hospital consolidation and community benefit provision in

TRANSCRIPT

New Hampshire Center for Public Policy Studies

HospitalConsolidationandCommunityBenefit

Community Benefit and Market Changes in New Hampshire

July2017

2

Author

SteveNorton

ExecutiveDirector

AboutthispaperOneoftheCenter’sprojectsinrecentyearshasbeentoaddressissuesregardingchangesinthehealthcaresectorinNewHampshire.Thispaperisthelatestinourseriesofreportsonthattopic.ThisreportwasfundedinpartbytheStateofNewHampshireAttorneyGeneral’soffice,butthefindingsandrecommendationsarethoseoftheCenterandnotnecessarilythoseoftheStateofNewHampshireortheAttorneyGeneral’sOffice.

Thispaper,aswithalloftheCenter’spublishedwork,isinthepublicdomainandmaybereproducedwithoutpermission.Indeed,theCenterwelcomesindividuals’andgroups’effortstoexpandthepaper’scirculationandideas,withappropriateattribution.

Writeto:NHCPPS,OneEagleSquare,Suite510,Concord,NH03301

3

Executive Summary NewHampshirehospitalshavefinancialresponsibilityforalmost$5.7billionintotalassetsasof2014,themostrecentyearforwhichcompleteauditedfinancialdataisavailable.Ofthat$5.7billion,almost10%ofthoseassetshavebeenapartofhospitalmergeractivities(Memorial,UpperConnecticutValley,Weeks,Littleton,Androscoggin,AlicePeckDay,LakesRegionandFranklinhospitals).CatholicMedicalCenter,HugginsHospital,andMonadnockHospital(accountingforanother$500millionincommunityassets)andWentworthDouglassHospital($500million)recentlyhadmergerrequestsbeforetheAttorneyGeneral’soffice.[Otherconversations–principallyMaryHitchcockandElliotHospital–representmorethan$2billioninadditionalassetspotentiallyaffectedbymergeractivities.Together,theseaffiliationactivitiesaccountfor2/3rdsoftheassetsofNewHampshire’s24non-profithospitals.

TheCharitableTrustsUnitintheNewHampshireAttorneyGeneral’sofficehasresponsibilityformonitoringtheseaffiliationactivities,andisrequiredtoensurethat:

“Theassetsofthehealthcarecharitabletrustandanyproceedstobereceivedonaccountofthetransactionshallcontinuetobedevotedtocharitablepurposesconsistentwiththecharitableobjectsofthehealthcarecharitabletrustandtheneedsofthecommunitywhichitserves”-Section7:19-b

Tothatend,theAttorneyGeneral’sofficerequestedareviewofexistingdataandinformationonthetypesandlevelofcommunitybenefitcurrentlybeingprovidedinthestate,andbythe4hospitalscurrentlyengagedinmergerdiscussions–WentworthDouglass,CatholicMedicalCenter,MonadnockandHuggins.Inaddition,thisanalysisprovidesinformationonwhattheacademicliteraturesuggeststheimpactofhospitalconsolidationcouldbeoncommunitybenefit.

Major Findings TheNHDepartmentofJusticeandtheInternalRevenueServiceofferarich–ifrelativelyimprecise–bodyofdataoncommunitybenefitthatcouldbeusedtobothincreasethetransparencyofconversationsregardingcommunitybenefitandprovideameansforholdinghospitalsaccountableforboththelevelandtypeofcommunitybenefitprovided.However,hospitalsaregivenwidelatitudeinreportingcommunitybenefit,whichmakescomparisonacrosshospitalsandovertimedifficult.Providingclearerinstructionstohospitalsonreportingrequirementscouldresultindatawhichtheattorneygeneralcouldusetotrackcommunitybenefitacrossmerginghospitals.

Theliteratureregardinghospitalconsolidationsuggestspolicymakersshouldbecautiousaboutclaimsthatmergerswouldautomaticallyincreasevalueinthehealthcaresystem(eitherthroughimprovementsinprice,qualityorboth).Thereisarobust–albeitdated-literaturesuggestingthatreductionsincompetitionandhospitalconsolidationresultinincreasesinprice.

Morerecentresearch,however,suggeststhatnotallmergersarethesameandthatmorerecentmergersmaydifferinkeyrespectstothosethathavehistoricallybeenevaluated.Specifically,thenatureofthemarkets,clinicalservicechanges,andgeographymatterontheimpactonprice.Thisemergingliteraturesuggeststhatmergersinvolvinghospitalsindifferentmarketsandgeographicallyfarfromoneanotherhavenoimpactonprices.Theliteratureontheimpactofconsolidationonqualityandothercommunitybenefitprovisionislessrobust,generallysuggestingnorelationshipbetweenconsolidationandqualityorthelevelofoverallcommunitybenefitprovision.

4

Finally,specifictothemergerscurrentlybeforetheAttorneyGeneral’soffice,theCharitableTrustsUnitwillhaveadifficulttimeassessingtheimpactofmergerswithoutadditionalinformationnotcurrentlyprovided.Asmentioned,theliteratureregardinghospitalconsolidation–andassociatedchangesinmarketcompetition–suggeststhattheclaimsregardingsuchactivities–reductionsinpricesandincreasesinquality,forexample–aresensitivetodefinitionsofmarketsandservicesthatwouldbeaffected.ThesearenotcurrentlydefinedinthedocumentsprovidedtotheAttorneyGeneral’soffice.

Policymakersandboardsofdirectorswillhaveahardtimeunderstandingthepotentialimpactofamergerwithoutadditionalinformationontheactualplansforintegration,includingthedegreeofclinicalintegrationthatmightoccur.TheAttorneyGeneral’soffice,likewise,wouldfinditimpossibletojudge–asitisrequiredtodo–theimpactofmergerswithoutclearerinformationonhowthemergerwillactuallyimpactclinicalservices.

Recommendations Inwhatfollows,weprovideaseriesofrecommendationsfortheAttorneyGeneralandotherpolicymakersinterestedinunderstandingmoreclearlytheimpactofmergeractivityoncommunitybenefitprovisioninNewHampshire.

Community Benefit Provision BoththeNewHampshireAttorneyGeneral’sofficeandtheIRScollectdataontheprovisionofcommunitybenefitbyNewHampshire’shospitals.Littleanalysishasbeenconductedonthisdata,butitisausefulsourceofdatawithwhichtheAttorneyGeneral’sofficeandhospitalboardscouldmonitorchangesincommunitybenefitprovisionovertime.

InouranalysisofdatacollectedbytheAttorneyGeneral’soffice,wefoundsignificantvariationinthelevelofcommunitybenefitbyhospital,andsignificantchangeovertimeinthelevelofcommunitybenefitprovidedbyagivenhospital.Someofthisvariationisduetoinconsistenciesinthewayinwhichthedataisreported.TheseinconsistenciesstemfromthefactthatboththeNHAttorneyGeneral’sofficeandtheIRSgivehospitalsbroadlatitudeinreporting.Theliteratureonhospitalconsolidationandtheprovisionofcommunitybenefitsuggeststhathospitalconsolidationcould,insomeinstances,resultinincreasesincommunitybenefits,andpotentiallyshifthowthosebenefitsareprovided.

Asaresultofthesefindings,werecommend:

• TheAttorneyGeneral’sofficeconveneaworkgrouptodiscussclarifyingthedefinitionofwhatshouldandshouldnotbeincludedasacommunitybenefit,basedonguidancefromtheCatholicHospitalAssociation,whichhasbeenaleaderinthedevelopmentofcommunitybenefitreportingpractices.ThisworkgroupshouldalsodiscusswhetherthestateshouldcontinuerequiringhospitalstoreportcommunitybenefitsbothtotheAttorneyGeneral’sofficeandtotheIRS.

