hotel market and the sell hotel investment market · 2 agenda • about jones lang lasalle hotels...

TRANSCRIPT

HOLD

BUY

SELL

LEASE

REFINANCE

DEVELOP

MANAGEMENT CONTRACTGraham Dodd

Ian Thompson

10 April 2008

The Manchester Hotel Market and the UK Hotel Investment Market

UK

2

Agenda

• About Jones Lang LaSalle Hotels

• Hotel Development

• UK Operating Market

• UK Investment Market

• Manchester Overview

• Liverpool Overview

• Leeds Overview

3

Who are we?

EMEA Americas Asia/Pacific

Investment Sales & Acquisitions Valuation & Advisory

Asset Management Corporate Finance

Development

4

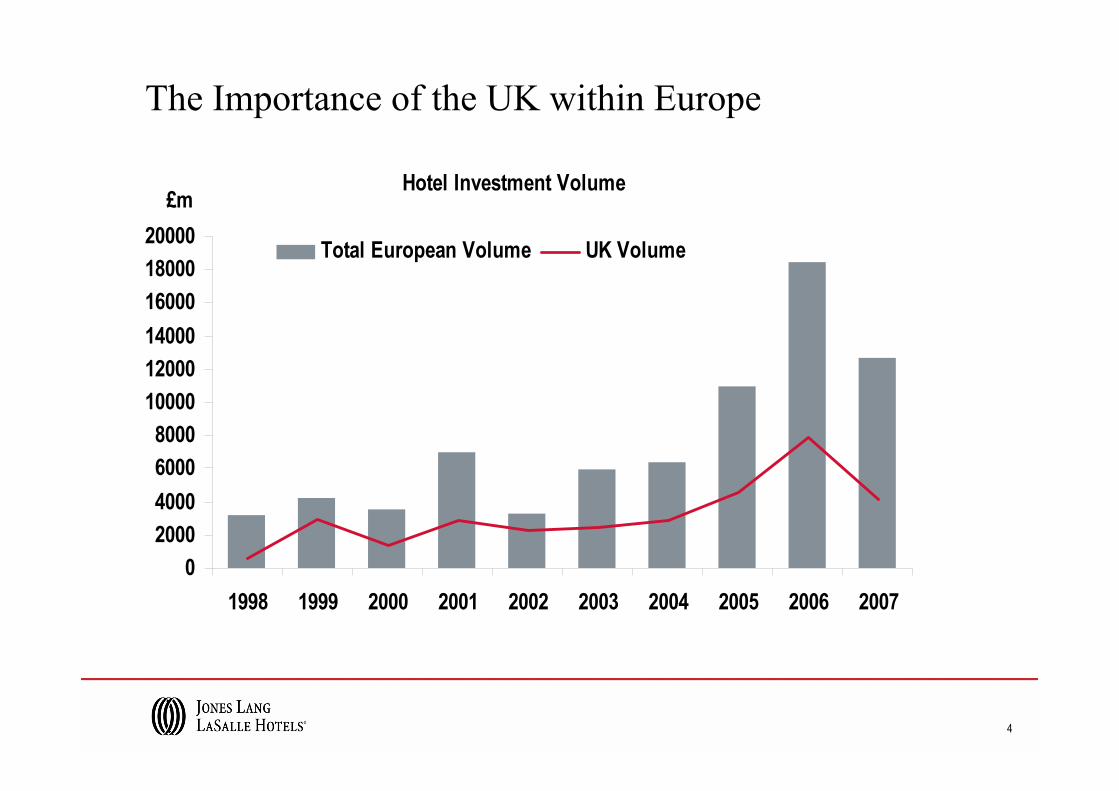

The Importance of the UK within Europe

Hotel Investment Volume

02000400060008000

100001200014000160001800020000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

£m

Total European Volume UK Volume

5

UK Transactions by Deal Structure - 2000 vs 2006/7

0%10%20%30%40%50%60%70%80%90%

VP Inv estment MC S & L P2P Corp Franchise

2000 2006 2007

- Owner / operator sales vastly reduced

- Management contract proliferation

- Sale and leaseback trend

6

Changing Buyer Profile

UK Transactions - Proportion of Buyers

0%

10%

20%

30%

40%

50%

60%

70%

80%

PublicHotel

Operator

PrivateHotel

Operator

PrivateEquity

HNWI PropertyCompany

InstitutionalInvestor

Developer REIT PublicCompany

2000 2006 2007

2000- Dominance of public and

private operators- Private Equity virtually non

existent2006- Move from public to private- Growing influence of private

equity- Emergence of PropCos and

HNWI2007- Accelerated interest from

PropCos and institutions, willingness to accept operational risk

7

What is the impact of the credit crunch on development?

