haywood’s junior mining universe

TRANSCRIPT

Haywood’s Junior Mining UniverseChris Thompson, P.Geo. (604-697-7433, [email protected])

Ben Asuncion (604-697-6149, [email protected])

-15%

-10%

-5%

0%

5%

10%

Au Ag Pt Pd Cu Ni Zn U

-15%

-10%

-5%

0%HDI HJEI HJPI HJBI HJDI HJUI

Leaked information from the Democratic Republic of Congo earlier this month, concerning a review of mining contracts, created turmoil for DRC-exposed companies. A number of these companies are included in Haywood’s Developer and Junior Exploration Indices, including Anvil Mining Limited, Banro Corporation, Moto Goldmines Limited, and Tiger Resources Limited. Since the initial leak, the government has tried to rebuild the bridges with the mining companies, and the recommendations are expected later this month.

Haywood developer & Junior exploration indices*

commodities

Stefan Ioannou, 416-507-2309

Andrew Kaip, 416-507-2417

Kerrry Smith, 416-507-2306

Chris Thompson, 604-697-7433

Eric Zaunscherb, 604-697-6089

Ben Asuncion, 604-697-6149

Josh Clelland, 416-507-2437

Nick Coutoulakis, 416-507-2435

Jungle Telegraph geTs Wrong number in The Congo Junior mining universe team

Haywood Junior commodity indices* performance

Vol. 2, No. 4; November 14, 2007

hayWood’s developer index (hdi): oCT 29 To nov 12, 2007Performance

Highlights The HDI lost 40 points, or 9%, to close at 438 for the period ending November 12, 2007, on the back of softening metals prices. Only four companies recorded percentage gains during the period; namely, Moto Goldmines, Inca Pacific Resources, Katanga Mining, and Detour Gold.

Gold (US$ /oz)Silver (US$ /oz)Platinum (US$ /oz)Palladium (US$ /oz)Copper (US$ /lb)Nickel (US$ /lb)Zinc (US$ /lb)Uranium (US$ /lb)

$832.00 6%$15.47 9%$1,433.00 -2%$373.00 0%$3.49 -11%$16.72 6%$1.37 -5%$92.00 8%

October 29 - November 12, 2007

P Metals (HJPI) B Metals (HJBI) Diamond (HJDI) Uranium (HJUI)*Note: Base: 100 (1/1/05)

Gain/Loss Close -47 676 -60 484 -12 197 -3 1366

Frontera Copper Corp (FCC–T)First Quantum Minerals (FM–T) Alamos Gold Inc. (AGI–T )Aquiline Resources Inc. (AQI–T )TEAL Exploration (TL–T) Detour Gold Corp (DGC–T)

Please see rating structure, important disclosure, risk profile parameters, disclaimers, and notes on pages 105 - 109

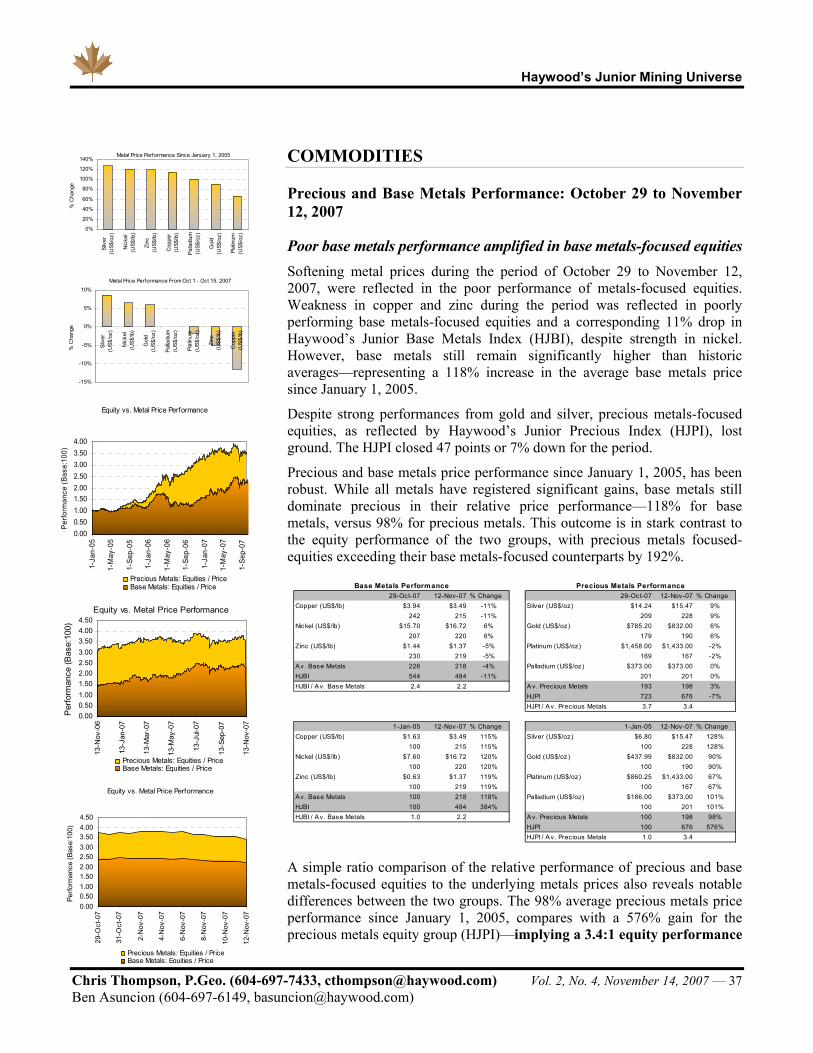

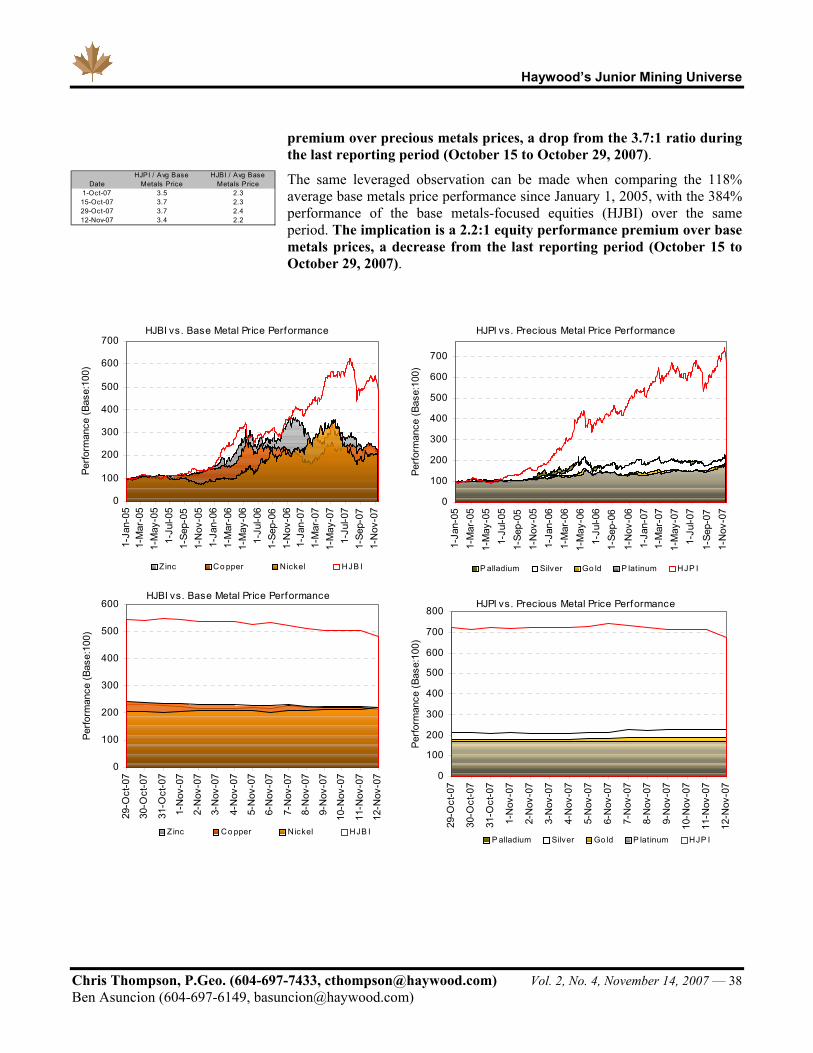

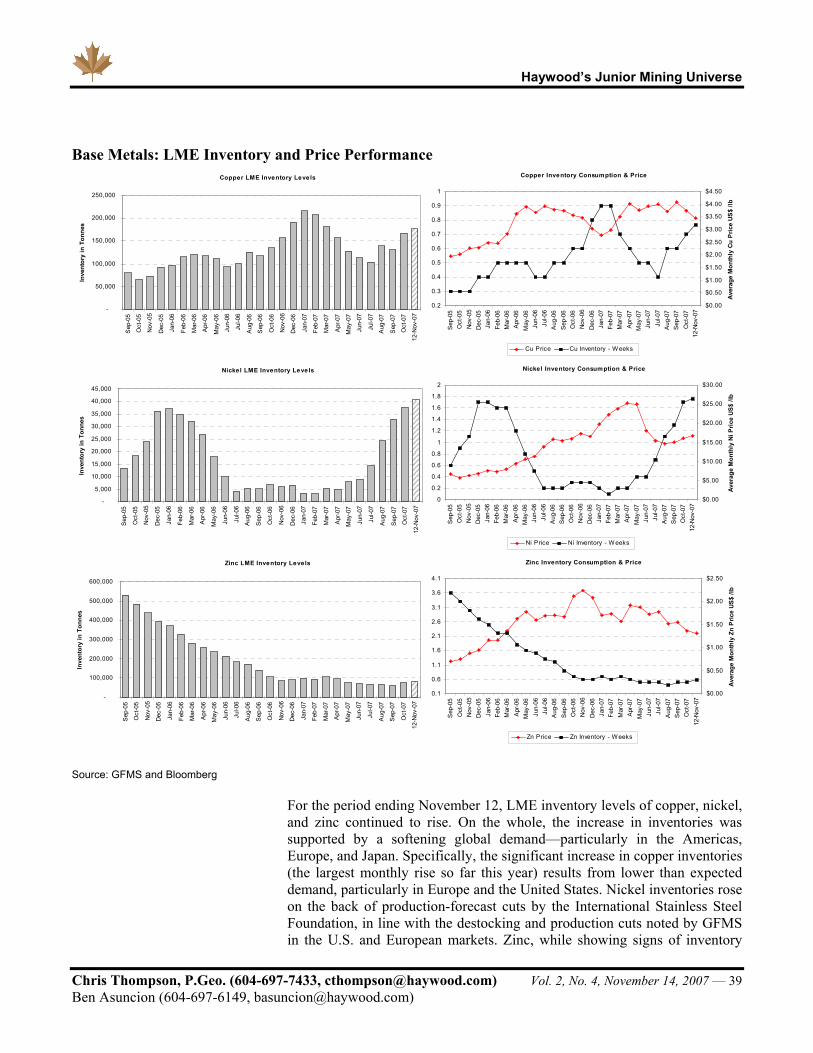

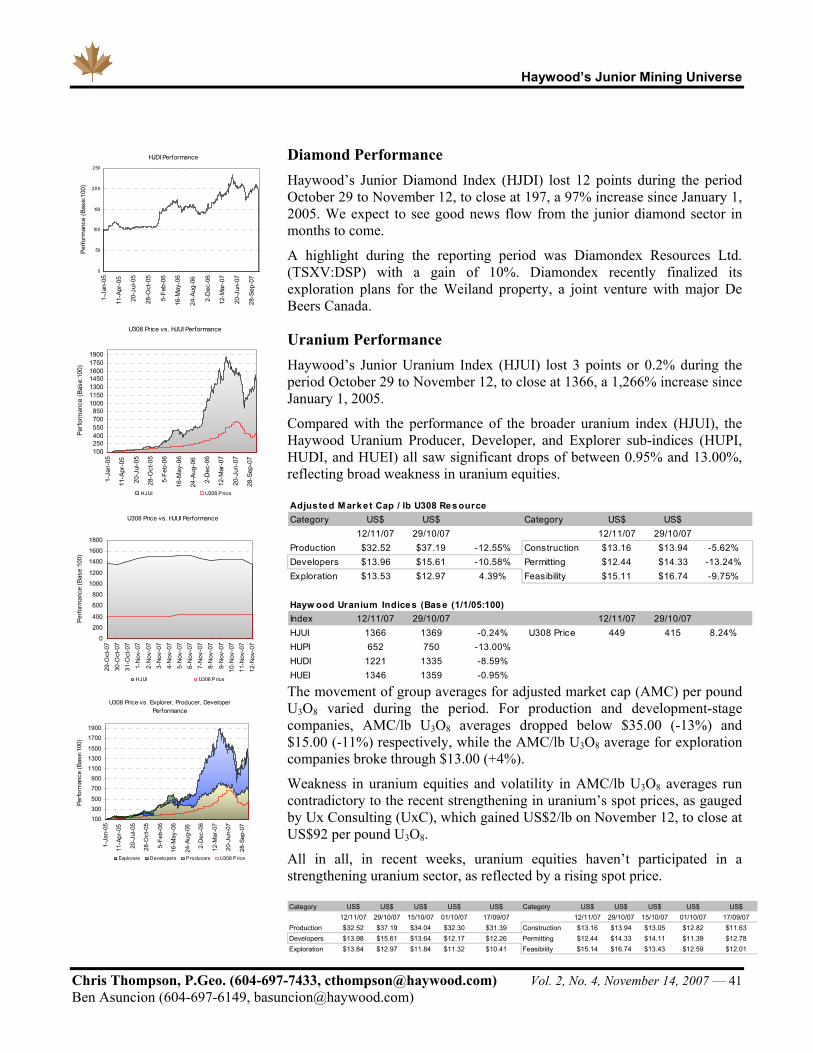

CommodiTies & CommodiTy-FoCused indiCes: oCT 29 To nov 12, 2007Poor base metals performance this period was amplified in base metals-focused equities, where a 4% drop in average base metals prices translated into an 11% drop in Haywood’s Junior Base Metals Index (HJBI). Conversely, the overall positive performance of precious metals was not reflected in Haywood’s Junior Precious Metals Index (HJPI). Similarly, recent appreciation in uranium prices did not translate into performance gains for junior uranium explorers, as reflected by Haywood’s Junior Uranium Index (HJUI). Wrapping up this period, Haywood’s Junior Diamond Index (HJDI) closed down 12 points, to finish at 197.

October 29 - November 12, 2007 HDI HJEI*Note: Base: 100 (1/1/05)

Gain/Loss Close -40 438 -23 833

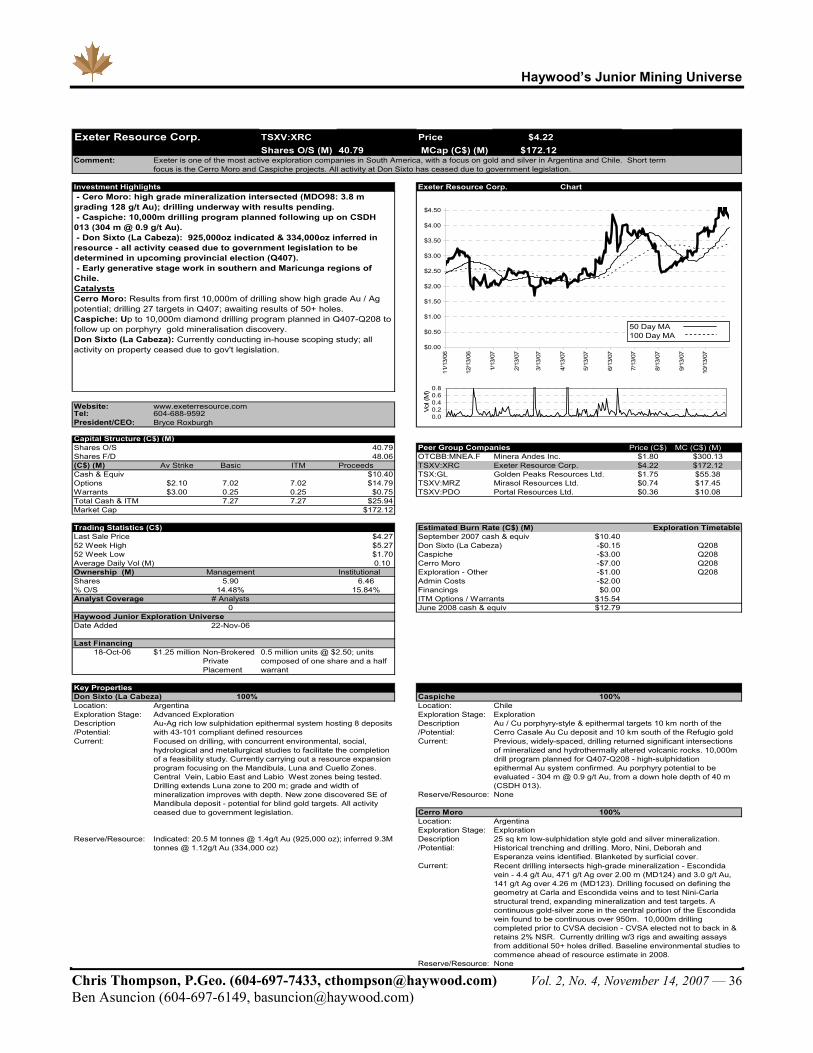

Company updaTe: exeTer resourCe

South American precious metals explorer Exeter Resource has switched gears from Don Sixto to Caspiche and Cerro Moro. With Don Sixto shelved for the time being, Exeter’s attention is now squarely focused on advancing its flagship Cerro Moro gold project in Argentina and testing the gold porphyry potential of its Caspiche project in Chile. With increased activity at Cerro Moro triggered by a back-in agreement that was not exercised, results for over 60 holes pending, and an aggressive drill program planned for Caspiche, Exeter is primed to deliver in Q4/07 through to H1/08.

recently publisHed 2- Week index perFormanCe 2- Week meTal priCe perFormanCe

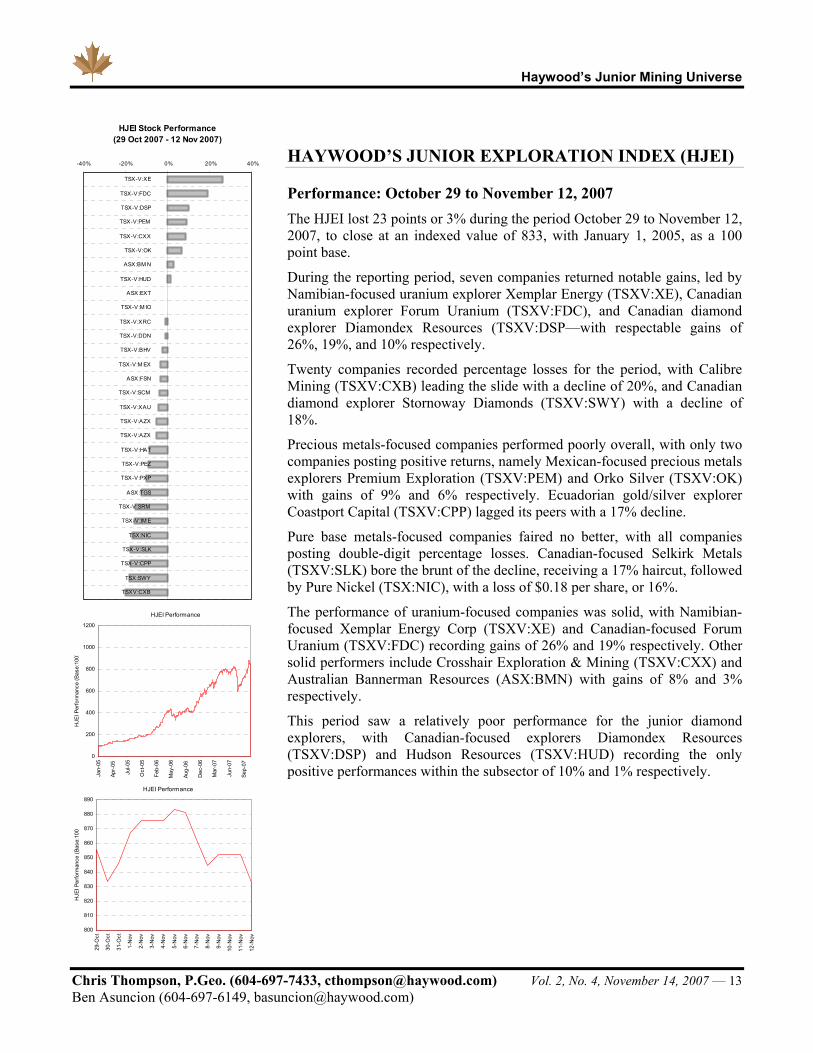

hayWood’s Junior exploraTion index (hJei): oCT 29 To nov 12, 2007Performance

Highlights The HJEI lost 23 points to close at an indexed value of 833. Out of the seven companies to record notable gains were two uranium explorers, Xemplar Energy and Forum Uranium, and Canadian diamond explorer Diamondex Resources, with returns of 26%, 19%, and 10% respectively.

