heavily incentivized evs start strong but face weak...

TRANSCRIPT

DRIVING GROWTH FOR THE REMARKETING PROFESSIONAL

GREENLIGHTISSUE 22

REDBUMPER’S NEW DEALER DIRECT PURCHASING PROGRAM P8

WILL BUYERS STAND BY SUBCOMPACTS IF FUEL PRICES DROP? P9

ELECTRIC SLIDEHeavily incentivized EVs

start strong but face weak long-term prospects P4

WATCH FOR CHRYSLER CAPITAL IN THE LANES COMING SOON. It’s the new wave in reconditioned vehicles with the same exacting standards you’ve come to expect from Santander.

QUALITY • PRICE • VALUE • SELECTION

PERFORMANCE SERVICE • SATISFACTION

PAST. PRESENT. FUTURE PERFECT.

10

Chrysler Capital’s Arrival

GreenLight Remarketing is published by Royal Media on behalf of Santander Consumer USA Inc. For more information about Santander Consumer USA or Road-Loans™ call 888.540.5626 or visit www.santanderconsumerusa.com. Royal Media can be found at www.royalmedia.com. ©2014 Santander Consumer USA Inc.

Chrysler Capital off-lease vehicles will hit the auc-tion lanes officially in 2015 – and we at Santander Consumer USA couldn’t be more excited.

Advance work has been underway for more than a year at SCUSA and Chrysler Capital.

It began just after Chrysler Capital was launched as a private-label, full-service lending program man-aged by Santander Consumer USA and Chrysler Group LLC under a 10-year agreement.

Planning for the Chrysler Capital program has been led by Steve Solo-mon, vice president of asset remarketing for both SCUSA and Chrysler Capital and a former regional sales manager at Chrysler.

Aimed at supporting a new Chrysler off-lease program, this will repre-sent Santander’s first foray into the off-lease marketplace and will help the Chrysler Group to re-establish an off-lease program after several years of outsourcing since Chrysler Finance was disbanded.

The first tangible signs of Chrysler Capital’s arrival will be announce-ment banners and promotional materials late this year introducing the brand and new program at about 15-18 automotive auctions. This is about one-third of the used-car auctions at which Santander vehicles currently are sold.

Vehicles available through the auctions will be two-, three- and four-year-old off-lease products that meet the same standards to which auction participants have become accustomed with Santander. Our company, of course, has been a major participant in the used-vehicle marketplace – at the auctions – where off-lease vehicles under the new program will carry the Chrysler Capital brand.

For more details on the off-lease program, see my leadership column “Making an impact” and Lauri Giesen’s article “Inside Line: A close look at Chrysler Capital’s plans for its off-lease program” in the GreenLight Remarketing Q1 edition on the InsideLane blog.

Then look for Chrysler Capital off-lease vehicles at an auction near you.

Brent HuismanSVP, Asset RemarketingSantander Consumer USA Inc.

