headlines - microsoft...technically, the us 10-yr yield could eventually test key 2.3% support, the...

TRANSCRIPT

Wednesday, 05 April 2017

P. 1

Rates: Will FOMC Minutes give more info on the Fed’s balance sheet run-off?

FOMC Minutes could give more insight on ending the Fed’s reinvestment policy, resulting in a steeper US yield curve. Last week’s market reaction (bull steepening) showed that the front end of the curve is also sensitive to the debate as running off the BS is an alternative for hiking rates, according to NY Fed Dudley. We expect 2.3% yield support (US 10y) to hold.

Currencies: USD still looking for a driver. US yields remain key

The dollar still shows a mixed picture. USD/JPY came close to the recent low but no real test occurred as US yields held above key support levels. EUR/USD hovers sideways in the 1.06 big figure. Today, the focus is on the US ADP report and the services ISM. The dollar probably needs really strong data to succeed any sustained gains ahead of the payrolls.

Calendar

• US equities managed to overcome initial weakness and eventually closed

nearly unchanged in an uneventful trading session. Overnight, Asian stock markets trade mixed with China outperforming after a 2-day holiday.

• Activity in Japan's services sector expanded at the fastest pace in 19 months in March as outstanding business improved, allowing companies to charge more for their goods. The services PMI increased from 51.3 to 52.9.

• The cost of coal used in steel-making in China has shot up nearly 9% on expectations supply will be crimped in the wake of a cyclone that struck Australia’s north-east coast last week.

• Marine Le Pen repeatedly lost her cool during a heated French presidential debate. She was rated the fourth-most-convincing candidate in two snap polls, , while communist-backed Jean-Luc Melenchon came out on top.

• Richmond Fed Lacker unexpectedly stepped down after revealing his involvement in a 2012 leak of confidential information that sparked a criminal investigation, prompted outrage on Capitol Hill and embarrassed the Fed.

• North Korea launched a medium-range ballistic missile off the east coast of the Korean Peninsula this morning, a day before US President Trump meets with Chinese President Xi for the first time.

• Today’s eco calendar is interesting with services PMI/ISM’s in EMU (final), the UK and the US. Additionally, the US ADP employment report and FOMC Minutes of the March meeting will be released.

Headlines

S&PEurostoxx 50NikkeiOilCRB

Gold2 yr US10 yr US

2yr DE10 yr DEEUR/USDUSD/JPYEUR/GBP

Wednesday, 05 April 2017

P. 2

US Treasury rally stopped ahead of key yield support

Yesterday, German bonds continued initially their rally, albeit at a slower pace in a session with uneventful eco data or events. Equities traded with a small negative bias, which was reversed in the US session, oil moved substantially higher from noon onwards and peripheral spreads narrowed a tad. So, it is a long stretch to call it a risk-off session. US Treasuries tried to follow Bunds up at the US open, but were slapped back as US bond holders took profit on the rally when key technical yield support (especially) for the US 10-yr was approached. Uncertainty ahead of the Fed Minutes and especially Friday’s payrolls may have played a role too. The euro area retail sales printed stronger than expected, but were ignored. The US trade deficit narrowed more than expected in February and the factory orders were in line with expectations. The German bonds followed the US Treasuries lower in the US session, but managed to keep some daily gains In a daily perspective, the German yield curve bull flattened with yields 1.6 bp (2-yr) higher to 2.6 bps (30-yr) lower. The US yield curve bear steepened with yields 2.6 bps (2-yr) to 4.7 bps (30-yr) higher. In the EMU bond markets, 10-yr yield peripheral spreads were 1 (Spain) to 3/5 bps (Italy/Portugal) lower, with Greece the exception ( up 9 bps) on news stories that the review of the bailout package might not be concluded at the next Eurogroup meeting.

Interesting US eco calendar.

The EMU eco calendar contains only the final reading of the PMI services business confidence, which won’t bring surprises. In the US, the March ADP employment report will be closely looked at, as it is a pointer for the important payrolls report Friday. Following an outsized 298 000 gain in private jobs in February, consensus expects a trend-like 185 000 in March. The February result was affected by special factors like unseasonal warm weather, which resulted in sharp increases in the good-producing sectors. This will not be repeated in March and even some payback may occur. The US Markit employment index fell back in March, but the ISM manufacturing employment sub-index rose more than 4 points to 58.9. Initial claims rose modestly higher throughout the month. So, all in all the labour market remained healthy in March, but a slowing compared to the weather clement January-February outcomes look likely. We side with consensus. The March Non-manufacturing ISM is expected to have eased slightly to 57 from 57.6, still a high level. As the correlation with the manufacturing ISM is rather strong, we might indeed see some easing.