• ThestateandhospitalsshouldIncreasethetransparencyofdataontheprovisionofcommunitybenefitandchangesovertime.Suchaneffortcouldtakemanydifferentforms.Hospitalscould,aspartoftheircommunitybenefitplanefforts,provideananalysisofchangesinthelevelandtypeofcommunitybenefitovertime.Similarly,thelegislaturecouldrequiretheAttorneyGeneral’sofficetoprepareanannualreportoncommunitybenefitprovision.

5

Changes in Prices and Quality Associated with Consolidation Thebodyofliteraturethathasemergedoverthelast20yearslargelysuggeststhathospitalconsolidationneitherlowerscostsnorconsistentlyimprovesthequalityofthecareprovided.However,thereareimportantqualificationstothesefindings.

Withrespecttoprices,itisonlyrecentlythattheliteraturehasbeguntoexplorethepossibilitythatthetypeofconsolidation–whetherthetwoorganizationsarecompetitorsforcertainservicescomparedtonon-competitors–andthelevelofadministrativeandthereforeclinicalintegration–materiallyimpactsthedegreetowhichconsolidationcouldimpactprices.Themostrecentanalysis(Dafny,2015)confirmedthatashospitalcompetitiondeclines,pricesrise.However,italsosuggestedthatthemergersofhospitalsthataremoredistant–andpotentiallynotcompetingforthesamepatientsorservices–hadlittleimpactonprices.

Withrespecttoqualityofcare,theliteratureisweakerstill.Nationalstudies–withthebestcontrolsandmostgeneralizableresults–havelookedataverynarrowsetofservices(principallyforacutemyocardialinfarction),andnonehavelookedatgeographyanddifferenttypesofservicecompetition(forexample,forprimary,tertiaryorquaternaryservices).

Beyondthesegeneralizations,however,theabilitytounderstandhowtheproposedaffiliationswouldimpactpriceandqualityisextremelylimitedasaresultofthefactthattheaffiliationdocumentsprovidedtotheAttorneyGeneral’sofficedescribegovernancechangesassociatedwiththemergers,butdonotprovideanydetailontheintegrationplanforservices.

Asaresultofthesefindings,werecommend:

• Hospitalboardsengagedinmergeractivitiescoulddevelopqualityandcostmonitoringplansthatlinkqualityandcostwithspecificclinicalservices,identifiedasimportantinthedevelopmentoftheirintegrationplans.Thesecouldalsobecomepartofthecommunitybenefitplancommunicationeffortswiththelocalcommunity.

TheNHAttorneyGeneral’sofficecouldsimilarlymonitorchangesinpricesandquality,usingstandardnationalqualitymeasures,suchasreadmissionratesinthecaseofquality,andwithpricedatafromtheNewHampshireComprehensiveHealthInformationDatabase,whichhasbeenusedbytheNewHampshireDepartmentofInsurance.

6

Part 1 - Measuring Community Benefit

TheNewHampshireAttorneyGeneral’sofficehasledthenationindevelopingacommunitybenefitsreportingprocessthatrequireshealthcarecharitabletruststoassesstheircommunity’sneeds,andquantitativelydocumenthowthecharitabletrustisfocusingresourcesonthoseproblems.Eachyear,NewHampshire’shealthcarecharitabletrustsmustprovidetheAttorneyGeneralwithareportontheircommunitybenefitactivities.

WiththepassageoftheAffordableCareAct,thefederalgovernmentfollowedsuit.TheACAaddedSection501(r),whichrequirednon-profithospitalstomeetanewsetofobligationsregardingcommunitybenefitstoqualifyfortax-exemptstatusundersection501(c)(3).TheserequirementsweresimilartothosedevelopedbyNewHampshire.Non-profithospitalswererequiredto:

• Conductacommunityhealthneedsassessmentandprovideanimplementationplan• Documentwrittenfinancialassistancepolicyforfreecaretothemedicallyindigent• ReportontheresourcesdevotedtovariouscommunitybenefitactivitiesontheIRS990,

underscheduleH

RelativetoNewHampshire’sreportingefforts,theACAwasnarrowerinthesensethattheactrelatedsolelytonon-profithospitals,whereasNewHampshire’slawrelatestoallhealthcarecharitabletrusts.Inaddition,thedatacollectedundertheIRSForm990ScheduleHformislessdetailedthanNewHampshire’scollectioneffort.Forthepurposeofthisanalysis,wehavefocusedouranalysisonthedatacollectedbytheNewHampshireAttorneyGeneral’soffice.1

NH’sCommunityBenefitReportingandDataAsaresultofincreasingscrutinyregardingthecostsoftaxexemptionsforhealthcarecharitabletrustsandthepotentialbenefitstheyprovide,statesacrossthecountrybegandevelopinglegislationtotrackandassesscommunitybenefitsinthelate1990sandearly2000s.NewHampshireledthecountryindevelopinglawswhichrequiredhealthcarecharitabletrusts2inNewHampshiretoreportonthebenefitsprovidedtothecommunitytheyserve.

TheNewHampshireLegislaturepassedSB69-knownasNH’scommunitybenefitsstatute-in1999.EffectiveJanuary1,2000,thebillrequiredthatnon-profithospitalsinNewHampshiredevelopacommunitybenefitsplan,areportonthecommunitybenefitactivitiesundertakenbythehospital,andinformationdescribingtheresultsofthesecommunityinvestments.TheCharitableTrustsUnitissueditsfirstcommunitybenefitsreportingforminSeptemberof2001.

1We reviewed a sample of hospitals’ community benefit reporting in both the Schedule H from the IRS form 990 and the NH Attorney General’s community benefit forms. They were similar in most instances, with differences attributable to slight differences in the reporting requirements. We chose to use the NH DOJ data as it was more readily available for recent years. As we note, a more detailed analysis should be conducted to decide whether reporting of the state specific data is necessary, given the IRS 990 requirements. 2 "Health care charitable trust'' means a charitable trust organized to directly provide health care services, including, but not limited to, hospitals, nursing homes, community health services, and medical-surgical or other diagnostic or therapeutic facilities or services.

