hugo bossgroup.hugoboss.com/files/0113_investor_meeting_presentation_2.pdf · integration of boss...

TRANSCRIPT

HUGO BOSS Investor Meeting Presentation January 2013

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 2 / 67

Agenda

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 3 / 67

American strategy update

Financial strategy update

Group medium-term strategy

Summary

Agenda

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 4 / 67

American strategy update

Financial strategy update

Group medium-term strategy

Summary

Continued strong top and bottom line momentum

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013

750

469350

267272275

+19%

2015e

3,000

… 2011

2,059

2010

1,729

2009

+34%

1,562

2008

1,686

2007

1,632

EBITDA before special items

Sales Sales and EBITDA before special items (in EUR million)

5 / 67

Successful execution of medium-term strategy

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 6 / 67

STRIVING FOR

OPERATIONAL

EXCELLENCE

STRENGTHENING

OUR

BRANDS

EXPLOITING

GLOBAL

GROWTH

OPPORTUNITIES

MAXIMIZING

CONSUMER FOCUS

TO DRIVE RETAIL

Strong portfolio of complementary brands

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 7 / 67

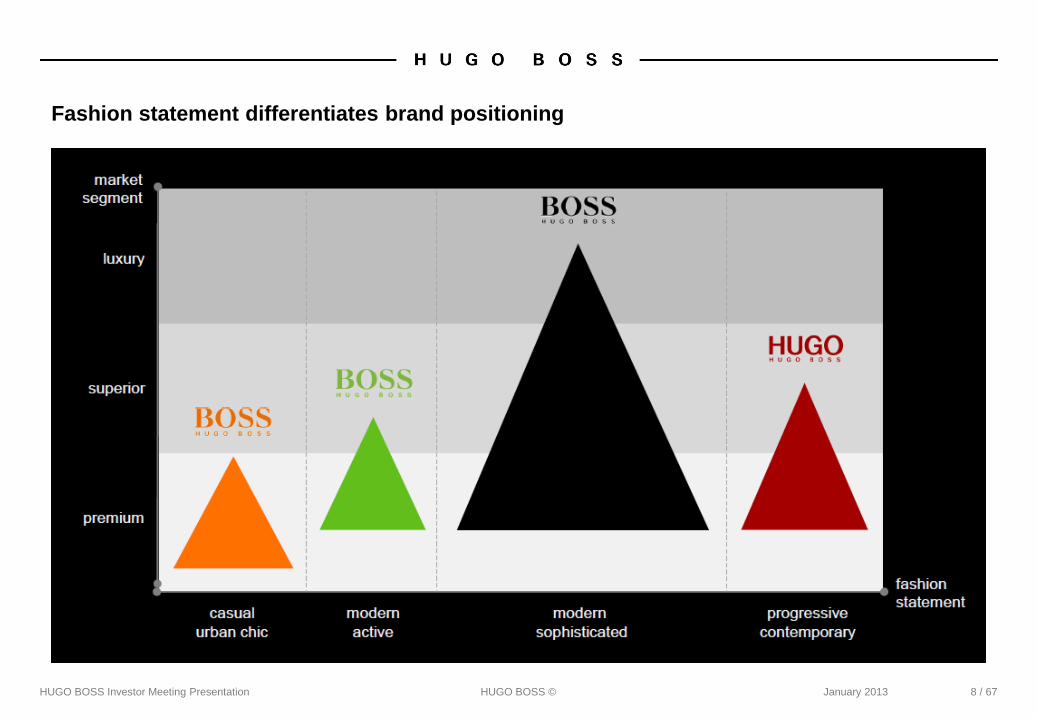

Fashion statement differentiates brand positioning

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 8 / 67

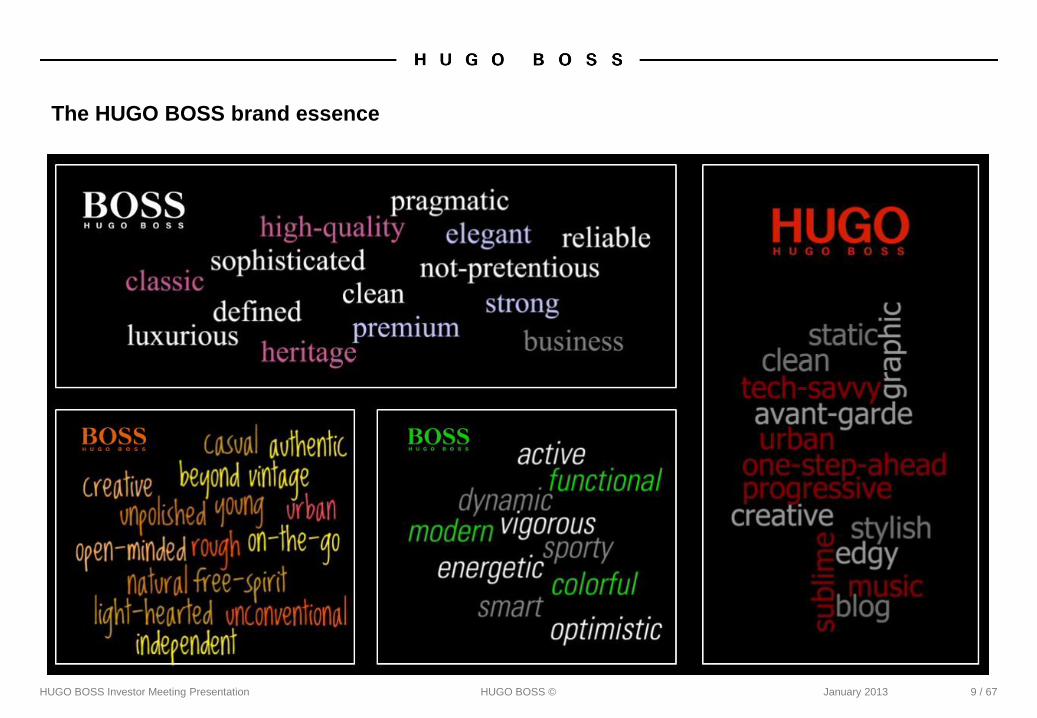

The HUGO BOSS brand essence

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 9 / 67

The HUGO BOSS brand essence (cont.)

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 10 / 67

Integration of BOSS Black and BOSS Selection elevates the core brand

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 11 / 67

■ Strengthens the core brand’s market position in luxury

clothing and sportswear

■ Leverages BOSS growth potential across different

fashion segments from premium to luxury

■ Maximizes the power and global recognition of the

BOSS logo

■ Simplifies communication and retail presentation

Made to Measure demonstrates unrivalled tailoring competence

