hmda data analysis for the cities of muskegon, muskegon ...€¦ · hmda data analysis for the...

TRANSCRIPT

HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and

Norton Shores

July 2019

Prepared for:

City of Muskegon City of Muskegon Heights City of Norton Shores 933 Terrace 2724 Peck Street 4814 Henry Street Muskegon, MI 49440 Muskegon Heights, MI 49444 Norton Shores, MI 49441

Prepared by:

Fair Housing Center of West Michigan 20 Hall Street SE Grand Rapids, MI 49507

HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Introduction

The Fair Housing Center of West Michigan (FHCWM) conducted this analysis of Home Mortgage Disclosure Act (HMDA) data at the request of the Cities of Muskegon, Muskegon Heights, and Norton Shores (herein collectively “the Cities” or “Tri City region”) in order to address a recommendation in the “2015 Analysis of Impediments to Fair Housing Choice” completed for the County of Muskegon and the Cities. The recommendation, restated from the Cities’ “2009 Analysis of Impediments to Fair Housing Choice”, reads as follows:

2009 Banking & Investment Recommendation #1: Mortgage Data and Policy: We recommend that a full-scale analysis of HMDA data – and disparities based on race, ethnicity, and poverty – be completed, and used to identify policies and other areas that need improvement.

HMDA requires many financial institutions to maintain, report, and publicly disclose loan-level information about mortgages. These data help show whether lenders are serving the housing needs of their communities; they give public officials information that helps them make decisions and policies; and they shed light on lending patterns that could be discriminatory. The public data are modified to protect applicant and borrower privacy. This regulation applies to certain financial institutions, including banks, savings associations, credit unions, and other mortgage lending institutions.

To conduct this analysis, the FHCWM utilized the software LendingPatternsTM – Premier, a product of CLC Compliance Technologies Inc. The FHCWM generated reports in LendingPatternsTM derived from the 2017 HMDA-Loan Application Registry (LAR) data published by the Federal Financial Institutions Examination Council (FFIEC). All LendingPatternsTM reports utilized in this analysis are included as appendices. Any errors or omissions in this report are the responsibility of the Fair Housing Center of West Michigan.

Data controls: The FHCWM looked only at Home Purchase loans for the Property Type of 1-4 Family properties. Therefore, this analysis did not include Loan Purpose of Home Improvement or Refinance Loans, or loans for Property Type of Multi-family or Manufactured housing. Loan Types considered included Conventional, and those made or guaranteed by the Federal Housing Administration (FHA), Veterans Affairs (VA), and Farm Service Agency (FSA)/Department of Agriculture Rural Housing Service (RHS). Further, the FHCWM excluded the Action Taken “Purchased” to exclude loans purchased by an institution in order to limit analysis to loans purchased by individuals. Therefore, any reference herein to loans, applications, denials, originations, properties, etc. has been controlled by the aforementioned factors. Please see the appendices for more detailed information regarding the data parameters for each report.

HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Table of Contents Market Overview ..................................................................................................................1 - 9

Where loans were made ...................................................................................................1 Which borrowers got loans ...............................................................................................3 Which institutions were getting the most applications and making the most loans .............7 Why loans were not originated .........................................................................................10

Disparity Analysis .................................................................................................................11 - 12 Redlining Risk Factor .........................................................................................................11 Top 5 Lender’s Originations in Majority White and Majority Minority Census Tracts in the Tri City Region ......................................................................................................12

Primary Conclusions ............................................................................................................13 - 15

Recommendations ................................................................................................................16 - 18

Appendix A: LendingPatternsTM Lender’s HMDA Overview reports

Appendix B: LendingPatternsTM Population Penetration Profile (Hispanic not a race) reports

Appendix C: LendingPatternsTM Lender Market Share reports and Table of Branch Locations of Top 5 Lenders

Appendix D: LendingPatternsTM Denial Reason Distribution reports

Appendix E: LendingPatternsTM FFIEC Redlining Risk Factor R2 reports

Appendix F: LendingPatternsTM Rank Lenders by Community Lending Performance report

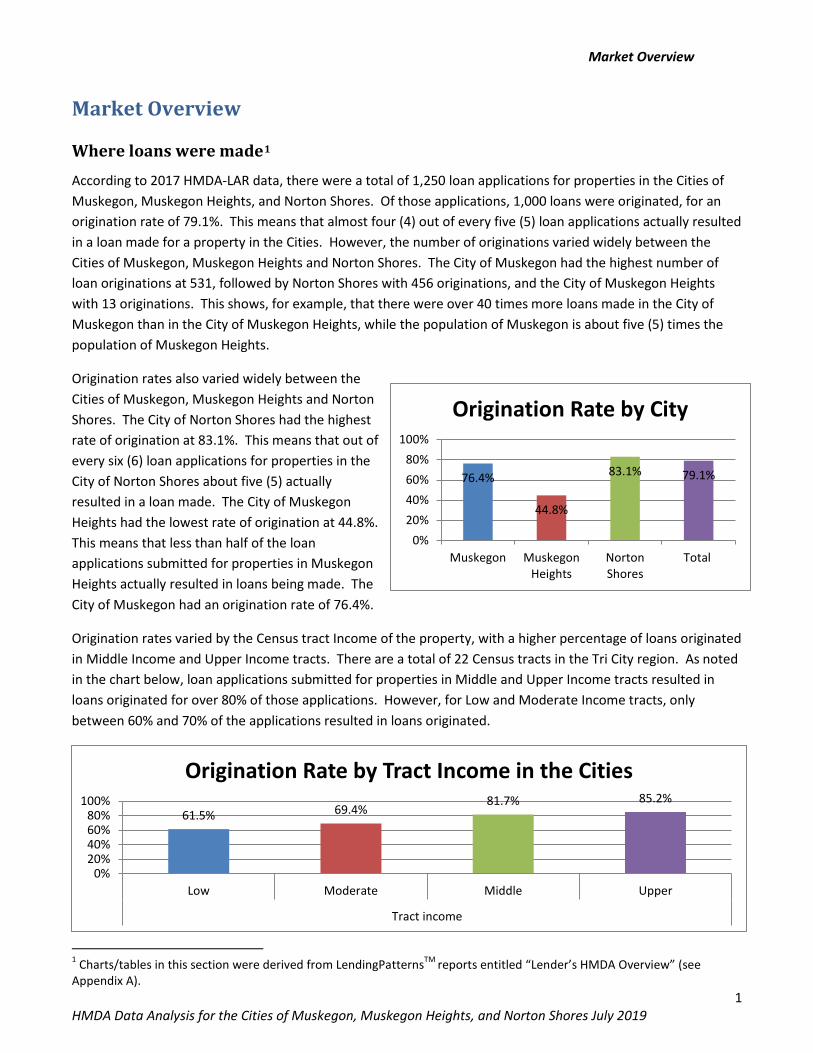

Market Overview

1 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

76.4%

44.8%

83.1% 79.1%

0%20%40%60%80%

100%

Muskegon MuskegonHeights

NortonShores

Total

Origination Rate by City

Market Overview

Where loans were made1 According to 2017 HMDA-LAR data, there were a total of 1,250 loan applications for properties in the Cities of Muskegon, Muskegon Heights, and Norton Shores. Of those applications, 1,000 loans were originated, for an origination rate of 79.1%. This means that almost four (4) out of every five (5) loan applications actually resulted in a loan made for a property in the Cities. However, the number of originations varied widely between the Cities of Muskegon, Muskegon Heights and Norton Shores. The City of Muskegon had the highest number of loan originations at 531, followed by Norton Shores with 456 originations, and the City of Muskegon Heights with 13 originations. This shows, for example, that there were over 40 times more loans made in the City of Muskegon than in the City of Muskegon Heights, while the population of Muskegon is about five (5) times the population of Muskegon Heights.

Origination rates also varied widely between the Cities of Muskegon, Muskegon Heights and Norton Shores. The City of Norton Shores had the highest rate of origination at 83.1%. This means that out of every six (6) loan applications for properties in the City of Norton Shores about five (5) actually resulted in a loan made. The City of Muskegon Heights had the lowest rate of origination at 44.8%. This means that less than half of the loan applications submitted for properties in Muskegon Heights actually resulted in loans being made. The City of Muskegon had an origination rate of 76.4%.

Origination rates varied by the Census tract Income of the property, with a higher percentage of loans originated in Middle Income and Upper Income tracts. There are a total of 22 Census tracts in the Tri City region. As noted in the chart below, loan applications submitted for properties in Middle and Upper Income tracts resulted in loans originated for over 80% of those applications. However, for Low and Moderate Income tracts, only between 60% and 70% of the applications resulted in loans originated.

1 Charts/tables in this section were derived from LendingPatternsTM reports entitled “Lender’s HMDA Overview” (see Appendix A).

61.5% 69.4% 81.7% 85.2%

0%20%40%60%80%

100%

Low Moderate Middle Upper

Tract income

Origination Rate by Tract Income in the Cities

Market Overview

2 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

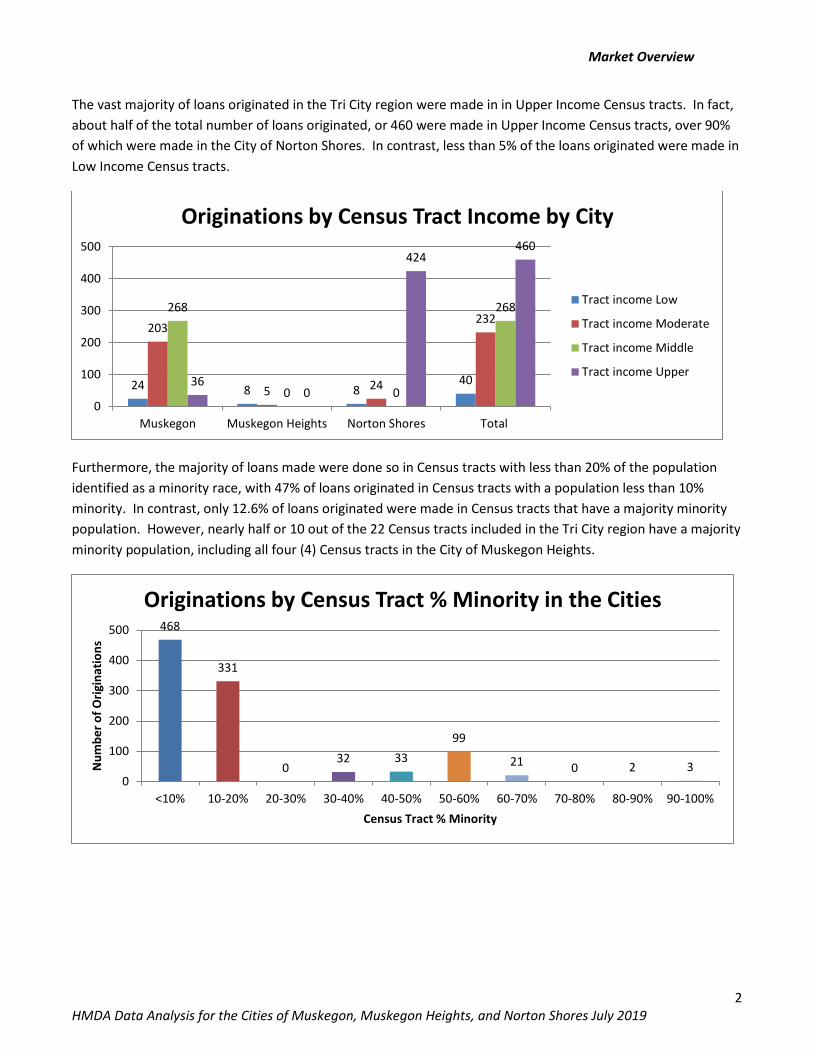

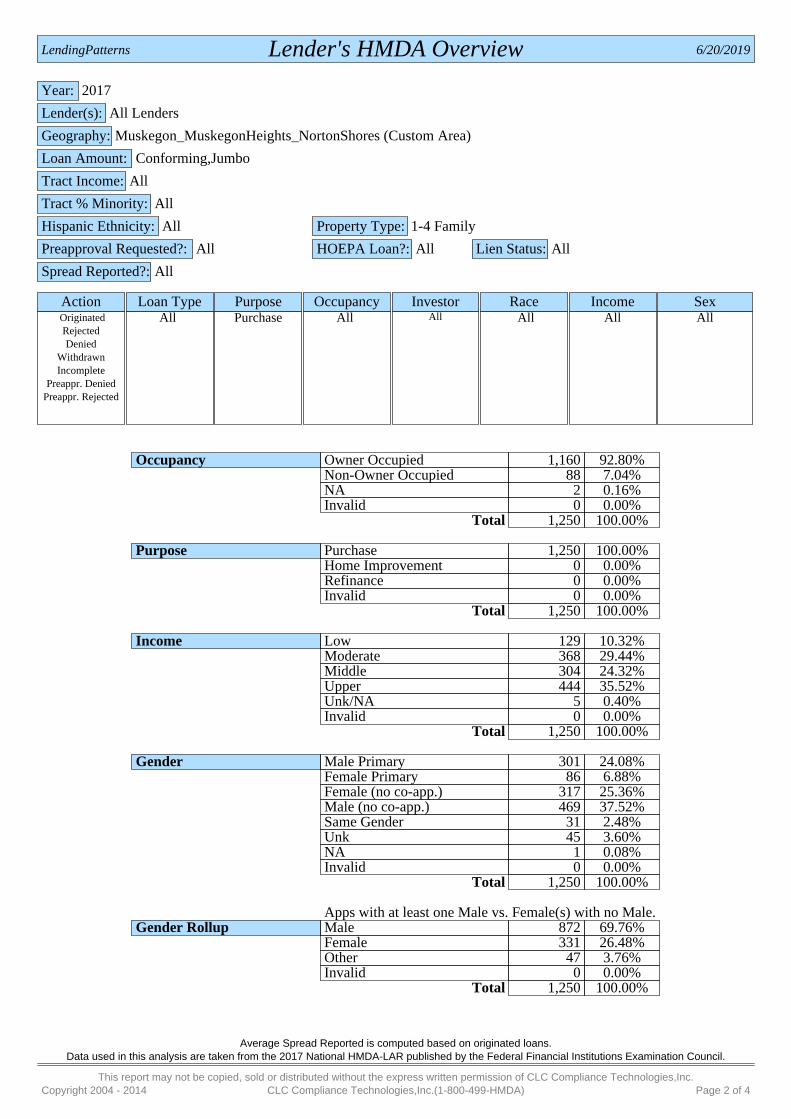

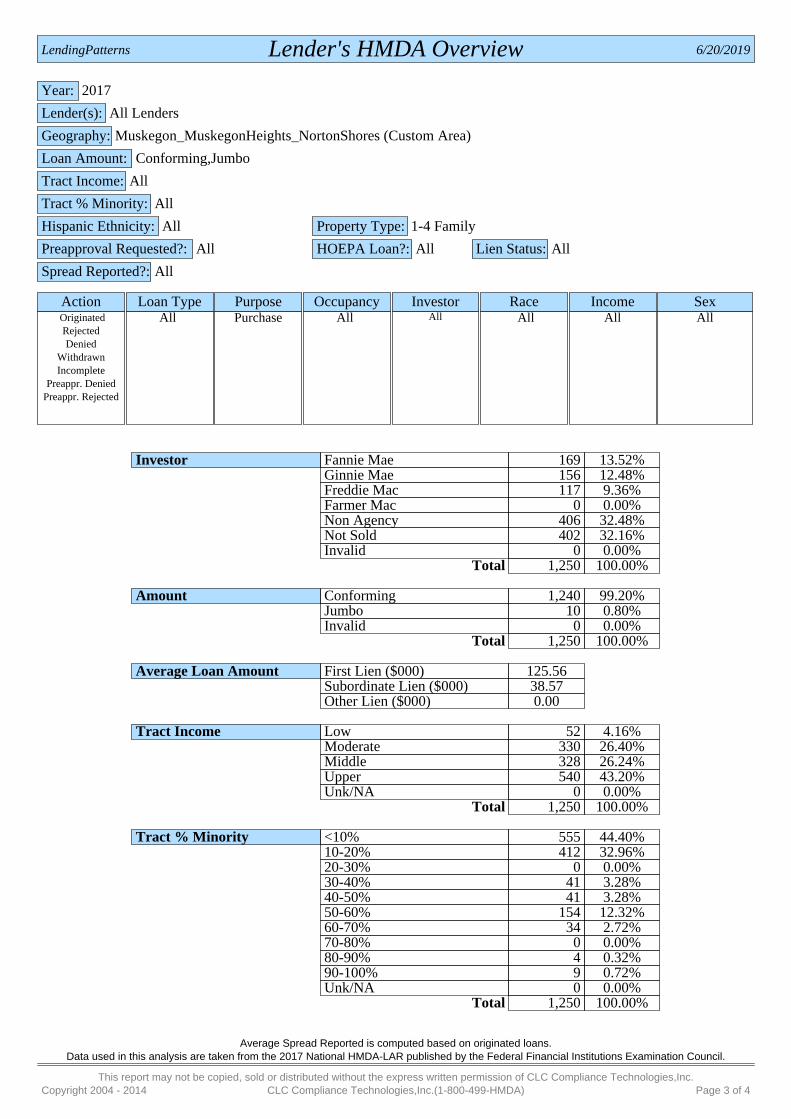

The vast majority of loans originated in the Tri City region were made in in Upper Income Census tracts. In fact, about half of the total number of loans originated, or 460 were made in Upper Income Census tracts, over 90% of which were made in the City of Norton Shores. In contrast, less than 5% of the loans originated were made in Low Income Census tracts.

Furthermore, the majority of loans made were done so in Census tracts with less than 20% of the population identified as a minority race, with 47% of loans originated in Census tracts with a population less than 10% minority. In contrast, only 12.6% of loans originated were made in Census tracts that have a majority minority population. However, nearly half or 10 out of the 22 Census tracts included in the Tri City region have a majority minority population, including all four (4) Census tracts in the City of Muskegon Heights.