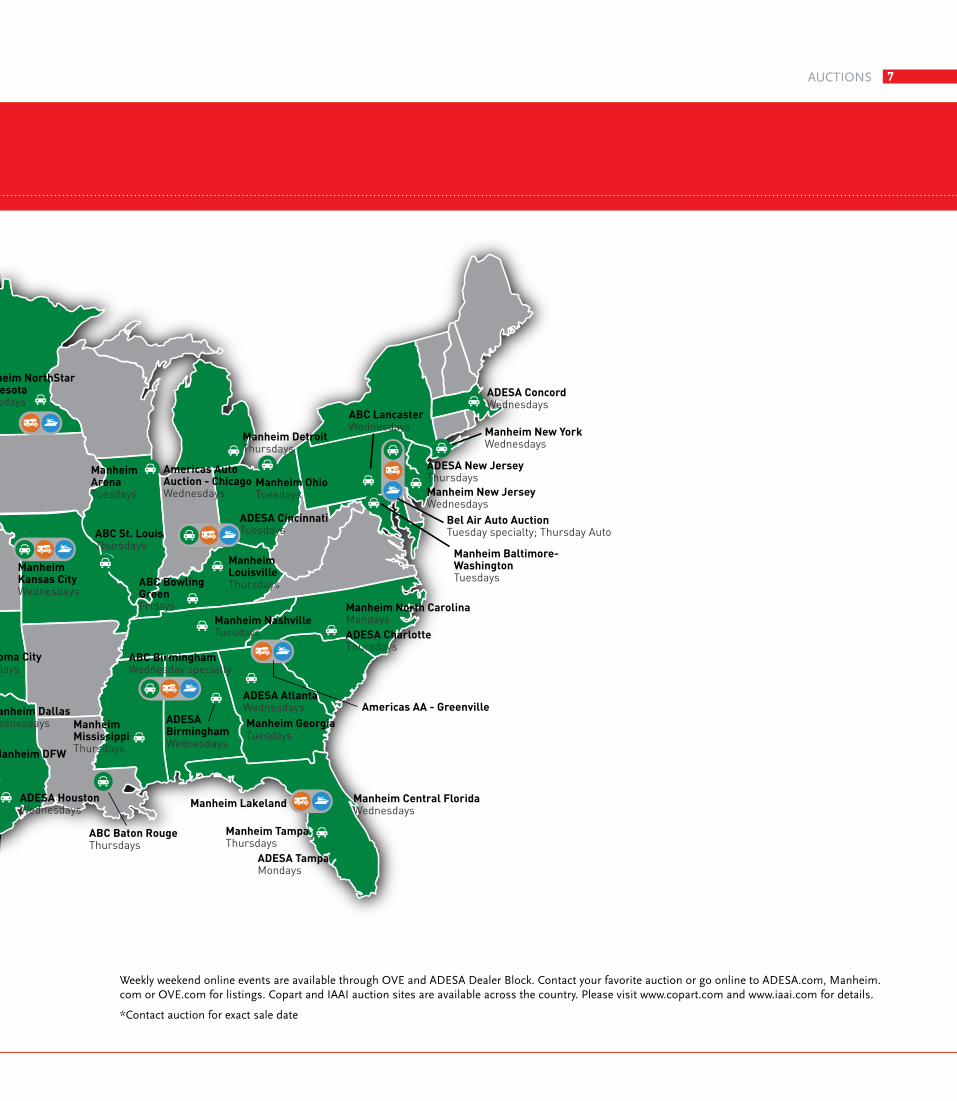

Active Auctions Buy Santander Consumer USA vehicles at auctions nationwide

DEALING DIRECT: RedBumper creates a digital method for dealers to buy consumers’ cars

Little Cars, Big Supply Big interest in — and a big supply of — small cars upends traditional thinking about pricing

Spring Slowdown Wholesale prices softened in May, potentially presaging further weakness

IN FRONT

CONTENTSLEADERSHIP

6

Digital Express Lane Avis bypasses the auction to sell directly to dealers

4

9

8

11

Electric Slide Electric cars cost more up front but deliver less equity on the backend

3

NICHE MARKETS

Electric cars cost more upfront but deliver less equity on the backend BY KAREN JONES

ELECTRIC CARS MAY BE THE HOT NEW thing — but they aren’t actually new at all. Nearly one-third of the vehicles on the road at the turn of the 20th century were

electric-powered. It wasn’t until Henry Ford’s gas-oline-powered Model T became mass-produced, which allowed gas-powered cars to win on price, power and performance, that electrics drove off into the sunset. Today a diverse set of 21st cen-tury electric cars are back in dealer showrooms, but consumer adoption has been slow and resale values remain less than stellar. Even with the success of Tesla, the electric poster child for luxury buyers, marketshare for purely electric vehicles (PEVs) this year through April 2014 is only 0.03 percent, according to Larry

Dixon, senior manager of market intelligence at the National Automobile Dealers Association. Tra-ditional hybrids, including the Toyota Prius, which has stayed the course for 10 years, command just 3 percent of the market to date this year. Dixon adds that he expects purchases of new electric vehicles and hybrids to remain “niche play-ers through 2020” and does not anticipate any sig-nificant growth “over the next five to seven years.”

ICE VS PEV: ANXIETY AND REALITYThe internal combustion engine (ICE) is a formi-dable technology to compete against. Not only is it fully entrenched in automotive mythology, but few drivers worry about how far their ICE vehicle will take them. Not so with PEVs. Anxiety over how

many miles one can expect per battery charge, aptly termed “range anxiety,” is a major deterrent. Drivers a century ago were nervous as well, but most drove shorter distances, and the system of streamlined highways which created the classic American road trip was far in the future. PEVs like Nissan’s Leaf advertise up to 100 miles per charge, and though hybrids like the Chevy Volt have “fail-safe” gasoline engines to help lessen range anxiety, the majority of consum-ers remain unconvinced. Battery-operated options like the heater will decrease range, which may not matter in Arizona, but will in Maine. Other contrib-uting factors dampening enthusiasm include an innate fear of new technology, higher sticker prices then ICEs, competition from increasingly efficient

ELECTRIC SLIDE4

NICHE MARKETS

ICEs, and perhaps the biggest arbiter of consumer car purchasing: gas prices.

