hksa pss qualification programme case analysis competition 2003 presented by: chan ka sing, kenneth...

TRANSCRIPT

HKSA PSSQualification Programme

Case Analysis Competition 2003

Presented by:Chan Ka Sing, KennethHeung Ka Lok, MikePoon Wing Ho, GaryTsang Lok Yin, Leo

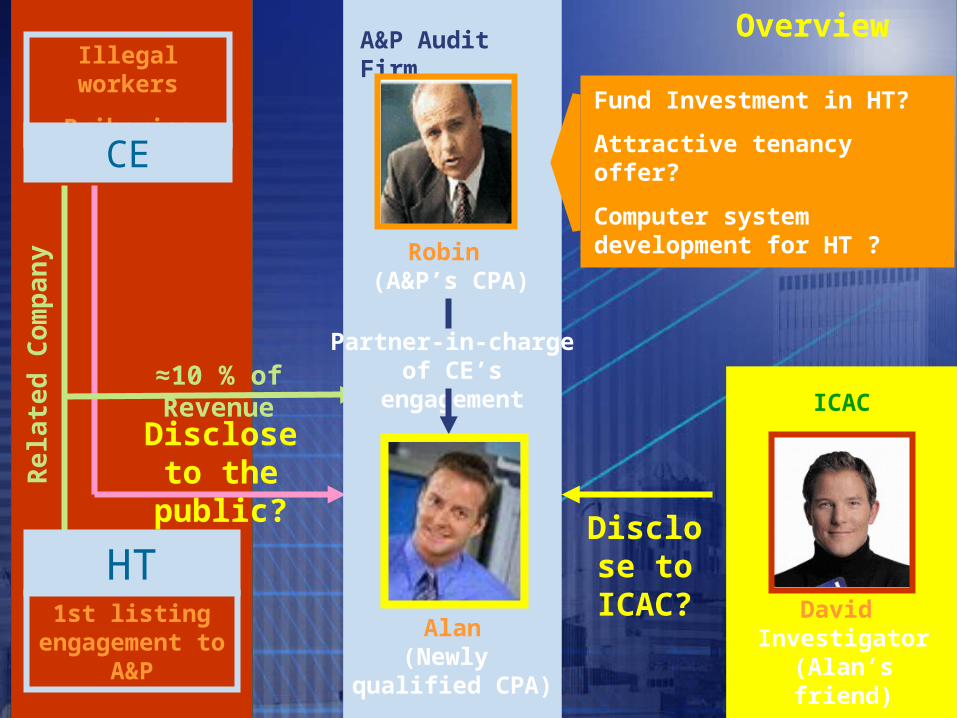

Re

late

d C

om

pa

ny

HT1st listing

engagement to A&P

Illegal workers

Briberies

CE

Disclose to the public?

≈10 % of Revenue

Disclose to

ICAC? David Investigator

(Alan’s friend)

ICAC

A&P Audit Firm

Alan(Newly

qualified CPA)

Robin (A&P’s CPA)

Partner-in-charge of CE’s engagement

Fund Investment in HT?

Attractive tenancy offer?

Computer system development for HT ?

Overview

Information should be solely for carrying out professional duty (HKSA Statement of Professional Ethics 1.204B.3)

Duty of confidentiality is NOT absolute (HKSA Statement of Professional Ethics 1.204A.1)