• Business as usual?- Strong operator demand- Positive long term view of trading, investment and funding

• What lenders are looking for in hotel developments- Appointment of hotel operator - Prefer city centre - Clear strategy and process, detailed business plan including costing and timeline- Description and track record of parties involved – building company, architects,

asset managers, operator - Ability to be re-let to alternative hotel operators

8

Which Brands will Win?

• Tie in with aggressive equity / development partner- Shiva (Hilton), WG Mitchell (Rezidor), Land Securities (Accor)

• Recognisable name in the UK- Hilton, Marriott, IHG, Starwood

• Consistency v flexibility of product- New builds v conversions

• Brand differentiation- From other brands and within their own brand stable

• Efficient construction / space requirement• Flexibility in structures - management / lease / site purchase

- Premier Inn, Accor

• Offer leases- Travelodge, Accor, Premier Inn, Golden Tulip, Jury’s Inn

9

New Brands Entering the UK Which Brands will Win?

10

What is the impact of the credit crunch on the operating market ?

• As of now, not much !• Upscale / mid market / limited service• Cyclicality versus counter cyclicality• Lease versus management contract• Increasing operating costs• Decreasing consumer spending / business confidence

11

What is the impact of the credit crunch on the investment market ?

• 2007 – A year of two halves• H2 2007 vs H1 2008• Yields moving out but how far?• Valuation dilemma

12

Where Are We Now?

• Slowdown in volume of transactions

• Some investor groups may withdraw but others may return

• Risk may be more properly analysed and priced in- Greater due diligence- More sensible projections- Greater emphasis on using sector-experienced professional teams- Banks committed to sector for the long term - Deal thresholds versus Closure certainty

13

Where Are We Going?

• Are investors now shying away from hotels as too risky – have we lost the new classes of investors?

• Will the trend towards accepting operational risk be reversed?

• Leases versus management contracts?

• Will we see discomfort or distress in the market?

• Price plateau or price correction?

14

Manchester Hotel Market

• Third Most visited city after London and Edinburgh• Improvement in facilities and infrastructure• Strong Conference and Events industry – G-Mex, MICC, Bridgewater Hall

and the MEN Arena• Major events scheduled for 2008• Strong leisure market – Cultural attractions, International Sports Facilities • International Airport

- 22 Million passengers 2007- 42 Million passengers forecast 2015

• Growth in International arrivals

General Overview

15

Manchester Hotel Market

• Approximately 66 graded hotels or 8,137 bedrooms

• Dominated by Four Star hotels – only two Five Star

• 2004 – Arora International, Radisson Edwardian,

• 2005 – Mostly budget hotels – Travelodge (Great Ancoats St), Quality Hotel, Travelodge (Airport), significant number of budget hotels in Greater Manchester

• 2006/07 – Hilton Deansgate, City Inn, Macdonald Hotel

• 2008 and beyond – 1,430 bedrooms either under construction or proposed including Etap and Ramada (Salford Quays), Crowne Plaza(Shudehill), Tulip Inn (Whitworth Street) and Park Inn (Cheetham Hill)

Existing and Future Hotel Supply

16

Manchester Hotel Market

• Average Room Rate – 2007 £74.7 - 2008(F) £77.0 +3.10%

• Occupancy – 2007 74.4% - 2008(F) 74.5% +0.2%

• RevPAR – 2007 £55.6 – 2008(F) £57.40 +3.2%

• As quality hotels continue to enter market = Positive ARR growth

• New supply = stagnant occupancy

Operating Market

17

Manchester Hotel Market

• Significant development activity in last few years

• Few single asset transactions

• Alias Hotel Rosetti sold to ABODE price in excess of £10m

• The Lowry was marketed during 2006 but never transacted

• Going back to 2004 the Midland was sold to QHotels for around £35m and the Radisson SAS at Manchester airport transacted at around £50m