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 12 / 67

■ Modern technology and uncompromising

quality “handmade in Germany”

■ Combines excellent craftsmanship,

premium materials and tailor made

service with efficient industrial

manufacturing

■ Permanently offered in several European

flagship stores

■ Rollout in Asia and U.S. under way

HUGO brand the Group’s fashion spearhead

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 13 / 67

■ Strong positioning as home of

avant-garde design

■ Focus on clean, minimalistic looks

addressing the fashion-forward consumer

■ Targeted expansion of stand-alone

retail presence

■ Significant growth potential in

underpenetrated markets

Strength in sportswear key competitive advantage

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 14 / 67

Sportswear elegance

Contemporary urban

sportswear

Active sportswear

Collection Occasion to wear

Casual Friday

Luxury Weekend

Daywear

Downtime

Party

Sporty lifestyle

Performance

All brands ready to exploit potential of global sportswear market

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 15 / 67

■ Offer the best price-value relationship in the premium segment

■ Enhance clarity of product branding

■ Firmly establish BOSS Orange as key premium lifestyle brand at wholesale

■ Convince in leading edge technical innovation

■ Strengthen distribution in golf performance accounts

■ Maximize commercial potential of golf pro cooperations

■ Strengthen product offering in luxury segment

■ Sharpen DNA of ‘Sportswear Elegance’

■ Increase focus on the Asian consumer

Clear womenswear strategy in place

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 16 / 67

■ Offer excellent and reliable fit with favorable

price-value ratio

■ Grow modern clothing business based on

tailoring expertise

■ Maximize brand potential in leisurewear

■ Grow shoes & accessories supplementing

core apparel offering

■ Introduce party capsules and evening

collection

Product

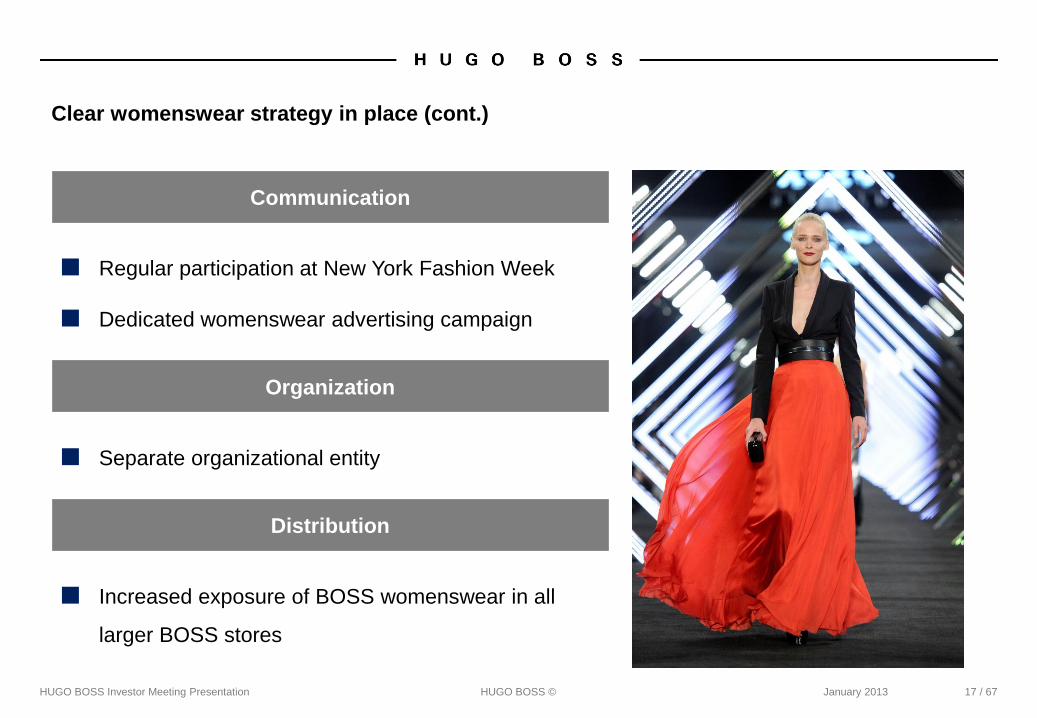

Clear womenswear strategy in place (cont.)