24 8 8 40

203

5 24

232 268

0 0

268

36 0

424 460

0

100

200

300

400

500

Muskegon Muskegon Heights Norton Shores Total

Originations by Census Tract Income by City

Tract income Low

Tract income Moderate

Tract income Middle

Tract income Upper

468

331

0 32 33

99

21 0 2 3 0

100

200

300

400

500

<10% 10-20% 20-30% 30-40% 40-50% 50-60% 60-70% 70-80% 80-90% 90-100%

Num

ber o

f Orig

inat

ions

Census Tract % Minority

Originations by Census Tract % Minority in the Cities

Market Overview

3 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

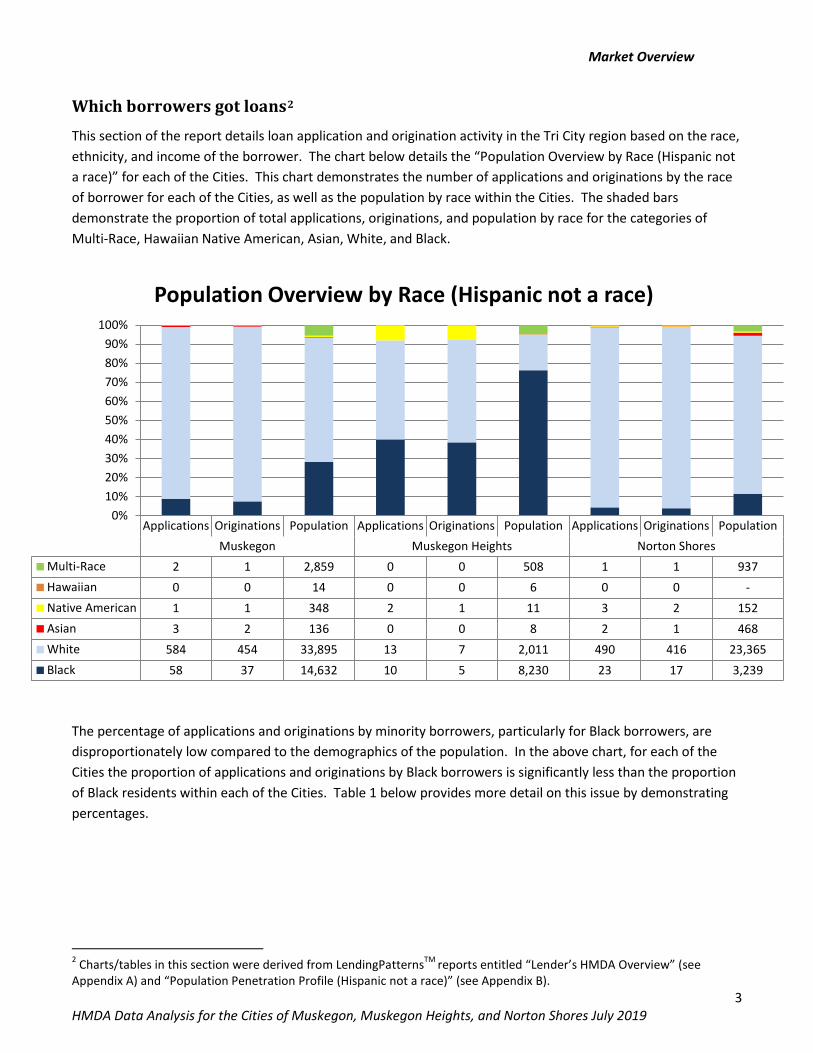

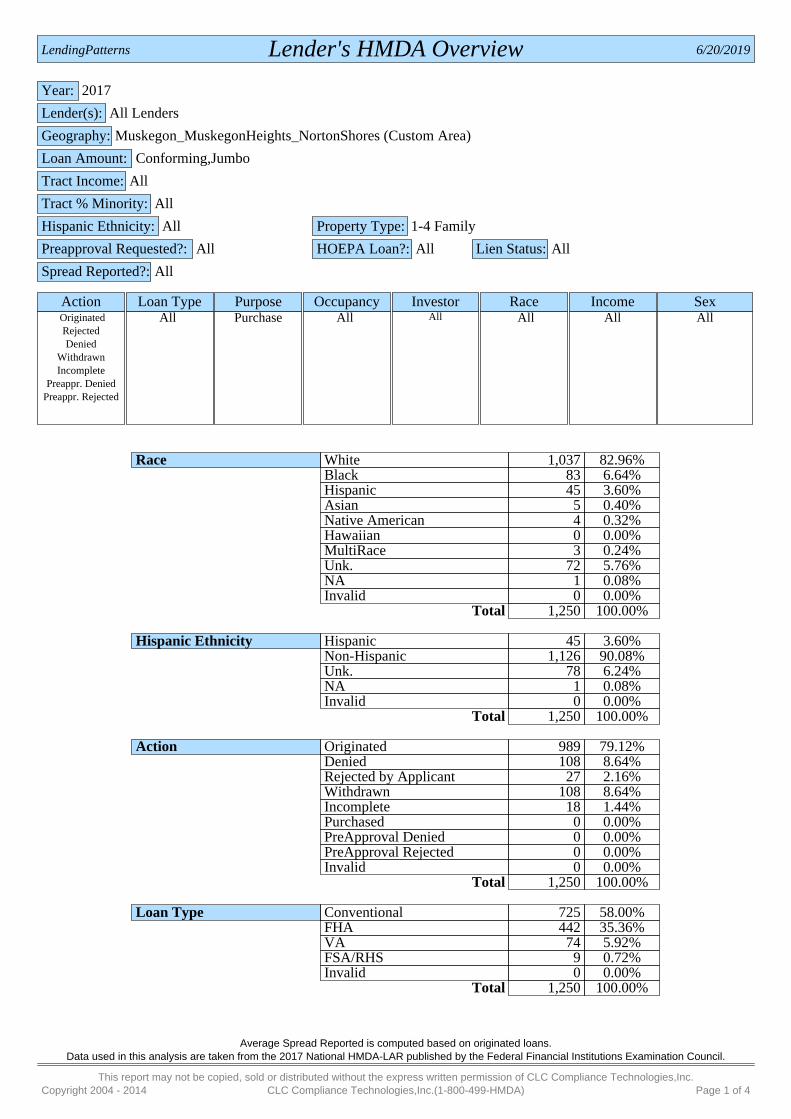

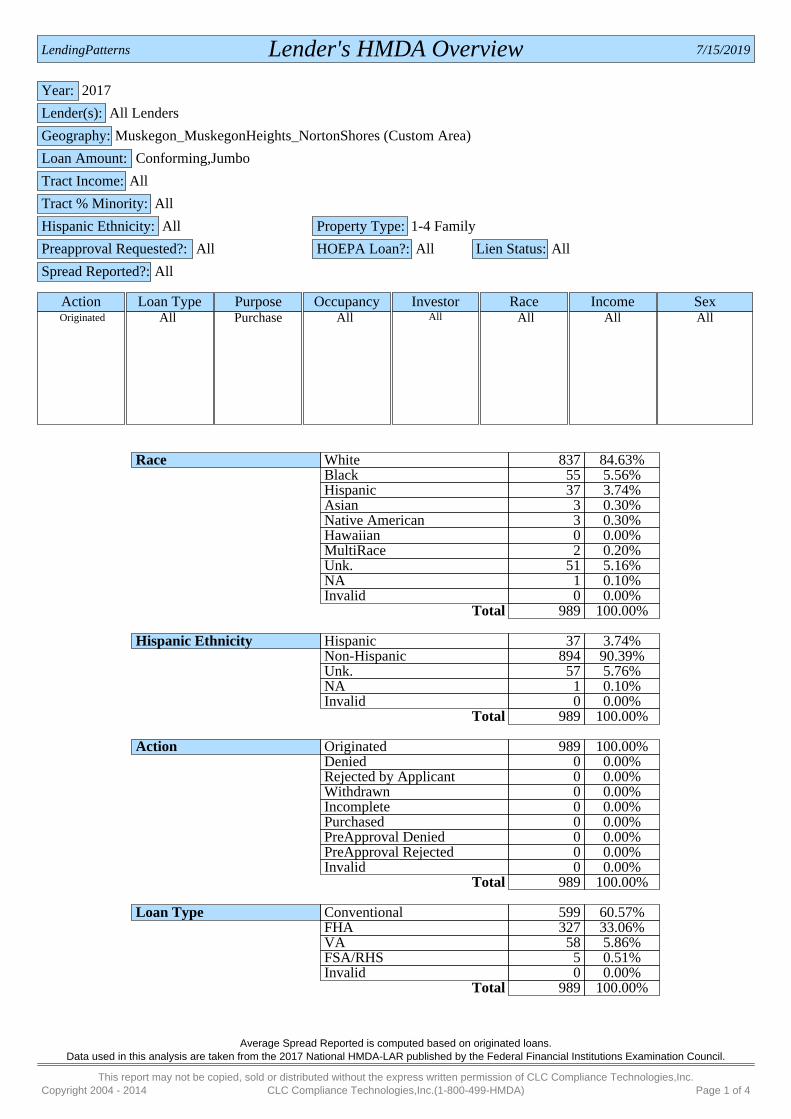

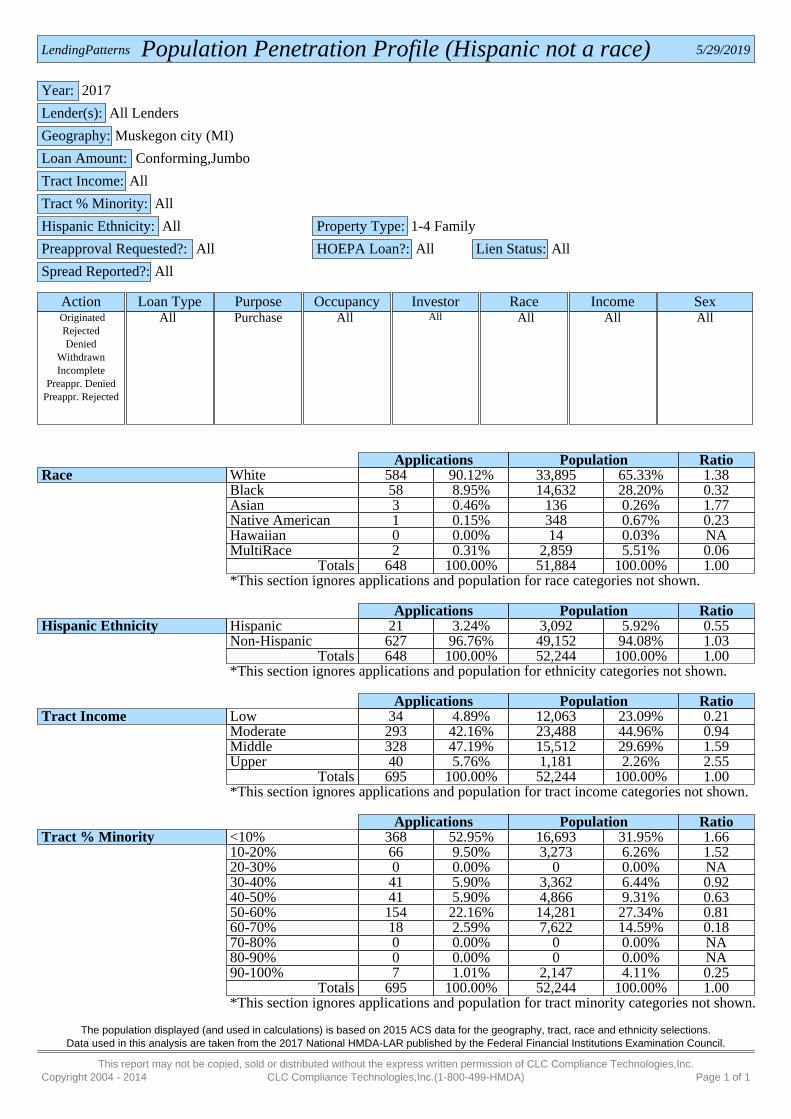

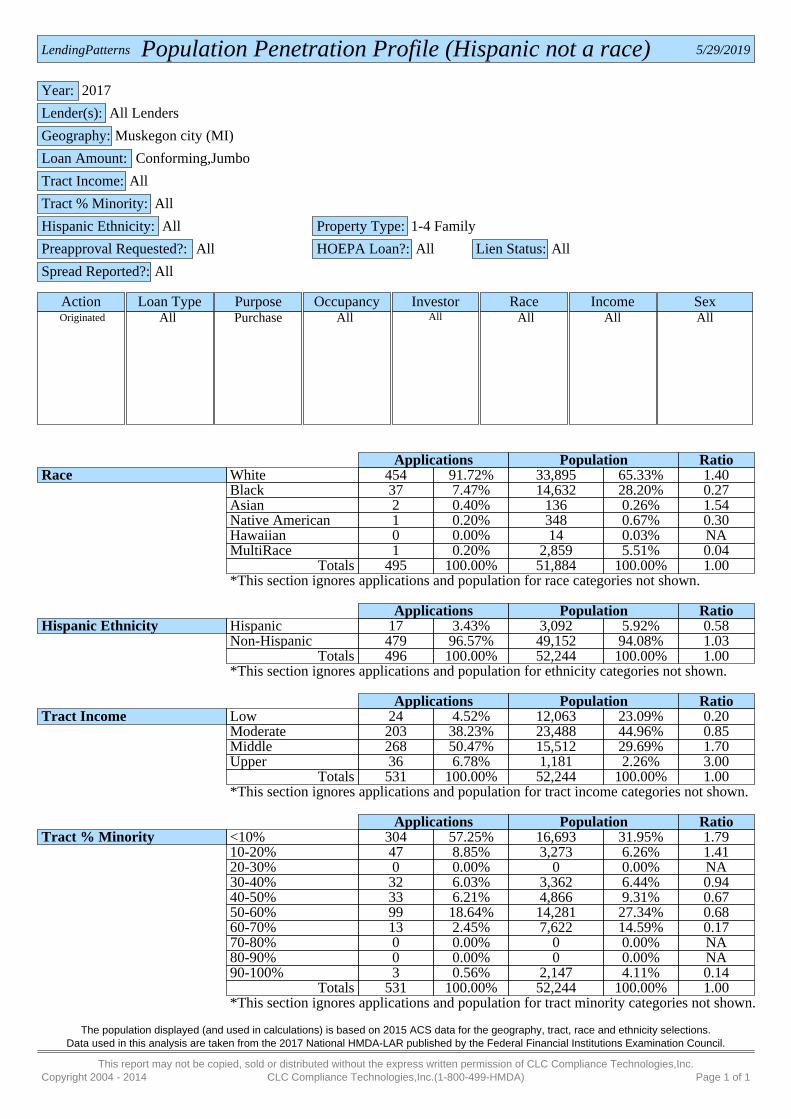

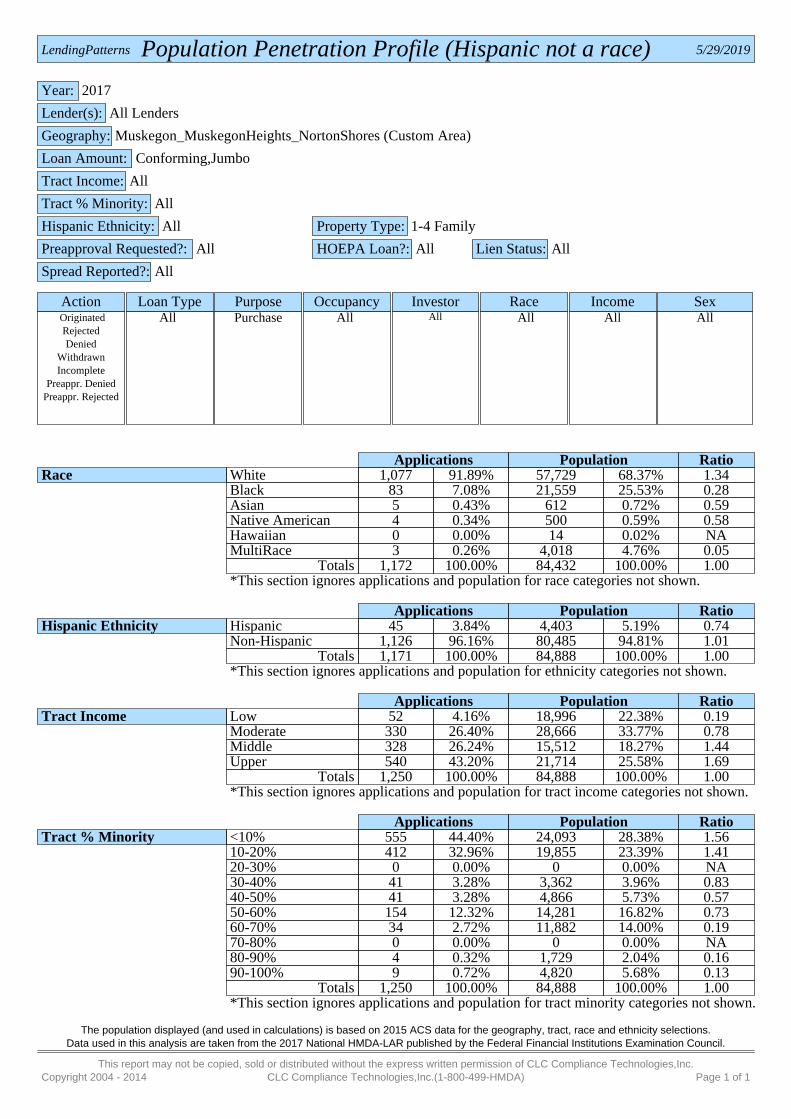

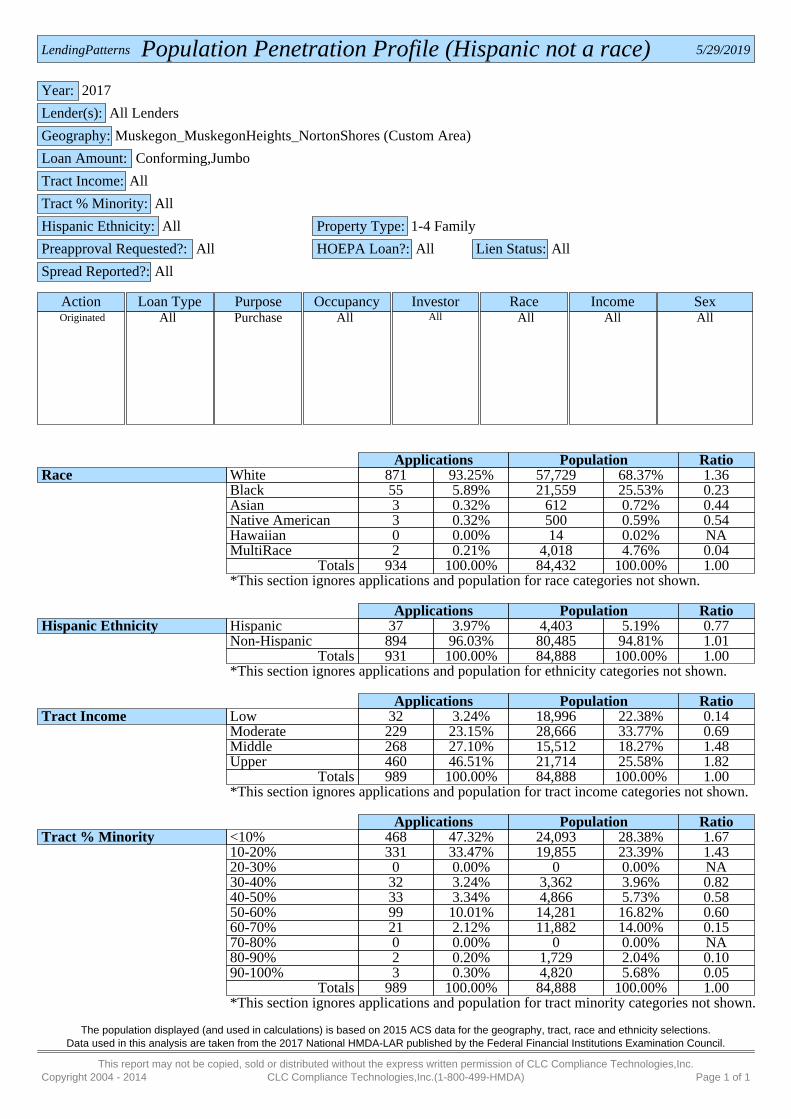

Which borrowers got loans2 This section of the report details loan application and origination activity in the Tri City region based on the race, ethnicity, and income of the borrower. The chart below details the “Population Overview by Race (Hispanic not a race)” for each of the Cities. This chart demonstrates the number of applications and originations by the race of borrower for each of the Cities, as well as the population by race within the Cities. The shaded bars demonstrate the proportion of total applications, originations, and population by race for the categories of Multi-Race, Hawaiian Native American, Asian, White, and Black.

The percentage of applications and originations by minority borrowers, particularly for Black borrowers, are disproportionately low compared to the demographics of the population. In the above chart, for each of the Cities the proportion of applications and originations by Black borrowers is significantly less than the proportion of Black residents within each of the Cities. Table 1 below provides more detail on this issue by demonstrating percentages.

2 Charts/tables in this section were derived from LendingPatternsTM reports entitled “Lender’s HMDA Overview” (see Appendix A) and “Population Penetration Profile (Hispanic not a race)” (see Appendix B).

Applications Originations Population Applications Originations Population Applications Originations PopulationMuskegon Muskegon Heights Norton Shores

Multi-Race 2 1 2,859 0 0 508 1 1 937Hawaiian 0 0 14 0 0 6 0 0 -Native American 1 1 348 2 1 11 3 2 152Asian 3 2 136 0 0 8 2 1 468White 584 454 33,895 13 7 2,011 490 416 23,365Black 58 37 14,632 10 5 8,230 23 17 3,239

0%10%20%30%40%50%60%70%80%90%

100%

Population Overview by Race (Hispanic not a race)

Market Overview

4 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

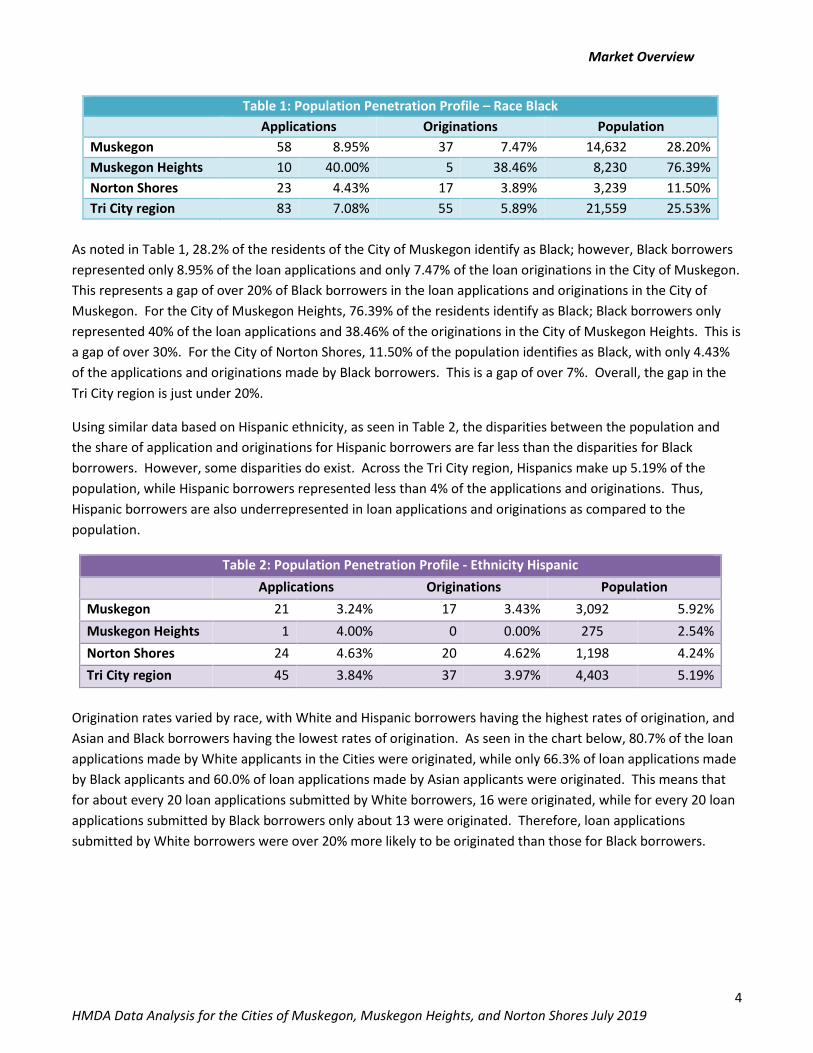

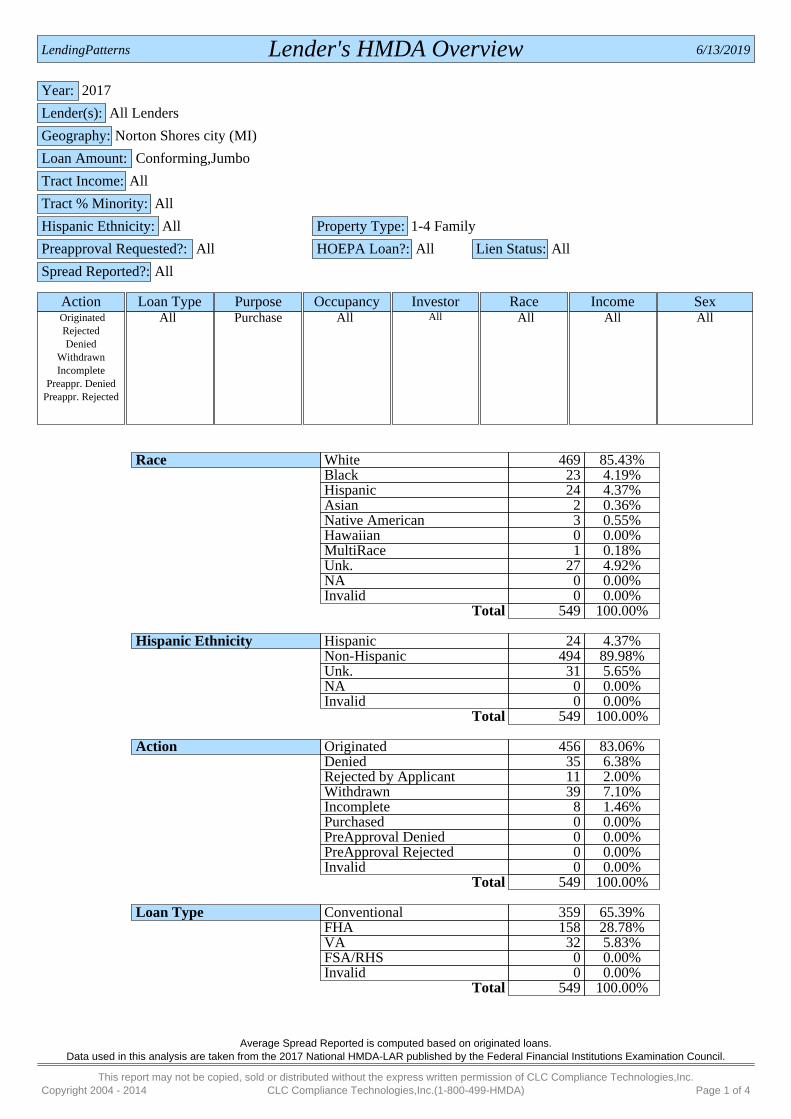

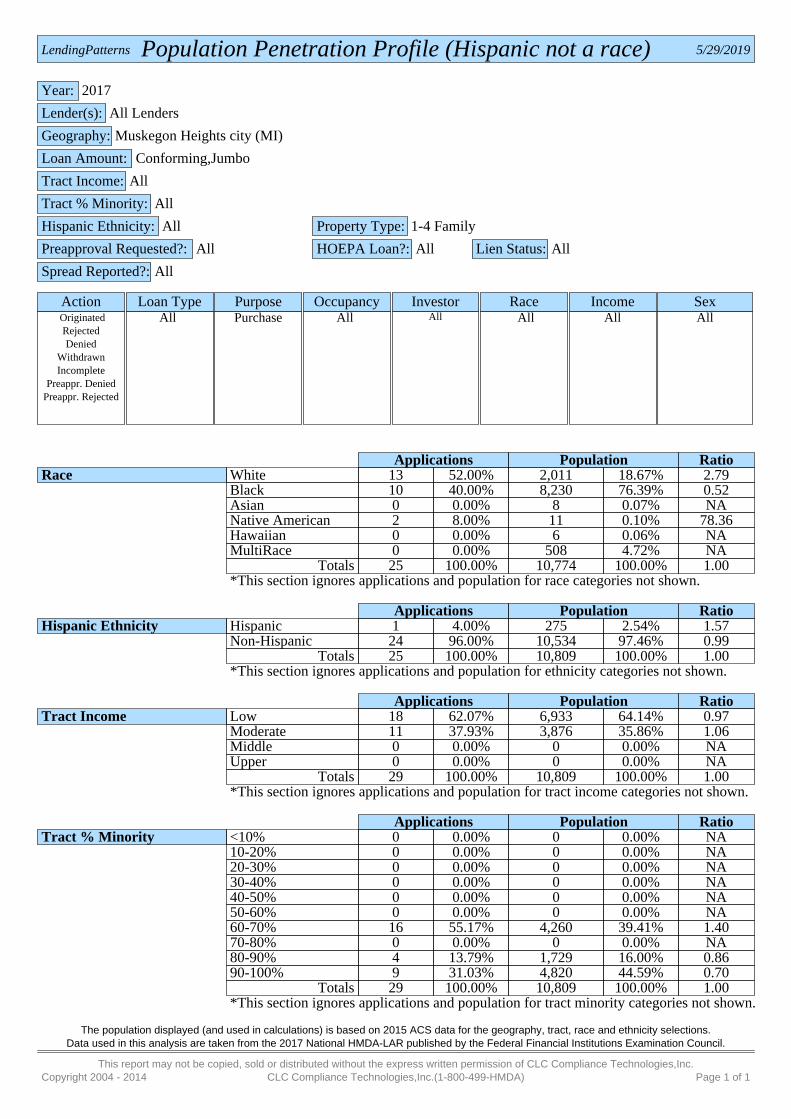

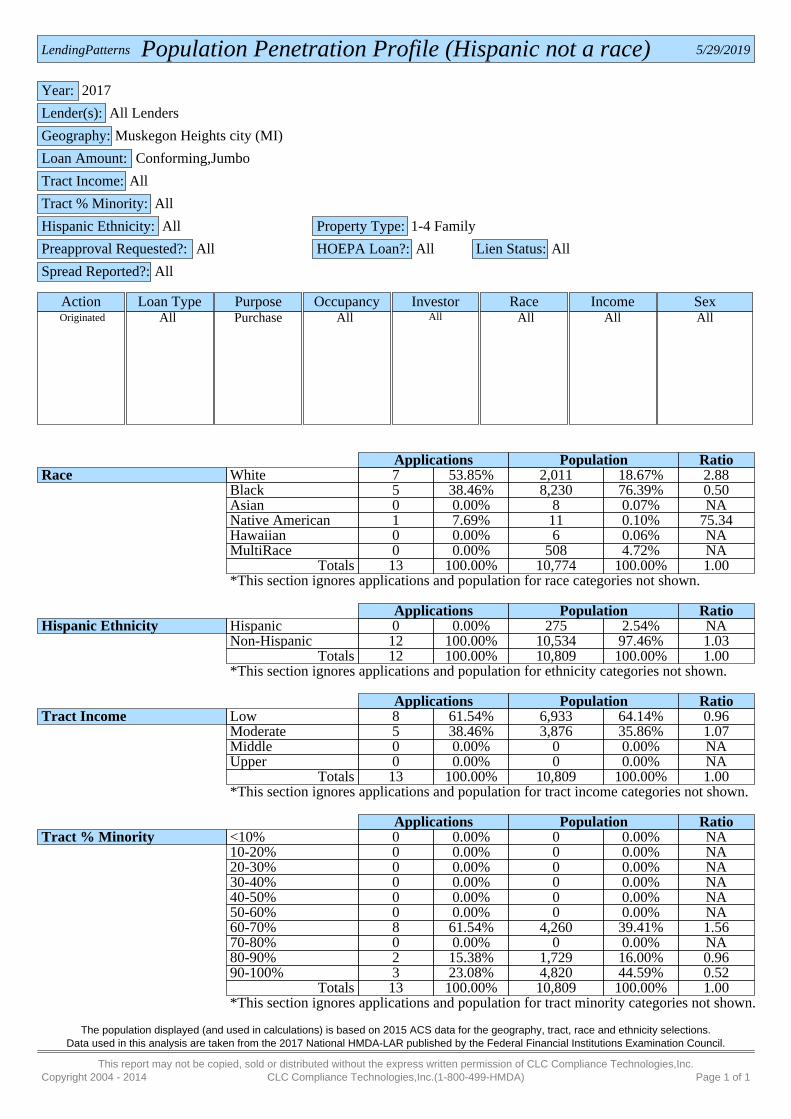

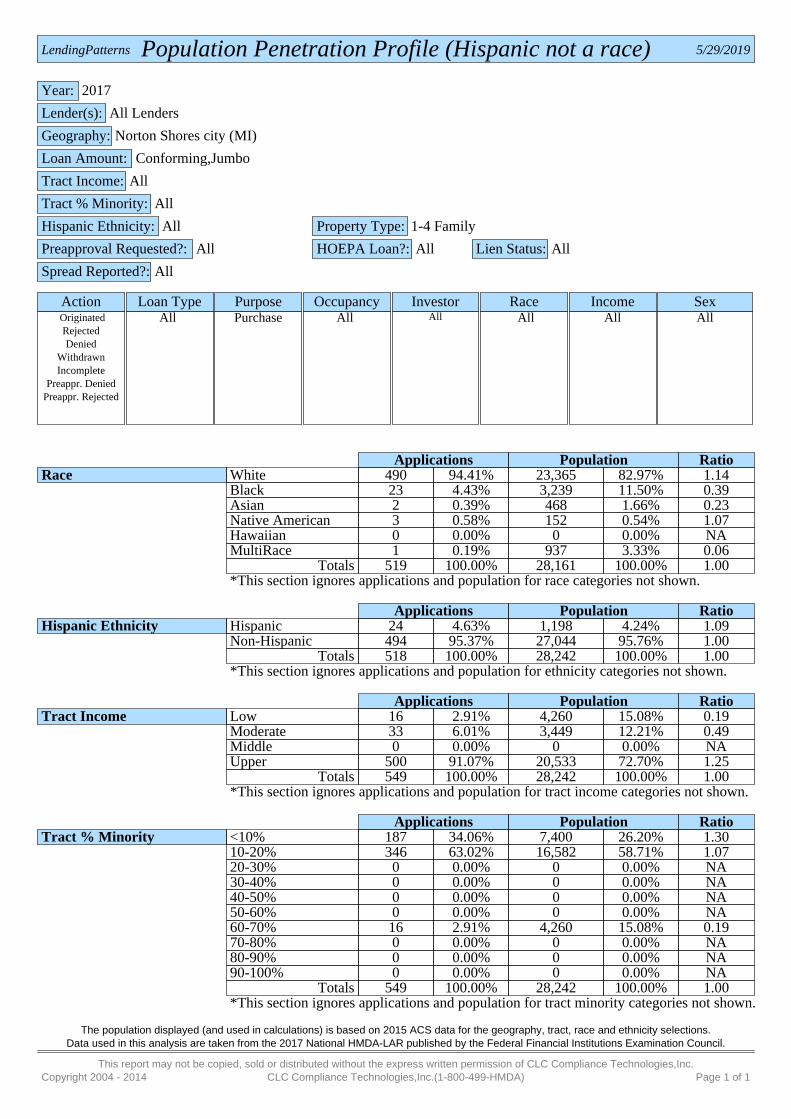

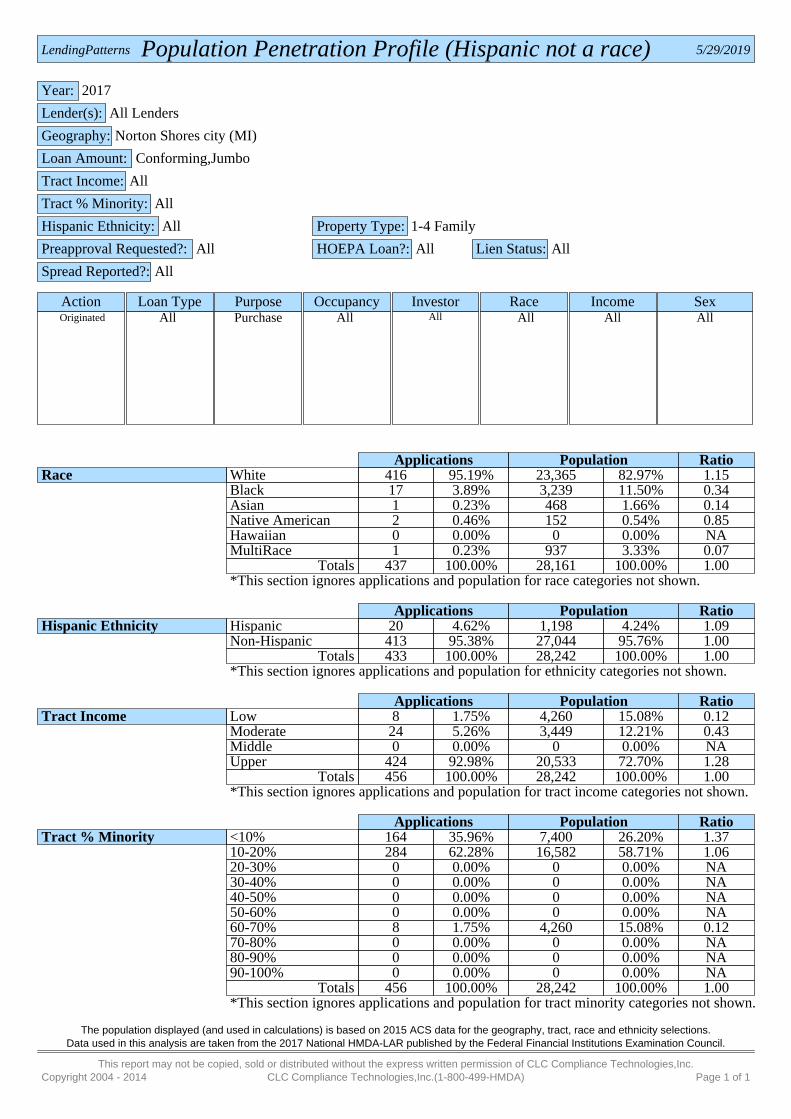

Table 1: Population Penetration Profile – Race Black Applications Originations Population Muskegon 58 8.95% 37 7.47% 14,632 28.20% Muskegon Heights 10 40.00% 5 38.46% 8,230 76.39% Norton Shores 23 4.43% 17 3.89% 3,239 11.50% Tri City region 83 7.08% 55 5.89% 21,559 25.53%

As noted in Table 1, 28.2% of the residents of the City of Muskegon identify as Black; however, Black borrowers represented only 8.95% of the loan applications and only 7.47% of the loan originations in the City of Muskegon. This represents a gap of over 20% of Black borrowers in the loan applications and originations in the City of Muskegon. For the City of Muskegon Heights, 76.39% of the residents identify as Black; Black borrowers only represented 40% of the loan applications and 38.46% of the originations in the City of Muskegon Heights. This is a gap of over 30%. For the City of Norton Shores, 11.50% of the population identifies as Black, with only 4.43% of the applications and originations made by Black borrowers. This is a gap of over 7%. Overall, the gap in the Tri City region is just under 20%.

Using similar data based on Hispanic ethnicity, as seen in Table 2, the disparities between the population and the share of application and originations for Hispanic borrowers are far less than the disparities for Black borrowers. However, some disparities do exist. Across the Tri City region, Hispanics make up 5.19% of the population, while Hispanic borrowers represented less than 4% of the applications and originations. Thus, Hispanic borrowers are also underrepresented in loan applications and originations as compared to the population.

Table 2: Population Penetration Profile - Ethnicity Hispanic Applications Originations Population Muskegon 21 3.24% 17 3.43% 3,092 5.92% Muskegon Heights 1 4.00% 0 0.00% 275 2.54% Norton Shores 24 4.63% 20 4.62% 1,198 4.24% Tri City region 45 3.84% 37 3.97% 4,403 5.19%

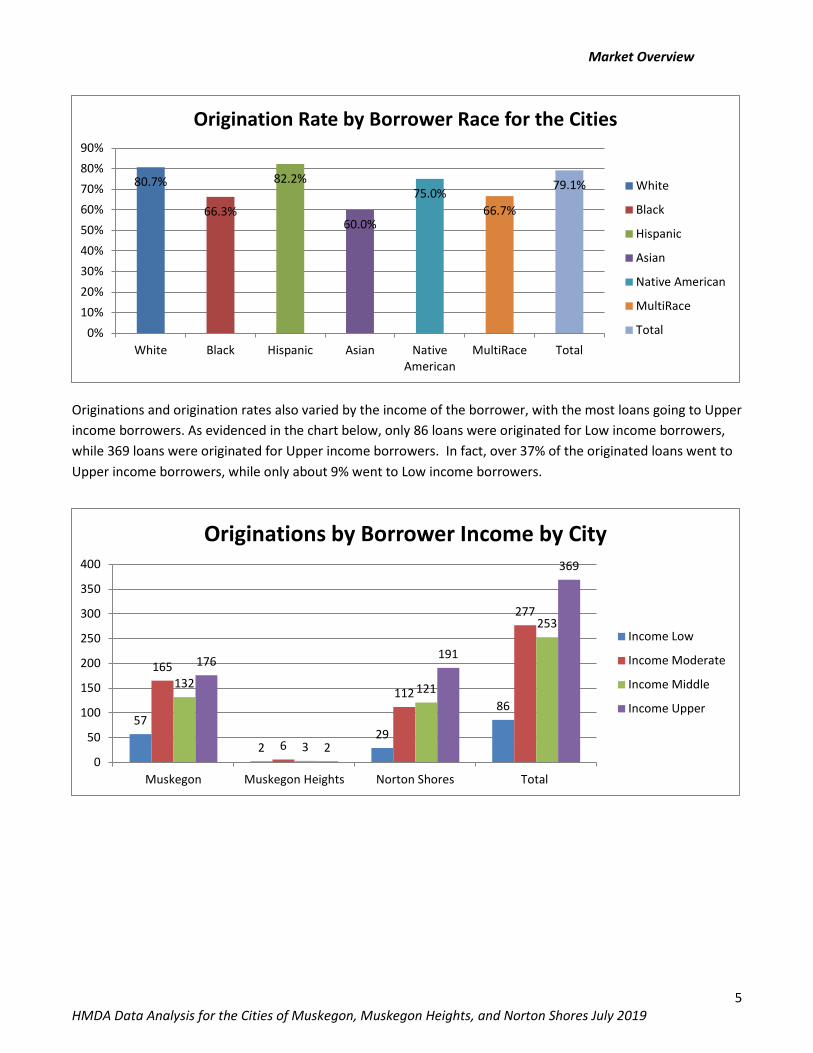

Origination rates varied by race, with White and Hispanic borrowers having the highest rates of origination, and Asian and Black borrowers having the lowest rates of origination. As seen in the chart below, 80.7% of the loan applications made by White applicants in the Cities were originated, while only 66.3% of loan applications made by Black applicants and 60.0% of loan applications made by Asian applicants were originated. This means that for about every 20 loan applications submitted by White borrowers, 16 were originated, while for every 20 loan applications submitted by Black borrowers only about 13 were originated. Therefore, loan applications submitted by White borrowers were over 20% more likely to be originated than those for Black borrowers.

Market Overview

5 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

57

2 29

86

165

6

112

277

132

3

121

253

176

2

191

369

0

50

100

150

200

250

300

350

400

Muskegon Muskegon Heights Norton Shores Total

Originations by Borrower Income by City

Income Low

Income Moderate

Income Middle

Income Upper

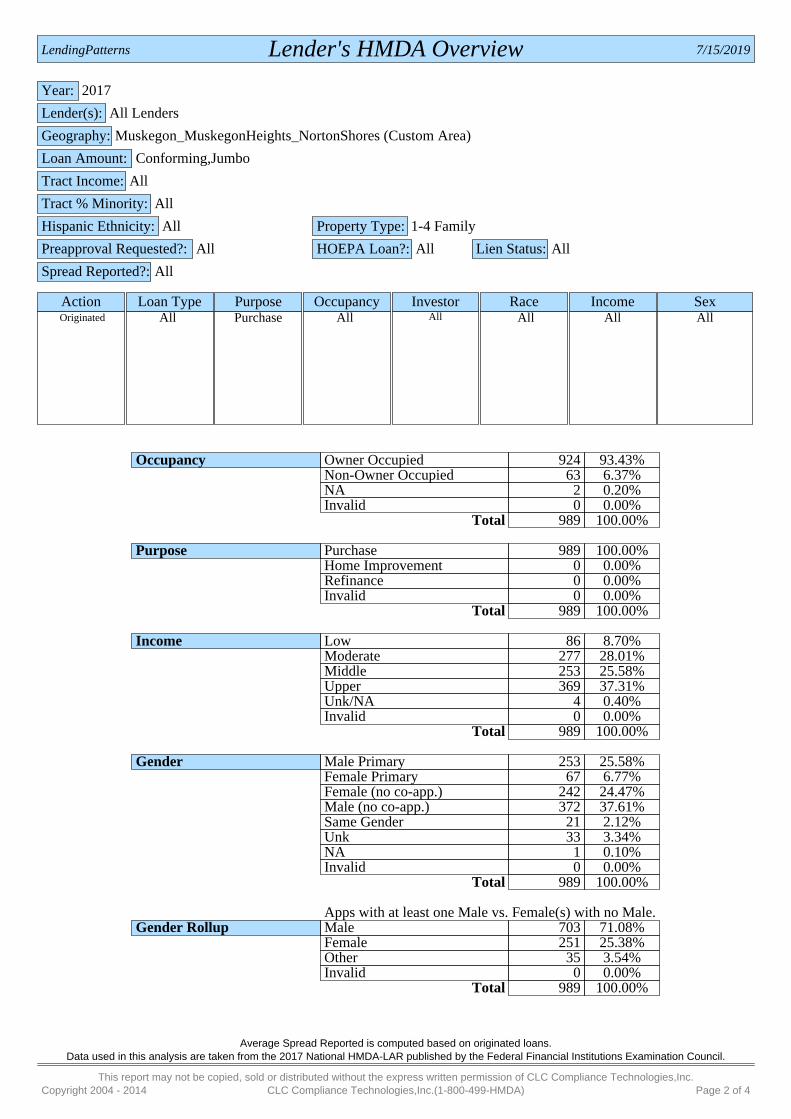

Originations and origination rates also varied by the income of the borrower, with the most loans going to Upper income borrowers. As evidenced in the chart below, only 86 loans were originated for Low income borrowers, while 369 loans were originated for Upper income borrowers. In fact, over 37% of the originated loans went to Upper income borrowers, while only about 9% went to Low income borrowers.