Rates

US yield -1d2 1,25 0,005 1,88 0,0210 2,35 0,0230 2,99 0,03

DE yield -1d2 -0,79 0,025 -0,45 -0,0110 0,26 -0,0230 1,05 -0,02

Bund rally slowed, while…

… profit taking on US Treasuries pushed yields back moderately higher

ADP report to show healthy labour market

Little impact expected

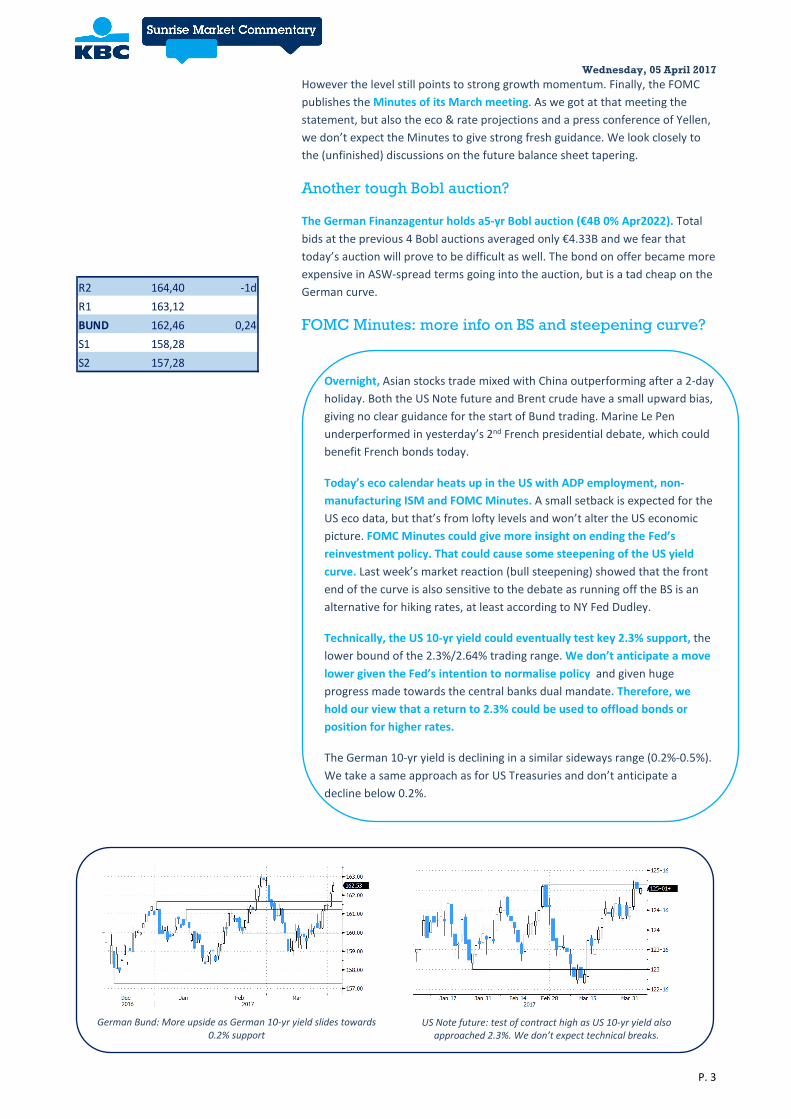

US T-Note future (black) and S&P future (orange): Profit taking T-Note future after 2017 high was tested .

Brent oil: Red alert is over as Brent moves away from €50/barrell on expectations of lower inventories and extension production cuts.

Wednesday, 05 April 2017

P. 3

However the level still points to strong growth momentum. Finally, the FOMC publishes the Minutes of its March meeting. As we got at that meeting the statement, but also the eco & rate projections and a press conference of Yellen, we don’t expect the Minutes to give strong fresh guidance. We look closely to the (unfinished) discussions on the future balance sheet tapering.

Another tough Bobl auction?

The German Finanzagentur holds a5-yr Bobl auction (€4B 0% Apr2022). Total bids at the previous 4 Bobl auctions averaged only €4.33B and we fear that today’s auction will prove to be difficult as well. The bond on offer became more expensive in ASW-spread terms going into the auction, but is a tad cheap on the German curve.