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 17 / 67

Communication

■ Regular participation at New York Fashion Week

■ Dedicated womenswear advertising campaign

Organization

■ Separate organizational entity

Distribution

■ Increased exposure of BOSS womenswear in all

larger BOSS stores

Unprecedented fashion show presence in 2013

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 18 / 67

Shanghai, May New York, September

HUGO showcases collections in Berlin

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 19 / 67

Berlin, January & July

Share of retail sales set to grow further

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 20 / 67

Wholesale

Retail

Royalties

Sales by distribution channel

2005

3%

75%

22%

2010

3%

57%

40%

2011

2%

53%

45%

2015e

2%

43%

55%

…

Introduction of four season cycle has made HUGO BOSS a true retailer

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 21 / 67

December January February March April

June July August September October

Spring 2012 Summer 2012

Fall 2012

Winter 2012

Introduction of four season cycle has made HUGO BOSS a true retailer (cont.)

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 22 / 67

Winter

12% 8%

Fall

40%

46%

Summer

11% 7%

Spring

37% 39%

2012

2011

Seasonal split of wholesale pre-order business

■ Fresher merchandise offering

■ Better adjustment to seasonal differences in

consumer demand

■ Immediate relevance at the point-of-sale

■ Working capital advantages

Development of collection complexity

-7%

2012e 2011

Faster and leaner development process enables market feedback loop

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 23 / 67

Brand module architecture supports more flexible merchandise offering

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 24 / 67

“S” Module

“XL” Module

“M” Module

Core range has demonstrated superior performance

Share of core range

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 25 / 67

0

10

20

30

40

50

60

70

0

5

10

15

20

25

30

35

40

Fall 2012

70%

33%

Spring 2012

67%

28%

Fall 2011

45%

15%

Units sold per style (Fall 2012)

x 4.7

Core range Non core range

Core range style/color (s/c)

