hp presentation final pdf (2008.12.22)

TRANSCRIPT

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 1/78

HP Strategic Analysis

Keep Aggressive:

Go Horizontally & Vertically

Nov. 27, 2008

Univer sity du Quebec en Outaouais

Presented to : Dr. Tamas Koplyay

MGP708QA

Strategy Formulation in High-tech and ProjectManagement Setting

Team Members

Arman Matti

Florentina Macovei

Jian ni Chen

Sahar Kamaly

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 2/78

Agenda

•Background Information (HP & IT Industry)

•Market Dynamics

•Corporate Profile

•Strategic Fits

•Recommendations

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 3/78

Importance of Corporate Strategy

“

“Quote”

organization is like a shipwithout a rudder, going aroundin circles.”

Joel Ross and Michael Kami

Strategy is management’s “game plan” to:

• Attract and please customers

• Stake out a market position

• Conduct operations

• Compete successfully

• Achieve organizational objectives

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 4/78

HP Background

HP Background

Hewlett-Packard Company (HP) is well known as a technology solutions provider to

consumer, businesses and institutions globally.

• HP was founded in 1939 in a garage building, where two college friends, Bill Hewlettand Dave Packard created a development lab and manufacturing facility for their innovative electronics products.

• Corporate headquarters is in Palo Alto, California.

• HP is a global provider of personal systems, imaging and printing products, andtechnology solutions. The company is the largest player in the inkjet printer and laser printer market. Hewlett-Packard is one of the major companies in the enterprisestorage and servers market. The company is also one of market leaders in the globalPC market.

• Hewlett-Packard generates revenues primarily through seven business divisions:personal systems group, imaging and printing group, enterprise storage and HPservices , HP financial services , software and corporate investments.

• The USA is the company's largest geographic market, accounted for 33.4% of thetotal revenues in fiscal 2007.

Non-US operations accounted for 66.6% of the total segment revenues in the fiscal year

2007.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 5/78

Market share

• Hewlett-Packard is the market leader in distributed performance and availabilitymanagement software market. The company also led the industry in thin client unitshipments with approximately 34% market share.

• Strong market position in various market segments enhances the brand image of the

company and provides economies of scale in procurement.

HP financial positioning

• World’s largest IT companies- Revenue totaling $113.1 billion at the end of July 2008and 325,000 employees

• Hewlett-Packard’s long-term debt ratio stood at 0.1 for the fiscal year ended October 2007 compared with IBM’s long-term debt ratio of 0.22 for fiscal year endedDecember 2006.

• Hewlett-Packard had cash and cash equivalent of $13,293 million compared to IBM’s$8,023 million for fiscal year ended December 2007.

• Strong financial position provides the company the flexibility of expanding itsgeographical coverage and product portfolio by acquisition.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 6/78

HP Mission, Vision and Values

•Mission: Create, Solve and Reach customers

•Vision:− Market Leadership

− Continuous growth

−Higher profits

•Values:

− Trust and respect

− Speed and agility

− Meaningful Innovation

− Integrity

− Efficiency

•

Mission: Create competitive advantage by optimizing availability, performance andoperational efficiency , solve their business problems

• Vision: Hewlett once said that the “HP Way was a core ideology” . . . [that] includesa deep respect for the individual, a dedication to affordable quality and reliability, acommitment to community responsibility, and a view that the company exists tomake technical contributions for the advancement and welfare of humanity.“

• Trust and respect for customers and employees – culture of inclusion

• Speed and agility - resourceful, adaptable and achieve results faster

• Meaningful Innovation – invest in useful and significant technology

• Integrity – open, honest and direct in dealings

• Achievements, contribution, results through teamwork - provide efficiency tocustomers

Strategy deals with a company’s competitive initiatives and business approachesand Business Model -- Concerns more if the revenues and costs flowing from thestrategy demonstrate that the business is profitable and viable

Before you formulate a strategy the organization need to have a clear Mission, Visionand Values.

•

A mission statement focuses on current business activities -- “who we are and whatwe do”

• Current product and service offerings

• Customer needs being served

• Technological and business capabilities

• A strategic vision concerns a firm’s future business path -- “where we are going”

• Markets to be pursued

• Future technology-product-customer focus

• Kind of company that management is trying to create

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 7/78

Corporate Profile

HP -- The Technology Solutions Provider

• HP: founded in 1939, California.

• IPO : November 1957

• Leading global provider

•

• Largest global IT company

• Market Advantage: leaders in some business segments

• Leading global provider in computing, imaging solutions and services for

business and home services,

• Market leader in printers and low-end servers, but trails Dell in PCs and IBM in

services

• Growing large size corporation with : more than 700 suppliers, 400 contract

manufacturing sites worldwide, 500 partners including leading software

pioneers, network service providers, and business, process specialists .

• Market Advantage – leader in providing mission-critical services and support

across all operating systems and to IT infrastructure, including storage, system

software, and the network.

• HP is a technology company that operates in more than 170 countries around the

world.

• HP provides infrastructure and business offerings from handheld devices to

some of the world's most powerful supercomputer installations (Itanium)

• Company offer consumers a comprehensive portfolio with a wide range of

products and services from digital photography to digital entertainment and from

computing to home printing.

• In 1959 HP becomes a global company by establishes a European marketing

organization in Geneva, Switzerland, and a manufacturing plant in Boeblingen,

Germany. From this base, HP steadily expands its European operations.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 8/78

• In 1962 HP enter the Fortune 500 US companies at number 460 and continues

to climb reaching number 11 in 2004 and 2008 remain at number 14

• HP Overall Positioning

• Number 1 - globally in the inkjet, all-in-one and single-function printers, mono

and color laser printers, scanners, print servers and ink and laser supplies

• Number 1 -globally in desktop PCs and notebooks,

• Number 2 - globally in Pocket PCs and workstations - The company is the

second largest entity in the servers market behind International Business

• Machines (IBM), with its server range extending from low-end systems to high-

end systems.

• Number 1 - globally in blade, x86, Windows®, Linux, UNIX and high-end UNIX

servers

• Number 10 - globally and Number 1 in the U.S. in Environment, Social Impact

Ratings by The Economist

• Number 22 - in the Accountability Rating, the first global index that evaluates

how well the world's 100 largest companies account for their impact on society

and the environment

• Listed on all four FTSE4Good Index lists — U.S., Global, UK and Europe —

which rate the performance of companies meeting globally recognized corporate

responsibility standards

• Source: IDC Q1 2008 for all categories except large-format printing, print servers

and supplies for which source is HP. ** Refers to factory revenue. Source: IDC

Q1 2008.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 9/78

Company profile - Revenues

$140,000

Revenue Comparison ($ millions)

$60,000

$80,000

$100,000

$120,000HP

IBM

DELL

$0

$20,000

,

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Note: For IBM and DELL, Revenues available only for 3 quarters

1. HP: a leading global provider of computing and imaging solutions and services -- is

focused on making technology and its benefits accessible to all. HP had total

revenue from continuing operations of $48.8 billion in its 2000 fiscal year

2. Before the merger with Compaq in 2000, HP focus on computers, Imaging and

printing services. Compaq core business was in computer, enterprise technology

and solutions. Apparently, HP wanted to expand its business territory to Enterprise

after its acquisition with Compaq. Looking at the Revenue graph HP doubled it's

enterprise business revenues in 2002, the same year after finishing the marriage

with Compaq.

3. Compaq: Founded in 1982, Compaq Computer Corporation (“Compaq”) and was a

leading global provider of enterprise technology and solutions. Compaq designs,

develops, manufactures and markets hardware, software, solutions and services,

including industry-leading enterprise computing solutions, fault-tolerant business-

critical solutions, communication products, and desktop and portable personal

computers that are sold in more than 200 countries.

4. From the graph continuous revenues growth except in 2001 when Compaq wasacquired and first year of merger the revenue were not so great also due to crisis in

high tech and low demand.

