handling of adjudication & appellate proceedings in service tax by: a.saiprasad b.com, ll.b,...

TRANSCRIPT

Handling of Adjudication & Appellate Proceedings

in Service Tax

By:A.Saiprasad

B.Com, LL.B, ACA, (Grad CISA), DISA, AMIMA

Advocate

Session Outline - I Visits by Departmental Officers Service Tax Audit Search Seizure & Summons Adjudication Proceedings

Issue of Show Cause Notice Reply to Show Cause Notice Personal Hearing Issue of Order in Original

Session Outline - II

Recovery Proceedings Reply to Coercive Letters

Appeals to Commissioner (Appeals) Time Limit, SOF, GOA, Cross Objections

Appeals to CESTAT Time Limit, SOF, GOA, Cross Objections

Practical Demonstration

Visit by Departmental Officers

One Fine Day…. Access to Regd. Premises – R.5A of STR, 94

Officer authorised by Commissioner Registered Premises Scrutiny Verification & Checks

Madurai Trade Notice No.103/99 dt.1.10.99 Routine Checks Barred Prior Notice – 15 clear days + Doc. Reqd.

Visit by Departmental Officers Any Restriction for Evasion Cases ?

Specific Information, Intelligence Reason to believe

No Restriction for Writing Letters Records to be produced on demand Immediate Reply

Board Circulars No.137/26/2007-CX 4 dt.1.1.08 224/37/2005-CX 6 dt.24.12.08

Audit Party Authorised CEO/ C & AG deputed Excise Audit 2000 norms followed Gathering Information - Letters Audit Frequency

Tax > 3 Crs – Every Yr Tax 1 Cr – 3 Crs – Once in 2 Yrs Tax 25 L – 1 Cr – Once in 5 Yrs Tax < 25 L – 2% of tax payers

Reply to Audit Note Records to be provided & Time Limit Audit Reply to Audit Paras

Example: Mgmt Con Services for EDP classes Letter head of Auditee Date of Reply Concise extract of Audit para General/ Background Info about Auditee Facts of the case

Reply to Audit Note

Audit Reply Contd… Evidences to support facts of the case Extract of Relevant Provision Reliance on Case Laws if any Furnishing of further info Copies of docs supporting as

evidences

Search & Seizure

S. 82 of FA, 94 – SEARCH & SEIZURE Document, Book or Thing Useful or Relevant to any proceeding Secreted JC – Authorise – SI SEARCH & SEIZE Cr.P.C Code Applicable

Summons S. 83 of FA, 94 r/w S.14 of CEA, 44

Summons – Person or Document Board Circular No.137/39/2007-CX

dt.26.2.07 Usual Mode of Communication ineffective Jeopardize interest of Revenue To tender evidence, To record statement Prior written permission - DC

Meaning of SCN Formal Communication to Show Cause why Actions proposed therein Must not be taken against the assessee Opportunity to explain defence Provides information about:

Computation of tax by department Arrival at taxable value by the department Department’s view of the provisions

When SCN not issued Service Tax + interest paid

On own accord Before Department’s awareness – No fraud etc Informs in writing to the department

ST + Int + Penalty paid At the time of audit – Though fraud etc. True & Correct information + Specified Records Penalty 1% p.m. of default – max 25% Informs in writing to the department

Show Cause Notice Date of Service of SCN

Back Dating Receipt Body of SCN

Example: CTCC issued to Edn Orgn. Details of Assessee Registration Details Facts of the case – whether twisted ? Incidental & Ancillary Information

Show Cause Notice

Body of SCN Period of Demand

Ordinary Period – 18 M from RD Extended Period – 5 Yrs from RD

Computation of Value of Taxable Service

P&L – All items on the Credit Side B/S – Debtors Incremental Value

Computation of Tax

Show Cause Notice Body of SCN

Inferences drawn from facts Extract of Relevant Provision

Whether any amendment/ additions/ deletions

Reference to Service Tax Return Not filed Value not included

Listing of Omission or Commission For Extended period of limitation

Show Cause Notice Body of SCN

Interest Provisions Penalty Provisions Operative Part of SCN – Calling upon to

show cause why: ST, Int, Penalty must not be demanded Service not a taxable service Classification under a particular service Valuation method to be adopted/ not adopted Abatement available/ not available