as % of total collection s/c

Value share of core range

Heat mapping technology newest in-store design innovation

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 26 / 67

Purpose Benefits

Enhances understanding of consumer behavior to drive operational performance

■ Generates traffic map

showing the actual

footpath of consumers

in the store over the

course of the day

■ Overlay with

transactional data

offers insights into

correlation between

traffic and sales per

product category

■ Optimizes product

and campaign

positioning

■ Supports optimization

of space utilization

and staff allocation

■ Assesses visual

merchandising

effectiveness

Window Window

Suit wall Shirt wall Bodywear

Shoes / A

ccess

Tie table

Belt Knitwear Outerwear

Knitw

ear

Entrance

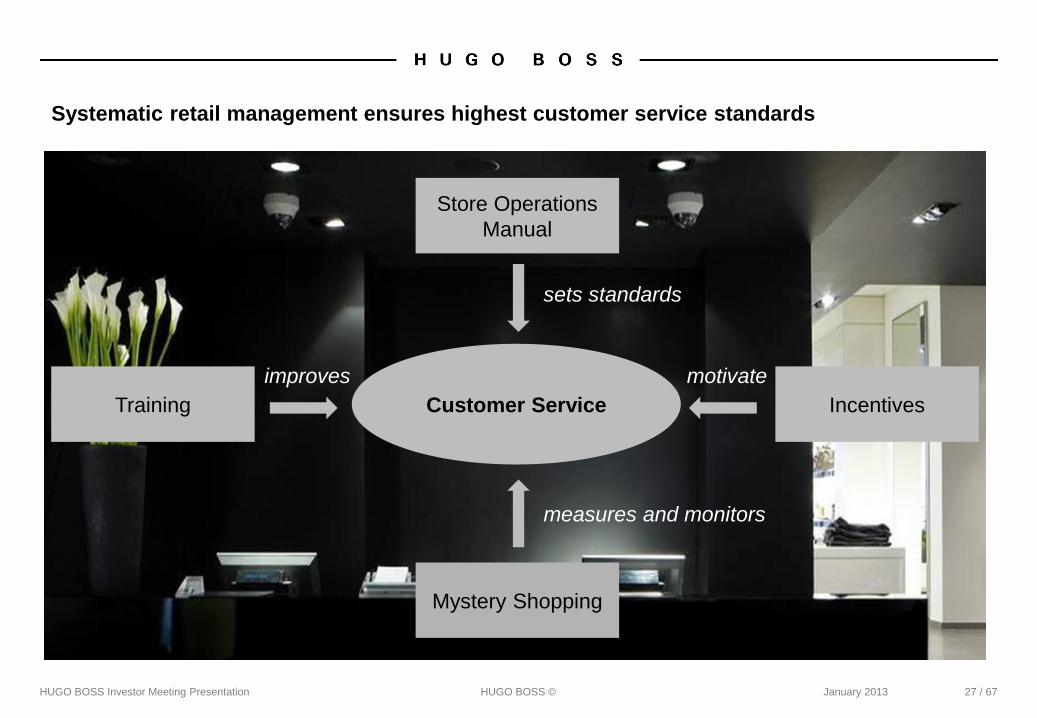

Systematic retail management ensures highest customer service standards

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 27 / 67

Customer Service Training

Mystery Shopping

Store Operations

Manual

Incentives

sets standards

measures and monitors

improves motivate

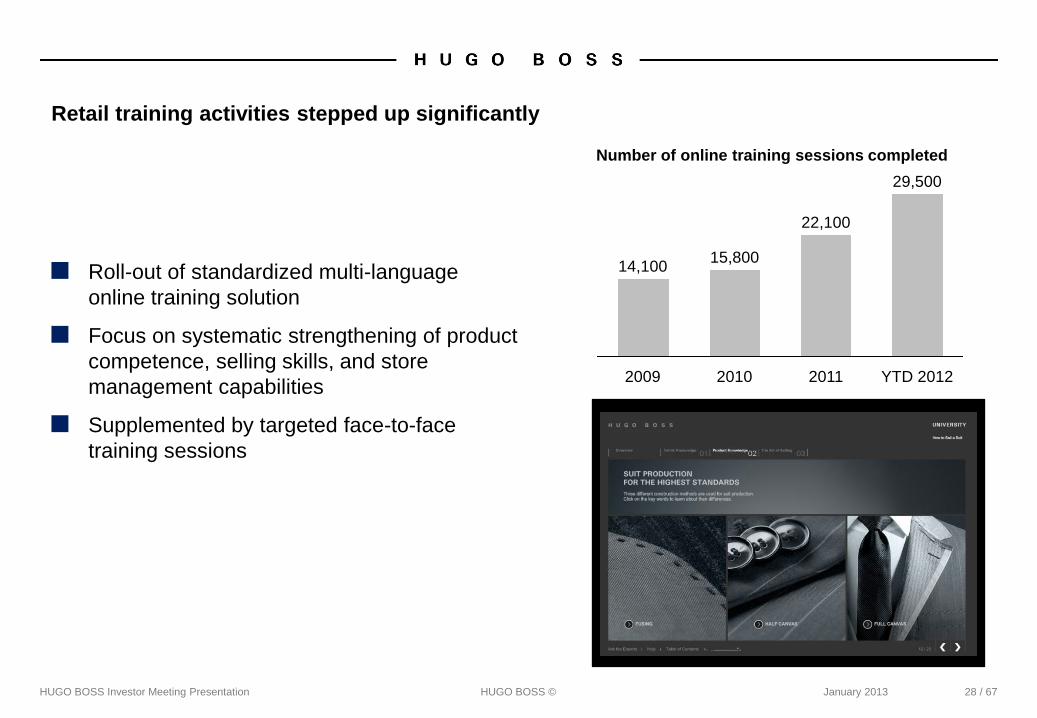

Retail training activities stepped up significantly

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 28 / 67

■ Roll-out of standardized multi-language

online training solution

■ Focus on systematic strengthening of product

competence, selling skills, and store

management capabilities

■ Supplemented by targeted face-to-face

training sessions

YTD 2012

29,500

2011

22,100

2010

15,800

2009

14,100

Number of online training sessions completed

CRM @ HUGO BOSS - Sharpen the end consumer focus

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 29 / 67

Understand our customers

Win new customers

Increase customer loyalty

Increase frequency of visits

Increase sales / turnover

Customer data

collection &

quality

Marketing

planning

Analysis &

segmentation

Worldwide HUGO BOSS CRM platform (IT)

