for the supply of CNG for vehicles)), in Oil and Gas (compressors and auxiliary systems

for processing gas from extraction to distribution), and in systems for the processing of

biomethane, hydrogen, and liquefied natural gas.

The purchase of the business unit is subject to the approval of the agreement with creditors.

Half-yearly financial report – H1 2012 ________________________________________________________________ 10

2. INTERIM REPORT ON OPERATING PERFORMANCE

This consolidated half-yearly financial report at 30 June 2012 was prepared pursuant to Legislative Decree 58/1998 and subsequent modifications, as well as by the Issuer Regulations issued by CONSOB.

This Report has been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and endorsed by the European Union, and has been prepared in accordance with IAS 34 - Interim Financial Reporting, applying the same accounting policies as adopted in preparing the consolidated financial statements at 31 December 2011. In partial exception to the provisions of IAS 34, this report provides detailed rather than synthetic schemes in order to provide a clearer view of the economic-patrimonial and financial dynamics that occurred over the six-month period. The explanatory notes are also presented in compliance with the information required by IAS 34 with the supplements considered useful for a clearer understanding of the half-yearly financial statements.

The consolidated financial statements of the Landi Group at 30 June 2012 close with a net profit for the Group of

€ 2,606 thousand, compared with a loss for the Group of € -2,397 in the first half of 2011.

Revenues (goods and services) amounted to € 139,155 thousand, up by 8.9% compared with the same period in

2011.

The gross operating profit (EBITDA) is equal to € 15,885 thousand, compared with € 10,885 in June 2011, an

increase of 45.9%.

The operating profit (EBIT) is equal to € 6,736 thousand, compared with € 1,797 in 2011, an increase of 274.8%.

The net financial position at 30 June 2012 is negative for € 71,565 thousand, while at 30 June 2011 it was negative

for € 80,394 thousand.

In the second quarter of this year the Landi Group achieved revenues of € 79,557 thousand, an increase of €

19,959 thousand compared with the first quarter of 2012 (+33.5%).

The Group's net profit for the second quarter was € 3,398 thousand, an increase of 16.1% compared with the

second quarter of 2011.

2.1. MACROECONOMIC CONTEXT AND REFERENCE MARKET

In the early months of 2012, world economic activity, although hampered by stagnation in Europe and the

slowdown in the U.S. and emerging economies, showed some acceleration expanding at a moderate pace, while

international trade showed general signs of recovery.

From April 2012 the economic environment weakened again, conditioned by uncertainty on the evolution of the

sovereign debt crisis in the Euro zone and fiscal policy in the United States, although there was an attenuation of

inflationary pressures due to the decline in the prices of raw materials. According to the latest projections by the

Half-yearly financial report – H1 2012 ________________________________________________________________ 11

International Monetary Fund (IMF), released in July 2012, global growth this year is expected to fall to 3.5%

(from 3.9% in 2011), held back by the fall in business in the Euro zone and a slowdown in emerging markets.

The signs of a slowdown arriving from the Eurozone are compounded by the volatility in financial markets,

characterized by a considerable increase in aversion to riskier assets.

At a global level, however, the trend in the car market is positive. Registrations of new cars actually increased

worldwide by 6.6% in the first half of 2012, mainly due to the growth seen in the United States, as well as in

China, India and Russia and to the recovery of the Japanese market.

The positive trend in this auto market, however, does not seem to reach the Euro zone countries where, during

the first six months of the year, there was a decline in registrations of 6.8% (according to data released by ACEA

– Association des Constructeurs Européens d’Automobiles) compared with the same period last year, although with

differing trends among the major countries. The exact figure just for the month of June showed a decrease

limited to 2.8%.

Amidst this economic uncertainty, registrations of new cars in Italy during the first half of 2012 showed a

decrease of 19.7% compared with the same period last year, despite a significant increase in registrations of cars

powered by LPG, up from 2.82% of total registrations in 2011 to 7.52% in 2012, as well as the registration of

CNG-powered cars, which increased from 1.94% in 2011 to 3.56% in 2012.

The Landi Group, in the macroeconomic context described above, was able to follow the growth trend of its own

business sector, although in a declining Italian and European auto market, while at the same time grabbing some

of the opportunities offered by the worldwide automotive market.

The commercial strategy of the Landi Group focused on the one hand on strengthening relations with major

OEM players in the European market and on the other, in driving sales in the After Market channel, especially in

emerging markets, such as Asia and Latin America where, increasingly, policies are implemented for

diversification of energy sources favoring the use of natural gas for vehicles.

2.2. COMPANY DEVELOPMENT

A leader in sustainable mobility since 1954, Landi Renzo holds about a 30% share of the world market for gas

fuel supply systems for motor vehicles, a sector that currently operates in a fleet of more than 30 million LPG or

CNG vehicles, a number that confirms the absolute primacy of technologies of this sector to promote ecological

mobility.

In recent years, technological innovation and continuous research have made Landi Renzo a prestigious brand

worldwide, increasingly aimed at the development of new expertise and functional choices in the context of a

strategy of growth and internationalization.

The continuous technological and quality development of its products, characterized by the combination of

seeking excellence in production, a flexible approach to the customer, and the international vocation (as

Half-yearly financial report – H1 2012 ________________________________________________________________ 12

demonstrated by the direct presence in key markets and indirect presence in more than 50 countries), are the

cornerstones underlying the company's success.

A key element of this strategy has been the ability to identify, with precise timing, each region capable of

expressing sales potential of innovative technologies for gas fuel supply systems.

With regard to the business sectors, alongside the historic After Market channel (retailers and importers), the

Group has also expressed its leadership through its collaboration with leading car manufacturers (Original

Equipment Manufacturing or “OEM” customers) worldwide, providing systems and installation services while

constantly monitoring quality at the critical stages of the production process.

During the first half of 2012, the Group finalized the development of dual fuel technology (diesel and CNG mix)

and continued with the HERS project (hybrid electric vehicles already on the road), showing its constant cutting

edge proposals for the use of energy sources with a lower environmental impact.

With regard to expansion of the product range, aimed at completing its offer and capacity for partnerships with

industrial and institutional partners, in July 2012 the Group expanded its business perimeter by renting a

business unit with subsequent conditional purchase, of the company Agave S.r.l. (formerly SAFE) operating in

the production of compressors for treatment of gases for multiple applications.

In the first half of 2012, the Group further strengthened its internationalization strategy, consolidating its

presence in the markets of the BRIC and neighboring countries, which are characterized by an increasing use of

CNG vehicles in the presence of substantial reserves of natural gas and government incentive policies.

2.3. INNOVATION, INDUSTRIAL RESEARCH AND DEVELOPMENT

During the first half of 2012, research continued on innovative technologies and development of fuel supply

systems that can contribute to reducing emissions of pollutants and greenhouse gases (CO2).

In particular, the Group introduced its new range of After Market CNG and LPG conversion kits to the market,

consisting of a series of new components developed during the previous year such as injectors, gearboxes,

electronic and multi-valve power units. The success of the sale of these kits supported further development

activities aimed at expanding the range of new products for the conversion of all types of vehicles. In this

context, the first conversion kits for direct injection petrol engines were recently presented: this type of engine,

increasingly widespread on the market, is characterized by the fact that the fuel is injected directly into the

combustion chamber with consequent optimization in terms of consumption and performance.

The guidelines used for the development of applications intended for direct injection engines are the same as

those used for adapting gas fuel supply systems to all the technological innovations that car manufacturers

introduce regarding the operation and control of the engine, including those of the latest generation.

With regard to collaboration with auto manufacturers, the first half of the year was characterized by the

development of systems to be applied to new car models for CNG and LPG supply, in order to complete the

entire range aimed at customers.

Half-yearly financial report – H1 2012 ________________________________________________________________ 13

Studies on the dual fuel diesel-CNG combustion process were continued, after the first approvals obtained in

2011, toward increasingly complex types of engines and applications, with particular reference to the buses used

in public transport as well as small goods vehicles. Thanks to this innovative dual fuel system it is now possible

to apply a dual diesel/CNG fuel supply, capable of reducing polluting emissions and running costs. The system

developed by the Landi Group allows CNG to be mixed with diesel, guaranteeing driving performances similar

to those obtained by full diesel engines. In this way, the system increases the fuel distance of vehicles, with

significant savings on consumption, and allows dual fuel supply to be reversed to diesel only at any time.

Research activities on new technologies are being continued both at the Cavriago headquarters and in the

branches, and were demonstrated during an event held at the new Research and Development Center in June

2012, at the same time as the NGV 2012 fair in Bologna.

On this occasion, a group of customers selected from around the world were able to test some of the

technologies recently implemented or under development on vehicles at their disposal, including systems for

direct injection vehicles, dual-fuel engines for ecological fleets, and applications for hybrid-electrical vehicles.

2.4. HUMAN RESOURCES, TRAINING AND SAFETY AT WORK

Human resources

The total number of employees of the Landi Group at 30 June 2012 was 860 units compared with 866 at 31

December 2011, an overall decrease of 6 units during the six-month period.

The following table lists the number of employees in the workforce.