7

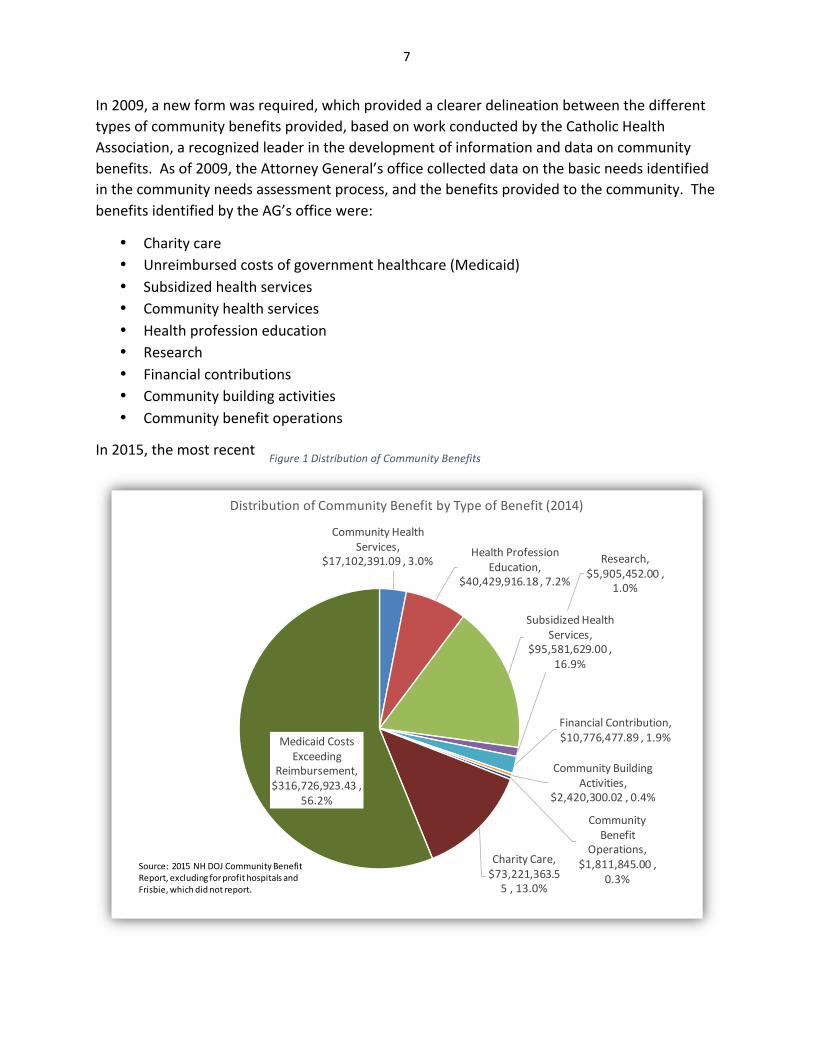

Figure1DistributionofCommunityBenefits

CommunityHealthServices,

$17,102,391.09,3.0%HealthProfession

Education,$40,429,916.18,7.2%

SubsidizedHealthServices,

$95,581,629.00,16.9%

Research,$5,905,452.00,

1.0%

FinancialContribution,$10,776,477.89,1.9%

CommunityBuildingActivities,

$2,420,300.02,0.4%

CommunityBenefit

Operations,$1,811,845.00,

0.3%

CharityCare,$73,221,363.55,13.0%

MedicaidCostsExceeding

Reimbursement,$316,726,923.43,

56.2%

DistributionofCommunityBenefitbyTypeofBenefit(2014)

Source:2015NH DOJCommunityBenefitReport,excludingforprofithospitalsandFrisbie,whichdidnotreport.

In2009,anewformwasrequired,whichprovidedaclearerdelineationbetweenthedifferenttypesofcommunitybenefitsprovided,basedonworkconductedbytheCatholicHealthAssociation,arecognizedleaderinthedevelopmentofinformationanddataoncommunitybenefits.Asof2009,theAttorneyGeneral’sofficecollecteddataonthebasicneedsidentifiedinthecommunityneedsassessmentprocess,andthebenefitsprovidedtothecommunity.ThebenefitsidentifiedbytheAG’sofficewere:

• Charitycare• Unreimbursedcostsofgovernmenthealthcare(Medicaid)• Subsidizedhealthservices• Communityhealthservices• Healthprofessioneducation• Research• Financialcontributions• Communitybuildingactivities• Communitybenefitoperations

In2015,themostrecent

8

yearforwhichcompletedataisavailable,NewHampshirecharitabletrustsprovidedalmost$564millionincommunitybenefit,accordingtoreportsfiledwiththeAttorneyGeneral’sCharitableTrustsUnit.Ofthattotalamount,56%resultedfromthefactthatMedicaidpayslessthantheexpensesassociatedwithprovidingservicestoMedicaidclients.Thesecondlargestshareresultedfromtheprovisionofsubsidizedhealthcareservices(17%).CharitableCare(at13%ofthetotal)cameinadistantthird.

Accordingtothesesamereports,theaveragehealthcarecharitabletrustprovidedalmost$22millionincommunitybenefit.MaryHitchcockprovidedover$180millionincommunitybenefit,withElliotandConcordhospitalprovidingmorethan$60million.Notsurprisingly,thelargerhospitalsaccountedforthelion’sshareofthecommunitybenefitprovided.

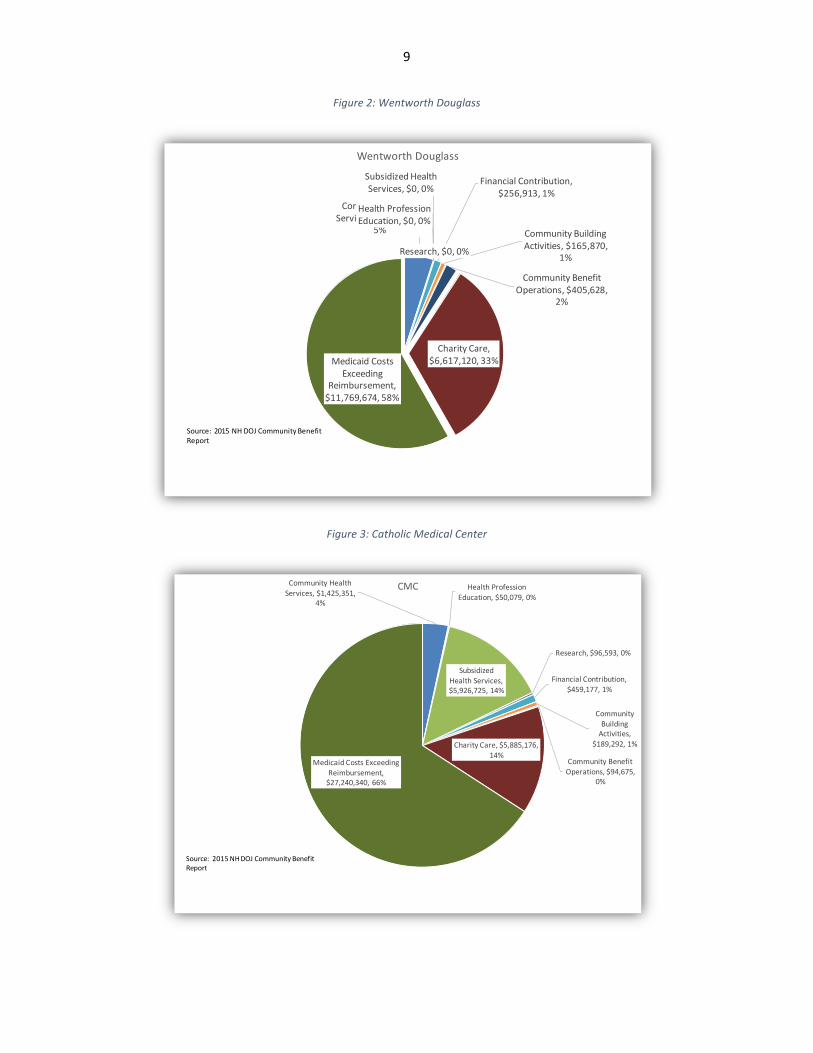

ThefiguresbelowincludedataforeachofthefourNHbasednon-profithospitalsthathavesoughtattorneygeneralapprovalformergeractivities.Whatisnotableaboutthisdataisthesignificantvariationinthedistributionofcommunitybenefitbytypebyhospital.Relativetotheotherhospitals,forexample,HugginsHospitalprovidedadisproportionateshareofitscommunitybenefitassubsidizedhealthservices.AreviewoftheunderlyingdatasuggeststhatHuggins3includedsubsidiesfortheirprimarycareservicesintheircommunitybenefitaccounting,somethingwhichonlyafewotherhospitalsdid,andwhichcouldarguablybeassumedtobeanormalcostofdoingbusiness.

3http://doj.nh.gov/charitable-trusts/community-benefits/documents/2015-huggins-hospital.pdf . This and all other data collected is available on the attorney general’s office website back to 2012.