80.7%

66.3%

82.2%

60.0%

75.0% 66.7%

79.1%

0%10%20%30%40%50%60%70%80%90%

White Black Hispanic Asian NativeAmerican

MultiRace Total

Origination Rate by Borrower Race for the Cities

White

Black

Hispanic

Asian

Native American

MultiRace

Total

Market Overview

6 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

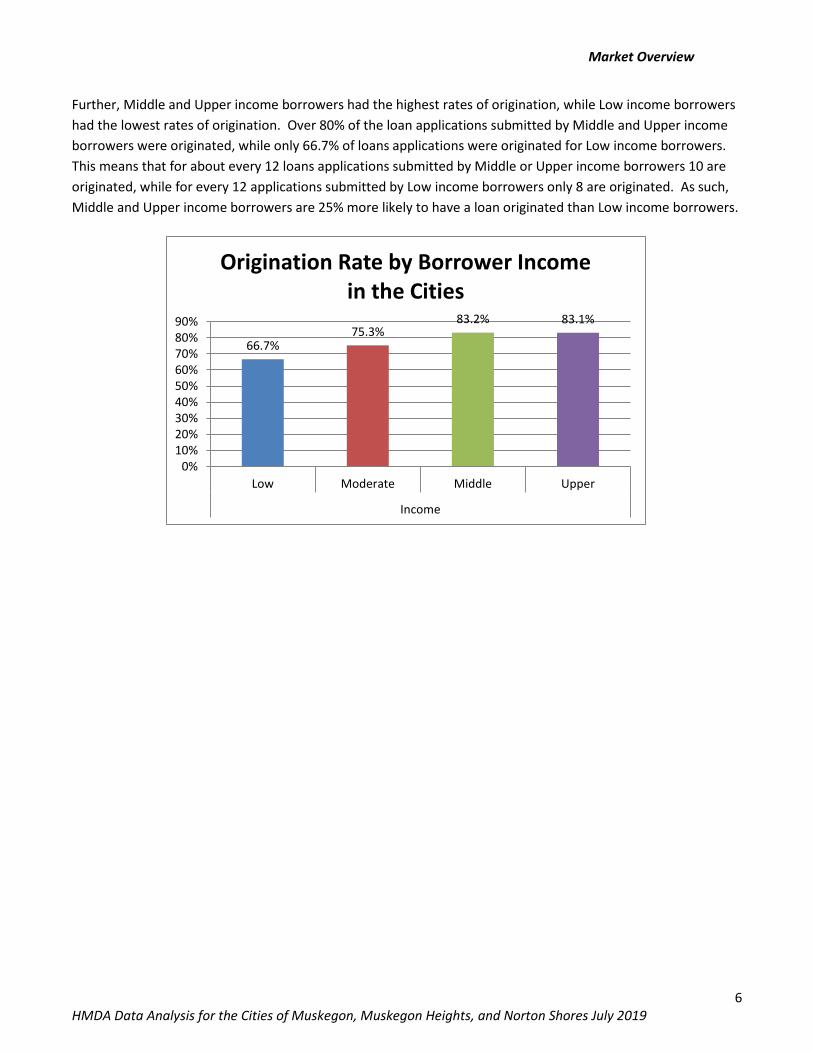

66.7% 75.3%

83.2% 83.1%

0%10%20%30%40%50%60%70%80%90%

Low Moderate Middle Upper

Income

Origination Rate by Borrower Income in the Cities

Further, Middle and Upper income borrowers had the highest rates of origination, while Low income borrowers had the lowest rates of origination. Over 80% of the loan applications submitted by Middle and Upper income borrowers were originated, while only 66.7% of loans applications were originated for Low income borrowers. This means that for about every 12 loans applications submitted by Middle or Upper income borrowers 10 are originated, while for every 12 applications submitted by Low income borrowers only 8 are originated. As such, Middle and Upper income borrowers are 25% more likely to have a loan originated than Low income borrowers.

