intra-group services cost contribution arrangements · low value-adding intra-group services cost...

TRANSCRIPT

Intra-group Services

Cost Contribution

ArrangementsDr. Axel von Bredow, PSP

18 May 2017

Intra-group Services / Cost Contribution Arrangements 2

Agenda

BEPS – aligning transfer pricing outcomes

with value creation

Low value-adding intra-group services

Cost contribution arrangements

Intra-group Services / Cost Contribution Arrangements 3

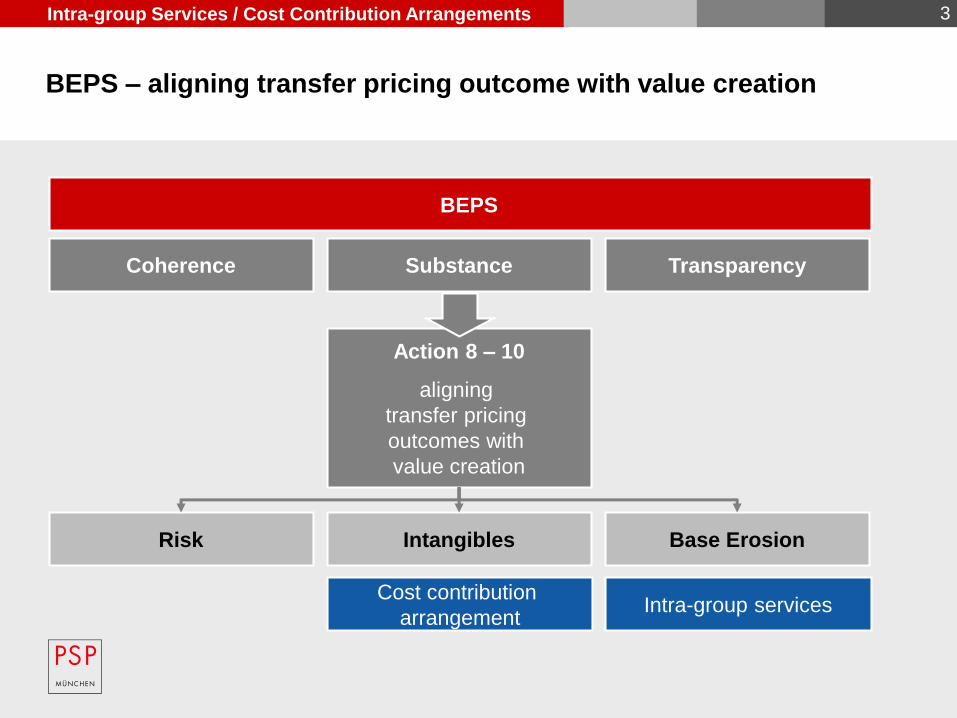

BEPS – aligning transfer pricing outcome with value creation

BEPS

Coherence Substance Transparency

Action 8 – 10

aligning

transfer pricing

outcomes with

value creation

Risk Intangibles Base Erosion

Intra-group servicesCost contribution

arrangement

Intra-group Services / Cost Contribution Arrangements 4

Agenda

BEPS – aligning transfer pricing outcomes with

value creation

Low value-adding intra-group services

Cost contribution arrangements

Intra-group Services / Cost Contribution Arrangements 5

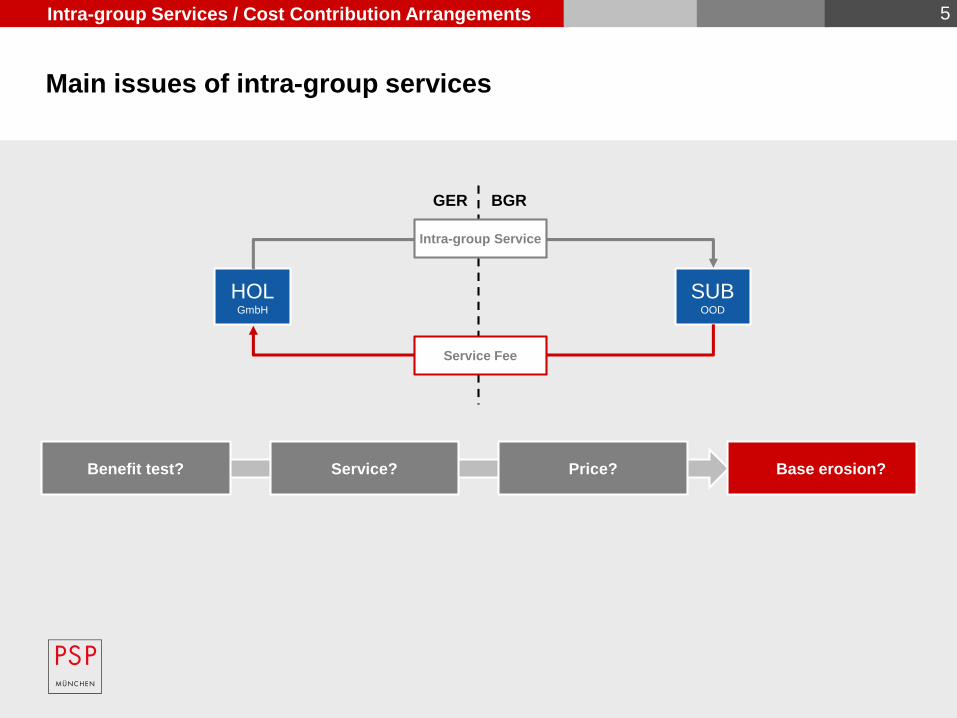

Main issues of intra-group services

HOLGmbH

SUBOOD

GER BGR

Intra-group Service

Service Fee

Price?Benefit test? Service? Base erosion?