9

Figure2:WentworthDouglass

Figure3:CatholicMedicalCenter

CommunityHealthServices,$1,005,764,

5%

HealthProfessionEducation,$0,0%

SubsidizedHealthServices,$0,0%

Research,$0,0%

FinancialContribution,$256,913,1%

CommunityBuildingActivities,$165,870,

1%

CommunityBenefitOperations,$405,628,

2%

CharityCare,$6,617,120,33%MedicaidCosts

ExceedingReimbursement,$11,769,674,58%

WentworthDouglass

Source:2015NH DOJCommunityBenefitReport

CommunityHealthServices,$1,425,351,

4%

HealthProfessionEducation,$50,079,0%

SubsidizedHealthServices,$5,926,725,14%

Research,$96,593,0%

FinancialContribution,$459,177,1%

CommunityBuildingActivities,

$189,292,1%

CommunityBenefitOperations,$94,675,

0%

CharityCare,$5,885,176,14%

MedicaidCostsExceedingReimbursement,$27,240,340,66%

CMC

Source:2015NHDOJCommunityBenefitReport

10

Figure4:Huggins

Figure5:Monadnock

CommunityHealthServices,$260,885,

4%HealthProfession

Education,$181,659,2%

SubsidizedHealthServices,$4,875,230,

66%

FinancialContribution,$50,716,1%

CommunityBuildingActivities,

$92,792,1%

CommunityBenefitOperations,$3,200,

0%CharityCare,

$1,057,000,14%

MedicaidCostsExceeding

Reimbursement,$876,644,12%

Huggins

CommunityHealthServices,$815,547,

18.05%Health

ProfessionEducation,

$5,821,0.13%

SubsidizedHealthServices,$533,208,

11.80%

FinancialContribution,$157,940,3.50%

CharityCare,$1,238,335,27.41%

MedicaidCostsExceeding

Reimbursement,$1,767,178,39.11%

Monadnock

11

Theoveralllevelofcommunitybenefiteffortvariedconsiderablyaswell,asshowninFigure6whichprovidesinformationshowingcommunitybenefitrelativetothesizeoftheorganization,asmeasuredbyoperatingexpenses.LakesRegionHospitalandUpperConnecticutValleyHospitalprovidedcommunitybenefitthatwasapproximately20%ofoperatingexpenses,comparedtoSpeareMemorial,St.JosephHospitalandMemorialHospital,eachofwhichprovidedcommunitybenefitsatmuchlowerlevels(lessthan5%).

Figure6:LevelofEffort:CommunityBenefitasashareofOperatingExpenses

Unreimbursed Medicaid Expenses

Asnoted,unreimbursedMedicaidexpensesaccountforthesinglelargestshareofcommunitybenefitactivities,rangingfrom.1%ofexpensesin2015toalmost10%,asshowninFigure 7.NewHampshirepaysforbasepaymentratesthroughmanagedcarearrangementsforservicesprovidedtoMedicaidbeneficiaries.Thesepaymentsaregenerallymuchlowerthantheexpensesassociatedwithprovidingthatcare.Inaddition,paymentpoliciesintheMedicaidprogramhavegenerallyrecognizedthedifficultfinancialpositionofmanyruralhospitals.

8.7%

13.9%

13.2%12.5%

16.6%

7.3%

15.7%

7.5%

13.9%

20.4%

6.2%

14.0%

3.1%

6.1%

15.3%

9.7%

4.7%3.8%

19.9%

11.6%11.4%

7.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

CommunityBenefit(IncludingMedicaidShortfall)asShareofOperatingExpensein2014

StateAverage=12.1%

12

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

UnreimbursedMedicaidExpenseas%ofOperatingExpense

Thosesmallruralhospitals–designatedcriticalaccesshospitals–incertaininstancesreceivedenhancedrates.4

Inaddition,NewHampshiremakessupplementalpaymentstohospitalstooffsetbothcharitycareandunreimbursedexpensesassociatedwithMedicaid.Nationally,allsupplementalMedicaidpaymentscombinedamountedto44percentofMedicaidfee-for-servicepaymentstohospitalsin2014.5ThesepaymentssignificantlyreducebothcharitycareandunreimbursedMedicaidexpenses.Similartothebasepayment,hospitalsreceivingcriticalaccessdesignationaretreateddifferently,withtheUncompensatedCareandMedicaidFundoffsettingupto75%ofthehospital’scharitycareandunreimbursedMedicaidexpenses,comparedto50%forallotherhospitals,aresultoflegislationpassedin2014.

4This includes Alice Peck Day, Androscoggin, Cottage, Franklin Regional, Huggins, Littleton, Memorial, Monadnock, New London, Speare, Upper Connecticut Valley, Valley Regional, and Weeks.] 5 https://www.macpac.gov/wp-content/uploads/2015/11/EXHIBIT-23.-Medicaid-Supplemental-Payments-to-Hospital-Providers-by-State-FY-2014-millions.pdf

Figure7:CommunityBenefitandMedicaid

13

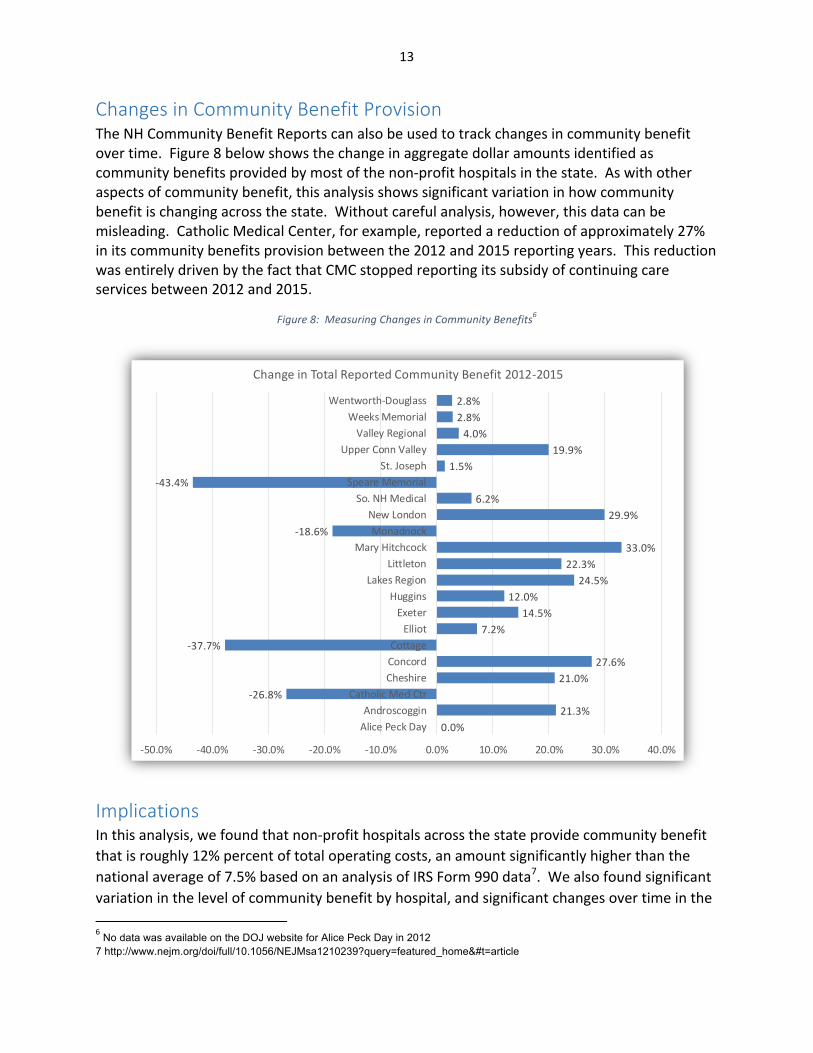

Changes in Community Benefit Provision TheNHCommunityBenefitReportscanalsobeusedtotrackchangesincommunitybenefitovertime.Figure8belowshowsthechangeinaggregatedollaramountsidentifiedascommunitybenefitsprovidedbymostofthenon-profithospitalsinthestate.Aswithotheraspectsofcommunitybenefit,thisanalysisshowssignificantvariationinhowcommunitybenefitischangingacrossthestate.Withoutcarefulanalysis,however,thisdatacanbemisleading.CatholicMedicalCenter,forexample,reportedareductionofapproximately27%initscommunitybenefitsprovisionbetweenthe2012and2015reportingyears.ThisreductionwasentirelydrivenbythefactthatCMCstoppedreportingitssubsidyofcontinuingcareservicesbetween2012and2015.