Market Overview

7 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

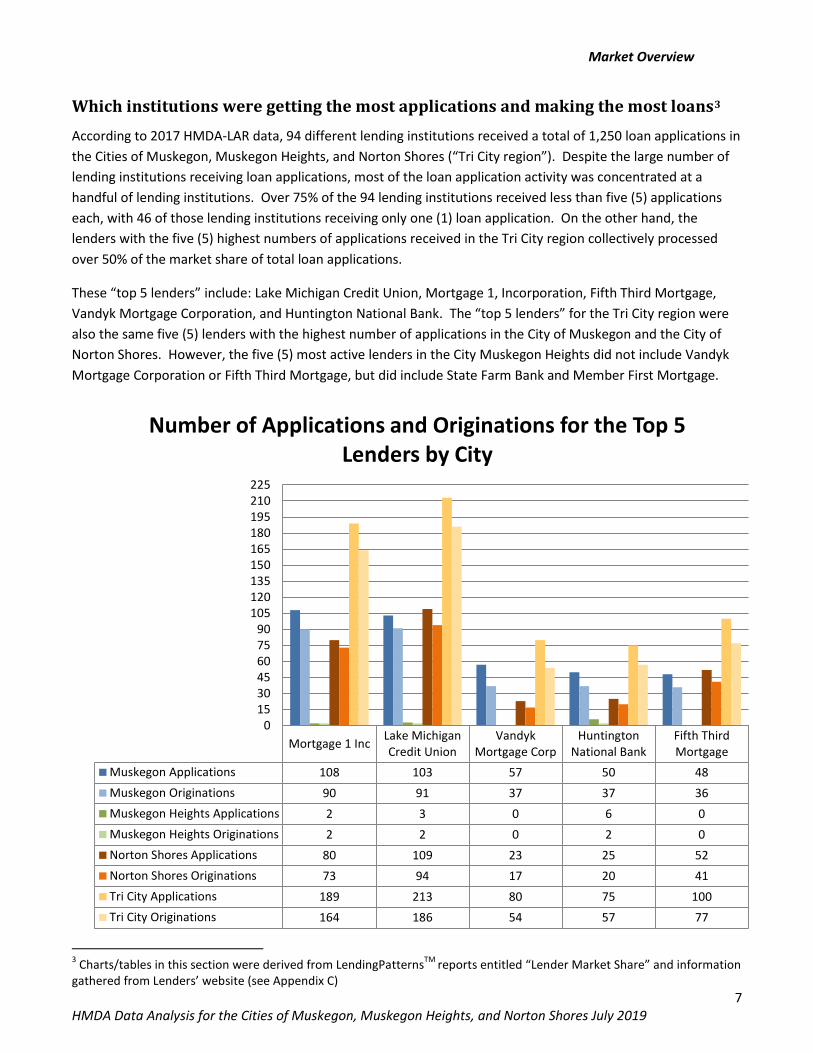

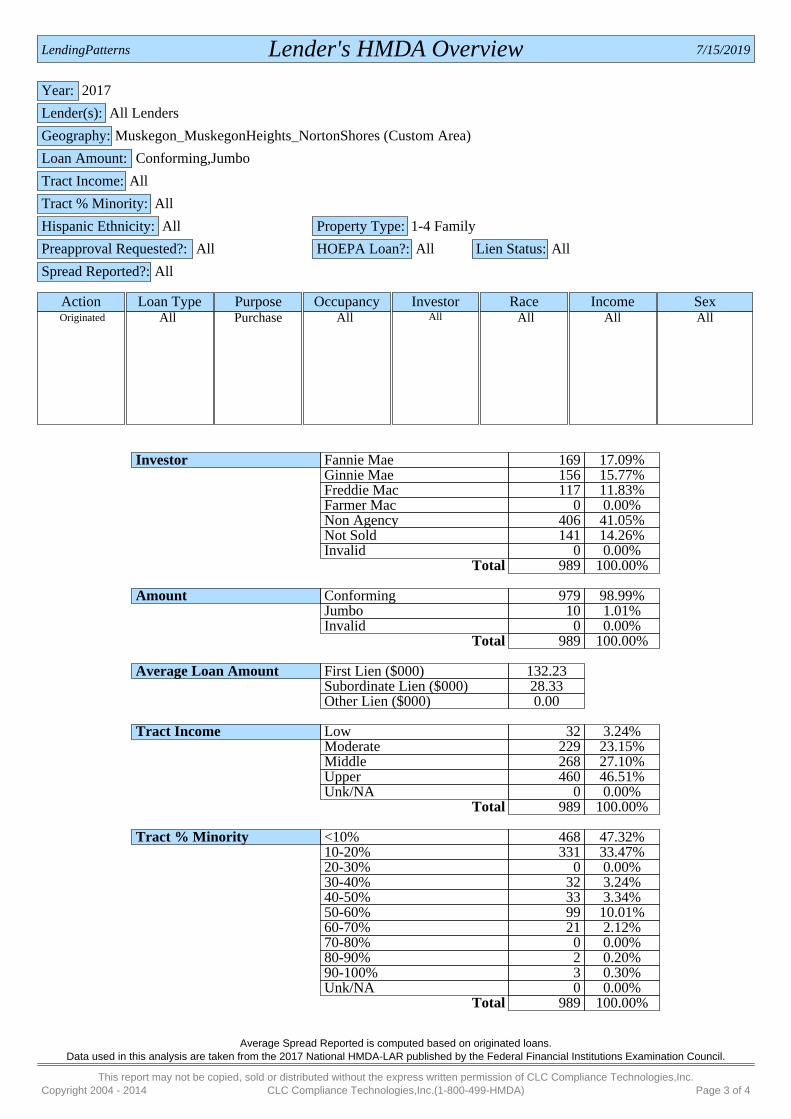

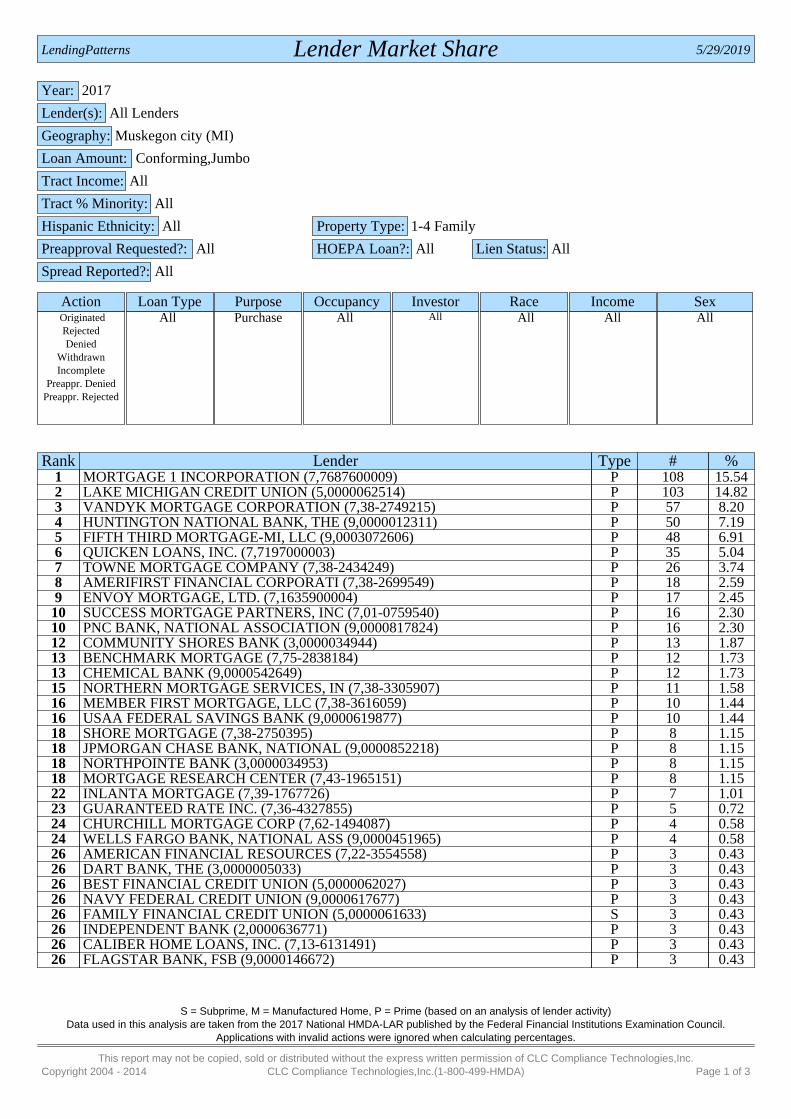

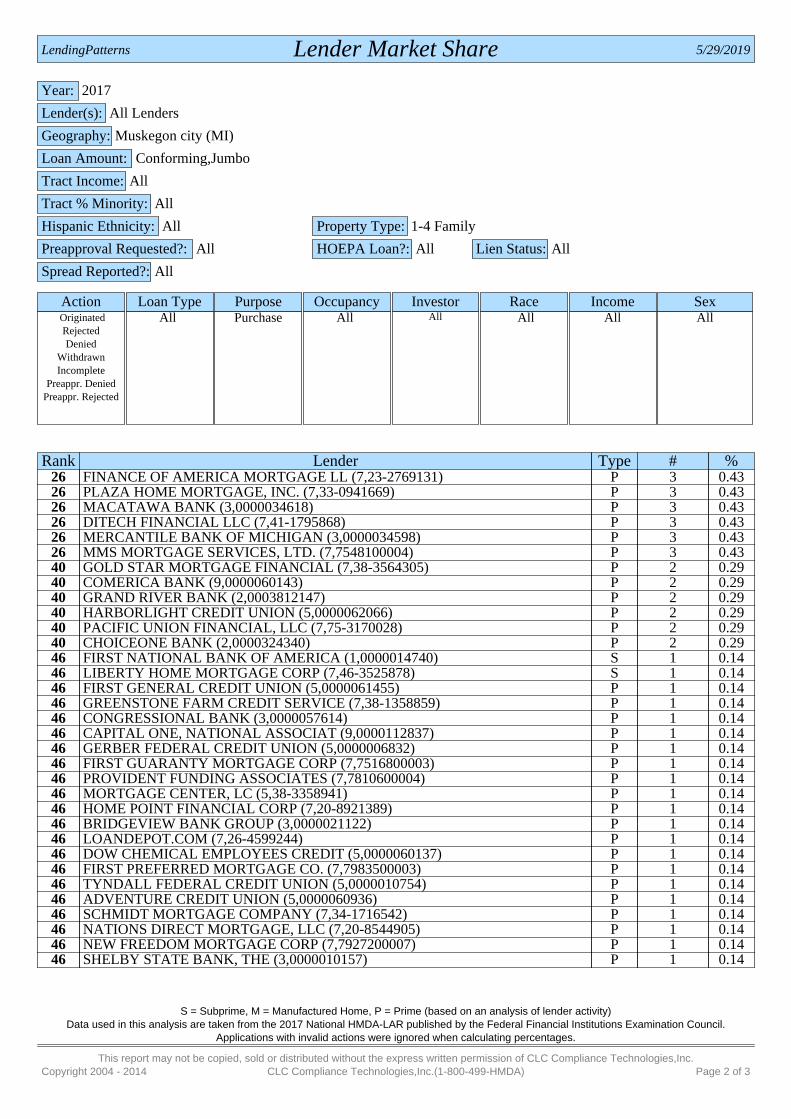

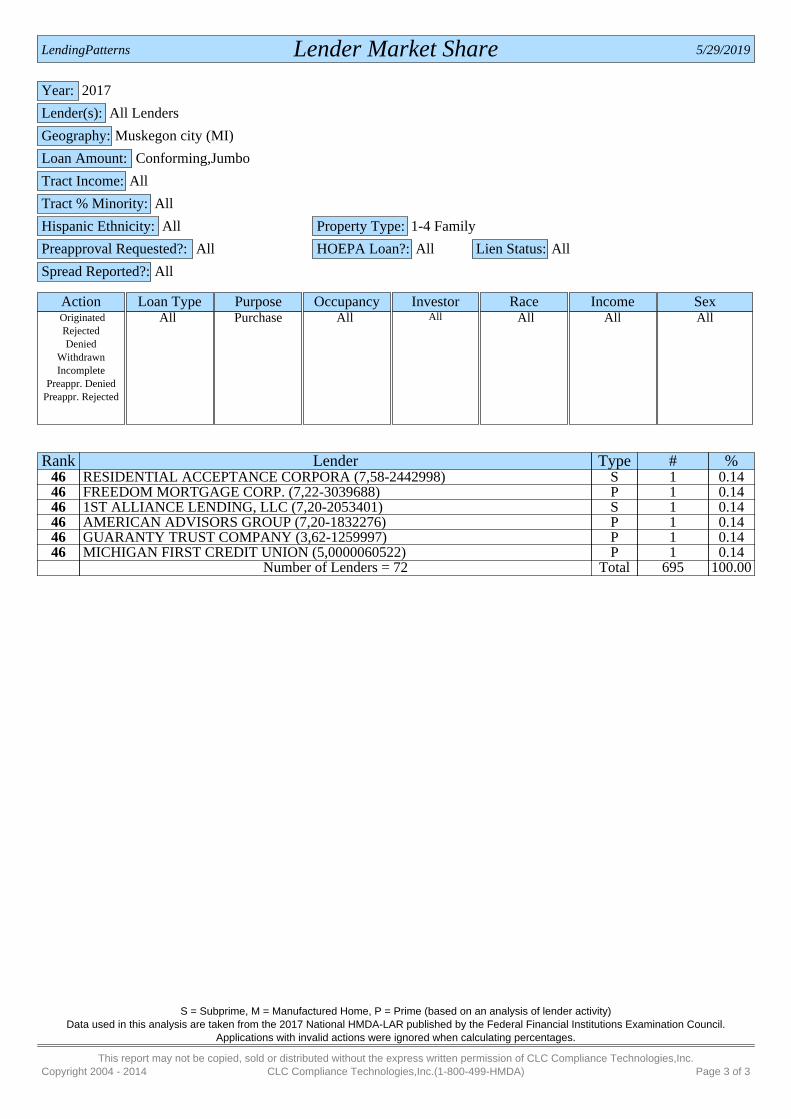

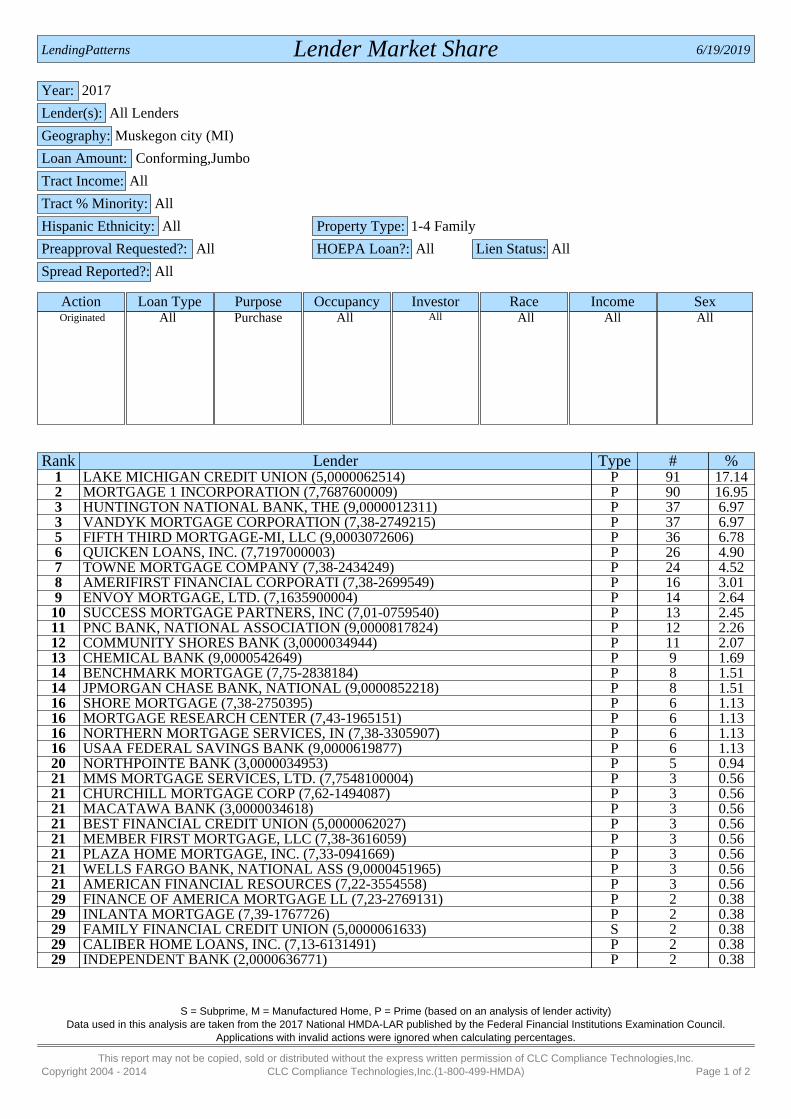

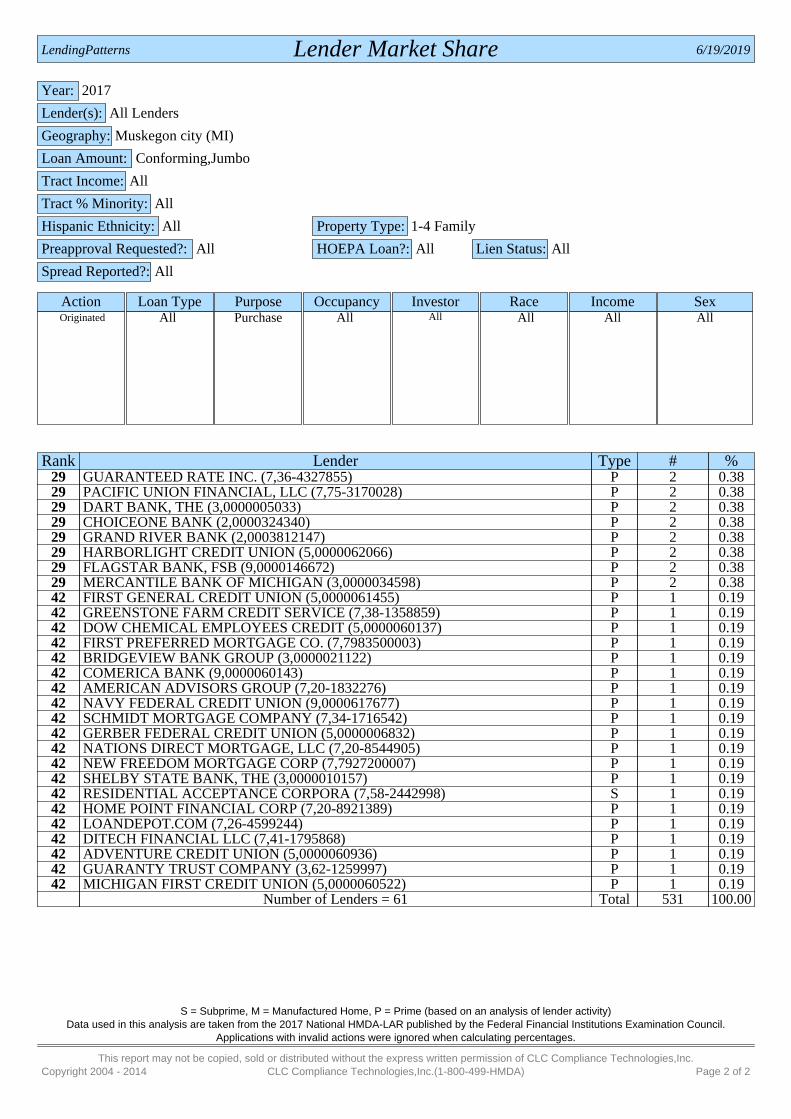

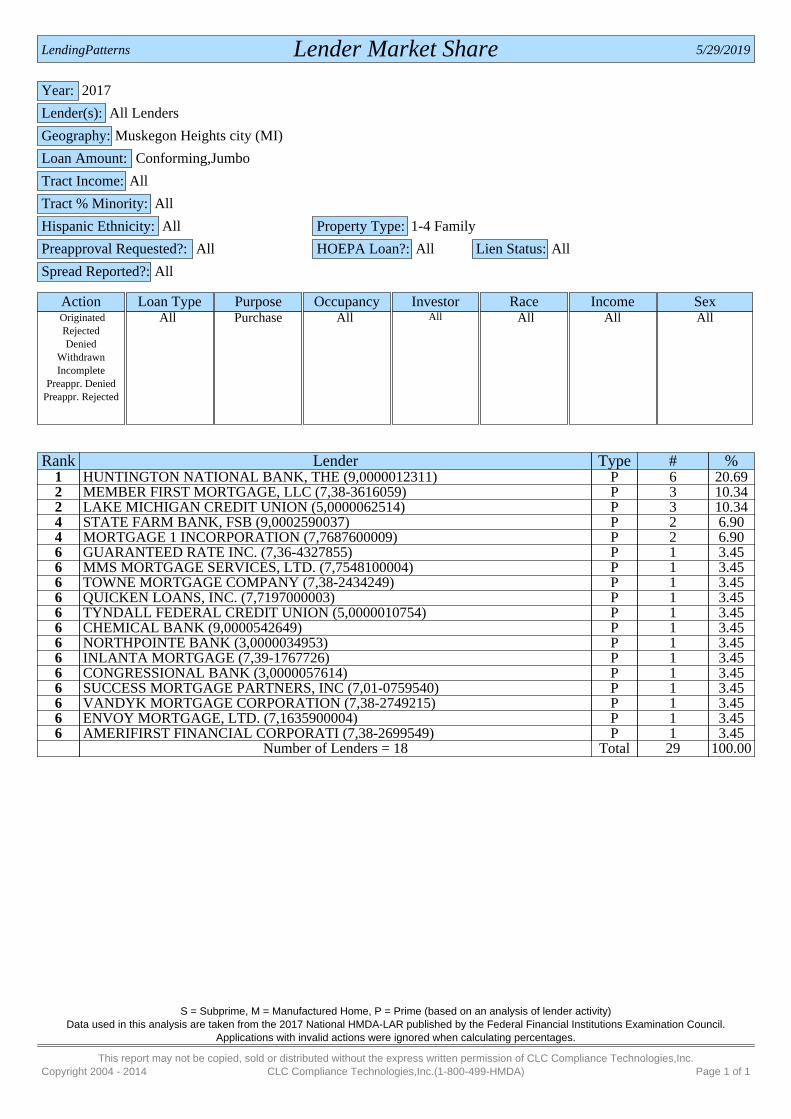

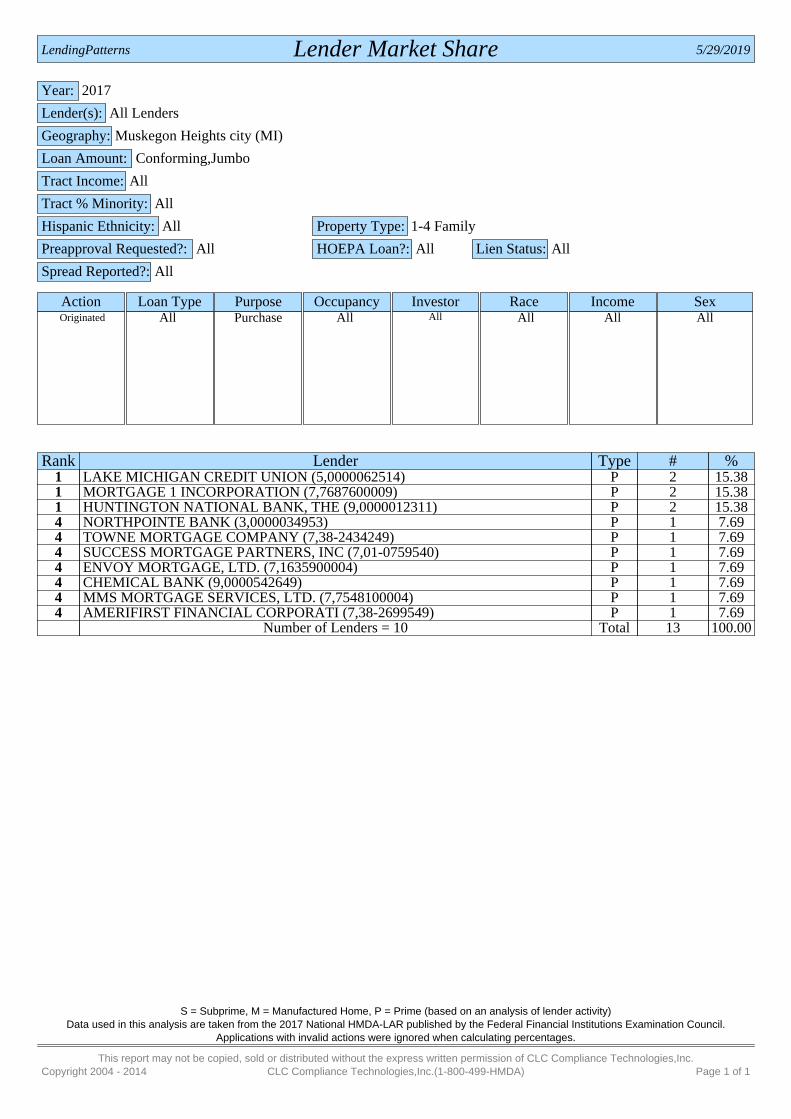

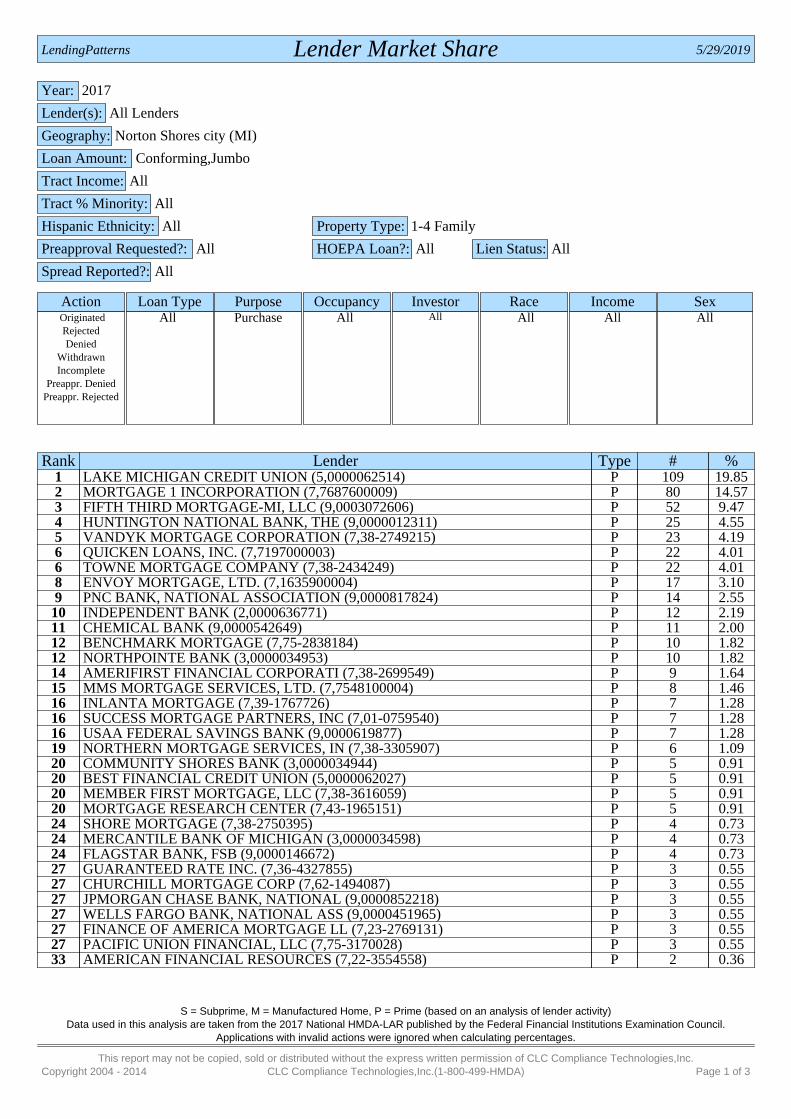

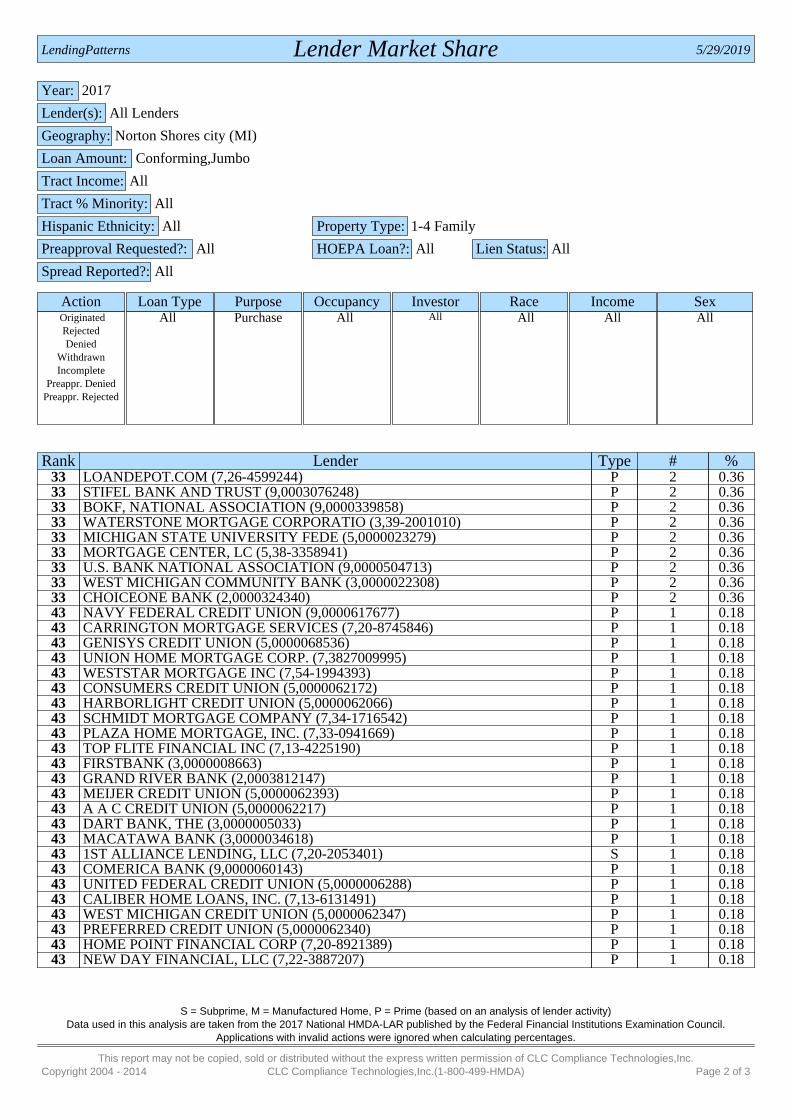

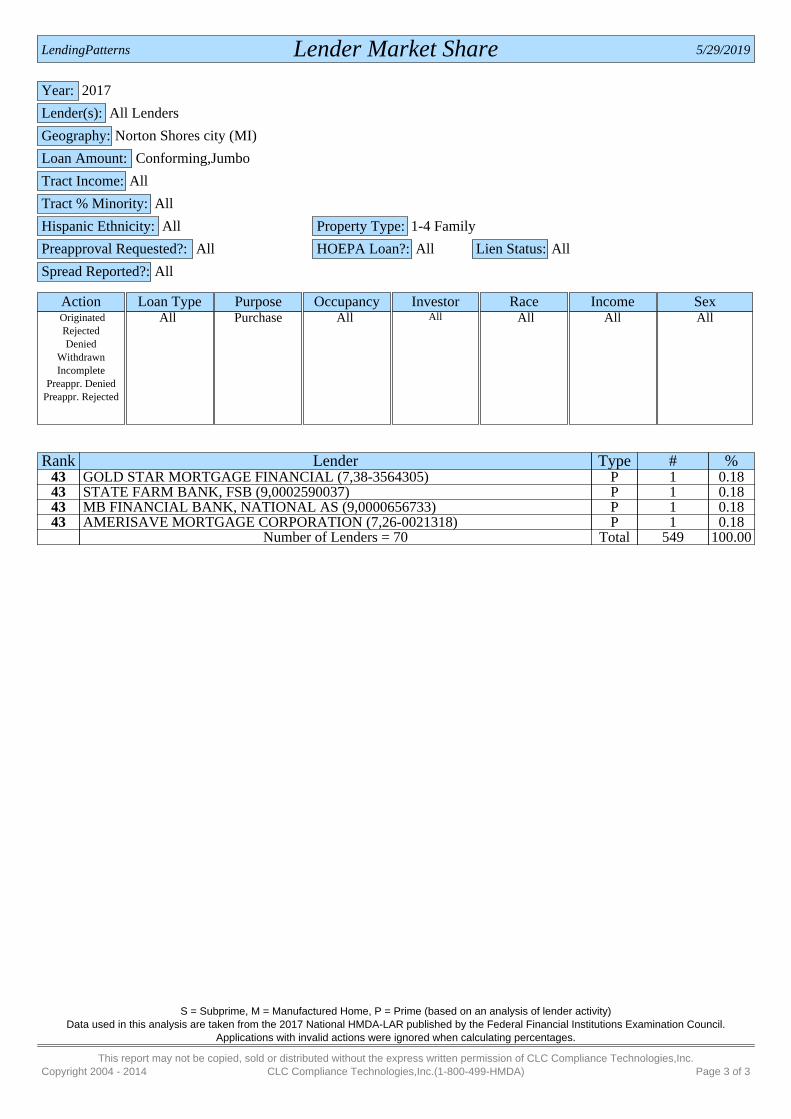

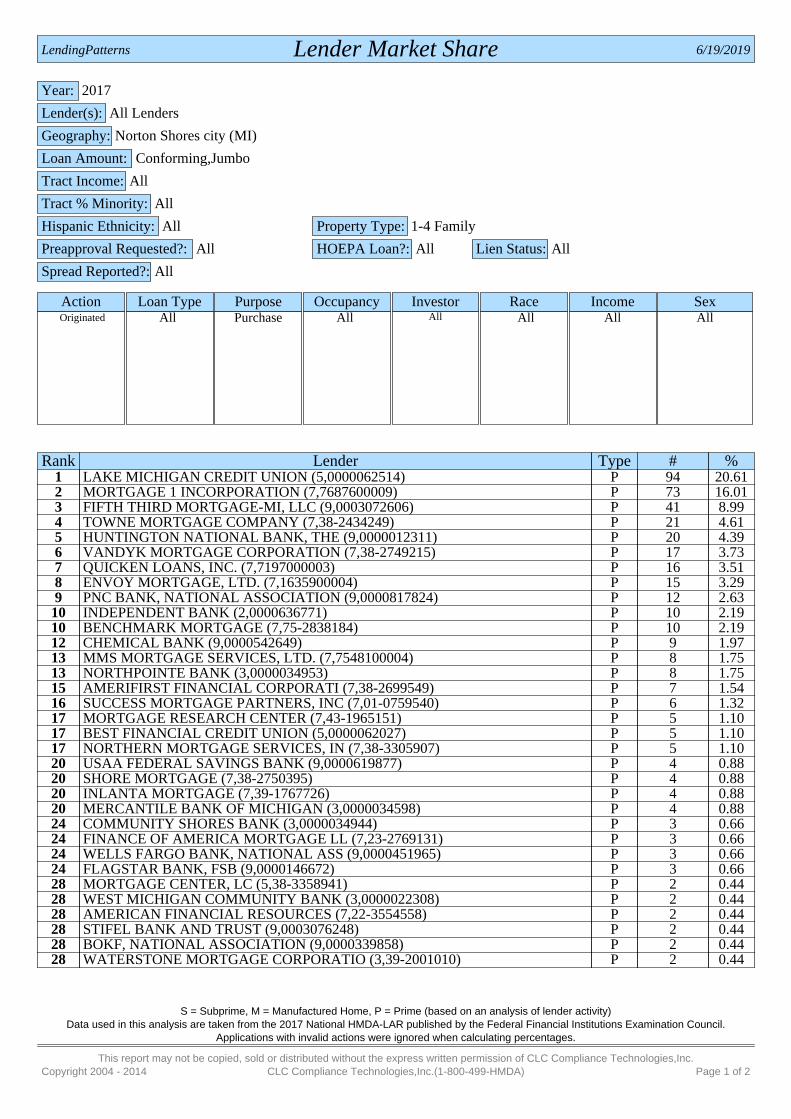

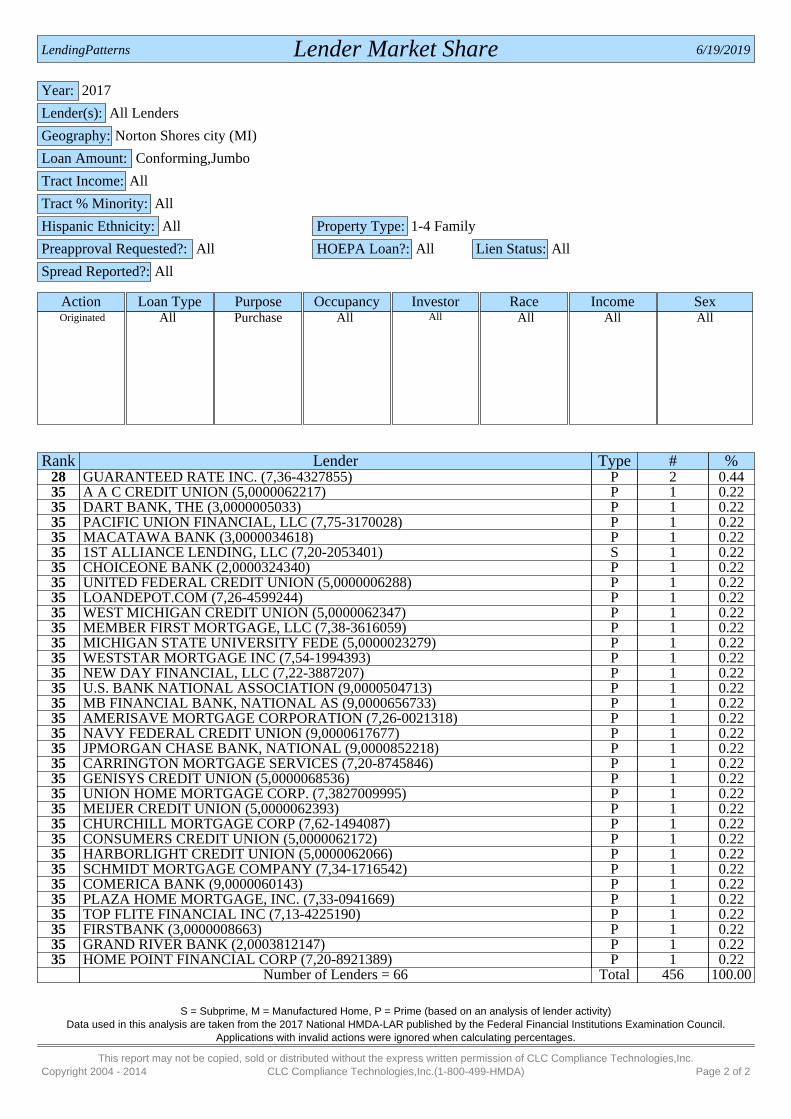

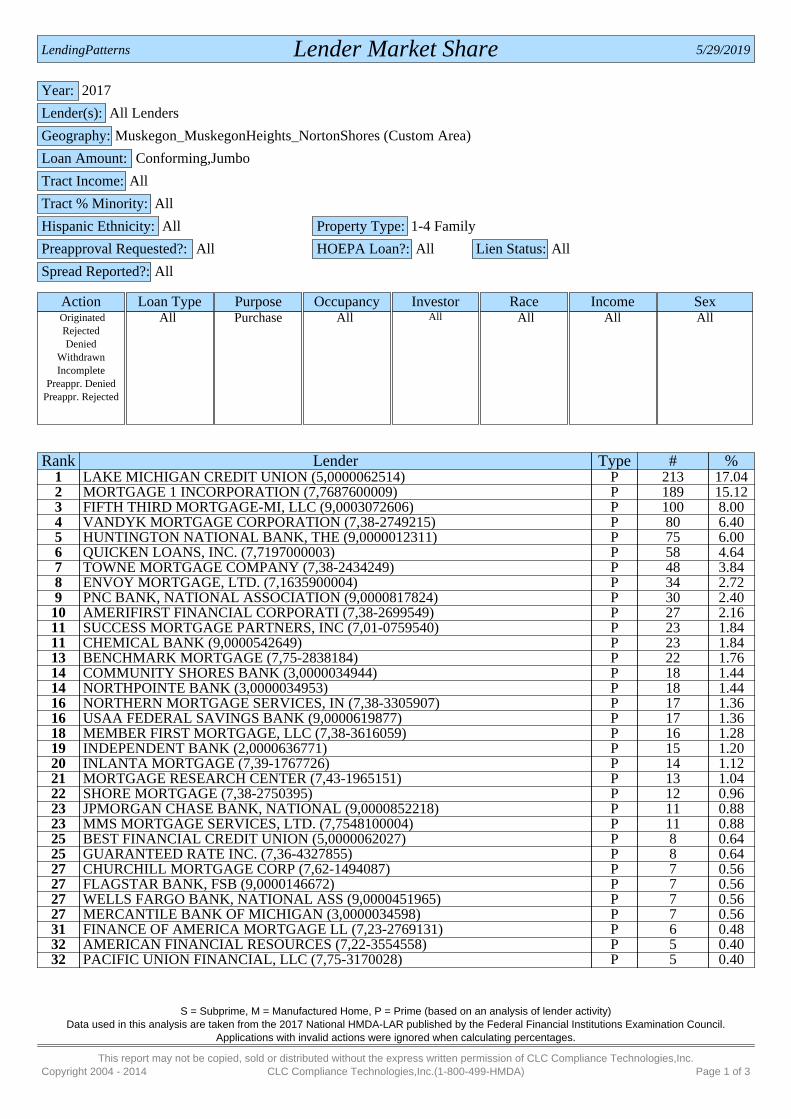

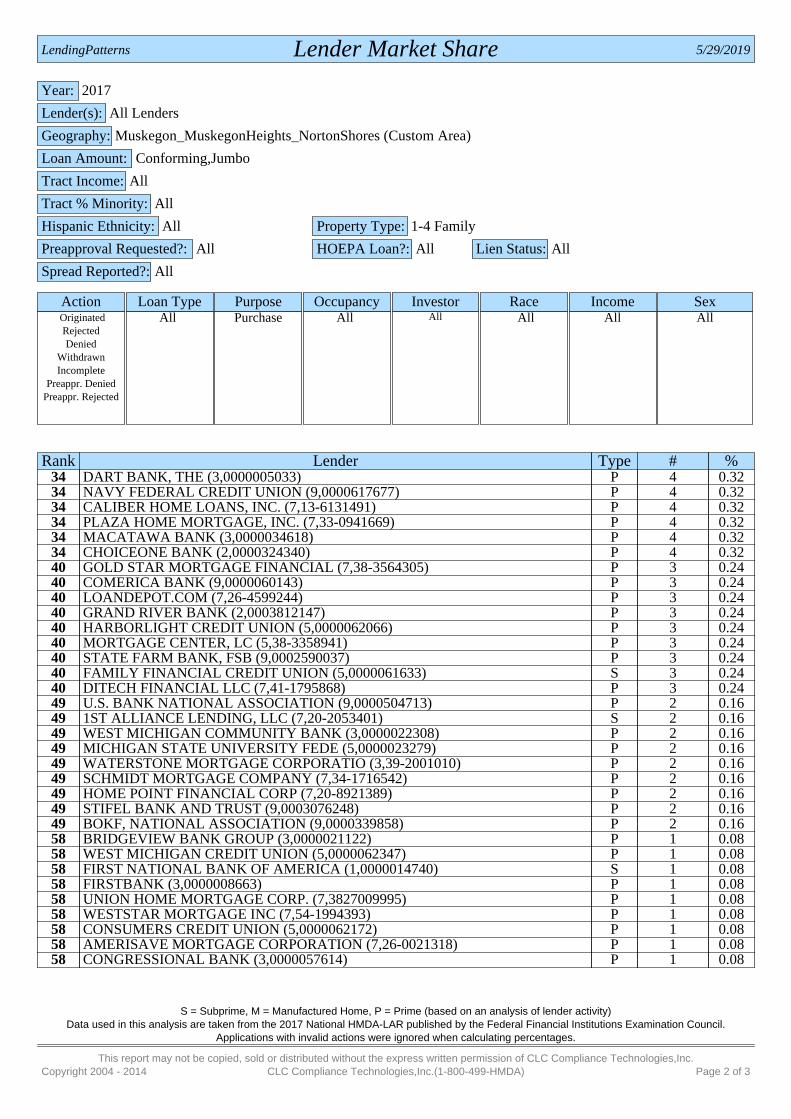

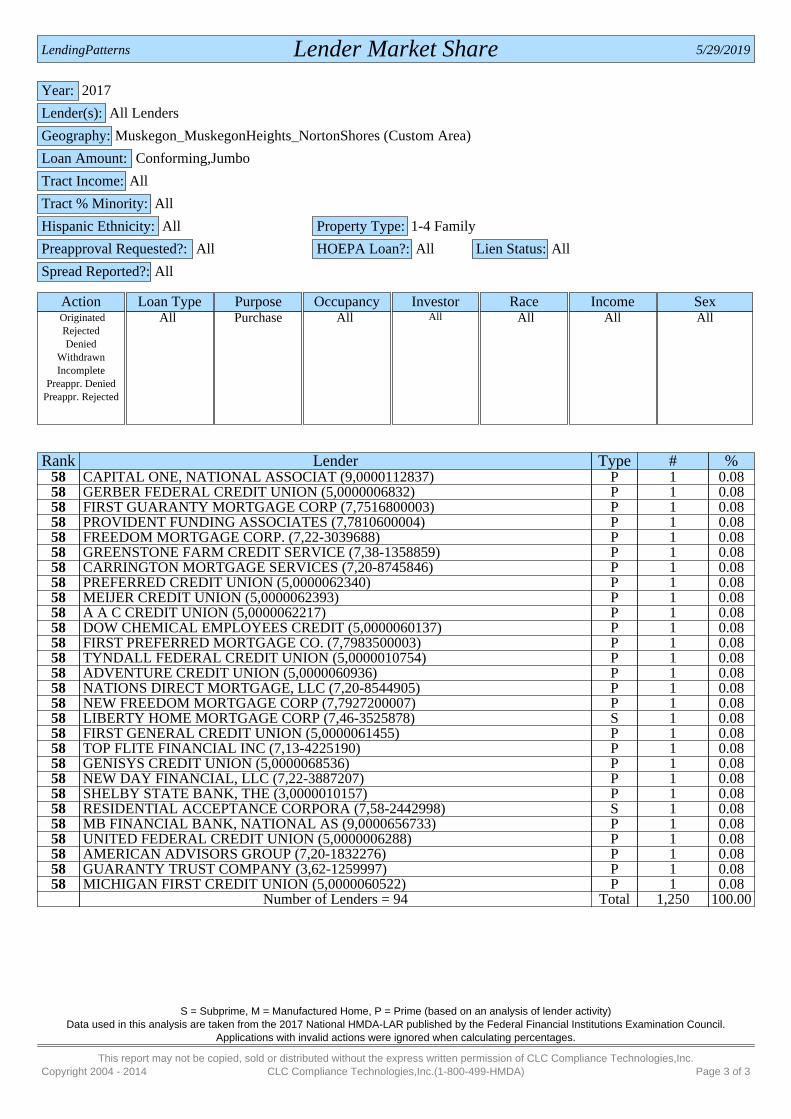

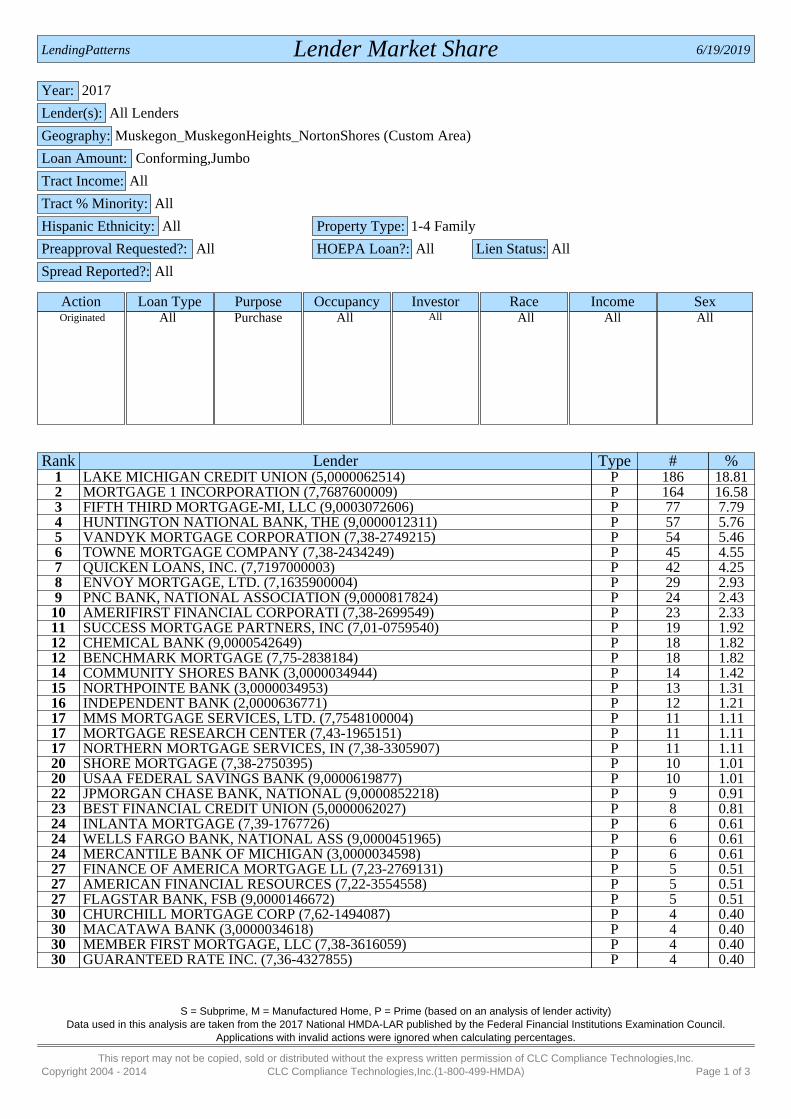

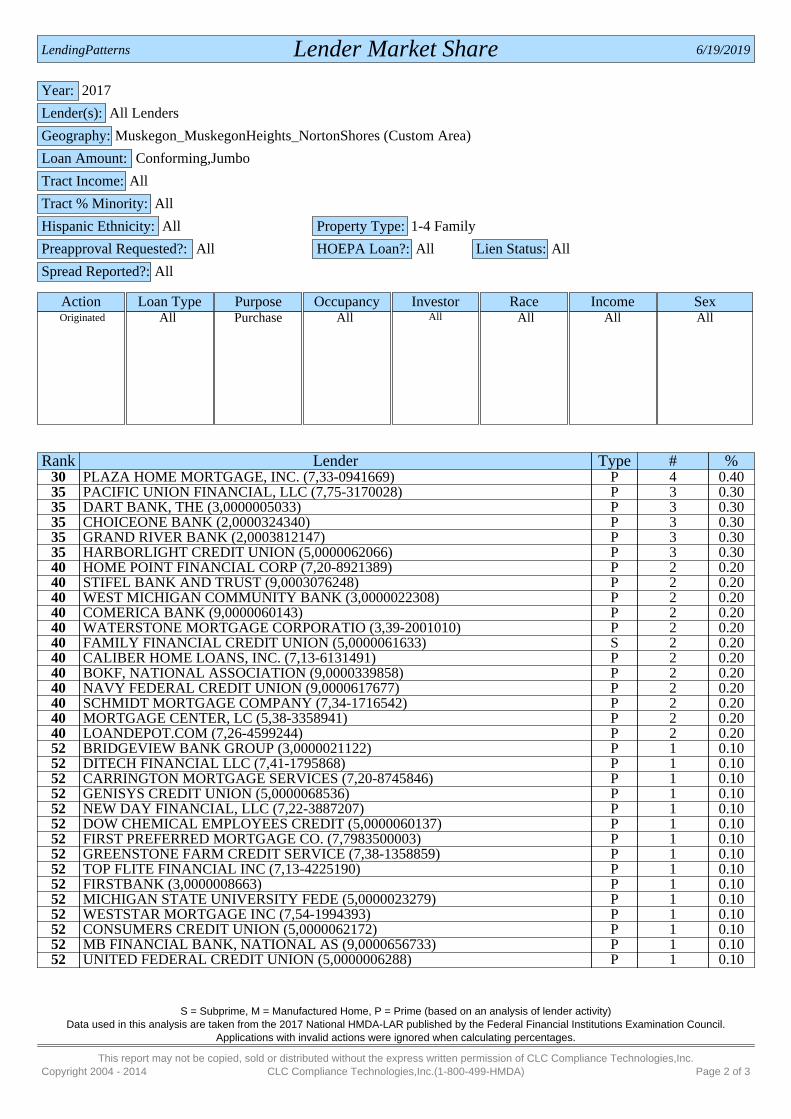

Which institutions were getting the most applications and making the most loans3 According to 2017 HMDA-LAR data, 94 different lending institutions received a total of 1,250 loan applications in the Cities of Muskegon, Muskegon Heights, and Norton Shores (“Tri City region”). Despite the large number of lending institutions receiving loan applications, most of the loan application activity was concentrated at a handful of lending institutions. Over 75% of the 94 lending institutions received less than five (5) applications each, with 46 of those lending institutions receiving only one (1) loan application. On the other hand, the lenders with the five (5) highest numbers of applications received in the Tri City region collectively processed over 50% of the market share of total loan applications.

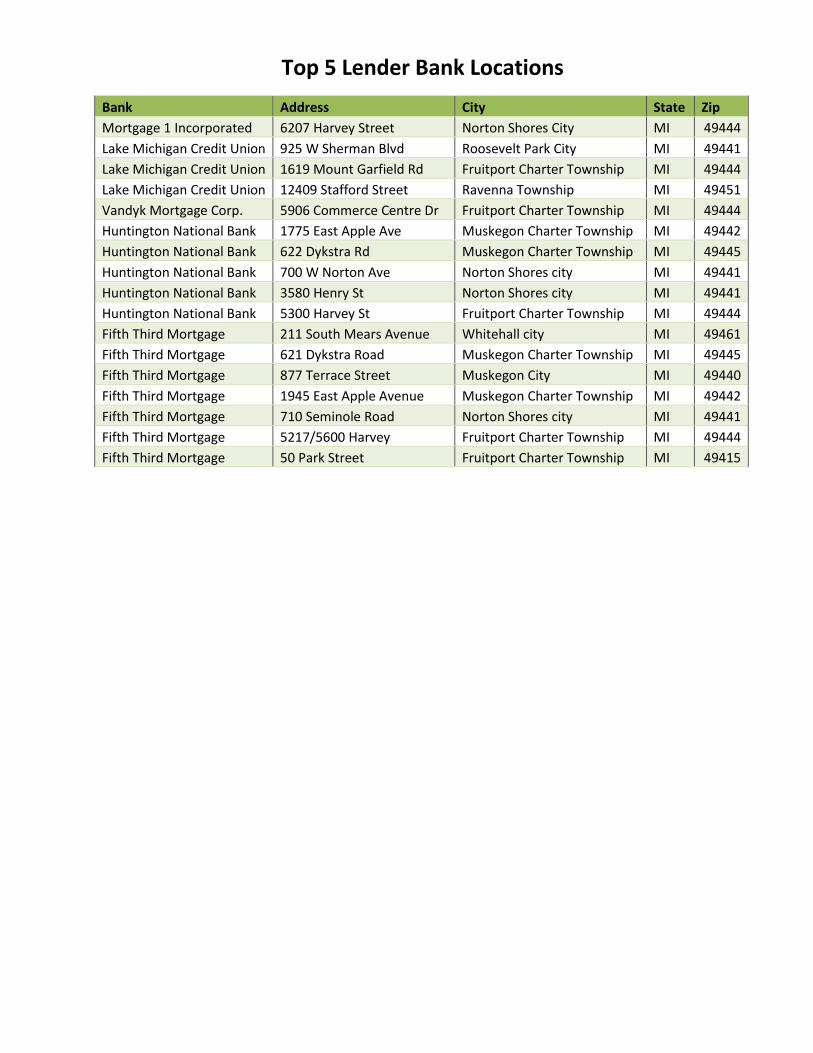

These “top 5 lenders” include: Lake Michigan Credit Union, Mortgage 1, Incorporation, Fifth Third Mortgage, Vandyk Mortgage Corporation, and Huntington National Bank. The “top 5 lenders” for the Tri City region were also the same five (5) lenders with the highest number of applications in the City of Muskegon and the City of Norton Shores. However, the five (5) most active lenders in the City Muskegon Heights did not include Vandyk Mortgage Corporation or Fifth Third Mortgage, but did include State Farm Bank and Member First Mortgage.

3 Charts/tables in this section were derived from LendingPatternsTM reports entitled “Lender Market Share” and information gathered from Lenders’ website (see Appendix C)

Mortgage 1 Inc Lake MichiganCredit Union

VandykMortgage Corp

HuntingtonNational Bank

Fifth ThirdMortgage

Muskegon Applications 108 103 57 50 48Muskegon Originations 90 91 37 37 36Muskegon Heights Applications 2 3 0 6 0Muskegon Heights Originations 2 2 0 2 0Norton Shores Applications 80 109 23 25 52Norton Shores Originations 73 94 17 20 41Tri City Applications 189 213 80 75 100Tri City Originations 164 186 54 57 77

0153045607590

105120135150165180195210225

Number of Applications and Originations for the Top 5 Lenders by City

Market Overview

8 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

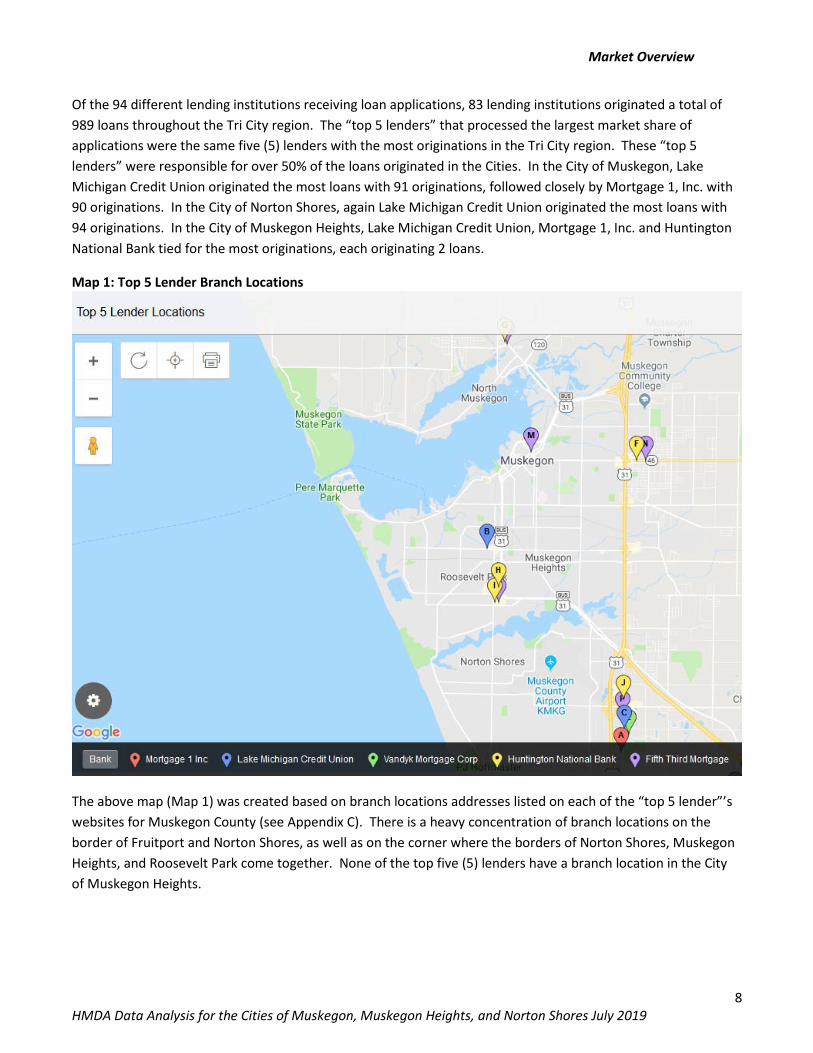

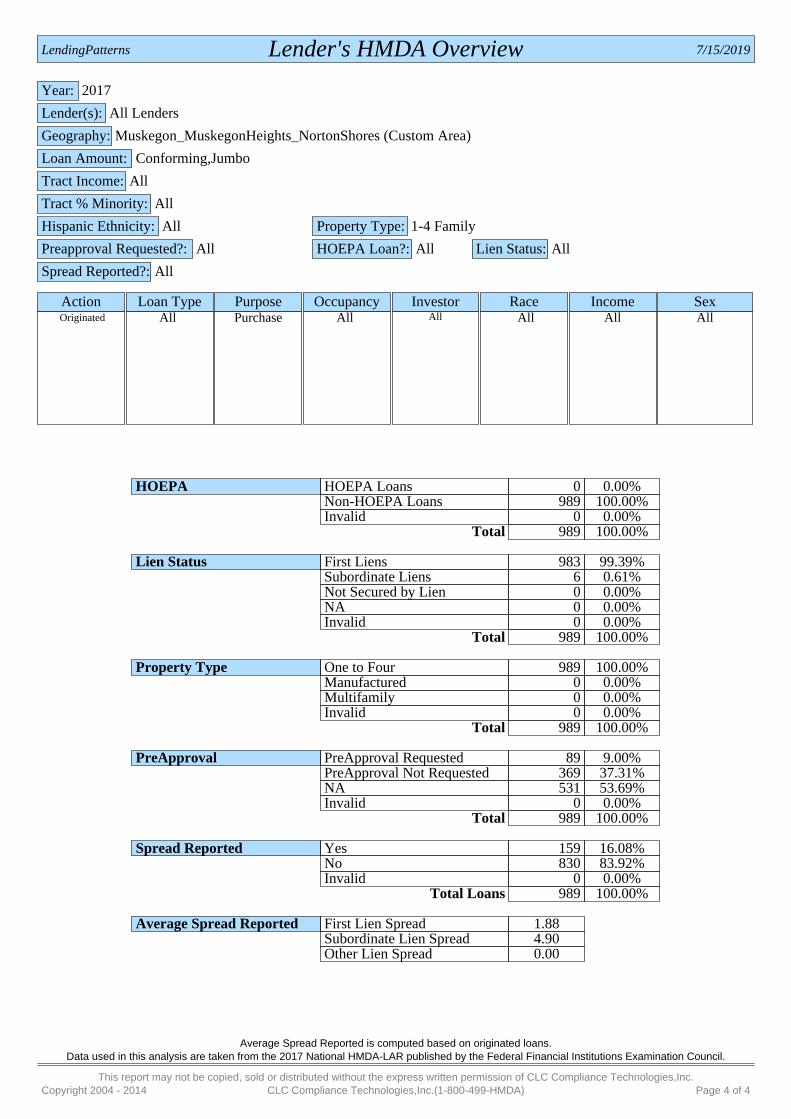

Of the 94 different lending institutions receiving loan applications, 83 lending institutions originated a total of 989 loans throughout the Tri City region. The “top 5 lenders” that processed the largest market share of applications were the same five (5) lenders with the most originations in the Tri City region. These “top 5 lenders” were responsible for over 50% of the loans originated in the Cities. In the City of Muskegon, Lake Michigan Credit Union originated the most loans with 91 originations, followed closely by Mortgage 1, Inc. with 90 originations. In the City of Norton Shores, again Lake Michigan Credit Union originated the most loans with 94 originations. In the City of Muskegon Heights, Lake Michigan Credit Union, Mortgage 1, Inc. and Huntington National Bank tied for the most originations, each originating 2 loans.