HUGO BOSS CRM strategy and guidelines

CRM

activities

Cross-channel knowledge and targeted activities as key competitive advantages

IT and system upgrades improve retail performance management

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 30 / 67

■ Retail operations almost entirely on SAP

■ Implementation of global retail merchandise

planning solution under way

■ In-store systems provide basis for systematic

performance measurement

Enhanced logistics infrastructure caters to growing retail business

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 31 / 67

■ Flat-packed goods distribution center Europe

Filderstadt, Germany

New construction

Start of operation: 2014

■ Regional distribution centers Asia

Shanghai and Hong Kong

Relocation and consolidation

Operational since 2011

■ Distribution center Mexico

Mexico City, Mexico

New setup

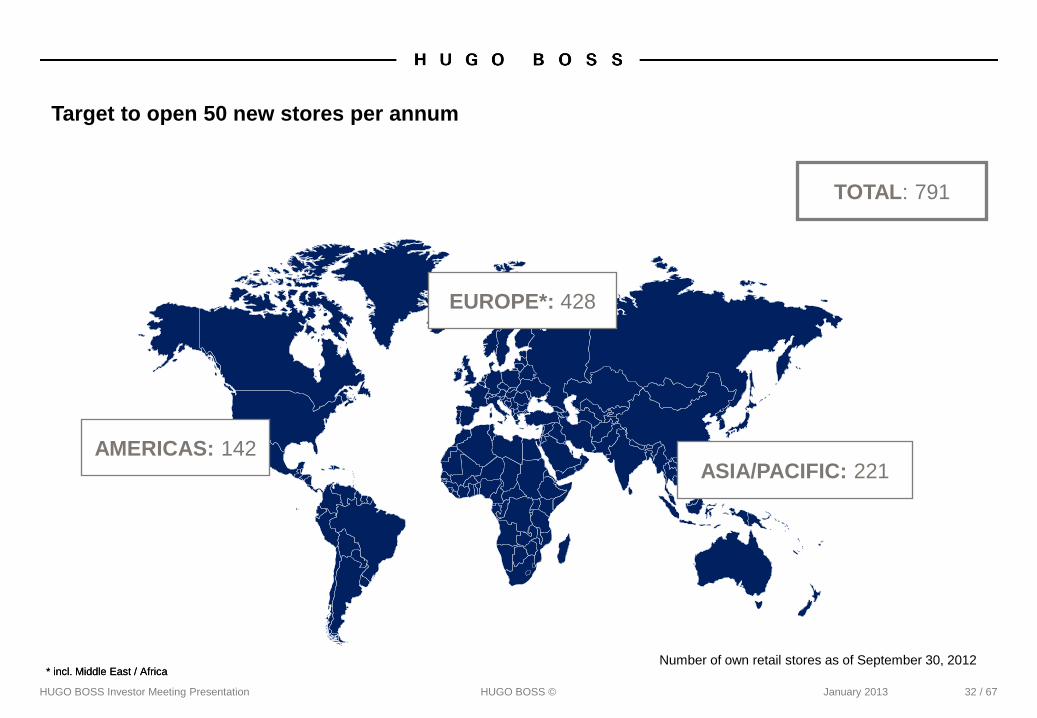

Target to open 50 new stores per annum

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 32 / 67

* incl. Middle East / Africa Number of own retail stores as of September 30, 2012

* incl. Middle East / Africa

TOTAL: 791

EUROPE*: 428

ASIA/PACIFIC: 221 AMERICAS: 142

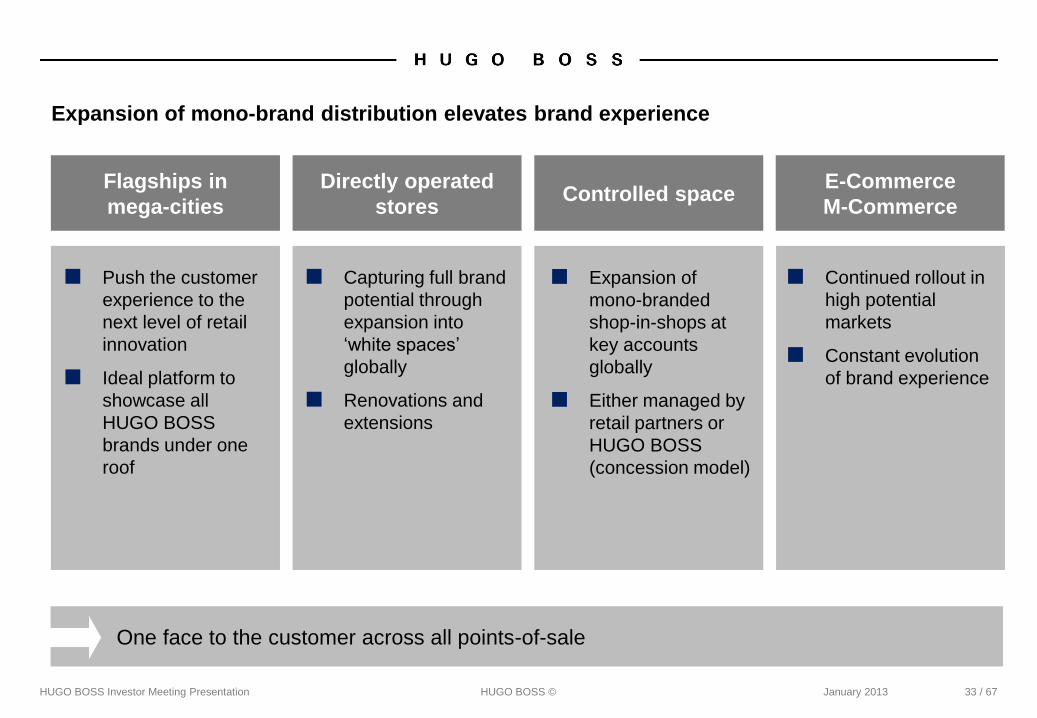

Expansion of mono-brand distribution elevates brand experience

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 33 / 67

Flagships in

mega-cities

Directly operated

stores Controlled space

E-Commerce

M-Commerce

One face to the customer across all points-of-sale

■ Push the customer

experience to the

next level of retail

innovation

■ Ideal platform to

showcase all

HUGO BOSS

brands under one

roof

■ Capturing full brand

potential through

expansion into

‘white spaces’

globally

■ Renovations and

extensions

■ Expansion of

mono-branded

shop-in-shops at

key accounts

globally

■ Either managed by

retail partners or

HUGO BOSS

(concession model)