Figure8:MeasuringChangesinCommunityBenefits6

Implications Inthisanalysis,wefoundthatnon-profithospitalsacrossthestateprovidecommunitybenefitthatisroughly12%percentoftotaloperatingcosts,anamountsignificantlyhigherthanthenationalaverageof7.5%basedonananalysisofIRSForm990data7.Wealsofoundsignificantvariationinthelevelofcommunitybenefitbyhospital,andsignificantchangesovertimeinthe6No data was available on the DOJ website for Alice Peck Day in 2012 7 http://www.nejm.org/doi/full/10.1056/NEJMsa1210239?query=featured_home&#t=article

0.0%21.3%

-26.8%21.0%

27.6%-37.7%

7.2%14.5%

12.0%24.5%

22.3%33.0%

-18.6%29.9%

6.2%-43.4%

1.5%19.9%

4.0%2.8%2.8%

-50.0% -40.0% -30.0% -20.0% -10.0% 0.0% 10.0% 20.0% 30.0% 40.0%

AlicePeckDayAndroscoggin

CatholicMedCtrCheshireConcordCottage

ElliotExeter

HugginsLakesRegion

LittletonMaryHitchcock

MonadnockNewLondon

So.NHMedicalSpeareMemorial

St.JosephUpperConnValley

ValleyRegionalWeeksMemorial

Wentworth-Douglass

ChangeinTotalReportedCommunityBenefit2012-2015

14

levelofcommunitybenefitprovidedbyagivenhospital.Someofthisvariationislikelyduetoinconsistenciesinthewayinwhichthedataisreported.TheseinconsistenciesstemfromthefactthatboththeNHAttorneyGeneral’sofficeandtheIRSgivehospitalsbroadlatitudeinreporting.

Forpolicymakersinterestedinunderstandingthecommunitybenefitenvironment,thisdatawouldprovideagoodbenchmarkagainstwhichchangesgoingforwardcouldbeassessed.Thestateandhospitalboardscouldusethisdatatoincreasethetransparencyofconversationsaboutcommunitybenefitprovision,astheyhavedonewithconversationsabouthealthcarecosts.Thiscouldtakedifferentforms.Hospitalscould,aspartoftheirlocalcommunitybenefitplanefforts,provideananalysisofchangesinthelevelof,andtypeofcommunitybenefitovertime.Alternatively,thelegislaturecouldrequiretheAttorneyGeneral’sofficetoprepareanannualreportoncommunitybenefitprovision.

Tousethistooleffectively,however,wouldrequireadditionalstepstoensuretheaccuracyofthedata.First,amoreindepthanalysisoftheNewHampshireCommunityBenefitdatashouldbeconducted,whichincludesamoreindepthanalysisofthedataanddiscussionswithhospitalsregardingthedefinitionandcalculationofthequantitativemeasuresofcommunitybenefit.

Thevariationinwhatisincluded(ornot)ascommunitybenefitbyhospitalssuggeststhatmoreclarityislikelyneededindefiningwhatisandwhatisnotcommunitybenefit.TheCenterrequesteddatafromeachofthehospitalsrecentlyinvolvedinmergerdiscussionswiththeAttorneyGeneral’sofficeontwoareasthatsignificantlyimpacttheoverallestimatesoftheprovisionofcommunitybenefit.

First,weaskedhospitalswhethertheMedicaidlosswasnetofanyexpenses(associatedwiththeMedicaidEnhancementTax)andrevenues(intheformofpaymentsbythestateforahighshareofcostsassociatedwithMedicaidanduncompensatedcare)associatedwiththestate’sdisproportionateshareprogram.Thehospitalsvariedconsiderablyinhowtheyreportedthisinformationonthecommunitybenefitforms.

Second,werequesteddataonthedegreetowhichhospitalsincludedthesubsidizationofphysicianpractices.Arguably,ahospital’sdecisiontopurchaseaphysicianpracticeisabusinessdecisionandshouldthereforenotimmediatelybeconsideredacommunitybenefitunlessitisidentifiedspecificallyinthehospital’scommunitybenefitplanorlinkedwithsomespecialneedwithinthecommunity.Heretoo,therewassignificantvariationinwhatwasincluded,andtherationaleforitsinclusion.

AnydecisionabouthowtoproceedwiththisdatashouldalsoincludeafullcomparisonoftheresultsrelativetodatacollectedbytheIRS.Fromthisanalysis,hospitals,theAttorneyGeneral,andlegislatorscouldclarifyandtightenthedefinitionofwhatisincludedasacommunitybenefitornottoensurecomparabilityovertime(andalsoacrosshospitals),anddiscuss

15

whetherornotthestateshouldcontinuecollectingdatafromthecharitabletrustsinNewHampshire,ordefertothecollectionofdatafromtheIRS.

Part 2 - Hospital Consolidation’s Impact on Community Benefits IntheCenter’sreviewofaffiliationdocuments,it’sclearthatinadditionto‘communitybenefit’asdefinedbytheNHDepartmentofJusticeaswellastheIRSintheirinstructions,thehospitalsthemselvesidentifythetripleaimofloweringcosts,improvingpublichealthandimprovingquality.Thetheorybehindtheseclaimsisthatconsolidationwillhelpimprovecoordinationofcare(viascaleorbyallowingforinvestmentininformationtechnologysystemsandotherprocessimprovementefforts).Consolidationcouldalsoeliminateduplication.Finally,bothhospitalsthemselvesandtheAffordableCareActhavemadetheargumentthatsuchconsolidationwillhelpcreatescalesufficienttoimprovepublichealth.

Inwhatfollows,wereviewtheliteratureontheimplicationofhospitalmergersoncommunitybenefit,pricesandquality.Inthisanalysis,wereviewliteratureforthelast20years,whichlooksatthelargeincreaseinmergersandacquisitionsinthelate1990sandmorerecentlyinearlytothemid2010s.

Figure9:HospitalMergersandAcquisitions,1998-20148

8American Hospital Association, Trendwatch Chartbook 2015, Chart 2.9

16

Charity Care

Severalarticleswerepublishedregardingtherelationshipbetweentheprovisionofcharitycareandthelevelofcompetitioninthe1990sandearly2000s.TheseincludedFrankandSalkever(1991),Gruber(1994),Mannetal.(1995),Mannetal.(1997)andGarmin(2006).Thesestudiesinvariouswaysassessedthehypothesisthatincreasedcompetitionwouldinhibitaprovider’sabilitytooffercharitycare.Underthistheory,hospitalconsolidationcould,becauseoftheresultantreductionincompetition,resultinanincreaseinuncompensatedcareprovision.

Theresultsoftheliteraturearemixed,butgenerallysuggestthatreductionsincompetitioncouldleadtoincreasesincharitycareprovision,allotherfactorsbeingequal.Gruber(1994)andMannetal.(1995)foundthatwhenfacedwithsystem-widechangesinreimbursementsystems,hospitalsdecreasedtheircharitycarefasterinrelativelycompetitivemarketsthaninrelativelyuncompetitivemarkets.CuellarandGertler(2005)9andGarmin(2006)foundsimilarresults.However,noneofthesestudiesdirectlymeasuredtherelationshipbetweenhospitalconsolidationandcharitycareprovision.

