hospitals' contribution to the high cost of u.s. health care

TRANSCRIPT

1

Nuoya Li Contributor: Jules Clark August 21, 2014

Hospitals Contribution to the High Cost of U.S. Health Care

Introduction

U.S health care costs have been burdening taxpayers and driving down the U.S. economy for

decades: they made up 17.2 percent of the Gross Domestic Product (GDP) in 2012 and are

projected to grow at an average rate of 5.8 percent from 2012-2022i, according to the Centers

for Medicare & Medicaid Services (CMS). The projected growth reflects coverage expansion and

Medicare payment adjustments implemented by the Affordable Care Act (ACA), as well as

general inflation in health care. In spite of its effort to improve access and quality of care, the

ACA or Obamacare, does not address the core problem of exceedingly high cost.

In the global context, the U.S. has taken a lead in total health cost since the middle 1990s.

Compared to other affluent countries, however, the U.S. fails to create a value-based system

with a positive return on its health care investment: in other words we spend more but do not

obtain better outcomes.

Comparing Health Care Metrics

Higher growth rates keep widening the gap between the U.S. and other developed countries,

most notably in terms of total and per capita health spending. Among the ten countries whose

GDP per capita are greater than the U.S., only Norway and Switzerland have higher health

expenditures per capita.

2

Table 1. A Lower Health “Return on Investment” in the U.S.

Source: World Bank Data, 2012

Table 1 compares the U.S. with both high income OECD and non-OECD countries by health

investment and selected outcomes in 2012. High income OECD countries outperform the U.S. in

life expectancy at birth and infant mortality rate. In sum, excessive spending on health care

puts a strain on the American consumer, without improving their personal health condition.

To understand this paradox, we examine where we are overspending and why the cost is not

enhancing value for patients.

Chart 1. Hospital care is the chief driver

Source: Haver, Centers for Medicare and Medicaid Services, 2013

Health expenditure per capita Health expenditure, total Mortality rate, infant Life expectancy at birth, total

(current US$) (% of GDP) (per 1,000 live births) (years)

U.S. 8895.115758 17.90905845 6 78.74146341

High income: OECD 5381.876661 12.9085045 4.437005221 80.68511915

High income: Non-OECD 967.2011977 4.891975581 8.87249661 73.44282465

Country

32%

21% 9% 2%

2% 2%

3%

4%

5%

3% 6%

1%

1%

6%

3%

U.S. Health care spending breakdown, 2013

Hospital CareExpenditures(Mil.$)

Physician And Clinical ServiceExpenditures(Mil.$)

Prescription DrugsExpenditures(Mil.$)

Research Expenditures(Mil.$)

3

Hospital care is the chief cost driver in the U.S. health care system. Other personal health care

expenditures like physician and clinical services, and prescription drugs also account for a big

portion of the total. Research on medical innovation to fight disease on the other hand is only a

small slice (2%) of the pie.

Chart 2. Hospital Care Weighs a Lot on Households

Source: 2014 Milliman Medical Index

The total annual cost of employer-sponsored health care for a typical family of four, measured

by the 2014 Milliman Medical Index (MMI) has more than doubled over the past 10 years. Its

growth rate is still well above that of the consumer price index (CPI). The MMI index takes

“utilization of care, the amount charged for each service, and the mix of services used” into

consideration while evaluating the cost under five separate categories: inpatient and outpatient

facility care, professional services, pharmacy and other services. These costs do not include

insurance premiums, but rather the medical expenses shared by employees and employers.

Since inpatient and outpatient care combined contribute to more than half of the MMI, hospital

Inpatient 31%

Outpatient 19%

Professional Services

31%

Pharmacy 15%

Other 4%

2014 MMI Components of Spending

4

cost plays a vital role in a family’s financial wellbeing. ii To help consumers resolve the puzzle, it

is time that we dive into the details of hospital cost, with a focus on utilization and pricing.