5. Applying different strategies over the years the HP maintained the second place

after the IBM up to year 2007 when HP revenues 104,286 millions versus 98,786

millions IBM revenues.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 10/78

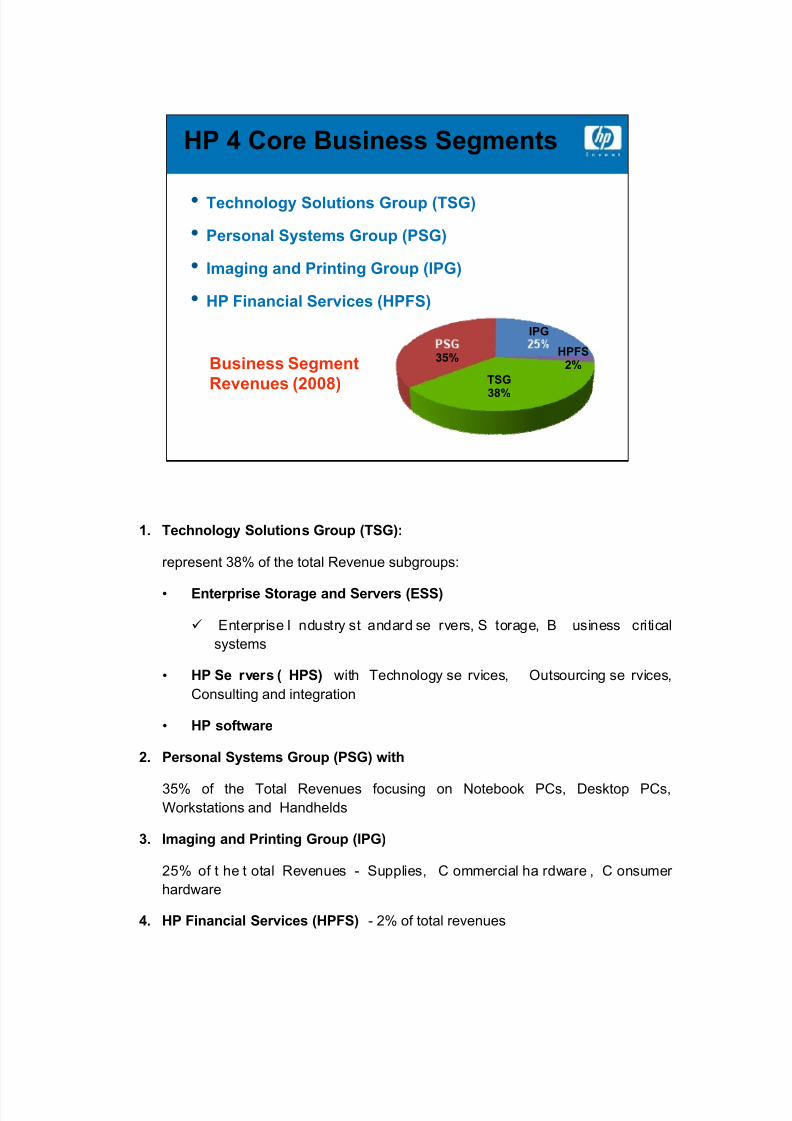

• Technology Solutions Group (TSG)

HP 4 Core Business Segments

• Personal Systems Group (PSG)

• Imaging and Printing Group (IPG)

• HP Financial Services (HPFS)

IPG

Business SegmentRevenues (2008)

HPFS2%

TSG

38%

35%

1. Technology Solutions Group (TSG):

represent 38% of the total Revenue subgroups:

• Enterprise Storage and Servers (ESS)

Enterprise I ndustry st andard se rvers, S torage, B usiness critical

systems

• HP Se rvers ( HPS) with Technology se rvices, Outsourcing se rvices,

Consulting and integration

• HP software

2. Personal Systems Group (PSG) with

35% of the Total Revenues focusing on Notebook PCs, Desktop PCs,Workstations and Handhelds

3. Imaging and Printing Group (IPG)

25% of t he t otal Revenues - Supplies, C ommercial ha rdware , C onsumer

hardware

4. HP Financial Services (HPFS) - 2% of total revenues

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 11/78

HP Products & Services

Services Imaging and Printing Hardware

• Technology

• Consulting &

• Printers • Digital Cameras

• Digital Presses • Cartridge & Paper

•

Hardware

• Server

• Storage

Software Solutions IPG

HPF

PSG

• IT management &Outsourcing

•

• Photo Kiosks

• Printing-related media

• Online photo services

• publishing & graphicsprinting solutions

IPG Solutions

• BTO Software Solutions

• Supports

• etwor

TSGS

PCs

e a e ro uc sHPFS & Others

• Digital Entertainment Center

• LCD flat-panel TV

• DVD writers

• RW drives

• HD DVD• Desktops • Workstations

• Laptops • Handhelds

• Financial management services

• Leasing

• Financing

• Utility programs

• Asset recovery services

• Data extracted from HP Quarter Report 2008 (Q1-Q4)

HP Products & Services

• Data extracted from HP Quarter Report 2008 (Q1-Q4)

•

IPG- Imaging and Printing Group

• PSG –Personal System Group

• HPFS- HP Financial Services

• TSG - Technology Solutions Group

• BTO: Business Technology Optimization

• Hewlett-Packard has high brand equity. The company is one of the leading

brands in the technology sector along with Microsoft, IBM and Intel. Hewlett-

Packard figured in ‘The 100 Top Brands 2008’ of Business Week magazine.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 12/78

HP History Line

•HPfounded

1939

• Agilentdivestiture

• Chan ed

2000

• HP-Compaqmerger

• Ac uired

2002

• Digital entertainmentstrategy announced

• Won Cor orate

2004

• AcquiredVoodoo PC

• Ac uired

2006

• Acquired EDS

• AcquiredLefthand

2008

1999

•

2001

•

2003

•

2005

•

2007

•

CEO Indigo

• Opened IndianR&D lab

Innovation Award

• Revolution imaging &printing projectiontechnology released

Mercury• Stated several

horizontalcooperation

spin off

unit - HPServices

• Announced

new 64-bitplatform

strategy

• Initiated Smallmedium business

market• Imaging & printing

simplify-technology

• Acquired 5companies

• Acquired 2companies toexpand Imaging &

printing• China R&D lab

established

center strategy

• 7 acquisitionscompleted

• AdvocatedGreen IT

• HP: The technology solutions provider

• 1938 - Stanford University graduates Bill Hewlett and Dave Packard collaborate onthe company's first product, an audio oscillator, in a Palo Alto garage.

• 1939: Hewlett and Packard formalize their partnership on Jan. 1, 1939, deciding thecompany's name with a coin toss.

• 1940: HP moves from the garage behind Hewlett and Packard's house to rentedbuildings in Palo Alto. The start of World War II brings increased U.S. governmentorders for electronic instruments. Revenues at year-end total $34,396.

• 1957: HP goes public on Nov. 6 for $16 per share.

• 1999: Agilent Technologies - spun off as a new company (a public subsidiary) fromthe existing HP organization.

• HP named Carleton (Carly) S. Fiorina as President and CEO

• The first Windows CE pocket-size PC with a color screen has been introduced.

• HP began a new brand campaign based on a single concept: invent. (Print andtelevision ads focus on the company's history of invention and innovation.)

• HP revenue: $42 billion. HP employees: 84,400.

• 2001 Created a new business unit (HP Services). The new organization includes ITconsulting, outsourcing, support, education and solutions deployment.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 13/78

• HP and Intel cooperated and announced a new technology product -- Itanium (theplatform for next-generation 64-bit computing)

• HP and Compaq announced a definitive merger agreement to create an $87 billionglobal technology leader.

• HP revenue: 45.2 billion. HP employees: 88,000.

• 2002:

• HP opened the research Labs in India;

• Completed the acquisition of Indigo

• Acquisition impacts: The acquisition extends HP's printing systems portfoliobeyond inkjet and LaserJet technology into a third high-speed color printtechnology - offset-quality digital press solutions and services for short-run,personalized business communications.) results: HP announced its largestconsumer product rollout

•

HP and Compaq officially merged

• Merged Impacts: lead global provider of products, technologies, solutions andservices to consumers and businesses. Business scope span IT infrastructure,personal computing and access devices, global services and imaging andprinting

• HP introduced its first tablet PC (collaborated with Compaq)

• HP revenue: 56.6 billion. HP employees: 141,000.

• 2003:

• The value proposition changed to high tech, low cost and the best total customer experience.

• Adapted Enterprise strategy to help businesses manage change and get more fromtheir IT investments. (New services, software, solutions and enterprise referencearchitecture designed to help companies measure, architect and manage change bycreating a tighter linkage between business and IT.)

• Simplified technology radically to help people "enjoy more"

• Impact: extends HP's leadership in imaging, printing and home computing intothe fast-growing digital photography and entertainment markets)

• Initiated the Smart Office that tailored support services to serve small and medium-sized business (SMB) market.

• 2005:

• Changed CEO: Mark Hurd was named the CEO and president of HP.

• HP acquired online photo service company – Snapfish.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 14/78

• HP announced a breakthrough printing platform (fastest home and office photoprinting devices)

• HP shipped the millionth x86 processor-based ProLiant server (, which was initiatedthe first shipment in 1993)

• HP acquired Scitex Vision and expanded its printing market to industrial professional

field. (Scitex Vision was a market leader in wide and super-wide format printers for signage and industrial applications such as billboards, banners, street advertisingand packaging.)

• HP establishes a research lab in China.( for more lab history, please refer toHISTORY AND MILESTONES SUPPLEMENTAL section hereinafter)

• Created the Halo Collaboration Studio, which enabled remote teams to work together in a setting so life-like that participants feel as though they are in the same room.

• 2006:

• CEO Mark Hurd was named as chairman of the board.

• HP acquired VoodooPC, a high-end gaming PC provider

• HP acquires Mercury Interactive Corp., (A software company, its core productwas WinRunner ), which was the subsidiary of HP for business technologyoptimization (BTO).

• Fortune 500 Ranking: 14

• HP revenue: $91.6 billion. HP employees: 156,000.

• 2008:

• HP's 2008 Fortune 500 ranking: No. 14

• HP's revenue for the four fiscal quarters ended July 31, 2008: $113.1 billion.