Intra-group Services / Cost Contribution Arrangements 6

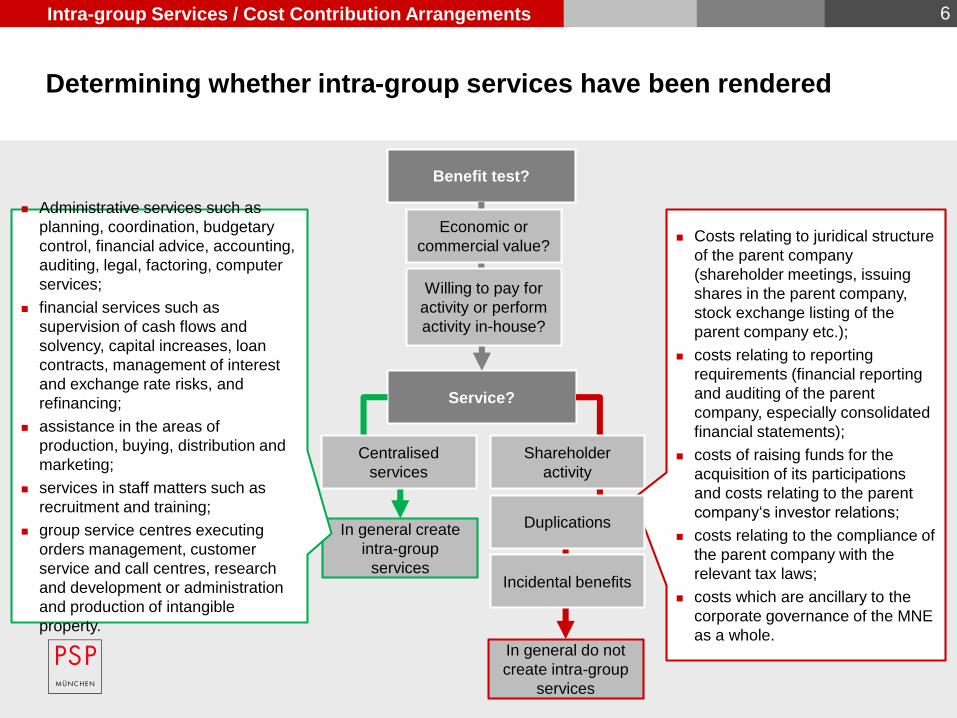

Determining whether intra-group services have been rendered

Benefit test?

Service?

In general do not

create intra-group

services

In general create

intra-group

services

Administrative services such as

planning, coordination, budgetary

control, financial advice, accounting,

auditing, legal, factoring, computer

services;

financial services such as

supervision of cash flows and

solvency, capital increases, loan

contracts, management of interest

and exchange rate risks, and

refinancing;

assistance in the areas of

production, buying, distribution and

marketing;

services in staff matters such as

recruitment and training;

group service centres executing

orders management, customer

service and call centres, research

and development or administration

and production of intangible

property.

Economic or

commercial value?

Willing to pay for

activity or perform

activity in-house?

Centralised

services

Shareholder

activity

Incidental benefits

Costs relating to juridical structure

of the parent company

(shareholder meetings, issuing

shares in the parent company,

stock exchange listing of the

parent company etc.);

costs relating to reporting

requirements (financial reporting

and auditing of the parent

company, especially consolidated

financial statements);

costs of raising funds for the

acquisition of its participations

and costs relating to the parent

company‘s investor relations;

costs relating to the compliance of

the parent company with the

relevant tax laws;

costs which are ancillary to the

corporate governance of the MNE

as a whole.

