head office level 37, 680 george street sydney nsw 2000 … · 2016-11-01 · 1 head office level...

TRANSCRIPT

1

Head Office Level 37, 680 George Street Sydney NSW 2000 Australia www.saiglobal.com SAI Global Limited ABN 67 050 611 642

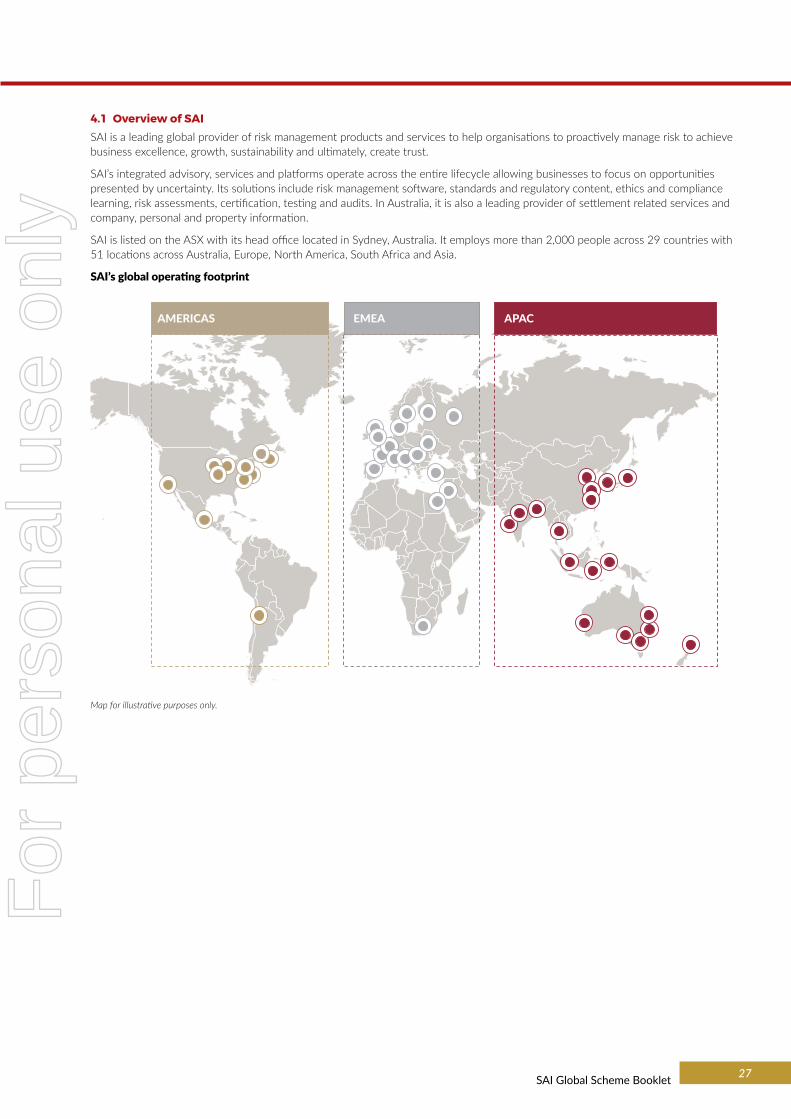

ASX ANNOUNCEMENT 1 November 2016 SAI GLOBAL/ BARING ASIA PRIVATE EQUITY FUND VI: SCHEME BOOKLET REGISTERED WITH ASIC 1 November 2016, Sydney, Australia: Further to the Company’s announcement on 26 September 2016, SAI Global Limited (SAI) today announced that the Australian Securities and Investments Commission (ASIC) has registered the scheme booklet (Scheme Booklet) in relation to the proposed acquisition of all of the shares in SAI by Casmar (Australia) Pty Limited (ACN 615 021 479), a wholly-owned subsidiary of the Baring Asia Private Equity Fund VI (Baring Asia), via a Scheme of Arrangement (the Scheme). This follows the issuance of orders by the Federal Court of Australia (the Court) today approving despatch of the Scheme Booklet to SAI shareholders and the convening of a meeting of SAI shareholders to consider and vote on the Scheme (Scheme Meeting), which was announced by SAI earlier today. Further, the Independent Expert appointed by the Board of Directors of SAI in relation to the Scheme, KPMG Corporate Finance, has concluded that the Scheme is in the best interests of SAI shareholders. A copy of the Scheme Booklet, including the Notice convening the Scheme Meeting and the Independent Expert's Report, is attached to this announcement. A copy of the Scheme Booklet, including the notice convening the Scheme Meeting and the Independent Expert's Report, will be sent to SAI shareholders on Friday, 4 November 2016. Those SAI shareholders who have previously elected to receive notifications from SAI’s share registry in electronic format, will also receive an email where they can download the Scheme Booklet and lodge their proxy votes online. If the Scheme is approved by SAI shareholders at the Scheme Meeting, and all other conditions precedent are satisfied or waived (where capable of waiver), SAI shareholders will receive a cash payment of AUD$4.75 per SAI share held on the Record Date in respect of the Scheme (Scheme Consideration). The Scheme Consideration is expected to be paid on Friday, 23 December 2016, being the expected Implementation Date in respect of the Scheme. The Board of Directors of SAI continues to unanimously recommend that SAI shareholders vote in favour of the Scheme at the upcoming Scheme Meeting, in the absence of a superior proposal. END Investor inquiries Dan Janes Managing Director Credit Suisse +61 2 8205 4166

Tim McKessar Director Credit Suisse +61 2 8205 4707

For

per

sona

l use

onl

y

2

Media inquiries John Frey GRACosway +61 411 361 361

For more information please visit www.saiglobal.com. About SAI Global SAI is a leading global provider of risk management products and services to businesses worldwide to proactively manage risk to achieve business excellence, growth, sustainability and ultimately, create trust. SAI’s integrated advisory, services and platforms operate across the entire lifecycle allowing businesses to focus on opportunities presented by uncertainty. Its solutions include risk management software, standards and regulatory content, ethics and compliance learning, risk assessments, certification, testing and audits. In Australia, it is also a leading provider of settlement related services; company, personal and property information. SAI is listed on the ASX with its head office located in Sydney, Australia. The company employs more than 2,000 people across 29 countries and 51 locations across Europe, North America and Asia. For more information, please visit www.saiglobal.com. About Baring Private Equity Asia Baring Private Equity Asia is one of the largest and most established independent alternative asset management firms in Asia, advising funds with total committed capital of over US$10 billion. The firm runs a pan-Asian investment program, sponsoring buyouts and providing growth capital to companies for expansion or acquisitions, as well as a private credit and a pan-Asian real estate private equity investment program. The firm has been investing in Asia since its formation in 1997 and has over 140 employees located across offices in Hong Kong, China, India, Japan and Singapore. Baring Private Equity Asia advised funds currently have over 35 portfolio companies active across Asia with a total of 150,000 employees and sales of approximately US$31 billion in 2015. For more information, please visit www.bpeasia.com.

For

per

sona

l use

onl

y

vote yes

Scheme Booklet This is an important document and requires your immediate attention. You should read this document carefully and in its entirety before deciding whether or not to vote in favour of the resolution to approve the Scheme. If you are in doubt as to what you should do, you should consult your legal, financial or other professional adviser.

If, after reading this Scheme Booklet, you have any questions about the Scheme or the number of SAI Shares you hold or how to vote, please call the Shareholder Information Line on 1300 654 848 (within Australia) or +61 1300 654 848 (outside Australia) Monday to Friday between 7.00am and 7.30pm (Sydney time).

If you have recently sold all of your SAI Shares, please disregard this document.

Financial Adviser

Legal Adviser

For a scheme of arrangement in relation to the proposed acquisition by BPEA BidCo of all SAI Shares held by Scheme Shareholders for $4.75 cash per SAI Share

Your Directors unanimously recommend that you approve the Scheme by voting in favour of the Scheme Resolution, in the absence of a superior proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of SAI Shareholders

SAI Global Limited ACN 050 611 642

For

per

sona

l use

onl

y

Important notices 2

Chairman’s Letter 4

Purpose of this Scheme Booklet 6

Next steps 7

Key dates 7

How to vote 8

Frequently asked questions 9

1 Summary of the Scheme 14

2 Key considerations relevant to your vote 16

3 Implementation of the Scheme 20

4 Information on SAI 26

5 Information on BPEA BidCo and Baring Private Equity Asia Group 35

6 What if the Scheme is not implemented? 41

7 Taxation implications for Scheme Shareholders 46

8 Additional information 49

9 Glossary 53

Attachment A Notice of Scheme Meeting 58

Attachment B Scheme Implementation Deed 61

Attachment C Scheme of Arrangement made under section 411 of the Corporations Act 123

Attachment D Deed Poll 139

Attachment E Independent Expert’s Report 148

Attachment F Sample Proxy Form 243

For

per

sona

l use

onl

y

1SAI Global Scheme Booklet

For

per

sona

l use

onl

y

2

SCHEME BOOKLET

ImportantNoticesDefined termsCapitalised terms used in this Scheme Booklet are defined in the Glossary in Section 9 of this Scheme Booklet.