Investment Market

18

Manchester Hotel Market

• 2008 is set to be a very active event year

• However supply is expected to grow by around 8%

• Overall we would concur with circa 3% RevPAR growth for 2008

• New hotel supply will lead to a polarization within the city – older hotels will be forced to contemplate refurbishments or risk losing market share

• Branding and location will be very important in terms of ensuring continued success

Conclusion

19

Liverpool Hotel Market

• European City of Culture 2008• Significant inward investment over last few years• Since 2002 Liverpool has seen an additional 600 bedrooms• Occupancy has largely been stable at around 73% • ARR increase from £53 to £63• Strong weekend market – softer during week• Marked improvement of quality – Malmaison, Hard Days Night Hotel and other

boutique hotels• 900 further rooms over next 2 years – Jurys Inn, Hilton and Staybridge Suites• 2008 set to be a good year – beyond this will be dependent on how Liverpool

continues to market itself to the global market

General Overview

20

Leeds Hotel Market

• A significant commercial hub – strong retail centre – well established legal and financial sector

• 1,500 new hotel rooms since 2002

• New supply from 2008 onwards – City Inn (333 beds), De Vere Village (109 beds), Hampton by Hilton (120 beds), Hilton (200 beds), Roomzzz (38 beds) plus other mixed use sites

• Next few years will be challenging with a 20% increase in supply forecast

• Conference and events market not as strong but could improve following new mixed use schemes in the city

General Overview

21

Performance Overview

Full Service Market - Key Performance

CITY_MARKET Occupancy Average Rate RevParOccupancy

% ptsAverage

Rate RevPar

Leeds 71.0% 65.01£ 46.15£ Liverpool 77.0% 72.02£ 55.48£ Manchester 78.9% 75.90£ 59.89£

Leeds 72.1% 66.64£ 48.01£ 1.1% 2.5% 4.0%Liverpool 73.3% 75.39£ 55.28£ -3.7% 4.7% -0.3%Manchester 75.9% 79.61£ 60.40£ -3.0% 4.9% 0.8%

Leeds 66.7% 66.73£ 44.52£ Liverpool 70.7% 72.26£ 51.12£ Manchester 72.6% 79.21£ 57.49£

Leeds 70.2% 67.74£ 47.57£ 3.5% 1.5% 6.8%Liverpool 69.9% 76.35£ 53.34£ -0.9% 5.7% 4.4%Manchester 67.9% 80.14£ 54.45£ -4.6% 1.2% -5.3%

Ytd Feb 07

Ytd Feb 08

YoY %

Year 2006

Year 2007

Source: TRI Hospitality Consulting

22

Performance Overview

Source: TRI Hospitality Consulting

Lodge Market - Key Performance

CITY_MARKET Occupancy Average Rate RevParOccupancy

% ptsAverage

Rate RevParYear 2006

Leeds 69.1% 44.34£ 30.65£ Liverpool 80.7% 43.37£ 34.99£ Manchester 75.2% 45.25£ 34.03£

Year 2007Leeds 68.9% 41.68£ 28.72£ -0.2% -6.0% -6.3%Liverpool 79.7% 45.59£ 36.35£ -0.9% 5.1% 3.9%Manchester 76.2% 46.37£ 35.34£ 1.0% 2.5% 3.8%

Note : Lodge sample adjusted to ensure no one operator represents more than 40% of hotel supply

YoY %

23

Full Service, Worldwide Coverage

• Valuation advice• Due Diligence • Transaction

negotiation• Mgmt. contract

negotiation• Debt financing• Equity structuring

INVESTMENT SALES

• Unparalleled track record

• Specialist hotel focus • Integrated global team

of experts• Worldwide investor

relationships

ACQUISITION SERVICES

• Corporate Stock exchange listing

• Takeover defense • Joint-venture

structuring • Balance-sheet

revaluation

ASSET MANAGEMENT

• Operational reviews • Operator selection /

negotiation • Budget appraisal /

negotiation • Benchmarking• Profitability

enhancement

• Arrange first mortgage, mezzanine and joint venture equity financing

FINANCING VALUATIONS

As the global leader in hotel advisory services and investment sales, we provide hotel owners, investors, financiers, and operators with a range of specialized hotel and leisure investment services.

24

Thank you

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2008