Duplications

Intra-group Services / Cost Contribution Arrangements 7

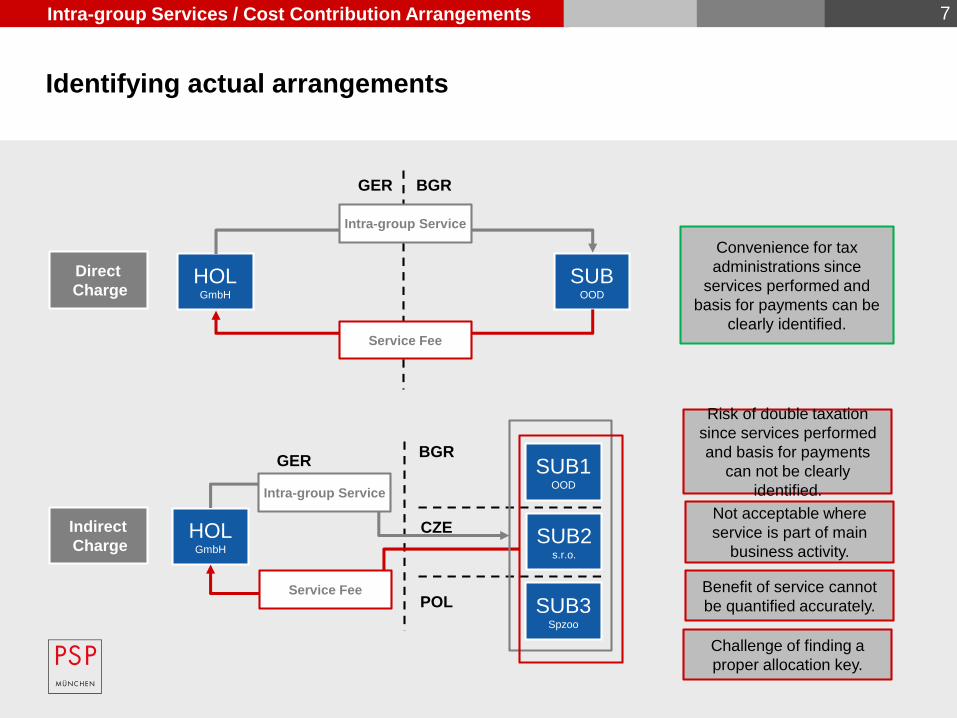

Identifying actual arrangements

Direct

Charge

Indirect

ChargeHOL

GmbH

SUB1OOD

GERBGR

SUB2s.r.o.

SUB3Spzoo

CZE

POL

Intra-group Service

Service Fee

Convenience for tax

administrations since

services performed and

basis for payments can be

clearly identified.

Risk of double taxation

since services performed

and basis for payments

can not be clearly

identified.

Not acceptable where

service is part of main

business activity.

Benefit of service cannot

be quantified accurately.

Challenge of finding a

proper allocation key.