FOMC Minutes: more info on BS and steepening curve?

Overnight, Asian stocks trade mixed with China outperforming after a 2-day holiday. Both the US Note future and Brent crude have a small upward bias, giving no clear guidance for the start of Bund trading. Marine Le Pen underperformed in yesterday’s 2nd French presidential debate, which could benefit French bonds today.

Today’s eco calendar heats up in the US with ADP employment, non-manufacturing ISM and FOMC Minutes. A small setback is expected for the US eco data, but that’s from lofty levels and won’t alter the US economic picture. FOMC Minutes could give more insight on ending the Fed’s reinvestment policy. That could cause some steepening of the US yield curve. Last week’s market reaction (bull steepening) showed that the front end of the curve is also sensitive to the debate as running off the BS is an alternative for hiking rates, at least according to NY Fed Dudley.

Technically, the US 10-yr yield could eventually test key 2.3% support, the lower bound of the 2.3%/2.64% trading range. We don’t anticipate a move lower given the Fed’s intention to normalise policy and given huge progress made towards the central banks dual mandate. Therefore, we hold our view that a return to 2.3% could be used to offload bonds or position for higher rates.

The German 10-yr yield is declining in a similar sideways range (0.2%-0.5%). We take a same approach as for US Treasuries and don’t anticipate a decline below 0.2%.

R2 164,40 -1dR1 163,12BUND 162,46 0,24S1 158,28S2 157,28

German Bund: More upside as German 10-yr yield slides towards 0.2% support

US Note future: test of contract high as US 10-yr yield also approached 2.3%. We don’t expect technical breaks.

Wednesday, 05 April 2017

P. 4

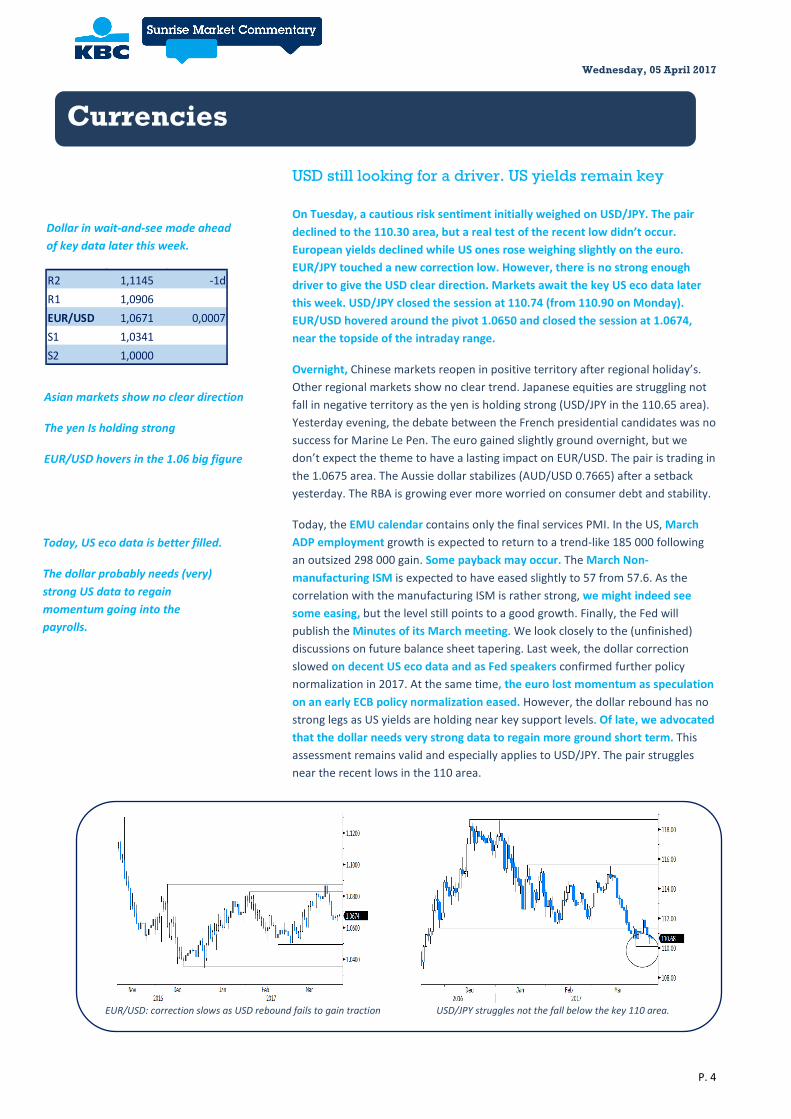

EUR/USD: correction slows as USD rebound fails to gain traction

USD/JPY struggles not the fall below the key 110 area.