• HP Announces Strategy to Bridge Gap Between Content Creation and Publishing (Jan)

• Cooperated horizontally:

• ProCurve Networking by HP Strengthens Network Security Through Integrationwith Microsoft NAP Technology

•

(Apr)

•

MySpace (Microsoft) and HP to Unlock Online Content Through the Power Of Print

HP Acquired LeftHand Networks to Extend Leadership in Storage andVirtualization Solutions

• Announced a new relationship with U.K.- based Timsons Ltd., the world’slargest book press manufacturer, to develop a digital inkjet system for short- andmedium-run book production. (Oct)

(Oct)

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 15/78

• HP and Foxconn Expand PC Business in Russia

• Completed $13.9 billion acquisition of EDS, and started integration sequence withHP Service.

(May)

(EDS was a $22 billion-plus global technology services, outsourcing and consultingleader that pioneered the IT outsourcing industry.)

• Signed a definitive agreement to acquire Colubris Networks Inc.,to Expand HPProCurve’s Wireless Technology (Aug)(http://www.hp.com/hpinfo/newsroom/press/2008/080811b.html?jumpid=reg_R1002_ USEN)

• Colubris is a Waltham, Mass.-based, privately-held global provider of intelligentwireless networks for enterprises and service providers. (Aug)

• HP plans to integrate Colubris’ extensive product line into its ProCurveNetworking product portfolio. This will expand HP ProCurve’s reach into verticalmarkets such as hospitality, transportation, healthcare, manufacturing, service

provider and education.• It will simplify operations and achieve lower total cost of ownership for their

storage-area network (SAN) environments

• HP Unveils Innovative Large-format Printing Solutions (Oct)

• HP Makes Big Investment in Consumer Tech Support - the aim of which is to enablepeople to get faster, more effective help with the HP technology products in their homes. (Feb)

• HP Introduces Servers, storage arrays, Customer Management Portfolio to ReduceCosts for Midsize Businesses

• Offered New Web Solutions, business/ marketing solutions and workshops (HP andSCORE Host Nationwide “Wellness” Workshops) for small organizations to reducecosts, :

• For enterprises: Announced a software and hardware storage virtualization solutionthat enabled enterprises to improve productivity. (Nov)

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 16/78

HP 4 Major Strategies

$118,364$120,000

$140,000

($ millions)

$39,330$42,371

$48,870$45,226

$56,588

$73,061$79,905

$86,696$91,658

$104,286

$40,000

$60,000

$80,000

$100,000

7-companyAcquisitions

R&D center

$2,678 $3,104 $3,561$624 -$923

$2,539 $3,497 $2,398$6,198 $7,264 $8,329

-$20,000

$0

$20,000

Revenues Net Incomes

• Strategy 1: Corporation Restructuring Strategy

HP spun off Agilent and focused on PC, imaging and printing market.

• Strategy 2: Merger Strategy (Horizontal)

Case: HP Compaq merger in 2002.

• Strategy 3: Acquisition Strategy ( Horizontal )

Case: Snapfish and other 11 imaging and printing companies acquisitions (from

2002 to 2008).

• Strategy 4: Acquisition Strategy (Horizontal and Vertical)

Case: EDS acquisition (2008).

Strategy - Focusing in things that HP can make a difference

2005- Organization starts focusing in their core fundamentals. To be competitive,being able to go to the marketplace and compete, and simplifying their organization,

HP will get their cost structure inline by focusing in leveraging the core assets.

HP is in the server business, storage business and in the management software

business markets that have large growth potential.

To be a leader in those markets HP has to take care of customers services.

Average per year HP ships 50 million printers, over 30 million PCs and a couple of

million industry standard servers.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 17/78

Customer Centric -. HP focused on getting a price-competitive product, created

value added for the customer, making sure that product is delivered in time and

offers good quality.

The HP goes to market by looking at the customer on a "segment of one" basis

understanding their service history, requirements for present and future giving

organization an opportunity to cross-sell and the ability to understand what their total

satisfaction with HP.

To improve customer experience, HP focuses on the importance of understanding

the entire experience and relationship that a customer has.

On the Enterprise Storage area HP continue to push on lowering the cost of

computing, leverage industry standards and continue to drive down the cost of

computing,

In the years to come HP is focusing in integration of management software, storage

management software, security and the ability to drive and manage that enterprise

remotely

Printing Imaging Business: For HP the printing-imaging business is a pretty strong

business that organization can compete well in the market place. Organization will

invest in R&D to increase the number of printed pages.

HP Services- organization is going to be very focused on the services business in IT

technology that will increase HP products sale. The services business is an

important business to HP since many organizations today start to look at outsourcingtheir business.

HP is a strong partnering company and we'll partner for some of those solutions to

make sure they support their customer.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 18/78

Revenue Trend per Segment

Revenue Trend of HP Business Segments

$25,000

$30,000

$35,000

$40,000

$45,000

,

TSG

IPG

PSG

$0

$5,000

$10,000

$15,000

$20,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

HPFS

• TSG

The r evenues o f TSG (Technology S olution Group) i ncreased al most 9 t imes

from 1998 to 2008 . A veragely, i t had 28 % r evenue i ncrease per y ear. Its

increasing rate was rank number 1 amongst 4 business segments in HP.

The TSG Revenues started to soar since 2001, after HP merged Compaq, from

2001 to 2002, the increasing rate of PSG group soared to 169% on a yearly

basis. The nex t hi ghest i ncreasing rate occu rred i n 2002 to 2003 fiscal y ear,

which r eached 38% . After 2003 , the i ncreasing sp eed slow dow n t o 8%

(maximum 12%/ year). In 2008, after HP acquired EDS, the TSG revenuesstarted to climb again, the increasing rate reached 19%/year.

Both the merger and acquisition strategies proved that HP made the right choice.

• PSG

Besides TSG, P SG i s the se cond co ntributor t o t he t otal r evenues in HP.

Averagely, PSG has 11% increasing rate/ year from 1998 to 2008. from 2001 to

2002 t wo fiscal y ears, a fter H P m erged C ompaq, i t’s revenues continued

dropping for 2 years, which can be understandable, because during that time, the

IT industry is going through an economy winter. Most of the companies who soldPCs had t heir revenues dropped dur ing t hat period. B ut t he bou nced bac k

numbers from 2002 to 2008 fiscal year illustrate that for a long run, this marriage

is worthy.

• IPG

Among three business segments, IPG is the group that keeps the lowest growth

since 2001. A lthough H P acquired Indigo(2002), sn apfish ( 2005) and o ther 10

companies from 2002 to 2008 , and it launched over hundreds o f products, it

seems that i t w as lack of some l ucky from t he i maging and p rinting market.

Maybe this group expand too fast horizontally, it need some vertical strategies,we will verify our assumption in the following models and SPACE analysis.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 19/78

•Background Information (HP & IT Industry)

•Market Dynamics

•Corporate Profile

ra eg c s

•Recommendations

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 20/78

Positioning Map – PCs

High

Quality

Price

LowHi h

Low

Competitors (PC)

• HP competes directly with Dell, Toshiba and Acer in terms of price and quality.

Other competitors such Lenovo and specially Apple have their niche, as it can be

seen from the diagram their prices are higher.

• HP (market share 18.9%)

• Dell (market share 16.4%)

• Acer ( market share 9.5%)

• Lenovo (market share 7.9%)

• Toshiba (market share 4.5%)

• Apple (market share 3.5%)

Reference: http://www.businessweek.com/investor/content/oct2008/pi2008106_

002546.htm

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 21/78

Positioning Map – Imaging & printing

Quality

Price

LowHi h

Low

Key takeaways from this slide:

Prices of al l major competitors are a l ittle h igher than H P, however in terms of

quality HP is third among competitors. They are still considered strong in imaging

and printing business and they offer all in one products.