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 1 Ben Asuncion (604-697-6149, [email protected])

TABLE OF CONTENTS

HAYWOOD’S DEVELOPER INDEX (HDI) .........................................................................................................................3 PERFORMANCE: OCTOBER 29 TO NOVEMBER 12, 2007 ............................................................................................................3 COMPANIES OFFICIALLY COVERED BY HAYWOOD...................................................................................................................3 HDI COMPANIES – PERFORMANCE: OCTOBER 29 TO NOVEMBER 12, 2007 ..............................................................................4 HIGHLIGHTS .............................................................................................................................................................................4

Moto Goldmines Ltd. ...........................................................................................................................................................4 Inca Pacific Resources Inc...................................................................................................................................................5 Australian Solomons Gold Ltd.............................................................................................................................................6

HDI COMPANIES: Q4/07 INVESTMENT HIGHLIGHTS AND CATALYSTS .....................................................................................7 HAYWOOD’S JUNIOR EXPLORATION INDEX (HJEI) ................................................................................................13

PERFORMANCE: OCTOBER 29 TO NOVEMBER 12, 2007 ..........................................................................................................13 HJEI COMPANIES – PERFORMANCE: OCTOBER 29 TO NOVEMBER 12, 2007 ...........................................................................14 HIGHLIGHTS ...........................................................................................................................................................................14

Xemplar Energy Corp........................................................................................................................................................14 Forum Uranium Corp........................................................................................................................................................15 Diamondex Resources Ltd. ................................................................................................................................................15 Premium Exploration Inc...................................................................................................................................................16 Crosshair Exploration & Mining Corp..............................................................................................................................16 Extract Resources Corp. ....................................................................................................................................................16

INVESTMENT HIGHLIGHTS. .....................................................................................................................................................18 HJEI COMPANIES: Q4/07 SCHEDULE OF NEWS FLOW ............................................................................................................19

COUNTRY UPDATE: DEMOCRATIC REPUBLIC OF CONGO ...................................................................................22 HAYWOOD UNIVERSE COMPANIES AFFECTED........................................................................................................................23 OUTLOOK ...............................................................................................................................................................................27

COMPANY UPDATE: EXETER RESOURCE CORP. (XRC–V) .....................................................................................29 COMPANY BACKGROUND .......................................................................................................................................................29 CAPITAL STRUCTURE .............................................................................................................................................................30 MARICUNGA-CASPICHE PROJECT, CHILE ...............................................................................................................................30 CERRO MORO PROJECT, ARGENTINA .....................................................................................................................................32 DON SIXTO, ARGENTINA ........................................................................................................................................................34 NEWS FLOW ...........................................................................................................................................................................34 KEY CATALYSTS ....................................................................................................................................................................35

COMMODITIES .....................................................................................................................................................................37 PRECIOUS AND BASE METALS PERFORMANCE: OCTOBER 29 TO NOVEMBER 12, 2007...........................................................37 BASE METALS: LME INVENTORY AND PRICE PERFORMANCE................................................................................................39 DIAMOND PERFORMANCE ......................................................................................................................................................41 URANIUM PERFORMANCE.......................................................................................................................................................41

APPENDIX: COMPANY TEAR SHEETS ...........................................................................................................................43 DISTRIBUTION ..........................................................................................................................................................................104 ANALYST CERTIFICATION ........................................................................................................................................................104 IMPORTANT DISCLOSURES........................................................................................................................................................104 RATING STRUCTURE.................................................................................................................................................................106 RISK PROFILE PARAMETERS .....................................................................................................................................................107 DISCLAIMERS ...........................................................................................................................................................................108

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 2 Ben Asuncion (604-697-6149, [email protected])

LIST OF INDICES

Index Title HDI Haywood's Developer Index HJBI Haywood's Junior Base Index HJDI Haywood's Junior Diamond Index HJEI Haywood's Junior Exploration Index HJPI Haywood's Junior Precious Index HJUI Haywood's Junior Uranium Index HUDI Haywood's Uranium Developer Index HUEI Haywood's Uranium Explorer Index HUPI Haywood's Uranium Producer Index

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 3 Ben Asuncion (604-697-6149, [email protected])

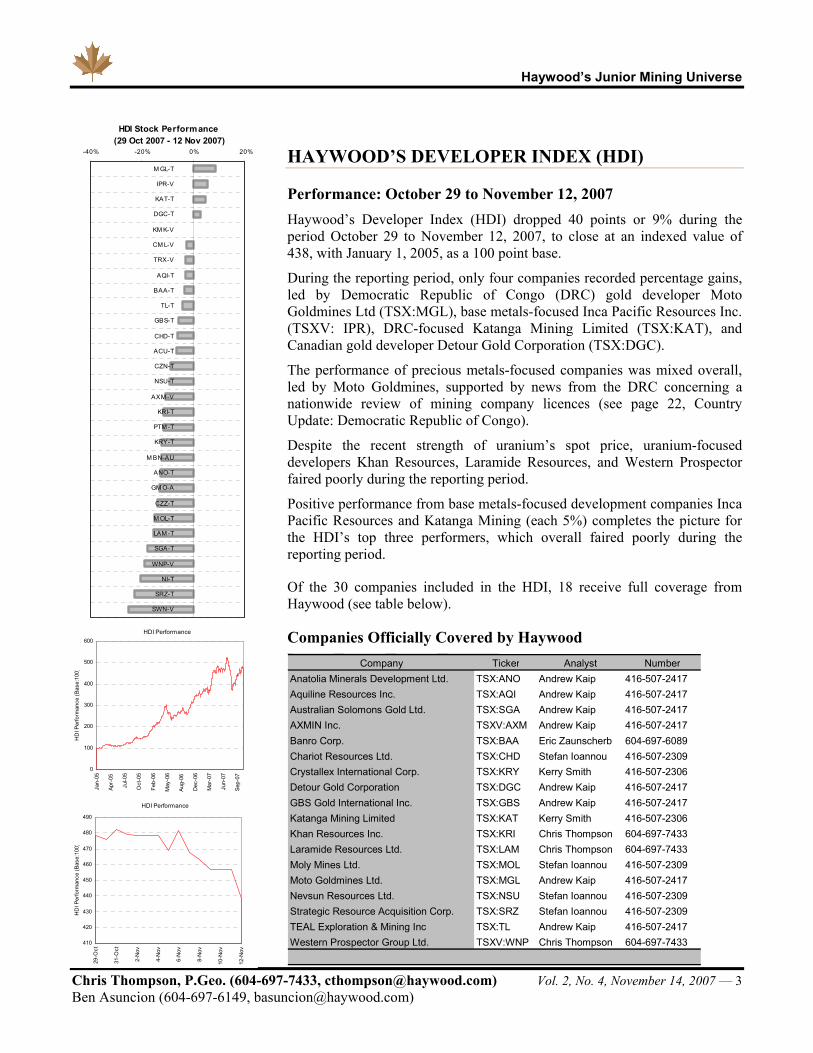

HAYWOOD’S DEVELOPER INDEX (HDI)

Performance: October 29 to November 12, 2007 Haywood’s Developer Index (HDI) dropped 40 points or 9% during the period October 29 to November 12, 2007, to close at an indexed value of 438, with January 1, 2005, as a 100 point base.

During the reporting period, only four companies recorded percentage gains, led by Democratic Republic of Congo (DRC) gold developer Moto Goldmines Ltd (TSX:MGL), base metals-focused Inca Pacific Resources Inc. (TSXV: IPR), DRC-focused Katanga Mining Limited (TSX:KAT), and Canadian gold developer Detour Gold Corporation (TSX:DGC).

The performance of precious metals-focused companies was mixed overall, led by Moto Goldmines, supported by news from the DRC concerning a nationwide review of mining company licences (see page 22, Country Update: Democratic Republic of Congo).

Despite the recent strength of uranium’s spot price, uranium-focused developers Khan Resources, Laramide Resources, and Western Prospector faired poorly during the reporting period.

Positive performance from base metals-focused development companies Inca Pacific Resources and Katanga Mining (each 5%) completes the picture for the HDI’s top three performers, which overall faired poorly during the reporting period.

Of the 30 companies included in the HDI, 18 receive full coverage from Haywood (see table below).

Companies Officially Covered by Haywood Company Ticker Analyst Number

Anatolia Minerals Development Ltd. TSX:ANO Andrew Kaip 416-507-2417Aquiline Resources Inc. TSX:AQI Andrew Kaip 416-507-2417Australian Solomons Gold Ltd. TSX:SGA Andrew Kaip 416-507-2417AXMIN Inc. TSXV:AXM Andrew Kaip 416-507-2417Banro Corp. TSX:BAA Eric Zaunscherb 604-697-6089Chariot Resources Ltd. TSX:CHD Stefan Ioannou 416-507-2309Crystallex International Corp. TSX:KRY Kerry Smith 416-507-2306Detour Gold Corporation TSX:DGC Andrew Kaip 416-507-2417GBS Gold International Inc. TSX:GBS Andrew Kaip 416-507-2417Katanga Mining Limited TSX:KAT Kerry Smith 416-507-2306Khan Resources Inc. TSX:KRI Chris Thompson 604-697-7433Laramide Resources Ltd. TSX:LAM Chris Thompson 604-697-7433Moly Mines Ltd. TSX:MOL Stefan Ioannou 416-507-2309Moto Goldmines Ltd. TSX:MGL Andrew Kaip 416-507-2417Nevsun Resources Ltd. TSX:NSU Stefan Ioannou 416-507-2309Strategic Resource Acquisition Corp. TSX:SRZ Stefan Ioannou 416-507-2309TEAL Exploration & Mining Inc TSX:TL Andrew Kaip 416-507-2417Western Prospector Group Ltd. TSXV:WNP Chris Thompson 604-697-7433

HDI Stock Performance (29 Oct 2007 - 12 Nov 2007)

-40% -20% 0% 20%

M GL-T

IPR-V

KAT-T

DGC-T

KM K-V

CM L-V

TRX-V

AQI-T

BAA-T

TL-T

GBS-T

CHD-T

ACU-T

CZN-T

NSU-T

AXM -V

KRI-T

PTM -T

KRY-T

M BN-AU

ANO-T

GM O-A

CZZ-T

M OL-T

LAM -T

SGA-T

WNP-V

NI-T

SRZ-T

SWN-V

HDI Performance

0

100

200

300

400

500

600

Jan-

05

Apr-

05

Jul-0

5

Oct

-05

Feb-

06

May

-06

Aug-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

HD

I Per

form

ance

(Bas

e:10

0)

HDI Performance

410

420

430

440

450

460

470

480

490

29-O

ct

31-O

ct

2-N

ov

4-N

ov

6-N

ov

8-N

ov

10-N

ov

12-N

ov

HD

I Per

form

ance

(Bas

e:10

0 )

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 4 Ben Asuncion (604-697-6149, [email protected])

HDI Companies – Performance: October 29 to November 12, 2007 Company Ticker Commodity Focus Area Focus 10/29/2007 11/12/2007 %

• Moto Goldmines Ltd. MGL-T Precious Metals Democratic Republic of the Congo 3.04$ 3.30$ 9%Inca Pacif ic Resources Inc. IPR-V Base Metals Peru 1.85$ 1.95$ 5%

• Katanga Mining Limited KAT-T Base Metals Democratic Republic of the Congo 15.77$ 16.52$ 5%• Detour Gold Corporation DGC-T Precious Metals Canada 9.05$ 9.29$ 3%

Continental Minerals Corp. KMK-V Precious, Base Metals China 1.41$ 1.41$ 0%Crow f light Minerals Inc. CML-V Base Metals Canada 0.80$ 0.78$ -3%Terrane Metals Corp. TRX-V Precious, Base Metals Canada 0.51$ 0.50$ -3%

• Aquiline Resources Inc. AQI-T Precious Metals Argentina 10.77$ 10.43$ -3%• Banro Corp. BAA-T Precious Metals Democratic Republic of the Congo 12.45$ 12.01$ -4%• TEAL Exploration & Mining Inc TL-T Base Metals DRC, Namibia, Zambia 5.15$ 4.95$ -4%• GBS Gold International Inc. GBS-T Precious Metals Australia 1.51$ 1.42$ -6%• Chariot Resources Ltd. CHD-T Base Metals Peru 1.15$ 1.08$ -6%

African Copper plc ACU-T Base Metals Botsw ana 1.82$ 1.68$ -8%Canadian Zinc Corp. CZN-T Base Metals Canada 0.89$ 0.81$ -9%

• Nevsun Resources Ltd. NSU-T Precious, Base Metals Af rica 2.08$ 1.89$ -9%• AXMIN Inc. AXM-V Precious Metals Af rica 0.94$ 0.84$ -11%• Khan Resources Inc. KRI-T Uranium Mongolia 2.74$ 2.43$ -11%

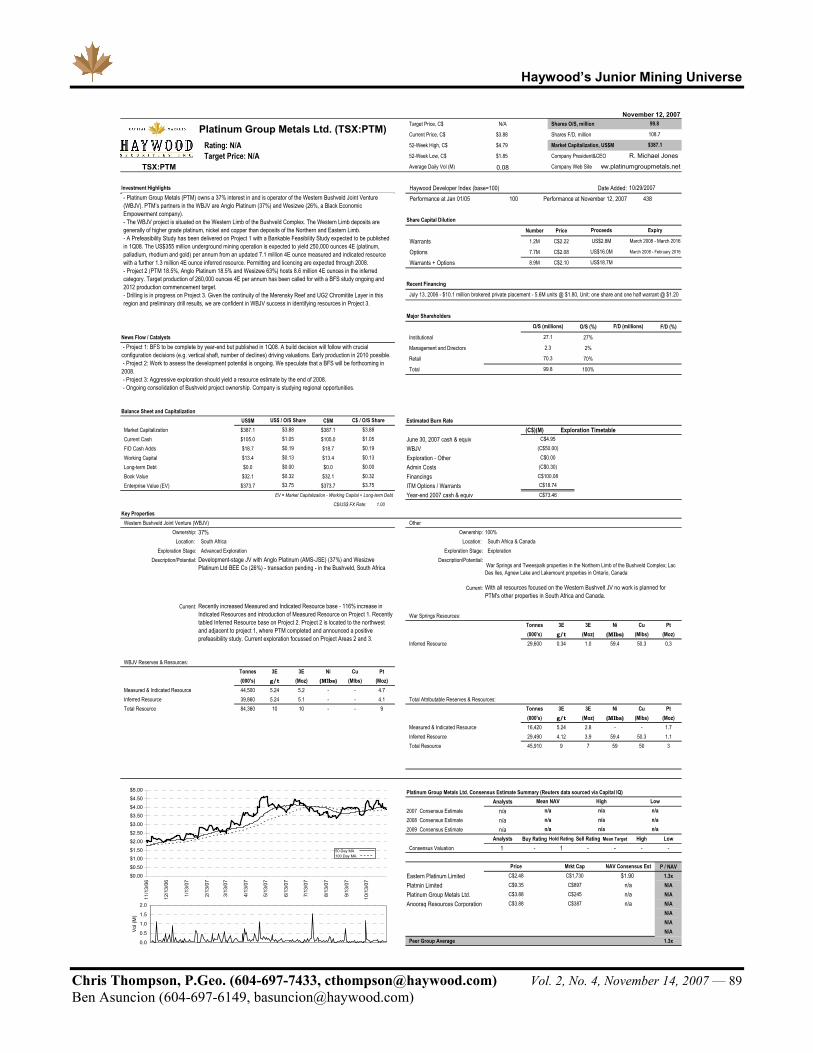

Platinum Group Metals Ltd. PTM-T Precious Metals Af rica, Canada 4.40$ 3.88$ -12%• Crystallex International Corp. KRY-T Precious Metals Venezuela 3.14$ 2.75$ -12%

Mirabela Nickel Ltd. MBN-AU Base Metals Brazil 6.26$ 5.48$ -12%• Anatolia Minerals Development Ltd. ANO-T Precious Metals Turkey 6.25$ 5.46$ -13%

General Moly, Inc. GMO-A Precious, Base Metals Nevada 9.80$ 8.50$ -13%Canadian Royalties Inc. CZZ-T Precious. Base Metals Canada 3.79$ 3.27$ -14%

• Moly Mines Ltd. MOL-T Precious, Base Metals Australia 4.11$ 3.49$ -15%• Laramide Resources Ltd. LAM-T Uranium Australia, USA 9.25$ 7.84$ -15%• Australian Solomons Gold Ltd. SGA-T Precious Metals Solomon Islands 0.90$ 0.74$ -18%• Western Prospector Group Ltd. WNP-V Uranium Mongolia 2.04$ 1.65$ -19%

Victory Nickel, Inc. NI-T Base Metals Canada 0.64$ 0.51$ -20%• Strategic Resource Acquisition Corp. SRZ-T Base Metals USA 5.05$ 3.90$ -23%

Selw yn Resources Ltd. SWN-V Base Metals Canada 0.52$ 0.39$ -25%

• Company is under formal coverage

Highlights

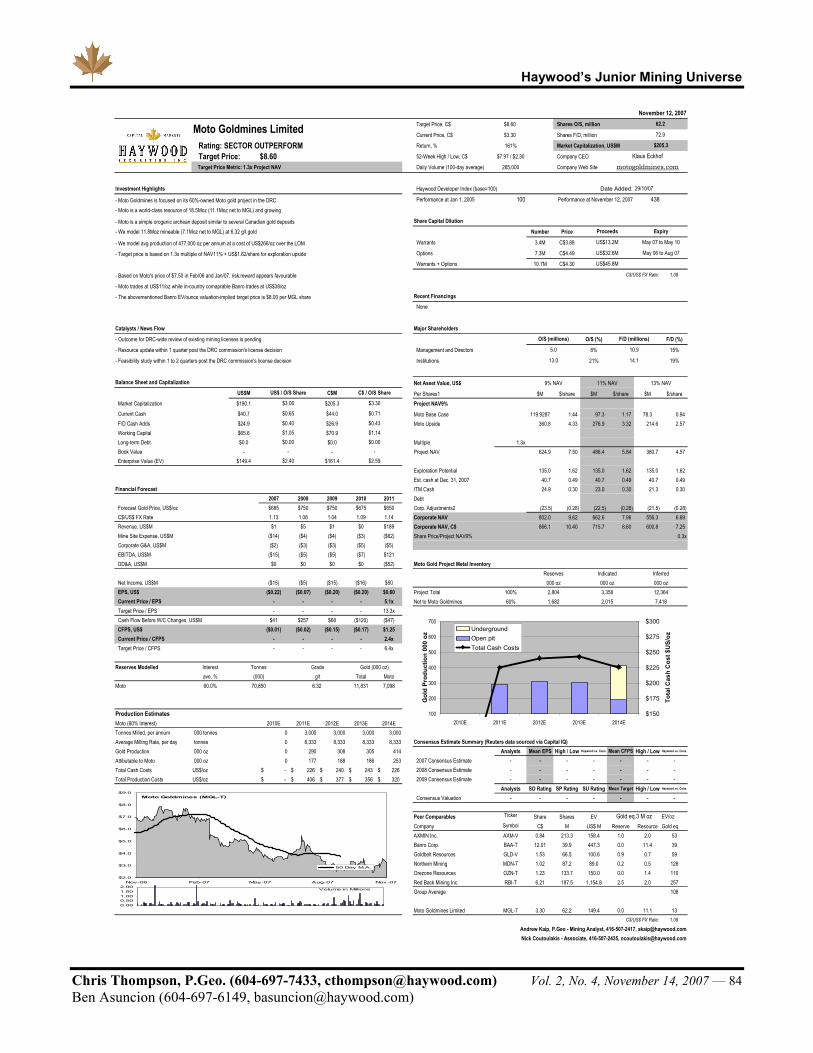

Moto Goldmines Ltd. (TSX:MGL) ($3.30: +9%: M Cap $215M) Rating: SECTOR OUTPERFORM 12-Month Target: $8.60 Risk: SPECULATIVE Analyst: Andrew Kaip (416-507-2417, [email protected])

Moto shares appreciated by 9% during the reporting period owing primarily to the announcement of unofficial results from the long-awaited mining company licence review in the DRC. As of Friday, November 3, 2007, what looked to be leaked commission results were published in an article by Le Phare, an independent news agency in Kinshasa. While unofficial, the article indicates that for several of the concessions that comprise the Moto Gold project, joint-venture partners Moto Goldmines and Borgamin are deficient in certain aspects of the joint-venture agreement with the parastatal company OKIMO. These aspects

Moto Goldmines Ltd. Chart

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

11/1

3/06

12/1

3/06

1/13

/07

2/13

/07

3/13

/07

4/13

/07

5/13

/07

6/13

/07

7/13

/07

8/13

/07

9/13

/07

10/1

3/07

0.0

5.0

10.0

1

Vol

(M)

50 Day MA100 Day MA

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 5 Ben Asuncion (604-697-6149, [email protected])

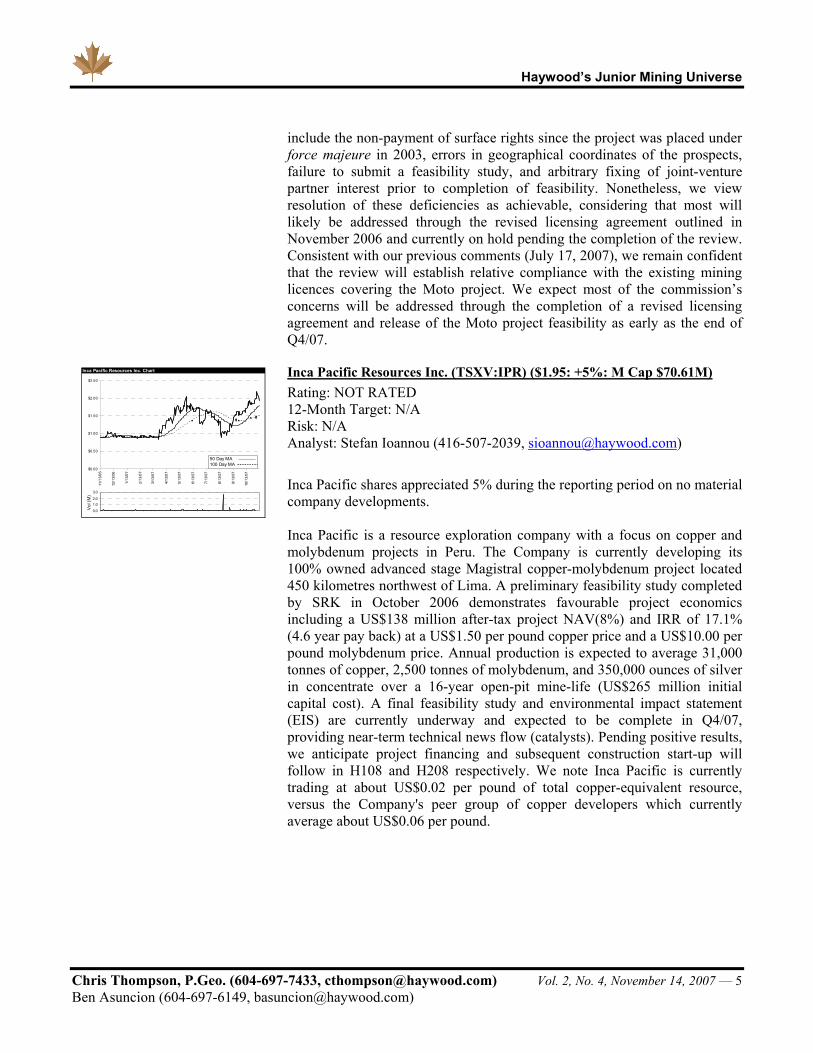

include the non-payment of surface rights since the project was placed under force majeure in 2003, errors in geographical coordinates of the prospects, failure to submit a feasibility study, and arbitrary fixing of joint-venture partner interest prior to completion of feasibility. Nonetheless, we view resolution of these deficiencies as achievable, considering that most will likely be addressed through the revised licensing agreement outlined in November 2006 and currently on hold pending the completion of the review. Consistent with our previous comments (July 17, 2007), we remain confident that the review will establish relative compliance with the existing mining licences covering the Moto project. We expect most of the commission’s concerns will be addressed through the completion of a revised licensing agreement and release of the Moto project feasibility as early as the end of Q4/07.