Overuse in Outpatient Care

Some argue that increased spending is caused by coverage expansion. It is indeed a positive

sign that the number of people covered by government or private insurance in the U.S. has

soared by 23.8 percent from 1987 to 2011. iii

In the meantime, hospitals are prompted to open new outpatient facilities for a growing

volume of visits. As a national trend, the number of outpatient visits rose more than 23 percent

from 2000 to 2009, whereas inpatient admission has flattened out in recent years. iv

Chart 3. Outpatient Spending Surpassing All Other Categories

Source: The 2012 Health Care Cost and Utilization Report

4.10% 4.00%

6.10%

3.80%

1.70%

4.00%

2.40%

6.50%

3.10% 3.80%

All categories Inpatient Outpatient Professional ProceduresPrescription Drugs

Annual Expenditure Per Capita by Catagories (2010-2012)

percent change 2010/2011 percent change 2011/2012

5

For individuals younger than 65 and covered by employer sponsored insurance (ESI), per capita

spending in outpatient care surged fastest from 2010 to 2012. The expansion in outpatient

visits to emergency rooms, outpatient surgery centers, and observation services was greatest

(7.2%). v

Table 2. Overuse in Outpatient Services

Source: 2012 OECD Health Data

OECD Health Data from 2012 reveals that the U.S. conducts way more Tonsillectomy (the

surgical removal of the tonsils), MRI (Magnetic resonance imaging) and CT exams than other

OECD countries. Notably, the U.S. ranked No.1 in knee replacements, and the total treatment

number in Medicare patients has increased by 162 percent in the past 20 years.vi As a

consequence, a debate about whether all tests are warranted has risen to the forefront. Karen

Sepucha, director of the Health Decision Sciences Center at Massachusetts General Hospital,

pointed out that the focuses of physicians and patients rarely overlap. She argues that effective

Items United States Rank compared with OECD countries OECD average

MRI units 31.6 2nd 12.5

per million population per million population

MRI exams 97.7 2nd 46.3

per 1 000 population per 1 000 population

CT scanners 40.7 3rd 22.6

per million population per million population

CT exams 265 3rd 123.8

per 1 000 population per 1 000 population

Tonsillectomy 254.4 1st 130.1

per 100 000 population per 100 000 population

Coronary bypass 79 3rd 47.3

per 100 000 population per 100 000 population

Knee replacements 226 1st 121.6

per 100 000 population per 100 000 population

Caesarean sections 32.9 6th 26.1

per 100 live births per 100 live births

6

communication with doctors as well as decision aids for different conditions will help patients

weigh the pros and cons of each treatment. vii

How we categorizer the use, and subsequent cost of each service is determined by whether a

person’s hospitals status is inpatient or outpatient. To be admitted as an inpatient patient, you

will need approvals from both your doctor and the hospital. Your hospital status in turn affects

how much you pay, including coinsurance, deductibles, and copayments, etc. viii

Therefore, to cope with the reimbursement shortfalls from Medicare and Medicaid inpatient

admissionsix , hospitals ease their financial pressures by enlarging the proportion of outpatient

services.

Physicians may exacerbate the condition by ordering as many tests as possible with less

emphasis on the patients’ individual needs. The perverse incentives stem from a system where

more and more types of services are covered, while prices are set by insurance companies, and

doctors are compensated for delivering each exam. This fee-for-service payment model is a far

cry from a fixed salary system, where doctor’s primary goal is to provide the patient with the

most effective and appropriate treatment.

Hospital Pricing Methodology

An overuse in outpatient services does not tell the whole story, however. Unit prices contribute

more to the waste of our health care expenditures than utilization does. According to an

analysis from the National Health Expenditure Accounts Team, 60 percent of the change in

personal health care spending from 2008 to 2009 can be attributed to general and medical

price inflation. As it relates to the price of hospital care, we propose that price discrimination

7

stems from hospital pricing methodologies for different payers —the government, private

insurers, and the uninsured.