Reference

• http://www.businessweek.com/investor/content/oct2008/pi2008106_002546.htm

• http://www.hp.com/sbso/expert/competitive.html

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 22/78

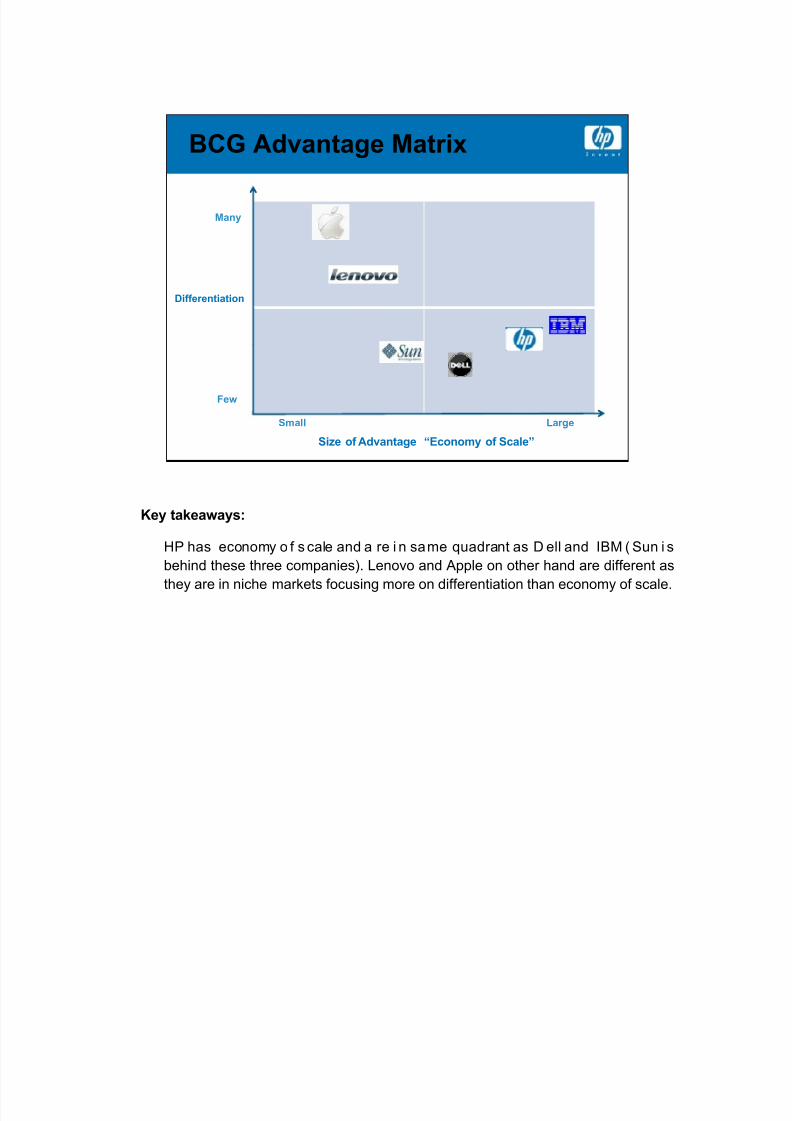

BCG Advantage Matrix

Many

Differentiation

Few

Small Large

Size of Advantage “Economy of Scale”

Key takeaways:

HP has economy o f s cale and a re i n same quadrant as D ell and IBM ( Sun i s

behind these three companies). Lenovo and Apple on other hand are different as

they are in niche markets focusing more on differentiation than economy of scale.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 23/78

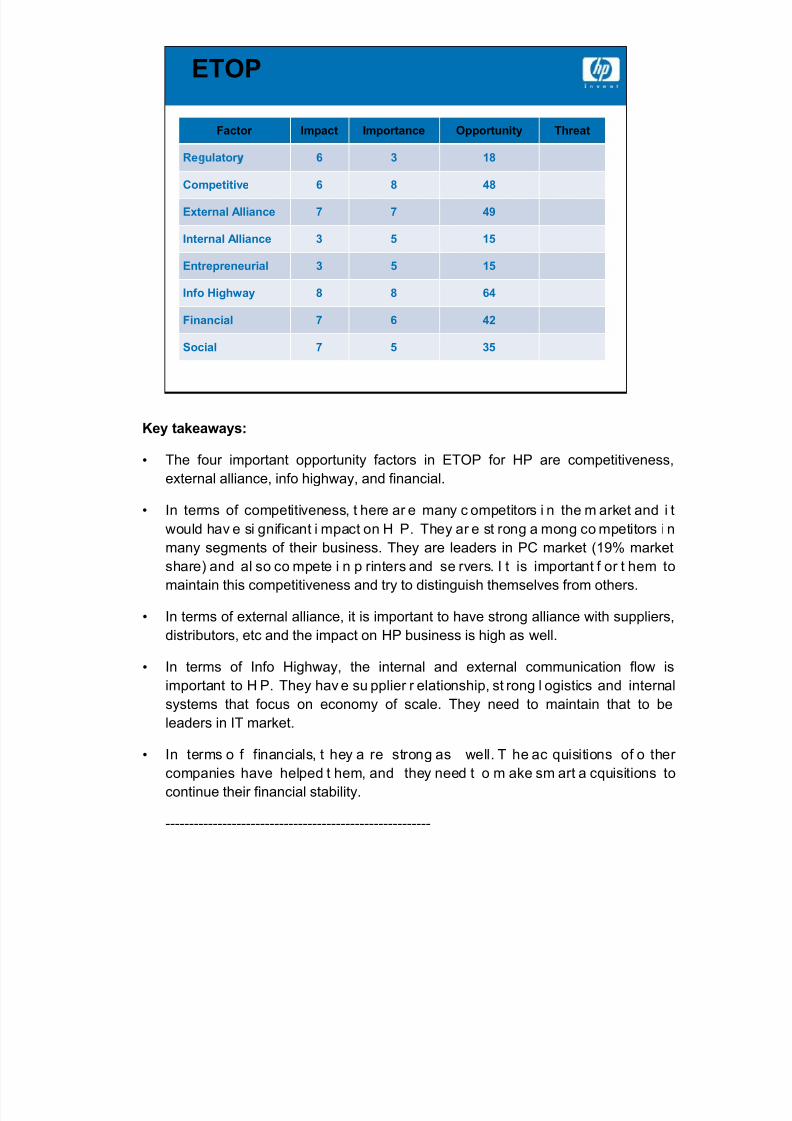

ETOP

Factor Impact Importance Opportunity Threat

Re ulator 6 3 18

Competitive 6 8 48

External Alliance 7 7 49

Internal Alliance 3 5 15

Entrepreneurial 3 5 15

Info Highway 8 8 64

Financial 7 6 42

Social 7 5 35

Key takeaways:

• The four important opportunity factors in ETOP for HP are competitiveness,

external alliance, info highway, and financial.

• In terms of competitiveness, t here ar e many c ompetitors i n the m arket and i t

would hav e si gnificant i mpact on H P. They ar e st rong a mong co mpetitors i n

many segments of their business. They are leaders in PC market (19% market

share) and al so co mpete i n p rinters and se rvers. I t is important f or t hem to

maintain this competitiveness and try to distinguish themselves from others.

• In terms of external alliance, it is important to have strong alliance with suppliers,

distributors, etc and the impact on HP business is high as well.

• In terms of Info Highway, the internal and external communication flow is

important to H P. They hav e su pplier r elationship, st rong l ogistics and internal

systems that focus on economy of scale. They need to maintain that to be

leaders in IT market.

• In terms o f financials, t hey a re strong as well. T he ac quisitions of o ther

companies have helped t hem, and they need t o m ake sm art a cquisitions to

continue their financial stability.

--------------------------------------------------------

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 24/78

Extra Information:

• Regulatory

•

Competitive

Holds strong market position, one of the leading IT companies (PC,printers, etc). Intense competition.

• External Alliance Strong, long-term, proven.

• Internal Alliance alliance between the segments, 4 groups (package selling)

• Entrepreneurial mature company, less entrepreneurial

• Info H ighway Internet ( internal and ex ternal communication, su ppliers and

logistics, financials)

•

Financial

HP has strong financials in recent years. It has reduced it is long termdebt from $4,494 million in 2003 to $4,997 million in 2007.

• Social Social responsibilities (internal and external), being fit with environment.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 25/78

IPG PSG

Effectiveness(externat focus)MarketPosition

Efficiency

(Internal focus)Operations

Product Life Cycle – Marketing/Strategy

Cost Leadership

Market DevelopmentProductDifferentiation Market Maintenance and defense

HP Financial &Software

HP Services

Market Pull Market Push Market Checkmate Market Expansion

Product development Focus Customers,

Focus on EfficiencyStrategies/Marketing

Product / service emphasis

Product / Production based

(Customers, Competitors, Suppliers)(customers) Competitors

Locked in Production / service emphasis

Production based

Hp i s a technology co mpany that i s competing in a mainly i n the mature market.

Their products in the TSG\ HPS and I PG segments, mostly have sh ort l ife cycles,

and always evolve. for HP to keep up with the innovations, they acquire companies

to lower risk compared to developing new products, to have a faster way to enter and

compete in the current market, and to have a quicker means to new capabilities

• As well t hey i nvest i n their R&D global l abs to realize new cu tting ed ge

innovations.

(If half of HP’s printing revenues were in the consumer market that would put 45% of

HP’s revenues in the consumer segment.) And where IBM now makes more than

half of its revenue from software and services, HP makes 80% of its revenues selling

hardware and (printing) supplies.

TSG:

• Server market facts: HP grew blade revenue 59.2%, year over year, gaining 6.2points of revenue market share while IBM lost 7.6 points of revenue share to fall

to 24.8%, more than 28 points behind HP.

• HP is the number 1 su pplier of I tanium based systems based on worldwide unit

volume and worldwide factory revenue. (ESS - HP growth was based only on the

Compaq merger and other acquisitions in 2005)

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 26/78

IPG:

In laser printers, HP holds a 55% worldwide market share as of the first quarter of

2007, acco rding t o research f irm I DC, f ar surpassing t he 10% share o f second-

ranked Samsung. In inkjet machines, too, HP's share is 45%, compared with

second-place Canon (CAJ), which holds a 26% share.