Reply to SCN

Letterhead of Counsel/ Assessee Reply Addressed to whom Details of SCN No. & Date Name of the Assessee Address of the Assessee Reference to POA, Vakalat Desire for Personal Hearing

Reply to SCN Summary of Allegations in SCN

Succinct, Brief, Most important points Defence Contentions

On Limitation On Merits On Interest On Penalty On Refund & On Such other specific issues

Reply to SCN

Preliminary Contentions…. SCN issued merely based on audit objection No independent investigation by Department

Swastik Tin Works v. CCE, 1986 (25) ELT 798 (Special Bench-Tribunal),

Indian Plastics Ltd. v. CCE, 1988 (35) ELT 434 (T), CIT v. Lucas TVS Ltd., 2001 (249) ITR 306 (SC), Indian and Eastern Newspaper Society v. CIT,

1979 (119) ITR 996 (SC)

Reply to SCN

Preliminary Contentions…. SCN – made up mind/ pre-deciding issues Evidences from the SCN – Reference

Madurai Metal Industries Vs UOI, 1991 (52) ELT 495 (Mad.).,

Siemens Ltd Vs.State of Maharashtra 2007 (207) ELT 168 (SC),

Reply to SCN

On Limitation – S. 73 Ordinary Period – S. 73(1) Extended Period – Proviso to S.73(1)

Relevant Date – S. 73(6) Filed Returns Not Filed Returns Date of payment/ refund of service

tax

Reply to SCN

On Limitation – Extended Period Fraud Collusion Wilful Mis-statement Suppression of facts Contravention of provision of act

With an intention to evade payment of tax

Reply to SCN - On Limitation

Correspondence with Department Attach as evidences to reply Proves department aware

Inter-departmental correspondence No clarity on levy

Case Laws Ugam Chand Bhandari Vs. CCE, 2004 (167)

ELT 491 (SC); Anand Nishikawa Co. Ltd V. CCE, 2005 (188)

ELT 149 (SC).

Reply to SCN - On Limitation

Prove Dept aware of primary facts No Duty to bring in legal inferences

Calcutta Discount Co. Vs. ITO, (1961) 41 ITR 191 (SC),

Parashuram Pottery Works Co. Ltd. v. ITO, (1977) 106 ITR 1 (SC),

Reply to SCN - On Limitation

Undue delay in issuance of SCN Delay > 18 M from Date of Knowledge(DOK) DOK = Audit Report, Mahazar, Summons DOK = Stmt of A’ee/ Dept, Letter/ Return filed

with dept. Rivaa Textile Industries Ltd. Vs. CCE & C, 2006

(197) ELT 555 (T) Dolphin Detective Agency Vs. CCE, 2006 (4) STR

217 (T), Bajaj Auto Ltd. Vs. CCE, 2006 (195) ELT 277 (T),

Reply to SCN - On Limitation

Bonafide Belief/ Doubt Clarification provided by Board SC/ HC/ Tribunal Decisions

SNS (Minerals) Ltd. v. UOI, 2007 (210) ELT 3 (SC)

Periodical SCNs – cannot allege suppression Reference to previous SCNs with No, Dt &

Period Nizam Sugar Factory Vs. UOI, 2006 (197) ELT 465

(SC), ECE Industries Limited v. CCE, 2004(164) ELT 236

(SC),

Reply to SCN - On Limitation

Burden of proof – Not Discharged Something positive Other than mere inaction Deliberate with holding of information Department’s knowledge of:

Facts Manufacturer’s action/ inaction

CCE v. Chemphar Drug and Liniments, 1989 (40) ELT 276 (SC) &

CCE v. Pioneer Scientific Glass Works, 2006 (197) ELT 308 (SC).

Reply to SCN - On Limitation

Shorn of proof No Reason to believe Absence of records/ materials

To prove omission & commissions TN Dadha Pharmaceuticals v. CCE, 2003 (152)

ELT 251 (SC) and New Decent Footware Industries v. UOI, 2002

(150) ELT 71 (Del.)