■ Continued rollout in

high potential

markets

■ Constant evolution

of brand experience

High-visibility flagship store openings planned in 2013

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 34 / 67

BOSS Store Shanghai,

Kerry Center

BOSS Store Tokyo,

Omotesando

BOSS Store Shanghai,

APM International

BOSS Store Amsterdam,

Leidsestraat BOSS Store Berlin,

Kurfürstendamm

Wholesale remains an important distribution channel

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 35 / 67

■ 40+ year business relationships

■ Reliable sell-through performance

■ Grown retail competence

■ Industry-leading delivery and service levels

HUGO BOSS is best positioned for further growth…

…despite structural headwinds

■ Limited space expansion

■ Mono-brand nature of fast growing emerging markets

■ Ongoing consolidation

■ Franchise takeovers

+7%

2011 2010

Average net sales per wholesale POS

45% // Retail

53% // Wholesale

2% // Royalties

38% // Multibrand

15% // Franchise

Sales by distribution channel 2011

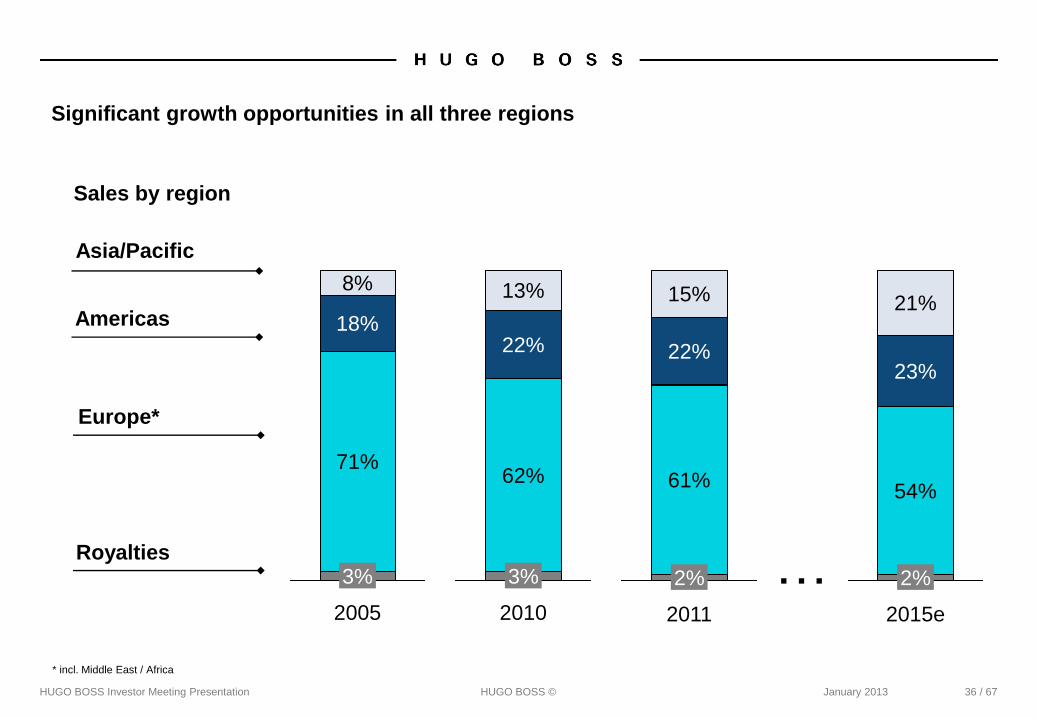

Significant growth opportunities in all three regions

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 36 / 67

Europe*

Royalties

Americas

Sales by region

2005

3%

71%

18%

8%

2010

3%

62%

22%

13%

2011

2%

61%

22%

15%

2015e

2%

54%

23%

21%

…

Asia/Pacific

* incl. Middle East / Africa

Agenda

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 37 / 67

American strategy update

Financial strategy update

Group medium-term strategy

Summary

Favorable brand perception across the region

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 38 / 67

■ Modern

■ Well-tailored

■ Easy to fit

■ Consistent

USA CANADA MEXICO BRAZIL

■ Seen as a premium

to entry luxury

■ High awareness of

individual brand

lines

■ BOSS Black and

HUGO are the

major brands

■ Prestigious

■ Good price-value

■ Easy to fit

■ Consistent

■ Luxurious

■ Classic

■ Elegant

■ Quality

■ Modern

■ Classic

■ Sophisticated

■ Masculine

■ Seen as an entry

into the luxury

world

■ Good brand

positioning in

clothing, jeans,

jersey and shirts

■ Recognized as a

fashion brand for

perfect fitted suits

■ A top of mind in

fragrances

HUGO BOSS has clear competitive advantages in the Americas

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 39 / 67

Style

■ HUGO BOSS leads the modern, wear-to-work market for men

and women

■ HUGO BOSS has great name recognition in all regional markets

Quality ■ HUGO BOSS is recognized as providing consistency in fit and quality

European lifestyle brand value in the Americas

■ HUGO BOSS is seen as having a strong price/value relationship Price

Broad portfolio of unique brands

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 40 / 67

U.S.A. Canada Mexico Brazil Americas*

BOSS

BOSS Selection

BOSS Orange

BOSS Green

HUGO

Differentiated brands allow us to speak to different customer segments

*All splits based on full year 2012 sales estimates

76% // BOSS

2% // BOSS Selection

8% // BOSS Orange

7% // BOSS Green

7% // HUGO

Attractive growth opportunities across several categories

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 41 / 67

HUGO menswear clothing

■ Introduction of suit separates in Fall ‘12 with positive

early response

BOSS womenswear clothing

■ Direct involvement with designers in the U.S. to increase

regionally relevant content

BOSS men’s shoes

■ Development of strong good/better/best strategy with

$295 Italian made shoes for Fall ‘13

BOSS replenishment programs

■ Relaunch of sportswear basics and bodywear

businesses over the course of 2013

Continued store expansion in the Americas

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 42 / 67

■ Total number of own retail stores in the Americas amounts to 142 stores at the

end of September 2012

■ Around 15 store openings across the region projected for 2013

■ Number of stores in Brazil to double between 2011 and 2013

33 35

22

43

Sep. 30, 2012

142

64

Dec. 31, 2009

108

53

Outlets

Stores

Shop-in-shops

Number of own retail POS // Americas

8

44

19

71

Brazil

Mexico

Canada

USA

Own retail POS in the Americas by country (as of Sep. 30, 2012)