HOLGmbH

SUBOOD

GER BGR

Intra-group Service

Service Fee

Intra-group Services / Cost Contribution Arrangements 8

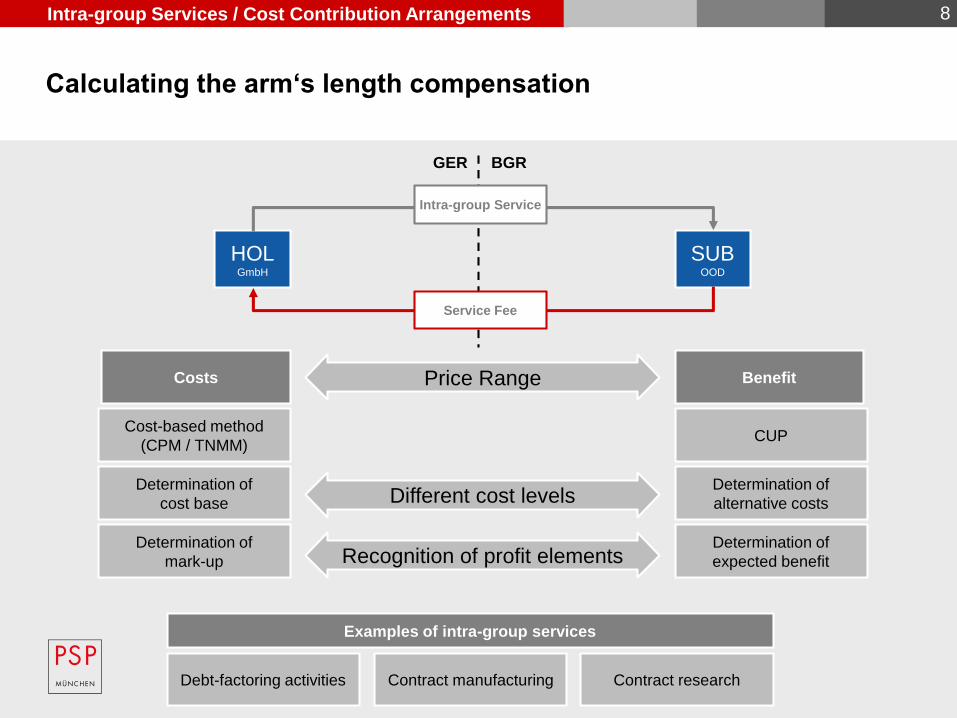

Calculating the arm‘s length compensation

Costs BenefitPrice Range

Cost-based method

(CPM / TNMM)CUP

Determination of

cost base

Determination of

mark-up

Different cost levels

Determination of

expected benefit

Determination of

alternative costs

Recognition of profit elements

Debt-factoring activities Contract manufacturing Contract research

HOLGmbH

SUBOOD

GER BGR

Intra-group Service

Service Fee

Examples of intra-group services

Intra-group Services / Cost Contribution Arrangements 9

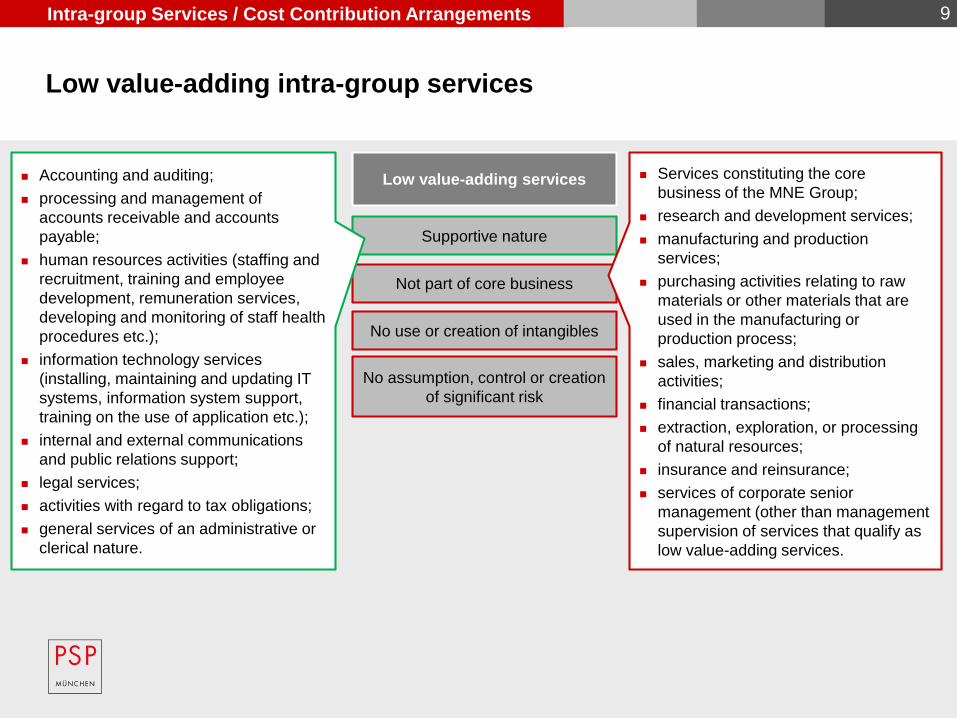

Low value-adding intra-group services

Low value-adding services

Not part of core business

Supportive nature

No use or creation of intangibles

No assumption, control or creation

of significant risk

Services constituting the core

business of the MNE Group;

research and development services;

manufacturing and production

services;

purchasing activities relating to raw

materials or other materials that are

used in the manufacturing or

production process;

sales, marketing and distribution

activities;

financial transactions;

extraction, exploration, or processing

of natural resources;

insurance and reinsurance;

services of corporate senior

management (other than management

supervision of services that qualify as

low value-adding services.

Accounting and auditing;

processing and management of

accounts receivable and accounts

payable;

human resources activities (staffing and

recruitment, training and employee

development, remuneration services,

developing and monitoring of staff health

procedures etc.);

information technology services

(installing, maintaining and updating IT

systems, information system support,

training on the use of application etc.);

internal and external communications

and public relations support;

legal services;

activities with regard to tax obligations;

general services of an administrative or

clerical nature.

Intra-group Services / Cost Contribution Arrangements 10

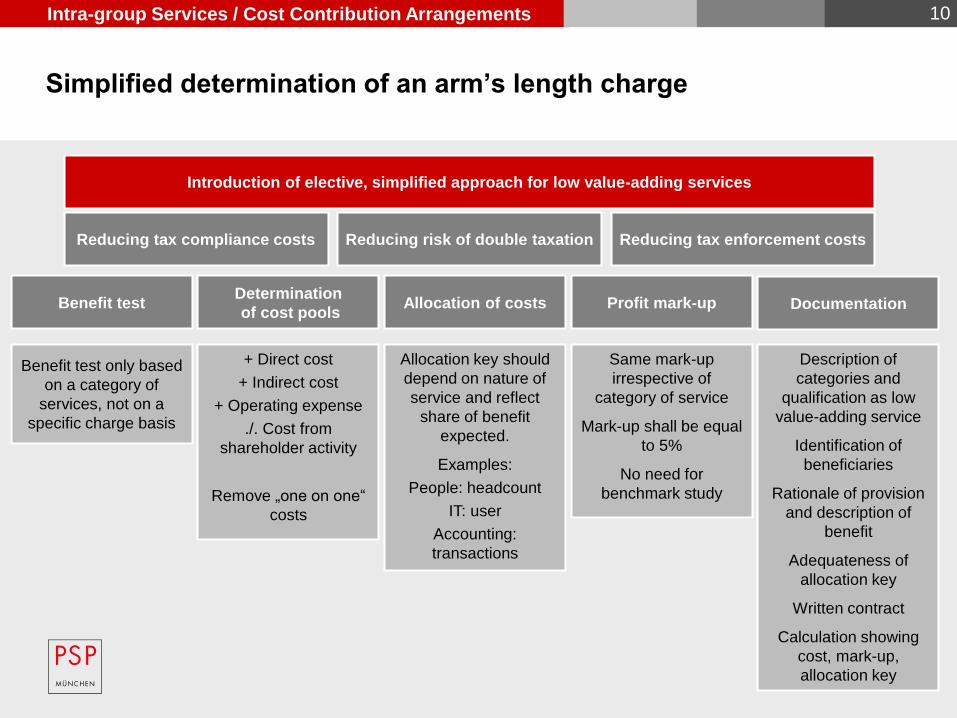

Simplified determination of an arm’s length charge

Introduction of elective, simplified approach for low value-adding services

Reducing tax compliance costs Reducing risk of double taxation Reducing tax enforcement costs