Reply to SCN - On Limitation

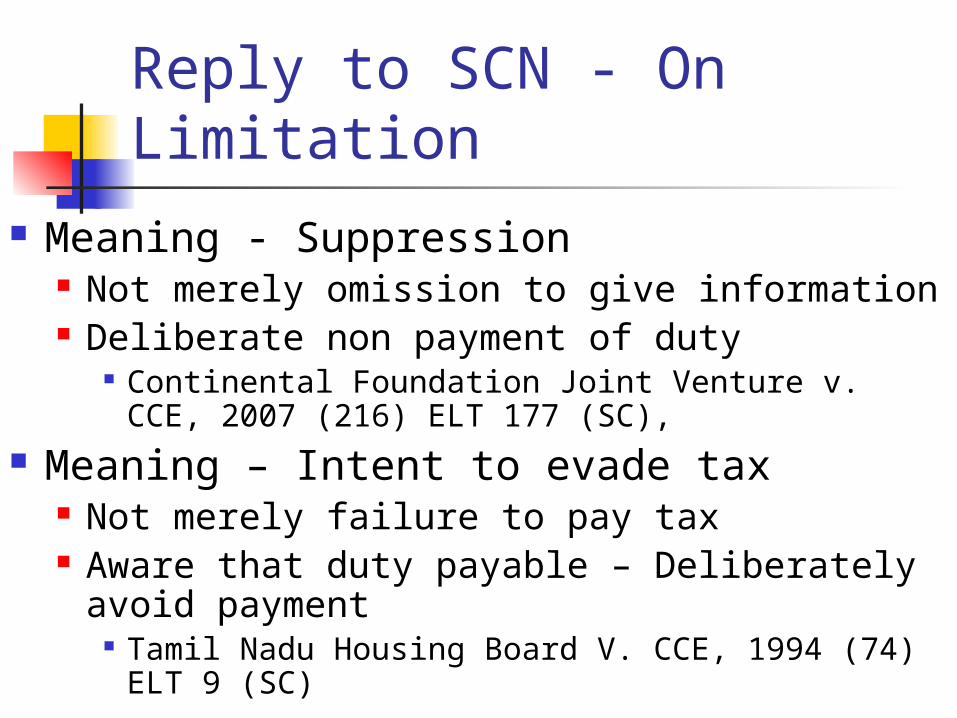

Meaning - Suppression Not merely omission to give information Deliberate non payment of duty

Continental Foundation Joint Venture v. CCE, 2007 (216) ELT 177 (SC),

Meaning – Intent to evade tax Not merely failure to pay tax Aware that duty payable – Deliberately avoid

payment Tamil Nadu Housing Board V. CCE, 1994 (74) ELT

9 (SC)

Reply to SCN – On Merits Extract Relevant Provision

Definition of the said service/ negative list Definition of declared service Amendment/ additions/ deletions/

substitutions Net effect not covered by definition

Interpretational issue Benefit of doubt to tax payer

Beyond scope and ambit of definition/ taxable service

Reply to SCN – On Merits

Rely on Board Circulars/ Trade Notices

Dept bound by circulars K. P. Varghese Vs. ITO, 1981 (131) ITR

597 (SC). Ranadey Micronutrients Vs. CCE, 1997

(87) ELT 19 (SC). Paper Products Limited Vs. CCE, 1999

(112) ELT 765 (SC).

Reply to SCN – On Merits

Reliance on: Interpretation of Statues

Construction of a term Law Lexicons

To prove the legal understanding of a term

Agnate & Cognate Statues Central Excise Act, 1944 Customs Act, 1962

Reply to SCN – On Merits

Reliance on Certificates given to A’ee by Govt Recognition granted by Govt

Institutions Documents founding the institution

Trust Deed, Partnership Deed MOA & AOA of Society Regn Deed

Agreements entered into with customers

Reply to SCN – On Merits Reliance on

Constitution – legislative entries Lack of power to tax certain area

Evidences on hand To prove - Not a service – Client

Agreements To prove – Value of service – Invoices To prove – Mistake in computation To prove – Eligibility to exemption To prove – Eligibility to abatement

