horizon scanning - eversheds · pdf fileretail finance round-up key developments in 2015 and...

TRANSCRIPT

Horizon scanning Retail finance round-up

Key developments in 2015 and horizon scanning for 2016

Retail finance round-up

Key developments in 2015 and horizon scanning for 2016

With the retail finance sector experiencing significant regulatory and legislative change, we reflect on the key developments in retail finance from 2015 and examine the outlook for 2016: What are the key themes and dates for the year ahead and what action do you need to take to prepare?

The regulatory landscape

It was a year of change for the Financial Conduct Authority. Martin Wheatley, who had led the FCA from its inception and during a time of record fines, stepped down as Chief Executive in September. Tracey McDermott, former Director of Supervision, moved up as temporary CEO. Chancellor George Osborne had said a “different leadership” was needed to take the regulator forward. The FCA is now undertaking a global search to recruit for Mr Wheatley’s permanent replacement. With three new board members also being recruited this year, how will the regulatory landscape change in 2016?

The emphasis is shifting from managing and mitigating risk to facilitating competition and embracing innovation. This change is reflected in the key themes emerging from the regulator.

Some areas of focus remain firmly on the agenda. As identified in its Business Plan for 2015/2016 published in March 2015, poor culture and control remains a high priority as does the pace of technological change, with the FCA concerned that the rapid development may outstrip firms’ investment, consumer capabilities and regulatory response. To assist firms with the challenges presented by technological change, the FCA launched Project Innovate at the end of 2014. Many of our clients are focused on digital projects. Our digital team is running a series of events through 2016 to build on the major event we held last year.

It has been an intense period of activity for the consumer credit sector. Nearly two years on from the transfer of regulation from the Office of Fair Trading to the FCA, the authorisation process is nearing completion. The allocated application periods for full authorisation are due to run until 31 March 2016. The FCA consulted on changes to the Consumer Credit Sourcebook (CONC) in February and amended rules came into force in November covering in particular financial promotions and joint borrowers. Looking ahead, the FCA will continue to focus on the consumer credit sector, identifying two areas specific to the sector in its Business Plan: Poor culture and practice in consumer credit affordability assessments; and a range of issues in unfair contract terms given sharper focus by developments in legislation (such as Consumer Rights Act) and legal precedents (following a number of cases before the European Court of Justice).

So against that background, we have set out below 12 key developments you should be aware of for 2015 and what to expect in these areas in the period ahead.

“We need to make sure that we have a landscape that ensures clean markets and protects consumers through fostering competition and innovation. A sustainable approach to regulation, which breaks the regulate, deregulate, repeat cycle is critical to that. This requires all of us – regulators, firms, and individuals alike – to play our part in changing the way financial services operates, not just for now but for the long term.”

Tracey McDermott: The Rapidity of Change delivered on 22 October 2015 at the City Banquet - Mansion House

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

3

Key developments for 2015

1. Senior Managers regime

In July 2015, the FCA and the PRA published the final rules (the Rules) aimed at improving individual accountability within the banking sector. The Rules cover the Senior Managers Regime, the Certification Regime and the Conduct Rules. The Senior Managers Regime allocates responsibility for certain areas of the business to senior personnel within the firm. Those who fall under the regime will continue to be pre-approved by regulators and firms must also ensure that procedures in place allow them to assess the fitness and propriety of staff. The Certification Regime applies to those who pose a significant risk of harm to the firm or any of its customers. The Conduct Rules then set out basic standards of behaviour which are expected of all staff, except those in ancillary functions.

Further clarification on the new regime was provided in a policy paper published in October. That made clear that senior managers would be subject to a new statutory duty of responsibility to take reasonable steps to prevent regulatory breaches in the areas of the firm for which they are responsible. The burden of proof will fall on the regulator.

In December, the FCA published Policy Statement PS15/29 setting out final amendments to the Decision Procedure and Penalties Manual (DEPP) and Enforcement Guide (EG) in light of the new accountability regime. Under the Banking Reform Act, in the new regime, senior managers may be prosecuted by the PRA or FCA in certain prescribed circumstances for taking a decision which caused a financial institution to fail. In PS15/29 the FCA explains that it has decided not to give guidance on the standards expected of senior managers specifically in relation to this offence because significant guidance is already available in the FCA Handbook.