This Scheme BookletThis Scheme Booklet includes the explanatory statement required to be sent to SAI Shareholders in relation to the Scheme under Part 5.1 of the Corporations Act. A copy of the proposed Scheme is set out in Attachment C to this Scheme Booklet.

You should read this Scheme Booklet carefully and in its entirety before making a decision as to how to vote on the resolution to be considered at the Scheme Meeting. If you are in doubt as to what you should do, you should consult your legal, financial or other professional adviser.

Responsibility for information(a) Except as provided in paragraphs (b)

to (d) below, the information in this Scheme Booklet has been provided by SAI and is the responsibility of SAI. Baring Private Equity Asia Group and their directors, officers and advisers do not assume any responsibility for the accuracy or completeness of any such SAI information.

(b) Baring Private Equity Asia Group has provided and is responsible for the Baring Private Equity Asia Group Information. SAI and its directors, officers and advisers do not assume any responsibility for the accuracy or completeness of the Baring Private Equity Asia Group Information.

(c) Ernst & Young has provided and is responsible for the information contained in Section 7 of this Scheme Booklet. Neither SAI nor the Baring Private Equity Asia Group assumes any responsibility for the accuracy or completeness of the information contained in Section 7 of this Scheme Booklet. Ernst & Young does not assume any responsibility for the accuracy or completeness of the information contained in this Scheme Booklet other than that contained in Section 7.

(d) The Independent Expert, KPMG Corporate Finance, has provided and is responsible for the information

contained in Attachment E to this Scheme Booklet. SAI does not assume any responsibility for the accuracy or completeness of the information contained in Attachment E to this Scheme Booklet except in relation to information given by it to the Independent Expert. The Baring Private Equity Asia Group does not assume any responsibility for the accuracy or completeness of the information contained in Attachment E to this Scheme Booklet. The Independent Expert does not assume any responsibility for the accuracy or completeness of the information contained in this Scheme Booklet other than that contained in Attachment E.

Link has had no involvement in the preparation of any part of this Scheme Booklet other than being named as SAI’s Share Registry. Link has not authorised or caused the issue of, and expressly disclaims and takes no responsibility for, any part of this Scheme Booklet.

Investment decisions The information in this Scheme Booklet does not constitute financial product advice. This Scheme Booklet has been prepared without reference to the investment objectives, financial situation or particular needs of any SAI Shareholder or any other person. This Scheme Booklet should not be relied on as the sole basis for any investment decision. Independent legal, financial and taxation advice should be sought before making any investment decision in relation to your SAI Shares.

ASIC and ASX involvementThis document is the explanatory statement for the scheme of arrangement between SAI and the holders of SAI Shares as at the Record Date for the purposes of section 412(1) of the Corporations Act. A copy of the proposed Scheme is included in this Scheme Booklet as Attachment C.

A copy of this Scheme Booklet (including the Independent Expert’s Report) has been lodged with and registered for the purposes of section 412(6) of the Corporations Act by ASIC. ASIC has been requested to provide a statement in accordance with section 411(17)(b) of the Corporations Act that ASIC has no objection to the Scheme.

If ASIC provides that statement, then it will be produced to the Court on the Court Approval Date.

Neither ASIC nor any of its officers take any responsibility for the contents of this Scheme Booklet.

A copy of this Scheme Booklet will be lodged with ASX. Neither ASX nor any of its officers take any responsibility for the contents of this Scheme Booklet.

Important notice associated with Court order under subsection 411(1) of the Corporations ActThe fact that under subsection 411(1) of the Corporations Act the Court has ordered that a meeting be convened and has approved the explanatory statement required to accompany the notice of the meeting does not mean that the Court:(a) has formed any view as to the merits

of the proposed Scheme or as to how members should vote (on this matter members must reach their own decision); or

(b) has prepared, or is responsible for the content of, the explanatory statement.

Notice regarding Second Court Hearing and if an SAI Shareholder wishes to oppose the SchemeThe date of the Second Court Hearing to approve the Scheme is 9 December 2016. The hearing will be at 2:15pm (Sydney time) at the Federal Court of Australia at Law Courts Building, 184 Phillip Street, Sydney NSW 2000.

Each SAI Shareholder has the right to appear and be heard at the Second Court Hearing and if so advised, oppose the approval of the Scheme at the Second Court Hearing. If you wish to oppose in this manner, you must file and serve on SAI a notice of appearance, in the prescribed form, together with any affidavit on which you wish to rely at the hearing. The notice of appearance and affidavit must be served on SAI at its address for service at least one day before 9 December 2016. The address for service for SAI is:c/- SAI Global Limited 680 George St, Sydney NSW 2000 (Attention: Company Secretary) Email: [email protected]

For

per

sona

l use

onl

y

3SAI Global Scheme Booklet

Disclosure regarding forward-looking statementsThis Scheme Booklet contains both historical and forward-looking statements.

The forward-looking statements in this Scheme Booklet are not based on historical facts, but rather reflect the current views of SAI or, in relation to the Baring Private Equity Asia Group Information, Baring Private Equity Asia Group, held only as at the date of this Scheme Booklet concerning future results and events and generally may be identified by the use of forward-looking words or phrases such as “believe”, “aim”, “expect”, “anticipated”, “intending”, “foreseeing”, “likely”, “should”, “planned”, “may”, “estimated”, “potential”, or other similar words and phrases. Similarly, statements that describe SAI’s and Baring Private Equity Asia Group’s objectives, plans, goals or expectations are or may be forward-looking statements.

The statements in this Scheme Booklet about the impact that the Scheme may have on the results of SAI’s operations, and the advantages and disadvantages anticipated to result from the Scheme, are also forward-looking statements.

Any forward-looking statements included in the Baring Private Equity Asia Group Information have been made on reasonable grounds. Although Baring Private Equity Asia Group believes that the views reflected in any forward-looking statements included in the Baring Private Equity Asia Group Information have been made on a reasonable basis, no assurance can be given that such views will prove to have been correct.

Any other forward-looking statements included in this Scheme Booklet and made by SAI have been made on reasonable grounds. Although SAI believes that the views reflected in any forward-looking statements in this Scheme Booklet (other than the Baring Private Equity Asia Group Information, the information in Section 7 and the information in Attachment E) have been made on a reasonable basis, no assurance can be given that such views will prove to have been correct.

These forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors that may cause either SAI’s or Baring Private Equity Asia Group’s actual results, performance or achievements to differ materially from the anticipated results, performance or achievements expressed, projected or implied by these forward-looking statements. Deviations as to future results, performance and achievements are both normal and to be expected. SAI Shareholders should note that the historical financial performance of SAI is no

assurance of future financial performance of SAI (whether the Scheme is implemented or not). SAI Shareholders should review carefully all of the information included in this Scheme Booklet. The forward-looking statements included in this Scheme Booklet are made only as of the date of this Scheme Booklet. Neither SAI, nor BPEA BidCo nor their directors give any representation, assurance or guarantee to SAI Shareholders that any forward-looking statements will actually occur or be achieved. SAI Shareholders are cautioned not to place undue reliance on such forward-looking statements.

Subject to any continuing obligations under law or the ASX Listing Rules, SAI, BPEA BidCo and Baring Private Equity Asia Group do not give any undertaking to update or revise any forward-looking statements after the date of this Scheme Booklet to reflect any change in expectations in relation to those statements or any change in events, conditions or circumstances on which any such statement is based.

Privacy and personal informationSAI and Baring Private Equity Asia Group may collect personal information to implement the Scheme. The personal information may include the names, contact details and details of holdings of SAI Shareholders, plus contact details of individuals appointed by SAI Shareholders as proxies, corporate representatives or attorneys at the Scheme Meeting. The collection of some of this information is required or authorised by the Corporations Act.

Link advises that personal information it holds about you (including your name, address, date of birth and details of the financial assets) is collected by Link organisations to administer your investment. Personal information is held on the public register in accordance with Chapter 2C of the Corporations Act. Some or all of your personal information may be disclosed to contracted third parties, or related Link companies in Australia and overseas. Your information may also be disclosed to Australian government agencies, law enforcement agencies and regulators, or as required under other Australian law, contract, and court or tribunal order. For further details about our personal information handling practices, including how you may access and correct your personal information and raise privacy concerns, visit our website at www.linkmarketservices.com.au for a copy of the Link condensed privacy statement, or contact us by phone on +61 1800 502 355 (free call within Australia) 9.00am to 5.00pm (Sydney time) Monday to Friday (excluding public holidays) to request a copy of our complete privacy policy.

The information may be disclosed to print and mail service providers, and to SAI and Baring Private Equity Asia Group and their respective related bodies corporate and advisers to the extent necessary to effect the Scheme. If the information outlined above is not collected, SAI may be hindered in, or prevented from, conducting the Scheme Meeting or implementing the Scheme effectively or at all. SAI Shareholders who appoint an individual as their proxy, corporate representative or attorney to vote at the Scheme Meeting should inform that individual of the matters outlined above.