Reply to SCN – On Merits

Reliance on Documents provided by clients

Product Details like brochures Technical details of services provided/ not

provided Different products provided by client

Some of which taxable on which tax already remitted Correspondences with chamber of commerce Correspondences with Government/ Board

Reply to SCN – On Merits

Reliance on Case laws – Covered issues Contradictory statements by SCN Vague statements by SCN Omission/ Commission not alleged by SCN Fundamentally incorrect provisions in SCN SCN not being signed

Reply to SCN – On Interest Not liable to tax

For reasons stated under limitation For reasons stated under merits

Since not liable to tax Not liable to interest Since interest accessory to demand

Case Laws: Pratibha Processors v. Union of India, 1996 (86)

ELT 12 (SC) and CC v. Jayathi Krishna & Co., 2000 (119) ELT 4 (SC)

Reply to SCN – On Penalty

Penalty – 3 Sections S. 76 – Mere non payment of ST

Rs.100/ day or 1% of Tax O/s for every month

Max Penalty – 50% of Tax S. 77 – For about 7 types of default

For defaults not covered elsewhere Eg: Not getting regd, Not filing returns

etc.

Reply to SCN – On Penalty

U/s 78 – Extended Period Levied when omission/ commission

commited Max Penalty 100% of ST True & Complete (T & C) – 50% of ST T & C + 30/ 60 days of OIO– 25% Transaction not recorded – No mitigation of

50% or 25%, though paid within time period

Reply to SCN – On Penalty

When S.78 penalty can be imposed ? Punishment Act of Deliberate Deception Intention to evade Duty – Proved UOI v. Rajasthan Spinning & Weaving

Mills, 2009 (238) ELT 3 (SC)

Reply to SCN – On Penalty

No extended period – No 78 penalty CCE V. Damnet Chemicals Pvt Ltd., 2007

(216) ELT 3 (SC) Devans Modern Breweries Ltd. V. CCE,

2006 (202) ELT 744 (SC) Strict Construction of Penal Provisions

CIT v. Sunderam Iyengar, AIR 1976 SC 255

Penalty – Summary ISituation Position

inRecords

Penalty &Provision

Mitigation CompleteWaiver

No fraud,suppressionetc.

Captured

1% of tax or Rs100 per day upto50% of taxamount: Sec 76

Totally mitigated if tax andinterest paid before issue ofnotice: Section 73(3)

On showingreasonablecause undersection 80

Penalty – Summary IISituation Positio

n inRecords

Penalty &Provision

Mitigation CompleteWaiver

Cases of fraud, suppression etc

Captured true and correct position in records

50% of tax amount: Proviso to Section 78

(a) 1% per month; max of25% if all dues paid beforenotice: Sec 73(4A);(b) 25% of tax if all duespaid within 30 days (90 daysfor small assesses): Provisosto Section 78

On showingreasonablecause undersection 80

Penalty – Summary III

Situation Position inRecords

Penalty &Provision

Mitigation

CompleteWaiver

Cases of fraud, suppression etc

Not socaptured

Equal amount:Section 78

No mitigation at all

Not possible

Reply to SCN – On Penalty

Interpretation of Statue – No penalty Since no intention to default Differences in understanding the statues

UG Sugars & Industries Ltd. v. CCE, 2004 (167) ELT 465 (T).

Standard Industries Ltd. v. CCE, 2007 (207) ELT 676 (T).

Fibre Foils Ltd. v. CCE, 2005 (190) ELT 352 (T).

Reply to SCN – On Penalty S. 80 – Reasonable Cause

Non Obstante Clause Over Rides S. 76, 77 & 78 Cause for non payment must be genuine

Bonafide Belief/ Doubt Based on Court Decisions Ignorance of law – no excuse

Case Laws CWT Vs. Sri Jagadish Prasad Choudhury, [1995] 211 ITR 472

(Pat.) In Motilal Padampat Sugar Mills Co. Ltd. Vs. State of Uttar

Pradesh, [1978] 118 ITR 326 (SC) , Vedabai v. Shantaram, [2002] 253 ITR 798 (SC)

Reply to SCN - Conclusion

Summary & Conclusion Action sought for by the reply Similar to prayer in appeals Permission for further written submissions Request for PH before adjudication Permission for submission at PH Request for drop of proceedings