USD still looking for a driver. US yields remain key

On Tuesday, a cautious risk sentiment initially weighed on USD/JPY. The pair declined to the 110.30 area, but a real test of the recent low didn’t occur. European yields declined while US ones rose weighing slightly on the euro. EUR/JPY touched a new correction low. However, there is no strong enough driver to give the USD clear direction. Markets await the key US eco data later this week. USD/JPY closed the session at 110.74 (from 110.90 on Monday). EUR/USD hovered around the pivot 1.0650 and closed the session at 1.0674, near the topside of the intraday range.

Overnight, Chinese markets reopen in positive territory after regional holiday’s. Other regional markets show no clear trend. Japanese equities are struggling not fall in negative territory as the yen is holding strong (USD/JPY in the 110.65 area). Yesterday evening, the debate between the French presidential candidates was no success for Marine Le Pen. The euro gained slightly ground overnight, but we don’t expect the theme to have a lasting impact on EUR/USD. The pair is trading in the 1.0675 area. The Aussie dollar stabilizes (AUD/USD 0.7665) after a setback yesterday. The RBA is growing ever more worried on consumer debt and stability.

Today, the EMU calendar contains only the final services PMI. In the US, March ADP employment growth is expected to return to a trend-like 185 000 following an outsized 298 000 gain. Some payback may occur. The March Non-manufacturing ISM is expected to have eased slightly to 57 from 57.6. As the correlation with the manufacturing ISM is rather strong, we might indeed see some easing, but the level still points to a good growth. Finally, the Fed will publish the Minutes of its March meeting. We look closely to the (unfinished) discussions on future balance sheet tapering. Last week, the dollar correction slowed on decent US eco data and as Fed speakers confirmed further policy normalization in 2017. At the same time, the euro lost momentum as speculation on an early ECB policy normalization eased. However, the dollar rebound has no strong legs as US yields are holding near key support levels. Of late, we advocated that the dollar needs very strong data to regain more ground short term. This assessment remains valid and especially applies to USD/JPY. The pair struggles near the recent lows in the 110 area.

Currencies

R2 1,1145 -1dR1 1,0906EUR/USD 1,0671 0,0007S1 1,0341S2 1,0000

Asian markets show no clear direction

The yen Is holding strong

EUR/USD hovers in the 1.06 big figure

Today, US eco data is better filled.

The dollar probably needs (very) strong US data to regain momentum going into the payrolls.

Dollar in wait-and-see mode ahead of key data later this week.

Wednesday, 05 April 2017

P. 5

We keep a close eye on US yields nearing key support levels. For EUR/USD, the repositioning away from early ECB normalization has been worked out. We maintain a cautious EUR/USD negative bias, but the decline is slowing. Big EUR/USD gains are unlikely if sentiment would become risk-off. From a technical point of view, USD/JPY last week failed to regain the 111.36/60 previous range bottom. A decline below 110 would signal more trouble ahead. EUR/USD extensively tested the topside of the MT range, but the test was rejected last week. The 1.0874/1.0906 area now looks a solid resistance. EUR/USD might return lower in the previous 1.0875/1.05 trading range.

Sterling corrects off the recent highs

Yesterday, sterling faced heavy selling at the onset of European trading which is a indication that the recent short squeeze has probably run its course. After the early morning repositioning sterling didn’t go anywhere. Cable hovered in the mid 1.24 big figure and closed the session at 1.2440. EUR/GBP traded close to, mostly slightly north of 0.8550 for most of the session. A late session up-tick of EUR/USD pushed EUR/GBP to close the session at 0.8580 (from 0.8545 on Monday evening).

Overnight, BRC shop prices declined -0.8% M/M (from -1.0%), in line with expectations. Sterling is holding near yesterday’s lows against the euro and the dollar. Later today, the UK services PMI is expected little changed at 53.4. In the past, this indicator had big market moving potential as services are the main driver for UK growth. This remains the case, but of late sterling was more sensitive to price data and, to a lesser extent, to Brexit headlines, rather than to activity data. Even so, we watch whether Brexit is having more impact on services activity. Mid-March, sterling found a better bid after higher than expected UK inflation and a more hawkish tone from the BoE. We changed our short-term bias on EUR/GBP from positive to neutral. The EUR/GBP 0.88/0.84 range should guide EUR/GBP trading medium term. Since late last week, the sterling rally/short-squeeze shows tentative signs of running into resistance, but we see no trigger for a real change in sentiment yet. Longer term, Brexit-complications remain a potential negative for sterling. We are not convinced that the BoE will raise rates anytime soon, even not after recent higher inflation data.