Manhasset, New York, USA

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 43 / 67

Beverly Center, California, USA

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 44 / 67

HUGO BOSS wins market share at wholesale

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 45 / 67

Q1 2012

Q2 2012

Q3 2012

Wholesale

sales

YTD Sep. ’12**

Reported comp store sales growth*

+3.5%

+4.8% +4.7% +3.3%

+9.3% +4.9% +11.2%

+4.4% +3.0% +3.7%

+5.0% +3.0% +5.0%

+14%

* Figures exclude online sales segment whenever available

** Total U.S. wholesale sales

+4.3% +5.3%

Controlled retail space upgrades brand presentation

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 46 / 67

■ Aggressive development over past two years

■ BOSS collection launched in 18 Neiman

Marcus doors

Shop-in-shop expansion Number of U.S. shop-in-shops

37

2

2013e

~70

2012e

~45

2011 2010

Transition to concession business model

■ Increased sales at retail through:

■ Dominant assortments

■ Controlled merchandising

■ Dedicated sales associates

■ Experience in the Americas region

Holt Renfrew shop-in-shop, Ste Foy, Canada

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 47 / 67

Target: USD 1 billion net sales in the Americas in 2015

Agenda

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 48 / 67

American strategy update

Financial strategy update

Group medium-term strategy

Summary

Continued focus on profitable growth

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 49 / 67

■ Space expansion and comp store sales growth

■ Growth across all regions

■ Above-average increases in underpenetrated

categories

■ Distribution channel mix to benefit

gross margin

■ Comp store sales growth to leverage

retail cost base

■ Marketing expenditures between 6%

and 7% of Group sales

■ Below-average growth of all other

operating expenses

+10%

2,059

3,000

2011 … 2015e

CAGR

+12.5%

469

750

CAGR

2011 … 2015e

Sales (in EUR million)

EBITDA (in EUR million)

Working capital management key focus to maximize free cash flow

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 50 / 67

Average trade net working capital as a percentage of sales at year-end (in %)

19.9

2011 2010

19.2

2009

24.6

2008

29.2

2007

28.2

Dividend strategy confirmed

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 51 / 67

0

10

20

30

40

50

60

70

80

90

2.50

2.00

1.50

1.00

0.50

0.00

2011

2.88

70%

2010

2.02

75%

2009

0.96

64%

2008

1.37

85% 3.00

1.45

65%

2006

1.19

64%

2005

1.00

65%

2004

0.84

67%

2003

0.78

67%

2002

0.75

71%

2007

Dividend* and payout ratio**

* Excluding special dividend // ** As a percentage of net profit attributable to the shareholders of the parent company

Dividend policy stipulates distribution of 60% to 80% of consolidated net profit

Payout ratio

Dividend

in EUR in %

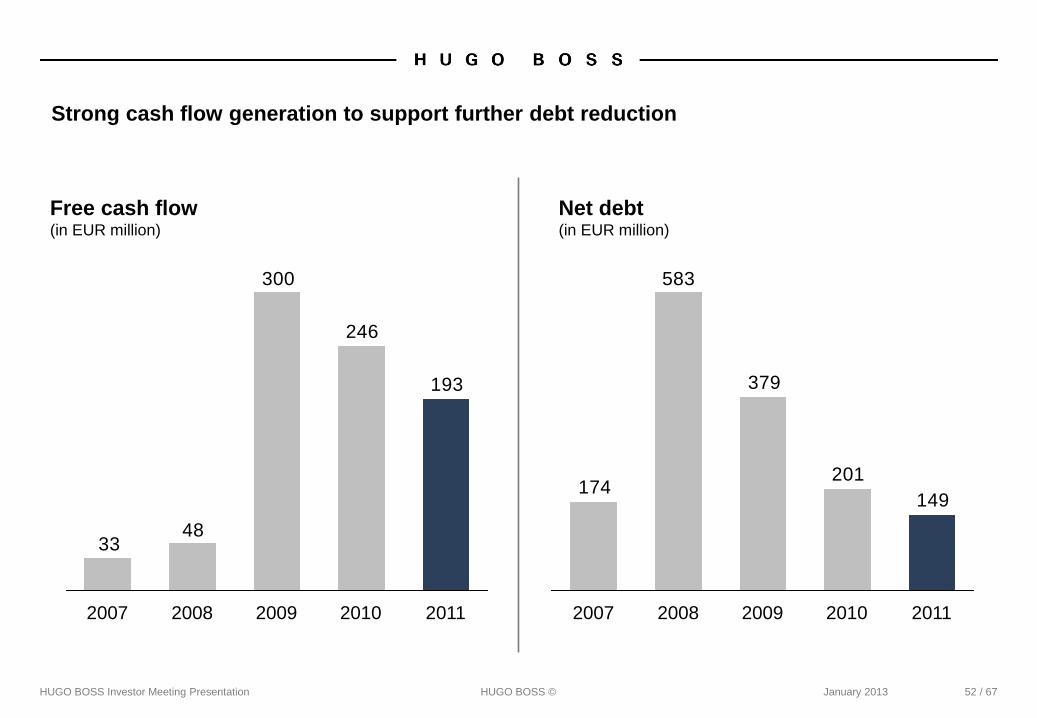

Strong cash flow generation to support further debt reduction

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 52 / 67

Free cash flow (in EUR million)