Notice to persons outside AustraliaThis Scheme Booklet and the Scheme are subject to Australian disclosure requirements, which may be different from the requirements applicable in other jurisdictions. The financial information included in this document is based on financial statements that have been prepared in accordance with Australian equivalents to International Financial Reporting Standards, which may differ from generally accepted accounting principles in other jurisdictions.

This Scheme Booklet and the Scheme do not in any way constitute an offer of securities in any place in which, or to any person to whom, it would not be lawful to make such an offer.

Effect of roundingA number of figures, amounts, percentages, estimates, calculations of value and fractions in this Scheme Booklet are subject to the effect of rounding. Accordingly, the actual calculation of these figures may differ from the figures set out in this Scheme Booklet.

Times and datesUnless otherwise stated, all times referred to in this Scheme Booklet are times in Sydney, Australia. All dates following the date of the Scheme Meeting are indicative only and are subject to the Court approval process and the satisfaction or, where applicable, waiver of the conditions precedent to the implementation of the Scheme (see Section 1.2 of this Scheme Booklet).

CurrencyThe financial amounts in this Scheme Booklet are expressed in Australian currency unless otherwise stated. A reference to $ and cents is to Australian currency, unless otherwise stated.

Date This Scheme Booklet is dated 1 November 2016.

For

per

sona

l use

onl

y

4

SCHEME BOOKLET

Chairman’sLetterDear SAI Shareholder,

On behalf of the SAI Board, I am pleased to provide you with this Scheme Booklet, which contains information for your consideration in relation to the proposed acquisition of SAI by BPEA BidCo.

On 26 September 2016, SAI announced that it had entered into a binding Scheme Implementation Deed with a subsidiary of the Baring Private Equity Asia Group, under which it is proposed that BPEA BidCo will acquire all of the shares in SAI by way of the Scheme1. The Scheme is subject to regulatory and shareholder approvals and other conditions precedent.

If the Scheme is approved and implemented, Scheme Shareholders will receive a cash payment of $4.75 per SAI Share.

Your directors believe that the Scheme provides an opportunity to realise certain cash proceeds at an attractive premium. The Scheme Consideration of $4.75 per SAI Share represents a:

• 32.3% premium to SAI’s closing share price of $3.59 on 23 September 2016, being the last trading day prior to the announcement of the Scheme on 26 September 2016;

• 35.0% premium to the 5-day VWAP of $3.52 to 23 September 2016;

• 35.5% premium to the 1-month VWAP of $3.51 to 23 September 2016;

• 34.0% premium to the 6-month VWAP of $3.54 to 23 September 2016; and

• 28.7% premium to the broker consensus target price of $3.69 prior to the announcement of the Scheme on 26 September 2016.2

The Scheme Consideration of $4.75 per SAI Shares implies a fully diluted market capitalisation for SAI of $1,079 million3 and an implied enterprise value of SAI of $1,237 million4.

Directors’ recommendation

Your directors unanimously recommend that SAI Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of SAI Shareholders.

Subject to those same qualifications, each of your directors intends to vote, or cause to be voted, all the SAI Shares held or controlled by them in favour of the Scheme at the Scheme Meeting.

In reaching this unanimous conclusion, your directors assessed the changing dynamics of the markets in which SAI operates and the uncertainties and risks that that SAI would face if it were to continue as an independent ASX-listed entity. Given these factors, your directors believe that the significant premium and limited conditions of BPEA BidCo’s cash offer presents a compelling opportunity to realise immediate and certain value for SAI Shareholders.

Further details regarding the SAI Directors’ unanimous recommendation is set out in Section 2.

Independent Expert

Your directors appointed KPMG Corporate Finance as the Independent Expert to assess the merits of the Scheme. The Independent Expert has concluded that the Scheme is in the best interests of SAI Shareholders, in the absence of a Superior Proposal.

The Independent Expert has assessed the full underlying value of SAI at between $4.31 and $4.90 per SAI Share. The Scheme Consideration of $4.75 per SAI Share is within this range.

A complete copy of the Independent Expert’s Report is included in Attachment E of this Scheme Booklet.

How to vote

Your vote is important. In order for the Scheme to be implemented, the Scheme Resolution must be approved by SAI Shareholders at the Scheme Meeting by the Requisite Majorities. The Scheme Meeting will be held at 10.00am (Sydney time) on Monday, 5 December 2016 at SMC Conference & Function Centre (Ionic Room), 66 Goulburn Street, Sydney.

For this reason, your directors encourage you to vote by attending the Scheme Meeting – if you are unable to attend the Scheme Meeting, the SAI Directors urge you to complete and return, in the enclosed reply paid envelope, the personalised proxy form that accompany this Scheme Booklet or lodge your proxy form online at Link’s website (www.linkmarketservices.com.au) in accordance with the instructions given there.

1. Baring Private Equity Asia Group has an economic exposure to 9.25 million SAI Shares representing approximately 4.3% of the SAI Shares on issue (as described in Section 5.6(a)).

2. The broker consensus target price of $3.69 prior to the announcement of the Scheme on 26 September 2016 has been calculated from 8 broker valuations dated between 18 August 2016 and 19 August 2016 being publicly available institutional broker target prices ranging from $3.45 to $3.95 known to SAI and published after SAI’s financial results for the financial year ending 30 June 2016.

3. Based on 227.1 million fully diluted shares on issue. Please refer to Section 4.5 for further detail on SAI’s issued securities.4. Implied fully diluted market capitalisation of $1,079 million plus net debt of $201 million and minority interests of $1.7 million as at 30 June 2016 less cash

proceeds from the exercise of SAI Options and SAI Performance Rights.

For

per

sona

l use

onl

y

5SAI Global Scheme Booklet

If you wish for the Scheme to proceed, it is important that you vote in favour of the Scheme.

Additional Information

Your directors encourage you to read this Scheme Booklet carefully and in its entirety, as it contains important information that will need to be considered before you vote on the Scheme Resolution. Your directors also encourage you to seek independent financial, legal and taxation advice before making any investment decision in relation to your SAI Shares.

If you require further information or have questions in relation to the Scheme or this Scheme Booklet, please contact the Shareholder Information Line on 1300 654 848 (within Australia) or +61 1300 654 848 (outside Australia) Monday to Friday between 7.00am and 7.30pm (Sydney time).

I would like to thank you for your ongoing support.

Yours sincerely,

Andrew DuttonChairmanSAI Global Limited

For

per

sona

l use

onl

y

Purpose of this Scheme Booklet

6

SCHEME BOOKLET

On 26 September 2016, the SAI Directors unanimously recommended that SAI Shareholders vote in favour of the Scheme under which BPEA BidCo would acquire all of the shares in SAI for $4.75 cash per SAI Share, in the absence of a Superior Proposal and subject to the Independent Expert concluding that the Scheme is in the best interests of SAI Shareholders.

Each SAI Director continues to recommend that SAI Shareholders vote in favour of the Scheme and intends to vote all SAI Shares that he or she controls in favour of the Scheme.

The purpose of this Scheme Booklet is to explain the terms of the proposed Scheme and provide you with information on the Scheme to assist you in your decision whether or not to vote in favour of the Scheme.

Voting will take place at the Scheme Meeting to be held at 10.00am on Monday, 5 December 2016 at SMC Conference & Function Centre (Ionic Room), 66 Goulburn Street, Sydney. You should read this Scheme Booklet in full before deciding how to vote. The Scheme has a number of advantages, disadvantages and risks, which may affect SAI Shareholders in different ways depending on their individual circumstances. SAI Shareholders should seek professional advice on their particular circumstances, as appropriate.

Reasons to vote in favour of the Scheme

✔ The SAI Directors unanimously recommend that SAI Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders

✔ The Independent Expert has concluded that the Scheme is in the best interests of SAI Shareholders, in the absence of a Superior Proposal

✔ The Scheme Consideration represents attractive value for SAI Shareholders

✔ SAI Shareholders will receive certain value of $4.75 cash per SAI Share for their investment in SAI

✔ SAI’s share price is likely to fall if the Scheme does not proceed and no Superior Proposal emerges

✔ No Superior Proposal has emerged since the announcement of the Scheme

✔ If the Scheme does not proceed, SAI Shareholders will continue to be exposed to risks associated with SAI’s business rather than realising certain value for their SAI Shares in a certain timeframe

✔ SAI Shareholders will not incur any stamp duty or brokerage charges if the Scheme proceeds

For more information about the reasons to vote in favour of the Scheme, please see Section 2.1 of this Scheme Booklet which SAI Shareholders should read carefully and in its entirety.

Reasons not to vote in favour of the Scheme

✘ You may disagree with the SAI Directors’ unanimous recommendation and the Independent Expert’s conclusion and believe that the Scheme is not in your best interests

✘ You may prefer to participate in the future financial performance of the SAI business

✘ You may wish to maintain your current investment profile

✘ The tax consequences of the Scheme may not suit your current financial position

✘ You may believe that there is potential for a Superior Proposal to be made in the foreseeable future

For more information about the reasons to vote against the Scheme, please see Section 2.2 of this Scheme Booklet which SAI Shareholders should read carefully and in its entirety.