Map 1: Top 5 Lender Branch Locations

The above map (Map 1) was created based on branch locations addresses listed on each of the “top 5 lender”’s websites for Muskegon County (see Appendix C). There is a heavy concentration of branch locations on the border of Fruitport and Norton Shores, as well as on the corner where the borders of Norton Shores, Muskegon Heights, and Roosevelt Park come together. None of the top five (5) lenders have a branch location in the City of Muskegon Heights.

Market Overview

9 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

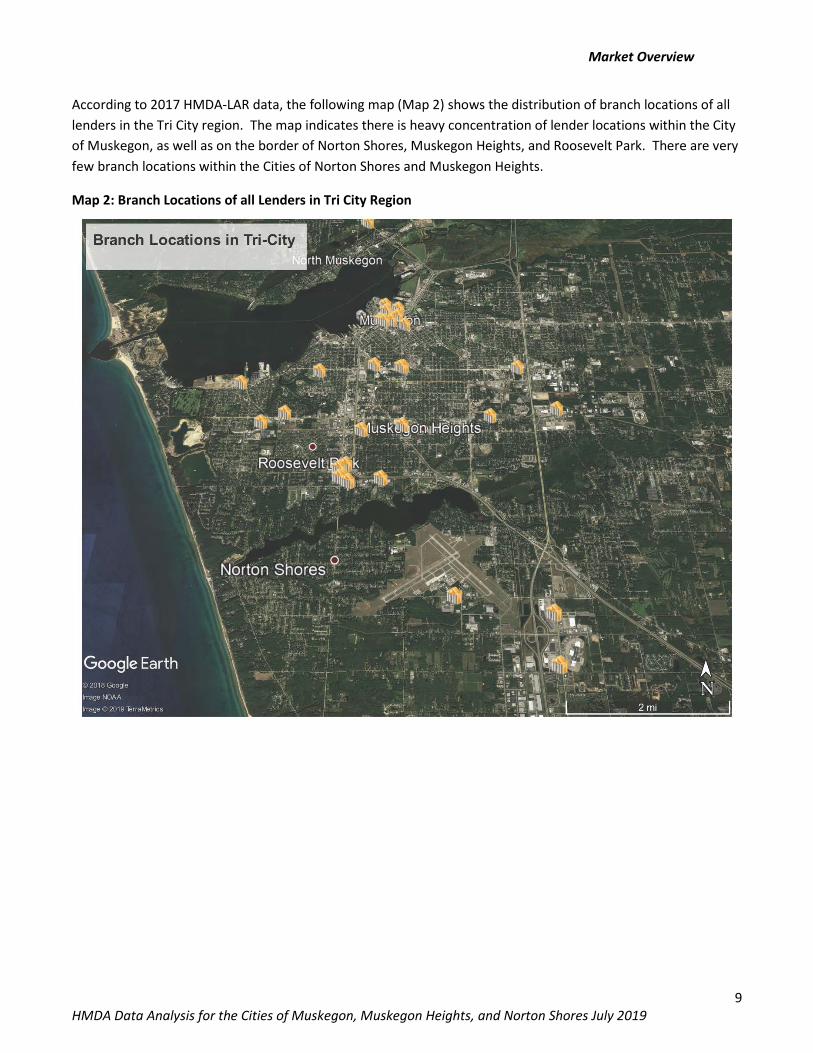

According to 2017 HMDA-LAR data, the following map (Map 2) shows the distribution of branch locations of all lenders in the Tri City region. The map indicates there is heavy concentration of lender locations within the City of Muskegon, as well as on the border of Norton Shores, Muskegon Heights, and Roosevelt Park. There are very few branch locations within the Cities of Norton Shores and Muskegon Heights.

Map 2: Branch Locations of all Lenders in Tri City Region

Market Overview

10 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

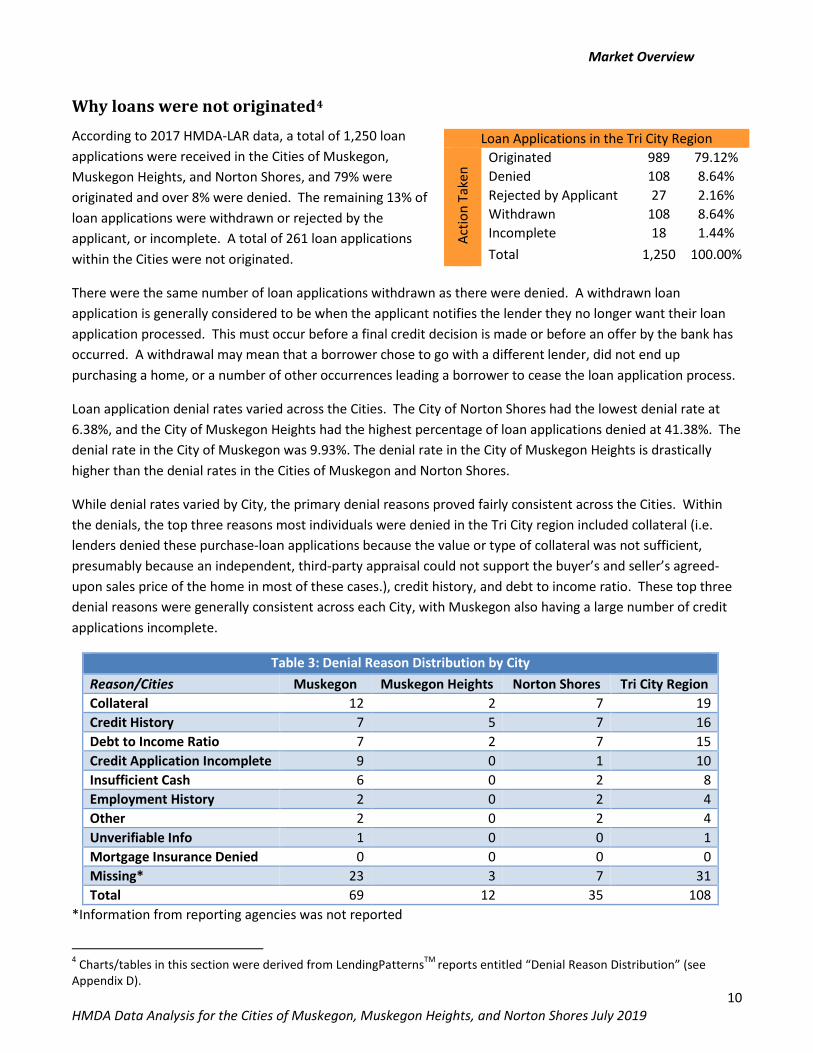

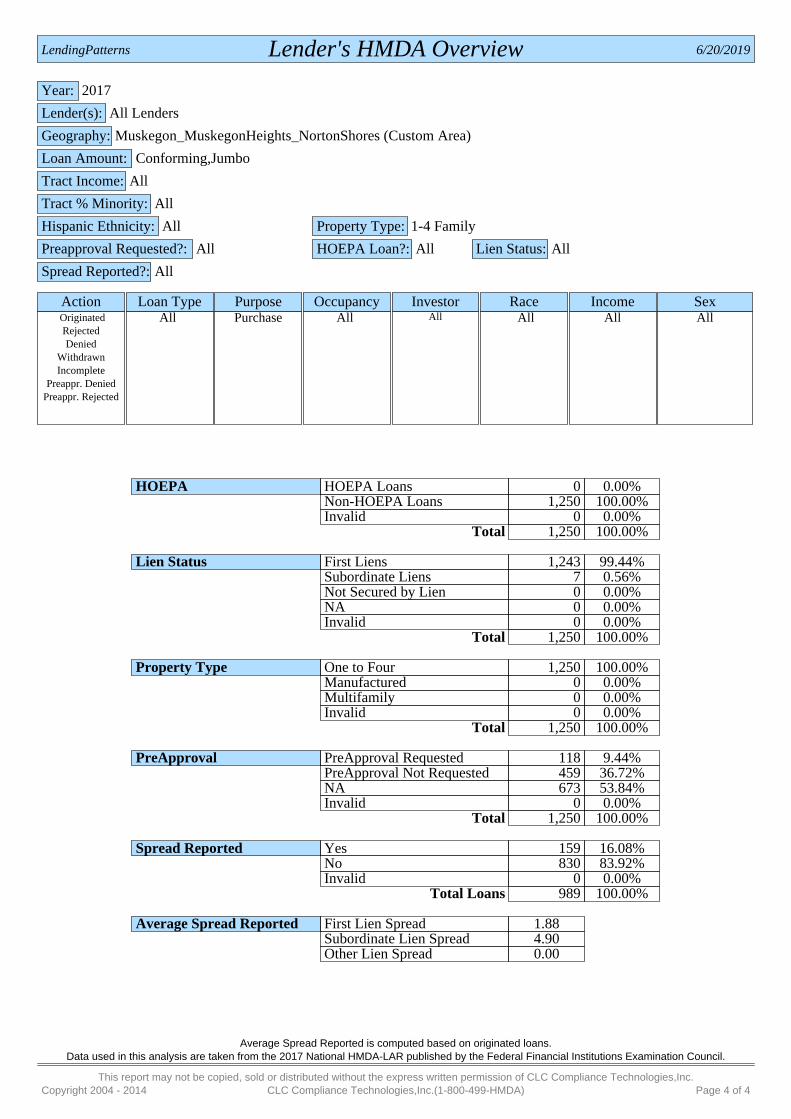

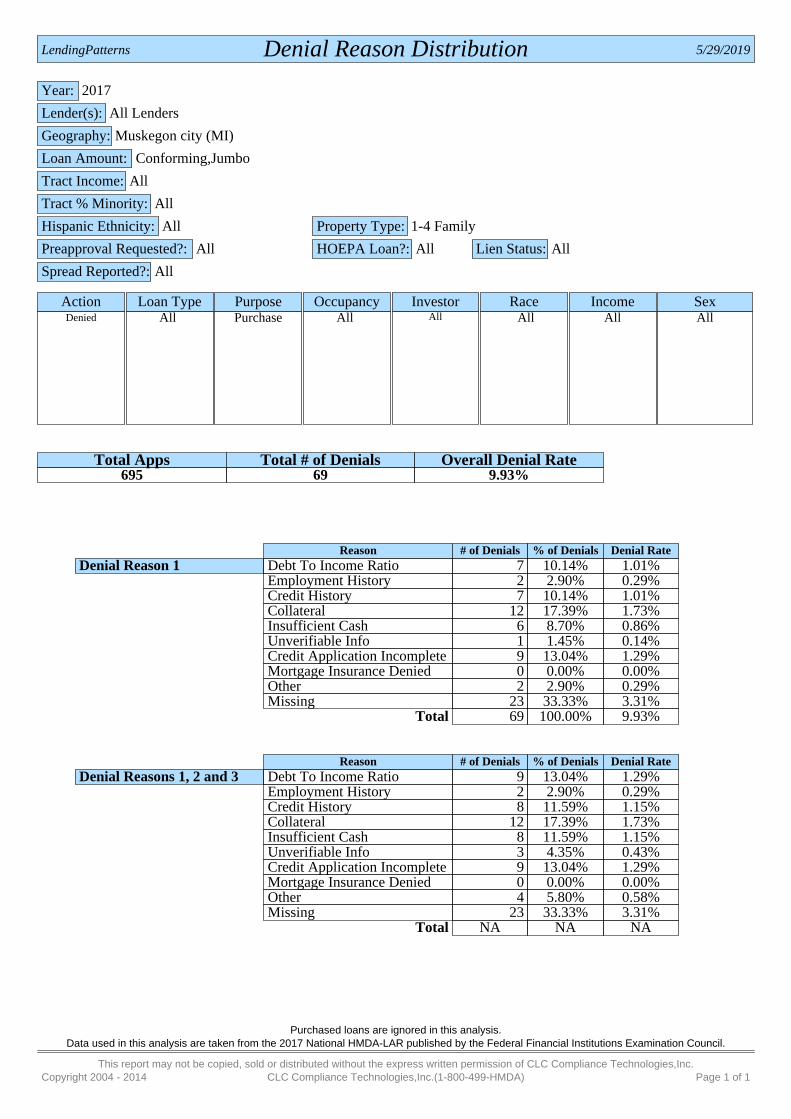

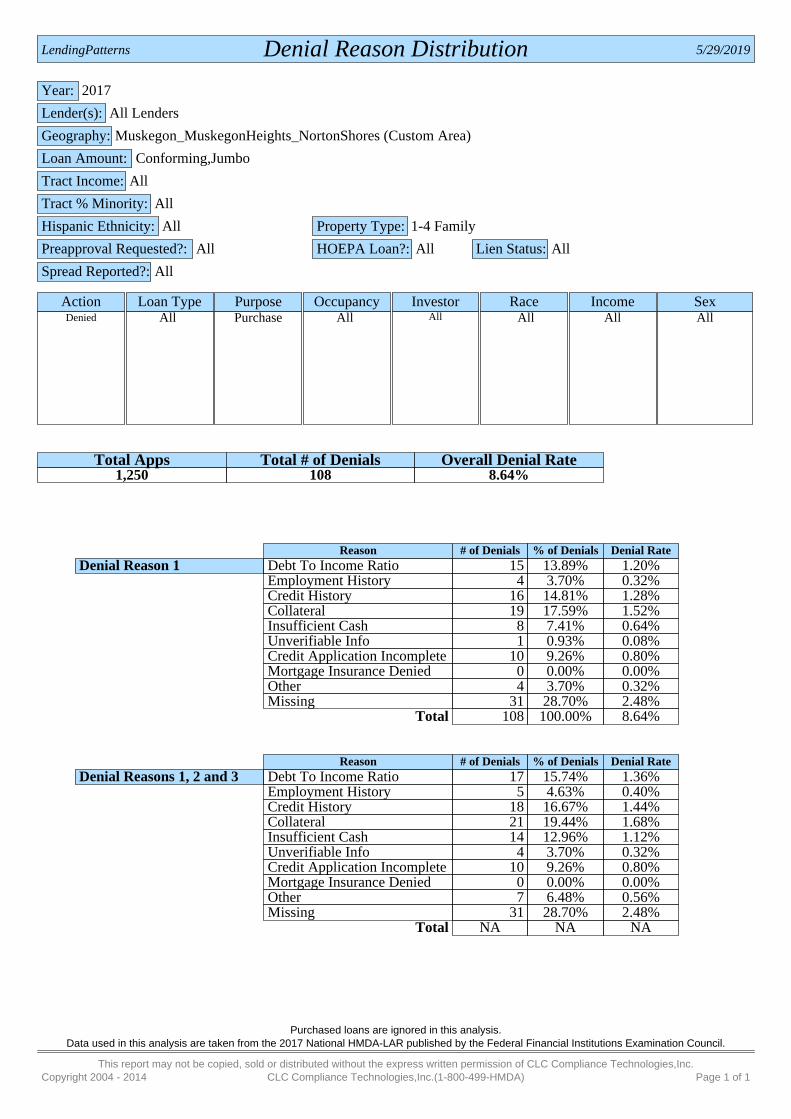

Why loans were not originated4 According to 2017 HMDA-LAR data, a total of 1,250 loan applications were received in the Cities of Muskegon, Muskegon Heights, and Norton Shores, and 79% were originated and over 8% were denied. The remaining 13% of loan applications were withdrawn or rejected by the applicant, or incomplete. A total of 261 loan applications within the Cities were not originated.

There were the same number of loan applications withdrawn as there were denied. A withdrawn loan application is generally considered to be when the applicant notifies the lender they no longer want their loan application processed. This must occur before a final credit decision is made or before an offer by the bank has occurred. A withdrawal may mean that a borrower chose to go with a different lender, did not end up purchasing a home, or a number of other occurrences leading a borrower to cease the loan application process.

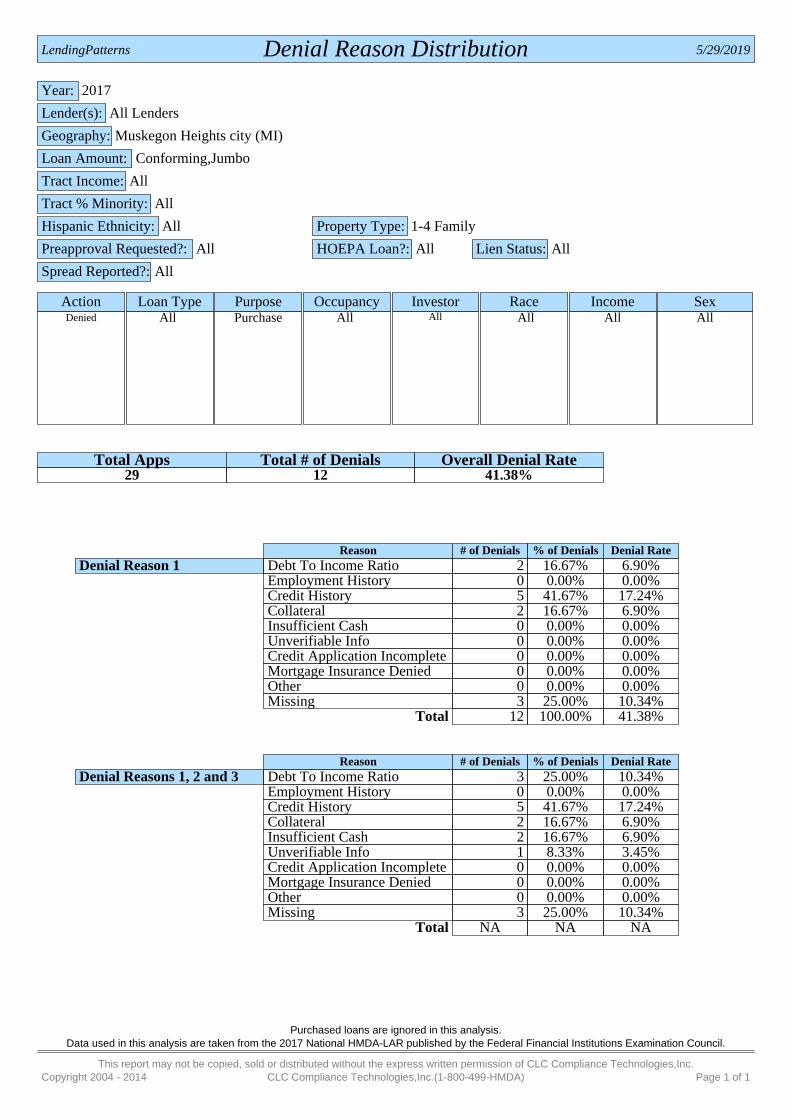

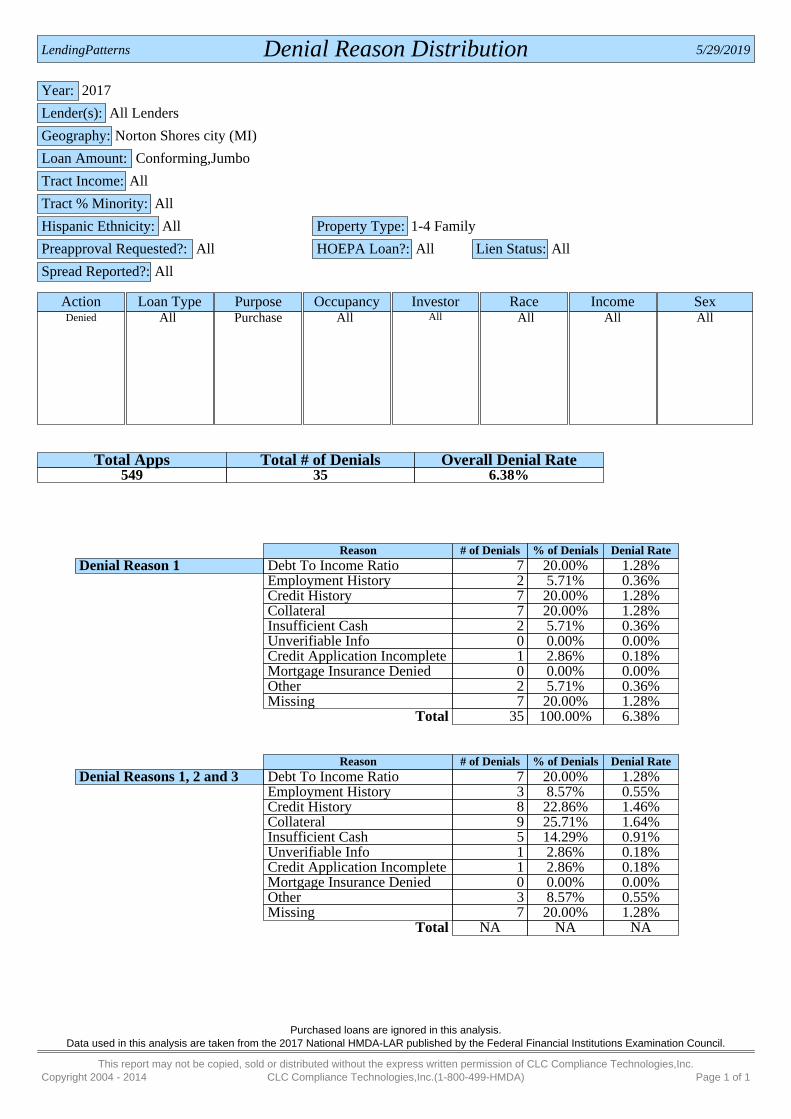

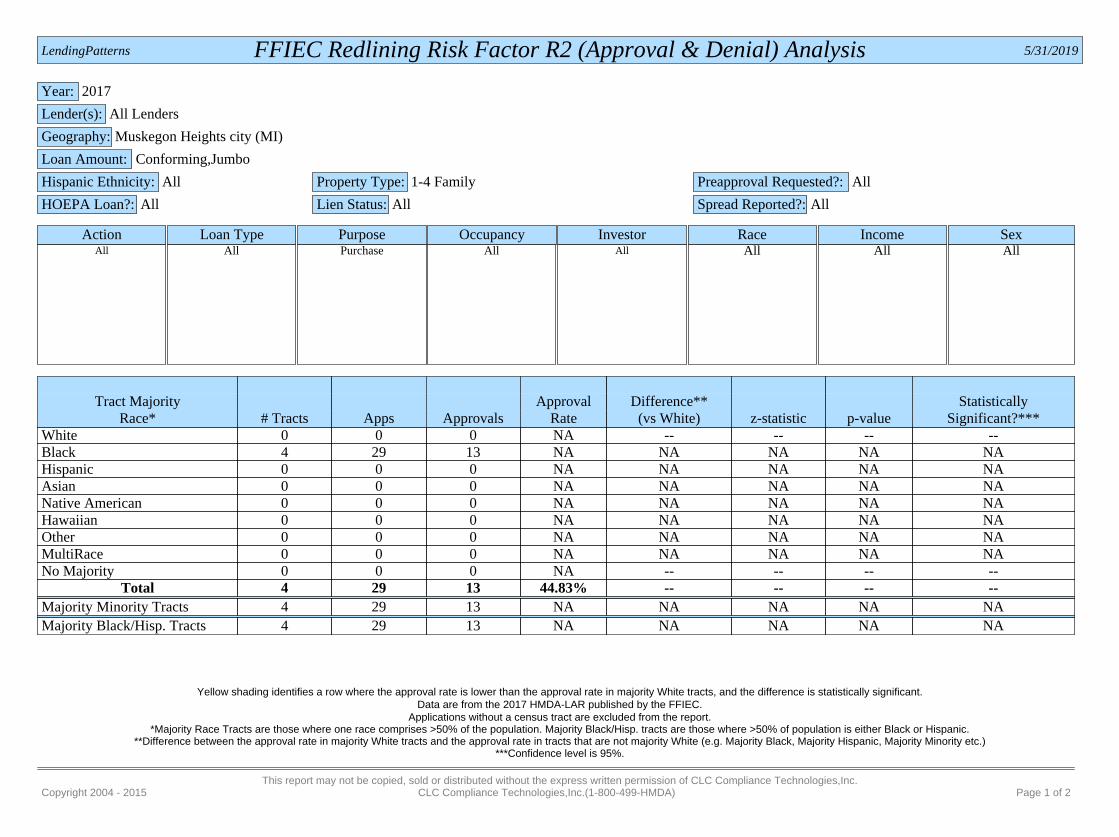

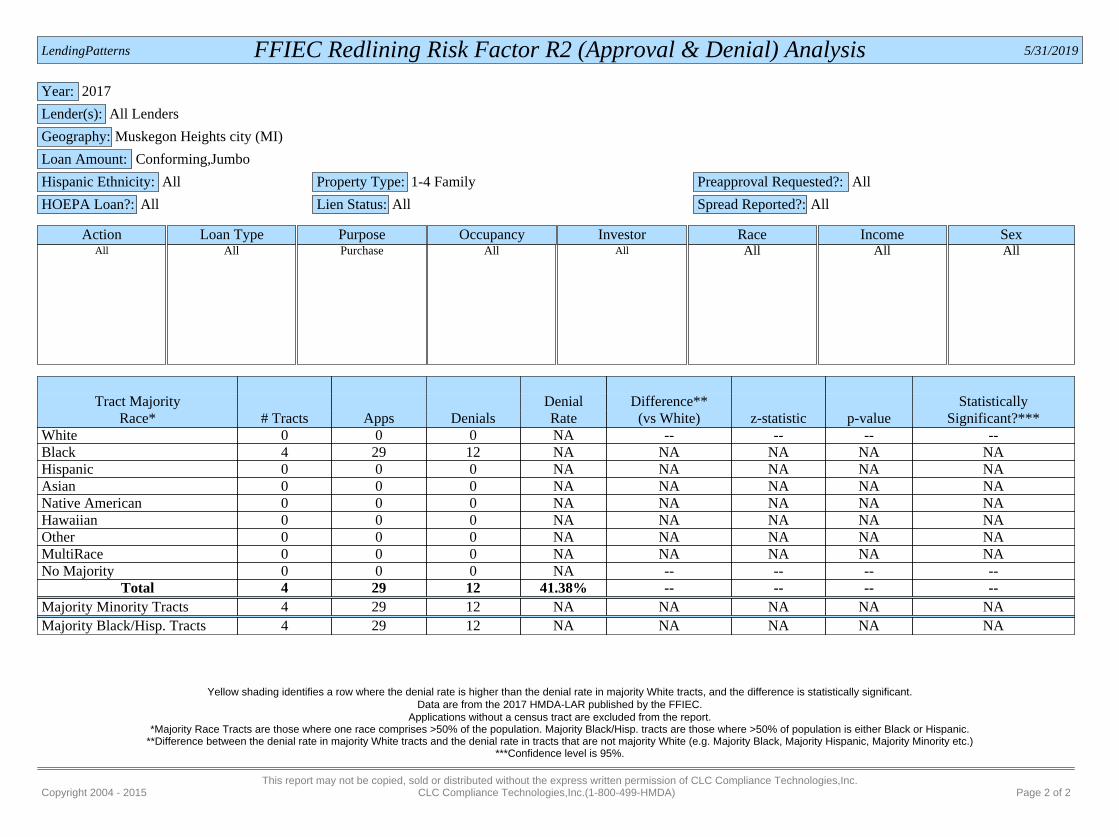

Loan application denial rates varied across the Cities. The City of Norton Shores had the lowest denial rate at 6.38%, and the City of Muskegon Heights had the highest percentage of loan applications denied at 41.38%. The denial rate in the City of Muskegon was 9.93%. The denial rate in the City of Muskegon Heights is drastically higher than the denial rates in the Cities of Muskegon and Norton Shores.

While denial rates varied by City, the primary denial reasons proved fairly consistent across the Cities. Within the denials, the top three reasons most individuals were denied in the Tri City region included collateral (i.e. lenders denied these purchase-loan applications because the value or type of collateral was not sufficient, presumably because an independent, third-party appraisal could not support the buyer’s and seller’s agreed-upon sales price of the home in most of these cases.), credit history, and debt to income ratio. These top three denial reasons were generally consistent across each City, with Muskegon also having a large number of credit applications incomplete.

Table 3: Denial Reason Distribution by City Reason/Cities Muskegon Muskegon Heights Norton Shores Tri City Region Collateral 12 2 7 19 Credit History 7 5 7 16 Debt to Income Ratio 7 2 7 15 Credit Application Incomplete 9 0 1 10 Insufficient Cash 6 0 2 8 Employment History 2 0 2 4 Other 2 0 2 4 Unverifiable Info 1 0 0 1 Mortgage Insurance Denied 0 0 0 0 Missing* 23 3 7 31 Total 69 12 35 108

*Information from reporting agencies was not reported

4 Charts/tables in this section were derived from LendingPatternsTM reports entitled “Denial Reason Distribution” (see Appendix D).