PSG (personal systems group) :

Hewlett-Packard remained the top se ller o f PCs i n the worldwide m arket, sh ipping

almost 14.8 million PCs and grabbing 18.4 percent of the worldwide market. Overall,

HP saw a 15.1 percent year-on-year growth in worldwide PC shipments. According

to Gartner HP remains the largest seller of PCs worldwide, although Dell is tops in

the U.S. and Acer is gaining ground.

HPS:

With i ts acquisition of EDS in 2008 HP st rategy is t o grow i ts on dem and-

infrastructure (outsourcing)

HP S ervices - This segment was slowly growing due to the Compaq merger and

other acquisitions such as Intria, Extrem logic, Triation, Synstar, and others in 2006

and 2007.

HP’s Services market ( 62% cu stomer su pport, 20% co nsulting a nd sy stems

integration, 18% managed services) is continuing to grow; customer support revenue

is up 9%, consulting and integration up 8%, and managed services up 50%.

Comments:

HP 4 segments were staidly growing by mostly acquisition :

In the TSG, PSG the biggest acquisition was the Compaq . During t2004 ,The PSG

and I PG so me or ganic growth w as achieved. 2 006 and 2007. Actually, r evenues

decline i n 2004, t he only year where no acq uisitions related to this segment were

made.

Signs of Maturity:

• Cost leadership: have economy of scale, where it was able to lower it’s prices (by

bringing uni t c ost dow n), and hav e hi gh v olumes. S ince 2005 , H P has

demonstrated its ability to improve profitability by focusing on costs.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 27/78

• It has currently 4 main business segments (Horizontal integration), and

throughout t he y ears from 2001 t ill now i t acq uired l ots of companies i n t he

various segments. It strategy is to buy competitors and expand its market share

way. (it buy market space).

• They are focused on being more efficient (cutting cost more then competitors).

• Knocking competition down (Compaq, EDS)

• They are no longer compete with smaller companies in the market, and compete

in the global market as well side by side with IBM.

• They want t o l ead a complete service so lutions to their mid and big si ze

companies. They adopting the One-Stop Shops: In other words, HP thinks want

to ov ercome i ts o f se parating out sourcing nee ds and sp reading them acr oss

vendors. HP seeks to be the first one-stop shop for outsourcing.

•

They have a stable growth, in a shake out market (buy smaller companies), andin a Push market as they are dealing with Early to late majority (depends on

segment).

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 28/78

Product Life Cycle – Competitions

Market Share Importance

IncreasingStable

No Competition Decreasingunstable

Increasingunstable

Equilibriumstable

Basis of Competitive Strength

Core Competencies Core Capabilities

Client base unstable

Client RelationsClient base stable Client base unstable

Competitor PressureLow asset base Maximum Decreasing

Economy of SState

High Barriers

SalesScope Scale

Synergy

Speed Span Structure SalesLow Barriers

HP was viewed as an innovative technology (core competency) information technology

company doing business in over 170 countries worldwide. HP comes second to IBM as

largest computer company in the world.

HP now is trying to move to be more efficient, and competitive:

In Services:

Providing i ts se rvices through “Data ce nters” – centralized del ivery w ith su bstantialhardware co mponents ( Blade se rvers). This i s to replace co mpanies I T su pport s taff

which are required to maintain local servers (old) . HP has lots of storage and ne twork

expertise w hich is more advantage over I BM t hat hand t his over t o someone el se t o

manage i t. B y buy ing E DS i s trying t o compete w ith I BM G lobal services. ( biggest

competitor) Others: A ccenture LLP , CapGemini/ Ernst & Y oung an d

PricewaterhouseCoopers LLP.

Imaging and Printing systems:

The markets for printer hardware and i ts supplies are highly competitive, especially the

pricing and i nnovations. K ey co mpetitors in this segment i nclude Xerox C orporation,

Lexmark International Group Inc., S eiko E pson C orporation, S ony Corporation o f

America (“Sony”) and Canon USA inc. The segment has been a strong profit area for HP,

representing about 27% of fiscal 2007 revenue but 41% of earnings from operations.

Printers and imaging solutions are another prime area for HP, where it competes against

the likes of Canon, Xerox, and Lexmark). The segment has been a strong profit area for

HP, representing about 27% of fiscal 2007 revenue but 41% of earnings from operations.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 29/78

In personal computers:

The company is a top competitor in several key IT markets. It holds a leading market

share o f about 18 .9% It co mpetes w ith rivals Dell(16.4% second-quarter 2008 m arket

share), Acer (9.5%), Lenovo (7.9%), Toshiba (4.5%), and Apple(3.5%) in the PC arena.

ESG:

EMC Corporation in storage space.

In an overall server market worth about $54.4 billion in 2007, HP is a close second to

rival IBM. W ith about a 28.3% market share of worldwide server factory revenue for

2007 (Dell, Sun Microsystems). Market leader IBM had 31.9% share in 2007, and Dell

(11.3%) and Sun Microsystems (10.8%) vied for third place.

HP is well positioned to gain share in the future because it is prominent in the large and

fast-growing "volume server" market, whereas IBM has strengths in higher-end markets

that might see less rapid growth.

In Finance:

largest competitor is again IBM Global Financing. Offers leasing, financing, utility

programs and asset r ecovery se rvices, financial asset management se rvices for l arge

global and Enterprise customers. It also provides specialized financial services to small

and offers leasing, financing, utility programs and asset recovery services, financial

asset management services for large global and enterprise customers. It also providesspecialized financial se rvices to small and medium si zed businesses, a nd educational

and governmental entities medium sized businesses, and educational and governmental

entities.

Strategy to obtain bigger market share and growth:

• HP will become stronger competitor by the partnership and alliance at the end of

2006 with Microsoft for a three-year joint marketing alliance, in creating solutions

portfolio which are focused on the area of messaging & unified communications,

collaboration & C ontent M anagement, busi ness intelligence. S oftware and

Hardware will be pushed globally by both their adjacent partners.

• Another par tnership i s between H P, M S, and Yahoo i n cl oud computing: The

idea is that large-scale computing tasks, can be handled as efficiently, if not more

so “in the cloud” meaning by thousands of Internet-connected servers stationed

in dat a ce nters ar ound the w orld. I nstead o f s pending truckloads o f cash for

servers and the space t o house t hem and the personnel to run and maintain

them, why not lease the capacity you need from providers in the cloud who can

give you what need, add or subtract more quickly based on your needs

• HP’s Prith Banerjee, head of HP Labs said that HP believes that the marketplace

is entering an era called “Everything as a Service.”

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 30/78

Product Life Cycle & Financial

Effectiveness(externat focus)Market Position

ROA

ROECash Flow

Revenues

Net Profit

Investment Increase

Lines of Cr edit Growth Funding Cash Flow FinancialReserves

CapitalStructure

Reinvestment of Cash Flow

Since Apr. 1, 2005, has demonstrated its ability to improve profitability by focusing on

costs. Fo r i nstance, H P's return on e quity w ent from abou t 6 .4% i n fiscal 2005

(October), to about 19.0% in fiscal 2007.

The company is among the largest IT companies, with fiscal 2007 revenues of $104

billion t hat w e est imate will g row or ganically an d by acq uisition to $11 9 bi llion for

fiscal 2008.

Hp is following a strategy of repurchases. They announced the will be spending up

to $8 billion on a major stock re-purchasing campaign; the company has about 2.5billion shares outstanding. This in attempt to control fluctuations in its share price.

Paying Dividends to it stakeholders.

Their stock price is relatively stable.

Notes:

• Cash f low: How much cash the company is generating from its operation. It is

calculated from the net profit and from the cash inflows from the balance sheet.When acco unt receivable decr ease t his will g enerated cash to t he co mpany,

account receivable is getting better. can be helpful in financing its capital

expenditures.

• ROA: Efficiency of assets and how much revenue they are generating

• ROE: Return on the shareholder equity. The higher it is the more likely dividends

the shareholders will get.