PANIC AT THE PUMPEric Lyman, vice president of industry insights at ALG and TrueCar Inc., says that during the 2008 gas crisis everyone panicked — both consum-ers and automakers. Suddenly, he says, “electrics and hybrids looked great,” and a 100-mile battery range seemed sufficient for many consumers. The Prius immediately became the “it” car as people scrambled to unload what the media routinely re-ferred to as “gas-guzzling SUVs.” Though gas prices are higher today than in 2008, they have been relatively stable over the last few years and the new-car market has read-justed, or fallen back into old patterns. “If there is one thing we have learned,” Lyman says, “it’s that consumer impact to gas prices is emotional, not practical — and it is short-lived.” Until the next price crisis at the pumps incites a panic, ICEs will remain the buyers’ choice, espe-cially since ICE fuel efficiency is catching up with hybrids and EVs, adds Lyman. “We see 40 miles to the gallon now, and that also slows the will to change to something new.”

THE TESLA FACTORFor the small percentage of consumers to whom im-age matters and money does not, most electric vehi-cles lacked the necessary pizzazz until Tesla roared into the market. With its 200-mile range and atten-tion to style, Tesla has solved the green car image problem for the luxury set. “It is a great-looking car which has achieved a cult following,” says Lyman, who likens its appeal to celebrity fashion designers that demand a premium price because wearing their clothes denotes a certain status. “I have a friend in L.A. who works in commer-cial real estate where it is all about image,” says Lyman. “His first car was a Range Rover. Three years later he bought a Prius. When I asked why, he replied, ‘Billionaires drive a Prius.’ Now the Tesla is suddenly an option for that consumer de-mographic.” The distinctive Prius design has al-ways said that the person behind the wheel takes environment issues seriously. Tesla says the same, but with Beverly Hills bling. For the less well-heeled, Tesla has confirmed it plans to offer a Gen3 $35,000 model by 2017.

STICKER SHOCKSticker price is still critical to the majority of car buyers, new and used. The combination of the

current government tax incentive of up to $7,500 toward buying a new EV, as well as aggressive mar-keting, are helping models like the Leaf pull ahead of the pack, says Eric Ibara, director of residual value consulting at Kelley Blue Book. He adds that over the first four months of 2014, Nissan has spent approximately $10,700 per Leaf in leasing incentives “so they can offer buy-ers a monthly payment of $199.” Chevy has spent $6,200 per year on the Volt. Ibara believes that the need for large incentives is further proof that con-sumers just are not ready for electrics yet.

RESIDUAL VALUEIncentives meant to help EVs on the front end hurt on the back. “The residual value of these cars starts low because they all come with a federal tax credit for buying them new,” says Ibara. (For a list of qualifying models and applicable tax credits visit www.fueleconomy.gov.) Because the credit is one-time only and does not apply to resale, Ibara says, “What buyer is go-ing to spend more on a used car than a new one? The people who buy these cars tend to be very ear-ly adapters and they want new cars. That means there is a very small market for used cars in this space to begin with.” Lyman concurs. “There is always a premium for buying something new — to be the first one to take it out of the shrink wrap or drive it off the lot.” Conversely, there is always a discount for buy-

ing something used, “otherwise we would all buy new.” That equation does not apply to green cars, where the combination of tax credits and incen-tives drops the price of new cars down near a one-year used-car sticker price. In order for remarketers to make money, Ly-man says, they do not necessarily have to reinvent the wheel, but rather understand that a different approach is needed. Although it’s a new technol-ogy and people looking for used green vehicles are a different kind of buyer, dealers should realize “it is still a car.” Lyman suggests that dealers looking to sell to green buyers should “definitely install a charging station,” keep the sales staff fully up to date with the technology, and be conversant with the advantages of green, in order to speak the lan-guage of environmentally conscious buyers. “Probably the best way to shore up used-car prices on EVs,” Blue Book’s Ibara suggests, “is for the finance company who owns the assets to offer subsidized interest rates on the used EV, so they can compete with new-car monthly payments.” The good news, says Dixon, is that even though EVs will remain a niche for a number of years, he feels depreciation will gradually improve. “We saw this with the hybrids in the past where it wasn’t un-common to see them lose 20 to 25 percent of their value in the first year, and we’ve seen similar [num-bers] with the Leaf and the Volt. But with each pass-ing year, that rate of depreciation has improved, and I think that will continue moving forward.”

THE COMPETITION The Chevrolet Volt and Nissan Leaf get the lion’s share of the public’s attention, but Ford also offers the Focus Electric (a full EV), the Fusion Energi and C-Max Energi (both plug-in hybrids), while Mitsubishi offers the fully electric iMiEV, the cheapest electric on the market from a major manufacturer.

CHEVROLET VOLT

MSRP: $34,185

NISSAN LEAF SV

MSRP: $32,000

FORD FOCUS ELECTRIC

MSRP: $35,170

MITSUBISHI IMIEV

MSRP: $34,185

MARKETSHARE YTD THROUGH APRIL 2014

Prices shown are before any credits, options or destination charges.