Company 30/06/2012 31/12/2011 30/06/2011

Landi Renzo S.p.A. 359 363 369

A.E.B. S.p.A. 189 172 181

Lovato Gas S.p.A. 107 108 105

Foreign companies 205 223 229

Total 860 866 884

The number of employees compared with the first half of 2011 shows a decrease of 24 units, mainly because of

the reduction in the number of employees at foreign subsidiaries in Iran and Pakistan.

Training

Landi Renzo believes that the training of human resources represents a fundamental investment for the

development of company activities and, for this purpose, promotes the sharing of business know-how between

employees through training initiatives put forward by “LANDIRENZO Corporate University”.

Half-yearly financial report – H1 2012 ________________________________________________________________ 14

The 2012 training plan is aimed at strengthening technical and managerial skills, as well as updating and

qualification of human resources. During the first half of 2012, more than 750 hours of training were carried out

with a strong focus on the issue of safety in the context of the new State-Region Agreement.

As regards the activity for discovering and promoting new talents, the companies of the Landi Group continued

to host students coming from university and post-university specialization paths, involved internships and

company field projects in Research and Development, Commercial and Business Development areas.

In the area of installer training, the R&D function and the Corporate University worked in close contact with

important results: 250 hours of training with more than 450 installers trained throughout the national territory.

Another important goal was attained by the Corporate University thanks to the issue of the first two books in

the series of publications created in collaboration with the Group Il Sole24Ore: “Landi Renzo and Sustainable

Mobility” and “Eco & Green Car, A guide to the ecological and sustainable car”.

Health, Safety and Environment

The Landi Group, which has always been active regarding safety in the workplace, is subject to the regulatory

principles pursuant to Legislative Decree no. 81 of 9 April 2008 regarding safety in the workplace.

On the strength of its OHSAS 18001:2007 certification, the Group continued with its activity of spreading

knowledge on safety and risk prevention in the workplace, also through innovative internal communication

systems for improved communication of the main standards and conduct regarding safety in the workplace.

Aware that environmental protection is one of the factors on which our future depends, the Group, in line with

its corporate mission, considered its commitment in this area within its own structures to be important,

spreading information on ecological topics in order to educate towards sustainable behavior while monitoring

the environmental impacts associated with its activities. Against this background, projects were started up for

the implementation of the Environmental Management System and ISO 14001 Certification, and to update the

Organization and Control Model pursuant to Legislative Decree 231/2001.

2.5. OPERATING PERFORMANCE

Consolidated results

In the first half of 2012, the Landi Group achieved revenues of € 139,155 thousand, an increase of 8.9% over the

previous year.

Gross operating profit amounted to € 15,885 thousand (+45.9%), while there a net profit for the Group equal to €

2,606 thousand was recorded, compared with a net loss of € -2,397 thousand in the first half of 2011.

The figures for the six-month period show a strong improvement in the results achieved for the second quarter

of 2012 in terms of both turnover and profit compared with the first quarter.

Half-yearly financial report – H1 2012 ________________________________________________________________ 15

The following table shows the evolution of the main economic performance indicators divided by six-month

period.

(thousands of Euros) H1 2012 % H2 2011 % H1 2011 %

Revenues (goods and services) 139,155 125,786 127,743

Other Revenue and Income 959 968 678

Operating costs -124,229 -89.3% -118,162 -

93.9% -117,536 -92.0%

Gross Operating Profit 15,885 11.4% 8,592 6.8% 10,885 8.5%

Amortization, depreciation and impairment losses -9,149 -6.6% -13,649 * -

10.9% -9,088 -7.1%

Operating Profit 6,736 4.8% -5,057 -4.0% 1,797 1.4%

Financial income 352 0.3% 211 0.2% 271 0.2%

Financial expenses -2,177 -1.6% -2,010 -1.6% -1,600 -1.3%

Exchange rate gains and losses -9 0.0% 391 0.3% -2,216 -1.7%

Profit (Loss) before tax 4,902 3.5% -6,465 -5.1% -1,748 -1.4%

Taxes -2,177 -1.6% -19 0.0% -907 -0.7%

Net profit (loss) for the Group and minority interests, including: 2,725 2.0% -6,484 -5.2% -2,655 -2.1%

Minority interests 119 0.1% 257 0.2% -258 -0.2%

Net Profit (Loss) of the Group 2,606 1.9% -6,741 -5.4% -2,397 -1.9%

* of which € 4,316 thousand relates to writedowns of tangible and intangible assets.

The increase in revenues recorded in the first half of 2012 compared with the same period in 2011 is primarily

due - while taking account of the negative trend of the South-West Asian market reasons that will be discussed

later - to the significant progress recorded in the Italian market (+96.7%) and in the European market (+35.8%)

and to the positive growth of the markets in the rest of the world (+11.8%).

In further detail, two macro elements can be highlighted that generated this positive performance compared to

last year:

the increase in registrations of LPG and CNG vehicles in Italy and Europe on EuroV engines;

the significant recovery in motor vehicle conversions in the After Market, favored mainly by the increase in

the price of traditional fuels, especially in Italy, and also as a result of the positive trend in demand in far east

countries and in some Latin American countries where the Group is increasing its penetration.

Breakdown of sales by business segment

Half-yearly financial report – H1 2012 ________________________________________________________________ 16

Q2 2012 v. Q2 2011

(Thousands of Euros) Q2 2012 % of

revenue Q2 2011

% of revenue

Change %

Gas sector - LPG line 55,761 70.1% 35,254 43.8% 20,507 58.2%

Gas sector - CNG line 19,876 25.0% 41,751 51.8% -21,875 -52.4%

Total revenues - GAS sector 75,637 95.1% 77,005 95.6% -1,368 -1.8% Other (Alarm systems, Sound, Aquatronics and Robotics) 3,920 4.9% 3,570 4.4% 350 9.8%

Total revenues 79,557 100.0% 80,575 100.0% -1,018 -1.3%

H1 2012 v. H1 2011

(Thousands of Euros) At 30/06/12 % of

revenue At 30/06/11

% of revenue

Change %

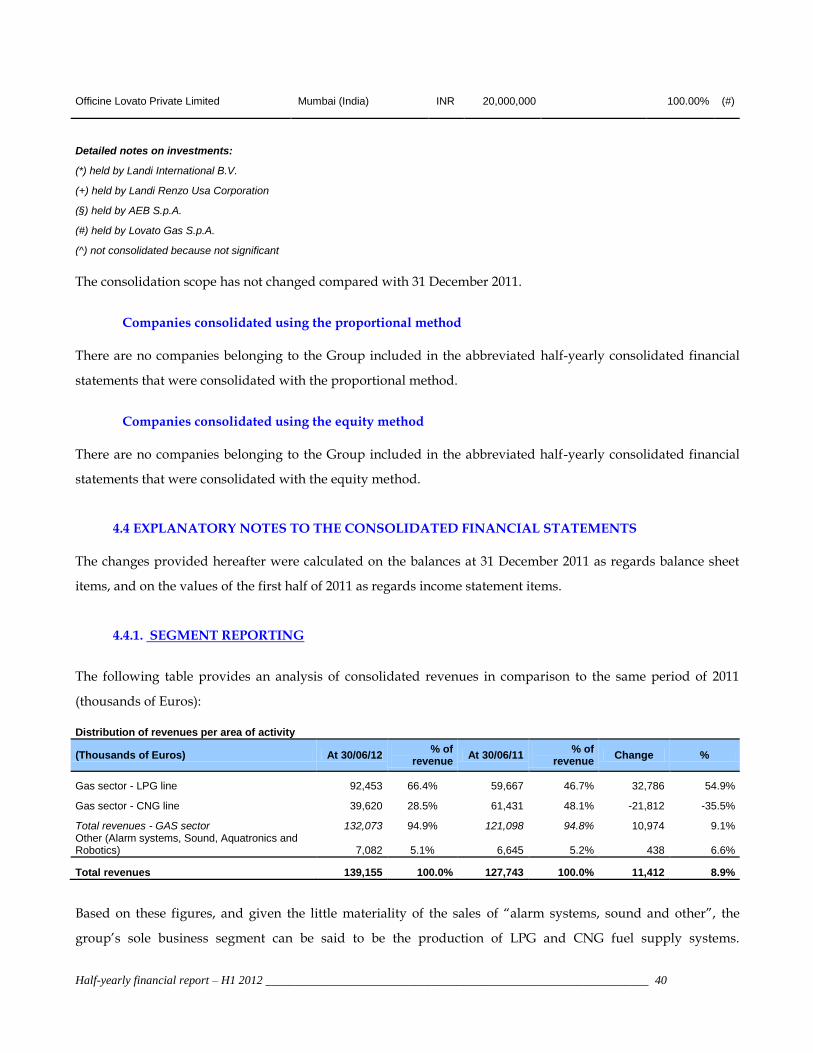

Gas sector - LPG line 92,453 66.4% 59,667 46.7% 32,786 54.9%

Gas sector - CNG line 39,620 28.5% 61,431 48.1% -21,812 -35.5%

Total revenues - GAS sector 132,073 94.9% 121,098 94.8% 10,974 9.1% Other (Alarm systems, Sound, Aquatronics and Robotics) 7,082 5.1% 6,645 5.2% 438 6.6%

Total revenues 139,155 100.0% 127,743 100.0% 11,412 8.9%

Revenues from sales of products and services in the GAS segment increased over the six months in question

from € 121,098 thousand in the first half of 2011 to € 132,073 thousand in the first half of 2012, recording an

increase of 9.1%. The increase (+ 54.9%) in six-monthly sales in the gas sector – LPG line was generated mainly

by the European markets, and in particular by the Italian market where there was a strong increase in demand

in both the OEM and After Market sectors, also favored by the increase in the price of traditional fuels (Petrol and

Diesel) recorded in the first part of 2012, as well as by the increasing interest regarding environmental and

energy issues. Sales in the gas segment - CNG line, on the other hand, dropped by 35.5% compared with the

first half of 2011, mainly due to the contraction of the market recorded in South-West Asia. This downturn can

be ascribed on the one hand to the significant slowdown in the Iranian market, which is suffering under trade

and financial restrictions as a result of the increasingly stringent embargo, and on the other to the contraction of

the Pakistani market as a result of unfavorable regulations.