Inca Pacific Resources Inc. (TSXV:IPR) ($1.95: +5%: M Cap $70.61M) Rating: NOT RATED 12-Month Target: N/A Risk: N/A Analyst: Stefan Ioannou (416-507-2039, [email protected])

Inca Pacific shares appreciated 5% during the reporting period on no material company developments. Inca Pacific is a resource exploration company with a focus on copper and molybdenum projects in Peru. The Company is currently developing its 100% owned advanced stage Magistral copper-molybdenum project located 450 kilometres northwest of Lima. A preliminary feasibility study completed by SRK in October 2006 demonstrates favourable project economics including a US$138 million after-tax project NAV(8%) and IRR of 17.1% (4.6 year pay back) at a US$1.50 per pound copper price and a US$10.00 per pound molybdenum price. Annual production is expected to average 31,000 tonnes of copper, 2,500 tonnes of molybdenum, and 350,000 ounces of silver in concentrate over a 16-year open-pit mine-life (US$265 million initial capital cost). A final feasibility study and environmental impact statement (EIS) are currently underway and expected to be complete in Q4/07, providing near-term technical news flow (catalysts). Pending positive results, we anticipate project financing and subsequent construction start-up will follow in H108 and H208 respectively. We note Inca Pacific is currently trading at about US$0.02 per pound of total copper-equivalent resource, versus the Company's peer group of copper developers which currently average about US$0.06 per pound.

Inca Pacific Resources Inc. Chart

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

11/1

3/06

12/1

3/06

1/13

/07

2/13

/07

3/13

/07

4/13

/07

5/13

/07

6/13

/07

7/13

/07

8/13

/07

9/13

/07

10/1

3/07

0.0

1.02.0

3.0

1

Vol

(M)

50 Day MA100 Day MA

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 6 Ben Asuncion (604-697-6149, [email protected])

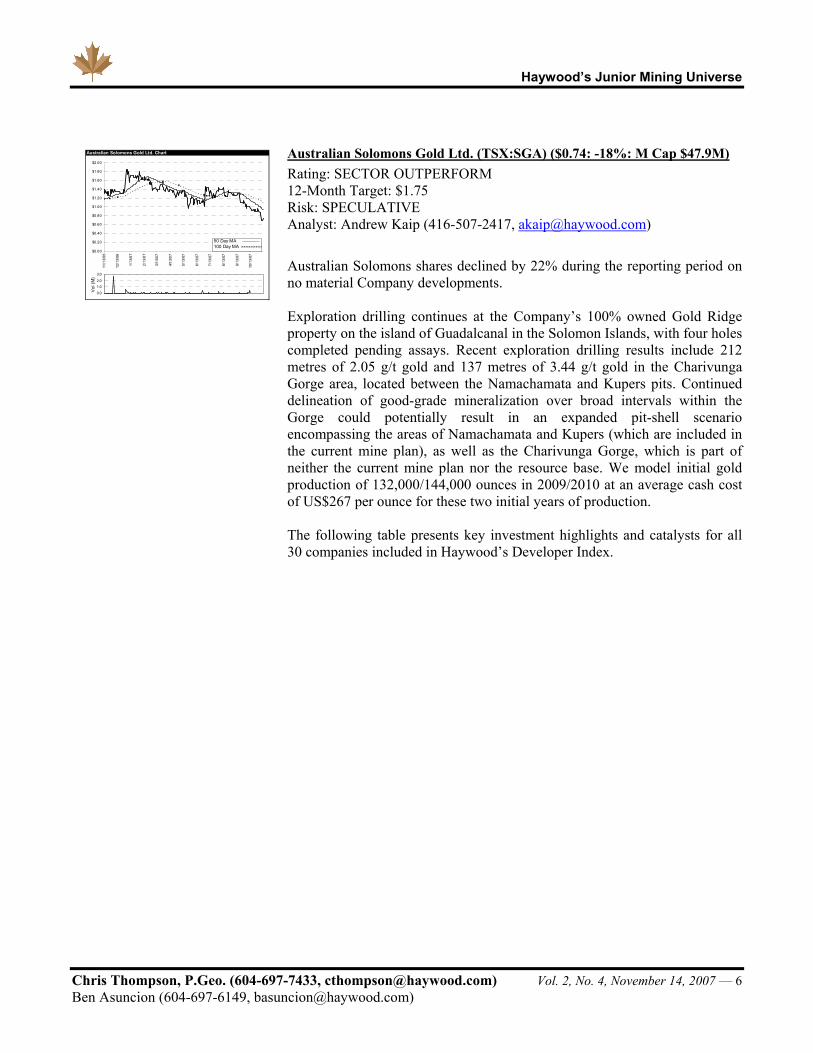

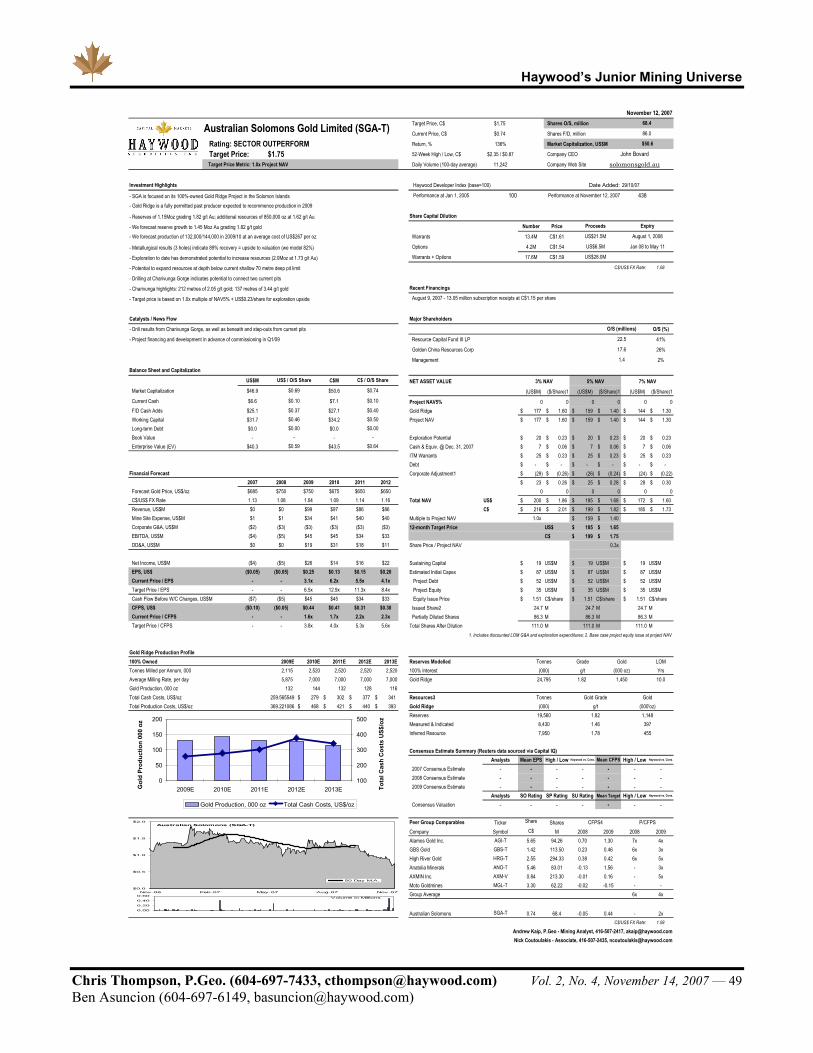

Australian Solomons Gold Ltd. (TSX:SGA) ($0.74: -18%: M Cap $47.9M) Rating: SECTOR OUTPERFORM 12-Month Target: $1.75 Risk: SPECULATIVE Analyst: Andrew Kaip (416-507-2417, [email protected])

Australian Solomons shares declined by 22% during the reporting period on no material Company developments. Exploration drilling continues at the Company’s 100% owned Gold Ridge property on the island of Guadalcanal in the Solomon Islands, with four holes completed pending assays. Recent exploration drilling results include 212 metres of 2.05 g/t gold and 137 metres of 3.44 g/t gold in the Charivunga Gorge area, located between the Namachamata and Kupers pits. Continued delineation of good-grade mineralization over broad intervals within the Gorge could potentially result in an expanded pit-shell scenario encompassing the areas of Namachamata and Kupers (which are included in the current mine plan), as well as the Charivunga Gorge, which is part of neither the current mine plan nor the resource base. We model initial gold production of 132,000/144,000 ounces in 2009/2010 at an average cash cost of US$267 per ounce for these two initial years of production. The following table presents key investment highlights and catalysts for all 30 companies included in Haywood’s Developer Index.

Australian Solomons Gold Ltd. Chart

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

11/1

3/06

12/1

3/06

1/13

/07

2/13

/07

3/13

/07

4/13

/07

5/13

/07

6/13

/07

7/13

/07

8/13

/07

9/13

/07

10/1

3/07

0.0

1.02.0

3.0

1

Vol

(M)

50 Day MA100 Day MA

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 7 Ben Asuncion (604-697-6149, [email protected])

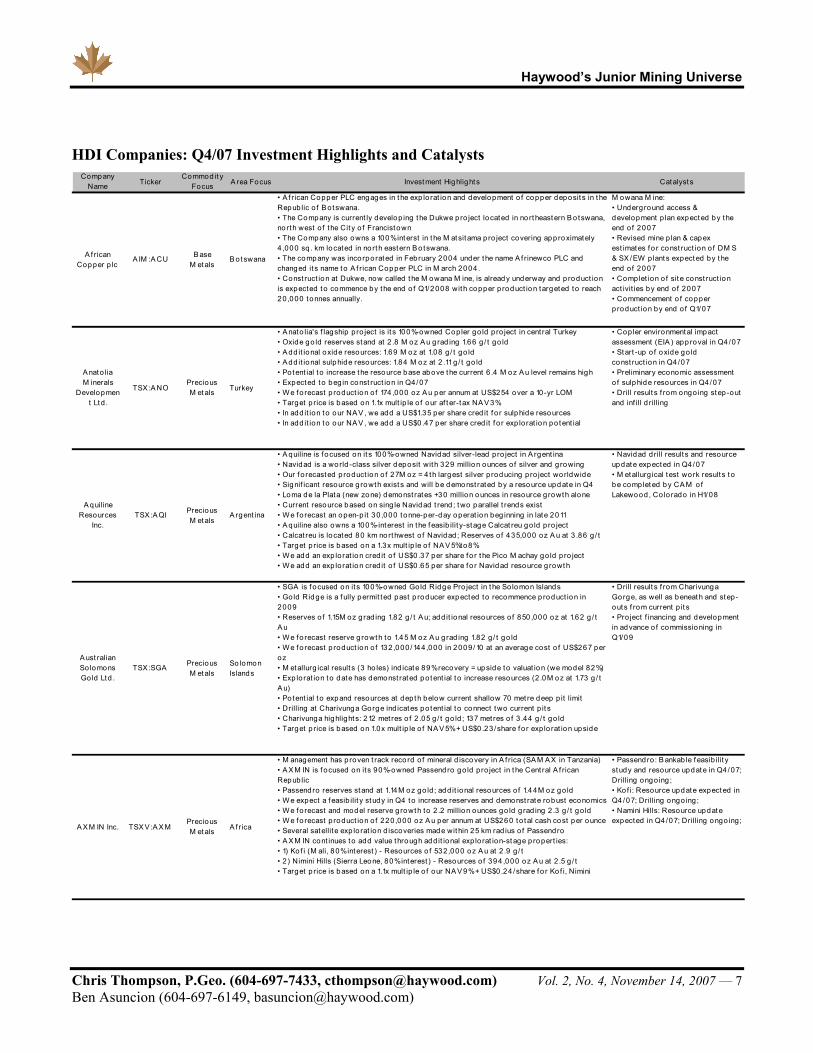

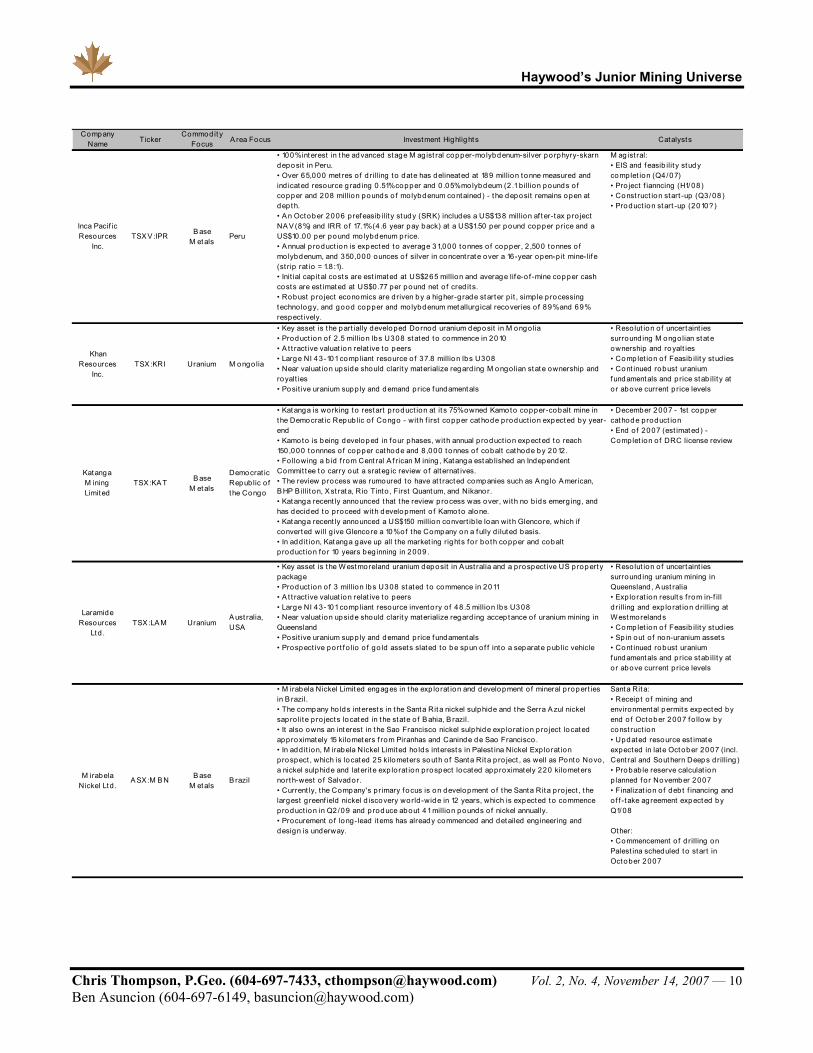

HDI Companies: Q4/07 Investment Highlights and Catalysts Company

Name TickerCommod it y

Focus A rea Focus Investment Highlight s Catalyst s

A f rican Copper p lc

A IM :A CU B ase M etals

B otswana

• A f rican Copper PLC engages in t he exp lorat ion and development o f copper deposit s in t he Republic o f B otswana. • The Company is current ly develop ing t he Dukwe p ro ject located in no rtheastern B o tswana, no rth west o f the Cit y o f Francistown• The Company also owns a 100% interst in t he M atsitama p ro ject covering approximately 4 ,000 sq . km located in no rth eastern B o tswana. • The company was incorporated in February 2004 under the name A f rinewco PLC and changed it s name to A f rican Copper PLC in M arch 2004 .• Const ruct ion at Dukwe, now called t he M owana M ine, is already underway and p roduct ion is expected to commence by the end o f Q1/2008 with copper p roduct ion targeted to reach 20,000 tonnes annually.

M owana M ine:• Underground access & development p lan expected by the end o f 2007• Revised mine p lan & capex est imates fo r const ruct ion o f DM S & SX /EW p lants expected by t he end o f 2007• Complet ion o f sit e const ruct ion act ivit ies by end o f 2007• Commencement o f copper p roduct ion by end o f Q1/07

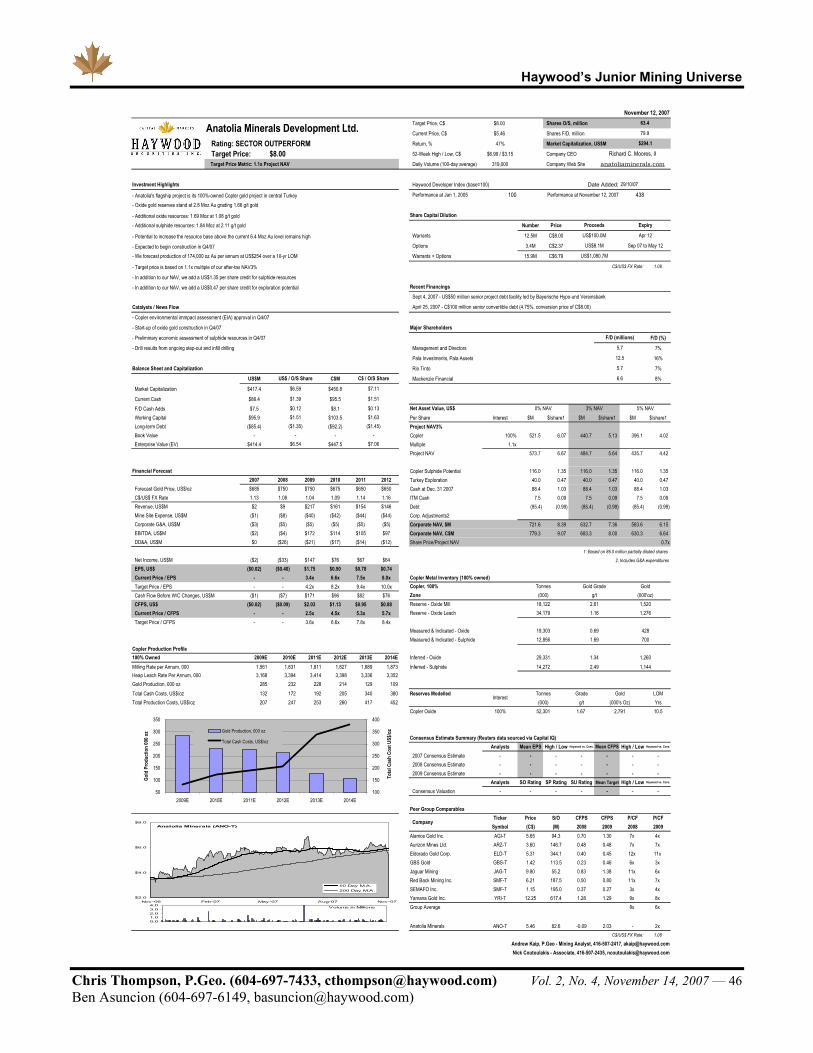

A nato lia M inerals

Development Ltd .

TSX :A NOPrecious M etals Turkey

• A nato lia's f lagship pro ject is it s 100%-owned Copler go ld p ro ject in cent ral Turkey• Oxide go ld reserves stand at 2 .8 M oz A u g rad ing 1.66 g / t go ld• A dd it ional oxide resources: 1.69 M oz at 1.08 g / t go ld• A dd it ional sulphide resources: 1.84 M oz at 2 .11 g / t go ld• Po tent ial t o increase the resource base above the current 6 .4 M oz A u level remains high• Expected to beg in const ruct ion in Q4/07• W e fo recast p roduct ion o f 174 ,000 oz A u per annum at US$254 over a 10-yr LOM• Target p rice is based on 1.1x mult ip le o f our af t er-t ax NA V 3%• In add it ion t o our NA V , we add a US$1.35 per share cred it f o r sulphide resources• In add it ion t o our NA V , we add a US$0.47 per share cred it f o r exp lorat ion potent ial

• Cop ler environmental impact assessment (EIA ) approval in Q4 /07• Start -up o f oxide go ld const ruct ion in Q4 /07• Preliminary economic assessment o f sulphide resources in Q4/07• Drill result s f rom ongo ing step -out and inf ill d rilling

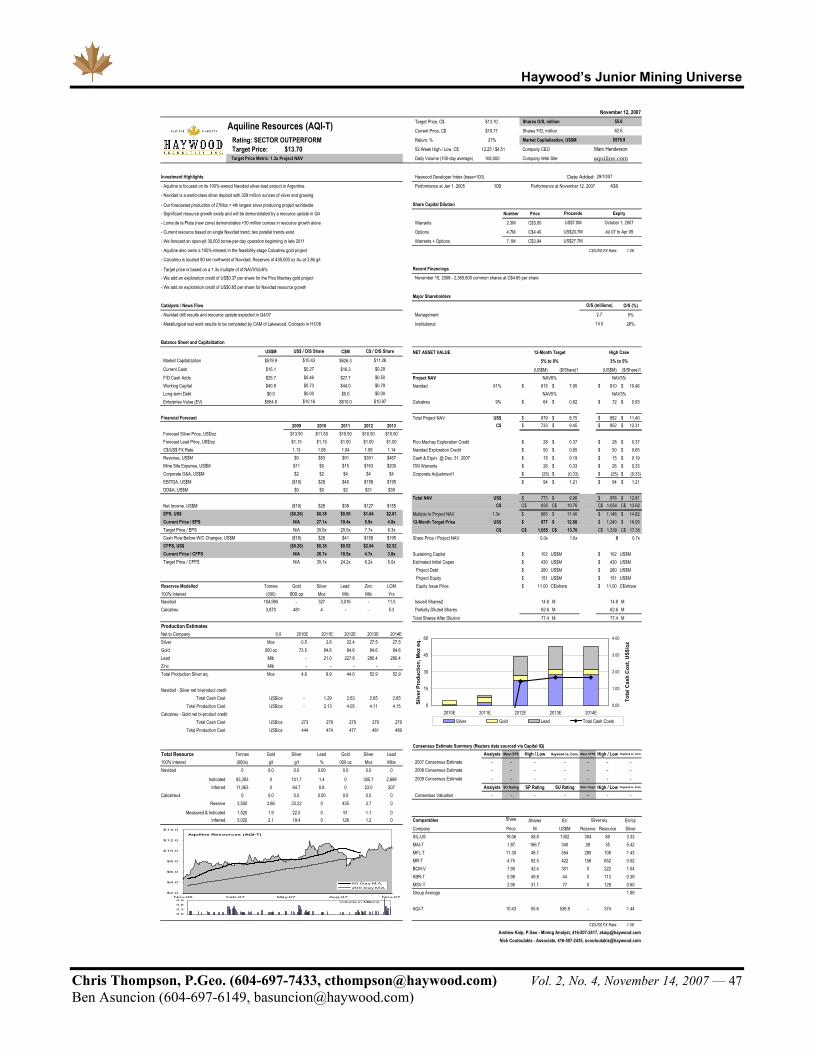

A quiline Resources

Inc.TSX :A QI Precious

M etalsA rgent ina

• A quiline is focused on it s 100%-owned Navidad silver-lead pro ject in A rgent ina• Navidad is a world -class silver deposit with 329 million ounces o f silver and g rowing• Our f o recasted p roduct ion o f 27M oz = 4 th largest silver producing pro ject worldwide• Signif icant resource g rowth exist s and will be demonst rated by a resource update in Q4• Loma de la Plata (new zone) demonst rates +30 million ounces in resource growth alone• Current resource based on sing le Navidad t rend ; two parallel t rends exist• W e fo recast an open-p it 30 ,000 tonne-per-day operat ion beg inning in late 2011• A quiline also owns a 100%-interest in the f easib ilit y-stage Calcat reu go ld pro ject• Calcat reu is located 80 km northwest o f Navidad ; Reserves o f 435,000 oz A u at 3 .86 g / t• Target p rice is based on a 1.3x mult ip le o f NA V 5%to8%• W e add an exp lorat ion cred it o f US$0.37 per share fo r t he Pico M achay go ld p ro ject• W e add an exp lorat ion cred it o f US$0.65 per share fo r Navidad resource g rowth

• Navidad d rill results and resource update expected in Q4/07• M etallurg ical test work results t o be comp leted by CA M o f Lakewood , Co lorado in H1/08

A ust ralian So lomons Gold Ltd .