AVERAGE TRADE IN VALUES FOR HEVS, PEV, PHEV, ICE

HEV: Traditional hybrids

PHEV: Plug-in electric vehicles with a small gasoline engine — Chevy Volt/Ford Fusion Energi

PEV: Plug-in electric vehicles only- Nissan Leaf, Tesla Model S, Ford Focus Electric

Gasoline ICE: average trade-in values for 2011-12 model years declined by 14-15 percent

HEVs: average trade-in values for 2011-12 model years declined by 14-16 percent

PEV and PHEV: average trade-in values for 2011-12 models declined by 18-22 percent.

3.0%

0.3%

0.3%

5

AUCTIONS

ACTIVE AUCTIONS

ADESA DallasThursdays

Manheim Kansas CityWednesdays

ADESA Golden GateTuesdays

ADESA New JerseyThursdays

Manheim New YorkWednesdays

ADESA CharlotteThursdays

Manheim LouisvilleThursdaysABC Bowling

GreenFridays

Brasher’s IdahoThursdays

Brasher’s Salt Lake CityTuesdays

ADESA TampaMondays

Manheim HawaiiWednesdays*

Manheim Denver

Manheim Southern CaliforniaThursdays

ADESA HoustonWednesdays

ABC BirminghamWednesday specialty

ADESA BirminghamWednesdays

ADESA AtlantaWednesdays

ADESA Los AngelesFridays

Manheim Dallas Wednesdays

ADESA CincinnatiTuesdays

ADESA PhoenixWednesdays

DAAOklahoma CityThursdays

ManheimSan AntonioWednesdays

ABC LancasterWednesdays

Manheim New JerseyWednesdays

Bel Air Auto AuctionTuesday specialty; Thursday Auto

ADESA ConcordWednesdays

Manheim GeorgiaTuesdays

Manheim TampaThursdays

Manheim Central FloridaWednesdays

Brasher’s RenoWednesdays

Americas Auto Auction - ChicagoWednesdays

Manheim ArenaTuesdays

Manheim NorthStar MinnesotaThursdays

Manheim North CarolinaMondays

Dealers AAof AlaskaWednesdays

Manheim DetroitThursdays

Brasher’s IdahoThursdays

Manheim OhioTuesdays

Manheim Nashville Tuesdays

ABC St. LouisThursdays

Manheim Baltimore-WashingtonTuesdays

ADESA San DiegoThursdays

Brasher’s Northwest*

Brasher’s Salt Lake CityTuesdays

Americas AA - Greenville

Brasher’s Sacramento

Manheim DFW

Manheim Lakeland

Manheim Tucson

Americas Auto AuctionTuesdays

Auto Auction

RV Auction (please contact auction for dates)

Boat Auction (please contact auction for dates)

Manheim MississippiThursdays

ABC Baton RougeThursdays

ADESA Colorado Springs

6

AUCTIONS

ACTIVE AUCTIONS

Weekly weekend online events are available through OVE and ADESA Dealer Block. Contact your favorite auction or go online to ADESA.com, Manheim.com or OVE.com for listings. Copart and IAAI auction sites are available across the country. Please visit www.copart.com and www.iaai.com for details.

*Contact auction for exact sale date

ADESA DallasThursdays

Manheim Kansas CityWednesdays

ADESA Golden GateTuesdays

ADESA New JerseyThursdays

Manheim New YorkWednesdays

ADESA CharlotteThursdays

Manheim LouisvilleThursdaysABC Bowling

GreenFridays

Brasher’s IdahoThursdays

Brasher’s Salt Lake CityTuesdays

ADESA TampaMondays

Manheim HawaiiWednesdays*

Manheim Denver

Manheim Southern CaliforniaThursdays

ADESA HoustonWednesdays

ABC BirminghamWednesday specialty

ADESA BirminghamWednesdays

ADESA AtlantaWednesdays

ADESA Los AngelesFridays

Manheim Dallas Wednesdays

ADESA CincinnatiTuesdays

ADESA PhoenixWednesdays

DAAOklahoma CityThursdays

ManheimSan AntonioWednesdays

ABC LancasterWednesdays

Manheim New JerseyWednesdays

Bel Air Auto AuctionTuesday specialty; Thursday Auto

ADESA ConcordWednesdays

Manheim GeorgiaTuesdays

Manheim TampaThursdays

Manheim Central FloridaWednesdays

Brasher’s RenoWednesdays

Americas Auto Auction - ChicagoWednesdays

Manheim ArenaTuesdays

Manheim NorthStar MinnesotaThursdays

Manheim North CarolinaMondays

Dealers AAof AlaskaWednesdays

Manheim DetroitThursdays

Brasher’s IdahoThursdays

Manheim OhioTuesdays

Manheim Nashville Tuesdays

ABC St. LouisThursdays

Manheim Baltimore-WashingtonTuesdays

ADESA San DiegoThursdays

Brasher’s Northwest*

Brasher’s Salt Lake CityTuesdays

Americas AA - Greenville

Brasher’s Sacramento

Manheim DFW

Manheim Lakeland

Manheim Tucson

Americas Auto AuctionTuesdays

Auto Auction

RV Auction (please contact auction for dates)