Loan Applications in the Tri City Region

Act

ion

Take

n

Originated 989 79.12% Denied 108 8.64% Rejected by Applicant 27 2.16% Withdrawn 108 8.64% Incomplete 18 1.44% Total 1,250 100.00%

Disparity Analysis

11 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Disparity Analysis

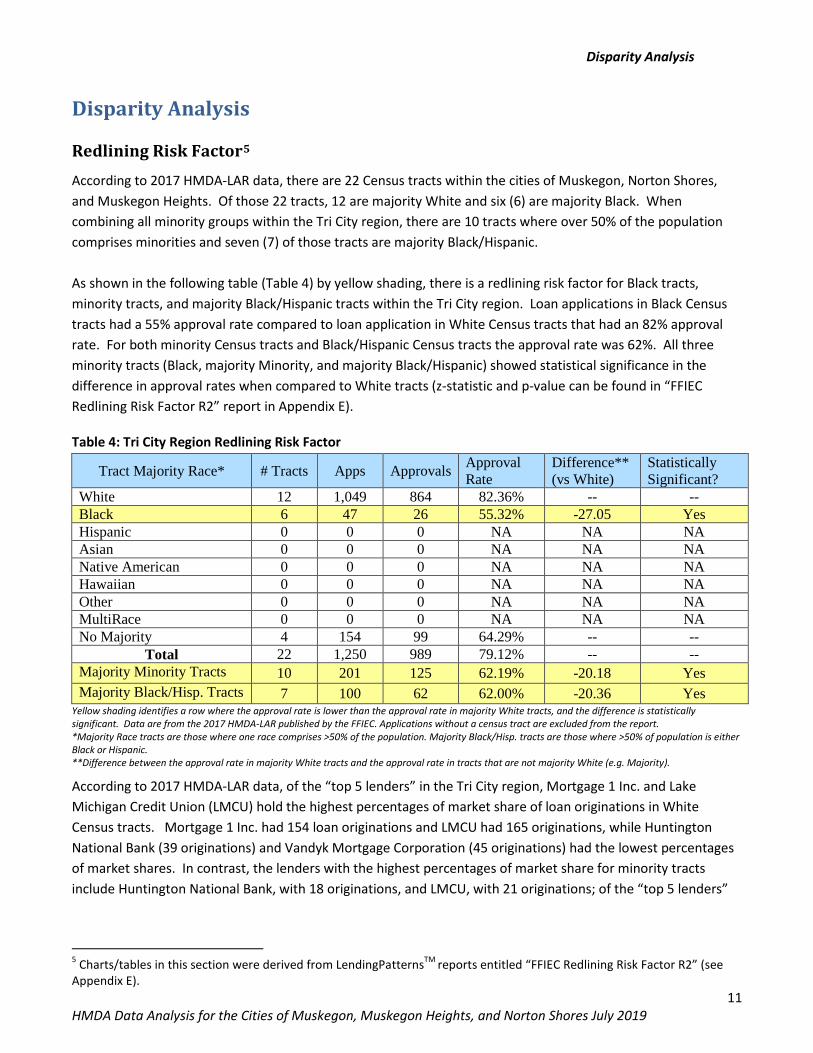

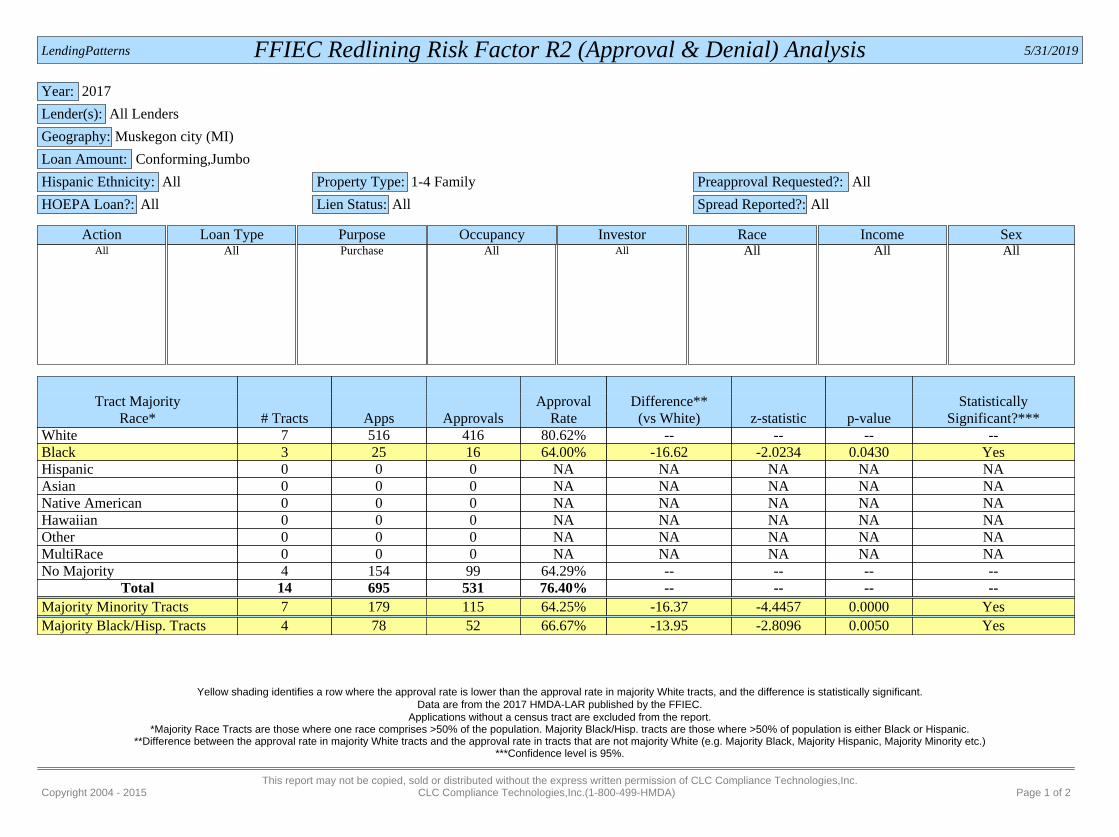

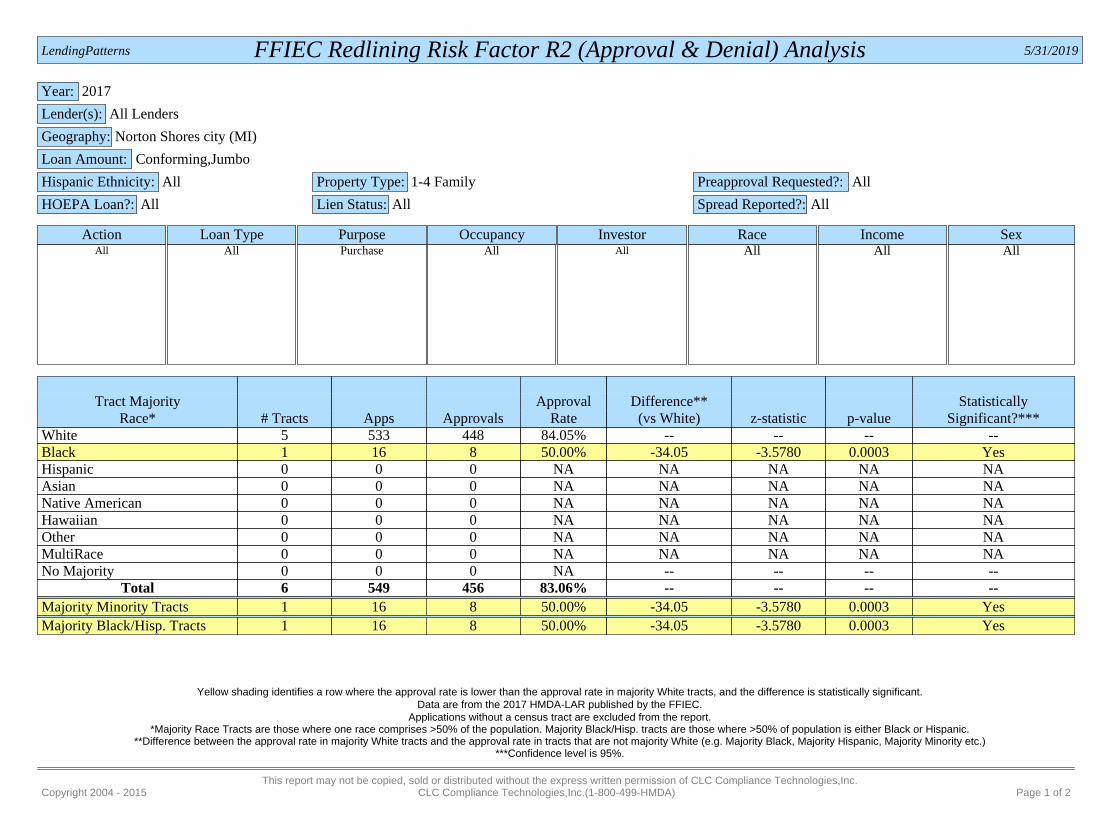

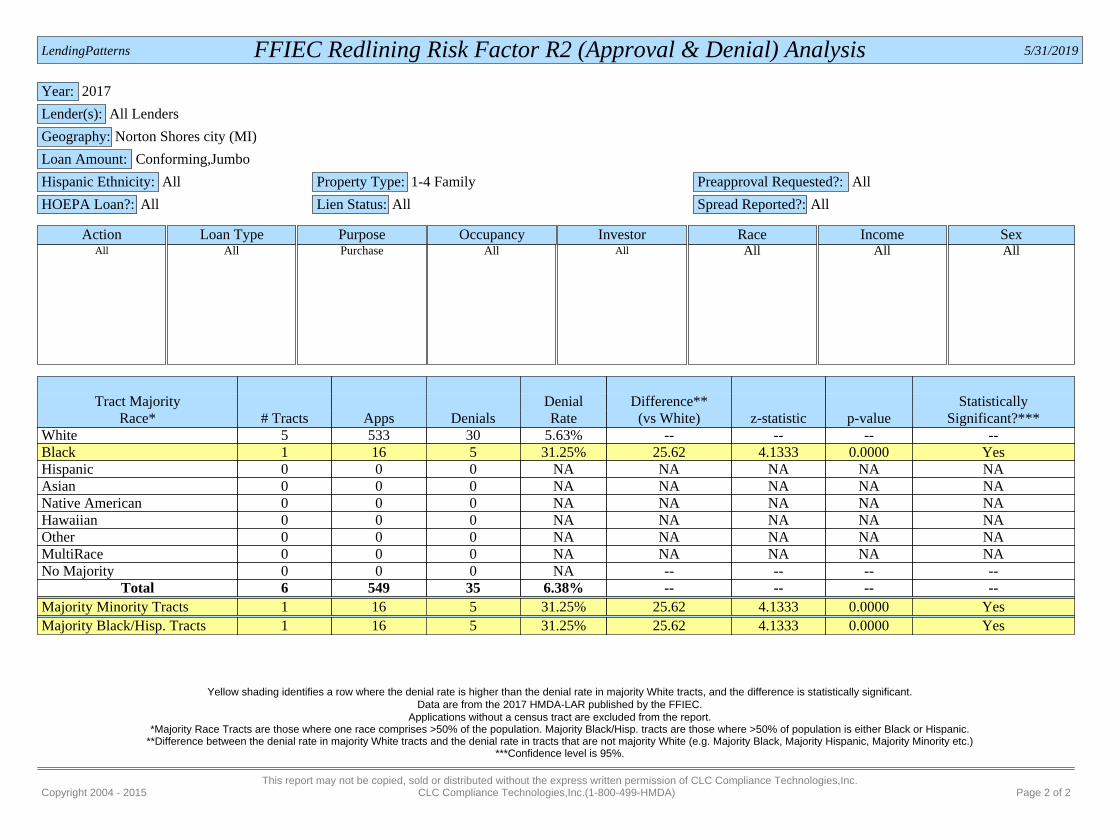

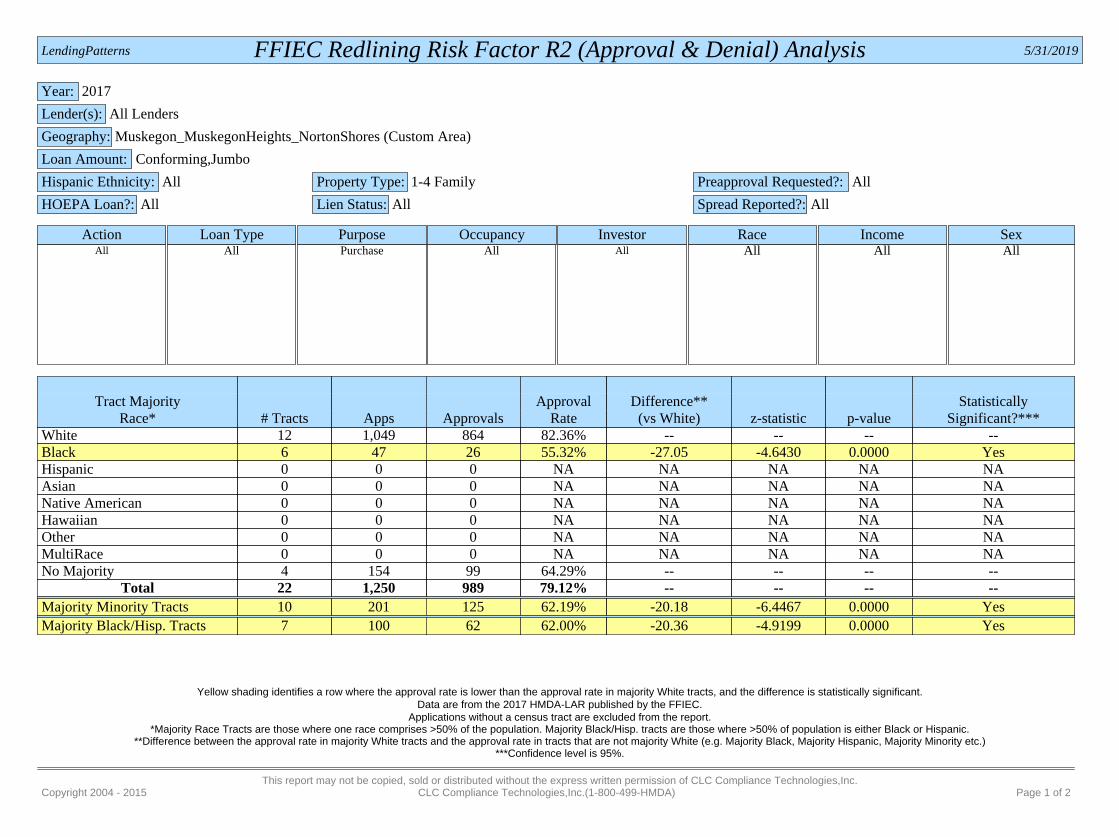

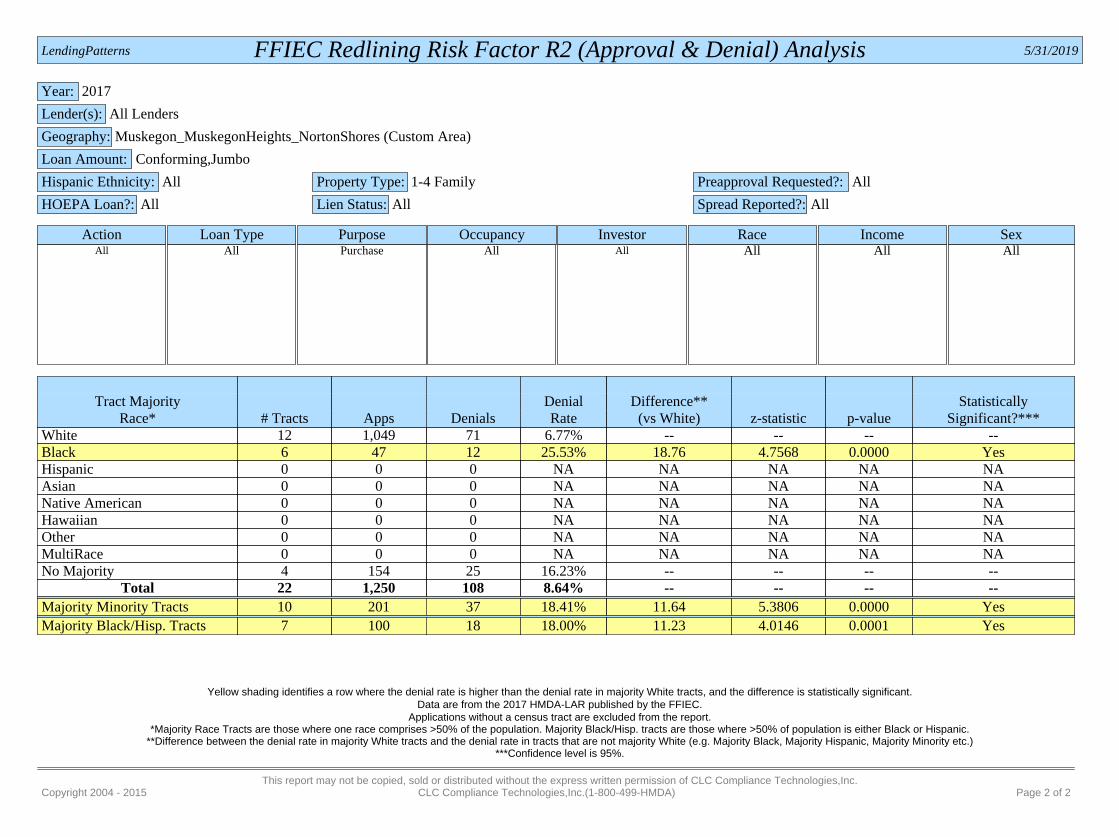

Redlining Risk Factor5 According to 2017 HMDA-LAR data, there are 22 Census tracts within the cities of Muskegon, Norton Shores, and Muskegon Heights. Of those 22 tracts, 12 are majority White and six (6) are majority Black. When combining all minority groups within the Tri City region, there are 10 tracts where over 50% of the population comprises minorities and seven (7) of those tracts are majority Black/Hispanic. As shown in the following table (Table 4) by yellow shading, there is a redlining risk factor for Black tracts, minority tracts, and majority Black/Hispanic tracts within the Tri City region. Loan applications in Black Census tracts had a 55% approval rate compared to loan application in White Census tracts that had an 82% approval rate. For both minority Census tracts and Black/Hispanic Census tracts the approval rate was 62%. All three minority tracts (Black, majority Minority, and majority Black/Hispanic) showed statistical significance in the difference in approval rates when compared to White tracts (z-statistic and p-value can be found in “FFIEC Redlining Risk Factor R2” report in Appendix E).

Table 4: Tri City Region Redlining Risk Factor

Tract Majority Race* # Tracts Apps Approvals Approval Rate

Difference** (vs White)

Statistically Significant?

White 12 1,049 864 82.36% -- -- Black 6 47 26 55.32% -27.05 Yes Hispanic 0 0 0 NA NA NA Asian 0 0 0 NA NA NA Native American 0 0 0 NA NA NA Hawaiian 0 0 0 NA NA NA Other 0 0 0 NA NA NA MultiRace 0 0 0 NA NA NA No Majority 4 154 99 64.29% -- --

Total 22 1,250 989 79.12% -- -- Majority Minority Tracts 10 201 125 62.19% -20.18 Yes Majority Black/Hisp. Tracts 7 100 62 62.00% -20.36 Yes

Yellow shading identifies a row where the approval rate is lower than the approval rate in majority White tracts, and the difference is statistically significant. Data are from the 2017 HMDA-LAR published by the FFIEC. Applications without a census tract are excluded from the report. *Majority Race tracts are those where one race comprises >50% of the population. Majority Black/Hisp. tracts are those where >50% of population is either Black or Hispanic. **Difference between the approval rate in majority White tracts and the approval rate in tracts that are not majority White (e.g. Majority).

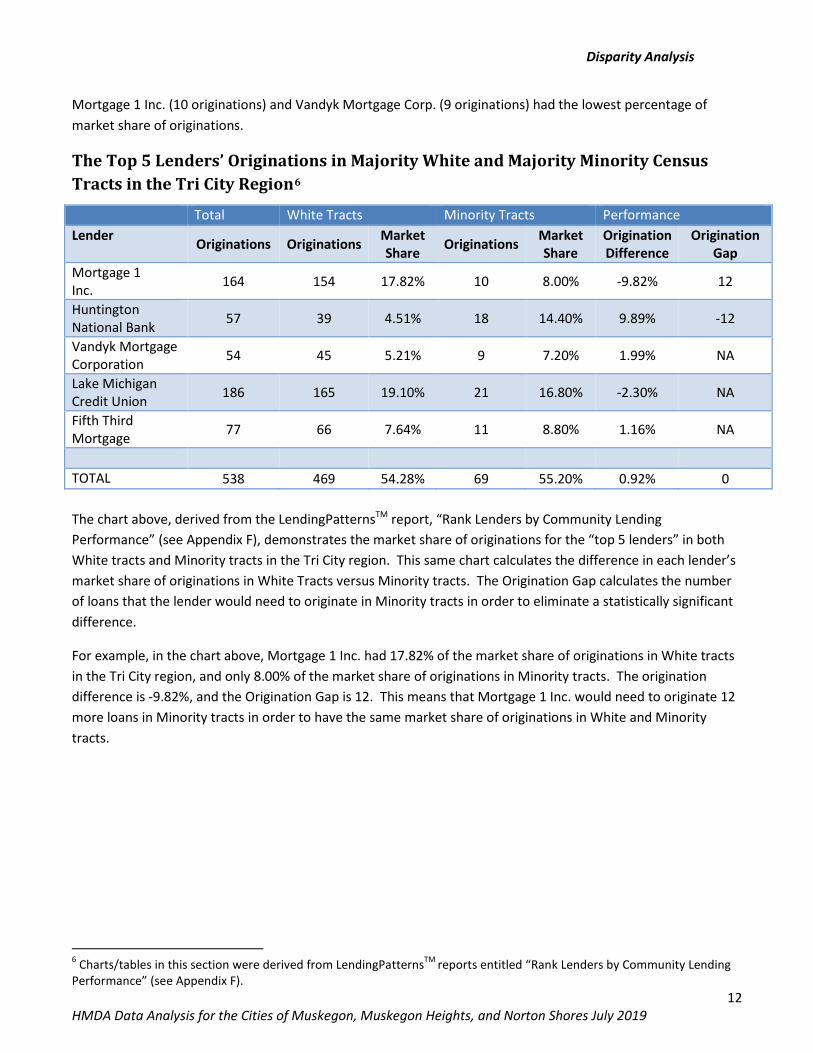

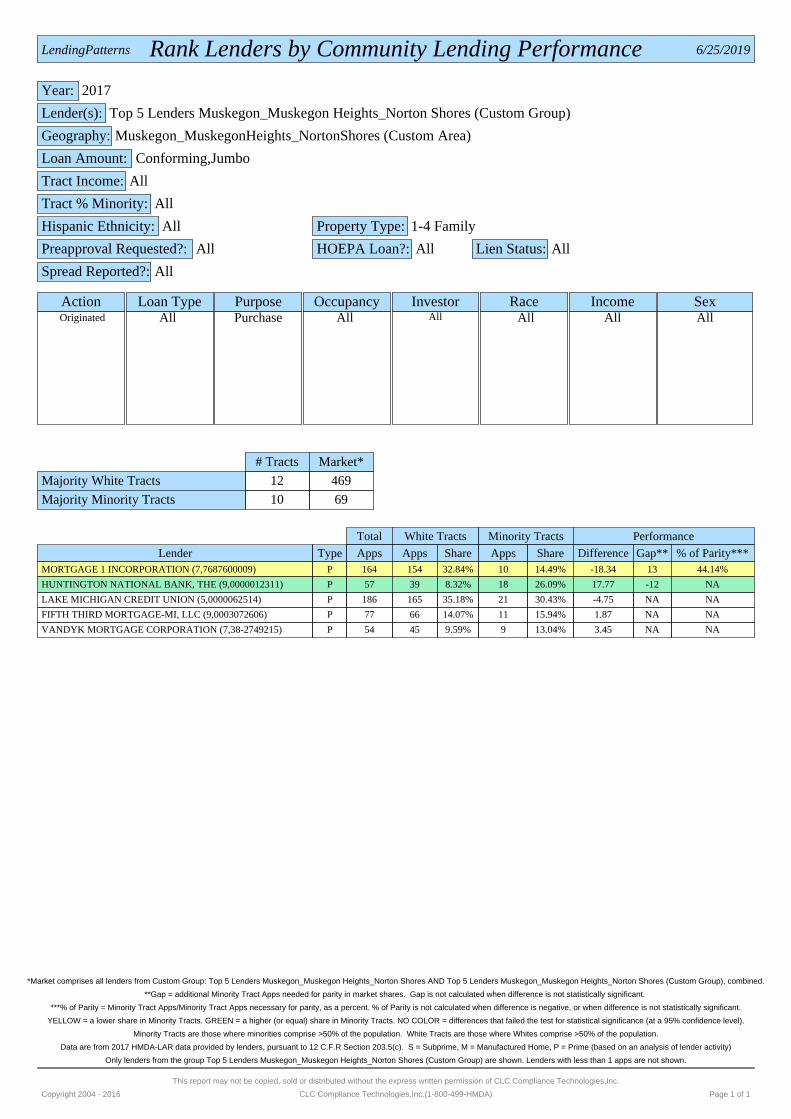

According to 2017 HMDA-LAR data, of the “top 5 lenders” in the Tri City region, Mortgage 1 Inc. and Lake Michigan Credit Union (LMCU) hold the highest percentages of market share of loan originations in White Census tracts. Mortgage 1 Inc. had 154 loan originations and LMCU had 165 originations, while Huntington National Bank (39 originations) and Vandyk Mortgage Corporation (45 originations) had the lowest percentages of market shares. In contrast, the lenders with the highest percentages of market share for minority tracts include Huntington National Bank, with 18 originations, and LMCU, with 21 originations; of the “top 5 lenders”

5 Charts/tables in this section were derived from LendingPatternsTM reports entitled “FFIEC Redlining Risk Factor R2” (see Appendix E).

Disparity Analysis

12 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Mortgage 1 Inc. (10 originations) and Vandyk Mortgage Corp. (9 originations) had the lowest percentage of market share of originations.

The Top 5 Lenders’ Originations in Majority White and Majority Minority Census Tracts in the Tri City Region6

Total White Tracts Minority Tracts Performance Lender Originations Originations Market

Share Originations Market Share

Origination Difference

Origination Gap

Mortgage 1 Inc. 164 154 17.82% 10 8.00% -9.82% 12

Huntington National Bank 57 39 4.51% 18 14.40% 9.89% -12

Vandyk Mortgage Corporation 54 45 5.21% 9 7.20% 1.99% NA

Lake Michigan Credit Union 186 165 19.10% 21 16.80% -2.30% NA

Fifth Third Mortgage 77 66 7.64% 11 8.80% 1.16% NA

TOTAL 538 469 54.28% 69 55.20% 0.92% 0 The chart above, derived from the LendingPatternsTM report, “Rank Lenders by Community Lending Performance” (see Appendix F), demonstrates the market share of originations for the “top 5 lenders” in both White tracts and Minority tracts in the Tri City region. This same chart calculates the difference in each lender’s market share of originations in White Tracts versus Minority tracts. The Origination Gap calculates the number of loans that the lender would need to originate in Minority tracts in order to eliminate a statistically significant difference.

For example, in the chart above, Mortgage 1 Inc. had 17.82% of the market share of originations in White tracts in the Tri City region, and only 8.00% of the market share of originations in Minority tracts. The origination difference is -9.82%, and the Origination Gap is 12. This means that Mortgage 1 Inc. would need to originate 12 more loans in Minority tracts in order to have the same market share of originations in White and Minority tracts.

6 Charts/tables in this section were derived from LendingPatternsTM reports entitled “Rank Lenders by Community Lending Performance” (see Appendix F).

Primary Conclusions

13 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Primary Conclusions

Market Overview

Where loans were made

Based upon 2017 HMDA data, Minority and Low and Middle Income Census tracts throughout the Tri City region are underrepresented in the total number of loans made. This is especially true in Muskegon Heights where a total of only 13 home purchase loans were originated in 2017.

• Of the 3 Cities, loan applications made in Norton Shores were the most likely to be originated, and applications in Muskegon Heights were the least likely to be originated.

• Both loan applications and loan originations from Low and Middle Income Census tracts throughout the three (3) Cities were underrepresented when compared to the relevant population and loans applied for and originated in High Income Census tracts.

• Loan applications and originations in Minority Census tracts in the Tri City region were also underrepresented as compared to the relevant population and loans applied for and originated in Non-Minority Census tracts.

• There were over 40 times more loans made in the City of Muskegon than in the City of Muskegon Heights, while the population of Muskegon is only about five (5) times the population of Muskegon Heights

• Muskegon Heights had a strikingly low number of loan activity. There were only 25 loan applications submitted for properties in Muskegon Heights during the year and only 13 loans originated.

Which borrowers got loans

Based upon 2017 HMDA data, White borrowers disproportionately applied for and received loans throughout the Tri City region. This was regardless of the racial demographics of the City. Further, Middle and Upper Income borrowers were 25% more likely to have their loan originated than a Low to Moderate Income borrower.

• The percentage of both applications and originations by minority borrowers, particularly for Black borrowers in each of the Cities, were disproportionately lower than the percentage of minorities within each of the Cities.

• Throughout the Cities, Low Income borrowers received very few loans, and experienced higher rates of denial.

Which institutions were getting the most applications and making the most loans

While the banking industry continues to change to meet the needs of its clients and the communities they serve, the location of branches and the types of services provided, including access to mortgage lenders does seem to impact the quantity, amount, and location of loan activity of the institution.

• The mortgage market in the Tri City region is very segmented in that 89 different lending institutions own 50% of the market share, many of whom received only 1 loan application each. Many of these

Primary Conclusions

14 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

lenders have no physical presence in the Tri City region. On the other hand, the “top 5 lenders” own the other 50% of the market share and do have branches located in certain parts of the Tri City region.

• There is a correlation between the access to physical branch locations and the number of applications received by each of the Cities.

o There were only 25 loan applications submitted in Muskegon Heights during 2017, 11 of which were submitted to the “top 5 lenders”. Not one of the “top 5 lenders” appears to have a branch located within the boundaries of Muskegon Heights.

o Despite the fact that the Cities of Muskegon Heights and Norton Shores both have few branch locations within the City limits, the City of Norton Shores had significantly more loan applications and originations than the City of Muskegon Heights.

Why loans were not originated

Over 20% of loan applications were not originated, primarily due to withdrawn and denied loan applications. The overall denial rate for mortgage applications was 8% for the Tri City region.

• Housing loan applications were denied by financial institutions for a variety of reasons, but credit history, a high amount of debt relative to income, and lack of collateral were the top three reasons for loan application denial across the Tri City region.

o Collateral – in many cases this means that the appraised value of the property was too low to support the loan amount. Some contributing factors to low appraised values could include, but not be limited to, lack of available sales comparables (especially due to sales inactivity in Muskegon Heights), lasting impact of the foreclosure crisis and lack of maintenance of Real Estate Owned properties, and underwriting issues that keep the valuations down. Appraisals that fail to support sufficient collateral for the loan amount have ripple effects on successful loan applications. When mortgages are not made for homes sold on a multiple listing service, there then can lack sufficient adequate comparables to support future appraisals or to support mortgages on new homes built in low income neighborhoods.

o Debt-to-income ratio and credit history were main barriers to getting a loan. Socio-economic factors continue to impact a borrower’s ability to access home loans. These factors may include stagnant wages for low to moderate income households, the rising cost of healthcare, the cost of college education, and others that can severely limit a borrower’s ability to qualify for a mortgage.

• The City of Muskegon Heights had over 40% of loan applications denied, a denial rate over 30% higher than the Cities of Muskegon or Norton Shores.

Disparity Analysis

The disparity between the loan application and origination rates among White applicants and minority applicants is significant as compared to the demographics of the Cities. Disparity in lending activity suggests that a higher proportion of minority households will be distanced from homeownership opportunities, thereby limiting the potential for these households to build equity and generational wealth through homeownership.

Primary Conclusions

15 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Redlining risk factor

• Minority Census tracts are underrepresented in loan applications and originations. Loan applications in Black Census tracts had a 55% approval rate compared to loan applications in White Census tracts that had an 82% approval rate. For both Minority Census tracts and Black/Hispanic Census tracts, the approval rate was 62%.

The Top 5 Lenders’ Originations in Majority White and Majority Minority Census Tracts

• Two (2) out of the “top 5 lenders” have disproportionate origination rates in White and Minority Census tracts, according to LendingPatternsTM. For example, Mortgage 1 had 17.82% of the market share of originations in White Census tracts in the Tri City region, but only 8.00% of the market share of originations in Minority Census tracts. The origination difference is -9.82%, and the Origination Gap is 12. This means that Mortgage 1 Inc. would need to originate 12 more loans in Minority Census tracts in order to have the same market share of originations in White and Minority Census tracts. This level of disparity is identified as statistically significant in a LendingPatternsTM redlining risk analysis.

Recommendations

16 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Recommendations

How the Cities of Muskegon, Muskegon Heights and Norton Shores might use this HMDA data

With the information in this report, the Cities of Muskegon, Muskegon Heights, and Norton Shores can decide what steps should be taken to address any disparities or issues that may serve as impediments to access to mortgage loans for its residents. These steps might include, but not be limited to, outreach and education efforts, homebuyer education programs and other programs for low-income borrowers, neighborhood stabilization efforts, collaborations with lending institutions and the real estate industry, community partnerships, and investigation of individuals or entities that appear to be in violation of fair housing laws. The Cities should consider the following recommendations in order to address the disparities and conclusions identified in this report:

RECOMMENDATION: Provide the public with information about the lending performance of institutions reporting under HMDA by making this report and any other relevant reports publicly available via accessible online and print venues.

RECOMMENDATION: Increase the number applications and originations from Minority and Low to Moderate Income borrowers and borrowers in Minority and Low to Moderate Income Census tracts.

Potential Action Steps:

o Expend resources on homebuyer outreach and education initiatives in order to increase the number of Minority and Low to Moderate Income borrowers who apply for loans.

o Partner with non-profit and faith-based organizations, real estate agents, lenders and others to provide greater education and outreach to Minority and Low to Moderate Income Census tracts to increase understanding of the dangers of and lessen the use of predatory lenders, reverse mortgages and other products that can reduce equity.

o Partner with non-profit and faith-based organizations, real estate agents, lenders and others to support the delivery of financial literacy classes and information to potential borrowers in preparation for seeking a mortgage as well as for students as a part of their high school and college curriculum. Financial literacy prepares households to qualify with the best credit terms, eliminates the major obstacles in the home buying process, and makes it possible for households to build equity through homeownership. Ensure that the information is provided in languages other than English to meet the needs of the community.

o Conduct creative, engaging efforts to help create demand for loans in Minority and Low to Moderate Income Census tracts. This could include outreach to real estate agents and brokers, lenders, and others regarding community assets. This could also include tours or promotional events in partnership with neighborhood organizations, business associations, Chambers of Commerce, etc. to bring real estate industry members, potential buyers, lenders and other into these Census tracts.

Recommendations

17 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

RECOMMENDATION: Support the loan-readiness of borrowers to reduce the number of loan applications denied due to credit history or debt-to-income ratio.