TSX :SGA Precious M etals

So lomon Islands

• SGA is f ocused on it s 100%-owned Gold Ridge Pro ject in t he So lomon Islands• Gold Ridge is a f ully permit ted past p roducer expected to recommence p roduct ion in 2009• Reserves o f 1.15M oz g rad ing 1.82 g / t A u; add it ional resources o f 850 ,000 oz at 1.62 g / t A u• W e fo recast reserve g rowth to 1.45 M oz A u grad ing 1.82 g / t go ld• W e fo recast p roduct ion o f 132,000 /144,000 in 2009/10 at an average cost o f US$267 per oz• M etallurg ical result s (3 ho les) ind icate 89% recovery = upside to valuat ion (we model 82%)• Exp lorat ion t o date has demonst rated potent ial t o increase resources (2 .0M oz at 1.73 g / t A u)• Po tent ial t o expand resources at depth below current shallow 70 met re deep p it limit• Drilling at Charivunga Gorge ind icates potent ial t o connect two current p it s• Charivunga highlight s: 212 met res o f 2 .05 g / t go ld ; 137 met res o f 3 .44 g / t go ld• Target p rice is based on 1.0x mult ip le o f NA V 5% + US$0.23 /share f or exp lo rat ion upside

• Drill result s f rom Charivunga Gorge, as well as beneath and step-outs f rom current p it s• Pro ject f inancing and development in advance o f commissioning in Q1/09

A X M IN Inc. TSX V :A X MPrecious M etals A f rica

• M anagement has p roven t rack record o f mineral d iscovery in A f rica (SA M A X in Tanzania)• A X M IN is f ocused on it s 90%-owned Passendro go ld pro ject in t he Cent ral A f rican Republic• Passendro reserves stand at 1.14M oz go ld ; add it ional resources o f 1.44M oz go ld• W e expect a f easib ilit y study in Q4 to increase reserves and demonst rate robust economics• W e fo recast and model reserve g rowth to 2 .2 million ounces go ld g rad ing 2 .3 g / t go ld• W e fo recast p roduct ion o f 220,000 oz A u per annum at US$260 to tal cash cost per ounce• Several satellite exp lo rat ion d iscoveries made wit hin 25 km rad ius o f Passendro• A X M IN cont inues t o add value through add it ional exp lo rat ion-stage p ropert ies:• 1) Ko f i (M ali, 80% interest ) - Resources o f 532,000 oz A u at 2 .9 g / t• 2 ) Nimini Hills (Sierra Leone, 80% interest ) - Resources o f 394 ,000 oz A u at 2 .5 g / t• Target p rice is based on a 1.1x mult ip le o f our NA V 9% + US$0.24 /share fo r Ko f i, Nimini

• Passendro: B ankab le f easib ilit y study and resource update in Q4/07; Drilling ongo ing ;• Ko f i: Resource update expected in Q4 /07; Drilling ongo ing ;• Namini Hills: Resource update expected in Q4 /07; Drilling ongo ing;

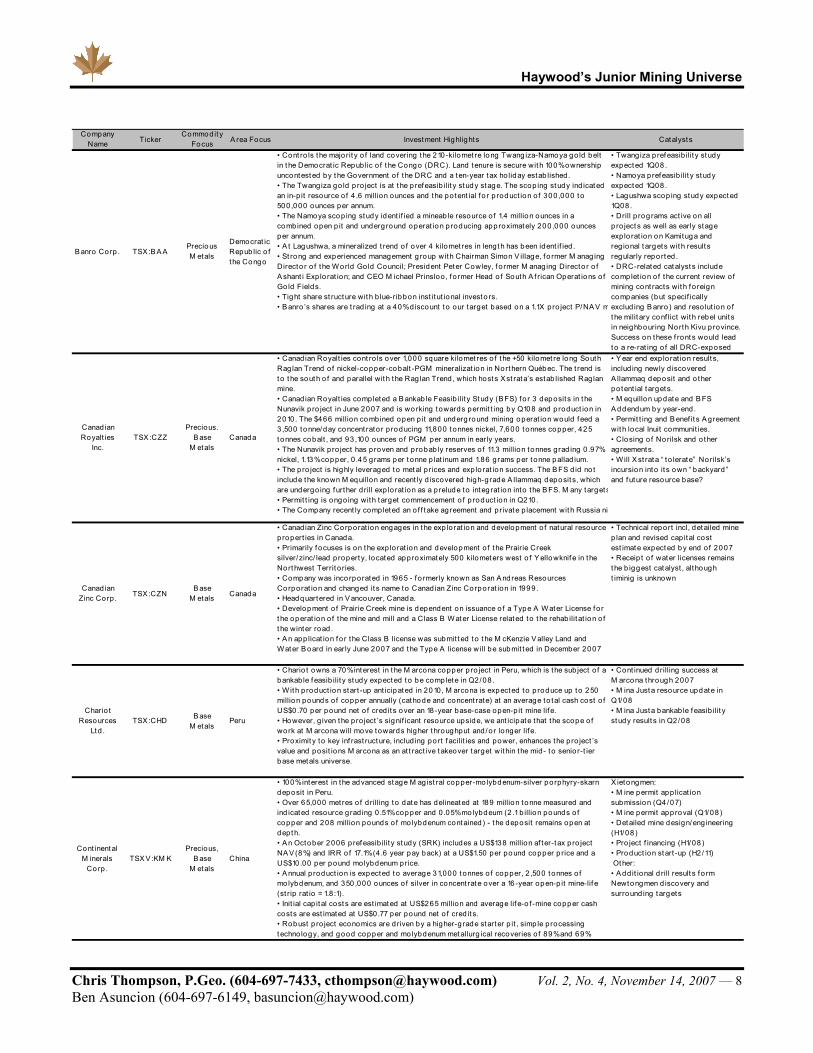

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 8 Ben Asuncion (604-697-6149, [email protected])

Company Name Ticker

Commodit y Focus A rea Focus Investment Highlights Catalysts

Banro Corp . TSX :B A APrecious M etals

Democrat ic Repub lic o f the Congo

• Cont ro ls the majorit y o f land covering the 210-kilomet re long Twang iza-Namoya go ld belt in t he Democrat ic Repub lic o f t he Congo (DRC). Land tenure is secure wit h 100% ownership uncontested by t he Government o f the DRC and a t en-year tax ho liday estab lished.• The Twangiza go ld p ro ject is at t he prefeasib ilit y study stage. The scop ing study ind icated an in-p it resource o f 4 .6 million ounces and the po tent ial fo r p roduct ion o f 300,000 to 500,000 ounces per annum.• The Namoya scop ing study ident if ied a mineab le resource o f 1.4 million ounces in a combined open p it and underg round operat ion p roducing approximately 200,000 ounces per annum.• A t Lagushwa, a mineralized t rend o f over 4 kilomet res in length has been ident if ied .• St rong and experienced management g roup with Chairman Simon V illage, fo rmer M anag ing Directo r o f the W orld Gold Council; President Peter Cowley, f o rmer M anaging Directo r o f A shant i Exp lo rat ion; and CEO M ichael Prinsloo, f o rmer Head o f South A f rican Operat ions o f Go ld Fields.• Tight share st ructure wit h b lue-ribbon inst itut ional investo rs.• B anro ’s shares are t rad ing at a 40% d iscount to our target based on a 1.1X pro ject P/NA V m

• Twangiza p refeasib ilit y study expected 1Q08.• Namoya prefeasib ilit y study expected 1Q08.• Lagushwa scop ing study expected 1Q08.• Drill p rog rams act ive on all p ro ject s as well as early stage exp lo rat ion on Kamituga and reg ional t argets wit h result s regularly reported.• DRC-related catalyst s include comp let ion o f the current review o f mining cont racts wit h f o reign companies (but specif ically exclud ing B anro ) and reso lut ion o f t he milit ary conf lict wit h rebel unit s in neighbouring North Kivu province. Success on these f ront s would lead t o a re-rat ing o f all DRC-exposed

Canadian Royalt ies

Inc.TSX :CZZ

Precious. B ase

M etalsCanada

• Canadian Royalt ies cont ro ls over 1,000 square kilomet res o f t he +50 kilomet re long South Rag lan Trend o f nickel-copper-cobalt -PGM mineralizat ion in Northern Québec. The t rend is t o t he south o f and parallel wit h the Rag lan Trend , which host s Xst rata’s estab lished Raglan mine. • Canad ian Royalt ies comp leted a B ankab le Feasib ilit y Study (BFS) fo r 3 deposits in t he Nunavik p ro ject in June 2007 and is working towards permit t ing by Q108 and product ion in 2010. The $466 million combined open p it and underg round mining operat ion would f eed a 3 ,500 tonne/day concent rator producing 11,800 tonnes nickel, 7,600 tonnes copper, 425 tonnes cobalt , and 93 ,100 ounces o f PGM per annum in early years.• The Nunavik pro ject has proven and p robab ly reserves o f 11.3 million tonnes grad ing 0 .97% nickel, 1.13% copper, 0 .45 grams per t onne p lat inum and 1.86 grams per t onne pallad ium.• The p ro ject is highly leveraged to metal p rices and exp lo rat ion success. The B FS d id not include the known M equillon and recent ly d iscovered high-grade A llammaq deposit s, which are undergo ing further drill exp lorat ion as a prelude to integ rat ion into the B FS. M any target s• Permit t ing is ongo ing with target commencement o f p roduct ion in Q210.• The Company recent ly completed an o f f take agreement and private p lacement wit h Russia ni

• Y ear end exp lorat ion result s, includ ing newly d iscovered A llammaq deposit and o ther potent ial target s.• M equillon update and B FS A ddendum by year-end .• Permit t ing and B enef it s A greement wit h local Inuit communit ies.• Closing o f Norilsk and o ther ag reements.• W ill X st rata “ to lerate” Norilsk’s incursion into it s own “ backyard ” and future resource base?

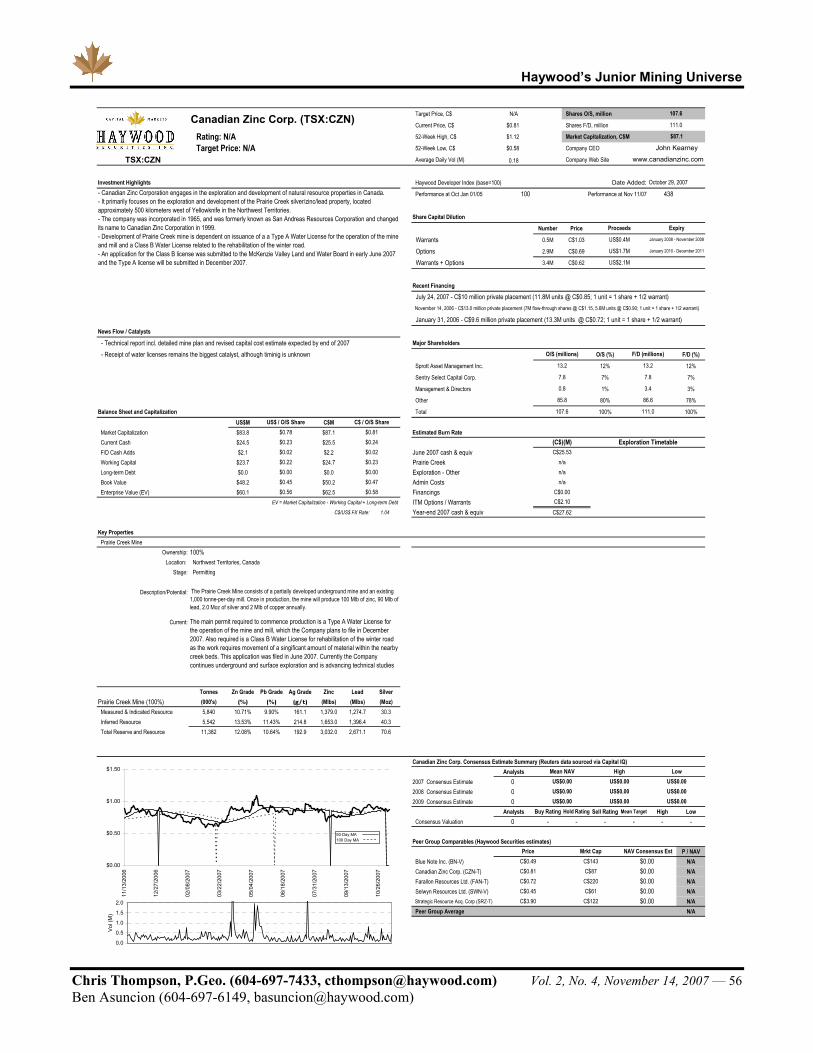

Canadian Zinc Corp. TSX :CZN

B ase M etals Canada

• Canadian Zinc Corporat ion engages in t he exp lorat ion and development o f natural resource p ropert ies in Canada. • Primarily f ocuses is on t he exp lorat ion and development o f the Prairie Creek silver/zinc/ lead propert y, located approximately 500 kilometers west o f Y ellowknif e in the Northwest Territ o ries. • Company was inco rporated in 1965 - f o rmerly known as San A ndreas Resources Corporat ion and changed it s name to Canadian Zinc Corporat ion in 1999. • Headquartered in V ancouver, Canada. • Development o f Prairie Creek mine is dependent on issuance o f a Type A W ater License for t he operat ion o f the mine and mill and a Class B W ater License related t o t he rehab ilit at ion o f t he winter road . • A n app licat ion f or the Class B license was submit t ed t o t he M cKenzie V alley Land and W ater B oard in early June 2007 and the Type A license will be submit t ed in December 2007

• Technical report incl, detailed mine p lan and revised cap ital cost est imate expected by end o f 2007• Receip t o f water licenses remains t he b iggest catalyst , although t iminig is unknown

Chario t Resources

Ltd .TSX :CHD B ase

M etalsPeru

• Chario t owns a 70% interest in t he M arcona copper p ro ject in Peru, which is the sub ject o f a bankab le f easib ilit y study expected t o be complete in Q2/08 . • W ith p roduct ion start -up ant icipated in 2010, M arcona is expected t o p roduce up t o 250 million pounds o f copper annually (cathode and concent rate) at an average to tal cash cost o f US$0.70 per pound net o f cred it s over an 18-year base-case open-p it mine life. • However, g iven t he pro ject ’s signif icant resource upside, we ant icipate that the scope o f work at M arcona will move towards higher t hroughput and/or longer lif e. • Proximit y to key inf rast ructure, includ ing po rt f acilit ies and power, enhances the pro ject ’s value and posit ions M arcona as an at t ract ive takeover target within the mid - t o senior-t ier base metals universe.

• Cont inued drilling success at M arcona through 2007• M ina Justa resource update in Q1/08• M ina Justa bankab le f easib ilit y study result s in Q2/08

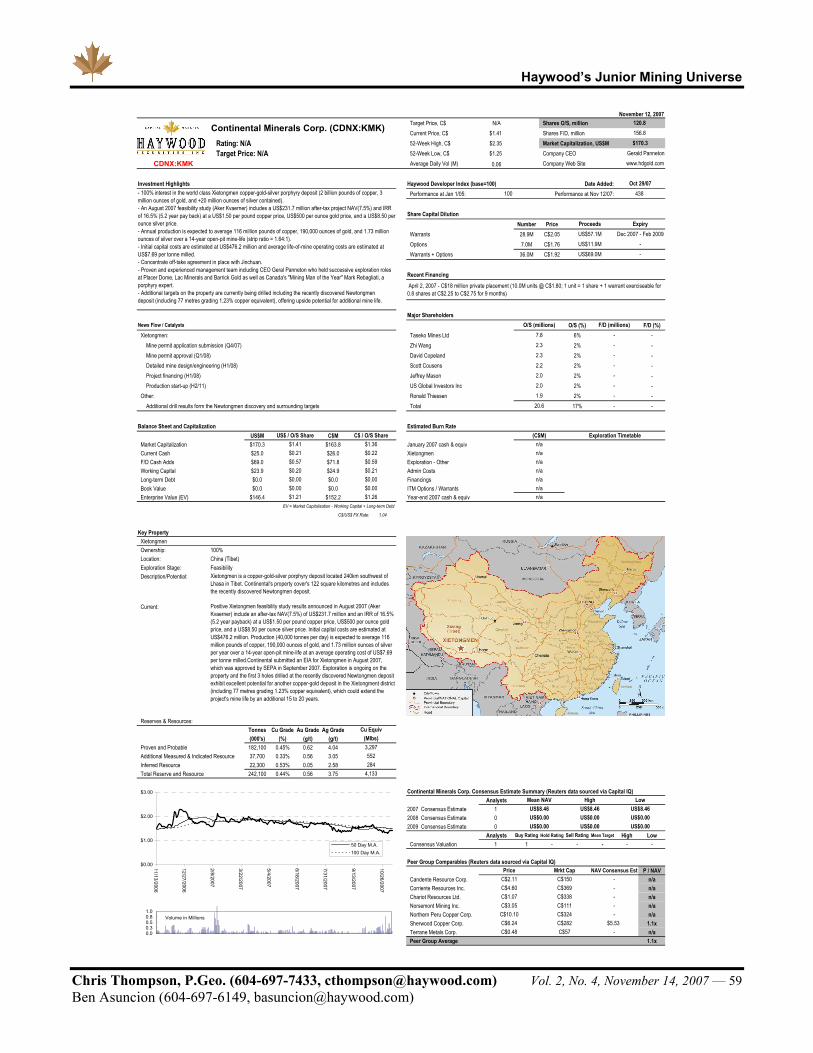

Cont inental M inerals

Corp .TSX V :KM K

Precious, B ase

M etalsChina

• 100% interest in the advanced stage M agist ral copper-mo lybdenum-silver porphyry-skarn deposit in Peru.• Over 65,000 met res o f d rilling to date has delineated at 189 million tonne measured and ind icated resource grad ing 0 .51% copper and 0 .05% mo lybdeum (2 .1 b illion pounds o f copper and 208 million pounds o f mo lybdenum contained) - the deposit remains open at depth.• A n October 2006 p refeasib ilit y study (SRK) includes a US$138 million af ter-t ax p ro ject NA V (8%) and IRR o f 17.1% (4 .6 year pay back) at a US$1.50 per pound copper p rice and a US$10 .00 per pound molybdenum price.• A nnual product ion is expected t o average 31,000 tonnes o f copper, 2 ,500 tonnes o f mo lybdenum, and 350 ,000 ounces o f silver in concent rate over a 16 -year open-p it mine-lif e (st rip rat io = 1.8 :1).• Init ial cap ital cost s are est imated at US$265 million and average lif e-o f -mine copper cash costs are est imated at US$0.77 per pound net o f cred it s.• Robust p ro ject economics are driven by a higher-g rade starter p it , simp le processing t echno logy, and good copper and mo lybdenum metallurg ical recoveries o f 89% and 69%

X ietongmen:• M ine permit app licat ion submission (Q4 /07)• M ine permit approval (Q1/08)• Detailed mine design/eng ineering (H1/08)• Pro ject f inancing (H1/08)• Product ion start -up (H2 /11) Other:• A dd it ional d rill result s fo rm Newtongmen d iscovery and surround ing t argets

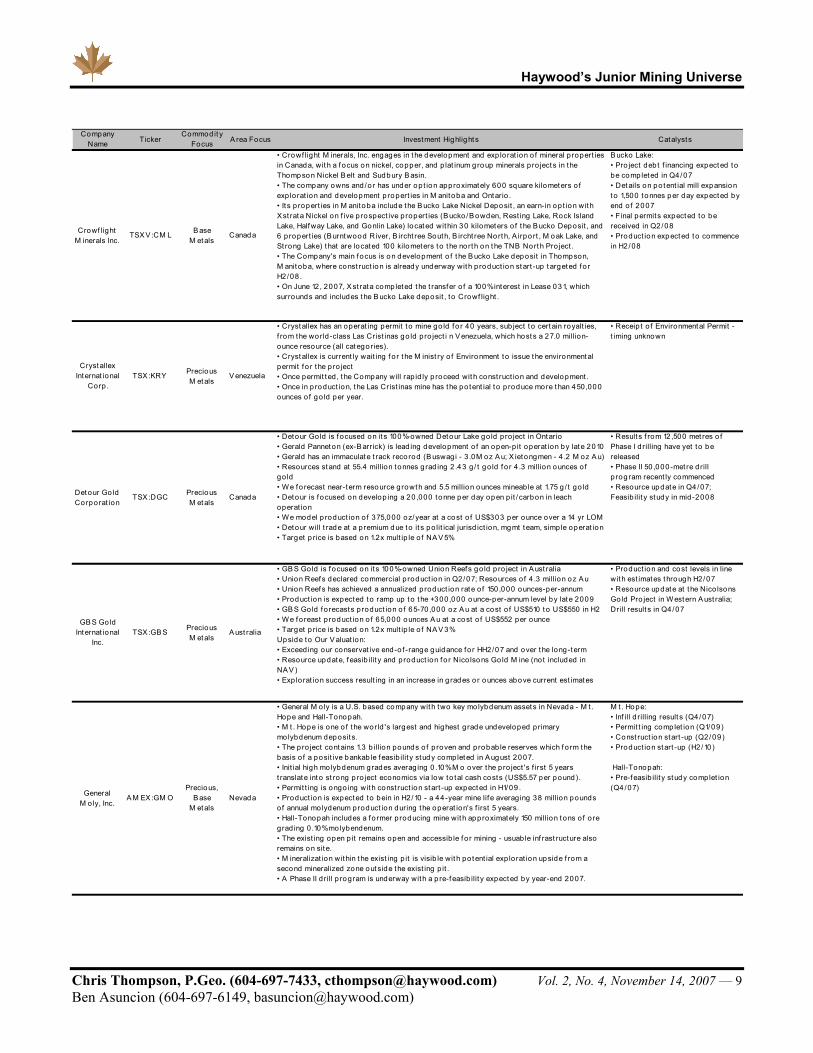

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 9 Ben Asuncion (604-697-6149, [email protected])

Company Name Ticker

Commodit y Focus A rea Focus Investment Highlight s Catalysts

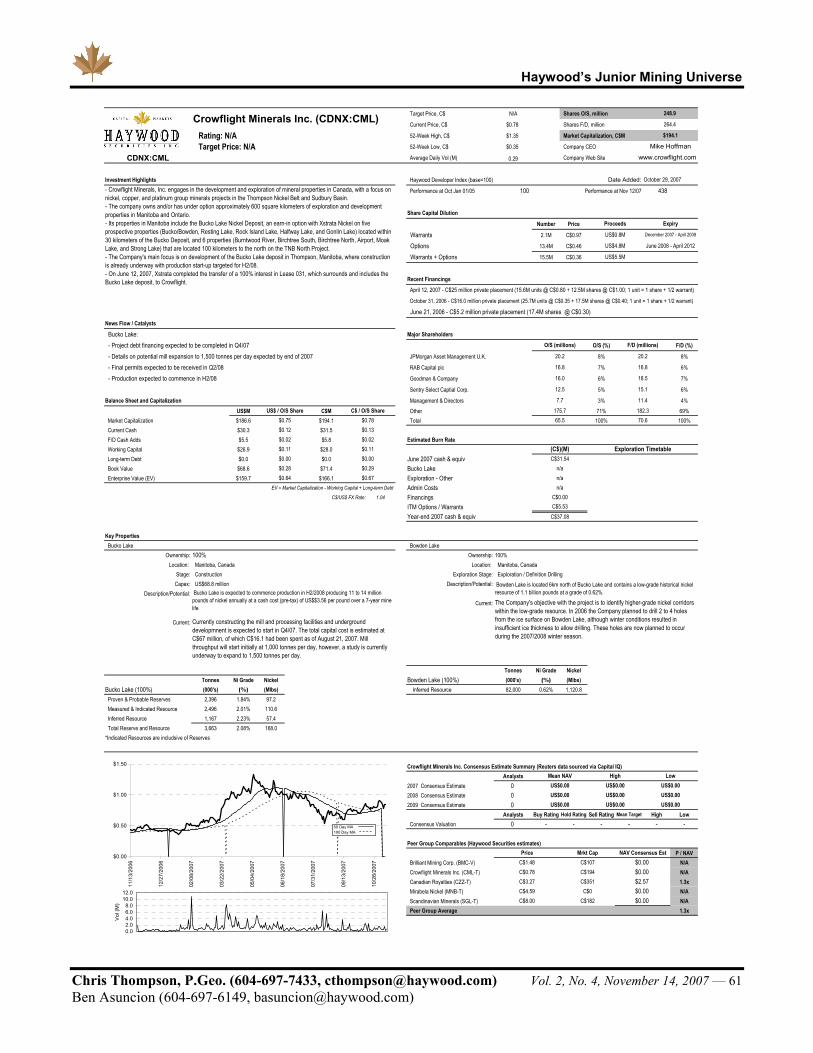

Crowf light M inerals Inc.