Government

The U.S. government supports individuals’ health demand in several dimensions: Medicaid

provides health care for low-income and disabled people; The Children’s Health Insurance

Program (CHIP) covers low-income children; Medicare, which we will discuss in details below,

covers mostly those older than 65.x

The government has its own pricing formulas when it pays hospitals on behalf of individuals

insured by these federal programs. To calculate the exact amount of payment, Medicare adopts

the “case-based” payment system where all hospitals are reimbursed at fixed rates. Those rates

are pre-determined for each treated case in a given category, and are set for a group of

hospitals to reflect the average expected cost in an average-performing hospital, incentivizing

hospitals to reduce their operating cost.

To relate the type of treatment and patients to the costs incurred by hospitals, the government

provides unique classification schemes: Diagnosis-related groups (DRGs) for inpatient services

and Ambulatory Payment Classifications (APCs) for outpatient services. The monetary

conversion factors track changes in technology and market conditions.

To calculate the payment for an inpatient consumer, the base payment rate is first adjusted for

geographical factors that include a labor-related share, a wage index and a cost-of-living

adjustment (COLA). For example, places with higher cost of living will adopt a higher base rate.

Medicare then multiplies the adjusted base rate by the relative payment weights of DRGs and

APCs which capture the average cost of providing services per case. Exceptionally, hospitals are

8

given extra reimbursement under certain circumstances to cover indirect costs from medical

education, a higher portion of low-income patients, etc. xi

Unlike for private insurance, hospital’s pricing formulas adopted for government sponsored

insurance have recently become fairly transparent with the public release of DRGs and APCs

data from CMS. Hospitals do not wield any bargaining power because the rates are fixed ahead

of time.

Private insurers

Unlike the government, private insurers pay hospitals mainly on discounted charges, negotiated

per-diems, or diagnosis related groups (DRGs).

Payment negotiations happen annually based on the monetary conversion factors, DRG weights

and myriad of fees. xii Whatever the method, the negotiation process between each hospital

and insurer bears an impact on the discount off the chargemaster price across a range of

services and thus on how much consumers pay for their health plan premiums. On a case basis,

payments are also adjusted for case severity or for some standard procedures.

A natural byproduct of one-on-one negotiations between the insurer and the hospital is the

possibility for price discrimination. This means that charges for identical goods and services may

differ by hospital and insurer, and enormous price differentials are largely driven by the

negotiating leverages of hospitals and insurers.

While a provider’s leverage lies in the range of services it offers, a private insurer bargains

according to its market share, specifically its ability to send patients to providers. Hospitals are

in a stronger negotiating position than primary care providers and specialists due to an

9

irreplaceable combination of reputation, location, and services such as the emergency room.xiii

Despite tentative steps towards price transparency between insurers and hospitals, the

majority of actual payments remain undisclosed to the public.

Uninsured

The uninsured do not rely on any pricing methodology or structure when they are billed for

hospital services. In most cases, there is no legal or regulatory constraint imposed on hospitals

for charging lofty prices. This leaves the uninsured at the mercy of hospitals, with no bargaining

power for granted discounts off the chargemaster. Many hospitals don’t charge the uninsured

the full chargemaster price knowing that the patients cannot afford to pay.

As a result of extremely high variability in pricing and minimal cost transparency, the uninsured

are placed in a vulnerable position where they tend to face exceptionally higher costs for the

same service than insured patients. As a result, most uninsured have no choice but to

accumulate debt or compromise their credit ratings. xiv

Fluctuations in APCs and DRGs

One aspect of the highly variable hospital prices is the wide range in the cost weights of DRGs

and APCs, which intend to measure the resource requirement of certain services.

Since Medicare payments to hospitals vary enormously under a regulated pricing system, those

covered under private insurance are faced with greater uncertainty and an unintelligible pricing

negotiation process.

10

To list a few examples of price differences across hospitals within one state for the same

service, we analyze the “Provider Utilization & Payment Data” from CMS. xv

For hospitals in Texas in 2012, the APC “Magnetic Resonance Imaging and Magnetic Resonance

Angiography without Contrast (MRI)” has an average total payment of $332.16 and its range

($219.34) is 66 percent of the average and 75 percent of the lowest price ($293.27).