Benefit test

Benefit test only based

on a category of

services, not on a

specific charge basis

Determination

of cost pools

+ Direct cost

+ Indirect cost

+ Operating expense

./. Cost from

shareholder activity

Remove „one on one“

costs

Allocation of costs

Allocation key should

depend on nature of

service and reflect

share of benefit

expected.

Examples:

People: headcount

IT: user

Accounting:

transactions

Profit mark-up

Same mark-up

irrespective of

category of service

Mark-up shall be equal

to 5%

No need for

benchmark study

Documentation

Description of

categories and

qualification as low

value-adding service

Identification of

beneficiaries

Rationale of provision

and description of

benefit

Adequateness of

allocation key

Written contract

Calculation showing

cost, mark-up,

allocation key

Intra-group Services / Cost Contribution Arrangements 11

Practical challenges applying the simplified approach

Introduction of elective, simplified approach for low value-adding services

Reducing tax compliance costs Reducing risk of double taxation Reducing tax enforcement costs

Benefit testDetermination

of cost poolsAllocation of costs Profit mark-up Documentation

When should

operating expense be

included in the cost

basis?

How are different cost

levels taken into

account?

Is the profit mark-up

limited by the

expected benefit?

Reduction of tax

compliance costs if no

benchmark study is

needed.

Simplification vs.

arm’s length profit

allocation?

No documentation of

specific individual acts

undertaken necessary.

How detailed must the

description of the

benefit be?

How detailed must the

description of the

applicability of the

allocation key be?

How are “one to one”

costs determind?

Should location

specific cost

advantages be

reflected in mark-up?

Intra-group Services / Cost Contribution Arrangements 12

Overview simplified approach

Low value-adding

intra-group service?

(Simplified) Benefit

test satisfied?

Documentation

prepared?

Threshold exceeded?

Application of

simplified

approach

No application of

simplified approach

No

No

No

Yes

Yes

Yes

No

Simplified determination

of arm´s length charges:

Step 1: calculation of

all costs

Step 2: remove „one on

one“ costs

Step 3: allocation

Step 4: mark-up

Step 5: determination

of charge

As long as the rules

for documentation

and reporting are

satisfied, the benefit

test is deemed to be

satisfied in respect

of the simplified

approach.

Review of the

simplified

approach

Yes

Intra-group Services / Cost Contribution Arrangements 13

Agenda

BEPS – aligning transfer pricing outcomes with

value creation

Low value-adding intra-group services

Cost contribution arrangements

Intra-group Services / Cost Contribution Arrangements 14

Main issues of cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

Idea of a CCA

Profit shifting?

CCA

Participants

share contributions

and risks

to joint development,

production or

obtaining of

intangibles, tangible

assets or services

which create benefit

for the participants

Assumption of a CCA

Participant’s

proportionate share

of overall

contributions

must be consistent with

proportionate share

of overall benefit,

Transfer pricing

analysis is based on

actual transaction and if

no deviation on

contractual

arrangements.