TSXV :CM L B ase M etals

Canada

• Crowf light M inerals, Inc. engages in t he development and exp lorat ion o f mineral p ropert ies in Canada, wit h a f ocus on nickel, copper, and p lat inum g roup minerals pro jects in the Thompson Nickel B elt and Sudbury B asin. • The company owns and /o r has under opt ion approximately 600 square kilometers o f exp lorat ion and development p ropert ies in M anitoba and Ontario . • It s p ropert ies in M anitoba include the B ucko Lake Nickel Deposit , an earn-in opt ion wit h Xst rata Nickel on f ive p rospect ive propert ies (Bucko /B owden, Rest ing Lake, Rock Island Lake, Halfway Lake, and Gonlin Lake) located within 30 kilometers o f t he Bucko Deposit , and 6 propert ies (Burntwood River, B ircht ree South, B ircht ree North, A irpo rt , M oak Lake, and St rong Lake) that are located 100 kilometers t o the north on t he TNB North Pro ject . • The Company's main focus is on development o f t he B ucko Lake deposit in Thompson, M anit oba, where const ruct ion is already underway with p roduct ion start -up t argeted fo r H2/08 . • On June 12, 2007, X st rata comp leted t he t ransfer o f a 100% interest in Lease 031, which surrounds and includes the B ucko Lake deposit , to Crowf light .

B ucko Lake:• Pro ject debt f inancing expected to be comp leted in Q4/07• Details on potent ial mill expansion to 1,500 tonnes per day expected by end o f 2007• Final permits expected to be received in Q2/08• Product ion expected t o commence in H2 /08

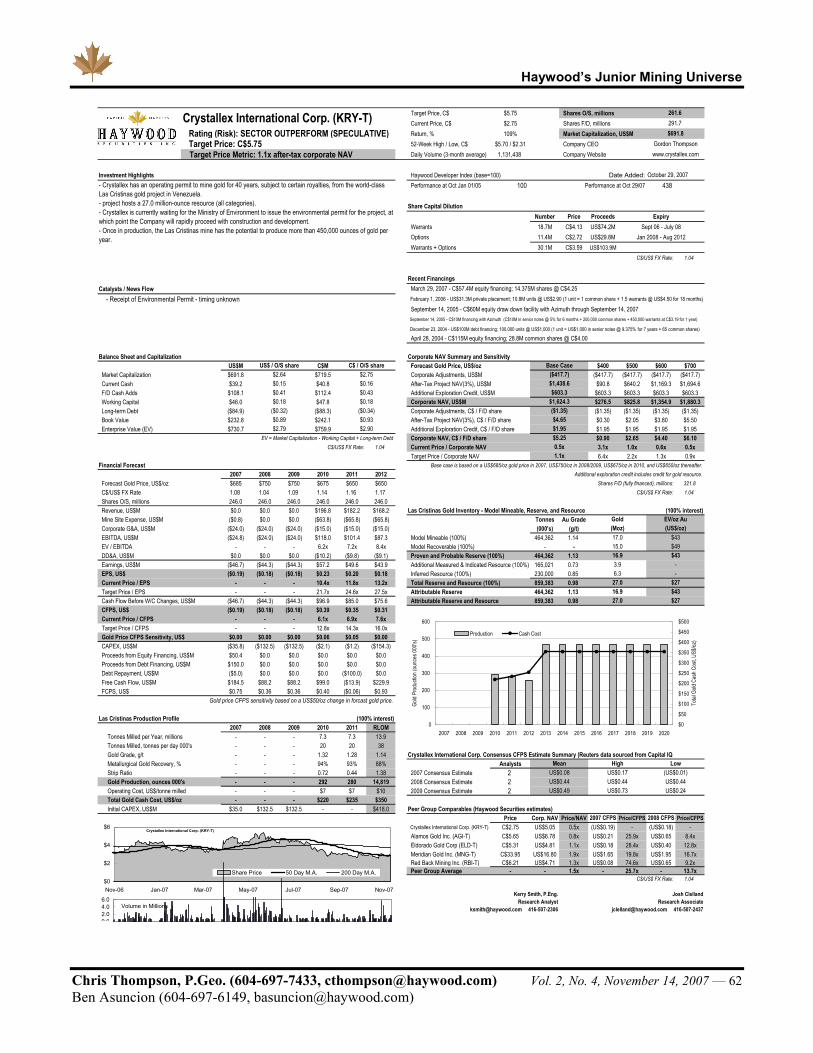

Crystallex Internat ional

Corp .TSX :KRY Precious

M etalsV enezuela

• Crystallex has an operat ing permit t o mine go ld fo r 40 years, sub ject t o certain royalt ies, f rom the world-class Las Crist inas go ld pro ject i n V enezuela, which host s a 27.0 million-ounce resource (all categories). • Crystallex is current ly wait ing f o r t he M inist ry o f Environment to issue the environmental permit fo r the pro ject • Once permit ted , t he Company will rap id ly p roceed wit h const ruct ion and development . • Once in p roduct ion, t he Las Crist inas mine has the potent ial t o p roduce more t han 450,000 ounces o f go ld per year.

• Receip t o f Environmental Permit - t iming unknown

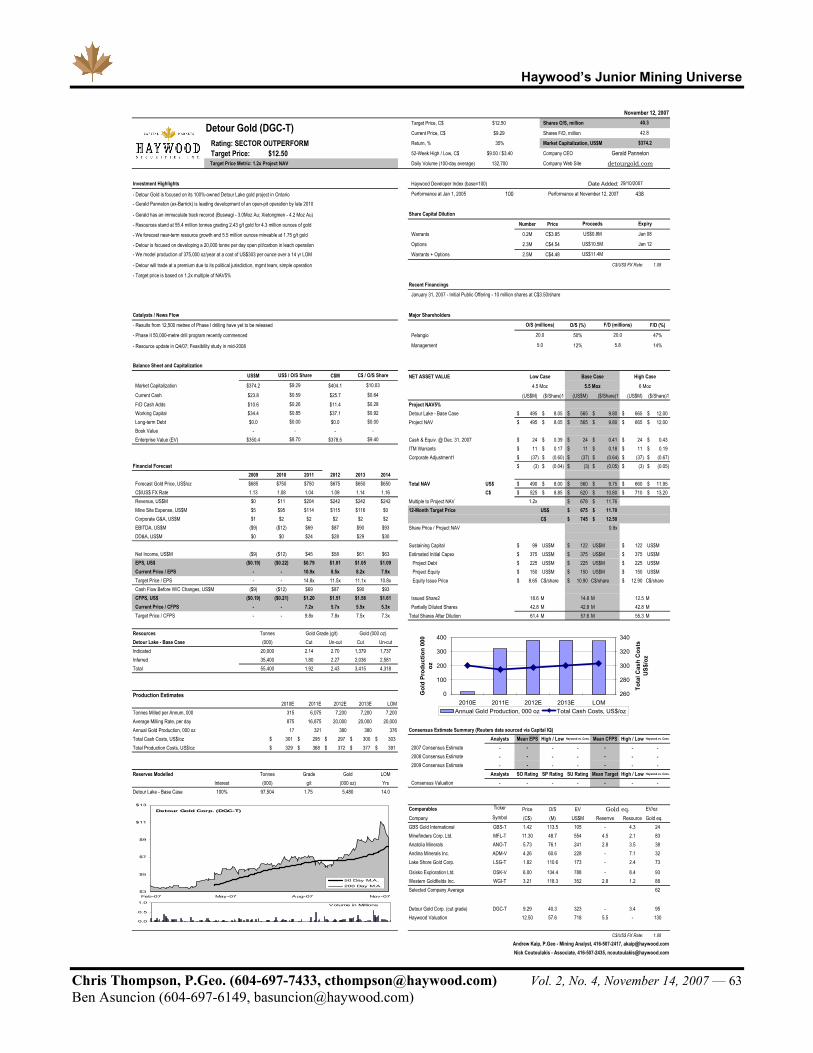

Detour Go ld Corporat ion

TSX :DGC Precious M etals

Canada

• Detour Gold is f ocused on it s 100%-owned Detour Lake go ld pro ject in Ontario• Gerald Panneton (ex-B arrick) is lead ing development o f an open-p it operat ion by late 2010• Gerald has an immaculate t rack recorod (B uswagi - 3 .0M oz A u; X ietongmen - 4 .2 M oz A u)• Resources stand at 55.4 million tonnes grad ing 2 .43 g / t go ld f o r 4 .3 million ounces o f go ld• W e fo recast near-term resource growth and 5.5 million ounces mineab le at 1.75 g / t go ld• Detour is focused on develop ing a 20 ,000 tonne per day open p it / carbon in leach operat ion• W e model p roduct ion o f 375,000 oz/year at a cost o f US$303 per ounce over a 14 yr LOM• Detour will t rade at a premium due to it s po lit ical jurisd ict ion, mgmt team, simple operat ion• Target p rice is based on 1.2x mult ip le o f NA V 5%

• Results f rom 12,500 met res o f Phase I d rilling have yet to be released• Phase II 50 ,000-met re drill p rog ram recent ly commenced• Resource update in Q4 /07; Feasib ilit y study in mid-2008

GB S Gold Internat ional

Inc.TSX :GB S Precious

M etalsA ust ralia

• GB S Gold is f ocused on it s 100%-owned Union Reefs go ld p ro ject in A ust ralia• Union Reefs declared commercial p roduct ion in Q2/07; Resources o f 4 .3 million oz Au• Union Reefs has achieved a annualized product ion rate o f 150,000 ounces-per-annum• Product ion is expected to ramp up t o t he +300,000 ounce-per-annum level by late 2009• GB S Gold fo recasts product ion o f 65-70 ,000 oz A u at a cost o f US$510 to US$550 in H2• W e fo reast product ion o f 65,000 ounces A u at a cost o f US$552 per ounce• Target p rice is based on 1.2x mult ip le o f NA V 3%Upside to Our V aluat ion:• Exceed ing our conservat ive end-o f -range guidance for HH2/07 and over t he long-term• Resource update, f easib ilit y and product ion f or Nico lsons Go ld M ine (not included in NA V )• Exp lorat ion success result ing in an increase in g rades o r ounces above current est imates

• Product ion and cost levels in line with est imates t hrough H2/07• Resource update at the Nico lsons Gold Pro ject in W estern A ust ralia; Drill result s in Q4 /07

General M oly, Inc.

A M EX :GM OPrecious,

B ase M etals

Nevada

• General M oly is a U.S. based company wit h two key molybdenum assets in Nevada - M t . Hope and Hall-Tonopah.• M t . Hope is one o f the world 's largest and highest grade undeveloped primary mo lybdenum deposits.• The p ro ject contains 1.3 b illion pounds o f p roven and probab le reserves which f orm the basis o f a posit ive bankab le f easib ilit y study completed in August 2007.• Init ial high molybdenum grades averag ing 0 .10% M o over the pro ject 's f irst 5 years t ranslate into st rong p ro ject economics via low to tal cash costs (US$5.57 per pound).• Permit t ing is ongo ing with const ruct ion start -up expected in H1/09 .• Product ion is expected to bein in H2/10 - a 44-year mine life averag ing 38 million pounds o f annual molydenum product ion during the operat ion's f irst 5 years.• Hall-Tonopah includes a fo rmer producing mine wit h approximately 150 million t ons o f o re grad ing 0 .10% mo lybendenum.• The exist ing open p it remains open and accessib le f o r mining - usuab le inf rast ructure also remains on site.• M ineralizat ion wit hin t he exist ing p it is visib le wit h potent ial exp lorat ion upside f rom a second mineralized zone outside the exist ing p it .• A Phase II d rill p rogram is underway with a p re-feasib ilit y expected by year-end 2007.

M t . Hope:• Inf ill d rilling result s (Q4/07)• Permit t ing comp let ion (Q1/09)• Const ruct ion start -up (Q2/09)• Product ion start -up (H2/10)

Hall-Tonopah:• Pre-feasib ilit y study complet ion (Q4 /07)

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 10 Ben Asuncion (604-697-6149, [email protected])

Company Name Ticker

Commodit y Focus A rea Focus Investment Highlight s Catalysts

Inca Pacif ic Resources

Inc.TSXV :IPR B ase

M etalsPeru

• 100% interest in t he advanced stage M agist ral copper-molybdenum-silver po rphyry-skarn deposit in Peru.• Over 65,000 met res o f drilling to date has delineated at 189 million tonne measured and ind icated resource g rad ing 0 .51% copper and 0 .05% molybdeum (2 .1 b illion pounds o f copper and 208 million pounds o f molybdenum contained) - the deposit remains open at depth.• A n October 2006 prefeasib ilit y study (SRK) includes a US$138 million af t er-tax pro ject NA V (8%) and IRR of 17.1% (4 .6 year pay back) at a US$1.50 per pound copper price and a US$10 .00 per pound molybdenum price.• A nnual p roduct ion is expected to average 31,000 tonnes o f copper, 2 ,500 tonnes o f mo lybdenum, and 350,000 ounces o f silver in concent rate over a 16-year open-p it mine-lif e (st rip rat io = 1.8 :1).• Init ial cap it al costs are est imated at US$265 million and average lif e-o f -mine copper cash costs are est imated at US$0.77 per pound net o f cred its.• Robust pro ject economics are driven by a higher-g rade starter p it , simple p rocessing techno logy, and good copper and molybdenum metallurg ical recoveries o f 89% and 69% respect ively.

M agist ral:• EIS and feasib ilit y study complet ion (Q4/07) • Pro ject f ianncing (H1/08)• Const ruct ion start -up (Q3/08)• Product ion start -up (2010?)

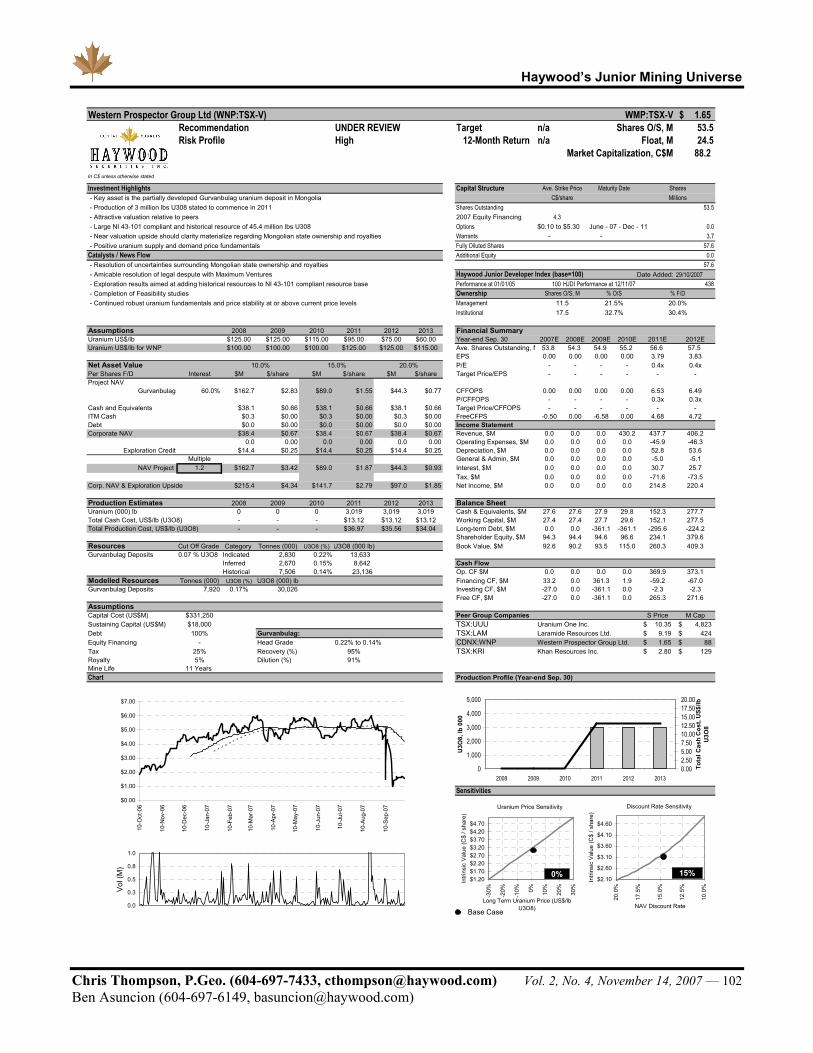

Khan Resources

Inc.TSX :KRI Uranium M ongo lia

• Key asset is the part ially developed Dornod uranium deposit in M ongo lia• Product ion o f 2 .5 million lbs U308 stated t o commence in 2010• A t t ract ive valuat ion relat ive to peers• Large NI 43-101 compliant resource o f 37.8 million lbs U308 • Near valuat ion upside should clarit y materialize regard ing M ongolian state ownership and royalt ies• Posit ive uranium supp ly and demand price f undamentals

• Reso lut ion o f uncertaint ies surround ing M ongolian state ownership and royalt ies • Comp let ion o f Feasib ilit y stud ies• Cont inued robust uranium fundamentals and price stab ilit y at o r above current price levels

Katanga M ining Limited

TSX:KA T B ase M etals

Democrat ic Republic o f the Congo

• Katanga is working t o restart p roduct ion at it s 75% owned Kamoto copper-cobalt mine in the Democrat ic Repub lic o f Congo - with f irst copper cathode p roduct ion expected by year-end• Kamoto is being developed in four phases, with annual p roduct ion expected to reach 150,000 tonnnes o f copper cathode and 8 ,000 tonnes o f cobalt cathode by 2012. • Fo llowing a b id f rom Cent ral A f rican M ining , Katanga estab lished an Independent Commit tee t o carry out a srateg ic review of alternat ives. • The review p rocess was rumoured to have at t racted companies such as Ang lo A merican, BHP B illit on, Xst rata, Rio Tinto , First Quantum, and Nikanor. • Katanga recent ly announced that the review p rocess was over, with no b ids emerg ing, and has decided to proceed with development o f Kamoto alone. • Katanga recent ly announced a US$150 million convert ib le loan wit h Glencore, which if converted will g ive Glencore a 10% of the Company on a f ully d iluted basis. • In add it ion, Katanga gave up all the market ing rights fo r both copper and cobalt p roduct ion fo r 10 years beg inning in 2009 .

• December 2007 - 1st copper cathode product ion• End o f 2007 (est imated) - Complet ion o f DRC license review

Laramide Resources

Ltd .TSX :LA M Uranium

A ust ralia, USA

• Key asset is the W estmoreland uranium deposit in A ust ralia and a p rospect ive US p ropert y package• Product ion o f 3 million lbs U308 stated t o commence in 2011• A t t ract ive valuat ion relat ive to peers• Large NI 43-101 compliant resource invento ry o f 48 .5 million lbs U308 • Near valuat ion upside should clarit y materialize regard ing accep tance o f uranium mining in Queensland• Posit ive uranium supp ly and demand price f undamentals• Prospect ive port f o lio o f go ld assets slated to be spun o f f into a separate pub lic vehicle

• Reso lut ion o f uncertaint ies surround ing uranium mining in Queensland , A ust ralia• Exp lorat ion result s f rom in-f ill d rilling and exp lo rat ion drilling at W estmorelands• Complet ion o f Feasib ilit y stud ies• Sp in out o f non-uranium assets• Cont inued robust uranium fundamentals and price stab ilit y at o r above current price levels

M irabela Nickel Ltd .

A SX:M B N B ase M etals

B razil

• M irabela Nickel Limited engages in t he exp lorat ion and development o f mineral p ropert ies in B razil. • The company ho lds interest s in the Santa Rit a nickel sulphide and the Serra A zul nickel sapro lite pro jects located in the state o f B ahia, B razil. • It also owns an interest in the Sao Francisco nickel sulphide exp lorat ion pro ject located approximately 15 kilometers f rom Piranhas and Caninde de Sao Francisco. • In add it ion, M irabela Nickel Limited ho lds interest s in Palest ina Nickel Exp lorat ion prospect , which is located 25 kilometers south o f Santa Rit a p ro ject , as well as Ponto Novo, a nickel sulphide and laterit e exp lorat ion prospect located approximately 220 kilometers north-west o f Salvador. • Current ly, the Company's primary focus is on development o f t he Santa Rita p ro ject , t he largest greenf ield nickel d iscovery world-wide in 12 years, which is expected to commence product ion in Q2 /09 and p roduce about 41 million pounds o f nickel annually. • Procurement o f long-lead it ems has already commenced and detailed eng ineering and design is underway.