Adjudication Order

Called as Order in Original Order based on SCN & Reply

thereto Order passed by:

AC, DC, JC, ADC Appealable to Commissioner (Appeals)

Commissioner Appealable to CESTAT

Persons passing Orders

Tax < Rs. 1 Lakh – Superintendent Tax Rs. 1 Lakh to 5 Lakhs – AC/DC Tax Rs.5 Lakhs to 50 Lakhs – JC Tax Rs. 20 Lakhs to 50 Lakhs – ADC Tax without limit – Commissioner

Board Circular No.97/8/2007 ST dt.23.8.07

Contents of OIO

Name of Assessee Date of Order Number of the Order To whom the appeal must be filed Where the appeal must be filed The Commissionerate under which OIO

passed

Contents of OIO

Details of the Assessee Brief facts of the case Allegations made by the SCN Operative part/ demand made by SCN Reply provided by the Assessee FINDINGS Order portion of the OIO

Contents of OIO

FINDINGS – Most important part of OIO Provides reasons for:

Demanding Duty/ Rejecting Refund Setting Aside Duty/ Granting Refund

Findings contains decision on: Limitation – Reason for invoking extended

period Merits – Why taxable, at what value, under

which classification subject to which exemptions/ abatement

Filing Appeal

First Appellate Authority Commissioner of CE (Appeals)

Orders passed by AC, DC, JC, ADC

Second Appellate Authority CESTAT

Jurisdiction - Southern Bench Located at Bangalore

Orders of Commissioner of CE/ ST Order of Commissioner of CE (A)

Incidental Information Time limit for filing appeal

2 months from date of service of OIO 1 month condonation of delay

Appeal Paper Book 2 copies to be submitted To contain SCN, Reply, OIO, Stay Application Other documents relied upon as evidence. Cleanly indexed and annexured along with

POA

Coercive Letter Letter received after OIO

But before time elapsed to file appeal After time elapsed for appeal but

Main Appeal/ Stay Appln pending hearing After PH is complete

Before Order In Appeal issued by CEA(A)

Letter issued demanding payment of Adjn levies by Recovery Cell/ Range Superintendent Non payment resulting in coercive actions by dept

Reply to Coercive Letter Statutory Right – To appeal

No demand during 2m + 1m period No demand after appeal registered No demand pending PH before CEA (A) No demand after PH before OIA

Circular No.396/29/98-C.X., dt.2.6.98, Circular No.788/21/04-CX., dt.25.5.04 Matigara Rolling Mills (P) Limited Vs. CCE, 2005 (185)

ELT 335 (T), FCM Travel Solutions (India) Private Limited v. CST,

2010 (18) STR 24 (T-Bang)

Commissioner Appeals Form ST 4

Initial Details – 7 points Statement of Facts Grounds of Appeal Verification & Prayer Stay Application