150 250

200 200

PS PS

Profit shifting

PS

Proportionate

share

PS

200PS

200PS

Intra-group Services / Cost Contribution Arrangements 15

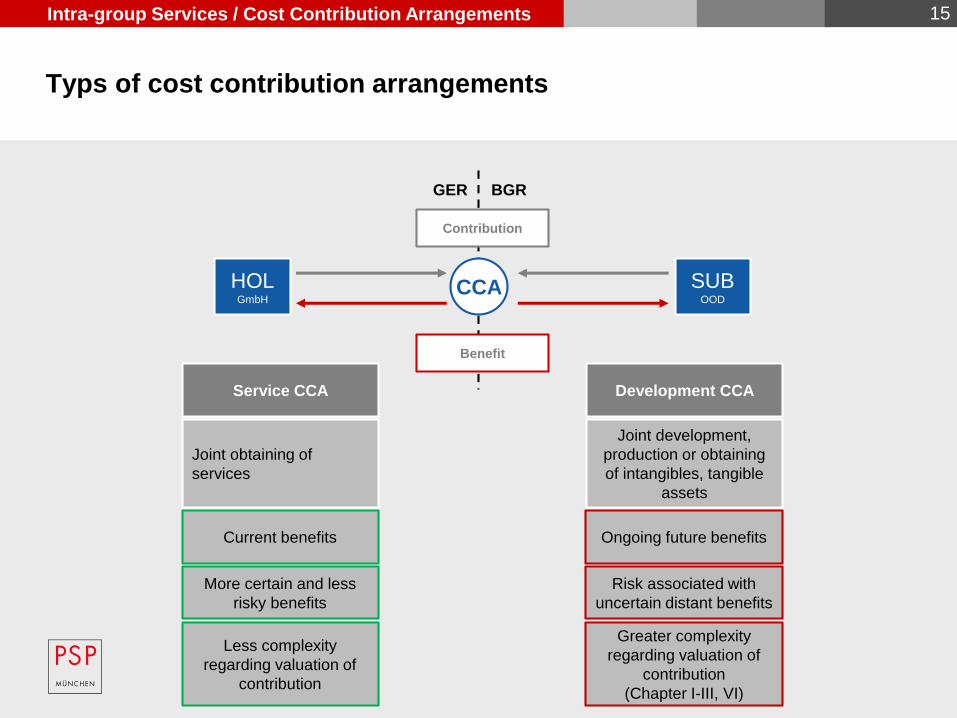

Typs of cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

Development CCA

CCA

Joint development,

production or obtaining

of intangibles, tangible

assets

Ongoing future benefits

Risk associated with

uncertain distant benefits

Greater complexity

regarding valuation of

contribution

(Chapter I-III, VI)

Service CCA

Joint obtaining of

services

Current benefits

More certain and less

risky benefits

Less complexity

regarding valuation of

contribution

Intra-group Services / Cost Contribution Arrangements 16

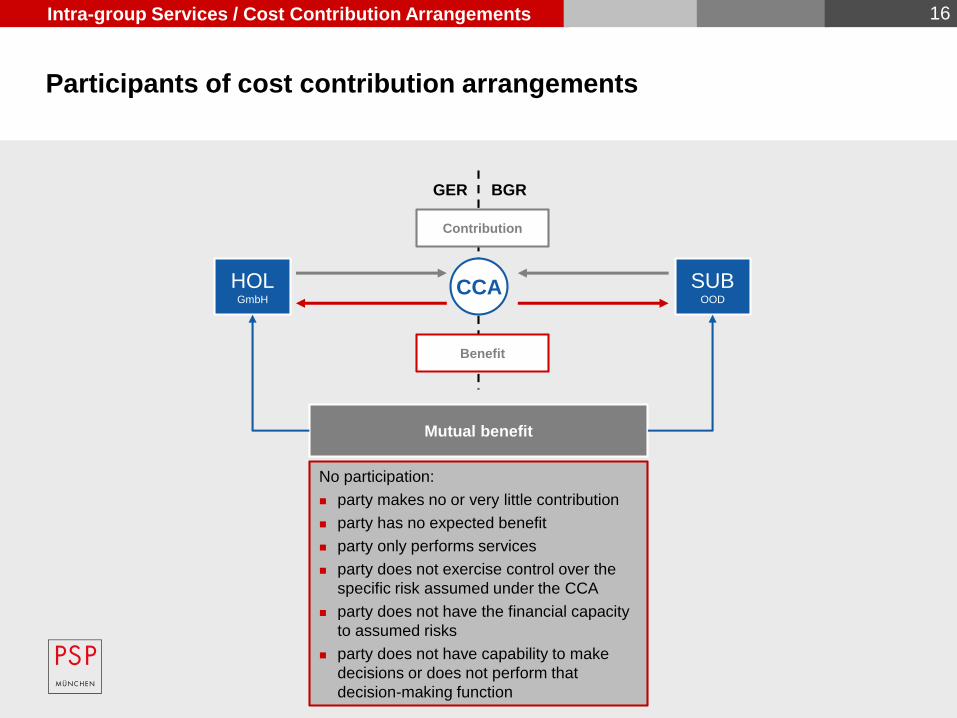

Participants of cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

Mutual benefit

CCA

No participation:

party makes no or very little contribution

party has no expected benefit

party only performs services

party does not exercise control over the

specific risk assumed under the CCA

party does not have the financial capacity

to assumed risks

party does not have capability to make

decisions or does not perform that

decision-making function

Intra-group Services / Cost Contribution Arrangements 17

Expected benefit from cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

CCA

Income generated or

costs saved

Projection of expected

benefit

Relevant allocation key

HOLGmbH

SUBOOD

CCA

200

200

Ben

efit: 4

00

Total benefit

Service CCA Development CCA

projected vs. actual

benefit

Multiple activity and

multiple allocation key

Intra-group Services / Cost Contribution Arrangements 18

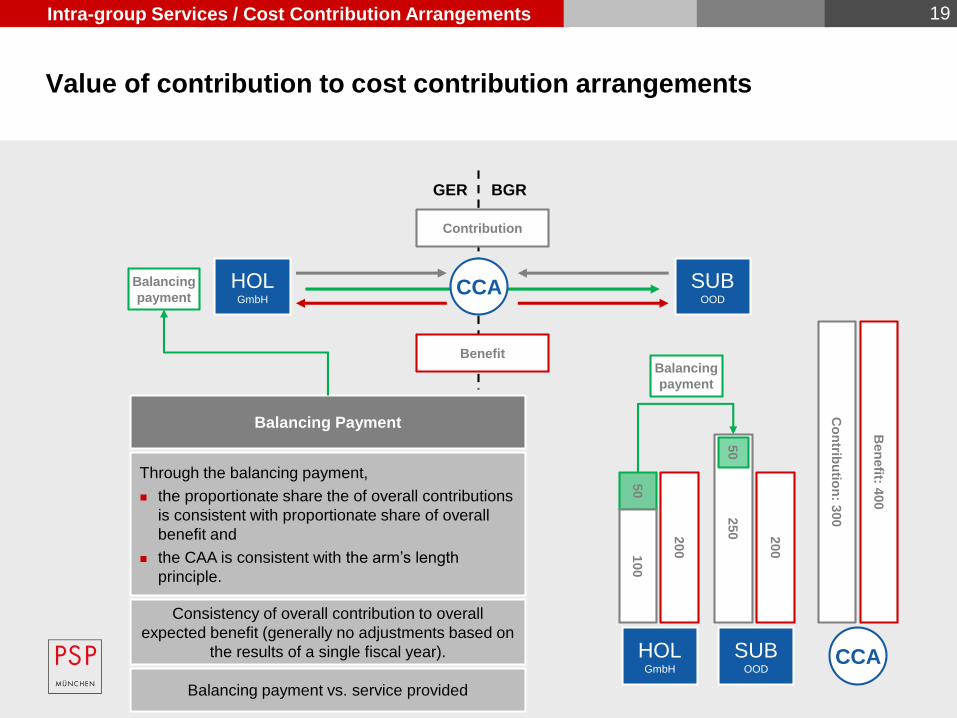

Value of contribution to cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

CCA

Total contribution

Services

Current contributions

Valuation according to arm’s length principle

Pre-existing

intangibles

Activity: R&D,

etc.Valuation based on value of

functions performed (Cost-

based approach in exceptional

cases)

Pre-existing contributions

Valuation based on expected

value of benefit (e.g.

Intangible)

HOLGmbH

SUBOOD

CCA

200

200

Ben

efit: 4

00

100

250

Co

ntrib

utio

n: 3

00

Value of contribution is assessed based on value at the time

they are contributed bearing in mind the sharing of risk and the

nature and extent of expected benefit

Risk

Value of

Contribution

Value of

Benefit

=

Intra-group Services / Cost Contribution Arrangements

250

19

Value of contribution to cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

Balancing Payment

Through the balancing payment,

the proportionate share the of overall contributions

is consistent with proportionate share of overall

benefit and

the CAA is consistent with the arm’s length

principle.

Consistency of overall contribution to overall

expected benefit (generally no adjustments based on

the results of a single fiscal year). HOLGmbH

SUBOOD

CCA

200

200

50

50

Balancing

payment

CCABalancing

payment

Balancing payment vs. service provided

Ben

efit: 4

00

Co

ntrib

utio

n: 3

00

100

Intra-group Services / Cost Contribution Arrangements 20

Entry, withdrawal, termination

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

CCABalancing

payment

Entry

Reassessment of proportionate shares of participants’ contribution and expected

benefit

Withdrawal

Party entering might

obtain an interest in any

results of prior CCA

(completed or work-in-

progress intangible)

Transfer part of respective

interest in results of prior

CCA: arm’s length buy-

in-payment

Party leaving might

transfer an interest in any

results of prior CCA

(completed or work-in-

progress intangible)