Revenues from the sales of products in the Alarms, Sound and Other sector increased by 6.6% from € 6,645

thousand to € 7,082 thousand.

Revenues from sales of products and services in the GAS segment for the quarter in question decreased, overall,

from € 77,005 thousand in the second quarter of 2011 to € 75,637 thousand in the second quarter of 2012,

recording a decrease of 1.8%.

Half-yearly financial report – H1 2012 ________________________________________________________________ 17

Within the Gas segment, revenues from the sale of LPG systems increased 58.2% from € 35,254 thousand to €

55,761 thousand. On the other hand, revenues from the sale of CNG systems dropped 52.4% from € 41,751

thousand to € 19,876 thousand.

Based on these figures, and given the little materiality of Alarm Systems, Sound and Other sales, the Landi

Group's sole business segment can be considered to be the “Gas Segment” for the production of LPG and CNG

fuel supply systems. Considering that the principal source of risks and benefits is connected with the activity

carried out and that the structure of the internal reporting uses a single activity segment, it is not considered

necessary to provide further specifications regarding the Gas Sector since it coincides substantially with that of

the entire company.

Geographical distribution of sales

Q2 2012 v. Q2 2011

(Thousands of Euros) Q2 2012 % of

revenue Q2 2011

% of revenue

Change %

Italy 24,589 30.9% 14,000 17.4% 10,589 75.6%

Europe (excluding Italy) 27,481 34.5% 20,727 25.7% 6,754 32.6%

South-west Asia 5,589 7.0% 19,295 23.9% -13,706 -71.0%

America 8,903 11.2% 14,912 18.5% -6,009 -40.3%

Rest of the World 12,995 16.3% 11,641 14.4% 1,354 11.6%

Total 79,557 100% 80,575 100% -1,018 -1.3%

H1 2012 v. H1 2011

(Thousands of Euros) At 30/06/12 % of

revenue At 30/06/11

% of revenue

Change %

Italy 42,954 30.9% 21,832 17.1% 21,122 96.7%

Europe (excluding Italy) 44,904 32.3% 33,068 25.9% 11,836 35.8%

South-west Asia 12,393 8.9% 35,171 27.5% -22,778 -64.8%

America 17,174 12.3% 18,233 14.3% -1,059 -5.8%

Rest of the World 21,730 15.6% 19,439 15.2% 2,291 11.8%

Total 139,155 100% 127,743 100% 11,412 8.9%

Half-yearly financial report – H1 2012 ________________________________________________________________ 18

Analyzing the geographical distribution of revenues, during the first half of 2012 the Landi Group realized

69.1% (82.9% at 30 June 2011) of its consolidated revenues abroad (32.3% in Europe and 36.8% outside Europe).

The Italian market, in the six-month period, grew by 96.7% compared with the same period of the previous year

and revenues stood at € 42,954 thousand. This increase was generated by the increase in the demand for cleaner

and cheaper fuels (LPG and CNG) and by the full availability, from the start of the year, of the product range for

the OEM channel, completely renewed with systems that comply with the requirements of the Euro V standard

currently in force. Indeed, even in the context of an automobile market in steep decline (814,132 registrations in

the first half of 2012, in other words -19.7% compared with first half of 2011 - data source UNRAE) the sales mix

of new cars equipped with LPG and CNG systems increased in significantly (from 4.76% in the first half of 2011

to 11.08% in the first half of 2012), generating a positive effect on the volumes and revenues recorded in the first

part of the year.

The After Market conversions market in Italy has also developed significantly: the data processed by the Ecogas

consortium show the number of conversions in the first half of 2012 as 101,884, a strong increase (+45%)

compared with the same period of the previous year when they amounted to 70,143. The Landi Group's share of

the national market on the After Market channel in the first half of 2012 was close to 28.5%.

The trend in revenues in Europe increased by 35.8% compared with first half of 2011: Group sales benefited both

from the growth of the main markets in this geographical area, and from the positive effect generated by the

market launch of a completely renovated product range for the After Market channel. We point out that there

were significant increases in sales in Eastern European countries, with excellent performances in Poland and

Romania, as well as in Western Europe - in particular France.

The South West Asian market, as already shown in the first quarter of 2012, recorded a downturn in sales of

64.8% compared with the same period in 2011, primarily due to a serious slowdown in the Iranian and Pakistani

markets

A decrease of 5.8% was recorded in the American markets compared with the same period last year, while the

markets in the Rest of the World recorded an increase of 11.8% as a result of the positive trend in demand in

Thailand and the good performance of the Indian market, where the Group recently signed a preliminary

agreement to set up a Joint Venture with a local partner operating in the automotive sector.

Profit

Over the six-month period the Gross Operating Profit (GOP) of the Landi Group was positive for € 15,885

thousand (11.4% of turnover), an increase of 45.9% compared with value recorded for the same in 2011 (8.5% of

turnover). This increase can be ascribed to the elements summarized below:

increase in sales volumes and turnover;

productive optimizations to reduce the incidence of costs of materials achieved through rationalization of

Half-yearly financial report – H1 2012 ________________________________________________________________ 19

supplies and better industrialization of the products;

activities for the reduction and rationalization of structural costs already in operation during the previous

year.

Operating Profit was equal to € 6,736 thousand, compared with € 1,797 thousand in the first half of 2011, after

taking account of the depreciation and amortization of tangible and intangible fixed assets for € 9,149 thousand,

compared with depreciation and amortization of € 9,088 thousand recorded in the same period of 2011.

The result before tax was positive and equal to € 4,902 thousand compared with a pre-tax loss of € -1,748

thousand recorded in the first half of the previous year.

The Net Result of the Group for the first half of 2012 showed a profit of € 2,606 thousand, compared with a

negative net result for the first half of 2011 equal to € -2,397.

The following table is included to provide a clearer representation and to understand the positive trend of the

key performance indicators of the Group, analyzed by quarters with the same consolidation scope.

CONSOLIDATED INCOME STATEMENT

Q2 2012 % Q1 2012 % Q4 2011 % Q3 2011 % (thousands of Euros)

Revenues (goods and services) 79,557 59,598 63,390 62,396

Gross Operating Profit 10,267 12.9% 5,618 9.4% 3,473 5.5% 5,119 8.2%

Operating Profit 5,661 7.1% 1,075 1.8% -1,265 -2.0% -3,792 -6.1%

Profit Before Tax 5,594 7.0% -692 -1.2% -2,230 -3.5% -4,235 -6.8% Net profit (loss) for the Group and minority interests 3,547 4.5% -822 -1.4% -1,271 -2.0% -5,213 -8.4%

Note that the results obtained in the second quarter of 2012 as well as showing a significant increase in turnover

of € 19,959 thousand compared with the first quarter of 2012, also record an improvement in gross operating

profit, 12.9% of turnover, a significant increase compared with trend in recent quarters.

More particularly, the economic results of the second quarter show:

- consolidated EBITDA up by 82.7% compared with the previous quarter and which has almost trebled

compared to the last quarter of 2011;

- a net result of € 3,547 thousand that follows the same positive trend - the first result in profit after three

quarters closed with a net loss.