The Senior Managers Regime will commence from 7 March 2016 for senior bankers. HM Treasury announced in October that it plans to extend the regime to all firms regulated by the FCA, including consumer credit firms. HM Treasury has introduced a Bill to Parliament and implementation is likely to be in 2018.

In the context of the new Senior Managers Regime, Martin Wheatley, the then FCA chief executive, commented: “Today’s rules are the latest changes aimed at embedding personal accountability in the culture of financial services and are a crucial step in rebuilding public trust.”

2. Consumer vulnerability

While there are already FCA Principles, Rules and Guidance in existence, the FCA is keen to broaden understanding and stimulate debate on consumer vulnerability and published its Occasional Paper 8 in February 2015. The paper aimed to provide practical help to firms in developing and implementing a vulnerability strategy. We summarised the challenges and our practical suggestions for dealing with vulnerability in a briefing earlier this year.

“A vulnerable customer is someone, who due to their personal circumstances, is especially susceptible to detriment, particularly when a firm is not acting with appropriate levels of care”. FCA Occasional Paper 8 – February 2015

There is no doubt that this is an issue rising up the regulatory agenda. In September, the British Banking Association (BBA) announced the launch of a Financial Services Vulnerability Taskforce by the financial services industry in a joint initiative with various charities and consumer groups. It will identify where good practice exists in the financial services sector, what practices exist in other sectors and where gaps in policy or systems could be improved. The Taskforce is expected to make recommendations for the adoption of best practice across the industry within six months.

Whilst we all anticipate with interest the outputs of the BBA taskforce, it is vital that firms review their current practices in respect of customer vulnerability. FCA activity in this area is set to increase as the FCA is concerned that vulnerability is often missed or when identified, appropriate measures are not implemented to ensure the customer is treated fairly. We have seen an increasing amount of work in this area, and some crucial aspects firms should consider are: How do staff identify vulnerability; do we define vulnerability; and do we take positive actions when vulnerability is identified?

“The crux is that vulnerability is part of the overall desired outcome to treat customers fairly, and so it is imperative for firms to gain a ‘temperature check’ of their position with respect to the FCA’s expectations”

Noreen Husain, Regulatory Director, Eversheds

4

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

The crux is that vulnerability is part of the overall desired outcome to treat customers fairly, and so it is imperative for firms to gain a ‘temperature check’ of their position with respect to the FCA’s expectations.