For

per

sona

l use

onl

y

Key Dates

Nextsteps

7SAI Global Scheme Booklet

(a) Carefully read this Scheme BookletThis is an important document and you should read it carefully and in its entirety before making a decision on how to vote at the Scheme Meeting.

(b) Vote on the SchemeAs an SAI Shareholder, you are entitled to vote on whether the Scheme should proceed at the Scheme Meeting.

Please refer to the following pages of this Scheme Booklet for details on how to vote at the Scheme Meeting, including by proxy.

(c) Seek further informationIf you have any questions in relation to the Scheme or the number of SAI Shares you hold or how to vote, please call the Shareholder Information Line on 1300 654 848 (within Australia) or +61 1300 654 848 (outside Australia) Monday to Friday between 7.00am and 7.30pm (Sydney time).

If you have any doubts as to the actions you should take or you have further questions, please contact your legal, investment or other professional adviser.

(d) Why you should voteAs an SAI Shareholder, you have a say in whether BPEA BidCo will acquire all of the issued shares in SAI. This is your opportunity to play a role in deciding the future of SAI.

10.00am (Sydney time) on Saturday 3 December 2016

Scheme Meeting proxies – the last date and time by which proxy forms (including proxies lodged online), powers of attorney or certificates of appointment of body corporate representative for the Scheme Meeting must be received by the Registry

7.00pm (Sydney time) on Saturday 3 December 2016

Meeting Record Date – date and time for determining eligibility to vote at the Scheme Meeting

10:00am (Sydney time) on Monday 5 December 2016

Scheme Meeting

IF SAI SHAREHOLDERS APPROVE THE SCHEME AT THE SCHEME MEETING

Friday 9 December 2016

Second Court Date to approve the Scheme

Monday 12 December 2016

Effective Date – this is the date on which the Scheme comes into effect and is binding on SAI Shareholders. Court order lodged with ASIC and announced on the ASX.

SAI Shares will be suspended from trading at the close of trading on the ASX on the Effective Date. If the Scheme proceeds, this will be the last day that SAI Shares will trade on the ASX.

7.00pm on Monday 19 December 2016 (5th Business Day after Effective Date)

Record Date – all SAI Shareholders who hold SAI Shares on the Record Date will be entitled to receive the Scheme Consideration.

Friday 23 December 2016 (4th Business Day after the Scheme Record Date)

Implementation Date – all Scheme Shareholders will be sent the Scheme Consideration to which they are entitled on this date.

All dates following the date of the Scheme Meeting are indicative only and are subject to the Court approval process and the satisfaction or, where applicable, waiver of the conditions precedent to the implementation of the Scheme (see Section 1.2 of this Scheme Booklet). All dates and times, unless otherwise indicated, refer to the date and time in Sydney, Australia. Any changes to the above timetable will be announced to ASX and notified on SAI’s website at https://www.saiglobal.com/.

For

per

sona

l use

onl

y

Howto vote

8

SCHEME BOOKLET

Who is entitled to vote at the Scheme Meeting?If you are on the Register as an SAI Shareholder at 7.00pm (Sydney time) on Saturday 3 December 2016, then you will be entitled to attend and vote at the Scheme Meeting.

Joint HoldersIn the case of SAI Shares held by joint holders, only one of the joint holders is entitled to vote. If more than one shareholder votes in respect of jointly held SAI Shares, only the vote of the SAI Shareholder whose name appears first in the Register will be counted.

Your vote is importantIn order for the Scheme to be implemented, the Scheme Resolution must be approved by SAI Shareholders at the Scheme Meeting.

For this reason the SAI Directors unanimously recommend that you vote in favour of the Scheme Resolution in the absence of a Superior Proposal and subject to the Independent Expert continuing to conclude that the Scheme is in the best interests of SAI Shareholders.

If you are unable to attend the Scheme Meeting, the SAI Directors urge you to complete and return, in the enclosed reply paid envelope, the personalised proxy form that accompanies this Scheme Booklet or lodge your proxy form online at Link’s website (www.linkmarketservices.com.au) in accordance with the instructions given there.

Location and details of Scheme MeetingThe details of the Scheme Meeting are as follows:

Location: SMC Conference & Function Centre (Ionic Room), 66 Goulburn Street, Sydney

Date: Monday, 5 December 2016

Time: 10.00am (Sydney time)

Scheme MeetingA copy of the Notice of Scheme Meeting is set out in Attachment A to this Scheme Booklet.

Section 3.1(b) of this Scheme Booklet provides details of the Scheme Resolution and the voting majorities that are required for the Scheme Resolution.

Voting in person, by attorney or corporate representative If you wish to vote in person, you must attend the Scheme Meeting.

If you cannot attend the Scheme Meeting, you may vote by proxy by completing the proxy form accompanying this Scheme Booklet.

Attorneys who plan to attend the Scheme Meeting should bring with them the original or a certified copy of the power of attorney under which they have been authorised to attend and vote at the Scheme Meeting. Attorneys who plan to attend and vote at the Scheme Meeting must provide a copy of the power of attorney and any authority under which the power of attorney was signed to the Registry by no later than 10:00am (Sydney time) on Saturday 3 December 2016 and should bring with them the original or a certified copy of the power of attorney and authority under which they have been authorised to attend and vote at the Scheme Meeting.

Given the last date for lodgement of a power of attorney or authority falls on a Saturday, please ensure that any power of attorney or authority which you intend to post or deliver is received by close of business on Friday 2 December 2016. SAI will accept copies of your power of attorney or authority received before 10:00am (Sydney time) on Saturday 3 December 2016.

A body corporate which is an SAI Shareholder may appoint an individual to act as its corporate representative. The appointment must comply with the requirements of section 250D of the Corporations Act. The representative should bring to the Scheme Meeting evidence of his or her appointment, including any authority under which it is signed.

Voting by proxy If you wish to appoint a proxy to attend and vote at the Scheme Meeting on your behalf, please complete and sign the personalised proxy form accompanying this Scheme Booklet in accordance with the instructions set out on the proxy form or lodge your proxy vote online at Link’s website (www.linkmarketservices.com.au) in accordance with the instructions given there. You may complete the proxy form in favour of the Chairperson of the Scheme Meeting or appoint up to two proxies to attend and vote on your behalf at the Scheme Meeting.

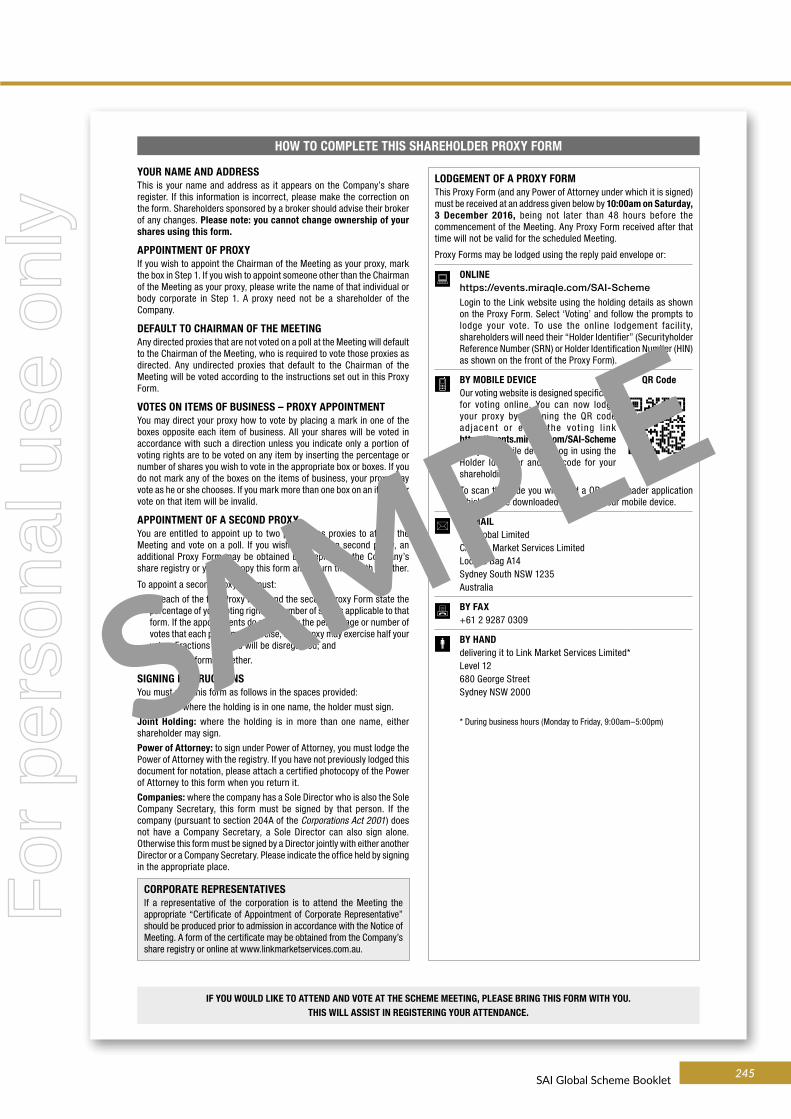

TO BE VALID, PROXY FORMS FOR THE SCHEME MEETING MUST BE RECEIVED BY THE REGISTRY BY NO LATER THAN 10.00AM (SYDNEY TIME) ON SATURDAY 3 DECEMBER 2016. Proxy forms, duly completed in accordance with the instructions set out on the proxy form, may be returned to the Registry:

• by posting them in the reply paid envelope provided;

• by delivering them to Link Market Services Limited at Level 12, 680 George Street, Sydney NSW 2000;

• by faxing them to +61 2 9287 0309;

• by posting them to SAI Global Limited C/- Link Market Services Limited, Locked Bag A14, Sydney South NSW 1235 Australia; or

• online: www.linkmarketservices.com.au

Login to the Link website using the details as shown on the proxy form. Select ‘Voting’ and follow the prompts to lodge your vote. To use the online voting facility, SAI Shareholders will need their “Holder Identifier” (Securityholder Reference Number (SRN) or Holder Identification Number (HIN) as shown on the front of the proxy form).

Given the last date for lodgement of proxy forms falls on a Saturday, please ensure that any proxy form which you intend to post or deliver is received by close of business on Friday 2 December 2016. SAI will accept proxies received by fax before 10:00am (Sydney time) on Saturday 3 December 2016.

For

per

sona

l use

onl

y

Frequentlyasked questions

9SAI Global Scheme Booklet

QUESTION ANSWER

AN OVERVIEW OF THE SCHEME

Why have I received this Scheme Booklet?

This Scheme Booklet has been sent to you because you are an SAI Shareholder and SAI Shareholders are being asked to vote on a Scheme which if approved will result in BPEA BidCo acquiring all SAI Shares for $4.75 cash per SAI Share.

This Scheme Booklet is intended to help you to decide how to vote on the Scheme Resolution which needs to be passed at the Scheme Meeting to allow the Scheme to proceed.

What is the Scheme? The Scheme is a scheme of arrangement between SAI and SAI Shareholders. A scheme of arrangement is a statutory procedure that is commonly used in transactions which may result in a change of ownership or control of a company.

On 26 September 2016, SAI and Baring Private Equity Asia Group announced the Scheme to ASX. If the Scheme is approved and implemented, Scheme Shareholders will receive $4.75 cash for each SAI Share they own.

Who are BPEA BidCo and the Baring Private Equity Asia Group?

BPEA BidCo is an Australian proprietary company limited by shares incorporated on 26 September 2016. It is a direct wholly owned subsidiary of Casmar Holdings (Australia) Pty Limited (ACN 615 020 409) which is an Australian proprietary company limited by shares incorporated on 26 September 2016. Casmar Holdings (Australia) Pty Limited is a direct wholly owned subsidiary of Casmar Pte. Limited which is a Singaporean proprietary company limited by shares incorporated on 12 November 2015. Casmar Pte. Limited is a direct wholly owned subsidiary of Casmar Holdings Pte. Limited which is a Singaporean proprietary company limited by shares incorporated on 12 November 2015. Casmar Holdings Pte. Limited is ultimately owned by three limited partnerships which comprise BAPE Fund VI. The investment funds comprising BAPE Fund VI are advised by Baring Private Equity Asia Group Limited (together with its related advisory entities, Baring Private Equity Asia).

Baring Private Equity Asia Group is one of the largest and most established independent alternative asset management firms in Asia, advising funds with total committed capital of over US$10 billion.

For more information on BPEA BidCo and the Baring Private Equity Asia Group please see Section 5 of this Scheme Booklet.

How will the Scheme be implemented?

In order for the Scheme to be implemented, all conditions precedent under the Scheme Implementation Deed must be satisfied or waived (where applicable), including that the Scheme Resolution must be approved by SAI Shareholders at the Scheme Meeting and the Scheme must be approved by the Court.

Details of this Scheme Resolution and the majorities required to approve the resolution are set out in Section 3.1(b) of this Scheme Booklet.

What do the SAI Directors recommend?

The SAI Directors unanimously recommend that you vote in favour of the Scheme Resolution to approve the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to conclude that the Scheme is in the best interests of SAI Shareholders.

How are the SAI Directors intending to vote?

Each of the SAI Directors intends to vote, or cause to be voted, in favour of the Scheme in respect of all the SAI Shares they control, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of SAI Shareholders.For

per

sona

l use

onl

y

10

FREQUENTLY ASKED QUESTIONS CONTINUED

QUESTION ANSWER

What is the Independent Expert’s opinion of the Scheme?

The Independent Expert concluded that the Scheme is in the best interests of SAI Shareholders, in the absence of a Superior Proposal. The Independent Expert, in arriving at this opinion, assessed whether the Scheme was fair and reasonable to the SAI Shareholders.

The Independent Expert has estimated the full underlying value of SAI to be in the range of $4.31 to $4.90 per share.

The Independent Expert’s Report is included as Attachment E to this Scheme Booklet.

The SAI Directors recommend that you read the Independent Expert’s Report carefully and in its entirety.

Why you may consider voting in favour of the Scheme

Reasons why you may consider voting in favour of the Scheme include:

• The SAI Directors unanimously recommend that SAI Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders;

• The Independent Expert has concluded that the Scheme is in the best interests of SAI Shareholders, in the absence of a Superior Proposal;

• The Scheme Consideration represents attractive value for SAI Shareholders;

• SAI Shareholders will receive certain value of $4.75 cash per SAI Share for their investment in SAI;

• SAI’s share price is likely to fall if the Scheme does not proceed and no Superior Proposal emerges;

• No Superior Proposal has emerged since the announcement of the Scheme;

• If the Scheme does not proceed, SAI Shareholders will continue to be exposed to risks associated with SAI’s business rather than realising certain value for their SAI Shares in a certain timeframe; and

• SAI Shareholders will not incur any stamp duty or brokerage charges if the Scheme proceeds.

Why you may consider voting against the Scheme

Reasons why you may consider voting against the Scheme include:

• You may disagree with the SAI Directors’ unanimous recommendation and the Independent Expert’s conclusion and believe that the Scheme is not in your best interests;

• You may prefer to participate in the future financial performance of the SAI business;

• You may wish to maintain your current investment profile;

• the tax consequences of the Scheme may not suit your current financial position; and

• you may believe there is the potential for a Superior Proposal to be made in the foreseeable future.

What will happen if a Superior Proposal emerges?

If SAI receives a proposal from a third party, the following applies:

• If the proposal is a Notifiable Proposal (defined in Section 3.7(d) below), SAI must notify BPEA BidCo in writing as soon as practicable and in any event within 2 Business Days of the material terms of the Notifiable Proposal (including, if known, the price, conditions precedent, timetable and any break fee) and, subject to the Fiduciary Exception (defined in Section 3.7(b) below), the identity of the third party making the Notifiable Proposal;

• SAI must not enter into a binding agreement to implement a Competing Proposal unless it is a Superior Proposal and SAI has notified the above details (including the identity of the third party making the Competing Proposal) to BPEA BidCo;

• BPEA BidCo will be given 3 Business Days’ notice during which it can put forward a counter proposal; and

• If BPEA BidCo provides a counter proposal and the SAI Directors decide, acting in good faith, that the counter proposal is more favourable to SAI Shareholders than the proposal from the third party, then the parties must use their best endeavours to promptly agree any amendments to the Scheme Implementation Deed as are reasonably necessary to implement the counter proposal.

Details of these provisions (and other provisions) of the Scheme Implementation Deed are set out in Section 3.

Since the announcement of the Scheme on 26 September 2016 and up to the date of this Scheme Booklet, no Superior Proposal has emerged.

For

per

sona

l use

onl

y

11SAI Global Scheme Booklet

5. The broker consensus target price of $3.69 prior to the announcement of the Scheme on 26 September 2016 has been calculated from 8 broker valuations dated between 18 August 2016 and 19 August 2016 being publicly available institutional broker target prices ranging from $3.45 to $3.95 known to SAI and published after SAI’s financial results for the financial year ending 30 June 2016.

QUESTION ANSWER

Is there a break fee payable?

Under the Scheme Implementation Deed, SAI must pay to BPEA BidCo a break fee of $10,785,480 (exclusive of GST) if certain events occur, including where a third party makes or announces a proposal to acquire an economic interest in 50% or more by value of the business or property of the SAI Group or gain Control of SAI before 26 March 2017 (or the earlier termination of the Scheme Implementation Deed) and completes such a transaction within 9 months of the announcement, where any SAI Director publicly withdraws or adversely changes his or her recommendation or voting intention in respect of the Scheme, an SAI Prescribed Occurrence occurs, or if BPEA BidCo terminates the Scheme Implementation Deed because of a material breach of the Scheme Implementation Deed by SAI.