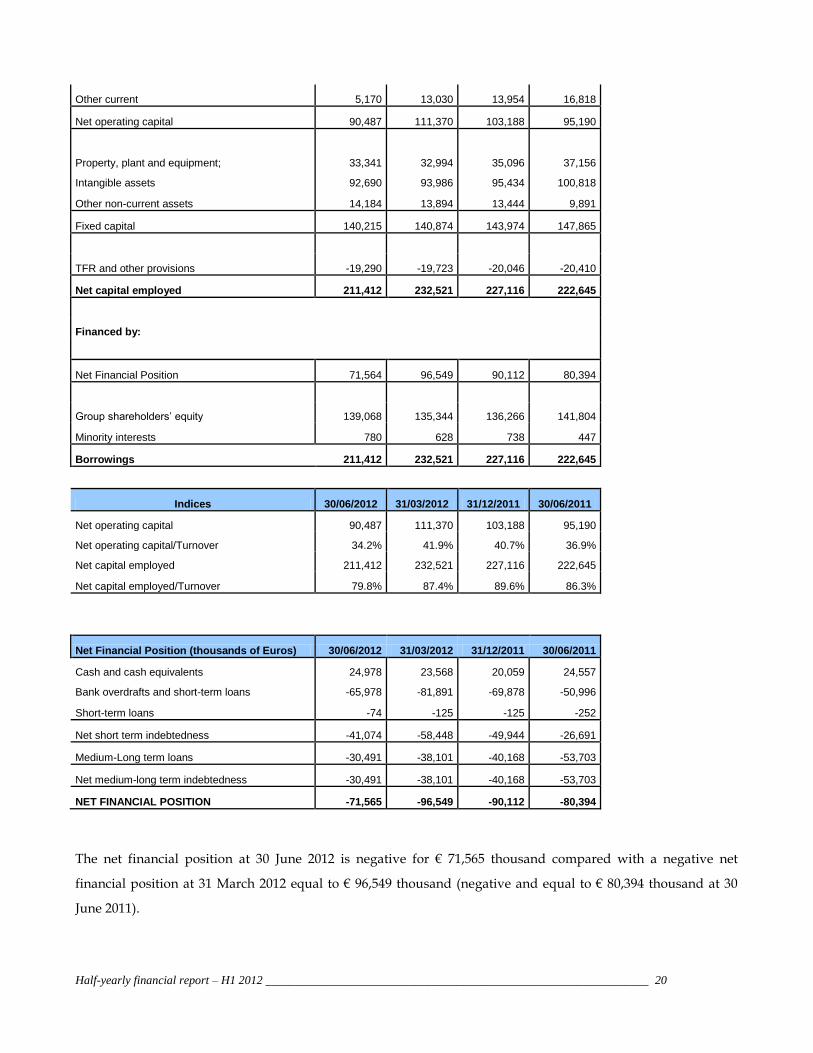

Net financial position

Financial Position (thousands of Euros) 30/06/2012 31/03/2012 31/12/2011 30/06/2011

Trade receivables 92,708 82,855 77,790 80,298

Inventories 79,028 72,052 67,408 74,079

Trade Payables -86,419 -56,567 -55,964 -76,005

Half-yearly financial report – H1 2012 ________________________________________________________________ 20

Other current 5,170 13,030 13,954 16,818

Net operating capital 90,487 111,370 103,188 95,190

Property, plant and equipment; 33,341 32,994 35,096 37,156

Intangible assets 92,690 93,986 95,434 100,818

Other non-current assets 14,184 13,894 13,444 9,891

Fixed capital 140,215 140,874 143,974 147,865

TFR and other provisions -19,290 -19,723 -20,046 -20,410

Net capital employed 211,412 232,521 227,116 222,645

Financed by:

Net Financial Position 71,564 96,549 90,112 80,394

Group shareholders’ equity 139,068 135,344 136,266 141,804

Minority interests 780 628 738 447

Borrowings 211,412 232,521 227,116 222,645

Indices 30/06/2012 31/03/2012 31/12/2011 30/06/2011

Net operating capital 90,487 111,370 103,188 95,190

Net operating capital/Turnover 34.2% 41.9% 40.7% 36.9%

Net capital employed 211,412 232,521 227,116 222,645

Net capital employed/Turnover 79.8% 87.4% 89.6% 86.3%

Net Financial Position (thousands of Euros) 30/06/2012 31/03/2012 31/12/2011 30/06/2011

Cash and cash equivalents 24,978 23,568 20,059 24,557

Bank overdrafts and short-term loans -65,978 -81,891 -69,878 -50,996

Short-term loans -74 -125 -125 -252

Net short term indebtedness -41,074 -58,448 -49,944 -26,691

Medium-Long term loans -30,491 -38,101 -40,168 -53,703

Net medium-long term indebtedness -30,491 -38,101 -40,168 -53,703

NET FINANCIAL POSITION -71,565 -96,549 -90,112 -80,394

The net financial position at 30 June 2012 is negative for € 71,565 thousand compared with a negative net

financial position at 31 March 2012 equal to € 96,549 thousand (negative and equal to € 80,394 thousand at 30

June 2011).

Half-yearly financial report – H1 2012 ________________________________________________________________ 21

The significant reduction in debt, which dropped in the quarter by € 24,984 thousand, is a result of greater

profits produced and the change in net working capital, with particular regard to the increase in trade payables.

Net operating capital (€ 90,487 thousand) decreased compared with 31 March 2012, by € 20,883 thousand, while

the percentage indicator, calculated on rolling turnover decreased from 41.9% to 34.2%.

An analysis of the individual items in comparison to the previous quarter shows:

- an increase in trade receivables equal to € 9,853 thousand as a result of increased revenue;

- a greater level of stocks amounting to € 6,976 thousand;

- a significant increase in trade payables of € 29,852 thousand primarily due to the increase in business volumes

as well as to the more favorable contractual conditions agreed with the suppliers;

- a reduction in other current assets of € 7,860 thousand, mostly due to assignment without recourse of the 2011

VAT credit of the parent company.

Net capital employed (€ 211,412 thousand), the fixed portion of which remains substantially unchanged,

decreased compared with 31 March 2012 by € 21,109 thousand, while the percentage indicator, calculated on

rolling turnover decreased from 87.4% to 79.8% .

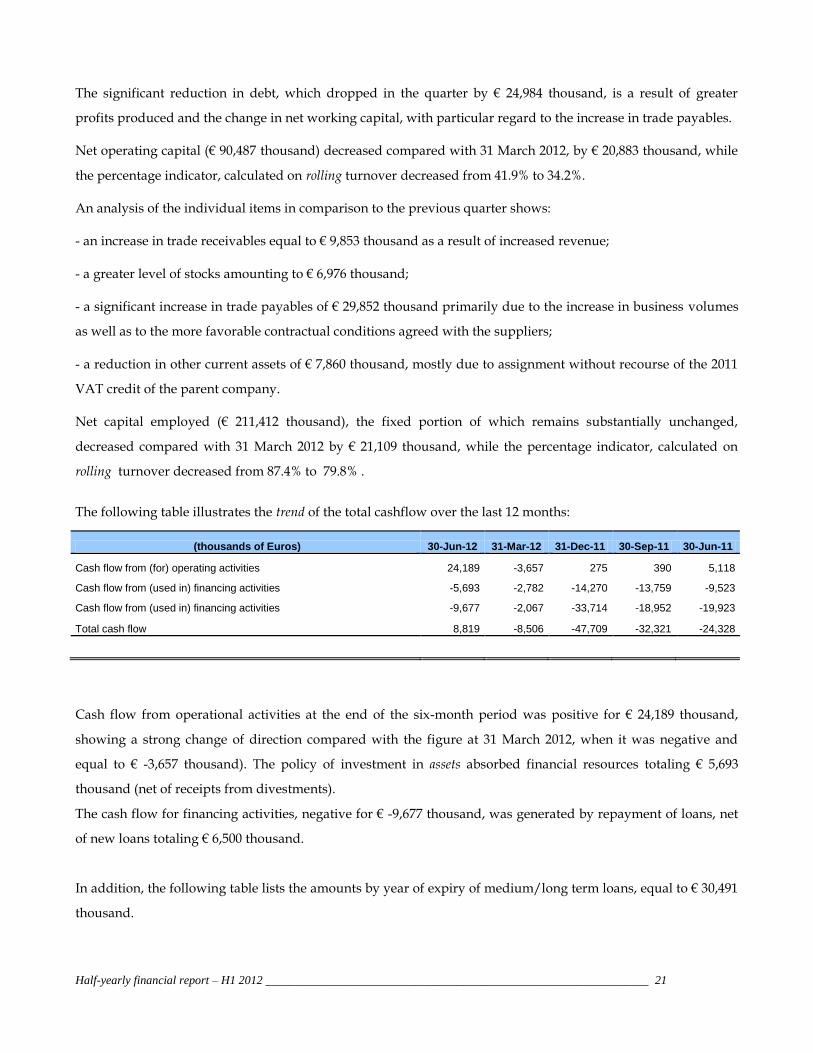

The following table illustrates the trend of the total cashflow over the last 12 months:

(thousands of Euros) 30-Jun-12 31-Mar-12 31-Dec-11 30-Sep-11 30-Jun-11

Cash flow from (for) operating activities 24,189 -3,657 275 390 5,118

Cash flow from (used in) financing activities -5,693 -2,782 -14,270 -13,759 -9,523

Cash flow from (used in) financing activities -9,677 -2,067 -33,714 -18,952 -19,923

Total cash flow 8,819 -8,506 -47,709 -32,321 -24,328

Cash flow from operational activities at the end of the six-month period was positive for € 24,189 thousand,

showing a strong change of direction compared with the figure at 31 March 2012, when it was negative and

equal to € -3,657 thousand). The policy of investment in assets absorbed financial resources totaling € 5,693

thousand (net of receipts from divestments).

The cash flow for financing activities, negative for € -9,677 thousand, was generated by repayment of loans, net

of new loans totaling € 6,500 thousand.

In addition, the following table lists the amounts by year of expiry of medium/long term loans, equal to € 30,491

thousand.

Half-yearly financial report – H1 2012 ________________________________________________________________ 22

Year falling due

(thousands of Euros) 2013 - H2 2014 2015

Medium-Long term loans 14,849 13,975 1,667

Investments

Investments in property, plant and equipment were equal to € 4,313 thousand (€ 4,153 thousand at 30 June 2011)

and relate both to the purchase of machinery and production equipment in order to deal with the new

production and business needs.

The increases in intangible assets were equal to € 1,416 thousand (€ 2,293 thousand at 30 June 2011) and relate

primarily to capitalized costs for the development of new products and the costs incurred for the

implementation of management software.