Boat Auction (please contact auction for dates)

Manheim MississippiThursdays

ABC Baton RougeThursdays

ADESA Colorado Springs

7

DEALING DIRECTDEALERS

A new online service offers dealers a way to by-pass the traditional auction channel and pur-chase cars straight from their owners.

CarOffer is a service that lets consumers list their cars for sale and dealers browse the offer-ings and make bids. It was introduced at the NADA convention in New Orleans in February 2014 by RedBumper, known for its inventory management system, and went live to a limited pool of users on March 17.

Using his mobile phone camera, a consumer can scan his VIN, take photos of the car — CarOf-fer requires six or seven photos covering certain angles — and upload the vehicle to CarOffer for sale. There is no cost to the consumer and CarOffer does not recoup any portion of the sale price, according to the company.

Consumers can expect a cash offer within two to three hours of posting on a business day, according to CarOffer chief executive Bruce Thompson. They then have seven days to re-deem the offer by dropping off the car and pick-ing up the check.

Once an offer is accepted, the condition of the vehicle is verified by one of CarOffer’s dealer partners. If the condition of the vehicle differs in any significant way from what was represented at the time of the sale, the bid can be adjusted on the spot before the financial side of the trans-action is completed.

Dealers pay a fee to use the service and are able to claim Zip codes for an additional month-ly fee determined by the population of the area. This gives dealers the exclusive right to bid on cars going up for sale in the Zip codes they li-cense. Zip codes are available on a first-come, first-serve basis.

Thompson started a service called American Auto Exchange in 2001. That service, now called DealerTrack AAX, covered some of the same ground as CarOffer. “Dealers buying direct from consumers is the holy grail,” Thompson tells

BY PHIL RYAN

RedBumper creates a new digital service allowing dealers to buy cars online straight from consumers

GreenLight Remarketing. “It’s what gives CarMax the edge the average dealer doesn’t have.”

Dealers can access the tool with their own mobile devices or through a desktop portal that displays a bidding queue as well as auction data, market data car history from Carfax and other sources. Dealers can also embed the tool as a widget on their sites.

“I want the dealer to invest in the brand to help build their markets, and to help build the national brand. The only way to do this is if they own the territory,” Thompson says. Sev-eral of CarOffer’s dealers showcase the brand in their advertising, such as Lou Fusz in the St. Louis area.

CarOffer estimates that, aside from the sav-ings on auction fees, dealers can make a $500-to-$1,000 profit on vehicles sold wholesale, or $1,000 to $1,500 on vehicles sold at retail.

The real win for dealers, however, is when the customer selling his car buys his replacement from the dealer. In this case, the car bought on CarOffer is effectively a trade-in. CarOffer esti-mates profits of $1,000 to $2,500 on sales such as these.

“Our initial pilot launch has been tremen-dously successful,” says Ziad Chartouni, CarOf-fer’s chief technology officer. “We’ve only opened up about 10 percent of our capacity during the soft launch.” CarOffer’s service is now available

to all qualified dealers.Thompson, CarOffer’s CEO, says the company

has licensed about 5,000 Zip codes since launch and averages about 30,000 bids per month. “We expect that to double next month,” Thompson said. “Volume has been off the charts.”

The company will also expand its offerings with several major partnerships in the coming months, Thompson says.

An early competitor to CarOffer, from the per-spective of the consumer, is the startup Beepi. This tool allows users to list their cars in much the same way as CarOffer, but instead of market-ing them to dealers, the app serves as a mar-ketplace for other consumers to view and make offers on the vehicle. Dealers are more reliable than private citizens in terms of honoring con-tracts and making payments, but consumer mistrust of dealers could still drive them to per-son-to-person models. And, given that CarOf-fer allows dealers to lock up certain Zip codes, Beepi offers a larger pool of potential buyers, as does Craigslist.

Selling on Craigslist is mocked in a humorous post on CarOffer’s blog, which is updated fre-quently, as are the company’s social media posts on Twitter and Facebook.