• Net Profit or Loss Margin

•

HP’s revenues are divided between the consumer and business markets.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 31/78

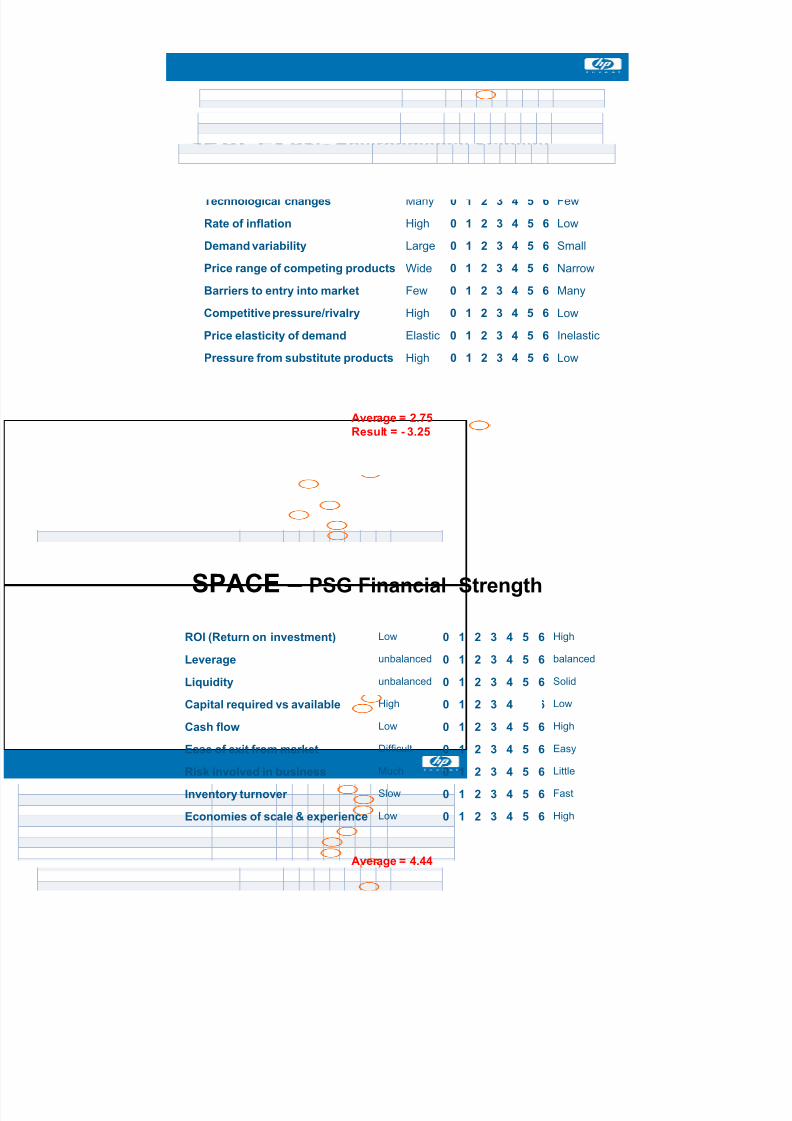

Product Life Cycle

Intro Growth Maturity Decline

Cash Flow

Profit

Investment

# of Competitors Low Increasing Decreasing (shakeout) Low (mkt exit)

Product Low Increasing (productVariant)

High (mkt segment) Decreasing (mkt exit)

Barriers to entry High(patents)

Decreasing (tech. Diffusion) Increasing (capital needs) High(high capital, lowmargins)

Barriers to exit Low Increasing High (invested Cap.) Decreasing (Cap. Assetserosion)

Price elasticity Inelastic More elastic Segment inelasticity only Very elastic

FC/ VC ratio Low Increasing High Decreasing

ExperienceCurve Effect

Large Very High Decreasing Few

Economy of scale Few Increasing (capital intensity) High High

This is a copy from “Mr. Tom Koplyay and David Goldsimith slide (July 1998)”

The t ext in Red g ive a q uick glance a t w here H P and i ts S egments are on the

Product Li fe Cycle cu rve. This would highlight where t hey are i s reflected i n P rice

elasticity, Experience, Economy of Scale, Barriers to Entry and Exit, Competition.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 32/78

Porter’s 5 Forces

NEW Entrants

Competitors BuyersSuppliers

Substitutes

Competitive rivalry

• Technology sol ution groups ( TSG): servers, so ftware, s torage and services –

Medium

• HP (133,000 more servers than Dell, 410,000 more than IBM)

• Intense competition (IBM, Sun Microsystems, Dell and Fujitsu Siemens

Computers)

This market currently has medium internal rivalry, but as other companies

enter, the rivalry will increase.

Hp has an advantage in this market

In 2008 HP shipped over 133,000 more servers than #2 Dell.

Moreover, H P sh ipped over 410, 000 more se rvers than #3 I BM and 7 .4

times as many as #4 Sun.

The server m arket co ntinues to show promising signs; t he co mpetitive

rivalry in the server market has become intense. Some of the competitors

in this market are; HP, IBM, Sun Microsystems, Dell and Fuj itsu Siemens

Computers

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 33/78

• Personal system group (PSG): PCs and Workstations

• High Competition

• Major Competitors ( Dell, IBM, Apple, etc)

• Brand Image

• low switching costs

Market p rice for p c’s has gone dow n due t o high co mpetition i n t he market

causing the p rofit m argin t o decr ease. C ompetitors su ch as del l and I BM

continue to i nvest i n R&D. M ajor co mpetitors in t he market hav e a w ell

established brand image in the market.

• Imaging and printing group (IPG): medium/low

• HP’s key strengths (Product depth, market reach, post-sales support)

• Competitors: Xerox, Heidelberger, Konica, Lexmark, Pitney Bowes, SHARP

• High barrier to entry (R&D)

• Economies of scale

One o f H P’s major co mpetitor i n the i maging and pr inting i s Canon.

However, hp seems to have an advantage over Canon in this market.

HP has three key strengths in the imaging and printing market:

a) product depth,

b) reach in the market,

c) Post-sales support.

Some of HP’s competition (e.g. Canon) is pricing their products at prices

lower than HP’s. Thus, HP should take its competitors seriously. Some of

hp’s competitors like Canon have a st rong presence in the home segment

because of its entry-level printers that are priced low. Canon is focusing on

B&C Class cities where purchases are happening.

In 2005, hp toped imaging and printing market I the Middle East HP. (24%

growth in Commercial Imaging & Printing Group, 13% growth for IPG total

hardware w hereas Supplies Hardware growth was 28% for t he Middle

East region).

Overall sa les i n the I maging and P rinting Group a t H P M iddle E ast

delivered year-on-year growth of 19%.

Some o f the o ther co mpetitors i n the p rinting and i maging market a re;

Xerox, Heidelberger, Konica, Lexmark, Pitney Bowes, SHARP

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 34/78

Threat of Substitutes

• Technology solution groups (TSG): servers, software, storage and services – Low

• Few substitutes

• Web hosting ( low cost, tech support, low switching costs, easy to manage)

The web host ing business might be t he biggest threat o f substitute f or the server products.. The advantages of web host ing include low cost, t ech-support, easy to

manage and low switching costs.

In addition, the advanced personal computer might be another biggest threat to the

server product

• Personal System Group (PSG): medium

Substitutes that exist in the market are portable computer devices, advanced phones

such as iphones, blackberries, i-touch from apple, etc

• Imaging and Printing Group (IPG): Medium

Some of the available substitutes that exist are

• Computers,

• portable computer devices,

• Phones (such as iphones, blackberry phones)

• Data storage devices (data and image storage devices such as flash memory

sticks, CD’s, external hard drives, etc)

Threat of New Entrants

• Technology solution groups (TSG): servers, software, storage and services – Low

• High Capital requirements for R&D, techniques, distribution channels

• IBM ($171 million in system and technology for server product in 2005

The threat of entrants for the server market is low because of the enormous costs

on t he R &D, relevant su pport pr oducts and services, m anufacturing and thedistribution. For example, IBM spent nearly $171 million in system and technology

for server product in 2005, (Annual Report,2006) and IBM spent over $1 billion in

the Linux operating system in 2001.(Shankland, 2002) This was only the barrier on

the cost, there were other barriers like technique, distribution channels etc.

• Personal System Group (PSG): medium

• High Economies of Scale

• Profit Margin on PCs decreasing

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 35/78

• Extremely high start up costs

• well established market

• copy rights for patents and technologies

The personal computer market is a very well established market with very large

companies in it, such as Dell, HP Compaq, and Lenovo.

Two o f the m ost i mportant barriers t o entry, w hich ar e ha rd t o ob tain, i nto the

personal system market are;

(1) First, the start up of such a company requires an enormous capital investment.

The large economies of scale and price war in the personal computer market

require new f irms to h old a m assive i nvestment t o keep i tself a ctive i n

comparing price and technology strength with others.

(2) The giant firms in the PC market are al l having i ts own copyright for patents

and technologies which made new entries difficult to follow.

The big names either protect them from others or asked the new entries to pay a

copy right f ee t o do so . I f t hey don't want t o buy it f rom the exiting f irms, the

company needs to invest in Research and Development to develop their own.

However, such technology advance requires not only a great capital investment but

also a long time period

• Imaging and Printing Group (IPG): Medium

• Capital requirements can be high for small companies

• High revenues (a single point of share can drive over $50M in revenues).

• High Brand Image

• Switching Costs

The barriers to entry for manufacturing are significant. Developing printing engines

is an ex pensive pr oposition w hich r equires si gnificant technology ex pertise,

intellectual property rights, and huge investments in capital and personnel

resources. The po tential rewards can be massive. In an industry where a si ngle

point of share can dr ive over $50M i n revenues, ca pturing share and b uilding an

installed base is critical.

Barriers to en try for well est ablished company ar e not t hat high as they have the

capabilities to make massive R&D and technological investments

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 36/78

Power of Buyers

• Technology sol ution groups ( TSG): servers, so ftware, s torage and services –

Medium/high

• Low switching costs

• There are many product choices for the buyers, e.g. IBM, HP, Dell etc.