Santa Rit a:• Receip t o f mining and environmental permits expected by end o f October 2007 fo llow by const ruct ion• Updated resource est imate expected in late October 2007 (incl. Cent ral and Southern Deeps drilling )• Probab le reserve calculat ion p lanned for November 2007• Finalizat ion o f debt f inancing and o f f -take agreement expected by Q1/08

Other:• Commencement o f drilling on Palest ina scheduled t o start in October 2007

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 11 Ben Asuncion (604-697-6149, [email protected])

Company Name Ticker

Commodit y Focus A rea Focus Investment Highlight s Catalysts

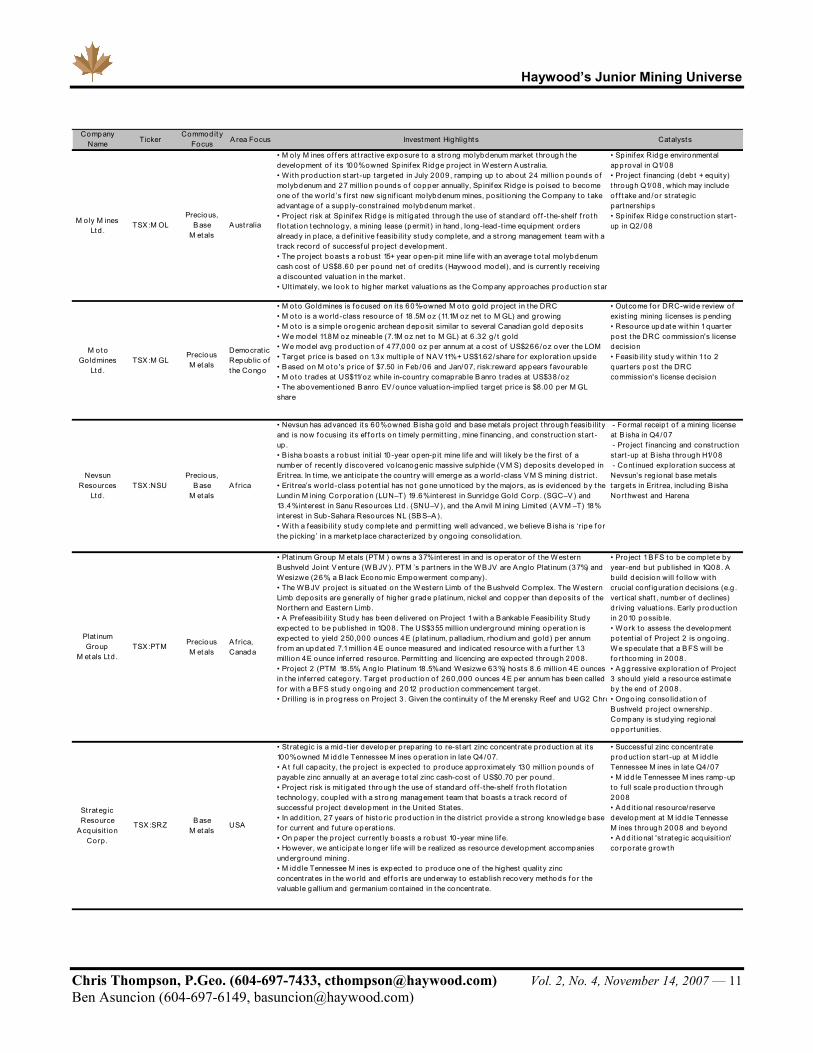

M oly M ines Ltd .

TSX :M OLPrecious,

B ase M etals

A ust ralia

• M oly M ines o f f ers at t ract ive exposure to a st rong molybdenum market through the development o f it s 100% owned Sp inif ex Ridge pro ject in W estern A ust ralia. • W ith product ion start -up targeted in July 2009 , ramping up to about 24 million pounds o f mo lybdenum and 27 million pounds o f copper annually, Sp inif ex Ridge is po ised to become one o f the world ’s f irst new signif icant molybdenum mines, posit ioning the Company to take advantage o f a supp ly-const rained molybdenum market . • Pro ject risk at Sp inif ex Ridge is mit igated t hrough the use o f standard o f f -t he-shelf f ro th f lo tat ion t echno logy, a mining lease (permit ) in hand , long-lead-t ime equipment orders already in p lace, a def init ive f easib ilit y study complete, and a st rong management team with a t rack record o f successful p ro ject development . • The p ro ject boasts a robust 15+ year open-p it mine lif e with an average to tal molybdenum cash cost o f US$8.60 per pound net o f cred it s (Haywood model), and is current ly receiving a d iscounted valuat ion in the market . • Ult imately, we look t o higher market valuat ions as t he Company approaches product ion star

• Sp inifex Ridge environmental approval in Q1/08• Pro ject f inancing (debt + equity) through Q1/08 , which may include o f f t ake and /or st rateg ic partnerships• Sp inifex Ridge const ruct ion start -up in Q2/08

M oto Go ldmines

Ltd .TSX :M GL

Precious M etals

Democrat ic Republic o f the Congo

• M oto Goldmines is focused on it s 60%-owned M oto go ld p ro ject in the DRC• M oto is a world -class resource o f 18.5M oz (11.1M oz net t o M GL) and growing• M oto is a simp le orogenic archean deposit similar t o several Canad ian go ld deposits• W e model 11.8M oz mineab le (7.1M oz net t o M GL) at 6 .32 g / t go ld• W e model avg p roduct ion o f 477,000 oz per annum at a cost o f US$266/oz over t he LOM• Target p rice is based on 1.3x mult ip le o f NA V 11% + US$1.62/share fo r exp lo rat ion upside• B ased on M oto 's price o f $7.50 in Feb/06 and Jan/07, risk:reward appears favourab le• M oto t rades at US$11/oz while in-count ry comaprab le B anro t rades at US$38 /oz• The abovement ioned B anro EV /ounce valuat ion-imp lied target p rice is $8 .00 per M GL share

• Outcome for DRC-wide review o f exist ing mining licenses is pend ing• Resource update wit hin 1 quarter post the DRC commission's license decision• Feasib ilit y study wit hin 1 to 2 quarters post t he DRC commission's license decision

Nevsun Resources

Ltd .TSX :NSU

Precious, B ase

M etalsA f rica

• Nevsun has advanced it s 60% owned B isha go ld and base metals pro ject t hrough feasib ilit y and is now focusing it s ef f o rt s on t imely permit t ing , mine f inancing , and const ruct ion start -up. • B isha boasts a robust init ial 10 -year open-p it mine life and will likely be the f irst o f a number o f recent ly d iscovered vo lcanogenic massive sulphide (V M S) deposit s developed in Erit rea. In t ime, we ant icipate t he count ry will emerge as a world-class V M S mining d ist rict .• Erit rea’s world-class potent ial has no t gone unno t iced by the majors, as is evidenced by t he Lund in M ining Corporat ion (LUN–T) 19 .6% interest in Sunridge Go ld Corp. (SGC–V ) and 13.4% interest in Sanu Resources Ltd . (SNU–V ), and the A nvil M ining Limited (A V M –T) 18% interest in Sub-Sahara Resources NL (SBS–A ). • W ith a feasib ilit y study comp lete and permit t ing well advanced , we believe B isha is ‘ripe f or the p icking ’ in a marketp lace characterized by ongo ing conso lidat ion.

- Formal receip t o f a mining license at B isha in Q4 /07 - Pro ject f inancing and const ruct ion start -up at B isha through H1/08 - Cont inued exp lorat ion success at Nevsun’s reg ional base metals targets in Erit rea, includ ing B isha Northwest and Harena

Plat inum Group

M etals Ltd .TSX :PTM Precious

M etalsA f rica, Canada

• Plat inum Group M etals (PTM ) owns a 37% interest in and is operato r o f the W estern Bushveld Jo int V enture (W BJV ). PTM ’s partners in t he W B JV are A ng lo Plat inum (37%) and Wesizwe (26%, a B lack Economic Empowerment company).• The W B JV pro ject is situated on the W estern Limb o f t he Bushveld Complex. The W estern Limb deposits are generally o f higher grade p lat inum, nickel and copper t han deposit s o f t he Northern and Eastern Limb.• A Prefeasib ilit y Study has been delivered on Pro ject 1 with a B ankab le Feasib ilit y Study expected t o be pub lished in 1Q08. The US$355 million underground mining operat ion is expected t o yield 250,000 ounces 4E (p lat inum, pallad ium, rhod ium and go ld ) per annum f rom an updated 7.1 million 4E ounce measured and ind icated resource with a furt her 1.3 million 4E ounce inferred resource. Permit t ing and licencing are expected through 2008.• Pro ject 2 (PTM 18 .5%, A ng lo Plat inum 18.5% and W esizwe 63%) hosts 8 .6 million 4E ounces in t he inferred category. Target product ion o f 260 ,000 ounces 4E per annum has been called for with a B FS study ongo ing and 2012 product ion commencement target .• Drilling is in progress on Pro ject 3 . Given the cont inuit y o f the M erensky Reef and UG2 Chro

• Pro ject 1 B FS to be complete by year-end but pub lished in 1Q08. A build decision will f o llow wit h crucial conf igurat ion decisions (e.g . vert ical shaf t , number o f declines) driving valuat ions. Early product ion in 2010 possib le.• W ork to assess the development po tent ial o f Pro ject 2 is ongo ing. W e speculate that a B FS will be fo rt hcoming in 2008.• A ggressive exp lorat ion o f Pro ject 3 should yield a resource est imate by t he end o f 2008.• Ongo ing conso lidat ion o f B ushveld pro ject ownership . Company is studying reg ional opportunit ies.

St rateg ic Resource

A cquisit ion Corp.

TSX:SRZ B ase M etals

USA

• St rateg ic is a mid -t ier developer preparing to re-start zinc concent rate product ion at it s 100% owned M idd le Tennessee M ines operat ion in late Q4/07. • A t f ull capacit y, the pro ject is expected to produce approximately 130 million pounds o f payab le zinc annually at an average to tal zinc cash-cost o f US$0.70 per pound. • Pro ject risk is mit igated through the use o f standard o f f -the-shelf f ro th f lo tat ion techno logy, coup led wit h a st rong management team that boasts a t rack record o f successful p ro ject development in t he Unit ed States. • In add it ion, 27 years o f histo ric product ion in the d ist rict p rovide a st rong knowledge base for current and future operat ions. • On paper the pro ject current ly boasts a robust 10-year mine lif e. • However, we ant icipate longer life will be realized as resource development accompanies underg round mining . • M idd le Tennessee M ines is expected t o produce one o f t he highest qualit y zinc concent rates in t he world and ef f ort s are underway to estab lish recovery methods fo r the valuab le gallium and germanium contained in t he concent rate.

• Successful zinc concent rate product ion start -up at M idd le Tennessee M ines in late Q4/07• M idd le Tennessee M ines ramp-up to full scale p roduct ion through 2008• A dd it ional resource/ reserve development at M idd le Tennesse M ines t hrough 2008 and beyond• A dd it ional 'st rateg ic acquisit ion' corporate growth

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 12 Ben Asuncion (604-697-6149, [email protected])

Company Name Ticker

Commodit y Focus A rea Focus Investment Highlights Catalyst s

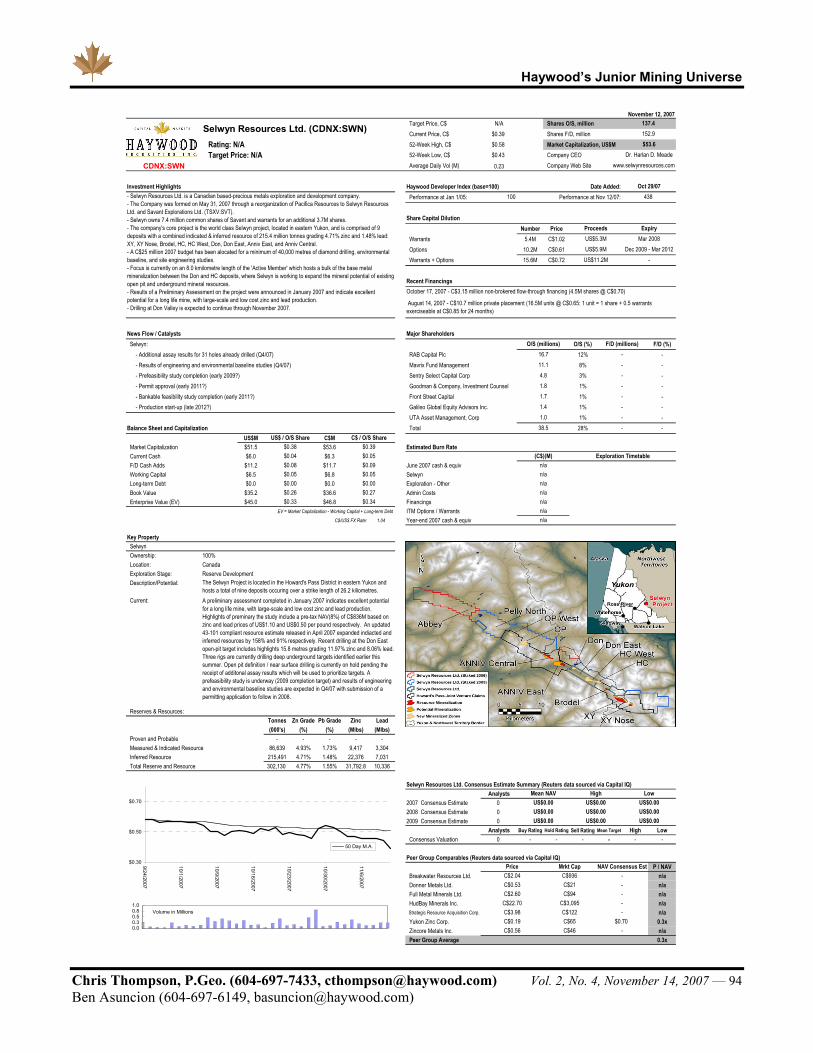

Selwyn Resources

Ltd .TSX V :SW N

B ase M etals Canada

• Selwyn Resources Ltd . is a Canad ian based-precious metals exp lo rat ion and development company. • The Company was formed on M ay 31, 2007 through a reo rganizat ion o f Pacif ica Resources t o Selwyn Resources Ltd . and Savant Exp lorat ions Ltd . (TSX V :SV T).• Selwyn owns 7.4 million common shares o f Savant and warrants fo r an add it ional 3 .7M shares.• The company's co re p ro ject is t he world class Selwyn p ro ject , located in eastern Y ukon, and is comprised o f 9 deposits wit h a combined ind icated & inferred resource o f 215.4 million tonnes grad ing 4 .71% zinc and 1.48% lead : X Y , X Y Nose, B rodel, HC, HC W est , Don, Don East , A nniv East , and A nniv Cent ral.• A C$25 million 2007 budget has been alocated fo r a minimum o f 40,000 met res o f d iamond drilling , environmental baseline, and sit e eng ineering stud ies. • Focus is current ly on an 8 .0 kmilomet re length o f the 'A ct ive M ember' which host s a bulk o f t he base metal mineralizat ion between the Don and HC deposit s, where Selwyn is working to expand the mineral potent ial o f exist ing open p it and underg round mineral resources.• Results o f a Preliminary A ssessment on t he pro ject were announced in January 2007 and ind i• Drilling at Don V alley is expected t o cont inue through November 2007.

• A dd it ional assay results f o r 31 ho les already d rilled (Q4 /07)• Result s o f eng ineering and environmental baseline stud ies (Q4/07)• Prefeasib ilit y study comp let ion (early 2009?)• Permit approval (early 2011?)• B ankab le feasib ilit y study comp let ion (early 2011?)• Product ion start -up (late 2012?)

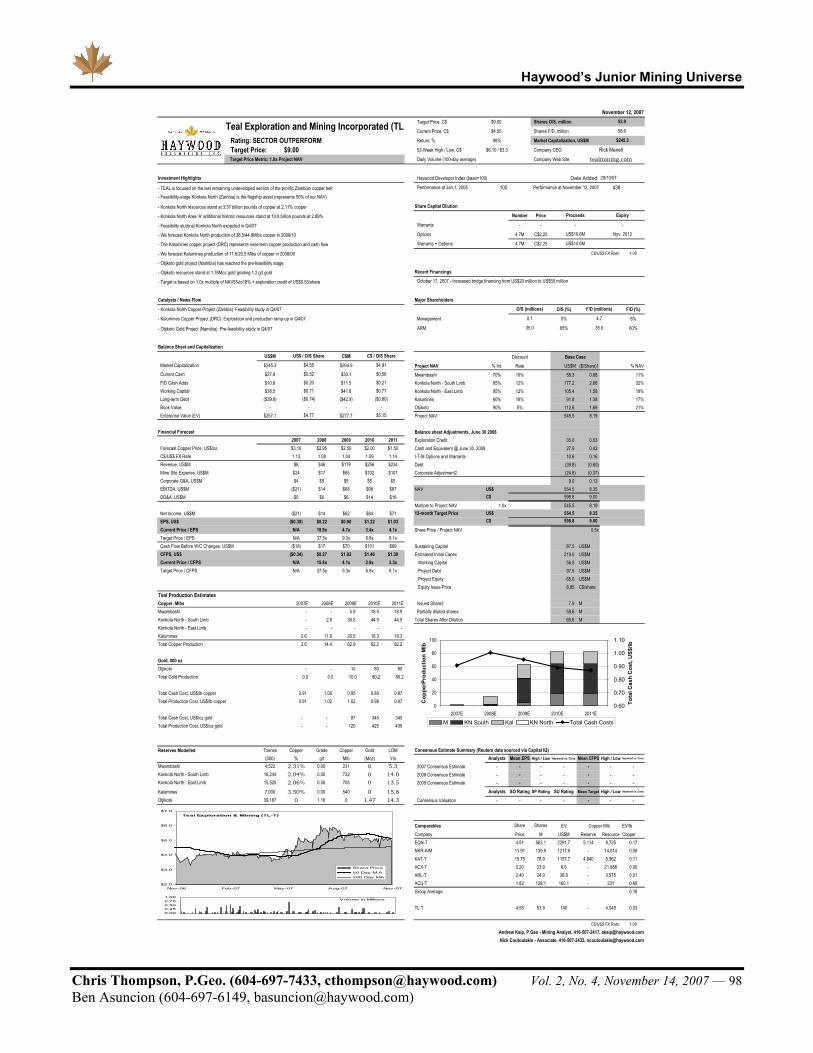

TEA L Exp lo rat ion & M ining Inc

TSX :TLB ase

M etals

DRC, Namib ia, Zambia

• TEA L is focused on the last remaining undeveloped sect ion o f t he pro lif ic Zamb ian copper belt• Feasib ilit y-stage Konko la North (Zamb ia) is t he f lagship asset (represents 50% o f our NA V )• Konko la North resources stand at 3 .37 b illion pounds o f copper at 2 .11% copper • Konko la North A rea 'A ' add it ional histo ric resources stand at 10.8 b illion pounds at 2 .89%• Feasib ilit y study at Konko la North expected in Q4/07• W e fo recast Konko la North product ion o f 36.5/44 .9M lbs copper in 2009 /10• The Kalumines copper pro ject (DRC) represents near-t erm copper p roduct ion and cash f low• W e fo recast Kalumines p roduct ion o f 11.6 /20 .5 M lbs o f copper in 2008/09• Ot jiko to go ld p ro ject (Namib ia) has reached the pre-feasib ilit y stage• Ot jiko to resources stand at 1.76M oz go ld g rad ing 1.2 g / t go ld• Target is based on 1.0x mult ip le o f NA V 5%to18% + exp lo rat ion cred it o f US$0 .53/share

• Konko la North Copper Pro ject (Zambia): Feasib ilit y study in Q4 /07• Kalumines Copper Pro ject (DRC): Exp lorat ion and p roduct ion ramp-up in Q4 /07• Ot jiko to Go ld Pro ject (Namib ia): Pre-feasib ilit y study in Q4/07

Terrane M etals Corp .

TSX V :TRXPrecious,

B ase M etals

Canada

• 100% interest in t he advanced stage M t . M illigan copper-go ld porphyry deposit in B rit ish Co lumbia (1.9 b illion pounds o f copper and 5.5 million ounces o f go ld contained). • A n October 2007 p reliminary economic assessment (W ardrop) includes a C$580 million p re-tax p ro ject NA V (8%) and IRR of 20.6% (3 .9 year pay back) at a US$2.50 per pound copper p rice and a US$550 per ounce go ld p rice.• A nnual product ion is expected t o average 90 million pounds o f copper and 221,530 ounces o f go ld over a 14.5-year open-p it mine-life (st rip rat io = 0 .8 :1).• Init ial cap ital costs are est imated at C$827 million and average lif e-o f -mine operat ing cost s are est imated at C$7.12 per tonne milled .• The p ro ject sit s within t he M cKenzie land use p lan, an area zoned for mine (and related inf rast ructure) development .• Terran'e p ro ject port f o lio extends beyond M t M illigan and includes a 100% interest in the advanced stage B erg copper-moly-silver pro ject in B rit ish Columb ia. In late June 2007, Terrane announced that it had commenced a 12,000 meter drilling p rogram at B erg and W ardrop Eng ineering has been cont racted t o deliver a NI 43-101 compliant resource est imate • Terrane's management t eam consist s o f t op notch geo log ists wit h an int imate knowledge o f • Global M ajor Pro ject s who was o rig inally responsib le f o r d iscovering the sit e.

M ount M illigan:• Full feasib ilit y study complet ion (Q1/08)• Environmental A ssessment Complet ion (mid -2008)• Const ruct ion Start -up (mid -20008)• Product ion Start -up (2011) B erg :• NI 43-101 compliant resource est imate (Q4/07)• Def init ion drilling results (H1/08)• Scop ing study complet ion (Q2/08)• Feasib ilit y study comp let ion (mid -2010)

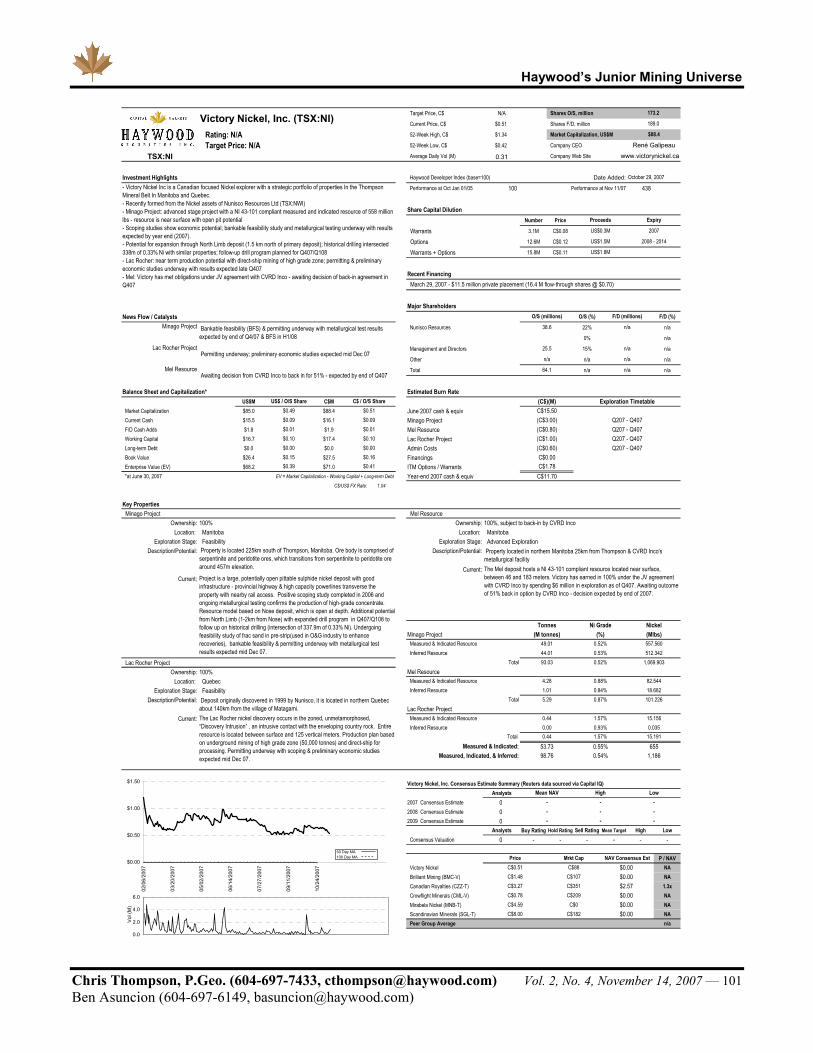

V ictory Nickel, Inc.