Statement of reconciliation between the data of the Parent Company's financial statements and the data of

the consolidated financial statements

Pursuant to CONSOB Communication no.6064293 of 28 July 2006, a reconciliation statement between the result

for the period and equity of the group with the corresponding values of the Parent Company is provided.

RECONCILIATION STATEMENT (in thousands of €) Equity at

30/06/2012

Result for the year at

30/06/2012 Equity at

31/12/2011

Result for the year at

31/12/2011

Equity and result for the year of the Parent Company 120,638 -108 120,745 -8,530 Difference in value between carrying value ad pro-quota value of the accounting equity of the consolidated companies 21,432 -627 18,225 501

Pro-quota results achieved by investees 0 5,634 0 2,977

Elimination of intercompany dividends 0 -1,999 0 -7,600

Elimination of the effects of intercompany commercial transactions -2,754 -294 -2,258 -164

Elimination of revaluation/write-down of investments 0 0 0 3681

Elimination of the effects of intercompany assets -248 0 -237 0

Accounting for financial leasing operations 0 0 -209 -2

Equity and result for the year from Consolidated Financial Statements 139,068 2,606 136,266 -9,138

Equity and result for the year of minority interests 780 119 738 -1

Equity and result for the year of the Group 139,848 2,725 137,004 -9,139

Half-yearly financial report – H1 2012 ________________________________________________________________ 23

Performance of the main companies of the Group

Landi Renzo S.p.A. (Parent Company)

In the first six months of 2012 Landi Renzo S.p.A. achieved revenues of € 72,740 thousand, compared with €

59,876 thousand in the first half of 2011, an increase of 21.5%. The increase in turnover can be ascribed primarily

to the increase in sales on the LPG line, primarily in Italy and Europe, achieving significant volumes on OEM

installations, and to consolidation in the After Market sector.

Gross Operating Profit was € 3,183 thousand, compared with a negative result of € 805 thousand at 30 June 2011.

The net financial position at 30 June 2012 is negative and equal to € -64,796 thousand, compared with a negative

net financial position at 31 December 2011 equal to € -87,281 thousand. At the close of the six-month period, the

Parent Company's workforce numbered 359 employees, an increase of 4 units compared with 31 December 2011.

Lovato Gas S.p.A.

The revenues of Lovato Gas dropped from € 33,825 thousand at 30 June 2011 to € 27,466 thousand at 30 June

2012, recording a decrease of 18.8% primarily due to the steep slowdown in the Iranian market, which is

suffering under trade and financial restrictions related to the increasingly stringent international embargo

provisions. The gross operating result of the first half of 2012 was positive and equal to € 3,183 thousand,

compared with a positive gross operating result equal to € 3,896 thousand reported in the first half of 2011. The

net financial position, negative, was € -13,899 thousand at 30 June 2012, compared with € -12,214 thousand at 31

December 2011.

A.E.B. S.p.A.

Revenues of A.E.B. S.p.A. at 30 June 2012 were € 41,957 thousand, including € 13,972 thousand from Group

companies, and were up by 26.4% compared with the same period of the previous year. The gross operating

result was positive and equal to € 7,390 thousand (17.6% of turnover).

The net financial position, positive, was equal to € 1,705 thousand at 30 June 2012 compared with € 4,157

thousand at 31 December 2011, after payment of dividends of € 2,000 thousand to the Parent Company.

The foreign subsidiaries of the Group, whose percentage weight in terms of revenue was 30% lower than

consolidated turnover, recorded an overall positive Gross Operating Profit, influenced to a large extent by the

good performance of the subsidiaries located in Romania and Poland.

Half-yearly financial report – H1 2012 ________________________________________________________________ 24

2.6. LANDI RENZO AND THE FINANCIAL MARKETS

The Landi Group maintains a constant dialog with its Shareholders through a responsible and transparent

activity of communication carried out by the Investor Relations office with the aim of providing a clear

explanation of the company's evolution. The Investor Relations function is also assigned the task of organizing

presentations, events and “Roadshows” that enable a direct relationship between the financial community and the

Group's Top management. For further information and to consult the economic-financial data, corporate

presentations, periodical publications, official communications and real time updates on the share price you can

visit the Investor Relations section of the site www.landi.it.

The following table summarizes the main share and stock market data for the six-month period.

Share Price and Stock Market Information (source Borsa Italiana S.p.A.)

Price at 2 January 2012 1.265

Price at 29 June 2012 1.35

Maximum price 2012 (02/01/12 - 29/06/12) 2.08

Minimum price 2012 (02/01/12 - 29/06/12) 1.228

Market Capitalization at 30 June 2012 151,875,000

Number of shares representing the share capital 112,500,000

The share capital is made up of 112,500,000 shares with a nominal value of € 0.10 per share, for a total of €

11,250,000.00.

2.7. POLICY FOR ANALYZING AND MANAGING RISKS CONNECTED WITH THE ACTIVITIES OF THE LANDI GROUP

This section provides information on exposure to risks connected with the activities of the Group as well as the

objectives, policies and processes for managing such risks and the methods used to asses and to mitigate them

mitigate them.

The Guidelines for the Internal Control System of the Landi Group defined by the Board of Directors identify the

Internal Control System as a cross-sectional process integrated with all the company activities, based on the

international principles of Enterprise risk management, and in particular on the framework CoSo Report indicated by

the Sarbanes-Oxley Act of 2002 as a reference best practice for the architecture of internal control systems. The

purpose of the Internal Control System is to help the Group to realize its performance and profit objectives, to

obtain reliable economic-financial information and to ensure compliance with the laws and regulations in force,

avoiding damage to the company's image and economic losses. In this process, particular importance is given to

the identification of corporate objectives and the classification and control of the business risks connected to

Half-yearly financial report – H1 2012 ________________________________________________________________ 25

them, through the implementation of specific actions aimed at containing such risks. There can be various types

of business risks: strategic, operational (related to the effectiveness and efficiency of business operations),

financial, reporting (related to the reliability of economic-financial information) and, lastly compliance (related to

the observance of the laws and regulations in force, to avoid the company suffering damage to its image or

and/or economic losses). In addition, all these risks can originate within or outside the Group. The exposure of

the Group to the above-mentioned risks has not changed significantly compared with 31 December 2011.

Those in charge of the various branches of company management identify and assess the risks within their

jurisdiction and identify actions to limit and reduce them (so-called “first line control”).

To the above-mentioned activities we can also add those of the Manager in charge of drafting corporate

documents and his staff (so-called “second level control”), the Supervisor for Internal Control (so-called “third

level control”), who continuously monitors the efficiency and effectiveness of the internal control system

through risk assessment activities, the cyclical performance of audit operations and the subsequent management

of follow up.

The results of the risk identification procedures are reported and discussed at the Top Management level of the

Group in order to create the prerequisites for their cover, insurance and for the assessment of the residual risk.

The following paragraphs describe the risks considered to be significant and connected with the activities of the

Group (the order in which they are listed does not imply any indication, either in terms of probability of their

occurrence or in terms of possible impact).

STRATEGIC RISKS

Risks connected with the international expansion strategy

The Group sells its products in more than 50 countries, in 11 of which it operates directly through its own

companies. During these six months, the Group achieved 69.1% of consolidated revenues abroad.

In pursuing its expansion strategy, the Landi Group has invested, and may invest more in the future, also in

countries characterized by considerable instability of their political institutions and/or at the center of situations

of international tension. The above-mentioned strategy could expose the Landi Group to various risks of a

macroeconomic nature, arising, for example, from changes in the political, social, economic and regulatory

systems of such countries or from extraordinary events such as acts of terrorism, civil disorder, restrictions on

trade, sanctions, limitation on foreign investment, nationalization and inadequate protection of intellectual

property rights. The probability of the above mentioned events actually occurring varies from country to

country and is difficult to predict. However, a constant monitoring activity is carried out by company Top

Half-yearly financial report – H1 2012 ________________________________________________________________ 26

management in order to become aware of any changes as early as possible, so as to minimize any economic

impact that may ensue.

Risks related to growth

The Group aims at continued growth by means of a strategy based on gaining strength in the markets where it is

already present and on further geographical expansion. In the context of such a strategy, the Group could

encounter difficulties in managing the adaptation of the structure and business model or in the ability to identify

market trends or the preferences of local consumers. Furthermore, the company may have to incur start-up costs

arising from the opening of new companies. Lastly, in the case where the Group's growth is pursued through

external lines through acquisition transactions, it may encounter, amongst other things, difficulties related to the

correct valuation of the assets acquired, to the integration of such assets and also to the failure to achieve the

expected synergy, which may have a negative impact on the activity and on the future economic-financial

results of the Group.

Risks connected with the recoverability of intangible assets, in particular goodwill

Intangible assets totaling € 92,690 thousand are reported in the consolidated financial statements at 30 June 2011,

including € 8,875 thousand for development expenditure, € 55,582 thousand for goodwill, € 28,233 thousand for

trademarks and licenses, as well as net prepaid tax totaling € 13,992 thousand. The recoverability of such values

is related to the materialization of future product plans and the cash generating unit to which they refer.

In particular, in the context of its development strategy, the Landi Group has acquired companies that have

allowed it to increase its market presence and to take advantage of the opportunities for growth that it provides.