Prima Facie Case Balance of Convenience Financial Hardship

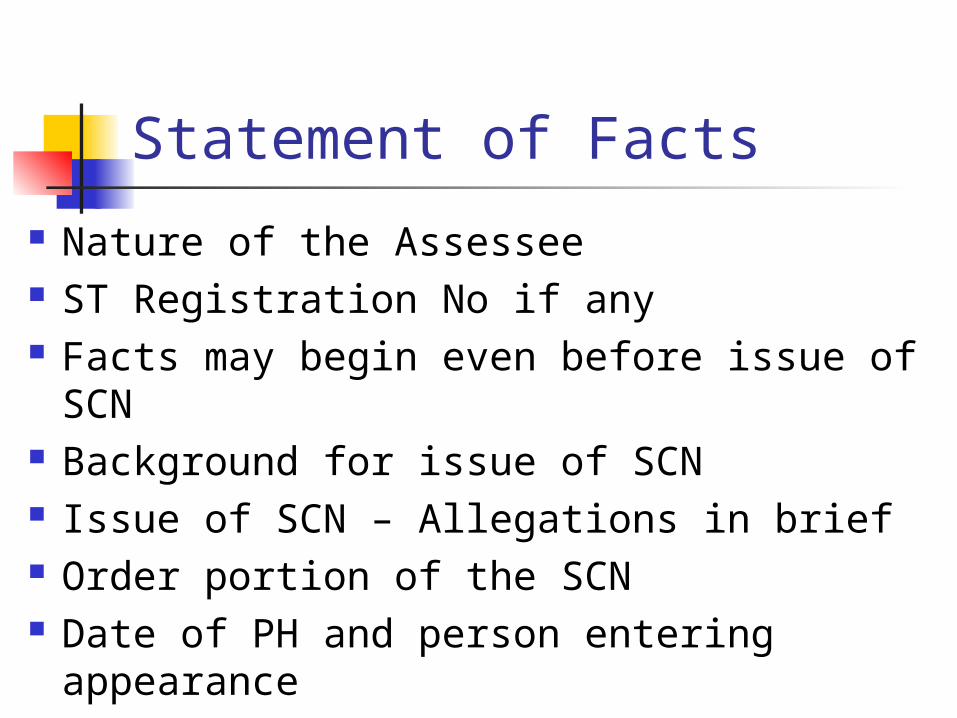

Statement of Facts

Nature of the Assessee ST Registration No if any Facts may begin even before issue of

SCN Background for issue of SCN Issue of SCN – Allegations in brief Order portion of the SCN Date of PH and person entering

appearance

Statement of Facts Order in Original No. & Date – Impugned

Order Order issued by whom – Respondent Demand made by OIO

Sections under which Tax, Int, Penalty demanded

Findings in the OIO Relating to Merits, Limitation & Penalty In brief

Grounds of Appeal

Demonstrate the mistakes in findings Mistakes in Findings on Limitation

Why finding on omission/ commission is incorrect

Departmental correspondences not considered ST 3 returns filed not considered Mahazar, Statement, Summons – contradicting

point not considered Burden of proof not discharged

Grounds of Appeal

Mistakes in Findings on Merits Incorrect provision reference made by OIO Certain provision which have been referred

to in Reply not considered Conditions which have been fulfilled –

treated as not satisfied Reference to documentary evidences in

Reply not considered

Grounds of Appeal Mistakes in Findings on Merits

Factual mistakes made by Findings Certain facts not considered Extraneous facts imbibed in OIO

Findings beyond allegations in SCN Adducing additional evidences

To prove the findings as factually incorrect Reliance on:

New case laws since filing reply New amendments made to law Board Circulars issued since filing reply

Grounds of Appeal

Mistakes in Findings on Interest & Penalty Incorrect Tax demand – Interest effect S.80 not invoked by Adjudicating Authority

Penalty not leviable due to reasonable cause SC/ HC/ Tribunal decisions

Issued since reply In relation to when penalty may be imposed Sec 76/ 78 penalty – not imposable simultaneously 25% penalty – if paid within 30 days of OIO service No penalty on interpretational issue

Grounds of Appeal

Prayer – Very Important Relief sought from appellate authority Set aside demand of tax, interest & penalty Classify service in a certain manner Value the service in a particular way Eligibility to avail exemption/ abatement

Ntfn Grant Refund along with interest

Grounds of Appeal

Verification That what is stated is true To the best of information & Knowledge To be signed by:

Assessee Authorised signatory of Assessee Rule 3 of CE (Appeals) Rules, 2001

Production of Additional Evidences Rule 5 of CE (Appeals) Rules, 2001 Effect of a comprehensive reply

Stay Application S. 83 of FA, 94 r/w S. 35F of CEA, 44 Reference to OIO No., Date, Demand Quantum of demand already paid – if any Amount of demand – Sought as stay Prima facie case –

Benara Valves Limited v. CCE, 2006 (204) ELT 513 (SC);

Mehsana District Milk PU Cooperative Ltd., Vs. UOI, 2003 (154) ELT 347 (SC)

Submissions on Balance of Convenience Submissions on undue hardship – with evidences