3. Supervisory model

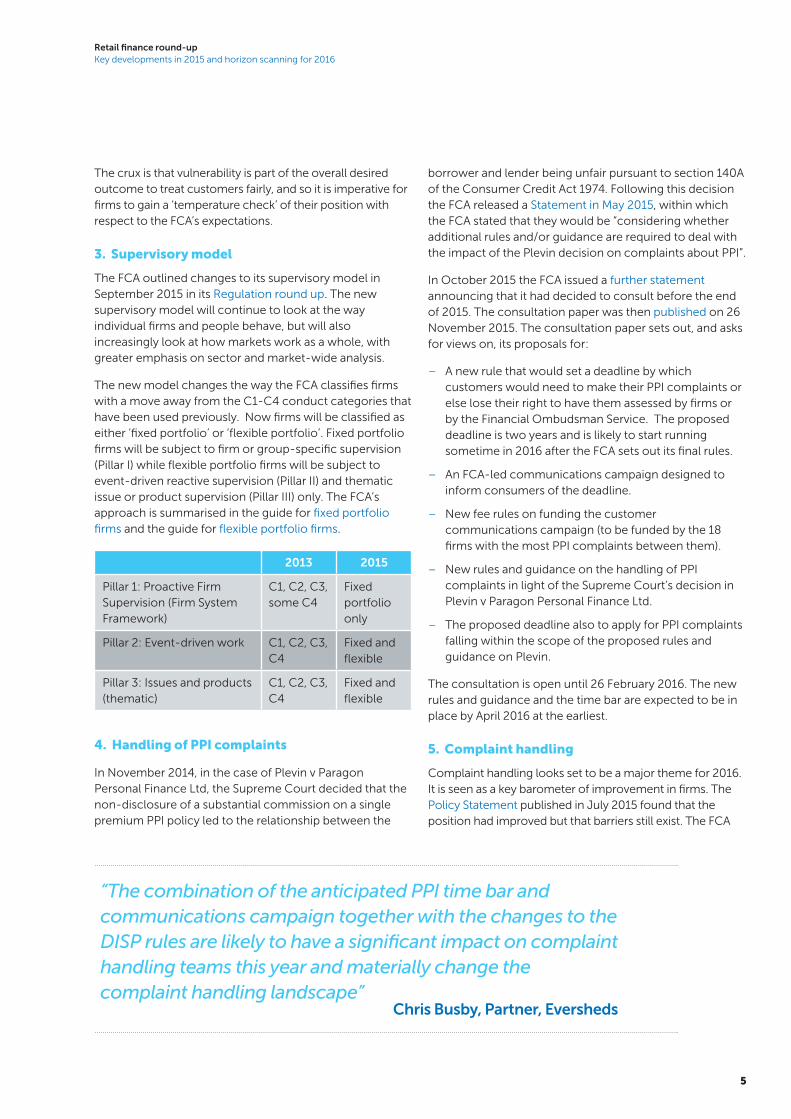

The FCA outlined changes to its supervisory model in September 2015 in its Regulation round up. The new supervisory model will continue to look at the way individual firms and people behave, but will also increasingly look at how markets work as a whole, with greater emphasis on sector and market-wide analysis.

The new model changes the way the FCA classifies firms with a move away from the C1-C4 conduct categories that have been used previously. Now firms will be classified as either ‘fixed portfolio’ or ‘flexible portfolio’. Fixed portfolio firms will be subject to firm or group-specific supervision (Pillar I) while flexible portfolio firms will be subject to event-driven reactive supervision (Pillar II) and thematic issue or product supervision (Pillar III) only. The FCA’s approach is summarised in the guide for fixed portfolio firms and the guide for flexible portfolio firms.

2013 2015

Pillar 1: Proactive Firm Supervision (Firm System Framework)

C1, C2, C3, some C4

Fixed portfolio only

Pillar 2: Event-driven work C1, C2, C3, C4

Fixed and flexible

Pillar 3: Issues and products (thematic)

C1, C2, C3, C4

Fixed and flexible

4. Handling of PPI complaints

In November 2014, in the case of Plevin v Paragon Personal Finance Ltd, the Supreme Court decided that the non-disclosure of a substantial commission on a single premium PPI policy led to the relationship between the

borrower and lender being unfair pursuant to section 140A of the Consumer Credit Act 1974. Following this decision the FCA released a Statement in May 2015, within which the FCA stated that they would be “considering whether additional rules and/or guidance are required to deal with the impact of the Plevin decision on complaints about PPI”.

In October 2015 the FCA issued a further statement announcing that it had decided to consult before the end of 2015. The consultation paper was then published on 26 November 2015. The consultation paper sets out, and asks for views on, its proposals for:

– A new rule that would set a deadline by which customers would need to make their PPI complaints or else lose their right to have them assessed by firms or by the Financial Ombudsman Service. The proposed deadline is two years and is likely to start running sometime in 2016 after the FCA sets out its final rules.

– An FCA-led communications campaign designed to inform consumers of the deadline.

– New fee rules on funding the customer communications campaign (to be funded by the 18 firms with the most PPI complaints between them).

– New rules and guidance on the handling of PPI complaints in light of the Supreme Court’s decision in Plevin v Paragon Personal Finance Ltd.

– The proposed deadline also to apply for PPI complaints falling within the scope of the proposed rules and guidance on Plevin.

The consultation is open until 26 February 2016. The new rules and guidance and the time bar are expected to be in place by April 2016 at the earliest.