Potential Action Steps:

o Partner with non-profit and faith-based organizations, real estate agents, lenders and others to support the delivery of credit counseling/credit repair to help prepare households to qualify for a mortgage loan. Ensure that the information is provided in languages other than English to meet the needs of the community.

o Partner with non-profit and faith-based organizations, real estate agents, lenders and others to create micro loan programs and other banking products to help potential borrowers remediate their deficient credit history.

RECOMMENDATION: Determine specific objectives regarding making loans and otherwise promoting greater investment activity in low-income and minority neighborhoods through discussions with lending institutions subject to the Community Reinvestment Act.

Potential Action Steps:

o Encourage lending institutions to ensure that banking services are extended to all Minority and Low to Moderate Income Census tracts and that banking branches are located in places that are convenient to those Census tracts.

o Limit the spread of predatory lenders such as payday lenders or check cashing services by working with traditional financial institutions to offer products and services that help households establish or re-establish checking, savings, and credit accounts.

o Work with underwriters to examine and adjust the criteria used by lenders to better reflect risk and value and to develop a more creative approach that better meets the needs of Minority and Low to Moderate Income Census tracts.

o The Cities can urge lenders to undertake a thorough review of their policies and practices to determine where disparities might exist. This information should be a basis for developing new loan origination and other decision making processes in an aggressive marketing plan to turn around the traditional treatment of minority homeseekers and the neighborhoods where they wish to purchase or improve housing. This requires setting goals, conveying the message to all levels of employees, aggressive outreach to people in minority, racially changing, and lower-income areas, and, where appropriate, providing new programs to reach potential lower-income borrowers. Such programs include reducing down payments and incorporating rehabilitation and "sweat equity" in mortgages.

Recommendations

18 HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

RECOMMENDATION: Develop and implement innovative and effective solutions to reduce the number of loan applications denied due to collateral and authentically increase and stabilize property valuations.

Potential Action Steps:

o Evaluate the feasibility of creating maintenance and small improvement escrow accounts or other home modification programs for affordable home buyers and/or existing homeowners that can be supplemented with local, state, or federal dollars to help cover the cost of repairs and increase property values.

o Evaluate the feasibility of creating and implementing post-purchase support programs in conjunction with non-profit development partners to provide preventative maintenance training as well as organize neighborhood programming such as associations, crime watch, and other initiatives aimed at strengthening and maintaining neighborhood stability.

o Promote fundamental changes in the criteria used by appraisers and real estate brokers who together with lending institutions play a part in the ultimate decisions about making credit available to potential borrowers.

Work with the appraisal industry to develop a more creative approach that better meets the needs of Minority and Low to Moderate Income Census tracts.

Encourage comparability studies to identify real estate comparables that more realistically reflect the values of homes being built in low income areas and areas that have similar housing that can be used for comparison in establishing real estate values.

Consider incentives for lower loan amounts.

RECOMMENDATION: Identify lending institutions that should be contacted to explain their lending policies and/or practices. Questions could include asking such institutions if they have reviewed and documented the reasons for discrepancies in lending rates by race or ethnicity, and if not, why not. Lending institutions should carry out a thorough self-assessment of policies and procedures to determine where unnecessary and inappropriate criteria or assumptions serve as barriers to providing credit in such neighborhoods to such potential borrowers.

RECOMMENDATION: Support research, investigations, and enforcement of lending institutions and mortgage companies pertaining to disparities, predatory lending, redlining and other practices and policies that may limit fair access to credit opportunity and homeownership.

HMDA Data Analysis for the Cities of Muskegon, Muskegon Heights, and Norton Shores July 2019

Appendix A

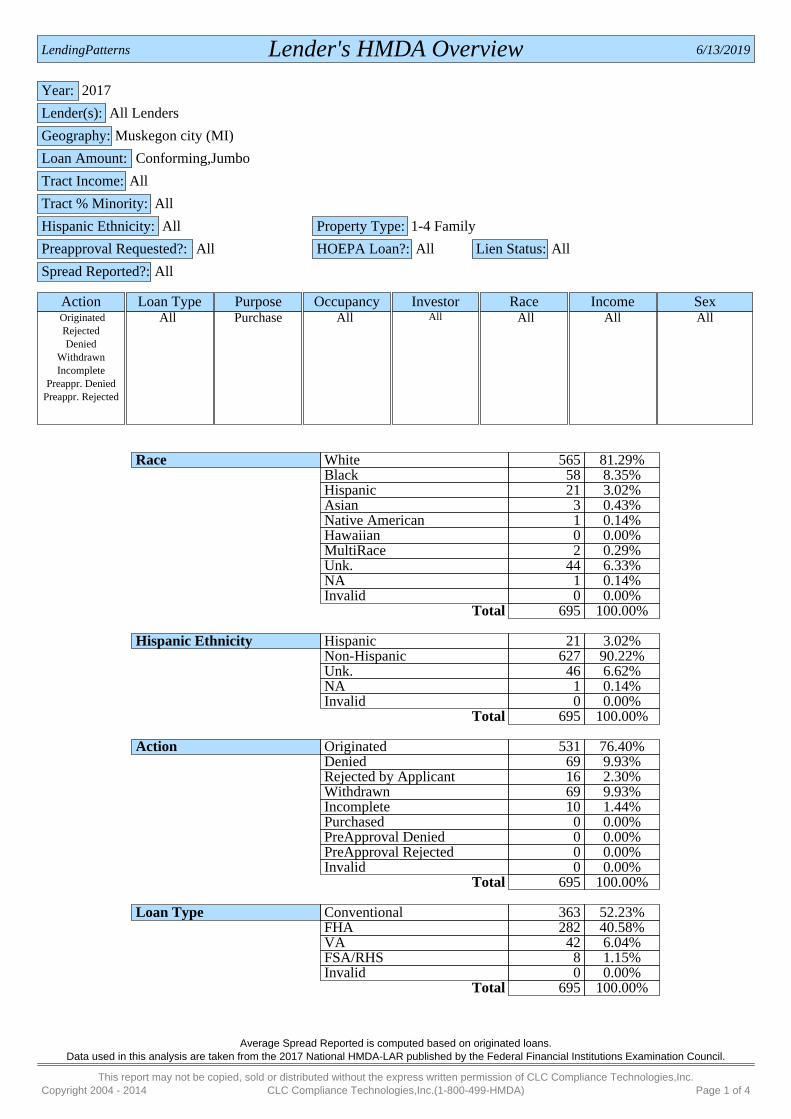

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

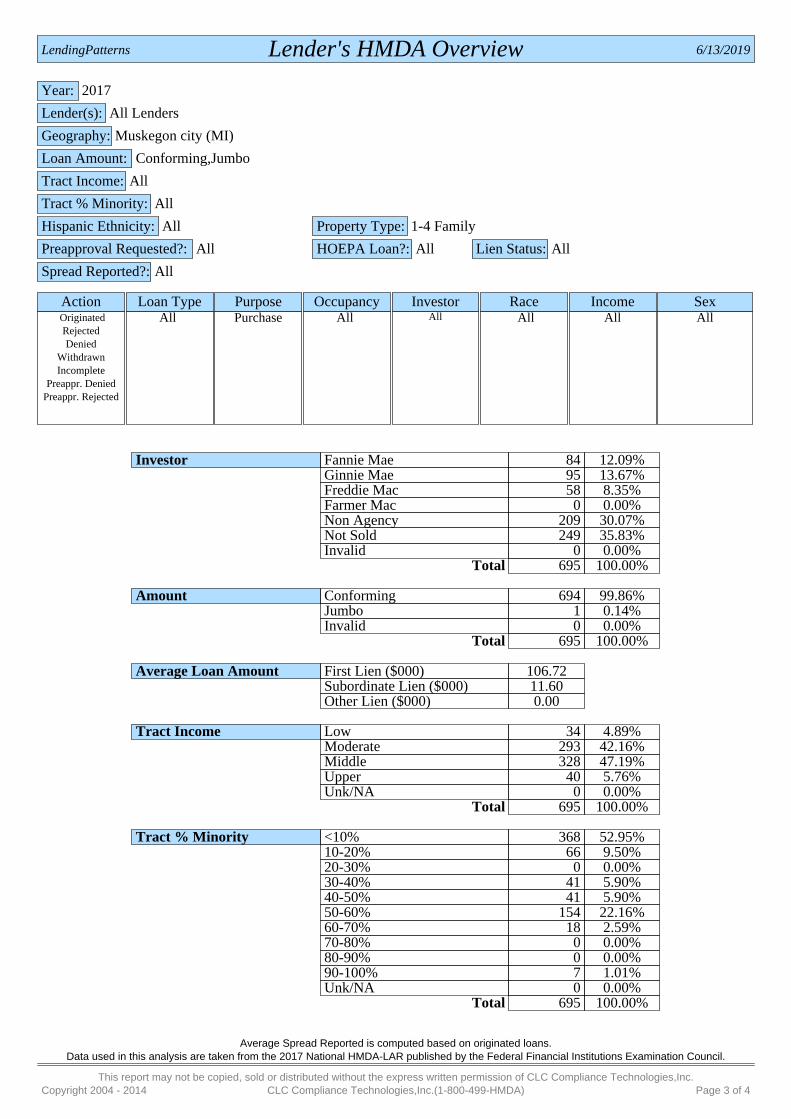

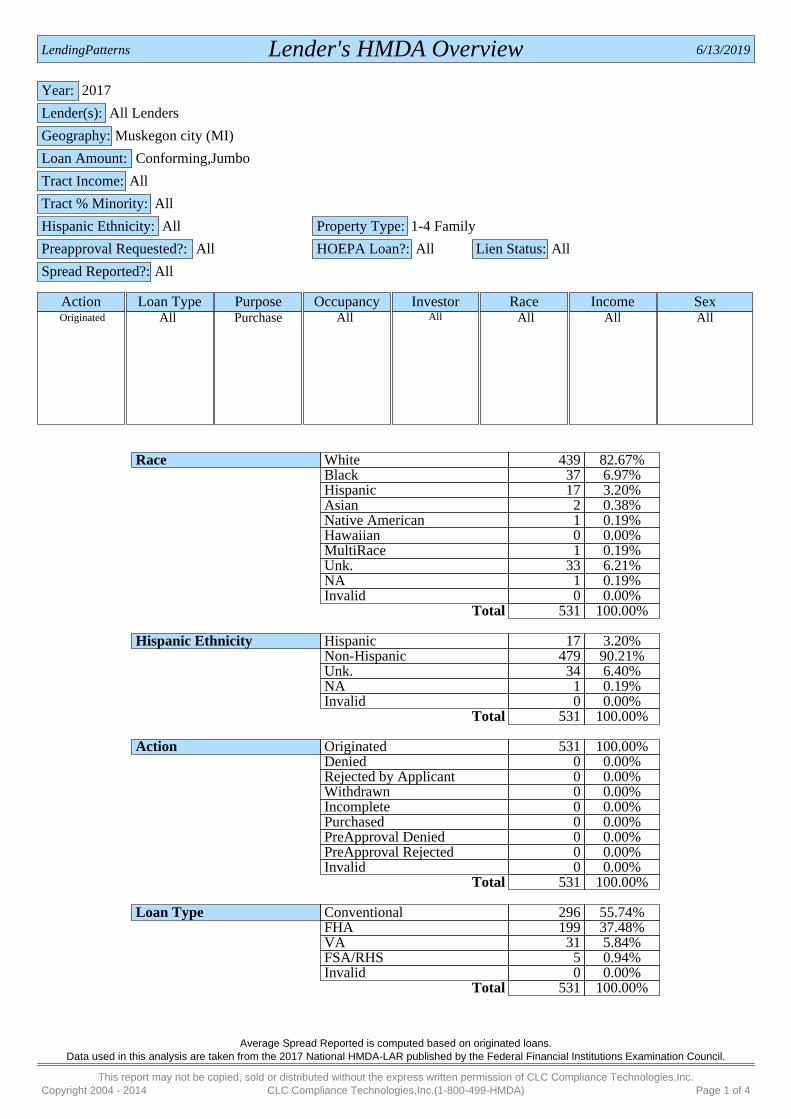

Race White 565 81.29%Black 58 8.35%Hispanic 21 3.02%Asian 3 0.43%Native American 1 0.14%Hawaiian 0 0.00%MultiRace 2 0.29%Unk. 44 6.33%NA 1 0.14%Invalid 0 0.00%

Total 695 100.00%

Hispanic Ethnicity Hispanic 21 3.02%Non-Hispanic 627 90.22%Unk. 46 6.62%NA 1 0.14%Invalid 0 0.00%

Total 695 100.00%

Action Originated 531 76.40%Denied 69 9.93%Rejected by Applicant 16 2.30%Withdrawn 69 9.93%Incomplete 10 1.44%Purchased 0 0.00%PreApproval Denied 0 0.00%PreApproval Rejected 0 0.00%Invalid 0 0.00%

Total 695 100.00%

Loan Type Conventional 363 52.23%FHA 282 40.58%VA 42 6.04%FSA/RHS 8 1.15%Invalid 0 0.00%

Total 695 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 1 of 4

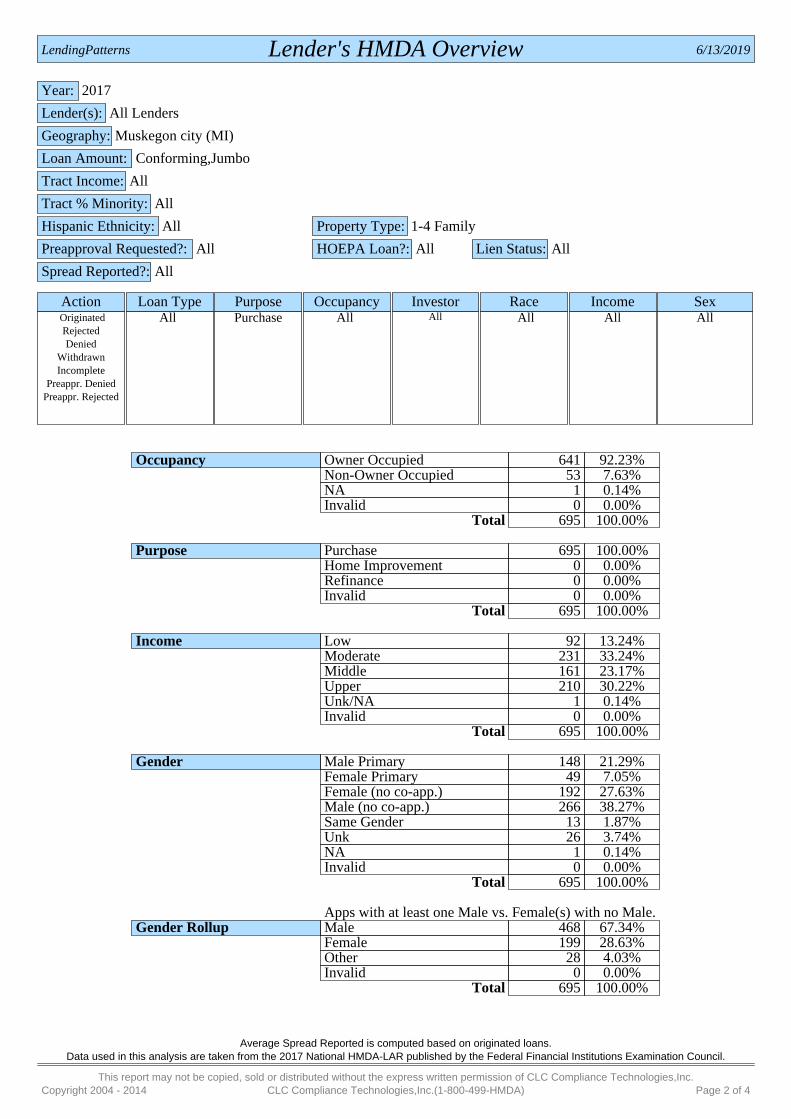

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

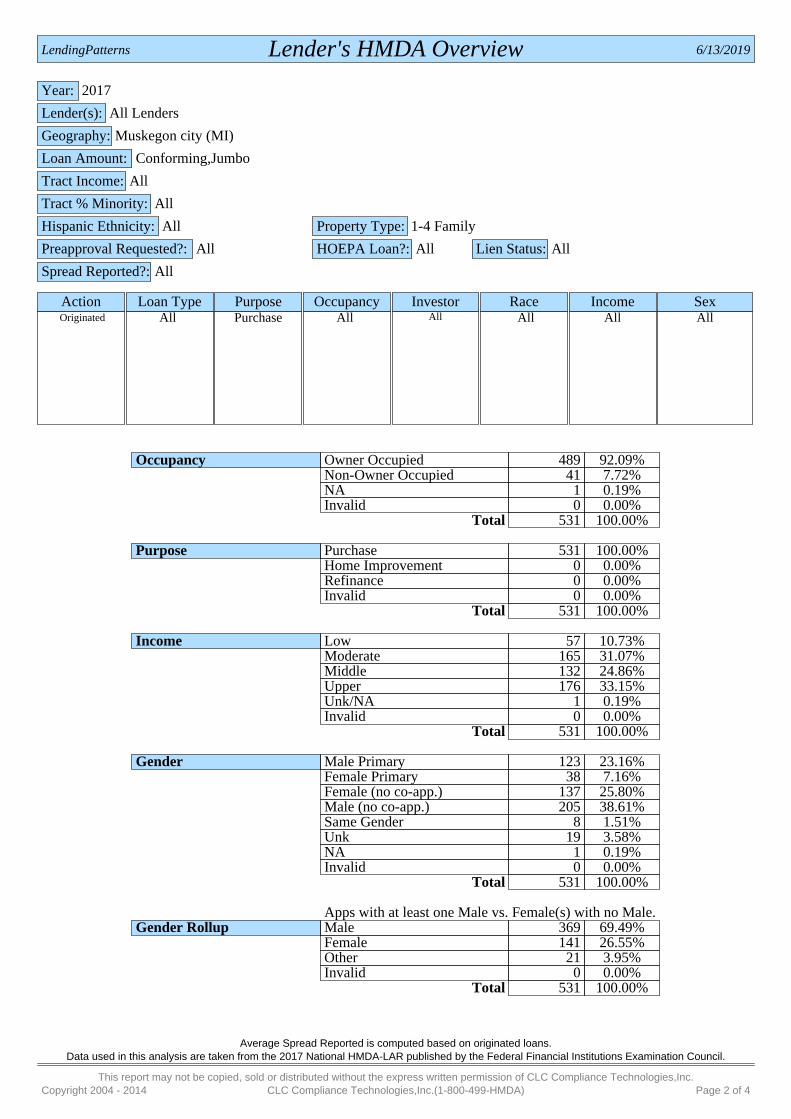

Occupancy Owner Occupied 641 92.23%Non-Owner Occupied 53 7.63%NA 1 0.14%Invalid 0 0.00%

Total 695 100.00%

Purpose Purchase 695 100.00%Home Improvement 0 0.00%Refinance 0 0.00%Invalid 0 0.00%

Total 695 100.00%

Income Low 92 13.24%Moderate 231 33.24%Middle 161 23.17%Upper 210 30.22%Unk/NA 1 0.14%Invalid 0 0.00%

Total 695 100.00%

Gender Male Primary 148 21.29%Female Primary 49 7.05%Female (no co-app.) 192 27.63%Male (no co-app.) 266 38.27%Same Gender 13 1.87%Unk 26 3.74%NA 1 0.14%Invalid 0 0.00%

Total 695 100.00%

Apps with at least one Male vs. Female(s) with no Male.Gender Rollup Male 468 67.34%

Female 199 28.63%Other 28 4.03%Invalid 0 0.00%

Total 695 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 2 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

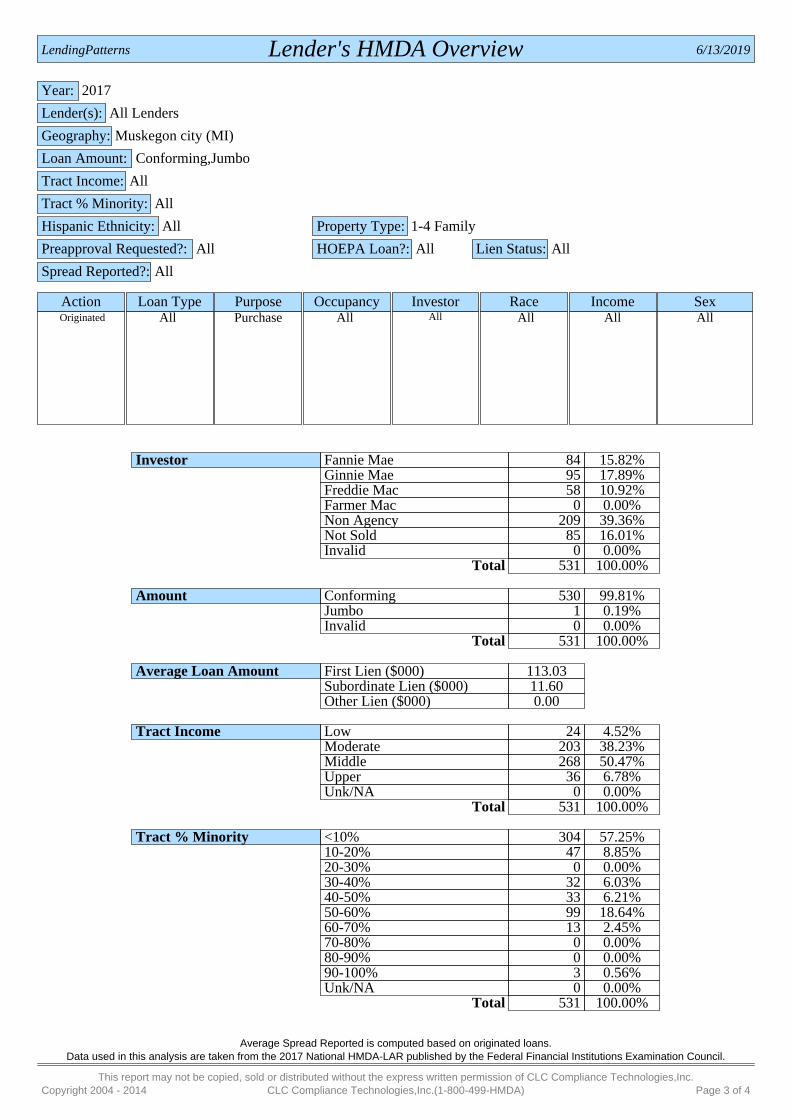

Investor Fannie Mae 84 12.09%Ginnie Mae 95 13.67%Freddie Mac 58 8.35%Farmer Mac 0 0.00%Non Agency 209 30.07%Not Sold 249 35.83%Invalid 0 0.00%

Total 695 100.00%

Amount Conforming 694 99.86%Jumbo 1 0.14%Invalid 0 0.00%

Total 695 100.00%

Average Loan Amount First Lien ($000) 106.72Subordinate Lien ($000) 11.60Other Lien ($000) 0.00

Tract Income Low 34 4.89%Moderate 293 42.16%Middle 328 47.19%Upper 40 5.76%Unk/NA 0 0.00%

Total 695 100.00%

Tract % Minority <10% 368 52.95%10-20% 66 9.50%20-30% 0 0.00%30-40% 41 5.90%40-50% 41 5.90%50-60% 154 22.16%60-70% 18 2.59%70-80% 0 0.00%80-90% 0 0.00%90-100% 7 1.01%Unk/NA 0 0.00%

Total 695 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 3 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

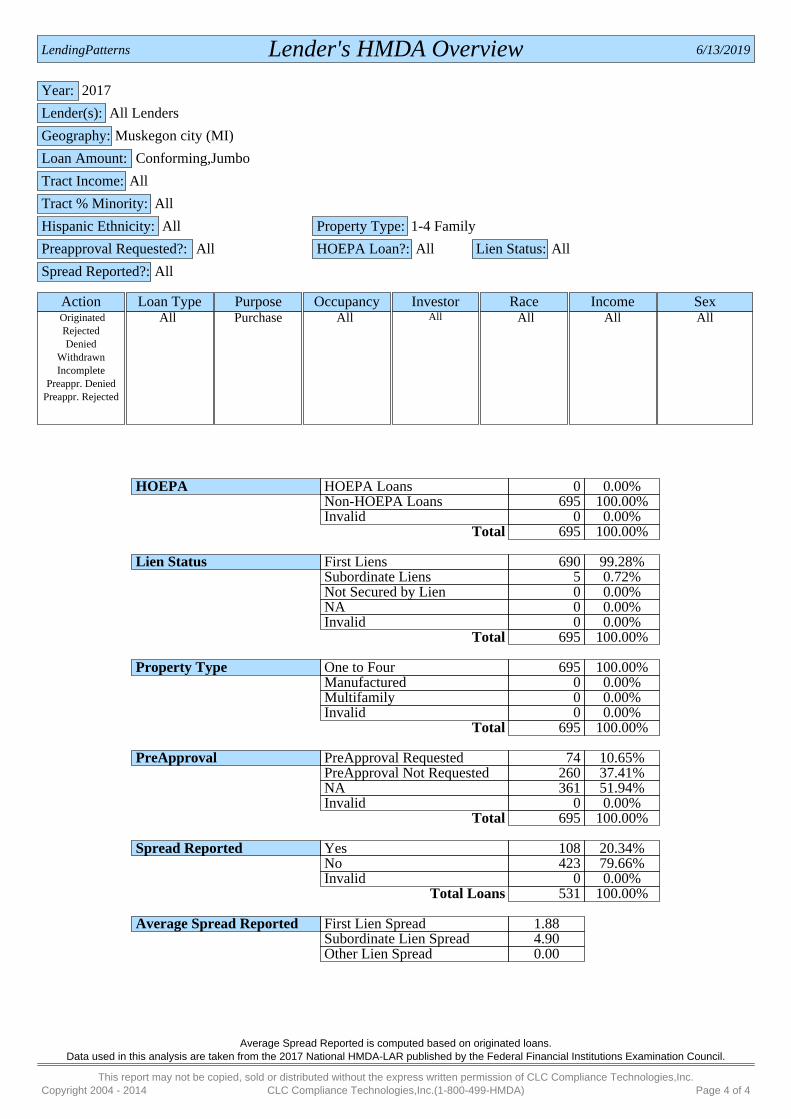

HOEPA HOEPA Loans 0 0.00%Non-HOEPA Loans 695 100.00%Invalid 0 0.00%

Total 695 100.00%

Lien Status First Liens 690 99.28%Subordinate Liens 5 0.72%Not Secured by Lien 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 695 100.00%

Property Type One to Four 695 100.00%Manufactured 0 0.00%Multifamily 0 0.00%Invalid 0 0.00%

Total 695 100.00%

PreApproval PreApproval Requested 74 10.65%PreApproval Not Requested 260 37.41%NA 361 51.94%Invalid 0 0.00%

Total 695 100.00%

Spread Reported Yes 108 20.34%No 423 79.66%Invalid 0 0.00%

Total Loans 531 100.00%

Average Spread Reported First Lien Spread 1.88Subordinate Lien Spread 4.90Other Lien Spread 0.00

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 4 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

Race White 439 82.67%Black 37 6.97%Hispanic 17 3.20%Asian 2 0.38%Native American 1 0.19%Hawaiian 0 0.00%MultiRace 1 0.19%Unk. 33 6.21%NA 1 0.19%Invalid 0 0.00%

Total 531 100.00%

Hispanic Ethnicity Hispanic 17 3.20%Non-Hispanic 479 90.21%Unk. 34 6.40%NA 1 0.19%Invalid 0 0.00%

Total 531 100.00%

Action Originated 531 100.00%Denied 0 0.00%Rejected by Applicant 0 0.00%Withdrawn 0 0.00%Incomplete 0 0.00%Purchased 0 0.00%PreApproval Denied 0 0.00%PreApproval Rejected 0 0.00%Invalid 0 0.00%

Total 531 100.00%

Loan Type Conventional 296 55.74%FHA 199 37.48%VA 31 5.84%FSA/RHS 5 0.94%Invalid 0 0.00%

Total 531 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 1 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

Occupancy Owner Occupied 489 92.09%Non-Owner Occupied 41 7.72%NA 1 0.19%Invalid 0 0.00%

Total 531 100.00%

Purpose Purchase 531 100.00%Home Improvement 0 0.00%Refinance 0 0.00%Invalid 0 0.00%

Total 531 100.00%

Income Low 57 10.73%Moderate 165 31.07%Middle 132 24.86%Upper 176 33.15%Unk/NA 1 0.19%Invalid 0 0.00%

Total 531 100.00%

Gender Male Primary 123 23.16%Female Primary 38 7.16%Female (no co-app.) 137 25.80%Male (no co-app.) 205 38.61%Same Gender 8 1.51%Unk 19 3.58%NA 1 0.19%Invalid 0 0.00%

Total 531 100.00%

Apps with at least one Male vs. Female(s) with no Male.Gender Rollup Male 369 69.49%

Female 141 26.55%Other 21 3.95%Invalid 0 0.00%

Total 531 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 2 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

Investor Fannie Mae 84 15.82%Ginnie Mae 95 17.89%Freddie Mac 58 10.92%Farmer Mac 0 0.00%Non Agency 209 39.36%Not Sold 85 16.01%Invalid 0 0.00%

Total 531 100.00%

Amount Conforming 530 99.81%Jumbo 1 0.19%Invalid 0 0.00%

Total 531 100.00%

Average Loan Amount First Lien ($000) 113.03Subordinate Lien ($000) 11.60Other Lien ($000) 0.00

Tract Income Low 24 4.52%Moderate 203 38.23%Middle 268 50.47%Upper 36 6.78%Unk/NA 0 0.00%

Total 531 100.00%

Tract % Minority <10% 304 57.25%10-20% 47 8.85%20-30% 0 0.00%30-40% 32 6.03%40-50% 33 6.21%50-60% 99 18.64%60-70% 13 2.45%70-80% 0 0.00%80-90% 0 0.00%90-100% 3 0.56%Unk/NA 0 0.00%

Total 531 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 3 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

HOEPA HOEPA Loans 0 0.00%Non-HOEPA Loans 531 100.00%Invalid 0 0.00%

Total 531 100.00%

Lien Status First Liens 526 99.06%Subordinate Liens 5 0.94%Not Secured by Lien 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 531 100.00%

Property Type One to Four 531 100.00%Manufactured 0 0.00%Multifamily 0 0.00%Invalid 0 0.00%

Total 531 100.00%

PreApproval PreApproval Requested 53 9.98%PreApproval Not Requested 200 37.66%NA 278 52.35%Invalid 0 0.00%

Total 531 100.00%

Spread Reported Yes 108 20.34%No 423 79.66%Invalid 0 0.00%

Total Loans 531 100.00%

Average Spread Reported First Lien Spread 1.88Subordinate Lien Spread 4.90Other Lien Spread 0.00

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 4 of 4

Lender's HMDA OverviewLendingPatterns 5/29/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

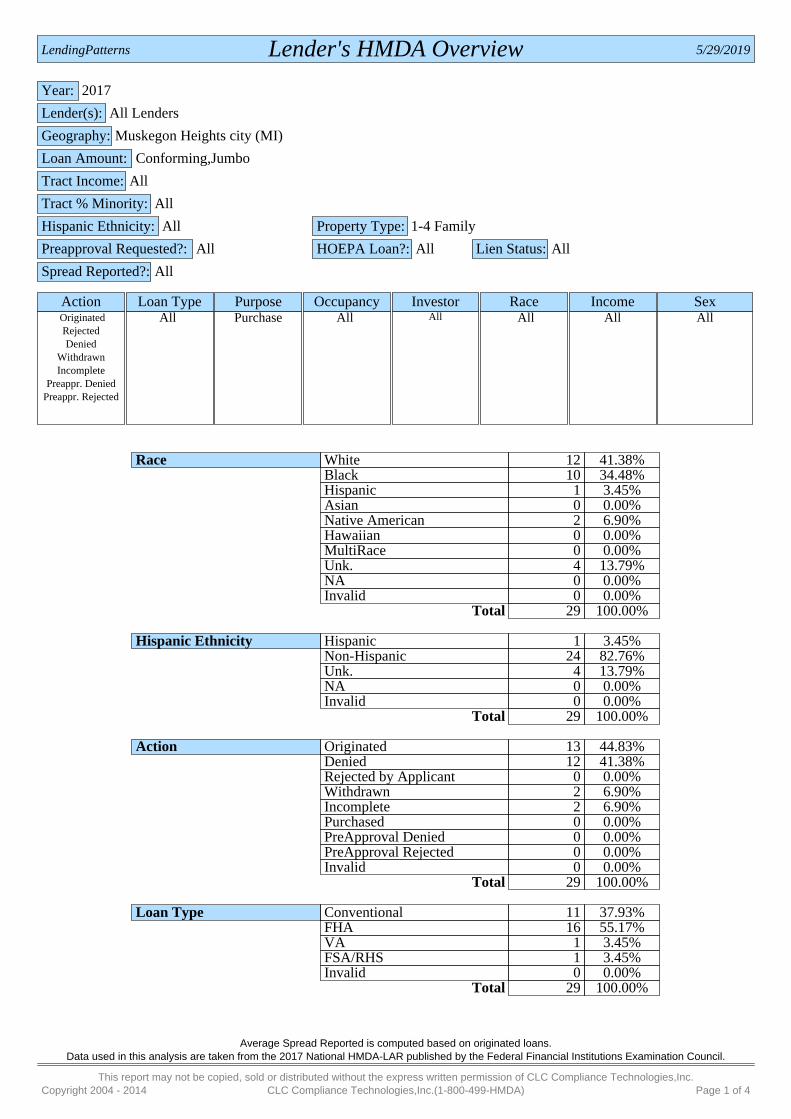

Race White 12 41.38%Black 10 34.48%Hispanic 1 3.45%Asian 0 0.00%Native American 2 6.90%Hawaiian 0 0.00%MultiRace 0 0.00%Unk. 4 13.79%NA 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Hispanic Ethnicity Hispanic 1 3.45%Non-Hispanic 24 82.76%Unk. 4 13.79%NA 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Action Originated 13 44.83%Denied 12 41.38%Rejected by Applicant 0 0.00%Withdrawn 2 6.90%Incomplete 2 6.90%Purchased 0 0.00%PreApproval Denied 0 0.00%PreApproval Rejected 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Loan Type Conventional 11 37.93%FHA 16 55.17%VA 1 3.45%FSA/RHS 1 3.45%Invalid 0 0.00%