TSX :NI B ase M etals

Canada

• V icto ry Nickel Inc is a Canad ian focused Nickel exp lo rer with a st rateg ic port f o lio o f p ropert ies In t he Thompson M ineral B elt In M anit oba and Quebec.• Recent ly f o rmed f rom the Nickel assets o f Nunisco Resources Ltd (TSX :NW I)• M inago Pro ject : advanced stage pro ject wit h a NI 43 -101 comp liant measured and ind icated resource o f 558 million lbs - resource is near surface with open p it po tent ial• Scop ing stud ies show economic potent ial; bankab le feasib ilit y study and metallurg ical t est ing underway with results expected by year end (2007).• Po tent ial fo r expansion t hrough North Limb deposit (1.5 km north o f p rimary deposit ); historical d rilling intersected 338m of 0 .33% Ni wit h similar p ropert ies; f o llow-up drill p rogram p lanned fo r Q407/Q108• Lac Rocher: near t erm p roduct ion potent ial with d irect -ship mining o f high grade zone; permit t ing & p reliminary economic stud ies underway wit h result s expected late Q407• M el: V icto ry has met ob ligat ions under JV agreement wit h CV RD Inco - await ing decision o f back-in ag reement in Q407

M inago Pro ject• B ankab le feasib ilit y (B FS) & permit t ing underway wit h metallurg ical t est results expected by end o f Q4/07 & B FS in H1/08

Lac Rocher Pro ject• Permit t ing underway; preliminary economic stud ies expected mid Dec 07

M el Resource• A wait ing decision f rom CV RD Inco to back in fo r 51% - expected by end o f Q407

W estern Prospector Group Ltd .

TSX V :W NP Uranium M ongo lia

• Key asset is the part ially developed Gurvanbulag uranium deposit in M ongo lia• Product ion o f 3 million lbs U308 stated to commence in 2011• A t t ract ive valuat ion relat ive to peers• Large NI 43 -101 comp liant and histo rical resource o f 45.4 million lbs U308 • Near valuat ion upside should clarit y materialize regard ing M ongo lian state ownership and royalt ies• Posit ive uranium supp ly and demand price fundamentals

• Reso lut ion o f uncertaint ies surround ing M ongo lian state ownership and royalt ies • A micab le reso lut ion o f legal despute wit h M aximum V entures • Exp lo rat ion results aimed at add ing historical resources t o NI 43-101 compliant resource base• Complet ion o f Feasib ilit y stud ies• Cont inued robust uranium fundamentals and price stab ilit y at o r above current p rice levels

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 13 Ben Asuncion (604-697-6149, [email protected])

HAYWOOD’S JUNIOR EXPLORATION INDEX (HJEI)

Performance: October 29 to November 12, 2007 The HJEI lost 23 points or 3% during the period October 29 to November 12, 2007, to close at an indexed value of 833, with January 1, 2005, as a 100 point base.

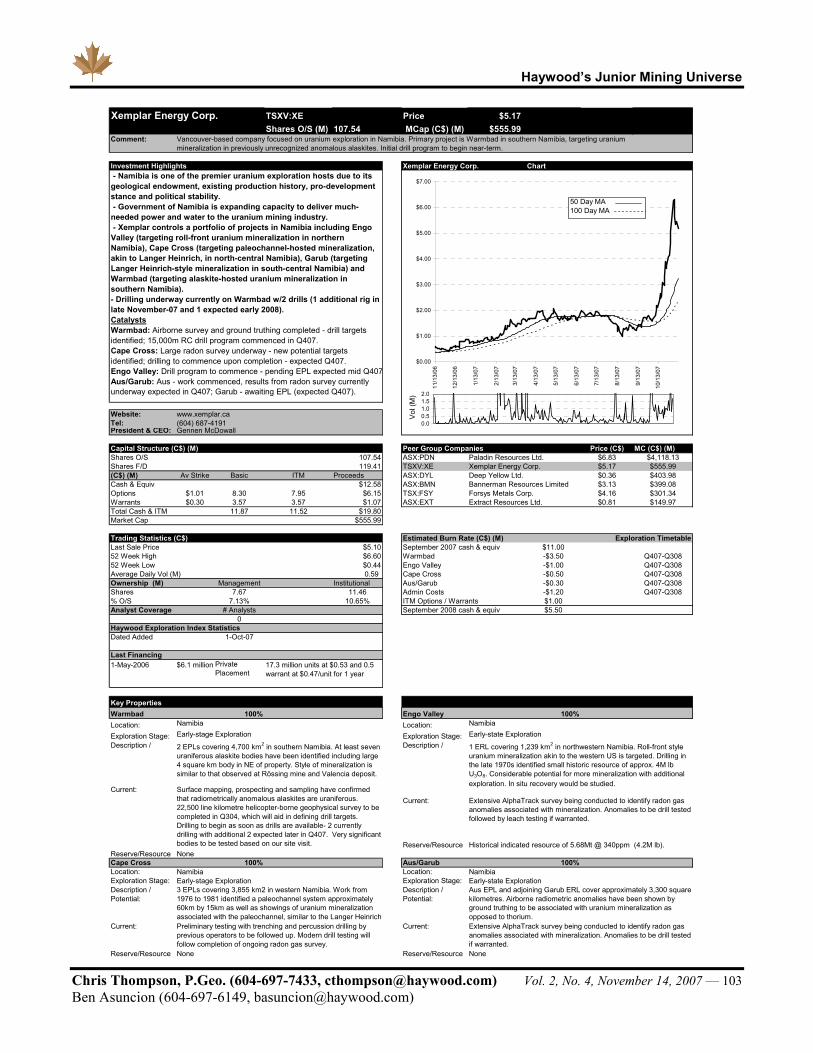

During the reporting period, seven companies returned notable gains, led by Namibian-focused uranium explorer Xemplar Energy (TSXV:XE), Canadian uranium explorer Forum Uranium (TSXV:FDC), and Canadian diamond explorer Diamondex Resources (TSXV:DSP—with respectable gains of 26%, 19%, and 10% respectively.

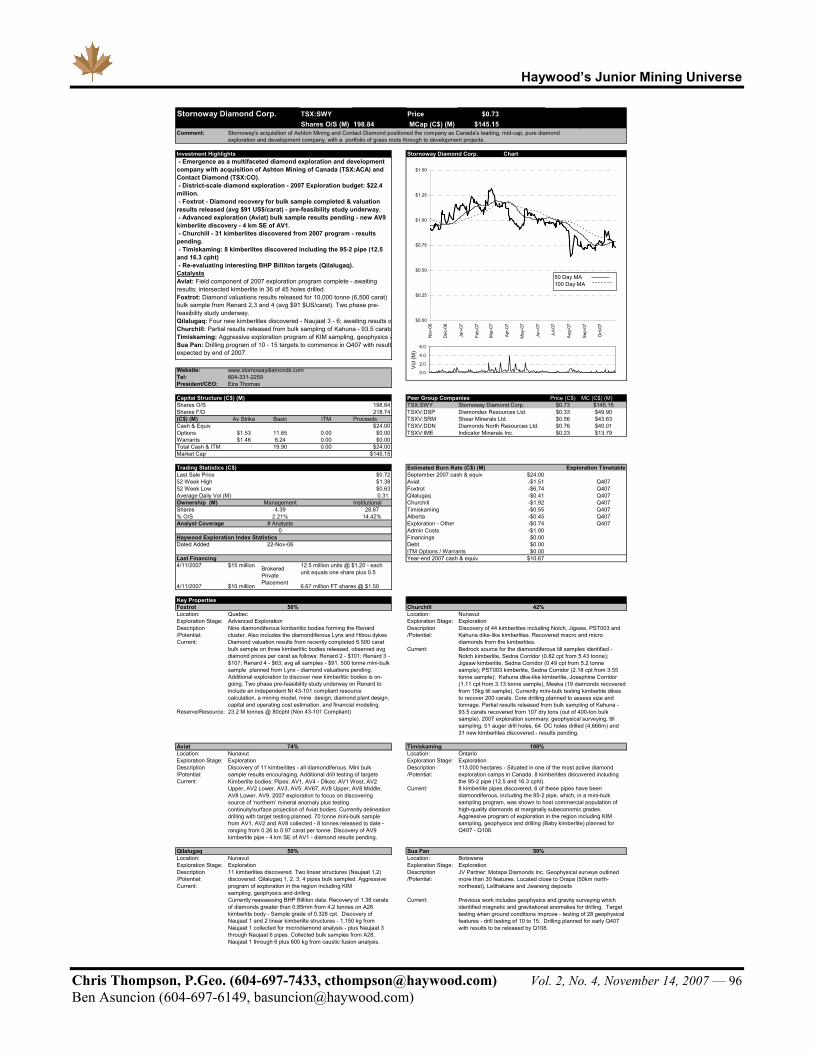

Twenty companies recorded percentage losses for the period, with Calibre Mining (TSXV:CXB) leading the slide with a decline of 20%, and Canadian diamond explorer Stornoway Diamonds (TSXV:SWY) with a decline of 18%.

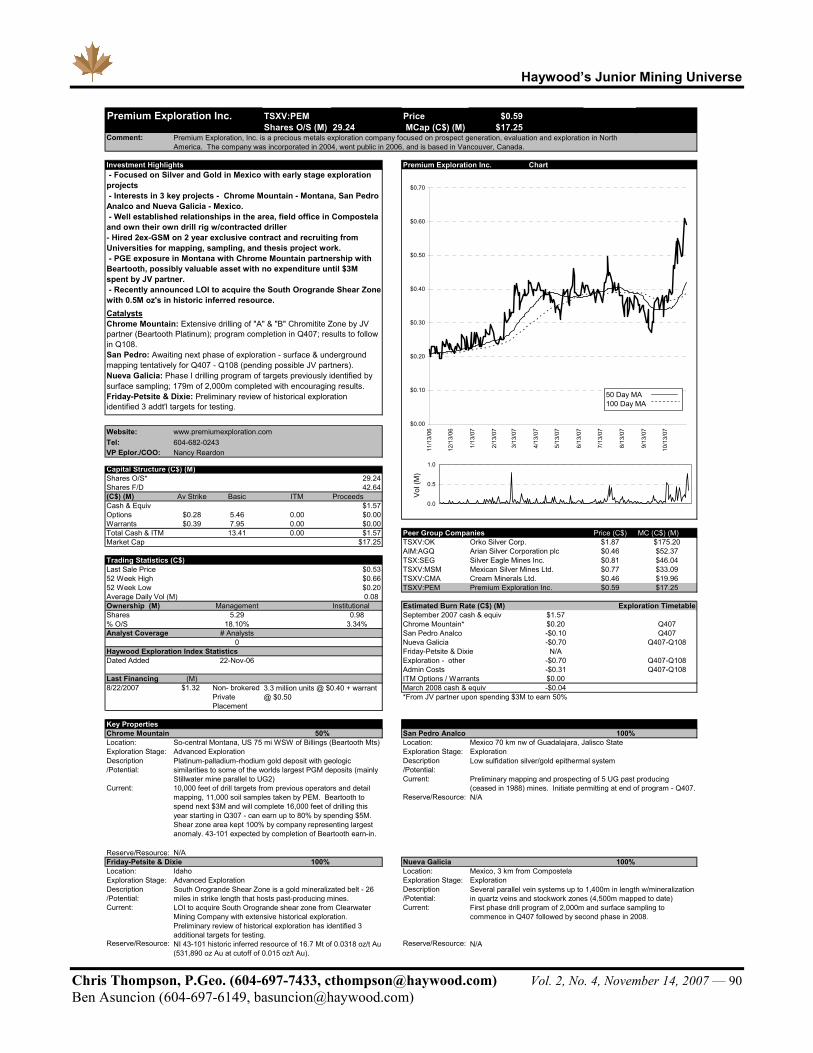

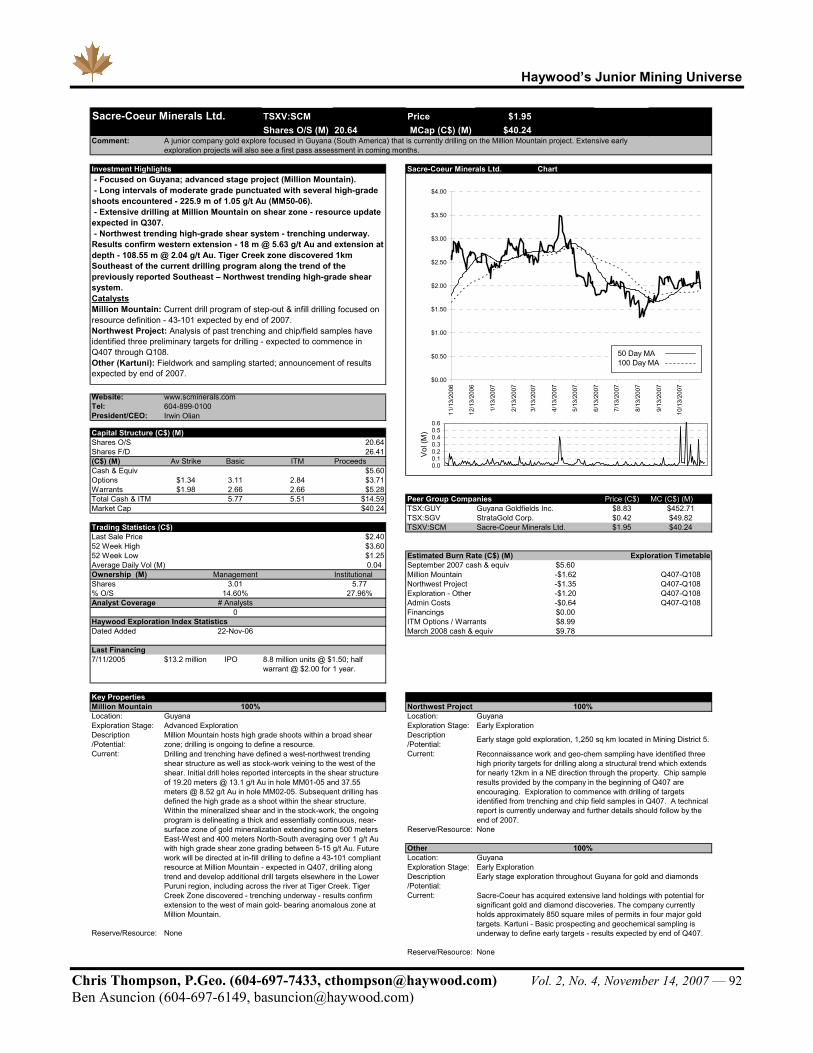

Precious metals-focused companies performed poorly overall, with only two companies posting positive returns, namely Mexican-focused precious metals explorers Premium Exploration (TSXV:PEM) and Orko Silver (TSXV:OK) with gains of 9% and 6% respectively. Ecuadorian gold/silver explorer Coastport Capital (TSXV:CPP) lagged its peers with a 17% decline.

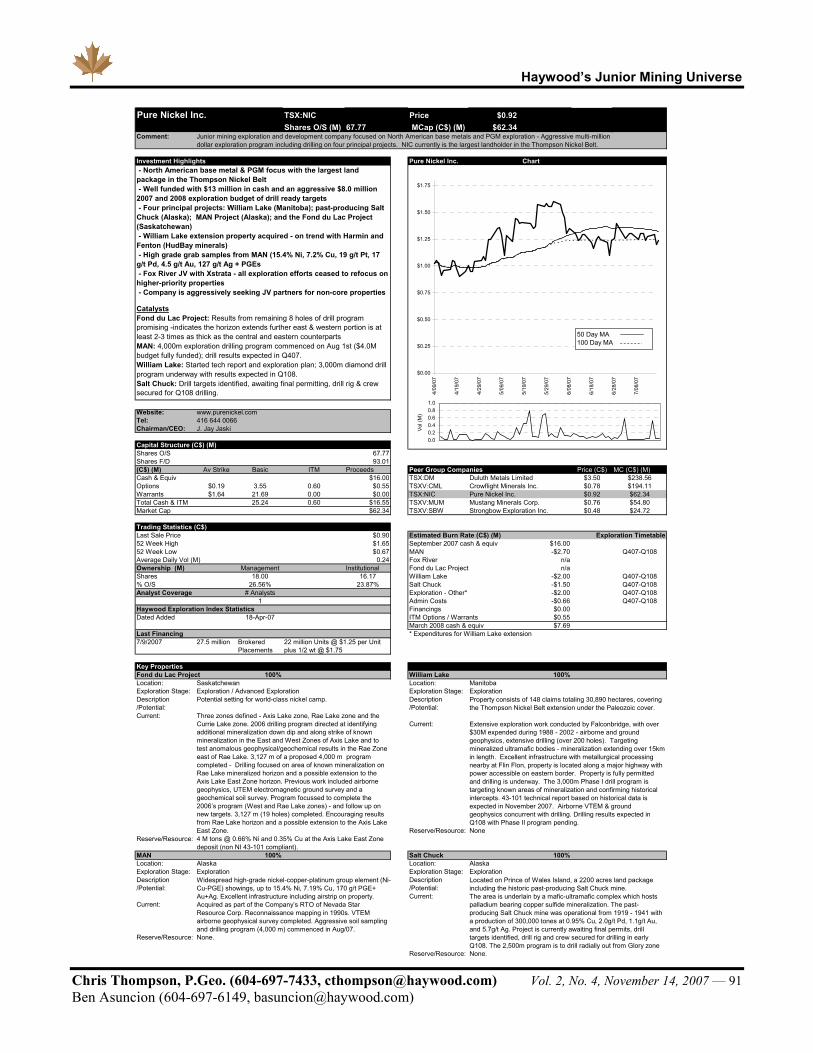

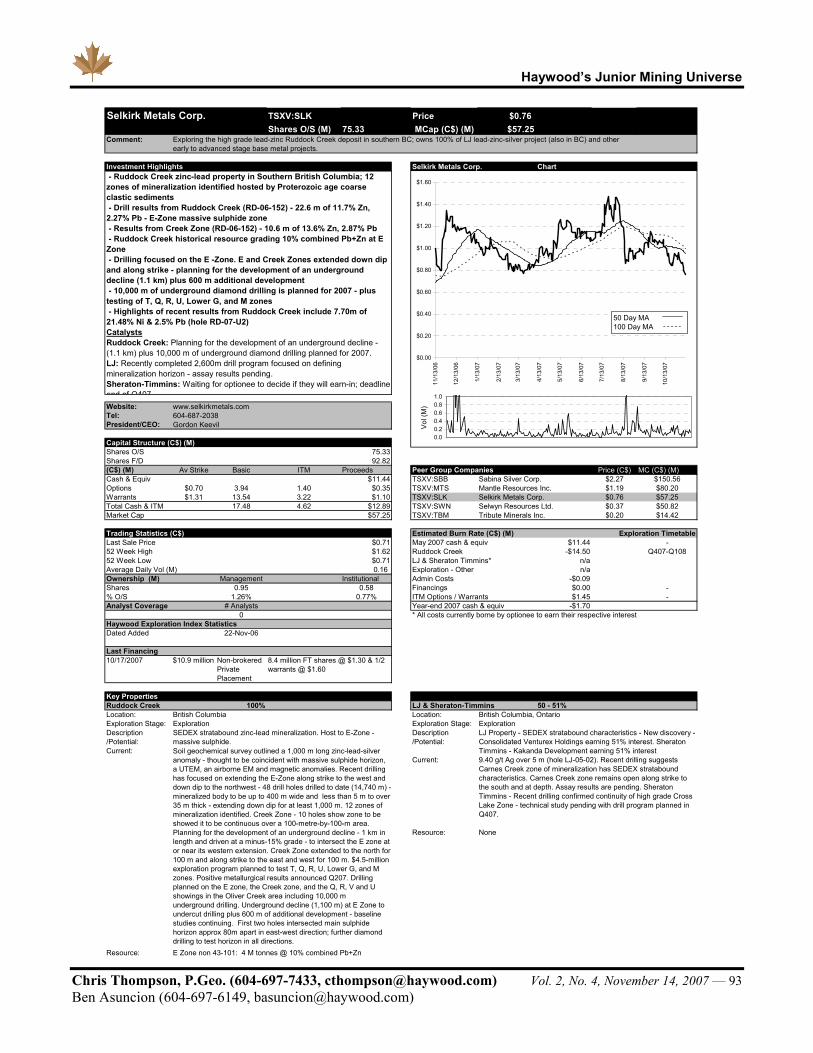

Pure base metals-focused companies faired no better, with all companies posting double-digit percentage losses. Canadian-focused Selkirk Metals (TSXV:SLK) bore the brunt of the decline, receiving a 17% haircut, followed by Pure Nickel (TSX:NIC), with a loss of $0.18 per share, or 16%.