In regard to such investments, recorded in the financial statements as goodwill, there is no guarantee that the

Landi Group will succeed in achieving the benefits originally expected from these operations.

The Landi Group constantly monitors the progress of performance in comparison to the forecast plans, initiating

the necessary corrective actions whenever unfavorable trends emerge that may involve significant changes in

expected cash flows used for impairment test when evaluating the coherency of the values recorded in the

financial statements.

OPERATING RISKS

Risks connected to relationships with OEM customers

The Landi Group distributes and sells its systems and components to the main automobile manufactures at a

world-wide level (OEM customers). In the half-year ending 30 June 2012, sales of systems and components by

the Landi Group to OEM customers represented approximately 37% of the total sales of such products. The

Group boasts long-standing relationships with the main world-wide automobile manufacturers. The ability of

Half-yearly financial report – H1 2012 ________________________________________________________________ 27

the group to strengthen the existing relationships with such customers, or to establish new relationships, is a

determining factor in order to consolidate the leadership position that Landi Group holds in the market. The

relationships with OEM customers are typically governed by agreements that do not require minimum purchase

quantities. Therefore the demand for predefined quantities of Landi Group products from such customers

cannot be guaranteed. In order to best satisfy the requirements of various customers to its best ability, the Landi

Group has over the last few years initiated a policy of delocalization of part of its production in countries where

it already has a number of customers and is attempting to do the same in other countries. Due to these

considerations, and also in the light of the competitive advantage acquired in the offer of solutions for the

development of sales in the After Market channel, the Group does not consider itself to be a subject with a

significant risk of dependency on OEM customers. However, it is not possible to exclude the fact that a possible

loss of important customers or a reduction in orders from them or a delay in collection compared to contractual

stipulations may determine negative effects on the economic-financial results of the Group.

Product liability risks

Any design or manufacturing defects in the products of the Landi Group, also attributable to third party subjects

such as suppliers and installers, may generate product liability against third party subjects. In addition, should

the products turn out to be defective or fail to comply with technical and legal specifications, the Landi Group,

also at the request of its customers, could be obliged to withdraw such products from the market while incurring

the related costs. For these reasons an insurance structure has been set up that is centered on master policies

negotiated and contracted centrally and local policies of initial risk. The latter guarantee immediate activation of

the cover which is supplemented by master policies where the impact of the damage exceeds the local maximum

amount. In addition, allocations are made to appropriate risk provisions determined on the basis of historical

analysis and through evaluation of the individual commercial contracts signed with the main customers.

FINANCIAL RISKS

Interest rate risk

The Landi Group is exposed to the interest rate risk associated both with cash at hand and with short, medium

and long term financing. The exposure refers mainly to the Euro zone. As regards exposure to the risk of interest

rate volatility, note that the financial indebtedness is regulated primarily by variable interest rates. Therefore, the

financial management of the Group remains exposed to fluctuations in interest rates, not having, at the date of

the present financial statements, subscribed to instruments covering the variability of the interest rates on loans

contracted with the banks.

Exchange risk

Half-yearly financial report – H1 2012 ________________________________________________________________ 28

The Landi Group sells part of its production and, although to much lesser degree, also purchases some

components also in Countries outside the Euro zone. In relation to the exchange risk, note that the amount of the

consolidated equity balances expressed in currency other than the functional currency is to be considered as

rather insignificant at Group level, although more important for the Iranian and Pakistani subsidiaries. The

Group has not subscribed to any instruments to cover exchange rate fluctuations and, in accordance with the

Group’s policy up to this moment, no speculative derivatives have been subscribed.

Credit risk

Credit risk is the risk that a customer or one of counterparts of a financial instrument causes a financial loss

through failure to fulfill an obligation and derives primarily from trade receivables, from other financial assets

and from guarantees that may have been given by the Group.

Trade receivables and other receivables

The Group normally deals with known and reliable customers. It is the Landi Group's policy to subject

customers requesting extended payment conditions to procedures for checking their credit class. This check also

includes external assessments when available. In addition, the balance of the receivables is monitored on a

fortnightly basis over the period, in order to minimize exposure to the risk of losses. Finally, regarding new

customers and those not operating in EU countries, a letter of credit to guarantee successful collection is

normally used, where possible.

The Parent Company insures part of its foreign receivables, which are not guaranteed by letters of credit,

through a leading Insurance Company and makes use of pro-soluto assignment of debts. The Group allocates a

provision for loss of value that reflects the estimated losses on trade receivables and on other creditors, made up

primarily of individual write-downs of significant exposures.

Lastly, we point out that the persistence or deterioration of the current economic and financial crisis could have

an impact, even significantly, on the capacity of some client companies to regularly meet their obligations to the

Group.

Other financial assets

The credit risk regarding the other financial assets of the Group, including cash and cash equivalents, presents a

maximum risk equal to the book value of these assets in the case of insolvency of the counterpart.

Guarantees

The policies of the Group provide for the issue of financial guarantees only in favor of subsidiary companies.

Liquidity risk

The liquidity risk is the risk that the Group may have difficulty in meeting obligations associated with financial

Half-yearly financial report – H1 2012 ________________________________________________________________ 29

liabilities. The Landi Group manages the liquidity risk by maintaining an adequate level of available financial

resources and bank credit granted by the main Credit Institutions, in order to satisfy the finance requirements of

the operational activity. The uncertainty in the markets in which the Group operates and of the financial markets

requires particular attention in managing the liquidity risk and, to this end, particular attention is given to the

actions aimed at generating financial resources with operating activities and at maintaining an adequate level of

cash and cash equivalents as an important factor in facing this and future years. Therefore, the Group expects to

deal with the necessities arising from receivables falling due and from investments planned by means of flows

deriving from operating activities, available liquidity, and the renewal or refinancing of bank loans.

The Group has not adopted a specific policy for management of the centralized treasury. In particular, the

management of the ordinary treasury is delegated locally to the individual companies of the Group, while the

extraordinary treasury is subject to the decision-making process of the Parent company.

2.8. OTHER INFORMATION Transactions with related parties

The creditor/debtor relationships and economic transactions with related companies are the subject of a specific

analysis in “Explanatory Notes to the Abbreviated Half-yearly Consolidated Financial Statements” to which you

may refer. Please also note that sales and purchases between the parties cannot be qualified as either atypical or

unusual, as they are part of the normal activities of the Group companies, and that they are carried out at normal

market values. Regarding the relationships with the parent company Girefin S.p.A., also bear in mind that the

Directors of Landi Renzo S.p.A. do NOT consider it to exercise the management and coordination activities

provided for by article 2497 of the Italian Civil Code. Lastly, please note that in accordance with CONSOB

Regulation 17221/2010, and pursuant to Article 2391-bis of the Civil Code, the Board of Directors has adopted

the specific procedure for transactions with related parties, available on the company website, to which you are

referred.

Positions or transactions deriving from atypical and/or unusual transactions

Pursuant to CONSOB communication no. 6064293 of July 28th 2006, note that during the six-month period no

atypical and/or unusual transactions occurred outside the normal operation of the company that could give rise

to doubts regarding the correctness and completeness of the information in the financial statements, conflicts of

interest, the protection of company assets or the safeguarding of minority stockholders.

Treasury shares and shares of parent companies

In compliance with the provisions of article 2428 of the Italian Civil Code, it is confirmed that during the year

2011 and the first six months of 2012 the Parent company did not negotiate any treasury shares or shares of

parent companies and does not at present hold any treasury shares or shares of parent companies.

Half-yearly financial report – H1 2012 ________________________________________________________________ 30

Sub-offices

No sub-offices were set up.

Half-yearly financial report – H1 2012 ________________________________________________________________ 31

2.9. SIGNIFICANT EVENTS AFTER CLOSING OF THE SIX-MONTH PERIOD AND FORECAST FOR OPERATIONS

After the closing of the six-month period and up to the present we point out that:

registrations of motor vehicles in Italy in the period January-July (ANFIA figures) totaled 928,064 units,

a decrease of 19.9% compared to the same period in 2011. In July 2012 a total of 109,380 vehicles were

registered, a decrease of 21.6% compared with volumes in 2011. also in July 2012 (UNRAE figures)

registration of LPG and CNG bi-fuel vehicles represented 13.4% of the total (5.2% in July 2011), including

9.8% LPG and 3.5% CNG.

since 18 July 2012, as mentioned in the introduction, the company structure acquired on rental with

conditional purchase of the former SAFE business unit has been active, for which, taking account of

current jobs in the portfolio, good revenue prospects are expected over the next six-month period.

on 30 July 2012 an agreement was signed setting up a joint venture in India between Landi Renzo S.p.A.

and Krishna Group, which will have the aim of becoming a leader in the supply of automobile gas

conversion systems for the Indian OEM sector, and in particular for the customer Maruti Suzuki.

Forecast for operations

The performance of the first six months is aligned with the Group's forecasts for the year 2012, posting positive

results regarding both revenues and margins, despite ongoing difficulties related to the macroeconomic scenario

and the reference market, including the business restrictions related to problematic countries in South West

Asia.