5. Complaint handling

Complaint handling looks set to be a major theme for 2016. It is seen as a key barometer of improvement in firms. The Policy Statement published in July 2015 found that the position had improved but that barriers still exist. The FCA

“The combination of the anticipated PPI time bar and communications campaign together with the changes to the DISP rules are likely to have a significant impact on complaint handling teams this year and materially change the complaint handling landscape”

Chris Busby, Partner, Eversheds

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

5

found that customers were not at the ‘heart’ of complaints and that technology could be a barrier. There were also issues with the quality of management information and the quality and breadth of root cause analysis.

There have already been a number of rule changes this year to implement the Alternative Dispute Resolution Directive (9 July 2015) and on call charges (26 October 2015). Further changes will take effect on 30 June 2016:

– To extend the ‘next business day rule’ where firms are permitted to handle complaints less formally and without sending a final response letter, to the close of three business days after the date of receipt;

– Firms must report all complaints, including those handled by the close of three business days after the firm receives them;

– Raising consumer awareness of the Financial Ombudsman Service by firms sending a ‘summary resolution communication’ following the resolution of complaints handled by the close of the third business day after receipt.

For a summary of the key issues arising from these changes, see the dedicated pages on our website from our complaint handling event in November 2015.

6. Credit card market study

On 3 November 2015, the FCA published its interim findings in respect of the credit card market study. This is a major study of one of the largest areas of unsecured

lending which the FCA regulates. There are around 30 million credit card holders in the UK. For further information on the FCA’s research, see the infographic produced by the FCA.

The FCA found that competition is working well for many consumers. Consumers valued the flexibility that credit cards provided and there was clear evidence of consumer switching between credit cards and using their credit cards for a range of purposes. However, the FCA is concerned about the scale of potentially problematic debt for consumers who are just above default levels and the incentives for firms to manage this. The FCA also want to see better information to assist those shopping around.

The next phase of the study is to discuss the interim findings and potential remedies with stakeholders, with the final report expected to be published in Spring 2016. Feedback on the initial findings was requested by 8 January 2016.

Businesses should consider the issues identified in relation to shopping around, switching, affordability and problem debt. If the FCA introduces potential remedies then compliance with the proposals will be required, therefore it may be helpful to identify, at this stage, any business processes or policies which may need to be amended to comply with the FCA proposals.

7. Payment Services Directive 2

PSD2 is part of a package of measures intended to modernise and improve the European retail payments

6

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

regulatory framework. It is a response to new innovative payment services across all channels, including internet and mobile devices, which seeks to improve security and consumer protection and address various areas of legal uncertainty in the original Payment Services Directive.

The text of the Payment Services Directive 2 has now been published in the Official Journal. It was published on 23 December and will enter into force on 12 January 2016. The deadline for transposition into national law is 13 January 2018.

For more information on PSD2, visit our Payments briefings hub.

8. CMA retail banking market investigation

The Competition and Markets Authority (CMA) has published a provisional report detailing its findings in its market investigation into the supply of retail banking services to personal current account customers and to small and medium sized enterprises (SME).

The CMA has provisionally found that a combination of low customer engagement, barriers to searching and switching and incumbency advantages in the provision of personal current accounts in both Great Britain and Northern Ireland are having an adverse effect on competition.

The CMA has proposed a series of possible remedies for the industry to consider. These include requiring banks to prompt customers to review their bank accounts at certain trigger points, such as when the bank closes a branch. The proposals also include suggestions to provide customers with a way of comparing the service quality of their account providers and to remove obstacles for overdraft users when considering whether to switch accounts, actually switching accounts and during the switching process.

The CMA will now consult and hold detailed discussions with all interested parties on the findings and possible remedies and will publish its final report in May 2016.

9. Financial advice market review

On 3 August 2015, HM Treasury announced the launch of a review looking at how financial advice could work better for consumers. The review will consider the current regulatory and legal framework governing the provision of financial advice and guidance to consumers, and its effectiveness in ensuring that all consumers have access to the information, advice and guidance necessary to enable them to make effective decisions about their finances.