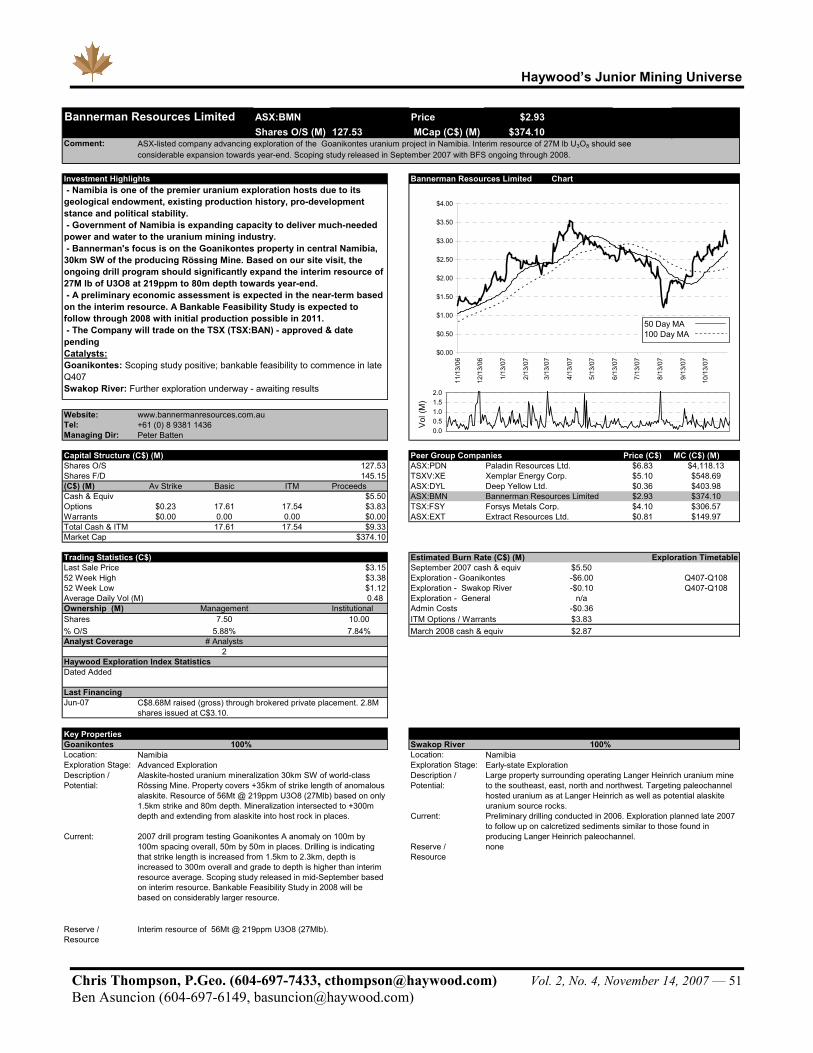

The performance of uranium-focused companies was solid, with Namibian-focused Xemplar Energy Corp (TSXV:XE) and Canadian-focused Forum Uranium (TSXV:FDC) recording gains of 26% and 19% respectively. Other solid performers include Crosshair Exploration & Mining (TSXV:CXX) and Australian Bannerman Resources (ASX:BMN) with gains of 8% and 3% respectively.

This period saw a relatively poor performance for the junior diamond explorers, with Canadian-focused explorers Diamondex Resources (TSXV:DSP) and Hudson Resources (TSXV:HUD) recording the only positive performances within the subsector of 10% and 1% respectively.

HJEI Stock Performance (29 Oct 2007 - 12 Nov 2007)

-40% -20% 0% 20% 40%

TSX-V:XE

TSX-V:FDC

TSX-V:DSP

TSX-V:PEM

TSX-V:CXX

TSX-V:OK

ASX:BM N

TSX-V:HUD

ASX:EXT

TSX-V:M IO

TSX-V:XRC

TSX-V:DDN

TSX-V:BHV

TSX-V:M EX

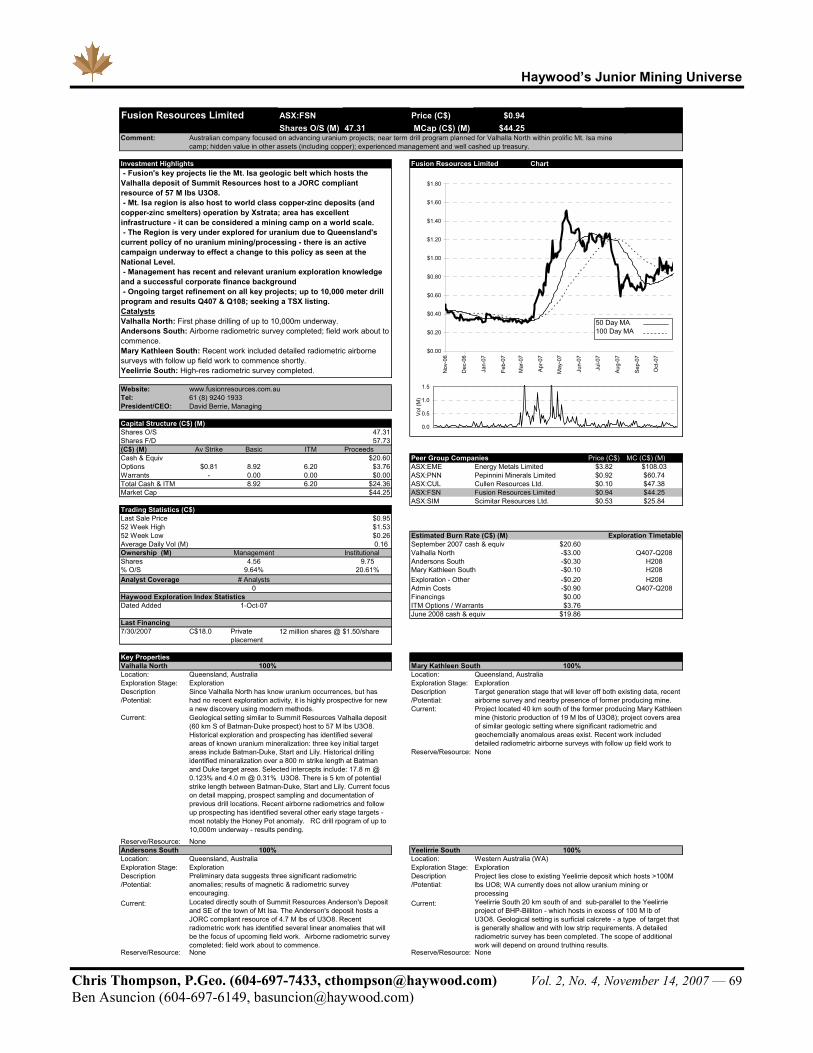

ASX:FSN

TSX-V:SCM

TSX-V:XAU

TSX-V:AZX

TSX-V:AZX

TSX-V:HAT

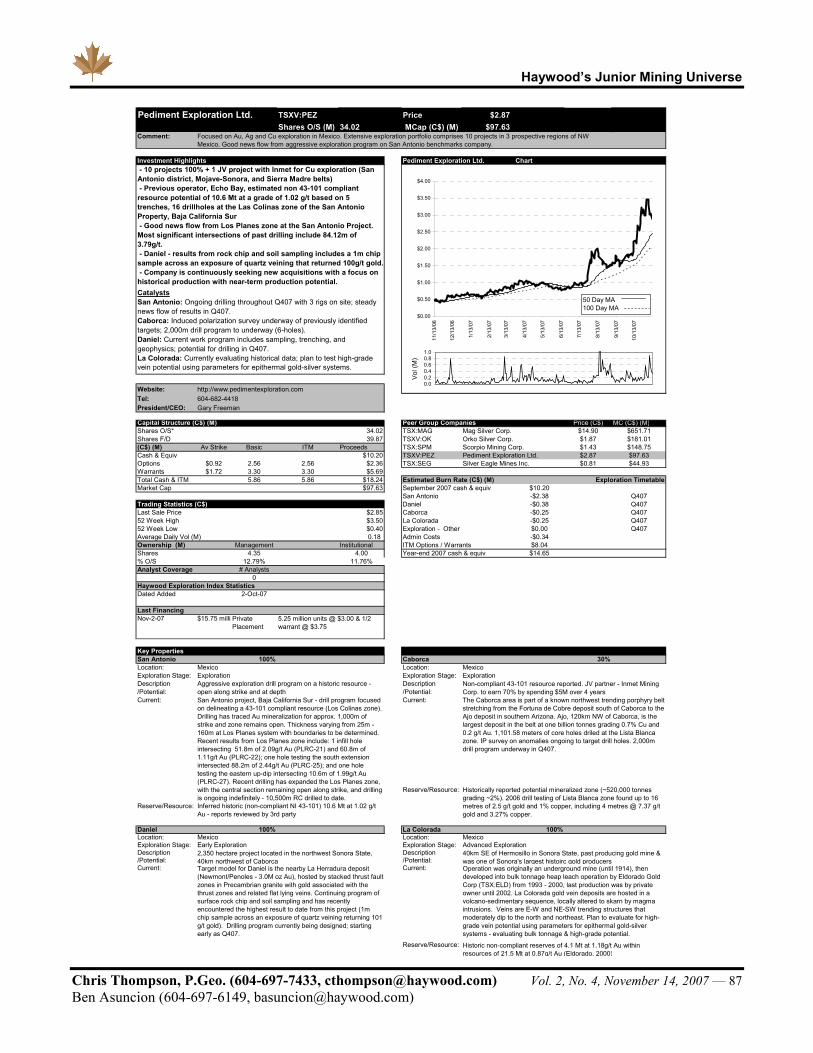

TSX-V:PEZ

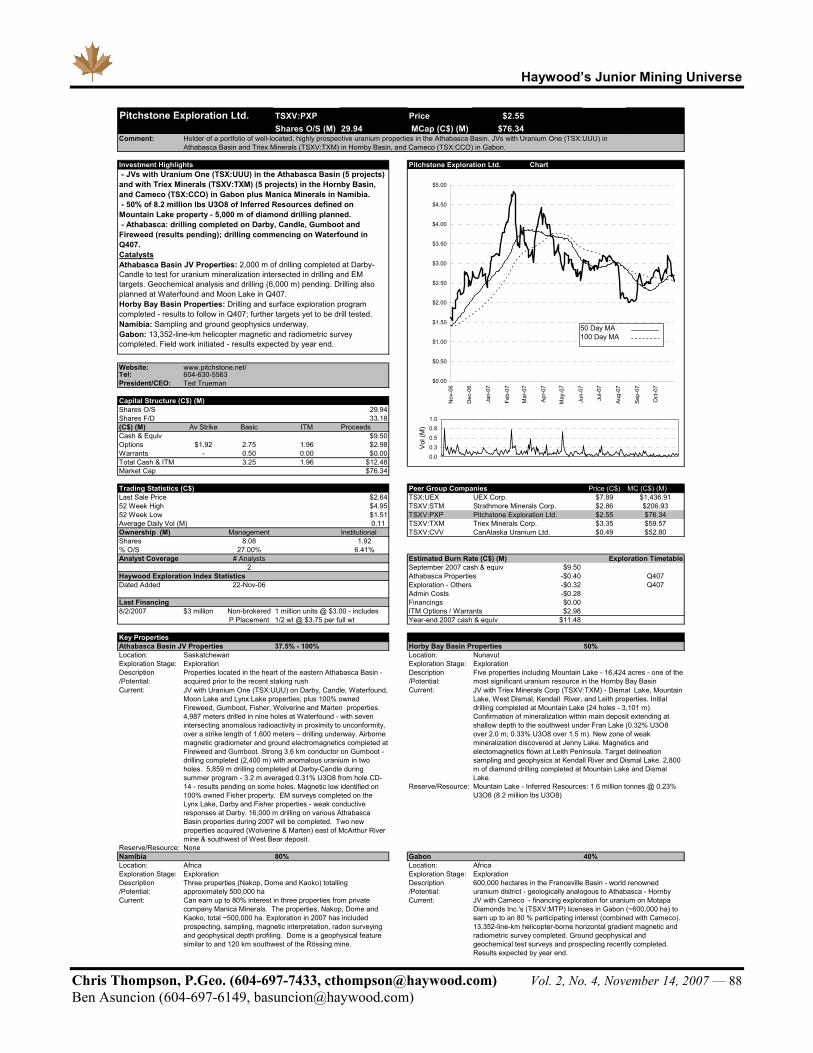

TSX-V:PXP

ASX:TGS

TSX-V:SRM

TSX-V:IM E

TSX:NIC

TSX-V:SLK

TSX-V:CPP

TSX:SWY

TSXV:CXB

HJEI Performance

0

200

400

600

800

1000

1200

Jan-

05

Apr-

05

Jul-0

5

Oct

-05

Feb-

06

May

-06

Aug-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

HJE

I Per

form

ance

(Bas

e:10

0)

HJEI Performance

800

810

820

830

840

850

860

870

880

890

29-O

ct

30-O

ct

31-O

ct

1-N

ov

2-N

ov

3-N

ov

4-N

ov

5-N

ov

6-N

ov

7-N

ov

8-N

ov

9-N

ov

10-N

ov

11-N

ov

12-N

ov

HJE

I Per

form

ance

(Bas

e:10

0 )

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 14 Ben Asuncion (604-697-6149, [email protected])

HJEI Companies – Performance: October 29 to November 12, 2007 Company Ticker Com m odity Focus Area Focus 10/29/2007 11/12/2007 %

Xemplar Energy Corp. TSX-V:XE Uranium Namibia 4.10$ 5.17$ 26%Forum Uranium Corp. TSX-V:FDC Uranium Canada 0.43$ 0.51$ 19%Diamondex Resources Ltd. TSX-V:DSP Diamond NW Territories, A lberta, Saskatchew an, Nunavut 0.31$ 0.34$ 10%Premium Exploration Inc. TSX-V:PEM Precious Metals USA, Mexico 0.54$ 0.59$ 9%Crosshair Exploration & Mining Corp. TSX-V:CXX Uranium, Gold New foundland, Labrador 2.27$ 2.46$ 8%Orko Silver Corp. TSX-V:OK Precious Metals Mexico 1.70$ 1.81$ 6%Bannerman Resources Limited ASX:BMN Uranium Namibia, Botsw ana, Australia 2.85$ 2.93$ 3%Hudson Resources Inc. TSX-V:HUD Diamond Greenland 0.67$ 0.68$ 1%Extract Resources Ltd. ASX:EXT Uranium Namibia 0.85$ 0.85$ 0%Mindoro Resources Ltd. TSX-V:MIO Precious, Base Metals Philippines 0.65$ 0.65$ 0%Exeter Resource Corp. TSX-V:XRC Precious, Base Metals Argentina, Chile 4.25$ 4.22$ -1%Diamonds North Resources Ltd. TSX-V:DDN Diamond NW Territories, Nunavut 0.85$ 0.84$ -1%Bellhaven Copper & Gold Inc. TSX-V:BHV Precious Metals Panama 0.89$ 0.87$ -2%Midlands Minerals Corporation TSX-V:MEX Precious Metals Ghana, Tanzania 0.31$ 0.30$ -3%Fusion Resources Limited ASX:FSN Uranium Australia 0.97$ 0.94$ -3%Sacre-Coeur Minerals Ltd. TSX-V:SCM Diamonds, Precious South America 2.03$ 1.95$ -4%AuEx Ventures Inc. TSX-V:XAU Precious Metals Nevada 2.60$ 2.48$ -5%Alexandria Minerals Corporation TSX-V:AZX Precious Metals Quebec 0.30$ 0.29$ -5%Alexandria Minerals Corporation TSX-V:AZX Precious Metals Quebec 0.30$ 0.29$ -5%Hathor Exploration Ltd. TSX-V:HAT Uranium Saskatchew an, British Columbia 0.83$ 0.76$ -8%Pediment Exploration Ltd. TSX-V:PEZ Precious Metals Mexico 3.16$ 2.87$ -9%Pitchstone Exploration Ltd. TSX-V:PXP Uranium Canada, Gabon 2.84$ 2.55$ -10%Tiger Resources Ltd. ASX:TGS Base Metals DRC 0.38$ 0.33$ -12%Shear Minerals Ltd. TSX-V:SRM Diamond Nunavut, NW Territories 0.59$ 0.50$ -15%Indicator Minerals Inc. TSX-V:IME Diamond Nunavut 0.26$ 0.22$ -15%Pure Nickel Inc. TSX:NIC Base Metals Canada, USA 1.10$ 0.92$ -16%Selkirk Metals Corp. TSX-V:SLK Base Metals British Columbia, Ontario 0.92$ 0.76$ -17%Coastport Capital, Inc. TSX-V:CPP Precious Metals Ecuador 0.32$ 0.26$ -17%Stornow ay Diamond Corp. TSX:SWY Diamond Quebec,Ontario, Nunavut, A lberta, Botsw ana 0.89$ 0.73$ -18%Calibre Mining Corp. TSXV:CXB Precious Metals Australia, New foundland 0.47$ 0.38$ -20%

Highlights

Xemplar Energy Corp. (TSXV:XE) ($5.17: +26%: M Cap $556.0M) Xemplar had another exemplary 2-week period ending November 12, 2007, with a gain of 26%. Xemplar has embarked on a multi-rig drill program on the wholly owned Warmbad property. The market is up dramatically on speculation that surface uranium mineralization in alaskites will extend to depth. Samples taken to date are out for assay.

Xemplar provided an update on exploration of the wholly owned Warmbad uranium project in south-central Namibia last week. The Company is targeting alaskite-hosted uranium mineralization similar to that found at the Rössing mine and nearby Valencia, Goanikontes, and Husab projects in a separate mineralized intrusive cluster to the north.

Xemplar has found more than 14 alaskite bodies outcropping in an area 40 kilometres by 28 kilometres. Three reverse circulation (RC) drill holes have been completed, and one diamond drill hole is progressing, all on the Big Yellow target body. All samples are out for assay in Johannesburg, but geologists have seen indications of uranium mineralization and will likely have scanned the core and chips with a scintillometer at minimum. Two

Xemplar Energy Corp. Chart

Price $5.17 $11.0MMarket Cap $556.0M $06.5MQ407-Q308 Burn Rate

Cash

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

11/1

3/06

12/1

3/06

1/13

/07

2/13

/07

3/13

/07

4/13

/07

5/13

/07

6/13

/07

7/13

/07

8/13

/07

9/13

/07

10/1

3/07

0.0

5.0

10.0

1

Vol

(M)

50 Day MA100 Day MA

Haywood’s Junior Mining Universe

Chris Thompson, P.Geo. (604-697-7433, [email protected]) Vol. 2, No. 4, November 14, 2007 — 15 Ben Asuncion (604-697-6149, [email protected])

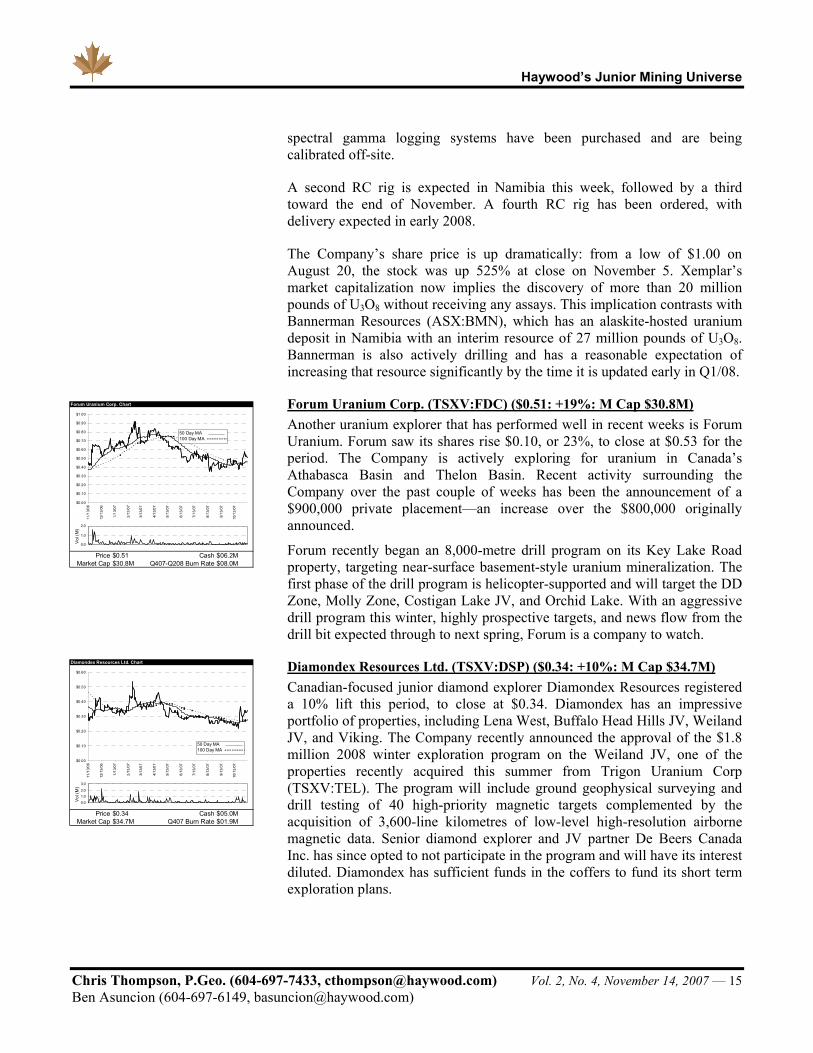

spectral gamma logging systems have been purchased and are being calibrated off-site.

A second RC rig is expected in Namibia this week, followed by a third toward the end of November. A fourth RC rig has been ordered, with delivery expected in early 2008.

The Company’s share price is up dramatically: from a low of $1.00 on August 20, the stock was up 525% at close on November 5. Xemplar’s market capitalization now implies the discovery of more than 20 million pounds of U3O8 without receiving any assays. This implication contrasts with Bannerman Resources (ASX:BMN), which has an alaskite-hosted uranium deposit in Namibia with an interim resource of 27 million pounds of U3O8. Bannerman is also actively drilling and has a reasonable expectation of increasing that resource significantly by the time it is updated early in Q1/08.

Forum Uranium Corp. (TSXV:FDC) ($0.51: +19%: M Cap $30.8M) Another uranium explorer that has performed well in recent weeks is Forum Uranium. Forum saw its shares rise $0.10, or 23%, to close at $0.53 for the period. The Company is actively exploring for uranium in Canada’s Athabasca Basin and Thelon Basin. Recent activity surrounding the Company over the past couple of weeks has been the announcement of a $900,000 private placement—an increase over the $800,000 originally announced.

Forum recently began an 8,000-metre drill program on its Key Lake Road property, targeting near-surface basement-style uranium mineralization. The first phase of the drill program is helicopter-supported and will target the DD Zone, Molly Zone, Costigan Lake JV, and Orchid Lake. With an aggressive drill program this winter, highly prospective targets, and news flow from the drill bit expected through to next spring, Forum is a company to watch.

Diamondex Resources Ltd. (TSXV:DSP) ($0.34: +10%: M Cap $34.7M) Canadian-focused junior diamond explorer Diamondex Resources registered a 10% lift this period, to close at $0.34. Diamondex has an impressive portfolio of properties, including Lena West, Buffalo Head Hills JV, Weiland JV, and Viking. The Company recently announced the approval of the $1.8 million 2008 winter exploration program on the Weiland JV, one of the properties recently acquired this summer from Trigon Uranium Corp (TSXV:TEL). The program will include ground geophysical surveying and drill testing of 40 high-priority magnetic targets complemented by the acquisition of 3,600-line kilometres of low-level high-resolution airborne magnetic data. Senior diamond explorer and JV partner De Beers Canada Inc. has since opted to not participate in the program and will have its interest diluted. Diamondex has sufficient funds in the coffers to fund its short term exploration plans.

Forum Uranium Corp. Chart

Price $0.51 $06.2MMarket Cap $30.8M $08.0MQ407-Q208 Burn Rate

Cash

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

11/1

3/06

12/1

3/06

1/13

/07

2/13

/07

3/13

/07

4/13

/07

5/13

/07

6/13

/07

7/13

/07

8/13

/07

9/13

/07

10/1

3/07

0.0

1.0

2.0

1

Vol

(M)

50 Day MA100 Day MA

Diamondex Resources Ltd. Chart

Price $0.34 $05.0MMarket Cap $34.7M $01.9MQ407 Burn Rate