R2 0,8881 -1dR1 0,8854EUR/GBP 0,8577 0,0006S1 0,8403S2 0,8304

EUR/GBP rebounds as sterling short-squeeze is easing

GBP/USD: sterling rally slows even as USD is also losing momentum

Wednesday, 05 April 2017

P. 6

Wednesday, 5 April Consensus Previous US 14:15 ADP Employment Change (Mar) 185k 298k 15:45 Markit US Services PMI (Mar F) 53.1 52.9 16:00 ISM Non-Manf. Composite (Mar) 57.0 57.6 20:00 FOMC Meeting Minutes -- -- Japan 02:30 Nikkei Japan PMI Services (Mar) A 52.9 51.3 02:30 Nikkei Japan PMI Composite (Mar) A 52.9- 52.2 UK 01:01 BRC Shop Price Index YoY (Mar) A -0.8% -1.0% 10:00 New Car Registrations YoY (Mar) -- -0.3% 10:30 Markit/CIPS UK Services PMI (Mar) 53.4 53.3 10:30 Markit/CIPS UK Composite PMI (Mar) 53.8 53.8 10:30 Unit Labor Costs YoY (4Q) 2% 2.3% EMU 10:00 Markit Eurozone Services PMI (Mar F) 56.5 56.5 10:00 Markit Eurozone Composite PMI (Mar F) 56.7 56.7 Germany 09:55 Markit Germany Services PMI (Mar F) 55.6 55.6 09:55 Markit/BME Germany Composite PMI (Mar F) 57.0 57.0 France 09:50 Markit France Services PMI (Mar F) 58.5 58.5 09:50 Markit France Composite PMI (Mar F) 57.6 57.6 Italy 09:45 Markit/ADACI Italy Services PMI (Mar) 54.3 54.1 09:45 Markit/ADACI Italy Composite PMI (Mar) 54.9 54.8 Spain 09:15 Markit Spain Services PMI (Mar) 57.4 57.7 09:15 Markit Spain Composite PMI (Mar) 57 57.0 Sweden 08:30 Swedbank/Silf PMI Services (Mar) -- 59.8 09:30 Industrial Production MoM / NSA YoY (Feb) 1.0%/2.4% 2.0%/1.3% Events 11:30 Germany to Sell €4B 0% 2022 Bobl 14:30 BOE Gertjan Vlieghe speaks in London