CarOffer is still new, and not one of the sev-eral industry experts reached for comment by GreenLight Remarketing was yet aware of it. In any case, CarOffer is another sign that the in-ternet and mobile devices are rapidly changing the ways cars are sold. Going forward, Dealers should expect to see consumers that are better informed about buying and selling their cars.

STOCKING THE LOTDealers have long offered to buy consumers’ existing vehicles with direct mailers like this — as trade-ins to generate new-car sales. The trade-ins were sometimes retailed but often sent to auction. But with used-car supplies constrained for several years, dealers have used the same methods to seek stock they primarily intend to retail themselves from customers.

8

DEALING DIRECTCARS

The increased popularity of high-quality small cars has changed the pricing landscape for subcompacts

LITTLE CARS, BIG SUPPLY

A combination of cheap prices and better fuel economy over the past several years has attract-ed frugal American consumers to subcompact cars like ants to a summer picnic. Those strong new car sales numbers have cut into the prices of subcompacts in the auction lanes.

“New sales exploded for the segment over the past few years,” says Larry Dixon, senior manag-er for market intelligence with the National Au-tomobile Dealers Association’s Used Car Guide. “You’re having an increased supply, and pretty significant growth of the segment. That popu-larity and that volume is going to help increase the rate of depreciation in the segment moving forward.”

According to Alec Gutierrez, senior market analyst for automotive insights at Kelley Blue Book, the increase in demand is also driven by a few particularly popular models, such as the Chevrolet Sonic and the Ford Fiesta.

“Both dealers and consumers just have far more viable options,” he says. The appeal of subcompacts grew as hard times continued for many Americans over the past several years. But one result of subcompacts going more main-stream is that some newer models are getting high-end touches such as leather interiors and other add-ons that can raise the prices consid-erably. This opens up the segment to new buy-ers beyond the highly price-sensitive and those looking for an entry-level vehicle.

Dixon notes that the wholesale supply for the subcompact segment is up 22 percent this year, a significantly higher figure than the overall ve-hicle supply increase of 9 percent.

Gutierrez, though, notes that while prices for

subcompacts are down about 6 percent versus the previous year, he “wouldn’t necessarily expect to see tremendous pressure on margins.” In oth-er words, though dealers are being paid less from customers for used subcompacts, they are also putting out less for them in the auction lanes.

A MORE STABLE FUTUREAs for what the future holds, Gutierrez sees pric-es on subcompacts stopping their downward plunge and beginning to level off.

“I expect to see that gap narrow somewhat,” he says, referring to the difference in subcom-pact pricing. “About a year ago, a lot of these were just showing up in the lanes for the very first time.”

That influx of a new generation of subcom-pacts resulted in a “unique window” and excite-ment among buyers that may have led to prices rising too quickly, he explains. The downward slip in subcompact pricing is already starting to reverse.

“Subcompact pricing is on an upward trajec-tory if we talk about where prices were a month

BY BEN GEIER

IS PAST PROLOGUE?In 1982, Americans were spoiled for choice when it came to small cars and eco-nomical options. After two oil shocks in a decade, buyers wanted economy cars or, at least, higher-MPG versions of regular cars.

Manufacturers were eager to oblige — selling everything from the Chevette and Datsun 210 to downsized Coupe DeVilles with diesel V8s. While the smallest cars of that era got good gas mileage, they often felt small, slow and cheap compared with larger vehicles. Oil prices began to decline in the 1980s — at first slowly and then dramatically after 1986 — and consumers’ memories of the oil crises began to fade.

Consumers abandoned diesels wholesale (GM’s very public problems with its diesels did not help) and opted for larger and larger vehicles, even after a brief gas price spike dur-ing the first Gulf war. By the mid-1990s, SUVs, sometimes as large and heavy as the biggest pre-

1973 American sedans, were popular and the selection of small vehicles had withered to just a few models, none particularly desirable. Organic demand for such cars brought a few new options in the mid-2000s, such as the Mini (in 2003) and Honda Fit (in 2006); but it took the fuel shock of 2008 to revive mass interest in quality small cars in the U.S.

Today, Americans have the best selection of small cars they’ve ever had — ones that gener-ally do not feel “cheap” even if they are inexpen-sive. The only question is, will consumers keep buying them even if fuel prices decline?

ago,” Gutierrez says. “We’re going to see pricing converge.”

Indeed, Tom Kontos, executive vice president analytical services with Adesa, saw a 4 percent rise in price for the segment from February to March.

Dixon offers another reason that subcompact pricing may begin level off — a possible dip in demand due to gas prices.

“Gasoline prices have moderated, and they’re expected to remain flat over the next year or two years,” he says. With gas prices steady, buyers become less concerned with maximum fuel ef-ficiency, and may turn their search to larger ve-hicles.

What can dealers do to maintain marketshare in a world where subcompacts are in such de-mand?