HM Treasury and the FCA launched the joint consultation in October exploring what can be done to improve customers’ access to financial advice. The consultation aims to consider some of the main issues which customers currently face such as the increasing complexity of financial products (and how they are described to the consumer) and the increasing number of products available on the market. The consultation acknowledges that individuals are facing increasingly complex choices and need the right help to make financial decisions. In this context, the consultation focuses on the following questions:

– What kind of financial advice do consumers want?

– Are there gaps between the financial advice that consumers want, and the financial advice that they can access and afford?

– How can these gaps be closed?

– What role could technology, such as “robo-advice”, play in improving access to financial advice?

The consultation closed on 22 December 2015 and a final report will be published ahead of the 2016 Budget.

This is another review which will consider how financial advice is provided to consumers, and what measures could be implemented to ensure that it works better in the future. The terms of reference for the review state that the review will consider the interplay between the regulatory framework for advice and the role of FOS in redress and time limits (including a potential 15 year bar). This will be of relevance to all lenders as statistics from FOS consistently show that awareness of FOS continues to improve amongst consumers and the number of complaints with which it deals continues to rise.

10. Claims management regulation

The Ministry of Justice published its 2014/15 Claims Management Regulation Annual Report in July 2015, covering the main developments, achievements and progress made in claims management regulation over the last 12 months and setting out priorities for the future. Work in 2015/16 will include nuisance calls, unsolicited marketing and unsubstantiated claims relating to financial products and services.

The Claims Management Regulator (CMR) has this year started to use its power to fine firms which infringe the CMR’s rules of conduct. The first fine was levied in August under new powers introduced in December 2014. Firms who break the CMR’s rules can now expect fines of up to

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

7

20% of their annual turnover, as well as having their trading licence suspended or removed.

HM Treasury has issued a review of claims management regulation to provide a more consistent outcome in the way that claims management companies (CMCs) conduct business. The review has been led by Carol Brady, a non-executive director of the Claims Management Regulation Board and Chair of the Trading Standards Institute. Some of the recommendations to be considered include: Further reform to existing regulation, with new resources and powers to the Claims Management Regulation Unit (CMRU), the regulatory body for CMCs; dual regulation between the CMRU and the FCA; creating a new independent regulator; and transferring responsibility for regulation of CMCs to the FCA. Final recommendations will be made in early 2016.

11. Mortgage Credit Directive

The Mortgage Credit Directive (MCD) is intended to foster a single market for mortgages and to protect consumers. It applies to secured credit (first and second charge loans) and home loans. The European Commission published the final MCD text in February 2014 and it must be implemented in the UK by 21 March 2016. The FCA has also amended the FCA Handbook to reflect the MCD changes. A copy of the final rules implementing the MCD was published in the FCA’s Policy Statement PS15-9 in March 2015.

The FCA has also published a webpage setting out answers to frequently asked questions in respect of the Mortgage Credit Directive. The FAQs cover topics including:

– The process for second charge mortgage brokers currently in their application period and who will require mortgage permissions under the MCD;

– How firms will complete the application process;

– The application process for second charge lenders with interim permission;

– The impact of the MCD on the approved persons requirements; and

– How regulatory fees are impacted by the applications process.

As the MCD applies equally to first and second charge mortgages, the government has decided that second charge mortgage regulation should move from the FCA’s consumer credit regime into the mortgage regime. This means that, to carry on second charge mortgage business after 21 March 2016, lenders, administrators and brokers have to be authorised and hold the correct mortgage permissions. The FCA has also been given powers to register and supervise firms carrying out Consumer Buy To Let (CBTL) activity.

The MCD will apply from 21 March 2016 and lenders will need to make substantial systems and process changes across a wide number of areas to comply with the MCD requirements. The sales process will change, along with the disclosure documents which lenders are obliged to give to consumers.

8

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

The main changes to mortgage lending resulting from the MCD are:

– Some buy-to-let mortgages (CBTL) will become regulated by the FCA.

– There will be a phased move to a Europe-wide standardised set of disclosure information to customers, via a European Standardised Information Sheet (ESIS).

– The requirements that relate to foreign currency loans will change.

– Lenders’ sales processes and documentation will need to be reviewed for compliance.