There appears to be a remarkable variation for some inpatient services. For hospitals in

California in 2102, “Major Joint Replacement or Reattachment Of Lower Extremity W MCC”, the

second most commonly used procedures in California, has an average total payment of

$17,422.28 and its range ($28,263.65) is 1.62 times the average and 1.86 times the lowest price

($15,193.82).

The DRG “Heart Failure & Shock W MCC”, the thirdly most commonly used procedures in

California, has an average total payment of $13,444.20 with a range ($23,555.75) 1.75 times

the average and 2.6 times the lowest price ($9,056.82).

Besides the DRGs and APCs weights, the costs of Tonsillectomy and knee replacements can be

complicated by age, overall health of the patient, the length of hospital stay, the type of

implant and the surgical approach, etc.xvi xvii In order to eliminate the tremendous price gap,

CalPERS introduced reference pricing for knee and hip replacement in 2011. xviii

Market Power: Insurance Companies vs. Hospitals

Dividing up hospital care by source of funds, we noticed that private insurance program

expenditures have been soaring faster than government sponsored ones. They have increased

by more than 20 percent in the past five years (2009-2013) and were highest in 2013. xix

11

Chart 4. Trends in Hospital Care by Source of Funds

Source: Haver, Centers for Medicaid and Medicare Services, 1965-2013

High and varying prices for privately insured patients underscore the relative bargaining power

of hospitals and insurance companies, in each instance.

Insurance companies include more hospitals for a broader provider networks so to fulfill the

demand from insurance plan purchasers. If insurance companies do not include must-have

providers in their plans, they may lose consumers to competitors. Larger insurance companies

are able to drive prices further down thanks to a comprehensive provider network. Industry

leaders like Cigna Corp. (CI) achieved a net profit margin of 6.3 percent in the second quarter of

2014xx, almost twice as much as the health insurance industry average (3.2%).xxi

It is an intuitive concept that fierce competition among health plans will drag revenues down

for insurance companies and force them to cut administrative and operating costs. Kate and

Robin found economically significant effects of health insurer competition on negotiated

hospital prices through their empirical investigation of the two largest commercial insurers in

0

50000

100000

150000

200000

250000

300000

350000

400000

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

Hospital Care Expenditures by Source of Funds

Private Health Insurance(Mil.$) Medicare(Mil.$) Medicaid(Mil.$)

12

California. The dataset contains insures’ transaction prices paid to hospitals along with their

provider networks.

Most hospitals will lower negotiated price if there is more competition between insurance

companies. For the most appealing hospitals, however, this does not hold true. They can take

advantage of increased competition by charging higher rates because consumers are disposed

to switch insurers when the most attractive hospital is dropped. This will allow hospitals to

bargain more aggressively and mitigate the original benefit of insurer competition. xxii