“They just want to have an adequate supply, a broad supply,” Dixon says, noting that this trend applies across segments. The best way to hold the proper inventory is to know the market, Dix-on says. “I’d say that just having an understand-ing of where prices are headed will allow them to make more intelligent purchase decisions.”

9

FLEET

DIGITAL EXPRESS LANEAvis bypasses the auctions to sell directly to dealers

Auto dealers will now be able to purchase used rental cars directly from Avis Budget Group Inc., eliminating the need to work through an auction company. Under a new program called AvisDi-rect that was announced in February, authorized auto dealers will be able to purchase late-model off-rental cars from Avis, Budget, Payless and Zipcar, in person and online.

The new program is expected to significantly reduce the fees associated with rental car pur-chases for both auto dealers and the rental car company, while reducing the potential revenue for auction houses, according to Nino Parco, chief executive of the Dallas-based Dealership Ex-perts, a consulting firm that advises auto dealers.

The program is a major change from how Avis had been selling its off-rental cars, which was to pay auction houses to sell them to deal-ers. “Now dealers can buy directly from us without having to go to an auction and with-out incurring auction fees,” says Greg Thibault, vice president of remarketing for Avis Budget Group. “Avis Direct allows us to continue to diversify our remarketing channels, increase efficiencies and offer dealers an alternative to buying vehicles at auctions.”

Avis will make its vehicles available to dealers in three ways. First, dealers can buy vehicles on-line through listings posted on a dedicated web-site. Dealers can also request a list of vehicles designated as eligible to sell and place an order. Finally, dealers can make an appointment and purchase vehicles directly off Avis lots. The price

are rented by business executives and families that don’t abuse them, Parco says. And they are maintained by rental companies that employ pro-fessionals to keep an eye on their condition and maintenance records.”

Avis is not the first rental car company to sell directly to dealers, but its multi-channel approach makes it one of the more ambitious fleet sales programs.

About seven years ago, Enterprise Rental tried a direct program, but the effort had limited success because it required dealers to visit Enterprise to purchase the cars in person, Parco explains. That added to the overall cost to dealers.

“Technology has advanced since that time and the Avis method of using a website will make it more successful. Dealers won’t have to pay for transportation, and they’ll be able to view autos and get all the information they need online,” Parco says.

Thibault says the website will include online photos of the cars offered for sale and indepen-dent third-party condition reports. Although Avis declines to say how many autos will be sold through the program, Thibault says it will involve hundreds of makes and models.

Parco expects other rental companies may fol-low suit and sell directly, as well. “There is no question that other rental companies are looking at this new Avis model and will follow Avis’ lead if it is successful,” he says.

of the cars will not change, no matter which sales channel dealers use.

The savings to dealers and Avis could be sub-stantial, according to Parco. He says auction houses typically charge rental companies approxi-mately $275 per vehicle, and then charge dealers another $275 to make a purchase. In addition, dealers often incur fees associated with getting to auction sites to make purchases. Some of the savings Avis earns by not having to pay to auction houses may now be passed on to dealers in lower prices on the autos, Parco says.

“This is great for dealers and the rental car companies,” Parco says. Auction houses may not be so pleased.

Previously, Avis had sold a small number of its autos directly to local dealers. These sales typi-cally were handled by regional Avis offices. The number of cars involved was limited, and vehicles were only available to dealers located near large rental fleets, Parco explains.

Off-rental cars represent a significant portion of the cars sold by many dealers, according to Parco. “In some large dealerships, rental cars can be as high as 20 percent to 30 percent of a dealers’ total pre-owned inventory.”

And rental cars often represent high-value ve-hicles. “Rental cars are typically late-model vehi-cles that rarely have more than 25,000 miles on them,” Parco says. “The typical rental car being sold has about 18,000 to 25,000 miles on it and is still under the manufacturer warranty.”

In addition to having low miles, the cars are usually in good condition. “Contrary to the ste-reotypes that rental cars are abused, most cars

BY LAURI GIESEN

Dealers can now access these cars as easily as the original customers could rent them. The AvisDirect program extends to the Budget, Payless and Zipcar fleets as well.

“ There is no question that other rental companies are looking at this new Avis model and will follow Avis’ lead if it is successful.”

— Nino Parco, Chief Executive, Dealership Experts

10

WHOLESALE USED-VEHICLE PRICE TRENDS

Source: ADESA Analytical Services

1This analysis is based on nearly seven million annual sales transactions from more than 170 of the largest U.S. wholesale auto auctions, including those of ADESA, as well as other auction companies. ADESA Analytical Services segregates these transactions using the J.D. Power and Associates Vehicle Segmentation Guide to study trends by model class.