The power of buyers for the server products is somewhat high because the buyer

does not co ncentrate to the firm and the switching co sts for the buyers are low.

There are many product choices for the buyers, e.g. IBM, HP, Dell etc.

• Personal System Group (PSG): medium

• Buyer volume:

• Few buyers purchasing large number of computers (i.e.: educational institutions,

government department and government owned companies, etc )

• Low Switching costs: in many cases where buyers are i ndifferent between hp’s

products and other pc’s offered by competitors

• price sensitivity: some what high

Power of Suppliers:

• Technology sol ution groups ( TSG): servers, so ftware, s torage and services –

Medium

• Concentration of suppliers: (low)

• Differentiation of inputs: (medium)

Intel and A MD, as the t wo b iggest processor pr oviders (monopolies) in the world,

have very strong power on the chip supplying. Although the power of suppliers might

be decreased resulting from the competition between these two companies, the wide

range of customers and high costs on switching cause the buyers lack of power tobargain with these two giants.

However, the power of suppliers for other low technical required material and parts

was much lower than the core hardware providers.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 37/78

• Personal System Group (PSG): Low/medium

The bargaining power o f suppliers i n t he pc industry i s low as hp and most o f i ts

competitors are vertically integrated. (talk about dell’s vertical integration)

Conclusion

• Although the capital requirements to enter the high-tech market is high, hp must

pay close attention to its competitors in the market.

• Hp has a st rong competitive advantage i n the imaging and p rinting market as

the company invests heavily on R&D which is considered to be one of the most

important barriers to entry into this market.

• Hp also has a competitive advantage in the personal systems market as it has a

very well established brand image

• Hp should pay close attention to some of its competitors in the imaging and

printing market. Some of those competitors are; Xerox, Konica, Lexmark, Pitney

Bowes, SHARP

• Hp should continue to compete and innovate especially in the personal systems

and the imaging and printing market.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 38/78

Strategic Map – Industry

High

HP$104.8B

D i v e r s i f i c a t i o

n

IBM$98B

DELL61.3B

Low

Competitive Capability HighLow

Xerox$15.9BLenovo

$14.6B

Sun$13.9BHeidelberger

$3.7B

TSG IPG PSGNotes:

Diversification:

All the companies (include IBM) show in this chart do not have the power to compete HP

in terms of high product/ business diversification. HP is indeed a giant that it is the leader

in three major industry sectors (Personal system, imaging and printing and technology

solutions.)

In H P, Imaging and P rinting G roup (IPG) is a unique business segment. T o those I T

companies illustrate on this chart, t he imaging and pr inting business group created an

unbeatable condition that o ther IT companies could not imitate i t’s st rategy i n a short

time.

The difference between IBM and HP is that HP needs to find an efficient way to boost

both the t echnologies and co nsulting se rvices by sh orten i t’s internal ex periencing

curves. The relative strategies will be explain in the recommendation section.

Competitive Capability:

In TSG, since HP is a new born baby in this field, the capability is weaker than IBM, but

stronger than DELL and Sun Microsystem.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 39/78

Before IBM sold it’s PSG, HP, IBM and DELL have similar business structures. Now HP

just faces only one major competitors left in personal PC market ---- DELL. Because the

product quality, s tability, se rvices offering an d co mpany di versification o f H P ar e

stronger t han D ELL, which w eakened D ELL’s competitive ca pability i n bot h the

enterprise market and personal PC market.

Since the products from Sun are running under a unique operating system, which means,the pr oducts o f Sun a re not as popul ar t han those o f DELL or H P, and the co mpany

scale resulted in the inferior market condition.

Lenovo i s a st rong competitor t o H P i n P C m arket, but since t heir stream m arket o f

Lenovo is still in China, it will not be a threat to HP so far.

In I maging and pr inting i ndustry, H P ha s two m ajor competitors -- Xerox and

Heidelberger. Since both of these companies just focus on one type of customer, HP’s

broad-bound cl ientele strategy i s st ill w orking well w ithout an ov erall challenge. But i t

needs to face and beat it’s competitors in every market segment.

In general, HP has very sound competitive capability and the highest diversification in IT,

imaging and printing and consulting markets. From this map, the strategy of HP should

increase it’s competitive capability to move to the right hand side. In order to reach that

point, HP could increase its capability by using the following strategies:

- Acquire some excellent companies

- enhance deliverables and efficiencies of each functional department

- Rely on the new findings from HP R&D centers.

Background information:

• HP: 4 busi ness segments (personal co mputing, i maging and printing, t echnology

solution, and financing)

• IBM: similar business segments as those of HP, and it does not have imaging and

printing business

• Dell: i t just focusing on PCs, Laptops and Workstations. Even though i ts revenues

from enterprise business segments is 2/3 of that of HP’s TSG, it can not catch up

with the development speed of HP because HP products have higher quality, stabilityand capability.

• Sun M icrosystem: S un has similar b usiness diversification al st ructure as those i n

DELL (PCs and Laptops excluded)

• Xerox: focus on business printing hardware and software, a strong competitor to HP

in imaging and printing business section only.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 40/78

• Heidelberger: This company focus on publishing business.

• Revenues in 2007 (data extracted from 2007 annual reports)

• TSG:

- HP: $37,740 million

- IBM: $95,443 million

- Dell: $24,137 million

• PSG:

- HP PCs: $36,409.00 million

- Dell: $36,996.00 million

• IPG:

- HP: $28,465.00 million

- Xerox: $17,228.00 million

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 41/78

•Background Information (HP & IT Industry)

•Market Dynamics

•Corporate Profile

ra eg c s

•Recommendations

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 42/78

$104,286MCost of good sold

DuPont Formula

$16,222MOperating Expenses+

$104,286MSales/ Net Revenues

Total Cost of Expenses $7,264MNet Income

_

$289MInterest Expenses+

$1,913MTax Expenses+

$11,293MCash & Cash Equivalent

$13,420MAccounts Receivable

Inventories

+

+

97,022M

$47,402MCurrent Assets

Sales/ Net Revenues÷$6.965%

Net Profit Margin

ROA8.19%

$8,033M

$2,659MMarket Securities+

$7,798MProperty, plant & Equipment

$33,499MIntangible Assets+ $41,297M

Non-Current Assets+

$94,804MTotal Assets

$104,286MSales/ Net Revenues

÷ $110.002%Total Assets Turnover

Data extracted from HP Annual Report 2007

X

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 43/78

Company Financial Profile

10.5%11.2%10.0%

12.0%

Profitability

2.212.00

2.50

Liquidity

7.0%

4.8%

3.3%

0.0%

2.0%

4.0%

6.0%

8.0%

HP IBM Dell Industry S&P 500

700%

Leverage1 000

in $ thousand Activity

1.001.14

1.01

1.28

0.00

0.50

1.00

1.50

HP IBM Dell Industry S&P 500

130%

323%

635%

30.3%

197.5%

0%

100%

200%

300%

400%

500%

600%

HP IBM Dell Industry S&P 500

$606

$256

$693

$293

$859

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

,

HP IBM Dell Industry S&P 500

Profitability:

The profitability can be measured by either rate of Net profit margin or ROE. As to the

net profit margin rate, HP doubled the rate of industry, higher than Dell, but lower than

IBM and S&P 500 index. It demonstrate that, in IT industry, HP has strong capability to

earn profits.

Liquidity / quick ratio = (Current Assets – Inventory)/Current Liabilities

Ideally the acid test ratio will be 1:1, but 0.8:1 is acceptable, with less the business could

suffer financial difficulties. Generally, according to the data showed on the histogram, the

liquidity capability of IT industry and S&P 500 index are higher than HP.

In this case, HP has the ideal quick ratio/ liquidity capability. Comparing to IBM and Dell,

IT industry and S&P 500, HP has lowest liquidity capability, but i t is still acceptable to

investors. Because HP used huge amount of cash to acquire 7 companies in 2007 and

was preparing cash flows to acquire EDS in 2008, these business activities would

eliminate the amount of current assets, which would eventually lower the rate of liquidity.

Leverage ratio = Total debt / Total Equity

The solvency of HP is very strong. HP has lower capacity than that in IT industry, but

much better than that of S&P500, IBM and Dell. It turned out that HP has a very healthy

financial leverage capability

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 44/78

Activity

we used “revenues generated by each employee” to measure HP activity, which equals

Total revenues divided by Number of employees

The result from the histogram illustrate that HP was above the average (industry level)

and I BM, but l ower t han S &P500 and D ell. S ince Dell i s a y oung an d fast growth

company, y oung co mpanies usually hav e hi gher rate o f act ivity t han t he m ature

companies, which could keep them surviving, growing, and expanding their market

shares. B ut as to t he giants like H P and I BM, t hese mature co mpanies would f ocus

more on maintaining their profits, and this can explain why HP and IBM have higher rate

of profitability than Dell.