Appeals to CESTAT Appeal which CESTAT can hear

Order in Original issued by Commissioner Order in Appeal issued by Commissioner

(Appeals) Appeal which CESTAT cannot hear

Rebate of CE Duty Goods Exported without payment of CE

duty Loss of Goods in Transit

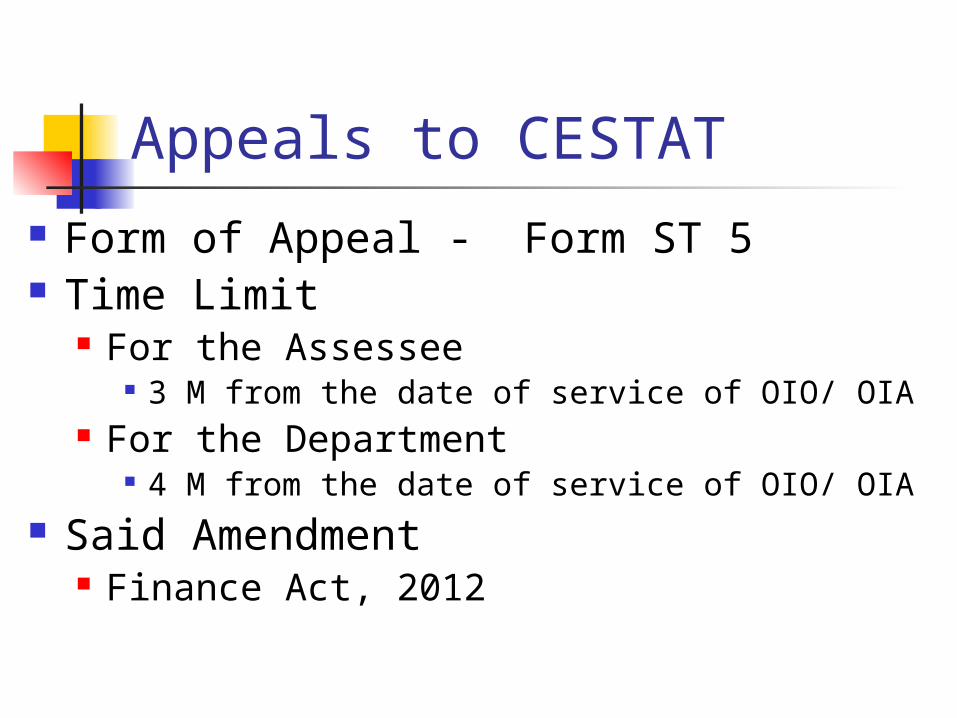

Appeals to CESTAT Form of Appeal - Form ST 5 Time Limit

For the Assessee 3 M from the date of service of OIO/ OIA

For the Department 4 M from the date of service of OIO/ OIA

Said Amendment Finance Act, 2012

Appeals to CESTAT

Statement of Facts In case of OIO

SOF similar to how filed before Commissioner Appeals

In case of OIA SOF - Addition to facts before Commissioner

Appeals OIA No. & Date – Impugned Order Findings of the OIA

Appeals to CESTAT

Whom to be made as Respondent In case of OIO

The Concerned Commissioner passing the OIO’ In case of OIA

NOT the Concerned CEA(A) who has passed the OIA

The Concerned Commissioner Under whose Jurisdiction OIO has been passed

Appeals to CESTAT How many appeals to be filed ? 5 SCNs – 1 Common OIO – 1 Common OIA

1 Appeal to be filed 5 SCNs – 5 Separate OIOs – 5 Separate OIA

5 Appeals to be filed 5 SCNs – 5 Separate OIOs – 1 Common OIA

5 Appeals to be filed Proviso to Rule 6A of CESTAT Rules, 82

Appeals to CESTAT

What to accompany MOA Division Bench

To be filed in Quadruplicate 1 copy of OIO/OIA – certified copy Certified Copy means

Original of the OIA/ OIO or Photocopy duly authenticated by concerned dept.

Single Bench To be filed in Triplicate

Appeals to CESTAT Memorandum of Cross Objection

When Department has filed the appeal To be filed within 45 days of service of notice To be filed in Form ST 6

Fee ST + Int + Penalty <= 5L - Rs.1,000 ST + Int + Penalty >5L, <= 50L – Rs.5,000 ST + Int + Penalty > 50L – Rs.10,000 Stay Application/ Misc Appln – Rs.500

Open House…

Thank You.