As regards the foreseeable future development of operations, the Landi Group confirms a positive outlook for

2012 with turnover up by more than 5% compared with 2011, and EBITDA margin greater than 10%, also due to

the consolidation of all the activities for optimization of structural and product costs already implemented as of

2011. The extraordinary operation linked to the company structure acquired on rental ex Safe represents, in the

current year, an additional turnover of more than € 6 million.

Cavriago, 28 August 2012

Chief Executive Officer: Claudio Carnevale

Half-yearly financial report – H1 2012 ________________________________________________________________ 32

3. ABBREVIATED SIX-MONTHLY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AS AT 30 JUN 2012

3.1. CONSOLIDATED STATEMENT OF FINANCIAL POSITION

ASSETS (thousands of Euros) Notes 30/06/2012 31/12/2011 30/06/2011

Non-current assets

Property, plant and equipment 2 33,341 35,096 37,156

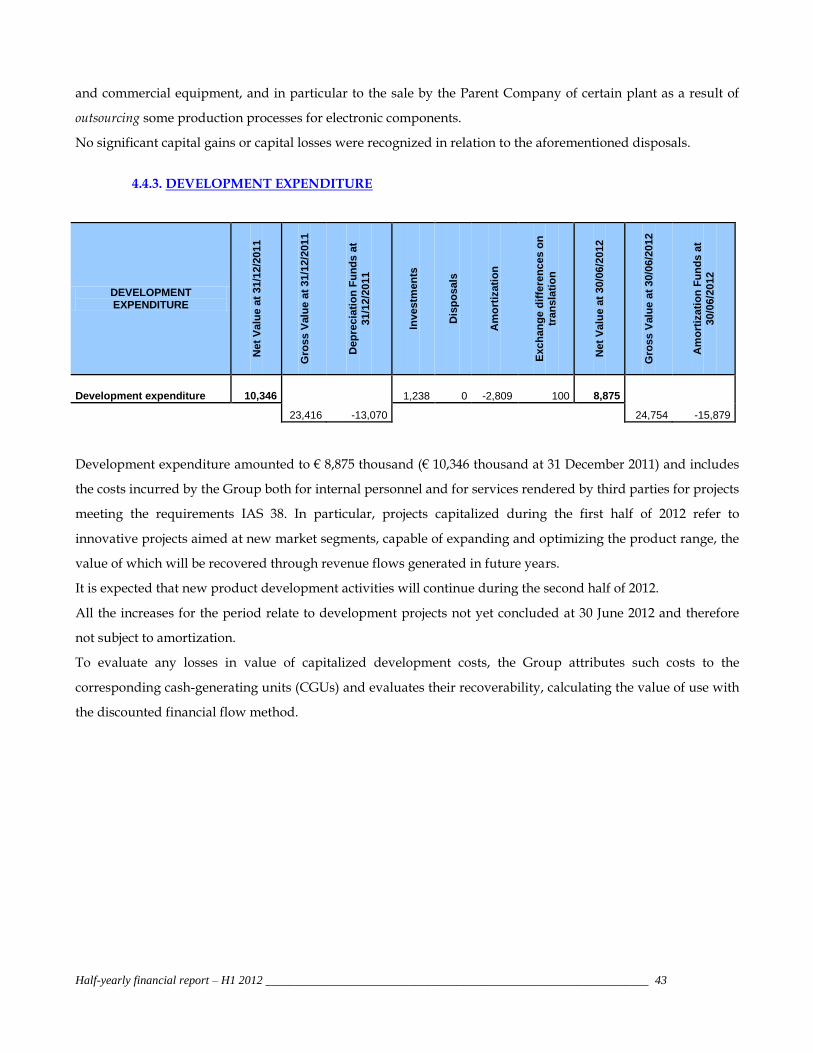

Development expenditure 3 8,875 10,346 10,992

Goodwill 4 55,582 55,582 59,498

Other intangible assets with finite useful lives 5 28,233 29,506 30,328

Other non-current financial assets 6 192 170 259

Deferred tax assets 7 13,992 13,274 9,632

Total non-current assets 140,215 143,974 147,865

Current assets

Trade receivables 8 92,423 77,429 79,837

Trade receivables - related parties 285 361 461

Inventories 9 79,028 67,408 74,079

Other receivables and current assets 10 20,549 27,452 30,389

Current financial assets 11 174 176 152

Cash and cash equivalents 12 24,978 20,059 24,557

Total current assets 217,437 192,885 209,475

TOTAL ASSETS 357,652 336,859 357,340

EQUITY AND LIABILITIES (thousands of Euros) 30/06/2012 31/12/2011 30/06/2011

Equity

Share capital 11,250 11,250 11,250

Other reserves 125,212 134,154 132,951

Profit (loss) for the period 2,606 -9,138 -2,397

Total equity attributable to the shareholders of the parent 139,068 136,266 141,804

Minority interests 780 738 447

TOTAL EQUITY 13 139,848 137,004 142,251

Non-current liabilities

Bank loans 14 30,442 40,119 53,580

Other non-current financial liabilities 15 49 49 123

Provisions for risks and charges 16 5,292 4,860 4,240

Defined benefit plans 17 2,938 2,835 3,067

Deferred tax liabilities 18 11,060 12,351 13,103

Total non-current liabilities 49,781 60,214 74,113

Current liabilities

Bank overdrafts and short-term loans 19 65,978 69,878 50,996

Other current financial liabilities 20 74 125 252

Trade payables 21 86,358 55,903 75,671

Trade payables – related parties 61 61 334

Tax liabilities 22 6,965 6,458 5,203

Other current liabilities 23 8,587 7,216 8,520

Total current liabilities 168,023 139,641 140,976

TOTAL EQUITY AND LIABILITIES 357,652 336,859 357,340

Half-yearly financial report – H1 2012 ________________________________________________________________ 33

3.2. GENERAL CONSOLIDATED INCOME STATEMENT

GENERAL CONSOLIDATED INCOME STATEMENT (thousands of Euro) Note

s 30/06/2012 30/06/2011

Revenues (goods and services) 24 139,143 126,844

Revenues (goods and services) - related parties 12 899

Other revenue and income 25 959 678

Cost of raw materials, consumables and goods and change in inventories 26 -62,422 -61,296

Costs for services and use of third party assets 27 -37,961 -32,976

Costs for services and use of third party assets – related parties -788 -762

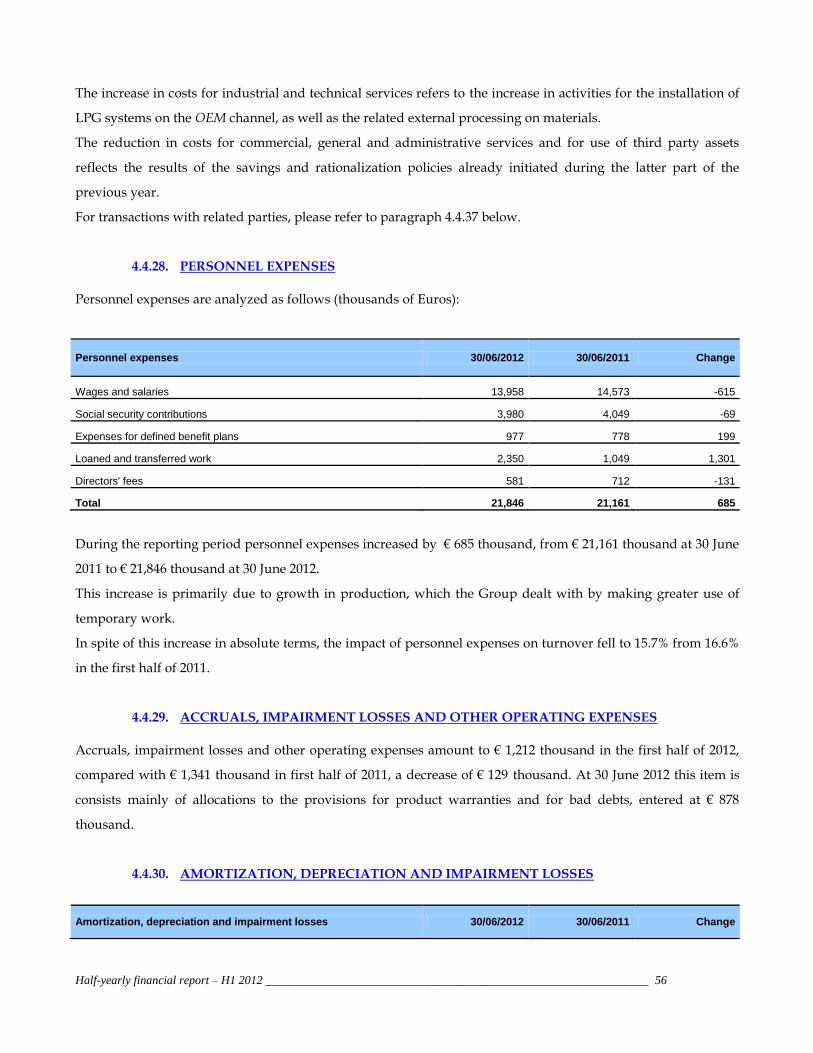

Personnel expenses 28 -21,846 -21,161

Accruals, doubtful debts and other operating expenses 29 -1,212 -1,341

Gross Operating Profit 15,885 10,885

Amortization, depreciation and impairment losses 30 -9,149 -9,088

Operating Profit 6,736 1,797

Financial income 31 352 271

Financial expenses 32 -2,177 -1,600

Exchange rate gains (losses) 33 -9 -2,216

Profit (Loss) before tax 4,902 -1,748

Taxes 34 -2,177 -907

Net profit (loss) for the Group and minority interests, including: 2,725 -2,655

Minority interests 119 -258

Net profit (loss) for the Group 2,606 -2,397

Basic earnings (loss) per share (calculated on 112,500,000 shares) 35 0.0232 -0.0213