Community Benefit Broadly Defined

Whilepolicymakersweregenerallyconcernedwiththeprovisionofcharitycare,overthecourseofthe2000s,states-andultimatelytheIRS-expandedthedefinitionofcommunitybenefittoincludeawholeseriesofcommunitybasedactivities,asdescribedelsewhere.This,alongwiththedataavailableasaresultoftheIRS’implementationofscheduleH,hasresultedinalimitednumberofstudiesassessingtheseothercommunitybenefitofferings.

Mostrecently,a2013articleintheNewEnglandJournalofMedicineusedscheduleHdatatodescribenon-profits’provisionofcharitablecare.Thatstudyfoundthathospitalsexpended7.5%oftheiroperatingexpensesforcommunitybenefitservices.Approximatelyhalfoftheseexpenditureswenttosubsidizingthecostofcareforpatientscoveredbymeans-testedprograms,primarilyMedicaid.10

Inadditiontodescribingthecharacteristicsoftheprovisionofcharitablecare,Younget.al.(2013)conductedregressionanalysestoassesstheimpactofvariousmarketcharacteristicsontheprovisionofcommunitybenefit.Forthisanalysis,theyanalyzeddirectpatientcareandcommunityservice.Theauthorsweretestingthehypothesisthatinstitutionalcharacteristics(solecommunityproviderstatus,amongothers)andmarketcharacteristics(includingmarketcompetition)wouldimpactthelevelsofcommunitybenefitprovision.

99How The Expansion Of Hospital Systems Has Affected Consumers Alison Evans Cuellar and Paul J. Gertler C 10 Gary J. Young, J.D., Ph.D., Chia-Hung Chou, Ph.D., Jeffrey Alexander, Ph.D., Shoou-Yih Daniel Lee, Ph.D., and Eli Raver N Engl J Med 2013; 368:1519-1527April 18, 2013

17

Forthemodelassessingdirectpatientcare,hospitalcommunitybenefitexpenditureswerepositivelyassociatedwithonlythestate-levelrequirementsforreportingcommunitybenefits.Thisresultsuggeststhatstateaccountabilitysystemsencouragetheprovisionofcommunitybenefits(andthatperhapsattorneysgeneralshouldincreasetheirreviewofthisimportanttrust).Forthemodelassessingcommunity-service,hospitalexpenditureswerepositivelyassociatedwithtwoinstitutional-levelcharacteristics—teachingstatusandsolecommunityproviderdesignation—andalsowithstate-levelreportingrequirementsforcommunitybenefits.Theresultsforteachingstatusarenotsurprisinggiventhefactthathealtheducationservicesareconsideredacommunitybenefit.Inbothmodels,theanalysisfoundnostatisticalrelationshipbetweenmarketcompetitionandthelevelofcommunitybenefit.

Public Health Improvement

Again,takingadvantageofdataavailablebecauseofstateandfederaleffortstomoreclearlydefinecommunitybenefits,avarietyofstudieshavesuggestedthatdeclinesincompetitioncouldlowertheprovisionofhealthimprovementactivitiesbecausehospitalsusetheseservicesasmarketingtools.C.Ginn,ShenandMoseley(2006),forexample,reviewedtheeffectofcommunitybenefitlaws,typeofownership,andcompetitiononhospital-basedhealthpromotionservices.Theyconcludedthatthehigherthelevelofcompetition–asmeasuredbytheHHI–themoresignificanttheprovisionofhospital-basedhealthpromotionservices,suggestingthathospitalsprovidetheseservicesatleastinpartforcompetitivereasons.D.GinnandMoseley(2009),andMoseley,Shen,andGinn(2010),E.Proenca,Rosko,andZinn(2000;2003)allsuggestthattheintensityofcompetitionissignificantlyandpositivelyassociatedwiththeprovisionofhospital-basedhealthpromotionservices.

Systems Vs. Mergers and Hospital Operating Expenses Intheory,hospitalmergerscanresultinefficienciesthroughtheeliminationofduplicativeactivities,includingtheintegrationofclinicalactivities.DranoveandLindrooth(2003)11attemptedtoassessthedegreeofintegrationthatoccursbydifferentiatingbetweensystemacquisitionsandmergers.Intheirdefinition,hospitalmergersinvolvethecombinationofseparatelicensesintoasinglefacilitylicense,withthehospitalsreportingasinglesetoffinancialandutilizationstatisticsandregulatedasasingleentity.Theoretically,theauthorsargue,amergerwouldallowformoreclinicalintegration,andtheauthorsconductapre-postanalysisofsystemconsolidationsandmergers,totestthehypothesisthatsuchintegrationlowersoperatingexpenses.

11Journal of Health Economics 22 (2003) 983–997

18

Theauthors’resultssuggestthatthegreatertheclinicalintegration,themorelikelyitisthattherewillbeoperatingexpensereductions.Theiranalysisofsystemconsolidations(comparingthosethatconsolidatedtothosethatdidn’t)showedaninsignificantimpactonoperatingexpenses.Theirre-analysisofsystemmergers,ontheotherhand,suggestedthatcontrollingforotherfactors,hospitalmergersresultedinareductionin14%ofoperatingexpensesandthatimpactremainedsignificantforfouryearspostthemerger.

PriceTheearlyliteratureonconsolidationthatoccurredinthe1990siswellsummarizedbyVogtandBrown(2006).Theyconductedameta-analysisofstudieslookingatvariousmethodsforunderstandingtheimpactofconsolidationonprices.Theresultsoftheirmeta-analysisledthemtotheconclusionthatthehospitalconsolidationinthe1990sraisedpricesbyatleastfivepercent,andlikelybysignificantlymore.

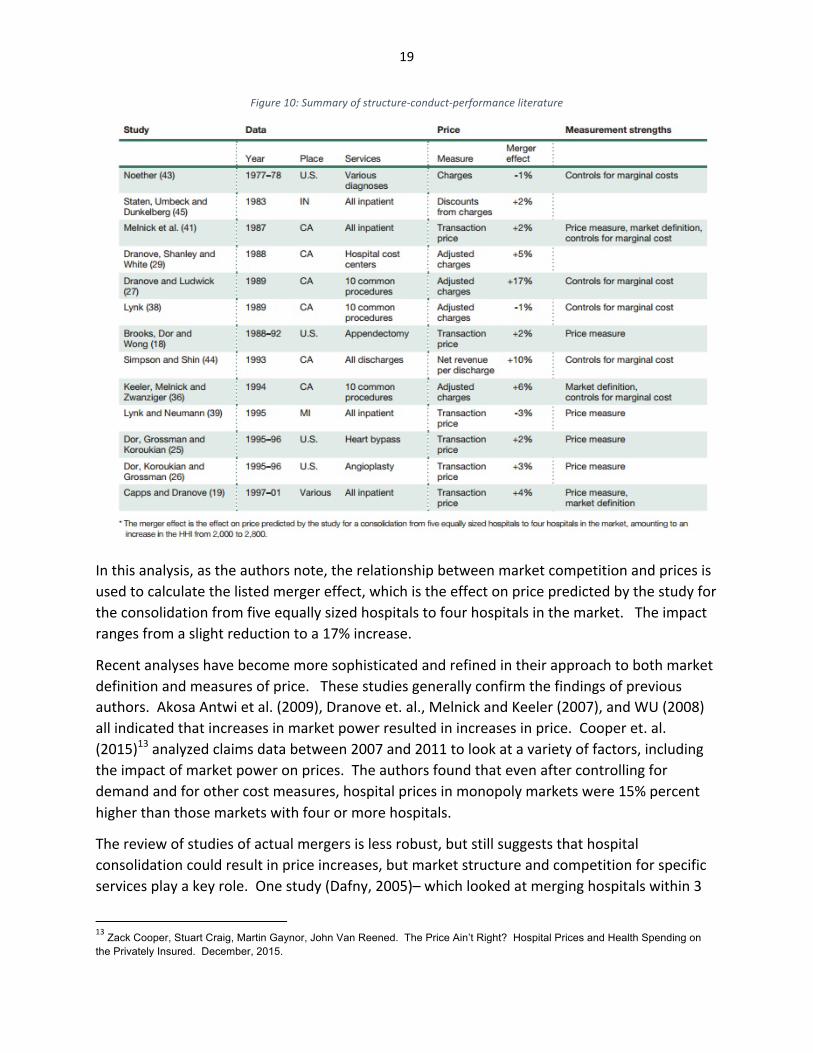

Thesinglelargestgroupofliteratureconductedwhattheauthorscallstructure-conduct-performanceanalysis,whichdonotanalyzeactualmergers,butlooksattheimpactofchangesinmarketstructure–usuallycompetitionasmeasuredbytheHerfindahlindex–anditsimpactonprices.Thefigurebelowshowstheauthors’selectionsofstudiesthatwerethemethodologicallymostsound12anddocumentsthevariationintheresults,allofwhichsuggestdeclinesinmarketcompetitionresultinincreasesinprices.