Details of these provisions (and other provisions) of the Scheme Implementation Deed are set out in Section 3.8.

What are the risks associated with an investment in SAI if the Scheme does not become Effective?

If the Scheme does not proceed, and no comparable proposal or Superior Proposal emerges, then the SAI share price may fall or trade at a price below the Scheme Consideration of $4.75 per SAI Share, at least in the near term.

In addition, if the Scheme does not become Effective and no Superior Proposal emerges, SAI Shareholders will continue to be subject to the specific risks associated with SAI’s business and other general risks.

Details of these risks are set out in Section 6.3.

AN OVERVIEW OF THE SCHEME CONSIDERATION

What is the Scheme Consideration?

Scheme Shareholders will receive cash consideration of $4.75 for each SAI Share they hold on the Record Date.

What is the premium of the Scheme Consideration to SAI’s Share price?

The Scheme Consideration of $4.75 cash per share represents a:

• 32.3% premium to SAI’s closing share price of $3.59 on 23 September 2016, being the last trading day prior to the announcement of the Scheme on 26 September 2016;

• 35.0% premium to the 5-day VWAP of $3.52 to 23 September 2016;

• 35.5% premium to the 1-month VWAP of $3.51 to 23 September 2016;

• 34.0% premium to the 6-month VWAP of $3.54 to 23 September 2016; and

• 28.7% premium to the broker consensus target price of $3.69 prior to the announcement of the Scheme on 26 September 2016.5

How is Baring Private Equity Asia Group funding the Scheme Consideration?

BPEA BidCo intends to fund the Scheme Consideration from committed funding through a combination of external debt and equity from certain other Baring Private Equity Asia Group members.

The total proceeds available to BPEA BidCo under these funding arrangements are in excess of the maximum amount that could be required to fund the Scheme Consideration.

For more information on Baring Private Equity Asia Group’s funding arrangements see Section 5.4 of this Scheme Booklet.

Who is entitled to participate in the Scheme?

Persons who hold SAI Shares on the Record Date (excluding Baring Private Equity Asia Group and its associates) will participate in the Scheme and, if the Scheme is approved and implemented, those persons will receive the Scheme Consideration of $4.75 cash in respect of each SAI Share held on the Record Date.

When will I receive the Scheme Consideration?

Provided the Scheme is approved and implemented, SAI Shareholders on the Register on the Record Date are expected to be sent the Scheme Consideration on the Implementation Date

What are the tax implications of the Scheme for you?

The tax implications for Scheme Shareholders if the Scheme is approved and implemented will depend on the specific taxation circumstances of each Scheme Shareholder.

General information about the likely Australian tax consequences of the Scheme is set out in Section 7 of this Scheme Booklet. You should not rely on those descriptions as advice for your own affairs.

For information about your individual financial or taxation circumstances please consult your financial, legal, taxation or other professional adviser.

For

per

sona

l use

onl

y

12

FREQUENTLY ASKED QUESTIONS CONTINUED

QUESTION ANSWER

Will I have to pay brokerage or stamp duty?

No, you will not have to pay brokerage or stamp duty if your SAI Shares are acquired under the Scheme.

Can I sell my SAI Shares now?

You can sell your SAI Shares on-market at any time before the close of trading on ASX on the Effective Date. However, if you do so you will receive the prevailing on-market price set at the time of sale which may not be the same price as the Scheme Consideration, and you may also be required to pay brokerage.

SCHEME, VOTING AND APPROVALS

Are there any conditions that must be satisfied or waived in order for the Scheme to be implemented?

Yes there are. The conditions which remain outstanding as at the date of this Scheme Booklet are:

• Court approval of the Scheme;

• the Scheme Resolution being passed by the Requisite Majorities (see Section 3.1(b) of this Scheme Booklet for further details) at the Scheme Meeting;

• no other orders or restraints being issued by any court or any Government Agency preventing the implementation of the Scheme are in place;

• BPEA BidCo receiving FIRB approval for the Scheme;

• no SAI Material Adverse Change or SAI Prescribed Occurrence occurs;

• no material breach of SAI’s representations and warranties occurs;

• the Independent Expert not publicly withdrawing, qualifying or changing its opinion that the Scheme is in the best interests of SAI Shareholders; and

• none of the Directors changing, qualify or withdrawing their recommendation of the Scheme or intention to vote, or cause to be voted, all the SAI Shares held or controlled by them in favour of the Scheme at the Scheme Meeting, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders.

The conditions of the Scheme are summarised in further detail in Section 1.2 of this Scheme Booklet.

SAI Shareholders should also be aware that the Scheme Implementation Deed may be terminated in certain circumstances (details of which are summarised in Section 3.6 of this Scheme Booklet). If the Scheme Implementation Deed is terminated, the Scheme will not proceed.

As at the date of this Scheme Booklet, the SAI Directors are not aware of any reason why these conditions should not be satisfied or waived.

What happens if these conditions are not satisfied or the Scheme Implementation Deed is terminated?

If the Scheme conditions are not satisfied or the Scheme Implementation Deed is terminated then the Scheme will not be implemented and, as set out in Section 6.1 of this Scheme Booklet:

• you will retain your SAI Shares and they will not be acquired by BPEA BidCo;

• you will not receive the proposed $4.75 per share Scheme Consideration;

• SAI will continue to operate as a stand-alone company listed on ASX; and

• if the Scheme does not proceed, and no comparable proposal or Superior Proposal emerges, then the SAI share price may fall or trade at a price below the Scheme Consideration of $4.75 per SAI Share, at least in the near term.

What happens if the Scheme is approved, all conditions are satisfied and it is implemented?

If the Scheme becomes Effective and you remain an SAI Shareholder as at the Record Date for the Scheme, all of your SAI Shares will be transferred to BPEA BidCo under the Scheme, and you will receive the Scheme Consideration of $4.75 cash for each SAI Share you hold on the Record Date.

Am I entitled to vote at the Scheme Meeting?

If you are registered as an SAI Shareholder on the Register at 7.00pm (Sydney time) on Saturday 3 December 2016, then you will be entitled to attend and vote at the Scheme Meeting.

Details of the Scheme Meeting and voting are on page 8.For

per

sona

l use

onl

y

13SAI Global Scheme Booklet

QUESTION ANSWER

How do I vote? Voting at the Scheme Meeting may be in person, by attorney, by proxy or, in the case of a corporation, by corporate representative. If you wish to vote in person, you must attend the Scheme Meeting.

If you cannot attend the Scheme Meeting, you may complete the enclosed personalised proxy form in accordance with the instructions or lodge your proxy form online at Link’s website (www.linkmarketservices.com.au) in accordance with the instructions given there. The deadline for lodging your proxy form for the Scheme Meeting is 10.00am (Sydney time) on Saturday 3 December 2016.

Given the last date for lodgement of proxy forms falls on a Saturday, please ensure that any proxy form which you intend to post or deliver is received by close of business on Friday 2 December 2016. SAI will accept proxies received by fax before 10:00am (Sydney time) on Saturday 3 December 2016.

Details of the Scheme Meeting and voting are on page 8.

When and where will the Scheme Meeting be held?

The Scheme Meeting will be held at 10.00am (Sydney time) on Monday, 5 December 2016 at SMC Conference & Function Centre (Ionic Room), 66 Goulburn Street, Sydney.

Is voting compulsory? Voting is not compulsory. However, the Scheme will only be successful if it is approved by the Requisite Majorities of SAI Shareholders so voting is important and SAI Directors encourage you to vote. If the Scheme is approved, you will be bound by the Scheme whether or not you voted and whether or not you voted in favour of it.

What vote is required to approve the Scheme?

For the Scheme to proceed, the Scheme Resolution must be passed by the following Requisite Majorities:

• a majority in number (more than 50%) of SAI Shareholders who vote on the Scheme Resolution (noting that the Court may waive this requirement); and

• at least 75% of the votes cast on the Scheme Resolution.

What happens if I do not vote or if I vote against the Scheme?

If you do not vote, or vote against the Scheme, the Scheme may not be approved at the Scheme Meeting by the Requisite Majorities of SAI Shareholders. If this occurs then the Scheme will not proceed, you will not receive the Scheme Consideration and you will remain an SAI Shareholder.

However, if the Scheme is approved by the Requisite Majorities and the Scheme is implemented, your SAI Shares will be transferred to BPEA BidCo under the Scheme and you will receive the Scheme Consideration for each SAI Share you hold on the Record Date whether or not you voted in favour of the Scheme

Can I keep my shares in SAI?

If the Scheme is implemented, your SAI Shares will be transferred to BPEA BidCo. This is so even if you did not vote at all or you voted against the Scheme Resolution at the Scheme Meeting.

When will the results of the Scheme Meeting be available?

The results of the Scheme Meeting will be available shortly after the conclusion of the Scheme Meeting and will be announced to the ASX once available. Even if the Scheme Resolution is passed at the Scheme Meeting by the Requisite Majorities, the Scheme will only proceed if Court approval of the Scheme is obtained and all of the other conditions precedent are satisfied or waived.