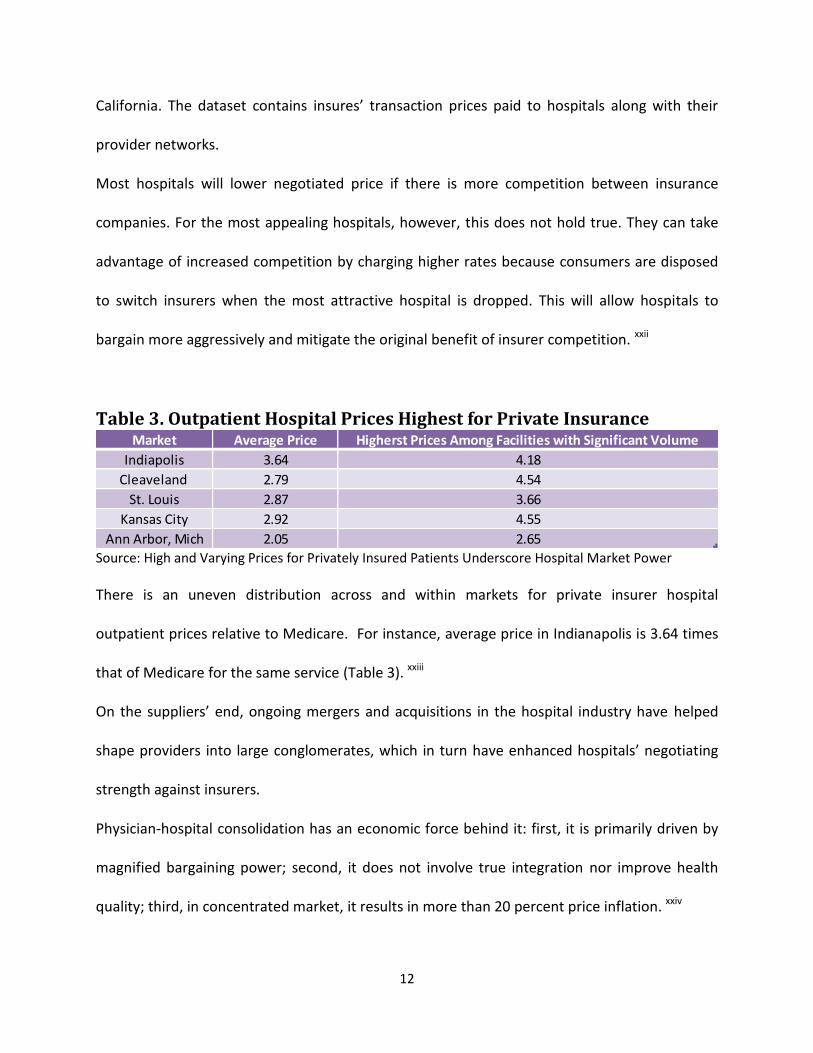

Table 3. Outpatient Hospital Prices Highest for Private Insurance

Source: High and Varying Prices for Privately Insured Patients Underscore Hospital Market Power

There is an uneven distribution across and within markets for private insurer hospital

outpatient prices relative to Medicare. For instance, average price in Indianapolis is 3.64 times

that of Medicare for the same service (Table 3). xxiii

On the suppliers’ end, ongoing mergers and acquisitions in the hospital industry have helped

shape providers into large conglomerates, which in turn have enhanced hospitals’ negotiating

strength against insurers.

Physician-hospital consolidation has an economic force behind it: first, it is primarily driven by

magnified bargaining power; second, it does not involve true integration nor improve health

quality; third, in concentrated market, it results in more than 20 percent price inflation. xxiv

Market Average Price Higherst Prices Among Facilities with Significant Volume

Indiapolis 3.64 4.18

Cleaveland 2.79 4.54

St. Louis 2.87 3.66

Kansas City 2.92 4.55

Ann Arbor, Mich 2.05 2.65

13

A Nevada patient’s original echocardiogram bill was $373 before the merger but jumped to

$1,605 after a hospital system purchased the physicians’ practice. xxv

Once a hospital gains a stronger market position, it is more likely to shift cost from public

payers to private insurers and the uninsured through price discrimination. In fact, while the

majority of doctors were self-employed a decade ago, a quarter of them have flocked to

hospitals and consolidated into practice groups. xxvi

Other Cost Drivers?

Medical Technology

Representing a sizable portion of health care in the U.S., hospitals serve as the crucial channel

through which technology pushes up total health spending. Mostly, cutting edge medical

technology leads to more expensive hospital treatment. Out of economic and legal incentives,

health care providers tend to form a strong cooperative relationship with equipment

manufacturers and drug producers. Consequently, hospitals conduct more tests, prescribe

more drugs and substitute low-cost services with high-cost options to generate significant

revenues.

