h.j. van burg, project director ntp october 2007 dutch taxonomy project (ntp) semantic data and...

Post on 20-Dec-2015

216 views

TRANSCRIPT

H.J. van Burg, Project Director NTPOctober 2007

Dutch Taxonomy Project (NTP)Semantic data and process interoperability andcontinuous auditing.

Index

• Reporting chain • The concept• The National Taxonomy• Case (2)• And where fits continuous auditing?

Regulatory Driven Reporting

Business

Accountant

Intermediary

Solution Provider 2

SolutionProvider 1

Bank

TAX

CoC

Statistics

Super Funds

Requests

Requests

Requests

Requests

Requests

Observations

• Information is not interconnected between domains • mainly due to different accounting principles and contexts

• Inefficiencies in preparation and compliance

• Reliability of information is lacking behind

The concept

• Rationalize: 1. data, 2. processes and 3. compliance• The rationalization process always complies with law

and starts with the common accounting practice businesses

• Data and process taxonomies interconnect (reporting) domains as well as interconnect law and common practice

• A taxonomy (data and process) drive control framework results in an effective and efficient reporting chain

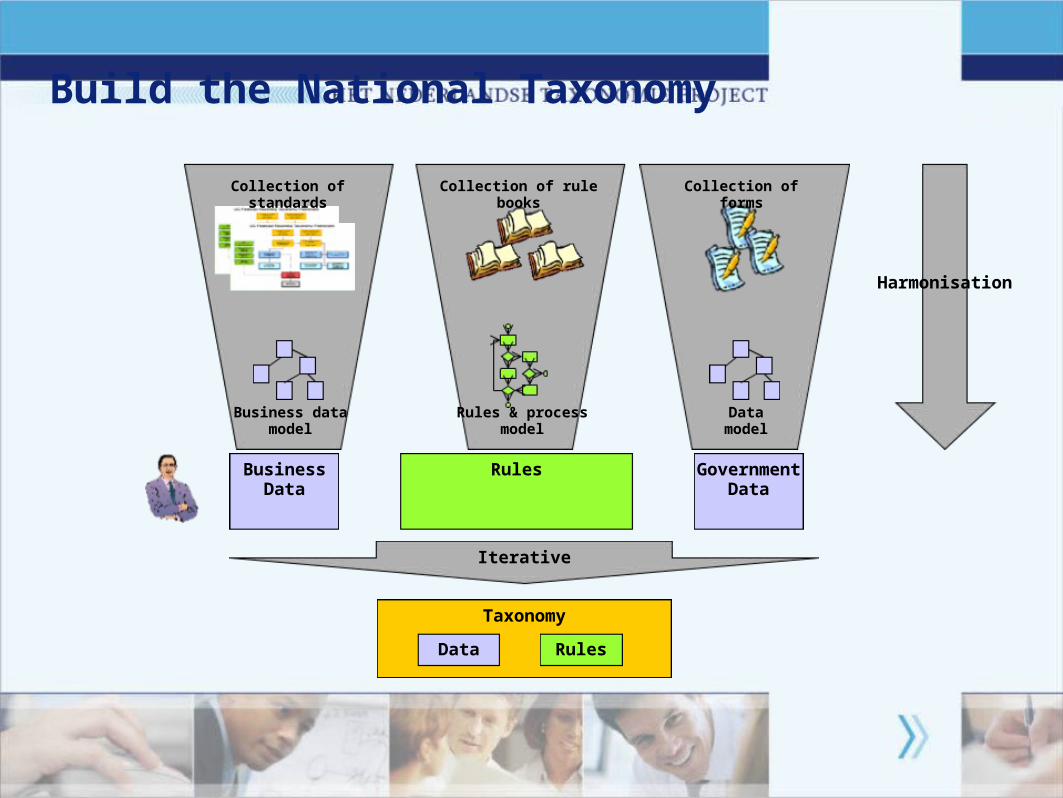

Build the National Taxonomy

Taxonomy

Data Rules

BusinessData

Government

Data

Rules

Iterative

Collection of forms

Datamodel

Collection of rule books

Collection of standards

Business datamodel

Rules & processmodel

Harmonisation

National Taxonomy – Roadmap

Taxonomy v1.0

Data Rules

Legislative burden reduction

Taxonomy v2.0

Data Rules

Taxonomy v3.0

Data Rules

Taxonomy v4.0

Data Rules

Law • Red Paper

Process server

Services

Validation service

Business Driven Regulatory Reporting

R1R2R3

TAX

CoC

Statistics

Statistics

Tax Reporting

Annual Accounts

Computer

FinancialPackage (FP)

Taxonomy

Taxonomy

Taxonomy

Taxonomy

Business

Intermediary

Director

Observations

• Information is interconnected between domains • common ground in accounting principles and contexts

• Preparation of report information is effective and efficient

• Reliability of information has increased but still there is a need for compliance

Case: Limited Corporation Tax Declaration (LCTD)

• Observationo More and more information is required (1.600 data elements)o Information is not interconnected with the annual accountso Tax advisers prepare the Limited Corporation Tax Declaration

(LCTD)

• Objectives (see paper)o Limit the amount of data element what is legally required (400)o Interconnect data en processes definitions (taxonomies) of LCTD

with the annual accountso Agree on mutual compliance

Case: LCTD

• Preparationo Design the Limited Corporation Tax Declaration extension

(objective: general accepted tax and interconnected accounting principles)

o Design the subsequent processes (objective: impose checks and balances)

o Agree on a Tax Control Framework (objective: segregation of responsibilities Intermediary and Tax Agent)

• Execution o Pilot and controlled

Case: Basel II

• Observationo Preconditions for implementation are not fulfilled:

No semantic interoperable data framework (accounting principles)

Reporting is not interconnected with annual of fiscal domain Expectation gab on assurance The existing gathering is inefficient and very expensive

• Objectives o Comply with the market!

Case: Basel II

• Preparation o Build a Basel II extension on the Dutch taxonomy

(objective: general accepted accounting principles and interconnect)

o Design the subsequent processes (objective: impose checks and balances)

o Agree on a Control Framework (objective: segregation of responsibilities Intermediary and Financial institute)

• Execution o Pilot starts in 2009

Continuous auditing

• Control Framework (Annual, Tax or / and Basel II):o Interconnect domains,o Segregation of responsibilities and o Scope prepares / auditing work

• Different purpose, contexts and frequencies of reporting requires continuous auditing work

• More and more auditing work will become part of the internal control framework

Thank you

More informationwww.xbrl-ntp.nl