What do I do if I oppose the Scheme?

If you, as an SAI Shareholder, oppose the Scheme, you should:

• call the Shareholder Information Line on 1300 654 848 (within Australia) or +61 1300 654 848 (outside Australia) Monday to Friday between 7.00am and 7.30pm (Sydney time) and obtain further information;

• attend the Scheme Meeting either in person or by proxy and vote against the Scheme Resolution; and/or

• if shareholders pass the Scheme Resolution at the Scheme Meeting and you wish to appear and be heard at the Second Court Hearing and if so advised, oppose the approval of the Scheme at the Second Court Hearing, you must lodge a notice of intention to appear at the Second Court Hearing, attend the hearing and indicate opposition to the Scheme.

FURTHER INFORMATION

What if I want further information?

If you have any questions about the Scheme or you would like additional copies of this Scheme Booklet, please contact the Shareholder Information Line on 1300 654 848 (within Australia) or +61 1300 654 848 (outside Australia) Monday to Friday between 7.00am and 7.30pm (Sydney time).

For information about your individual financial or taxation circumstances please consult your financial, legal, taxation or other professional adviser.

For

per

sona

l use

onl

y

14

1Summary of the Scheme

For

per

sona

l use

onl

y

15SAI Global Scheme Booklet

1.1 Scheme

On 26 September 2016, the SAI Board recommended to SAI Shareholders a proposal which, if implemented, will deliver to Scheme Shareholders $4.75 cash for the acquisition of each SAI Share pursuant to the Scheme.

This Scheme Booklet outlines the proposal being put to SAI Shareholders in relation to the Scheme, pursuant to which BPEA BidCo will, subject to approval by SAI Shareholders and the Court, acquire all of the SAI Shares on issue for cash consideration of $4.75 per SAI Share.

1.2 Conditions precedent

The Scheme is subject to a number of conditions precedent. The following conditions precedent are outstanding as at the date of this Scheme Booklet: (a) (FIRB) BPEA BidCo has received FIRB approval for the Scheme.(b) (Court approval) The Court approves the Scheme in accordance with section 411(4)(b) of the Corporations Act.(c) (Shareholder approval) SAI Shareholders agree to the Scheme at the Scheme Meeting by the Requisite Majorities.(d) (No Restraints) Before and as at the Delivery Time:

(i) there is not in effect any temporary restraining order, preliminary or permanent injunction or other preliminary or final decision, order or decree issued by any court of competent jurisdiction or by any Government Agency, nor is there in effect any other legal restraint or prohibition; and

(ii) no action or investigation is announced or commenced by any Government Agency,

which restrains, prohibits, impedes or otherwise materially adversely impacts upon (or could reasonably be expected to restrain, prohibit or otherwise materially adversely impede or impact upon) the completion of the Scheme.

(e) (No SAI Material Adverse Change) No SAI Material Adverse Change occurs between the date of the Scheme Implementation Deed and the Delivery Time.

(f) (No SAI Prescribed Occurrence) No SAI Prescribed Occurrence occurs between the date of the Scheme Implementation Deed and the Delivery Time.

(g) (SAI representations and warranties) There has been no material breach of the representations and warranties given by SAI in the Scheme Implementation Deed.

(h) (Independent Expert) The Independent Expert not publicly withdrawing, qualifying or changing its opinion that the Scheme is in the best interests of SAI Shareholders at any time up to the Delivery Time.

(i) (Directors’ Recommendation) None of the Directors changing, qualifying or withdrawing their recommendation of the Scheme or intention to vote, or cause to be voted, all the SAI Shares held or controlled by them in favour of the Scheme at the Scheme Meeting, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders.

The conditions of the Scheme are set out in full in clause 3 of the Scheme Implementation Deed which is Attachment B to this Scheme Booklet.

1.3 Implementation of the Scheme

The Scheme is proposed to be undertaken pursuant to a Court approved scheme of arrangement. A scheme of arrangement is a legal arrangement that shareholders vote on and, if the Requisite Majorities of shareholders vote in favour of it and it is approved by the Court, it binds the company and all of its shareholders upon the Court orders approving the scheme of arrangement being lodged with ASIC. Approval of a scheme of arrangement requires a 50% majority of the number of shareholders voting (unless the Court orders otherwise) and a 75% majority of the total votes cast being in favour of the Scheme, as well as approval by the Court.

The Scheme will become binding on SAI and SAI Shareholders only if the conditions to the Scheme are satisfied or waived.

1.4 If the Scheme is approved

If the Scheme is approved and implemented and you remain an SAI Shareholder as at the Record Date for the Scheme, each of your SAI Shares will be acquired by BPEA BidCo for cash consideration of $4.75 per SAI Share.

For

per

sona

l use

onl

y

16

2Key considerations relevant to your vote

For

per

sona

l use

onl

y

17SAI Global Scheme Booklet

This Section sets out the reasons why the SAI Directors consider that you should vote in favour of the Scheme. The SAI Directors acknowledge that there are reasons to vote against the Scheme (see Section 2.2 titled “Reasons why you may vote against the Scheme”), however, they believe that the reasons to vote in favour of the Scheme significantly outweigh the reasons to vote against the Scheme.

2.1 Reasons to vote in favour of the Scheme

(a) The SAI Directors unanimously recommend that SAI Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders

The SAI Directors unanimously recommend that, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders, you vote in favour of the Scheme Resolution required to implement the Scheme at the Scheme Meeting.

In reaching their recommendation, your SAI Directors have assessed the Scheme having regard to the reasons to vote in favour of, or against, the Scheme, as set out in this Scheme Booklet.

In the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme is in the best interests of SAI Shareholders, each of the SAI Directors intends to vote all SAI Shares held or controlled by them in favour of the Scheme. The interests of SAI Directors are set out in Section 8.1.

(b) The Independent Expert has concluded that the Scheme is in the best interests of SAI Shareholders, in the absence of a Superior Proposal

SAI appointed KMPG Corporate Finance as the Independent Expert to prepare an Independent Expert’s Report providing an opinion on whether the Scheme is in the best interests of SAI Shareholders.

The Independent Expert has concluded that the Scheme is in the best interests of SAI Shareholders, in the absence of a Superior Proposal.

The basis for this conclusion is that the Scheme Consideration of $4.75 per SAI Share is within the valuation (as concluded by the Independent Expert) of $4.31 to $4.90 per SAI Share.

The Independent Expert has made a number of observations in relation to the Scheme, including:(i) the Scheme Consideration represents a substantial premium to the trading price of SAI Shares before the announcement of the

Scheme. Therefore, the Scheme represents the best opportunity for SAI Shareholders to realise a control value for their SAI Shares in the absence of a Superior Proposal;

(ii) the Scheme Consideration is in cash and allows Scheme Shareholders to immediately realise the value from the investment and provides certainty of the pre-tax amount they will receive;

(iii) no Superior Proposal has emerged since the announcement of the Scheme. Accordingly, the Scheme represents a clear opportunity for the SAI Shareholders to monetise their investment at a significant premium to the trading prices of SAI Shares before the Scheme was announced; and

(iv) in the absence of the Scheme or a Superior Proposal, the SAI Share price is likely to fall to levels which do not reflect a control premium.

The SAI Directors encourage you to read the Independent Expert’s Report in full. A copy of the Independent Expert’s Report which includes the reasons why the Independent Expert reached its conclusion is included in Attachment E.

(c) The Scheme Consideration represents attractive value for SAI ShareholdersThe Scheme Consideration of $4.75 cash per SAI Share, which will be paid to SAI Shareholders if the Scheme is implemented, represents a significant premium to SAI’s share price prior to announcement of the Scheme on 26 September 2016.

The Scheme Consideration of $4.75 cash per SAI Share represents a premium of:(i) 32.3% to SAI’s closing share price of $3.59 on 23 September 2016 being the last trading day prior to announcement of the Scheme;(ii) 35.0% to the 5-day volume weighted average price (VWAP) of $3.52 to 23 September 2016;(iii) 35.5% to the 1-month VWAP of $3.51 to 23 September 2016;(iv) 34.0% to the 6-month VWAP of $3.54 to 23 September 2016; and(v) 28.7% to the broker consensus target price of $3.69 prior to announcement of the Scheme.6

6. The broker consensus target price of $3.69 prior to the announcement of the Scheme on 26 September 2016 has been calculated from 8 broker valuations dated between 18 August 2016 and 19 August 2016 being publicly available institutional broker target prices ranging from $3.45 to $3.95 known to SAI and published after SAI’s financial results for the financial year ending 30 June 2016.