Transfer part of respective

interest in results of prior

CCA: arm’s length buy-

out-payment

Termination

Participant retains an

interest in the results of

the CCA consistent with

their proportionate share

of contributions

or

Participant is

appropriately

compensated for any

transfer of interest

Intra-group Services / Cost Contribution Arrangements 21

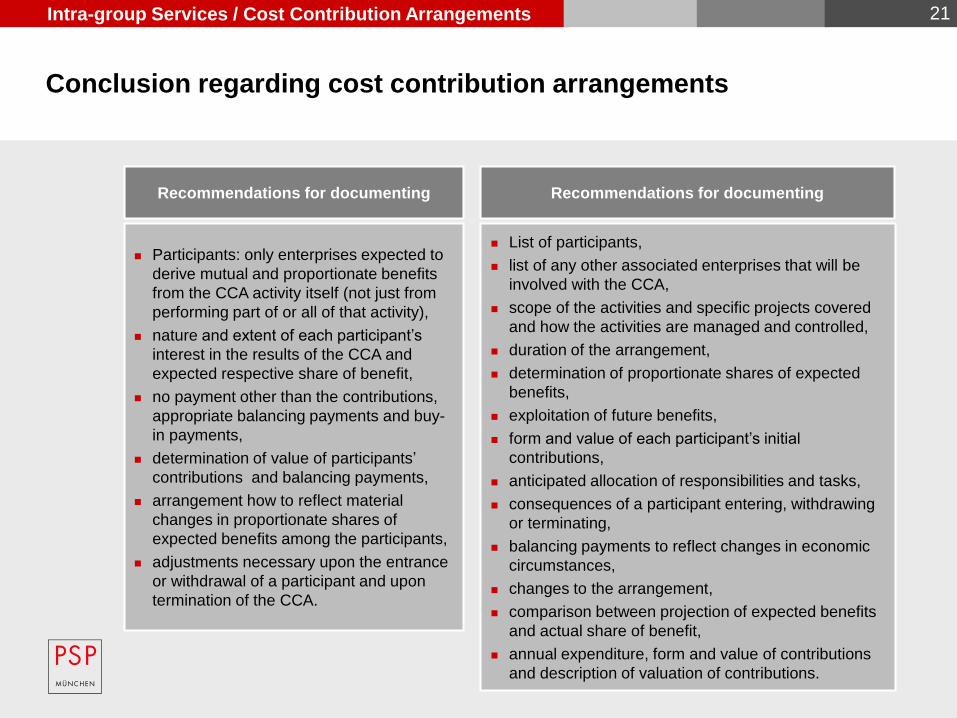

Conclusion regarding cost contribution arrangements

Recommendations for documenting

Participants: only enterprises expected to

derive mutual and proportionate benefits

from the CCA activity itself (not just from

performing part of or all of that activity),

nature and extent of each participant’s

interest in the results of the CCA and

expected respective share of benefit,

no payment other than the contributions,

appropriate balancing payments and buy-

in payments,

determination of value of participants’

contributions and balancing payments,

arrangement how to reflect material

changes in proportionate shares of

expected benefits among the participants,

adjustments necessary upon the entrance

or withdrawal of a participant and upon

termination of the CCA.

Recommendations for documenting

List of participants,

list of any other associated enterprises that will be

involved with the CCA,

scope of the activities and specific projects covered

and how the activities are managed and controlled,

duration of the arrangement,

determination of proportionate shares of expected

benefits,

exploitation of future benefits,

form and value of each participant’s initial

contributions,

anticipated allocation of responsibilities and tasks,

consequences of a participant entering, withdrawing

or terminating,

balancing payments to reflect changes in economic

circumstances,

changes to the arrangement,

comparison between projection of expected benefits

and actual share of benefit,

annual expenditure, form and value of contributions

and description of valuation of contributions.

Intra-group Services / Cost Contribution Arrangements 22

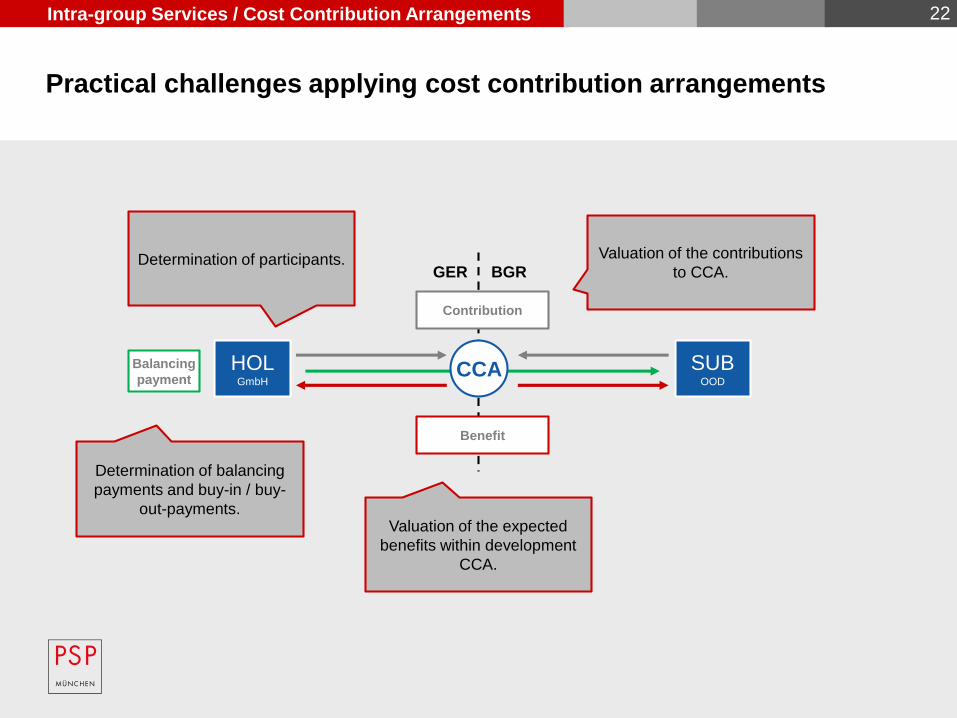

Practical challenges applying cost contribution arrangements

HOLGmbH

SUBOOD

GER BGR

Contribution

Benefit

CCABalancing

payment

Valuation of the expected

benefits within development

CCA.

Valuation of the contributions

to CCA.Determination of participants.

Determination of balancing

payments and buy-in / buy-

out-payments.

Intra-group Services / Cost Contribution Arrangements 23

Thank you very much for your attention

Peters, Schönberger & Partner

Rechtsanwälte Wirtschaftsprüfer

Steuerberater

Schackstraße 2

80539 Munich

Phone: +49 89 3 81 72 - 0

Fax: +49 89 3 81 72 - 204

Email: [email protected]

Internet: www.psp.eu

Speaker

Dr. Axel von Bredow, MBR