Diluted earnings (loss) per share 0.0232 -0.0213

OTHER COMPONENTS OF THE GENERAL INCOME STATEMENT (thousands of Euro) 30/06/2012 30/06/2011

Net profit (loss) for the Group and minority interests: 2,725 -2,655

Exchange rate differences from conversion of foreign operations 191 -1,609

Other Equity movements from foreign operations 0 0

Profits/Losses recorded directly to Equity net of tax effects 191 -1,609

Total general income statement for the year 2,916 -4,264

Profit (loss) for Shareholders of the Parent Company 2,803 -3,952

Minority interests 113 -312

Half-yearly financial report – H1 2012 ________________________________________________________________ 34

3.3. CONSOLIDATED CASH FLOW STATEMENT

CASH FLOW STATEMENT (thousands of Euros) 30/06/2012 31/12/2011 30/06/2011

Opening cash and cash equivalents -49,819 -2,110 -2,110

Profit (Loss) before tax (less minority interests) 4,782 -8,212 -1,489

Adjustments for:

Net financial Income / (Charges) including exchange rate differences 1,834 4,737 4,878

Amortization, depreciation and impairment losses 9,149 18,421 9,088

Impairment of tangible and intangible fixed assets 0 4,316 0

Changes in provisions and benefits for employees 347 343 22

Changes in other provisions 1,105 107 -513

Net change in deferred taxes -2,008 -2,567 0

(Increase) decrease in current assets:

Inventories -11,621 -428 -7,099

trade receivables -14,994 2,757 348

trade receivables – related parties 76 351 251

receivables from others and other receivables 6,526 -6,149 -9,062

Increase (decrease) in current liabilities:

trade payables 30,454 -4,285 11,198

trade payables – related parties 0 -293 -20

payables to others and other liabilities 1,321 1,747 1,796

Financial flow from (for) operating activities 26,971 10,845 9,398

Net interest paid (including exchange rate differences realized) -1,630 -4,737 -1,334

Income taxes paid -1,152 -5,833 -2,946

Net financial flow from (for) operating activities 24,189 275 5,118

Investments in intangible assets -1,062 -1,307 -1,559

Development expenditure -1,238 -3,089 -1,450

Investments in property, plant and equipment -3,850 -10,495 -6,514

Proceeds from the sale of fixed assets 478 569 0

Investments in other non-current financial assets -21 52 0

Financial flow for acquisition of equity investments -5,693 -14,270 -9,523

Dividends paid in the period 0 -6,188 -6,188

Loans obtained/repaid to/from banks and other financial backers during the period -9,677 -27,079 -13,417

Payments for reduction of payables for financial leasing 0 -447 -318

Financial flow from (for) financing activities -9,677 -33,714 -19,923

Total financial flow 8,819 -47,709 -24,328

Closing cash and cash equivalents -41,000 -49,819 -26,438

This statement, as required by IAS 7 paragraph 18, was prepared using the indirect method; the items posted in the current year were uniformly included in the previous year's statement. The opening and closing cash and cash equivalents reflect the difference between cash and cash equivalents and bank overdrafts and short-term loans.

Half-yearly financial report – H1 2012 ________________________________________________________________ 35

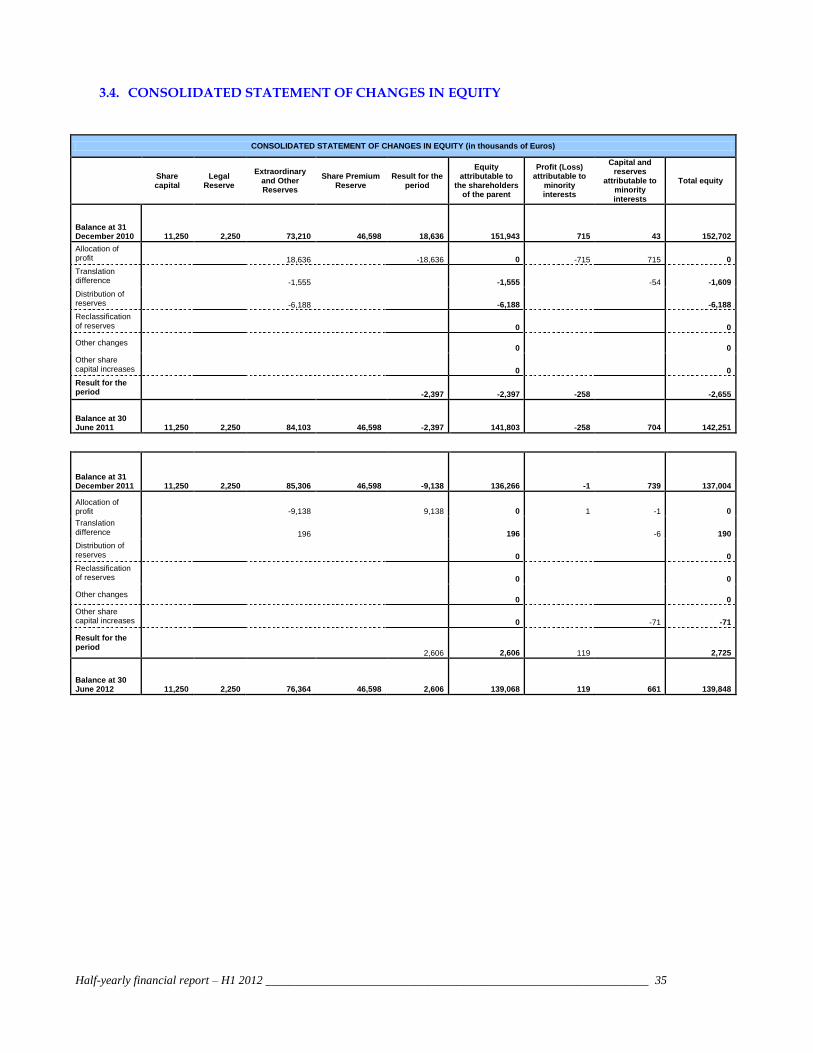

3.4. CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY (in thousands of Euros)

Share capital

Legal Reserve

Extraordinary and Other Reserves

Share Premium Reserve

Result for the period

Equity attributable to

the shareholders of the parent

Profit (Loss) attributable to

minority interests

Capital and reserves

attributable to minority interests

Total equity

Balance at 31 December 2010 11,250 2,250 73,210 46,598 18,636 151,943 715 43 152,702

Allocation of profit 18,636 -18,636 0 -715 715 0

Translation difference -1,555 -1,555 -54 -1,609

Distribution of reserves -6,188 -6,188 -6,188

Reclassification of reserves 0 0

Other changes 0 0

Other share capital increases 0 0

Result for the period -2,397 -2,397 -258 -2,655

Balance at 30 June 2011 11,250 2,250 84,103 46,598 -2,397 141,803 -258 704 142,251

Balance at 31 December 2011 11,250 2,250 85,306 46,598 -9,138 136,266 -1 739 137,004

Allocation of profit -9,138 9,138 0 1 -1 0

Translation difference 196 196 -6 190

Distribution of reserves 0 0

Reclassification of reserves 0 0

Other changes 0 0

Other share capital increases 0 -71 -71

Result for the period

2,606 2,606 119 2,725

Balance at 30 June 2012 11,250 2,250 76,364 46,598 2,606 139,068 119 661 139,848

Half-yearly financial report – H1 2012 ________________________________________________________________ 36

4. EXPLANATORY NOTES TO THE ABBREVIATED SIX-MONTHLY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AS AT 30 JUNE 2012

4.1. GENERAL INFORMATION

The LANDI RENZO Group has been active for more than fifty years in the automotive fuel supply systems

sector operating in the design, manufacture installation and sale of eco-compatible LPG and CNG systems (the

“LPG line” and “CNG line” respectively). To a much lesser extent, the Group also deals with car audio and

alarm systems under the MED brand through its subsidiary A.E.B. S.p.A. The Group also maintains commercial

and technical collaboration relationships with the main car manufacturers at a world-wide level (OEM

customers) and with independent retailers and importers (After Market customers).

Note that the structure of the Group has not changed compared with 31 December 2011.

The parent company of the LANDI RENZO Group is Landi Renzo S.p.A. with its registered office in Cavriago

(RE). The company is listed on the Milan Stock Exchange in the FTSE Italy STAR segment.

4.2. GENERAL PREPARATION CRITERIA AND CONSOLIDATION PRINCIPLES

4.2.1. Premise

The abbreviated half-yearly consolidated financial statements at 30 June 2012 were prepared pursuant to Article

154-ter of Legislative Decree 58/1998 “Consolidated Financial Law (Testo Unico della Finanza)”, in accordance

with the provisions of international accounting principles (IAS/IFRS) recognized in the European Community,

and in particular those of IAS 34 “Interim Financial Statements”. In partial exception to the provisions of IAS 34,