An important subset of technological advancements in health care, are drugs in the

pharmaceutical industry. The price of prescription drugs in the U.S. is 50 percent higher than

that of comparable products in other developed countries.xxvii Both drug utilization and price

increased last year, with an overall drug trend reaching 3.8 percent per member, per month

compared to a moderate growth (0.8 percent) in traditional medications. xxviii

14

Chart 5. Average Profit Margin by Field

Source: Yahoo Finance; Aetna; American Hospital Association Resource Center Blog

Not surprisingly, major drug manufactures are the biggest winners, the single player with a

rising net profit margin from 2012 to 2014, as is exhibited by a simple comparison of industries.

xxix xxx xxxi

With more than 70 percent of Americans depending on at least one prescription drug, xxxii the

ACA does not tackle the problem of high drug costs but assists consumers by incorporating

prescription drug coverage as one of the 10 essential benefits in all individual and small group

health plans.

Administrative Cost

Insurance companies and hospitals can accrue high administrative costs and service fees, due to

the multitude of players in our health care system. Because hospitals and clinics lack a

standardized, transparent payment system, they incur substantial costs through interacting

with insurance providers, smaller associated facilities and other provider-owned subsidiaries.

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Health CarePlans

Hospitals MedicalAppliances &Equipment

Biotechnology Major DrugManufactures

2012

2014

15

They process insurance-related (BIR) activities billing for each test, visit and procedure,

regardless of whether their patients are covered by private or public insurance. Without superb

management, the time, effort and personnel involved create additional redundancy and

inefficiency for hospitals.

The Prospect of Hospital Regulation and Consumer Empowerment

As the chief driver of the exorbitant cost of U.S. health care, hospitals contribute to the status

quo with an overuse in outpatient care, an inconsistent pricing method for various payers, an

enhanced leveraging position, as well as groundbreaking medical technology and an onerous

administrative structure. There is a variety of policy implications that could help eradicate these

defects.

On the quantity side, to avoid an overuse of outpatient services, the government should

partially cut off the economic alignment between hospitals and equipment producers. With

regard to price discrimination, we need hospitals to better inform patients on price, specifically

those who are billed from the chargemaster. To further contain costs, we should put a cap on

hospitals’ outsized profits. Other financial and legal means that empower the physicians could

also curb hospitals’ consolidation and thus their bargaining power over prices. For instance,

safe-harbor defenses will protect doctors from being sued for medical liability and reduce the

likelihood of overprescribing.

Considering the interest clout’s relentless lobbying, hospital regulation has an unpromising

prospect for the moment, but feasible solutions do exist for consumers to save money.

16

Most urgently, they should be offered clear, reliable information about the prices, quantities

and quality of hospitals’ services to do a cost-benefit analysis on their own. Once one set of

weights for DRGs and APCs are established nationwide and once hospitals reveal a monetary

conversions factor to the public, patients would be able to compare prices in the same region

and pick up the price differences among providers. If and when accomplished, we may attain

“reference pricing” and an all-payer system without extra regulation.xxxiii Building an IT platform

paves the way for consumer-directed health care which could maximize value for patients. xxxiv

The platform will bolster an integrated, multidisciplinary care system with a complete set of

aggregated data, a uniform interpretation standard, and a medical record accessible to all

parties. It will also give providers the incentive to perform better care for a larger market share

with higher profits.

IT platform is no longer merely a vague concept. FAIR Health and Colorado Medical Price

Compare, among others run free websites to boost cost transparency. Capable of estimating

their medical/dental expenditures and comparing prices in different regions, consumers benefit

from developing financial literacy on health care.

In conclusion, our takeaway from this research is how we perceive the future of a value-based

and less costly health care system. A comparison with other wealthy nations unveils our

spending to be less efficient. In a deeply flawed system, we are held back by overprescribed

tests and a lopsided hospital pricing structure. By getting rid of price discrimination or

inconsistent charges for different payers, we could prevent hospitals from shifting cost to

17

privately insured and uninsured patients. This is only possible if all providers, insurers, and the

government are actively engaged in reducing cost and resolving potential conflicts of interest.