(1) Illegal Workers Issue

Labor costs were significantly low

CE’s customers were aware of the practice

(2) Briberies Issue

Unexplained payments were found

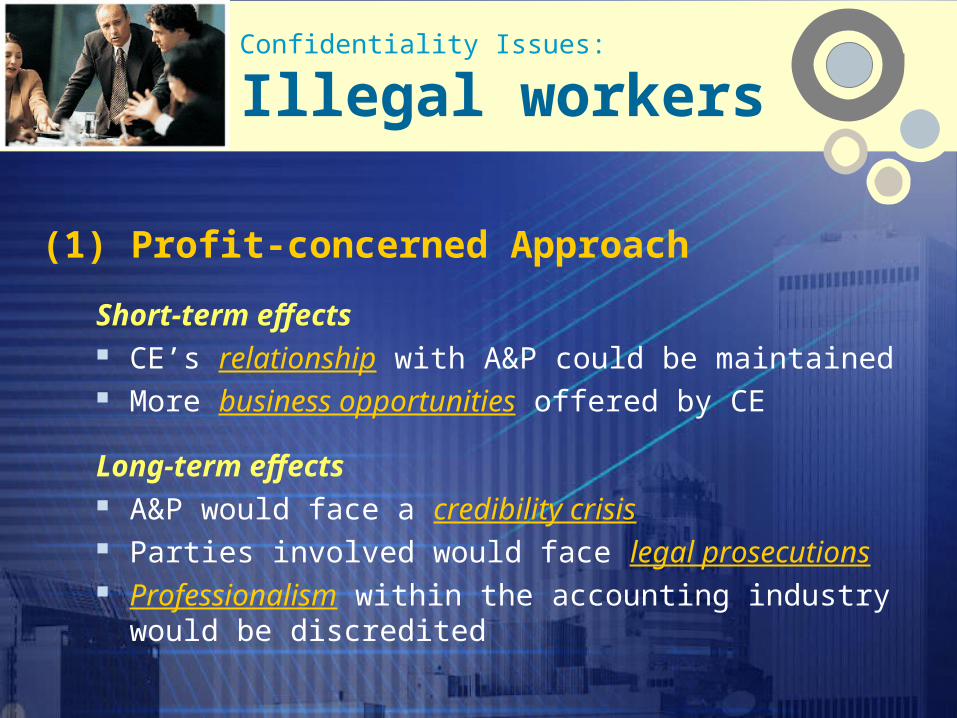

Confidentiality Issues:

Introduction

(1) Profit-concerned Approach

Short-term effects CE’s relationship with A&P could be maintained More business opportunities offered by CE

Long-term effects A&P would face a credibility crisis Parties involved would face legal prosecutions Professionalism within the accounting industry would

be discredited

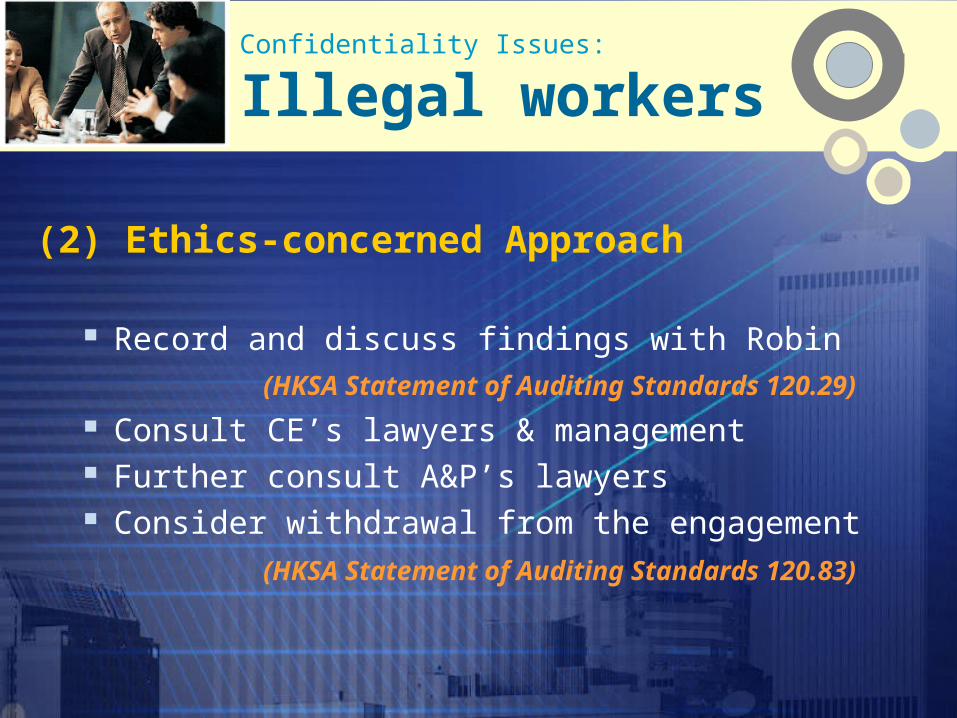

Confidentiality Issues:

Illegal workers

(2) Ethics-concerned Approach

Record and discuss findings with Robin

(HKSA Statement of Auditing Standards 120.29)

Consult CE’s lawyers & management Further consult A&P’s lawyers Consider withdrawal from the engagement

(HKSA Statement of Auditing Standards 120.83)

Confidentiality Issues:

Illegal workers

Short-term effects Relationship between A&P and CE would be strained A&P would lose business from CE & HT

Long-term effects Reputation of A&P could be retained Alan could continue pursuing his career Integrity of the accounting profession could be maintained

(2) Ethics-concerned Approach (Cont’d)

Confidentiality Issues:

Illegal workers

Alan SHOULD:

Persuade Robin not to disclose, but to discuss with CE’s management

(HKSA Statement of Professional Ethics 1.204A.16)

Suggest withdrawal from the engagement Remind CE the possibility of detecting its illegal acts by

competitors Propose to investigate A&P’s default in previous years

Recommendation

Confidentiality Issues:

Illegal workers

Disclose to David due to the public interest and authorization

(Prevention of Bribery Ordinance S.13&14(d))

Duty of Confidentiality is NOT absolute

(HKSA Statement of Professional Ethics 1.204B.11)

Confidentiality Issues:

Briberies

Relationship-concerned Approach Preserve his relationship with David

Professionalism of Alan & A&P would be challenged

Ethics-concerned Approach Maintain professionalism of Alan & A&P

Relationship between Alan & David would be impaired

Trade-off Relationship & Professionalism

Unauthorized under law Breach of professional duty

Not disclose Not in a position to discuss CE’s affairs

Authorized under law Sustain a close relationship with David

Disclose to other investigators Avoid misunderstanding

Legal advice to clarify the legal duty

Recommendation

Confidentiality Issues:

Briberies

Appointed as reporting accountant of HT and auditor of CE

Independence should be remained(HKSA Statements of Professional Ethics 1.203)

Recommendation Suggest another colleague to be in-charge of the IPO project

( HKSA Statement of Auditing Guideline 3.340)

Other services: IPOIndependence Issues:

≈10% annual revenue from CE’s group

Recurring fees < 15% of gross fees & practice( HKSA Statements of Professional Ethics 1.203.4)

Recommendation Closely monitor A&P’s position when audit fees from

CE’s group > 10% of its annual revenue

Audit FeeIndependence Issues:

Robin’s wife invests in a fund which contains HT’s share

Avoid any direct/ indirect personal benefits from an engagement

( HKSA Statement of Professional Ethics 1.203.15)

Recommendation Dispose the fund as soon as possible

( HKSA Statement of Professional Ethics 1.203.17)

Fund InvestmentIndependence Issues:

Receive tenancy offer = conflict of interest

Threaten the objectivity of Robin

( HKSA Statement of Professional Ethics 1.203.34 & 35)

Value of the rental offer ≠ modest

Breach of the Prevention of Bribery Ordinance

Recommendation Reject the offer

Tenancy OfferIndependence Issues:

Robin’s son has business with HT

Close relationship between Robin & HT,

which endanger objectivity of Robin( HKSA Statement of Professional Ethics 1.203.12)

Recommendation Arrange other partners to be in-charge of the

engagement

Advisory for computer system

Independence Issues:

As Stephen Chan, Deputy Director of HKSA, once wrote,

“Auditors are required to exercise professional judgment, rather than following certain prescriptive rules, such that independence of mind and independence in appearance

are not compromised”

ExcerptConclusion:

PresentWhen confronted with ethical dilemma,

he should bear in mind his: Professionalism, and Commitment

Future Setting up Independent Investigation Board Helping to exercise professional judgment

Present & FutureConclusion:

The EndThank You for Your Attention