This is the latest in a series of regulatory changes for mortgage providers, following on from the FCA’s Mortgage Market Review rules, applicable from 26 April 2014, and the transfer of credit regulation from the Office for Fair Trading to the FCA on 1 April 2014.

12. Payday lending market investigation

The high-cost short-term lending market continued to attract attention from the regulators this year. In March 2015, the FCA published its final report on Arrears and Forbearance in High-Cost Short-term Credit. The FCA found unacceptable practices from many lenders, including failure to recognise customers in financial difficulty; failure to direct people to free debt advice; and firms offering inflexible repayment options. However the FCA recognised that firms were making changes to improve. It also warned firms that those wishing to continue conducting regulated consumer credit activity must ensure they comply.

On 13 August 2015, the CMA made the Payday Lending Market Investigation Order 2015, following its market investigation into the supply of payday lending in the UK.

The Order prohibits online payday lenders from supplying payday loans unless the lender has published information on a payday loan price comparison website authorised by the FCA. In addition, with effect from 13 August 2016, payday lenders will be prohibited from supplying payday loans unless customers are provided with a summary of the cost of borrowing. The Order is intended to increase price competition between payday lenders and help borrowers.

The FCA published a consultation paper in response to the CMA’s final report into payday lending in October 2015. The consultation paper contains proposals for additional standards for price comparison websites (PCWs) which compare high-cost short-term credit products and invites views on them. Specifically, PCWs should:

– Rank products in ascending order of price according to the total amount payable and not give products greater prominence as a result of commercial relationships.

– Ensure any additional advertising on PCWs for high-cost, short-term credit is outside the ranking tables and not interspersed with it.

– Enable consumers to search according to the amount and duration of the loan that they require.

– Disclose on their website the extent of their market coverage by listing the number and names of firms whose products they compare.

The consultation is open until 28 January 2016.

The interim findings of the FCA’s credit card market study, refer specifically to the consultation in respect of price comparison websites. Businesses should therefore review the content of the consultation paper and look out for the policy statement when published.