18

Bibliography

i The Centers for Medicare & Medicaid Services (CMS), National Health Expenditures Projections 2012-2022 ii 2014 Milliman Medical Index, Christopher S. Girod, Lorraine W. Mayne, Scott A. Weltz, Susan K. Hart iii Author’s calculation from “Income, Poverty and Health Insurance Coverage in the United States: 2011.”, Table C-1, Carmen DeNavas-Walt, Bernadette D. Proctor, Jessica C. Smith, 2012 iv Assessment of Cost Trends and Price Differences for U. S. Hospitals, Margaret E. Guerin-Calvert and Guillermo Israilevich, 2011 v The 2012 Health Care Cost and Utilization Re-port, Health Care Cost Institute Inc., 2013 vi The Journal of the American Medical Association vii Do you really need a knee replacement?, The Boston Globe, Courtney Humphries, 2012 viii Are You a Hospital Inpatient or Outpatient, Centers for Medicare & Medicaid Services ix Assessment of Cost Trends and Price Differences for U.S. Hospitals, Margaret E. Guerin-Calvert and Guillermo Israilevich, 2011 x USA.gov, Citizens, Health Insurance, Nutrition, and Food Safety Health Insurance xi Acute Care Hospital Inpatient Prospective Payment System, Department of Health and Human Services, Centers for Medicare & Medicaid Services xii The Pricing Of U.S. Hospital Services: Chaos Behind A Veil Of Secrecy, Health Affairs, Uwe E. Reinhardt, 2006 xiii High and Varying Prices for Privately Insured Patients Underscore Hospital Market Power, Health System Change Research Brief, Chapin White, Amelia M. Bond And James D. Reschovsky, 2013 xiv Key Facts about the Uninsured Population, the Kaiser Family Foundation, 2013 xv Provider Utilization & Payment Data, The Centers for Medicare & Medicaid Services xvi How Much Does A Tonsillectomy Cost?, COSTEVALUATION.COM xvii Understanding Knee Replacement Costs: What's On the Bill?, Healthline, Samuel Greengard, Medically Reviewed by George Krucik, MD, 2012 xviii The Potential of Reference Pricing to Generate Health Care Savings: Lessons from a California Pioneer, Health System Change Research Brief, manda E. Lechner, Rebecca Gourevitch, Paul B. Ginsburg, 2013 xix High and Varying Prices for Privately Insured Patients Underscore Hospital Market Power, Health System Change Research Brief, Chapin White, Amelia M. Bond And James D. Reschovsky, 2013 xx Second Quarter 2014 Earnings News Release, Cigna Quarterly Reports And Sec Filings xxi Yahoo Finance, Industry Browser - Healthcare - Health Care Plans - Company List xxii Insurer Competition and Negotiated Hospital Prices, Kate Ho and Robin S. Lee, 2013 xxiii High and Varying Prices for Privately Insured Patients Underscore Hospital Market Power, Health System Change Research Brief, Chapin White, Amelia M. Bond And James D. Reschovsky, 2013 xxiv Robert Wood Johnson Foundation, The Impact of Hospital Consolidation, Gaynor M, and Town R, 2012 xxv Same Doctor Visit, Double the Cost, Wall Street Journal, 2012 xxvi Bureau of Labor Statistics xxvii McKinsey & Company xxviii Prescription Drug Trend Increased in 2013, 2014 Insights report, CVS Caremark xxix Yahoo Finance, Industry Browser - Healthcare - Health Care Plans - Company List xxx The Facts About Rising Health Care Costs, Aetna, 2010 xxxi US hospitals total margin 5.53%: TRUVEN 2012 data, American Hospital Association Resource Center Blog, posted by kmgarber, 2013

19

xxxii Nearly 7 in 10 Americans Take Prescription Drugs, Mayo Clinic, Olmsted Medical Center, 2013 xxxiii The Pricing Of U.S. Hospital Services: Chaos Behind A Veil Of Secrecy, Health Affairs, Uwe E. Reinhardt, 2006 xxxiv The Strategy That Will Fix Health Care, Harvard Business Review, Michael E. Porter and Thomas H. Lee, 2013