Calendar

Wednesday, 05 April 2017

P. 7

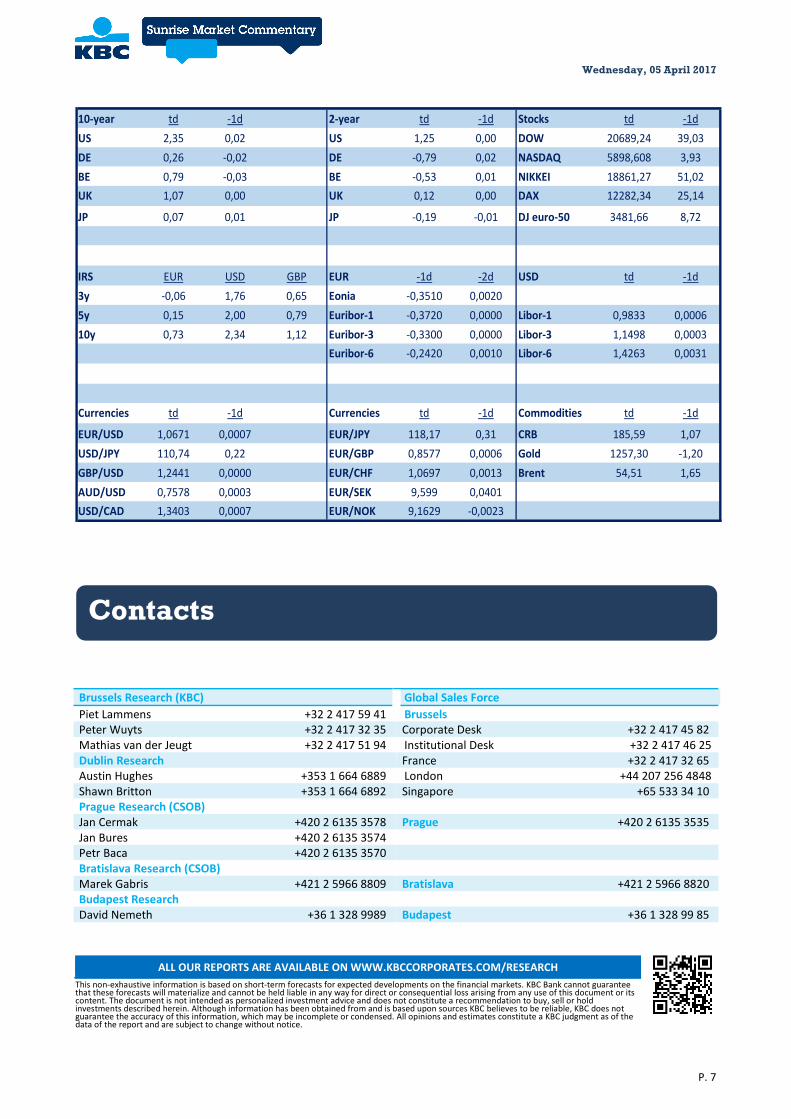

10-year td -1d 2-year td -1d Stocks td -1dUS 2,35 0,02 US 1,25 0,00 DOW 20689,24 39,03DE 0,26 -0,02 DE -0,79 0,02 NASDAQ 5898,608 3,93BE 0,79 -0,03 BE -0,53 0,01 NIKKEI 18861,27 51,02UK 1,07 0,00 UK 0,12 0,00 DAX 12282,34 25,14

JP 0,07 0,01 JP -0,19 -0,01 DJ euro-50 3481,66 8,72

IRS EUR USD GBP EUR -1d -2d USD td -1d3y -0,06 1,76 0,65 Eonia -0,3510 0,00205y 0,15 2,00 0,79 Euribor-1 -0,3720 0,0000 Libor-1 0,9833 0,000610y 0,73 2,34 1,12 Euribor-3 -0,3300 0,0000 Libor-3 1,1498 0,0003

Euribor-6 -0,2420 0,0010 Libor-6 1,4263 0,0031

Currencies td -1d Currencies td -1d Commodities td -1d

EUR/USD 1,0671 0,0007 EUR/JPY 118,17 0,31 CRB 185,59 1,07USD/JPY 110,74 0,22 EUR/GBP 0,8577 0,0006 Gold 1257,30 -1,20GBP/USD 1,2441 0,0000 EUR/CHF 1,0697 0,0013 Brent 54,51 1,65AUD/USD 0,7578 0,0003 EUR/SEK 9,599 0,0401USD/CAD 1,3403 0,0007 EUR/NOK 9,1629 -0,0023

Brussels Research (KBC) Global Sales Force Piet Lammens +32 2 417 59 41 Brussels Peter Wuyts +32 2 417 32 35 Corporate Desk +32 2 417 45 82 Mathias van der Jeugt +32 2 417 51 94 Institutional Desk +32 2 417 46 25 Dublin Research France +32 2 417 32 65 Austin Hughes +353 1 664 6889 London +44 207 256 4848 Shawn Britton +353 1 664 6892 Singapore +65 533 34 10 Prague Research (CSOB) Jan Cermak +420 2 6135 3578 Prague +420 2 6135 3535 Jan Bures +420 2 6135 3574 Petr Baca +420 2 6135 3570 Bratislava Research (CSOB) Marek Gabris +421 2 5966 8809 Bratislava +421 2 5966 8820 Budapest Research David Nemeth +36 1 328 9989 Budapest +36 1 328 99 85

ALL OUR REPORTS ARE AVAILABLE ON WWW.KBCCORPORATES.COM/RESEARCH This non exhaustive information is based on short term forecasts for expected developments

This non-exhaustive information is based on short-term forecasts for expected developments on the financial markets. KBC Bank cannot guarantee that these forecasts will materialize and cannot be held liable in any way for direct or consequential loss arising from any use of this document or its content. The document is not intended as personalized investment advice and does not constitute a recommendation to buy, sell or hold investments described herein. Although information has been obtained from and is based upon sources KBC believes to be reliable, KBC does not guarantee the accuracy of this information, which may be incomplete or condensed. All opinions and estimates constitute a KBC judgment as of the data of the report and are subject to change without notice.

Contacts