Total 29 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 1 of 4

Lender's HMDA OverviewLendingPatterns 5/29/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

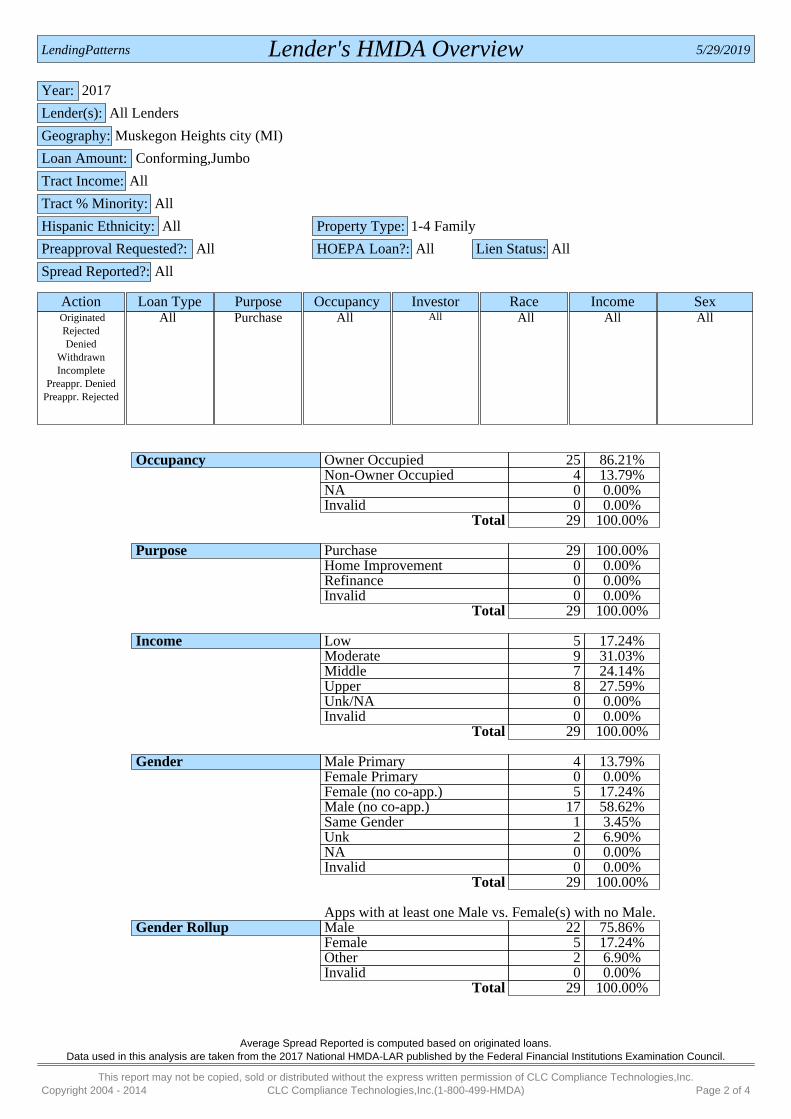

Occupancy Owner Occupied 25 86.21%Non-Owner Occupied 4 13.79%NA 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Purpose Purchase 29 100.00%Home Improvement 0 0.00%Refinance 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Income Low 5 17.24%Moderate 9 31.03%Middle 7 24.14%Upper 8 27.59%Unk/NA 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Gender Male Primary 4 13.79%Female Primary 0 0.00%Female (no co-app.) 5 17.24%Male (no co-app.) 17 58.62%Same Gender 1 3.45%Unk 2 6.90%NA 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Apps with at least one Male vs. Female(s) with no Male.Gender Rollup Male 22 75.86%

Female 5 17.24%Other 2 6.90%Invalid 0 0.00%

Total 29 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 2 of 4

Lender's HMDA OverviewLendingPatterns 5/29/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

Investor Fannie Mae 2 6.90%Ginnie Mae 3 10.34%Freddie Mac 1 3.45%Farmer Mac 0 0.00%Non Agency 6 20.69%Not Sold 17 58.62%Invalid 0 0.00%

Total 29 100.00%

Amount Conforming 29 100.00%Jumbo 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Average Loan Amount First Lien ($000) 58.00Subordinate Lien ($000) 0.00Other Lien ($000) 0.00

Tract Income Low 18 62.07%Moderate 11 37.93%Middle 0 0.00%Upper 0 0.00%Unk/NA 0 0.00%

Total 29 100.00%

Tract % Minority <10% 0 0.00%10-20% 0 0.00%20-30% 0 0.00%30-40% 0 0.00%40-50% 0 0.00%50-60% 0 0.00%60-70% 16 55.17%70-80% 0 0.00%80-90% 4 13.79%90-100% 9 31.03%Unk/NA 0 0.00%

Total 29 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 3 of 4

Lender's HMDA OverviewLendingPatterns 5/29/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

HOEPA HOEPA Loans 0 0.00%Non-HOEPA Loans 29 100.00%Invalid 0 0.00%

Total 29 100.00%

Lien Status First Liens 29 100.00%Subordinate Liens 0 0.00%Not Secured by Lien 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 29 100.00%

Property Type One to Four 29 100.00%Manufactured 0 0.00%Multifamily 0 0.00%Invalid 0 0.00%

Total 29 100.00%

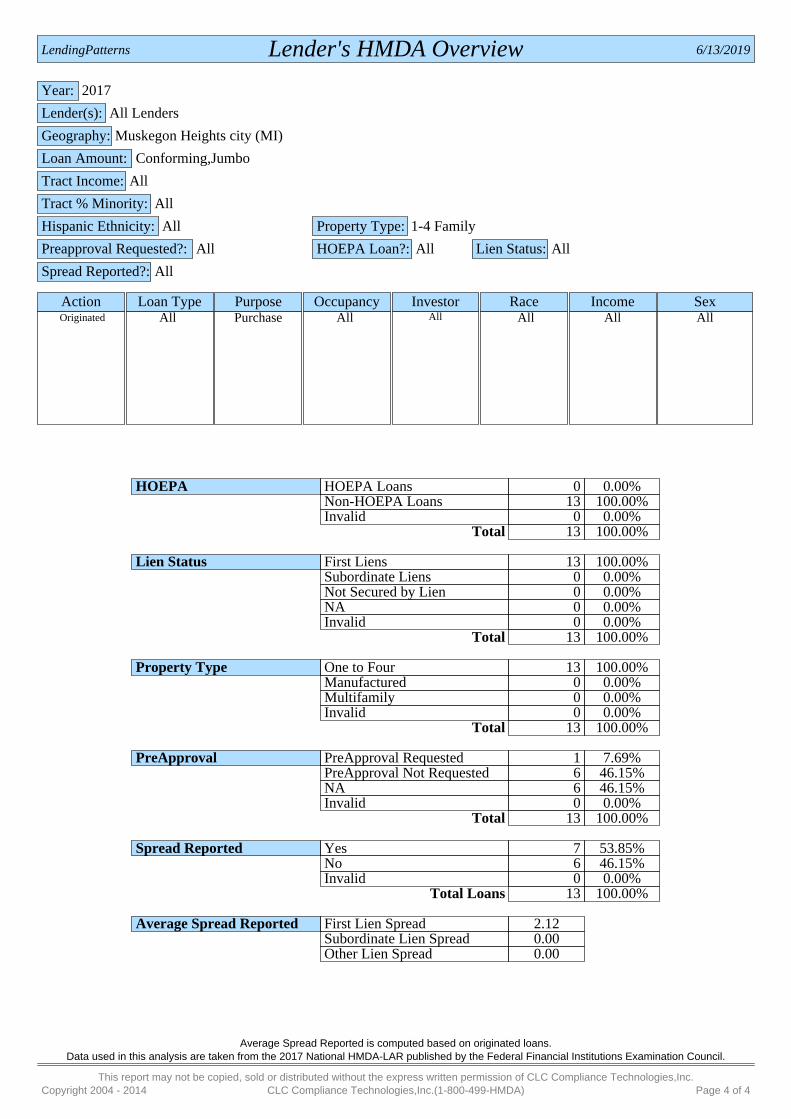

PreApproval PreApproval Requested 2 6.90%PreApproval Not Requested 8 27.59%NA 19 65.52%Invalid 0 0.00%

Total 29 100.00%

Spread Reported Yes 7 53.85%No 6 46.15%Invalid 0 0.00%

Total Loans 13 100.00%

Average Spread Reported First Lien Spread 2.12Subordinate Lien Spread 0.00Other Lien Spread 0.00

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 4 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

Race White 7 53.85%Black 5 38.46%Hispanic 0 0.00%Asian 0 0.00%Native American 1 7.69%Hawaiian 0 0.00%MultiRace 0 0.00%Unk. 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Hispanic Ethnicity Hispanic 0 0.00%Non-Hispanic 12 92.31%Unk. 1 7.69%NA 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Action Originated 13 100.00%Denied 0 0.00%Rejected by Applicant 0 0.00%Withdrawn 0 0.00%Incomplete 0 0.00%Purchased 0 0.00%PreApproval Denied 0 0.00%PreApproval Rejected 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Loan Type Conventional 4 30.77%FHA 9 69.23%VA 0 0.00%FSA/RHS 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 1 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

Occupancy Owner Occupied 12 92.31%Non-Owner Occupied 1 7.69%NA 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Purpose Purchase 13 100.00%Home Improvement 0 0.00%Refinance 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Income Low 2 15.38%Moderate 6 46.15%Middle 3 23.08%Upper 2 15.38%Unk/NA 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Gender Male Primary 1 7.69%Female Primary 0 0.00%Female (no co-app.) 4 30.77%Male (no co-app.) 8 61.54%Same Gender 0 0.00%Unk 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Apps with at least one Male vs. Female(s) with no Male.Gender Rollup Male 9 69.23%

Female 4 30.77%Other 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 2 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

Investor Fannie Mae 2 15.38%Ginnie Mae 3 23.08%Freddie Mac 1 7.69%Farmer Mac 0 0.00%Non Agency 6 46.15%Not Sold 1 7.69%Invalid 0 0.00%

Total 13 100.00%

Amount Conforming 13 100.00%Jumbo 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Average Loan Amount First Lien ($000) 59.23Subordinate Lien ($000) 0.00Other Lien ($000) 0.00

Tract Income Low 8 61.54%Moderate 5 38.46%Middle 0 0.00%Upper 0 0.00%Unk/NA 0 0.00%

Total 13 100.00%

Tract % Minority <10% 0 0.00%10-20% 0 0.00%20-30% 0 0.00%30-40% 0 0.00%40-50% 0 0.00%50-60% 0 0.00%60-70% 8 61.54%70-80% 0 0.00%80-90% 2 15.38%90-100% 3 23.08%Unk/NA 0 0.00%

Total 13 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 3 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Muskegon Heights city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

HOEPA HOEPA Loans 0 0.00%Non-HOEPA Loans 13 100.00%Invalid 0 0.00%

Total 13 100.00%

Lien Status First Liens 13 100.00%Subordinate Liens 0 0.00%Not Secured by Lien 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 13 100.00%

Property Type One to Four 13 100.00%Manufactured 0 0.00%Multifamily 0 0.00%Invalid 0 0.00%

Total 13 100.00%

PreApproval PreApproval Requested 1 7.69%PreApproval Not Requested 6 46.15%NA 6 46.15%Invalid 0 0.00%

Total 13 100.00%

Spread Reported Yes 7 53.85%No 6 46.15%Invalid 0 0.00%

Total Loans 13 100.00%

Average Spread Reported First Lien Spread 2.12Subordinate Lien Spread 0.00Other Lien Spread 0.00

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 4 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Norton Shores city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

Race White 469 85.43%Black 23 4.19%Hispanic 24 4.37%Asian 2 0.36%Native American 3 0.55%Hawaiian 0 0.00%MultiRace 1 0.18%Unk. 27 4.92%NA 0 0.00%Invalid 0 0.00%

Total 549 100.00%

Hispanic Ethnicity Hispanic 24 4.37%Non-Hispanic 494 89.98%Unk. 31 5.65%NA 0 0.00%Invalid 0 0.00%

Total 549 100.00%

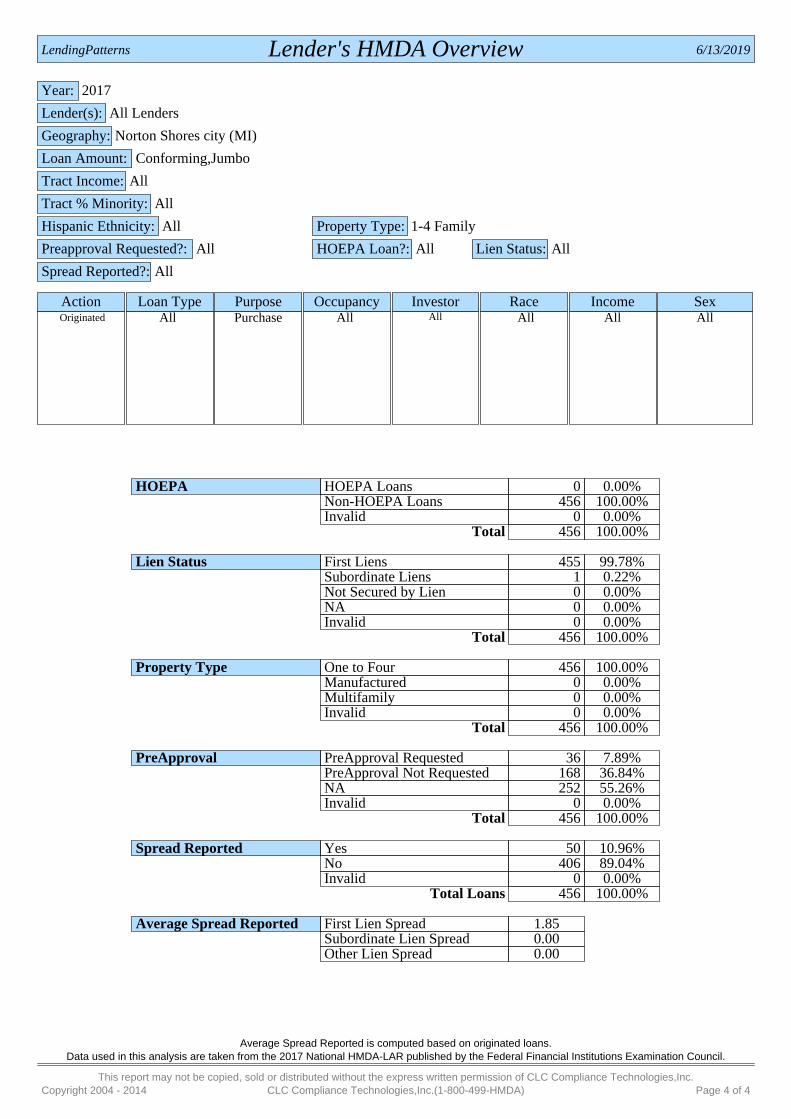

Action Originated 456 83.06%Denied 35 6.38%Rejected by Applicant 11 2.00%Withdrawn 39 7.10%Incomplete 8 1.46%Purchased 0 0.00%PreApproval Denied 0 0.00%PreApproval Rejected 0 0.00%Invalid 0 0.00%

Total 549 100.00%

Loan Type Conventional 359 65.39%FHA 158 28.78%VA 32 5.83%FSA/RHS 0 0.00%Invalid 0 0.00%

Total 549 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 1 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Norton Shores city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

Occupancy Owner Occupied 513 93.44%Non-Owner Occupied 35 6.38%NA 1 0.18%Invalid 0 0.00%

Total 549 100.00%

Purpose Purchase 549 100.00%Home Improvement 0 0.00%Refinance 0 0.00%Invalid 0 0.00%

Total 549 100.00%

Income Low 37 6.74%Moderate 136 24.77%Middle 143 26.05%Upper 229 41.71%Unk/NA 4 0.73%Invalid 0 0.00%

Total 549 100.00%

Gender Male Primary 152 27.69%Female Primary 37 6.74%Female (no co-app.) 125 22.77%Male (no co-app.) 199 36.25%Same Gender 18 3.28%Unk 18 3.28%NA 0 0.00%Invalid 0 0.00%

Total 549 100.00%

Apps with at least one Male vs. Female(s) with no Male.Gender Rollup Male 399 72.68%

Female 132 24.04%Other 18 3.28%Invalid 0 0.00%

Total 549 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 2 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Norton Shores city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

Investor Fannie Mae 84 15.30%Ginnie Mae 61 11.11%Freddie Mac 59 10.75%Farmer Mac 0 0.00%Non Agency 196 35.70%Not Sold 149 27.14%Invalid 0 0.00%

Total 549 100.00%

Amount Conforming 540 98.36%Jumbo 9 1.64%Invalid 0 0.00%

Total 549 100.00%

Average Loan Amount First Lien ($000) 149.62Subordinate Lien ($000) 106.00Other Lien ($000) 0.00

Tract Income Low 16 2.91%Moderate 33 6.01%Middle 0 0.00%Upper 500 91.07%Unk/NA 0 0.00%

Total 549 100.00%

Tract % Minority <10% 187 34.06%10-20% 346 63.02%20-30% 0 0.00%30-40% 0 0.00%40-50% 0 0.00%50-60% 0 0.00%60-70% 16 2.91%70-80% 0 0.00%80-90% 0 0.00%90-100% 0 0.00%Unk/NA 0 0.00%

Total 549 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 3 of 4

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Norton Shores city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated

RejectedDenied

WithdrawnIncomplete

Preappr. DeniedPreappr. Rejected

All Purchase All All All All All

HOEPA HOEPA Loans 0 0.00%Non-HOEPA Loans 549 100.00%Invalid 0 0.00%

Total 549 100.00%

Lien Status First Liens 547 99.64%Subordinate Liens 2 0.36%Not Secured by Lien 0 0.00%NA 0 0.00%Invalid 0 0.00%

Total 549 100.00%

Property Type One to Four 549 100.00%Manufactured 0 0.00%Multifamily 0 0.00%Invalid 0 0.00%

Total 549 100.00%

PreApproval PreApproval Requested 44 8.01%PreApproval Not Requested 197 35.88%NA 308 56.10%Invalid 0 0.00%

Total 549 100.00%

Spread Reported Yes 50 10.96%No 406 89.04%Invalid 0 0.00%

Total Loans 456 100.00%

Average Spread Reported First Lien Spread 1.85Subordinate Lien Spread 0.00Other Lien Spread 0.00

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 4 of 4

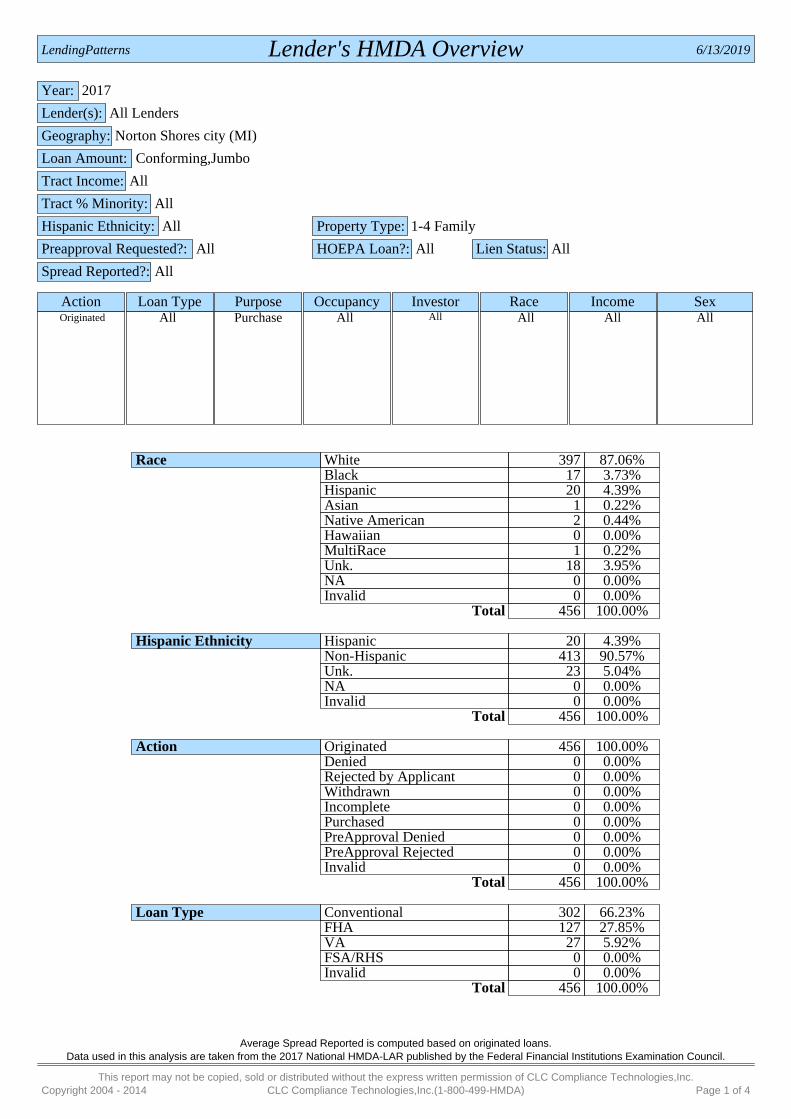

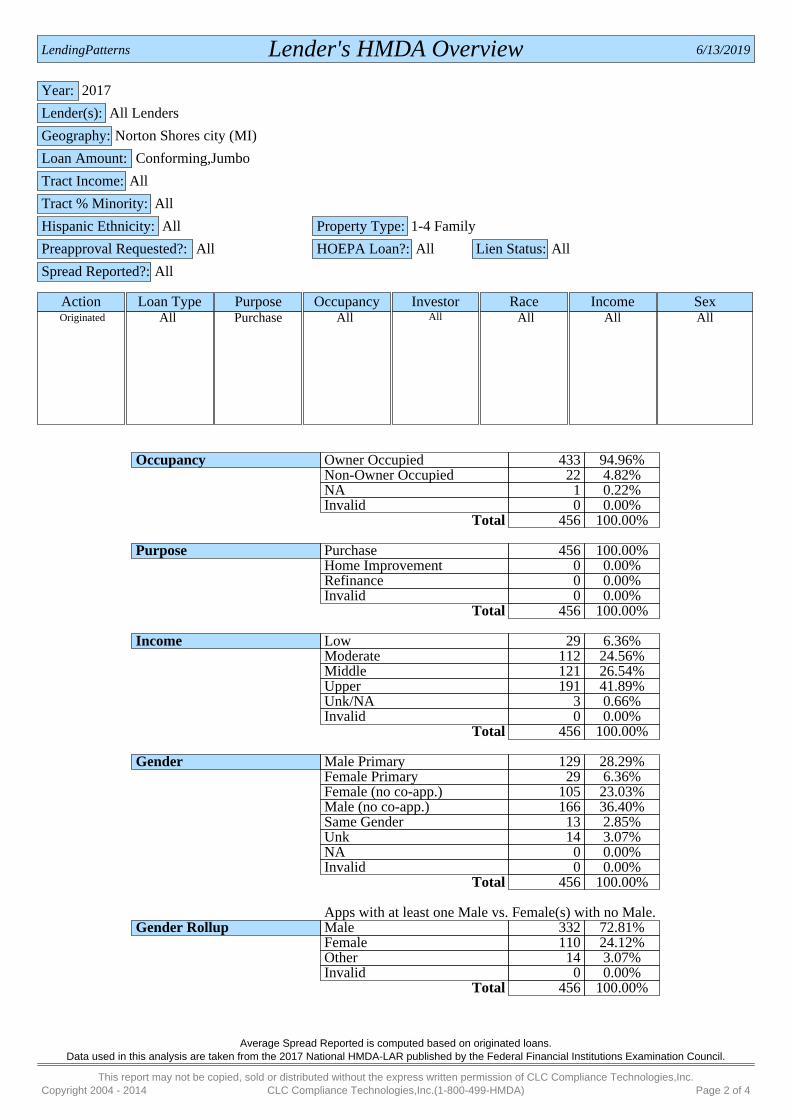

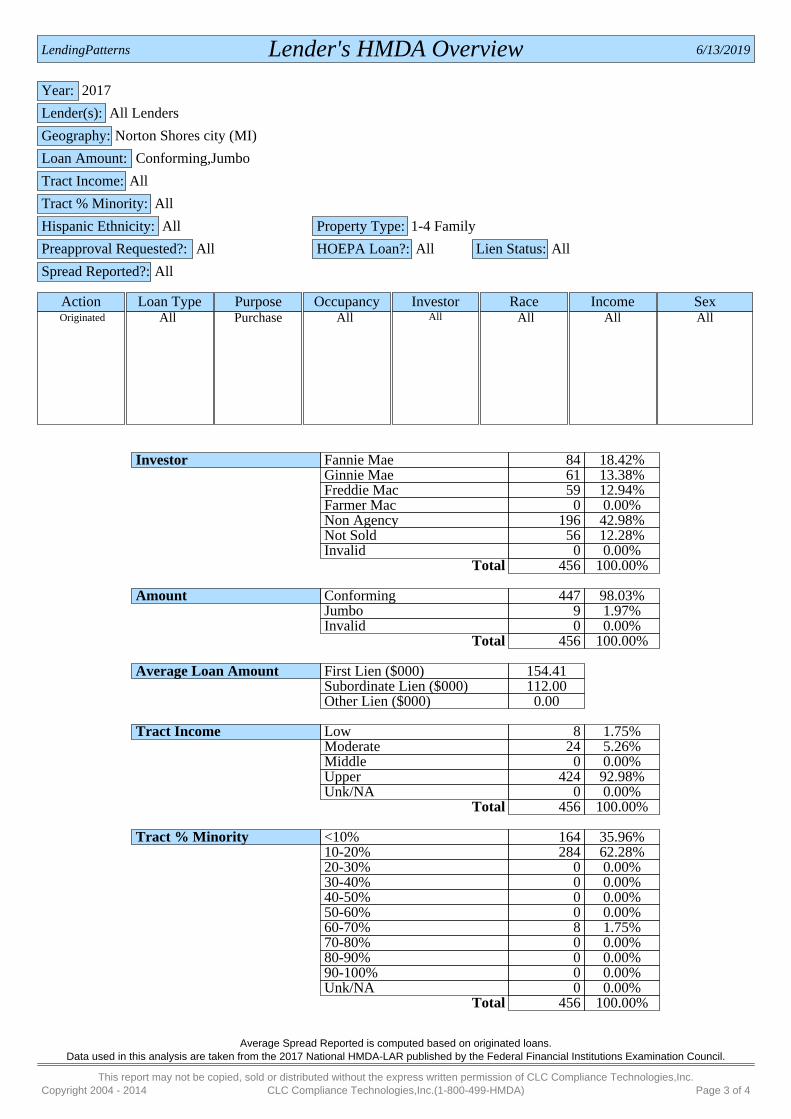

Lender's HMDA OverviewLendingPatterns 6/13/2019

Year: 2017

Lender(s): All Lenders

Geography: Norton Shores city (MI)

Loan Amount: Conforming,Jumbo

Tract Income: All

Tract % Minority: All

Hispanic Ethnicity: All Property Type: 1-4 Family

Preapproval Requested?: All HOEPA Loan?: All Lien Status: All

Spread Reported?: All

Action Loan Type Purpose Occupancy Investor Race Income Sex Originated All Purchase All All All All All

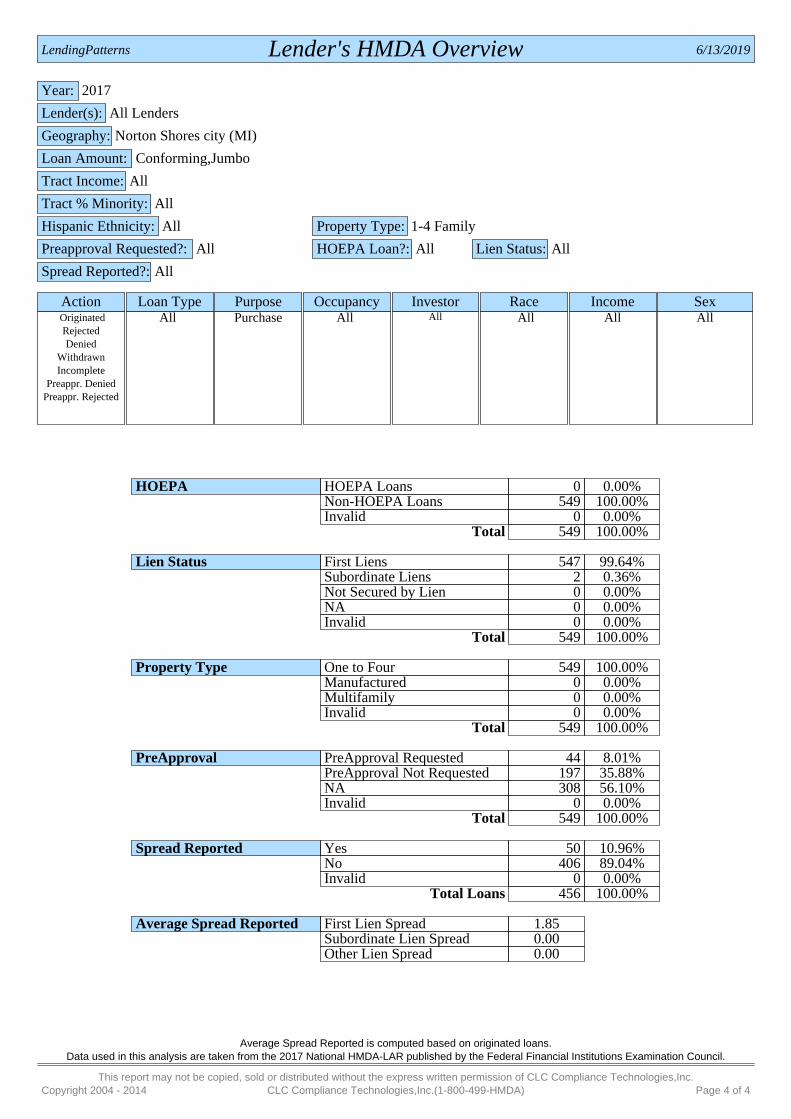

Race White 397 87.06%Black 17 3.73%Hispanic 20 4.39%Asian 1 0.22%Native American 2 0.44%Hawaiian 0 0.00%MultiRace 1 0.22%Unk. 18 3.95%NA 0 0.00%Invalid 0 0.00%

Total 456 100.00%

Hispanic Ethnicity Hispanic 20 4.39%Non-Hispanic 413 90.57%Unk. 23 5.04%NA 0 0.00%Invalid 0 0.00%

Total 456 100.00%

Action Originated 456 100.00%Denied 0 0.00%Rejected by Applicant 0 0.00%Withdrawn 0 0.00%Incomplete 0 0.00%Purchased 0 0.00%PreApproval Denied 0 0.00%PreApproval Rejected 0 0.00%Invalid 0 0.00%

Total 456 100.00%

Loan Type Conventional 302 66.23%FHA 127 27.85%VA 27 5.92%FSA/RHS 0 0.00%Invalid 0 0.00%

Total 456 100.00%

Average Spread Reported is computed based on originated loans.Data used in this analysis are taken from the 2017 National HMDA-LAR published by the Federal Financial Institutions Examination Council.

This report may not be copied, sold or distributed without the express written permission of CLC Compliance Technologies,Inc.Copyright 2004 - 2014 CLC Compliance Technologies,Inc.(1-800-499-HMDA) Page 1 of 4