The views and analysis provided herein relate to the vehicle remarketing industry as a whole and may not relate directly to KAR Auction Services Inc. The views and analysis are not the views of KAR Auction Services, its management or its subsidiaries, and their accuracy is not warranted. The statements contained in this report and statements that the company may make orally in connection with this report that are not historical facts are forward-looking statements. Words such as “should,” “may,” “will,” “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “bode”, “promises”, “likely to” and similar expressions identify forward-looking statements. Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the results projected, expressed or implied by the forward-looking statements. Factors that could cause or contribute to such differences include those matters disclosed in the company’s Securities and Exchange Commission filings. The company does not undertake any obligation to update any forward-looking statements.

AVERAGE PRICES ($/UNIT) LAST MONTH VS.

May 14 Apr. 14 May 13 Prior Mo. Prior Yr.

Total Trucks $10,892 $10,918 $9,750 -0.2% 11.7%

Mini Van $7,299 $7,310 $6,558 -0.2% 11.3%

Fullsize Van $11,243 $10,921 $9,872 2.9% 13.9%

Mini SUV $12,991 $13,308 $11,053 -2.4% 17.5%

Midsize SUV $8,390 $8,378 $7,164 0.1% 17.1%

Fullsize SUV $10,896 $10,723 $10,580 1.6% 3.0%

Luxury SUV $19,778 $19,582 $18,673 1.0% 5.9%

Compact Pickup $7,705 $7,777 $7,441 -0.9% 3.6%

Fullsize Pickup $13,305 $13,450 $11,810 -1.1% 12.7%

TRENDS

Wholesale prices in May softened from their April spring-market/tax-season peak, although they remain significantly above year-ago levels. Retail demand, particularly for “certifiable” units for record CPO sales, helped absorb off-rental volume and grow-ing off-lease supply without significant price declines. However, there was some hesitancy from a few sellers to accept May’s lower prices, and this was reflected in low con-version rates for those consignors.

May’s downturn could be a precursor to further softening, especially in areas such as the Northeast, where the growth in off-lease supply is expected to be concentrated.According to ADESA Analytical Services’ monthly analysis of Wholesale Used Vehicle Prices by Vehicle Model Class1, wholesale used vehicle prices in May averaged $10,321 — down 1.5 percent compared with April, and up 5.4 percent relative to May 2013. Truck prices con-tinue to generally hold firmer than car prices.

Prices for used vehicles remarketed by manufacturers were down 1.4 percent month-over-month and up 5 percent year-over-year, as more off-rental program units entered the market, many of which were no-sold. Prices

After a strong spring, May wholesale prices soften, perhaps presaging further declines

for fleet/lease consignors were down 1.5 percent sequentially and up 4.2 percent annually, as more off-rental risk units entered the market (although in many cases these too were no-sold) along with more off-lease vehicles. Dealer consignors saw a 2.5 percent average price decrease versus April, and a 3.7 percent uptick versus May 2013, as they wholesaled units obtained in part from trade-ins generated via May’s strong new vehicle sales.

Based on data from CNW Marketing/Research, retail used vehicle sales in May were up 12.3 per-cent month-over-month and 3.9 percent year-over-year. Sales of certified pre-owned (CPO) ve-hicles were a record 207,371 units, up 7.4 percent versus April and up 10.9 percent from the prior year, based on figures from Autodata.

BY TOM KONTOS

Tom Kontos

SPRING SLOWDOWN

AVERAGE PRICES ($/UNIT) LAST MONTH VS.

May 14 Apr. 14 May 13 Prior Mo. Prior Yr.

Total All Vehicles $10,321 $10,481 $9,796 -1.5% 5.4%

Total Cars $9,230 $9,373 $8,934 -1.5% 3.3%

Compact Car $7,266 $7,470 $7,087 -2.7% 2.5%

Midsize Car $8,503 $8,613 $8,192 -1.3% 3.8%

Fullsize Car $7,185 $7,296 $7,240 -1.5% -0.8%

Luxury Car $12,677 $12,563 $12,224 0.9% 3.7%

Sporty Car $13,149 $13,427 $12,849 -2.1% 2.3%

Total Crossovers $12,821 $13,222 $12,936 -3.0% -0.9%

Compact CUV $11,589 $11,977 $11,352 -3.2% 2.1%

Mid/Fullsize CUV $14,093 $14,478 $14,537 -2.7% -3.1%

11

As one of the largest remarketers of vehicles in the country, Santander Consumer USA offers the right selection of vehicles in the right places with the right coverage.

Dealers swinging for the green choose Santander Consumer USA for its exacting

standards on vehicle makeovers before resale.Anything else would be a shank.

TEE TIME

Quality • Price Value • Selection

Performance Service

Satisfaction