For

per

sona

l use

onl

y

18

2. KEY CONSIDERATIONS RELEVANT TO YOUR VOTE CONTINUED

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

BROKERCONSENSUS

6 MONTH VWAP TO 23 SEPTEMBER 2016

1 MONTH VWAP TO 23 SEPTEMBER 2016

5 DAY VWAP TO 23 SEPTEMBER 2016

LAST CLOSE 23 SEPTEMBER 2016

(A$

PER

SHA

RE)

Scheme Consideration $4.75

$3.59 $3.52 $3.51 $3.54 $3.69

32.3% 35.0% 35.5% 34.0% 28.7%

(d) SAI Shareholders will receive certain value of $4.75 cash per SAI Share for their investment in SAIThe offer from BPEA BidCo is a 100% cash offer.

More specifically, if the Scheme is implemented, Scheme Shareholders will receive $4.75 in cash for each SAI Share held by them at the Scheme Record Date (currently expected to be Monday 19 December 2016), to be paid on or about the Implementation Date, which is currently expected to be Friday 23 December 2016.

In contrast, if the Scheme does not proceed, the amount which SAI Shareholders will be able to realise for their investment in SAI Shares will be uncertain.

The Scheme removes this uncertainty for SAI Shareholders. For details of risks relating to remaining an SAI Shareholder, see Section 6.3.

(e) SAI’s share price is likely to fall if the Scheme does not proceed and no Superior Proposal emergesIf the Scheme is not implemented, and in the absence of a Superior Proposal, SAI Shares are likely to trade below the price at which they have traded since announcement of the Scheme on 26 September 2016.

In addition, the future trading price of SAI Shares will continue to be subject to market volatility compared to the certain value of $4.75 cash per SAI Share available under the Scheme.

The chart below shows SAI’s share price performance over the last three years to 27 October 2016, the last practicable trading day before the date of this Scheme Booklet.

SAI historical share price performance

$2.75

$3.00

$3.25

$3.50

$3.75

$4.00

$4.25

$4.50

$4.75

$5.00

$5.25

$5.50

OCT 13 APR 14 OCT 14 APR 15 OCT 15 APR 15 OCT 16

CLO

SIN

G P

RICE

(A$

PER

SAI S

HA

RE)

26 May 14PEP non-binding

indicative andconditional proposal

13 Oct 14SAI concludesstrategic review 26 Sep 16

Announcement of Scheme

Scheme Consideration $4.75

Source: IRESS7

The closing price of SAI Shares on the ASX on 23 September 2016, being the last trading day prior to announcement of the Scheme, was $3.59.

The closing price for SAI Shares on the ASX on 27 October 2016, the last practicable trading day before the date of this Scheme Booklet, was $4.66.

7. Market data as at 27 October 2016, being the last practicable date before the date of the Scheme Booklet.

For

per

sona

l use

onl

y

19SAI Global Scheme Booklet

During the three months ending 27 October 2016:(i) The highest recorded daily closing price for SAI Shares on the ASX was $4.70 on 28 September 2016; and(ii) The lowest recorded daily closing price for SAI Shares on the ASX was $3.30 on 11 August 2016.

(f) No Superior Proposal has emerged since the announcement of the SchemeSince the announcement of the Scheme Implementation Deed on 26 September 2016 and up to the date of this Scheme Booklet, no Superior Proposal has emerged.

Your SAI Directors have not become aware of any alternative proposal and have no basis for believing that a Superior Proposal will be received.

(g) If the Scheme does not proceed, SAI Shareholders will continue to be exposed to risks associated with SAI’s business rather than realising certain value for their SAI Shares in a certain timeframe

If the Scheme does not proceed, the amount which SAI Shareholders will be able to realise in terms of price and future dividends will necessarily be uncertain and subject to a number of risks outlined in Section 6.3.

Among other things, this will be subject to the performance of SAI’s business from time to time (in particular, the uncertainties associated with SAI’s outlook as described in Section 6.2), general economic conditions and the movements in the share market.

The Scheme removes these risks and uncertainties for SAI Shareholders and allows SAI Shareholders to exit their investment in SAI at a price that the SAI Directors consider compelling. If the Scheme is approved and implemented, these risks and uncertainties will be assumed by BPEA BidCo, as the sole shareholder of SAI following implementation of the Scheme.

(h) SAI Shareholders will not incur any stamp duty or brokerage charges if the Scheme proceedsSAI Shareholders will not incur any brokerage or stamp duty on the transfer of your SAI Shares to BPEA BidCo under the Scheme.

2.2 Reasons why you may vote against the Scheme

(a) You may disagree with the SAI Directors’ unanimous recommendation and the Independent Expert’s conclusion and believe that the Scheme is not in your best interests

You may disagree with recommendation of the SAI Directors, who have unanimously recommended that SAI Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal.

In addition, you may disagree with the conclusion of the Independent Expert, who has concluded that the Scheme is is in the best interests of SAI Shareholders, in the absence of a Superior Proposal.

(b) You may prefer to participate in the future financial performance of the SAI business If the Scheme is implemented you will no longer be an SAI Shareholder. This will mean that you will not participate in the future performance, potential upside or future prospects of SAI, including any benefits from being an SAI Shareholder. This will mean that SAI Shareholders will not retain any exposure to SAI’s assets or have the potential to share in the value that could be generated by SAI in the future. However, as with all investments in securities, there can be no guarantee as to future performance of SAI.

(c) You may wish to maintain your current investment profileYou may wish to maintain your investment in SAI in order to have an investment in a publicly listed company with the specific characteristics of SAI in terms of industry, operational profile, size, capital structure and potential dividend stream.

Implementation of the Scheme may result in a disadvantage to those who wish to maintain their investment profile. SAI Shareholders who wish to maintain their investment profile may find it difficult to find an investment with a similar profile to that of SAI and they may incur transaction costs undertaking any new investment.

(d) The tax consequences of the Scheme may not suit your current financial positionImplementation of the Scheme may trigger taxation consequences for SAI Shareholders. A taxable gain may be realised from the disposal of your SAI Shares.

SAI Shareholders should read the general taxation considerations outlined in Section 7 of this Scheme Booklet and seek professional taxation advice with respect to their individual tax situation.

(e) You may believe that there is potential for a Superior Proposal to be made in the foreseeable futureYou may believe that there is a potential for a Superior Proposal to be made in the foreseeable future.

Since the execution of the Scheme Implementation Deed on 26 September 2016 and as at the date of this Scheme Booklet, no Superior Proposal has emerged and the SAI Directors have no basis for believing that an alternative proposal will emerge.

The Scheme Implementation Deed prohibits SAI from soliciting a Competing Proposal. However, SAI is permitted to respond to any Competing Proposal should the SAI Directors determine that failing to do so would likely constitute a breach of their fiduciary or statutory duties. Further details of the key terms in the Scheme Implementation Deed are provided in Attachment B.

For

per

sona

l use

onl

y

20

3Implementation of the Scheme

For

per

sona

l use

onl

y

21SAI Global Scheme Booklet

3.1 Steps for implementing the Scheme

(a) Preliminary stepsSAI and BPEA BidCo entered into the Scheme Implementation Deed on 26 September 2016 pursuant to which, among other things, SAI agreed to propose the Scheme.

BPEA BidCo will execute the Deed Poll pursuant to which BPEA BidCo will, subject to the Scheme becoming Effective, agree to provide to each Scheme Shareholder the Scheme Consideration to which each Scheme Shareholder is entitled under the terms of the Scheme.

A copy of the proposed Scheme is set out in Attachment B to this Scheme Booklet.

A copy of the proposed Deed Poll is set out in Attachment D to this Scheme Booklet.

(b) Scheme MeetingThe Court has ordered that the Scheme Meeting be held at 10.00am (Sydney time) on Monday, 5 December 2016 at SMC Conference & Function Centre (Ionic Room), 66 Goulburn Street, Sydney for the purposes of approving the Scheme Resolution. The Notice of Scheme Meeting for SAI Shareholders which sets out the Scheme Resolution is included in Attachment A to this Scheme Booklet.

Each SAI Shareholder who is registered on the Register at 7.00pm (Sydney time) on Saturday, 3 December 2016 is entitled to attend and vote at the Scheme Meeting, either in person or by proxy or attorney or in the case of a body corporate, by its corporate representative appointed in accordance with section 250D of the Corporations Act.

Instructions on how to attend and vote at the Scheme Meeting in person, or to appoint a proxy to attend and vote on your behalf, are set out on page 8 of this Scheme Booklet.

The Scheme Resolution must be approved by:(i) a majority in number (more than 50%) of SAI Shareholders present and voting at the Scheme Meeting (whether in person, by proxy,

by attorney or, in the case of corporate SAI Shareholders, by a corporate representative) (the Headcount Test); and(ii) at least 75% of the total number of votes cast on the Scheme Resolution at the Scheme Meeting.

It should be noted that the Court has the power to waive the Headcount Test.

(c) Second Court hearingIn the event that:(i) the Scheme Resolution is approved by the Requisite Majorities of SAI Shareholders at the Scheme Meeting; and(ii) all conditions precedent of the Scheme have been satisfied or remain capable of being satisfied, or waived (if applicable),

SAI will apply to the Court for orders approving the Scheme. The Second Court Hearing is expected to be held on 9 December 2016.