12Based on the definition of the market, controls for other factors which could impact prices, and the measure of price.

19

Figure10:Summaryofstructure-conduct-performanceliterature

Inthisanalysis,astheauthorsnote,therelationshipbetweenmarketcompetitionandpricesisusedtocalculatethelistedmergereffect,whichistheeffectonpricepredictedbythestudyfortheconsolidationfromfiveequallysizedhospitalstofourhospitalsinthemarket.Theimpactrangesfromaslightreductiontoa17%increase.

Recentanalyseshavebecomemoresophisticatedandrefinedintheirapproachtobothmarketdefinitionandmeasuresofprice.Thesestudiesgenerallyconfirmthefindingsofpreviousauthors.AkosaAntwietal.(2009),Dranoveet.al.,MelnickandKeeler(2007),andWU(2008)allindicatedthatincreasesinmarketpowerresultedinincreasesinprice.Cooperet.al.(2015)13analyzedclaimsdatabetween2007and2011tolookatavarietyoffactors,includingtheimpactofmarketpoweronprices.Theauthorsfoundthatevenaftercontrollingfordemandandforothercostmeasures,hospitalpricesinmonopolymarketswere15%percenthigherthanthosemarketswithfourormorehospitals.

Thereviewofstudiesofactualmergersislessrobust,butstillsuggeststhathospitalconsolidationcouldresultinpriceincreases,butmarketstructureandcompetitionforspecificservicesplayakeyrole.Onestudy(Dafny,2005)–whichlookedatmerginghospitalswithin3

13Zack Cooper, Stuart Craig, Martin Gaynor, John Van Reened. The Price Ain’t Right? Hospital Prices and Health Spending on the Privately Insured. December, 2015.

20

milesofeachother–showeda40percentincreaseinpricesoverthelongrun.14Ontheotherhand,Connor(1997),andConnorandFeldman(1998)foundthatpricesrosemoreslowlyinmergerthaninnon-mergermarkets,exceptinthoseareaswheremarketcompetitionwaslowalready.Theauthorsarguethattheirmarketdefinitionwasoverlybroad(amongotherconcerns)buthighlightthefactthatmarket(andpotentiallyproduct)definitionisveryimportanttounderstandingthepriceimpactsofhospitalconsolidation.

Whilemoststudieshavelookedathorizontalmergersinthesamegeographicarea,Dafnyet.al.(2016)15tooktheliteratureastepfurtherandlookedatboththosehospitalsthatmergedwithinthesamestate,andthosethatmergedacrossstatelines.Similartoworkpreviouslyconducted,Dafny(2005)foundthathospitalsgainingmemberswithinastatesawpriceincreasesof6-10percent,whilehospitalsgainingsystemmembersout-of-stateexhibitnostatisticallysignificantchangesinprice.

Quality of Care Thereislittleevidencetosuggestthatqualityimproveswithincreasinghospitalconcentration.KesslerandMcClellan(2000),Mukameletal.(2002),Shen(2003),andKesslerandGeppert(2005)allusedMedicaredatatoassessvariousmeasuresofmortality,principallywithafocusonacutemyocardialinfarction.Thesestudiesfoundthattherewaseithernoimpact,oraslightdecreaseinthequalityofcareasmeasuredbyAMImortalityassociatedwithincreasinghospitalconcentration.MorerecentstudiesoftheNationalHealthServiceshowsimilarresults(Cooperetal.2011,Gaynoretal,2010,Bloometal.2010).

StudiesonthefullpopulationoftheU.S.showsimilarresults(Mukameletal.2001;GowrisankaranandTown,2003;Volpetal.,2005).Cuellaretal.(2003)lookatmorebroadmeasuresofqualityofcare,includingratesofreadmission,adversepatientsafetyevents,andmortality,andfoundweakresults,withonlyonemeasure–ratesofoverusedprocedures–decliningassociatedwithincreasingmarketconcentration.

14Dafny L. Estimation and Identification of Merger Effects: an Application to Hospital Mergers. 2005, Mimeo, Northwestern University.15Leemore Dafny, Kate Ho, Robin Lee. The Price Effects of Cross-Market Hospital Mergers.” March, 2016.

21

Bibliography

HospitalConsolidationandHealthcareMarketsCuellar,AlisonEvansandPaulJ.Gertler.“TrendsInHospitalConsolidation:TheFormationOfLocalSystems.HealthAffairs22,no.6,2003Dafny,LeemoreS.2014.“HospitalIndustryConsolidation-StillMoretoCome?"NewEnglandJournalofMedicine,370,2014Ramirez,Edith.2014.“AntitrustEnforcementinHealthCare-ControllingCosts,ImprovingQuality."NewEnglandJournalofMedicine,(374)KilaruAS,WiebeDJ,KarpDN,LoveJ,KallanMJ,CarrBG.“Dohospitalserviceareasandhospitalreferralregionsdefinediscretehealthcarepopulations?”

MedicalCare,53(6),2015.

GeneralLiteratureonCommunityBenefitBarnett,K.,&Somerville,M.HospitalcommunitybenefitaftertheACA:ScheduleHandhospitalcommunitybenefit–Opportunitiesandchallengesforthestates(IssueBrief).Baltimore,MD:TheHilltopInstitute,UMBC,2012Bazzoli,GloriaJ.,JanP.Clement,andHui-MenHsieh,“CommunityBenefitActivitiesofPrivate,NonprofitHospitals,”JournalofHealth,Politics,andLaw,35(6),2010.

Corrigan,Janet,ElliottFisher,andScottHeiser,“HospitalCommunityBenefitPrograms:IncreasingBenefitstoCommunities,”JournaloftheAmericanMedicalAssociation313,no.12,2015

Ferdinand,AlvaO.,PatienJosueEpane,andNirMenachemi,"CommunityBenefitsProvidedbyReligious,OtherNonprofit,andFor-ProfitHospitals:ALongitudinalAnalysis,"HealthCareManagementReview;2013.GarmonChristopher.“HospitalCompetitionandCharityCare.”FTCBureauofEconomicsWorkingPaperNo.285,2006

Ginn,GregoryO.,JayJ.Shen,andCharlesB.Moseley,"TheImpactofStateCommunityBenefitLawsontheCommunityHealthOrientationandHealthPromotionServicesofHospitals,"JournalofHealthPolitics,PolicyandLaw,Volume31,Number2,2006

22

Ginn,GregoryO.andCharlesB.Moseley,"CommunityBenefitLaws,HospitalOwnership,CommunityOrientationActivities,andHealthPromotionServices,"HealthCareManagementReview,34(2),2009.Ginn,GregoryO.andCharlesB.Moseley,"CommunityHealthOrientation,Community-basedQualityImprovement,andHealthPromotionServicesinHospitals,"JournalofHealthcareManagement,49(5),2004.