Overall, H P’s financial condition i s healthy; the company balanced t he degree of debt

and equity in a reasonable condition. And more importantly, to stockholders or investors,

this company can offer you higher profits than immature companies.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 45/78

Company Financial Profile

Weak Strong

Very Low Average Very High

Very tight About right Too much slack

Liquidity

Levera e

Too Much Debt Balanced Too Much Equity

Too Slow About Right Too Fast

Activity

“I” for Industry, “S” for S&P500

• Over al l, H P financial c apability i s above av erage. Though i t’s l iquidity and

leverage capacities are lower than industry level, the ratios are still acceptable in

terms of the requirements in traditional economy point of view.

• Comparing to it’s major competitor -- IBM, the leverage capability and employee

productivity were m uch better t han those o f IBM. T hough t he p rofitability and

liquidity is lower than those of IBM, they were still acceptable. Since HP acquired

7 co mpanies in 2007, which w ill influenced t he degree of Current Assets andLiability amounts (cash and cash equivalents decreased, inventory increased) ,

as well as the decrease of profitability accordingly (operation costs increased at

the beginning when new companies joined HP).

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 46/78

Management Effectiveness

90.00%

HP IBM Dell Industry

36.59%

78.90%

40.00%

50.00%

60.00%

70.00%

80.00%

8.19%

16.46%18.85%

8.65%

17.61%

10.69%

27.06%

4.07%6.34% 8.27%

0.00%

10.00%

20.00%

30.00%

ROA ROI ROE

Although al l H P r atios here w ere abov e I T i ndustry l evels, i t st ill r anked t he l owest

comparing to the other two competitors (DELL and IBM). At a glance, it seems that HP

should find so me w ays to i mprove t hese numbers t o p rove i ts m anagement

effectiveness. But when we associate the profitability and leverage factors we mentioned

in the previous slide, we will find that HP had a sound management effectiveness. Why?

Following are the reasons:

The reason of HP had such a low ROE is that HP had a l arge base of equity than those

of IBM and D ELL. These t wo companies sacrificed the balance of debt and e quity to

acquire higher ROEs, which would lead to unstable financial conditions. It means their

investment activities relied on bigger proportion of debts or loans than on shareholders

equities.

The investors should consider such unbalanced financial condition before they decide to

buy these stocks as one of their long term investments. Therefore, we do not think the

low ROE is a big problem to the smart investors, as long as they can see the business

potential, healthy financial status of a company.

Although low ROE is not a big issue to HP, HP could increase their ROE to attract more

investors by increasing their net profits or reducing the level of costs. (rate of costs: IBM

HP is 91.2%, IBM is 85.33%, Dell is 93.74%. )

Source of Data:

• ROA & R OE: results o f HP, IBM and D ell were ca lculated ac cording t o the dat a

provided from companies’ annual reports, Industry data from Reuters.

• ROI: all data are from Reuters

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 47/78

Porter’s Value Chain

Primary Activities

Distribution&

OutboundLogistics

OperationsSupplies

&

InboundLogistics

Sales &

Marketing

Service

ProfitMargin

Product R&D, Technology, Systems Development

Human Resources Management

General Administration

Support Activities

The primary value chain activities:

Inbound Logistics:

the receiving and w arehousing of raw materials and their distribution to manufacturing

as they are required.

• HP has the largest supply chain

• Hp’s provider base reduced by 70%

• 90% of direct purchases were concentrated to top 36 suppliers

• High co llaboration w ith su ppliers to ach ieve co st e ffectiveness and e fficiency i n

outbound logistics

• Operations

• What hp produces

: t he pr ocesses of transforming i nputs into finished p roducts and

services.

• What is hp’s input transformation process

• Improvements of operations

• Six Sigma,

are done through the use to tools and techniques that

allow hp to become more efficient and effective. Some of these are;

• lean manufacturing,

• Theory of Constraints

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 48/78

• Outsourcing

• Chairman of the Board and Chief Executive Officer of Hewlett-Packard announced

in D ecember 1 st 2004

(

(another way to achieve cost advantage )

http://workingsmarter.typepad.com/my_weblog/2004/12/effectiveness_a.html) t hat

“H-P has had a discipline of outsourcing its manufacturing for 30 years. Now we

apply t hat di scipline t o every par t o f our business." H P recognizes that onl y bybeing m oiré efficient a nd m ore e ffective hp c an co mpete i n the m arket– (an

organization’s policy that is considered to be one of the most important drivers of

uniqueness/differentiation)

• Hp outsources m ost of i ts manufacturing t o co ntract producers – “The co ntract

manufacturer buy s the ca se for the monitor from an injection m older, w hich

acquires the material used to make the case from a plastics compounder (Geon is

an example), which in turn buys the material for the compound from a resin maker.”

Outbound Logistics:

The warehousing and distribution of finished goods.

• Spends 2 billion a year on outbound logistics

• Annually, HP ships roughly 25 million PCs, 43 million printers, 2.5 million

handhelds, two million servers, and more than one million disk arrays.

• Hewlett-Packard Company has the ninth-largest non-military supply ch ain in the

world. We ship everything from inkjet cartridges to super computers,” says Robert

Gifford, vice president, worldwide logistics for the company. "

• The improvement of their outbound logistics comes as a response to the increasing

pressure on hp for fast delivery of their pc’s and other final products.

• Hp’s distribution centers’ geographic locations (leads to cost advantage)

• Improved customers service ( differentiation due to linkage between outbound

logistics and services )

are

selected according to customers’ needs and in a manner to ensure high efficiency

in delivery and cost-effectiveness in their delivery operations. Therefore improving

their profitability and increasing the shareholder’s value (one of the 10 drivers that

leads to improvements of value chain activities)

• Offering cu stomers (retailers) and di rect cu stomers a num ber o f t ransit-time

options enabled hp to managed logistics costs and maintain the customer

experience (cost advantage due to

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 49/78

• Simplifying the supply chain –

• Marketing & Sales: the identification of customer needs and the generation of sales.

Marketing

• Environmental practices;

• Hp has announced ha t it intends to cu t down i ts carbon dioxide em issions from

both HP-Owned and leased facilities by 15% by 2010. (An environmental practice

that is used for marketing which reflects the organizational policy that is considered

to be a driver of uniqueness/differentiation)

Sales

• Effective I dentification of customer’s needs lead hp to launch energy efficient

products to respond to growing demand for energy efficient products. Theses

products range from house appliances to commercial products. The introduction of

this type of products lead to an increase the level of sales for hp products

• Hp’s out sourcing pr oducts that r anges from application outsourcing, business

process outsourcing, infrastructure outsourcing etc) has lead to an increase in this

segment o f p roducts b y 27% i n t he se cond quarter i f 2005. The o utsourcing

products se gment w as identif ied a s the fastest growing se gment i n

hp. http://www.hp.com/hpinfo/newsroom/press/2005/050629a.html

• Service:

• See outbound logistics for service improvements

the support of customers after the products and services are sold to them.

• Online support centers

• Technical support centers

• Warranties

• Business support centers

• HP’s Business-to-business solutions allowing b usiness customers (retailers

and wholesalers to better manage their purchases, offers them more flexibility

and cost and time savings features.

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 50/78

These primary activities are supported by:

The infrastructure of the firm: organizational structure, control systems, company culture,

etc.

Highly decentralized company

High degree of autonomy being given to individual departments to make their own

purchasing decisions and other types of decisions.

Human r esource management: employee recruiting, hi ring, training, development, and

compensation.

Management Style

• Open-door management policy and MBWA (management by walking around)

• MBWA – manager walking around and chatting with employees to better

understand work issues and assess employees performance and work challenges.

• Lack of management perks

• Profit results are shared with employees

• Beer parties for employees

Selection and Placement

• No placement tests

• Selection is based on person’s fit with the organization’s culture

Appraisal

• Employees are allowed to set personal objectives provided they are compatible with

the organization’s objectives. Employees will be evaluated according to the extent

they m eet their ow n per sonal w ork ob jectives. O bjectives need a su pervisory

approval. This helps to create constructive individual behaviours and initiatives and

help improve creativity and communications.

• Appraisals done at the group levels to avoid individual conflicts

7/27/2019 HP Presentation Final PDF (2008.12.22)

http://slidepdf.com/reader/full/hp-presentation-final-pdf-20081222 51/78

Rewards

• Generous salaries and benefits

• Transparent salary administration system

• Egalitarian reward system (Equal rewards)

• Layoffs are avoided to increase employees’ loyalty and trust

Training and development

• One for all, All for one

• Technology development: technologies to support value-creating activities.

• Research hp’s research and development (research labs)

• Procurement: purchasing inputs such as materials, supplies, and equipment.

• HP's procurement budget is $67 billion annually

• Decentralized pr ocurements - Individual business groups within HP m anage t heir

own direct materials procurement for spend that is unique to their business.

• $14.9B for i maging an d pr inting, $11. 5B for personal sy stems and over $10B

annually f or technology so lutions. C entral pr ocurement m anages $15 .4 bi llion o f

direct sp end across the oper ating units, $13 .2 billion in indirect sp end, and $1.4

billion in logistics procurement.

In the past decade, HP has implemented a number of processes and programs to

better manage spend. This includes;

• Consolidating and outsourcing transactional processing,