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

9

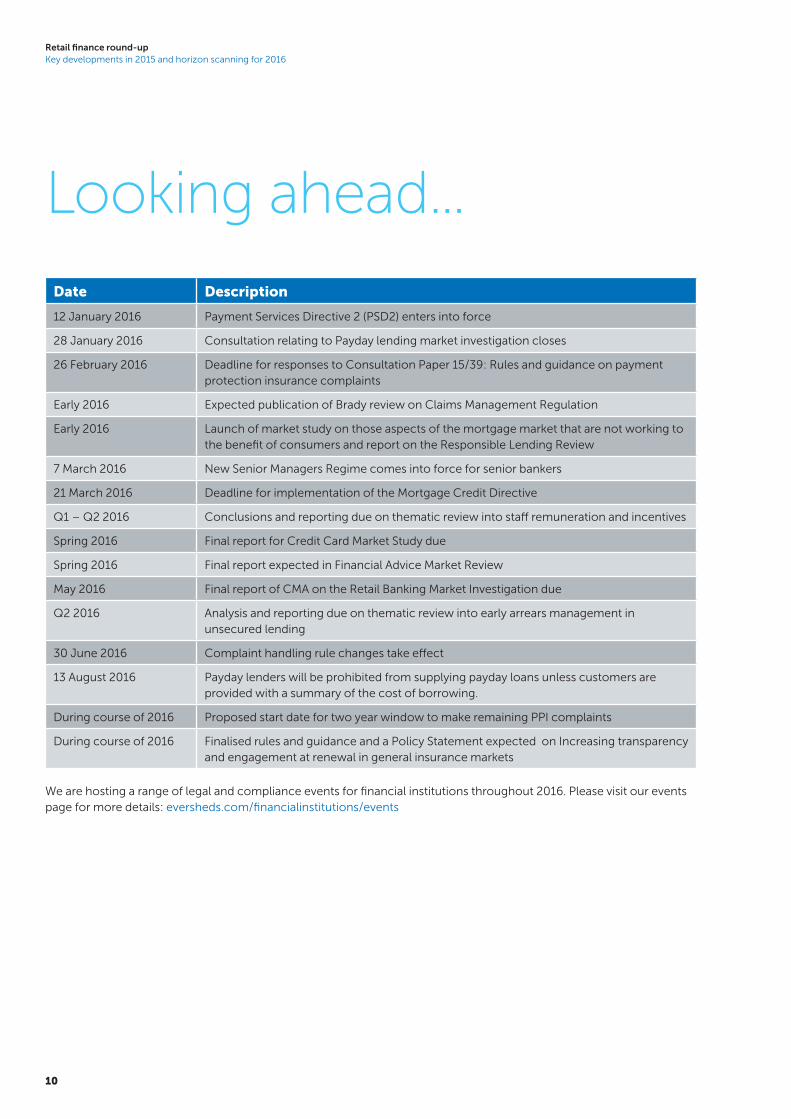

Looking ahead...

Date Description

12 January 2016 Payment Services Directive 2 (PSD2) enters into force

28 January 2016 Consultation relating to Payday lending market investigation closes

26 February 2016 Deadline for responses to Consultation Paper 15/39: Rules and guidance on payment protection insurance complaints

Early 2016 Expected publication of Brady review on Claims Management Regulation

Early 2016 Launch of market study on those aspects of the mortgage market that are not working to the benefit of consumers and report on the Responsible Lending Review

7 March 2016 New Senior Managers Regime comes into force for senior bankers

21 March 2016 Deadline for implementation of the Mortgage Credit Directive

Q1 – Q2 2016 Conclusions and reporting due on thematic review into staff remuneration and incentives

Spring 2016 Final report for Credit Card Market Study due

Spring 2016 Final report expected in Financial Advice Market Review

May 2016 Final report of CMA on the Retail Banking Market Investigation due

Q2 2016 Analysis and reporting due on thematic review into early arrears management in unsecured lending

30 June 2016 Complaint handling rule changes take effect

13 August 2016 Payday lenders will be prohibited from supplying payday loans unless customers are provided with a summary of the cost of borrowing.

During course of 2016 Proposed start date for two year window to make remaining PPI complaints

During course of 2016 Finalised rules and guidance and a Policy Statement expected on Increasing transparency and engagement at renewal in general insurance markets

We are hosting a range of legal and compliance events for financial institutions throughout 2016. Please visit our events page for more details: eversheds.com/financialinstitutions/events

10

Retail finance round-up Key developments in 2015 and horizon scanning for 2016

Contacts

Greg Brandman Partner

T: +44 20 7919 [email protected]

Simon Collins Managing Director

T: +44 20 7919 [email protected]

Senior managers regime

Jo Owens Principal Associate

T: +44 20 7919 [email protected]

Noreen Husain Regulatory Director

T: +44 20 7919 [email protected]

Consumer vulnerability

Chris Busby Partner

T: +44 121 232 [email protected]

Rebecca Copley Partner

T: +971 4 389 [email protected]

PPI, complaint handling and claims management regulation

Geraint Thomas Partner

T: +44 29 2047 [email protected]

Mortgage Credit Directive

Julia Woodward-Carlton Partner

T: +44 20 7919 [email protected]

CMA retail banking market investigation

Clare Hughes Partner

T: +44 20 7919 [email protected]

Jo Owens Principal Associate

T: +44 20 7919 [email protected]

Credit card market study/Payday lending market investigation

Richard Jones Partner

T: +44 161 831 [email protected]

Payment services/PSD2 David Saunders Partner

T: +44 20 7919 [email protected]

Supervisory model

Chris Busby Partner

T: +44 121 232 [email protected]

Financial advice market review

Geraint Thomas Partner

T: +44 29 2047 [email protected]

Andrew Henderson Partner

T: +44 20 7919 [email protected]

Julia Woodward-Carlton Partner

T: +44 20 7919 [email protected]

eversheds.com

©Eversheds LLP 2016 © Eversheds International 2016. All rights are reserved to their respective owners. Eversheds International is an international legal practice, the members of which are separate and distinct legal entities.DT05578_01/16