Young,Gary,Chia-HungChou,JeffreyAlexander,Shoou-YihDanielLee,andEliRaver,“ProvisionofCommunityBenefitsbyTax-ExemptU.S.Hospitals,”NewEnglandJournalofMedicine368,no.16,2013.

InternalRevenueService,ReporttoCongressonPrivateTax-Exempt,Taxable,andGovernment-OwnedHospitals(Washington,DC:DepartmentoftheTreasury,2015.

Moseley,CharlesB.,Jay,J.Shen,andGregoryO.Ginn,“TheLong-termCoerciveEffectofStateCommunityBenefitLawsonHospitalCommunityHealthOrientation,”NevadaJournalofPublicHealth,7(1),2010.

Rubin,DanielB,SimoneSingh,andGaryYoung.“TaxExemptHospitalsandCommunitybenefit:NewDirectionsinPolicyandPractice.”Annu.Rev.PublicHealth,36,2015.

Somerville,MarthaH.,GayleD.Nelson,CarlH.Mueller,andCynthiaL.Boddie-Willis,“HospitalCommunityBenefitsaftertheACA:PresentPosture,FutureChallenges”,Baltimore,MD:HilltopInstitute,2013.

Somerville,MarthaH.,GayleD.Nelson,CarlH.Mueller.“HospitalCommunityBenefitsaftertheACA:TheStateLawLandscape”TheHilltopInstitute,IssueBrief.2013.Schlesinger,MarkandBradfordH.Gray.“HowNonprofitsMatterInAmericanMedicine,AndWhatToDoAboutIt”HealthAffairs25,no.4,2006

Young,Gary,Chia-HungChou,JeffreyAlexander,Shoou-YihDanielLee,andEliRaver,“ProvisionofCommunityBenefitsbyTax-ExemptU.S.Hospitals,”NewEnglandJournalofMedicine368,no.16,2013.

Price–CappsC,DranoveD.“HospitalConsolidationandNegotiatedPPOPrices.”HealthAffairs,vol.23,no.2,2004.

23

Cooper,Zack,StuartCraig,MartinGaynor,JohnVanReened.ThePriceAin’tRight?HospitalPricesandHealthSpendingonthePrivatelyInsured.NationalBureauofEconomicResearch,2015.Cuellar,AlisonEvansandPaulJ.Gertler“HowTheExpansionOfHospitalSystemsHasAffectedConsumers.”HealthAffairs24,no.1,2005.Cutler,DavidM.,andFionaScott-Morton.“Hospitals,MarketShareandConsolidation."JournalofAmericanMedicalAssociation,310(18),2013.Dafny,Leemore,KateHoandRobinLee.“ThePriceEffectsofCross-MarketHospitalMergers.”NationalBureauofEconomicsWorkingPaper,2016.DafnyLeemore.“EstimationandIdentificationofMergerEffects:AnApplicationtoHospitalMergers.”JournalofLawandEconomics,vol.52,no.3,2009.Dranove,David,RichardLindrooth.“HospitalConsolidationandcosts:anotherlookattheevidence.”JournalofHealthEconomics22,2003.Gaynor,Martin,andRobertTown.“TheImpactofHospitalConsolidation:Update."Princeton,NJ:RobertWoodJohnstonFoundation.2012.Haas-WilsonD.GarmonC.“HospitalMergersandCompetitiveEffects:TwoRetrospectiveAnalyses.”InternationalJournaloftheEconomicsofBusiness,vol.18,no.1,2011.MelnickG,KeelerE.“TheEffectsofMulti-HospitalSystemsonHospitalPrices.”JournalofHealthEconomics,vol.26,no.2,2007.MoriyaAS,VogtWB,GaynorM.“HospitalPricesandMarketStructureintheHospitalandInsuranceIndustries.”HealthEconomics,PolicyandLaw,vol.5,no.4,2010.PropperC,BurgessS,GreenK.“DoesCompetitionbetweenHospitalsImprovetheQualityofCare?HospitalDeathRatesandtheNHSInternalMarket.”JournalofPublicEconomics,vol.88,no.7–8,2004.ThompsonE.“TheEffectofHospitalMergersonInpatientPrices:ACaseStudyoftheNewHanover-CapeFearTransaction,”InternationalJournaloftheEconomicsofBusiness,vol.18,no.1,2011.VogtWB,TownRJ.HowHasHospitalConsolidationAffectedthePriceandQualityofHospitalCare?ResearchSynthesisReportNo.9.Princeton,NJ:RobertWoodJohnsonFoundation,2006..

24

QualityBloomN,PropperC,SeilerS,VanReenenJ.“TheImpactofCompetitiononManagementQuality:EvidencefromPublicHospitals.”WorkingPaperNo.16032.NationalBureauofEconomicResearch,2010.

CooperZ,GibbonsS,JonesS,McGuireA.“DoesHospitalCompetitionSaveLives?EvidencefromtheEnglishNHSPatientChoiceReforms.”TheEconomicJournal,vol.121,no.554,2011.

CutlerDM,HuckmanRS,KolstadJT.“InputConstraintsandtheEfficiencyofEntry:LessonsfromCardiacSurgery.”AmericanEconomicJournal:EconomicPolicy,vol.2,no.1,2010.

Gaynor,Martin,R.Moreno-Serra,andC.Propper,DeathbyMarketPower:Reform,CompetitionandPatientOutcomesintheNationalHealthService,WorkingPaperNo.16164,NationalBureauofEconomicResearch,2010.

GowrisankaranG,TownR.“Competition,PayersandHospitalQuality.”HealthServicesResearch,vol.38,no.6PartI,2003.

HoV,HamiltonB.“HospitalMergersandAcquisitions:DoesMarketConsolidationHarmPatients?”JournalofHealthEconomics,vol.19,no.5,2000.

KesslerD,McClellanM.“IsHospitalCompetitionSociallyWasteful?”QuarterlyJournalofEconomics,vol.115,no.2,2000.

KesslerD,GeppertJ.TheEffectsofCompetitiononVariationintheQualityandCostofMedicalCare.NationalBureauofEconomicResearch,NBERWorkingPaper#11226,2005.

MukamelD,ZwanzigerJ,TomaszewskiK,“HMOPenetration,Competition,andRisk-AdjustedHospitalMortality.”HealthServicesResearch,vol.36,no.6,2001.

MukamelD,ZwanzigerJ,BamezaiA.“HospitalCompetition,ResourceAllocationandQualityofCare.”BMCHealthServicesResearch,vol.2.no.10,2002.

MutterR,WongH.TheEffectsofHospitalCompetitiononInpatientQualityofCare.AgencyforHealthCareResearchandQuality,2004.

RogowskiJ,JainAK,EscarceJJ.“HospitalCompetition,ManagedCare,andMortalityafterHospitalizationforMedicalConditionsinCalifornia.”HealthServicesResearch,vol.42,no.2,2007.

SariN.“DoCompetitionandManagedCareImproveQuality?”HealthEconomics,vol.11,no.7,Oct2002.

25

ShortellS,HughesE.“TheEffectsofRegulation,Competition,andOwnershiponMortalityRatesAmongHospitalInpatients.”NewEnglandJournalofMedicine,vol.318,no.17,1988.

ShenYC.“TheEffectofFinancialPressureontheQualityofCareinHospitals.”JournalofHealthEconomics,vol.22,no.2,2003.

VolppK.KetchamJ,EpsteinA,WilliamsS.“TheEffectsofPriceCompetitionandReducedSubsidesforUncompensatedCareonHospitalMortality.”HealthServicesResearch,vol.40,no.4,2005.