Net debt (in EUR million)

149

201

379

583

174

2011 2010 2009 2008 2007

193

246

300

4833

2011 2010 2009 2008 2007

Agenda

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 53 / 67

American strategy update

Financial strategy update

Group medium-term strategy

Summary

2012 guidance confirmed

Growth of EBITDA before special items 10% to 12%

HUGO BOSS Investor Meeting Presentation HUGO BOSS ©

2012 Outlook

Sales growth (currency-adjusted) Up to 10%

Capex Above prior year level

Own retail network Around 80 net organic openings

January 2013 54 / 67

Growth of EBITDA before special items 10% to 12%

HUGO BOSS on track for achievement of short- and medium-term targets

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 55 / 67

■ Transformation from wholesale-minded to consumer-

focused company well under way

■ All four strategy pillars contribute to growth

■ Strong performance in the Americas

■ Further progress towards achievement

of medium-term targets in 2013

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 56 / 67

BACKUP

5-Year Overview

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 57 / 67

in EUR million 2011 2010 2009 2008 2007Earnings PositionSales 2,058.8 1,729.4 1,561.9 1,686.1 1,632.0Gross Profit 1,264.8 1,027.2 847.1 891.0 845.0EBITDA 467.5 336.1 224.5 236.0 287.1EBITDA before special items 469.0 349.8 267.2 272.4 274.7EBIT 394.1 263.9 155.4 175.0 219.7Net income attributable to equity holders of the parent company 284.5 185.9 104.0 112.1 154.2Financial Position and DividendFree cash flow 193.3 246.3 299.5 48.1 33.0Net debt 149.1 201.1 379.1 583.2 173.6Capital expenditures 108.5 55.6 48.3 118.8 84.7Depreciation/amortization 73.4 72.2 69.1 61.0 67.4Dividend 199,1 139.7 66.6 94.9 100.4Special dividend - - - - 345.1Asset and Liability StructureTotal assets 1,449.0 1,355.4 1,065.4 1,161.6 1,039.3Shareholders' equity 523.2 361.2 205.5 202.9 550.7Trade net working capital 407.4 204.8 223.0 391.9 397.4Non-current assets 524.9 467.2 435.0 463.0 400.5Key FiguresGross profit margin in % 61.4 59.4 54.2 52.8 51.8Adjusted EBITDA margin in %* 22.8 20.2 17.1 16.2 16.8EBIT margin in % 19.1 15.3 10.0 10.4 13.5Total leverage** 0.3 0.6 1.4 2.1 0.6Equity ratio in % 36.1 26.6 19.3 17.5 53.0

* EBITDA before special items/Sales* * Net debt/EBITDA before special items and expenses for the "Stock Appreciation Rights Program"

Sales (in EUR million)

Gross margin (in %)

EBITDA before special items (in EUR million)

Net debt (in EUR million)

Nine months results at a glance

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 58 / 67

+11%

9M 2012

1,739

9M 2011

1,560

+1.2pp

9M 2012

61.1%

9M 2011

59.9%

250247

+1%

Sep. 30, 2012 Sep. 30, 2011

392372

+5%

9M 2012 9M 2011

Profit & loss statement

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 59 / 67

* Basic and diluted shares

** Preferred shares were converted into ordinary shares on June 15, 2012

in EUR million Q3 2012 Q3 2011 Change in %Jan.-Sep.

2012Jan.-Sep.

2011 Change in %

Net sales 646.3 615.0 5 1,738.5 1,559.6 11

Cost of sales (245.0) (241.1) (2) (642.8) (596.4) (8)Direct selling expenses (12.6) (12.0) (5) (34.0) (29.0) (17)

Gross profit 388.7 361.9 7 1,061.7 934.2 14in % of sales 60.1 58.8 1.3 pp 61.1 59.9 1.2 pp

Selling and distribution expenses (193.2) (159.1) (21) (573.3) (473.2) (21)Administration costs and other operating income and expenses (52.7) (43.1) (22) (156.8) (139.6) (12)

Operating result (EBIT) 142.8 159.7 (11) 331.6 321.4 3in % of sales 22.1 26.0 (3.9 pp) 19.1 20.6 (1.5 pp)

Net interest income/expense (4.2) (4.1) (2) (11.6) (11.8) 2Other financial items (2.6) 2.0 <(100) (3.4) 1.2 <(100)

Financial result (6.8) (2.1) <(100) (15.0) (10.6) (42)

Earnings before taxes 136.0 157.6 (14) 316.6 310.8 2Income taxes (32.6) (37.9) 14 (76.0) (74.6) (2)

Net income 103.4 119.7 (14) 240.6 236.2 2

Attributable to:Equity holders of the parent company 103.6 118.0 (12) 237.7 231.1 3Minority interests (0.2) 1.7 <(100) 2.9 5.1 (43)

Net income 103.4 119.7 (14) 240.6 236.2 2

Earnings per share (EUR)*Ordinary share 1.50 1.71 (12) 3.44 3.34 3Preferred share** 1.71 3.35

EBITDA before special items 165.4 177.1 (7) 391.7 372.1 5in % of sales 25.6 28.8 (3.2 pp) 22.5 23.9 (1.4 pp)

Sales by distribution channel

HUGO BOSS Investor Meeting Presentation HUGO BOSS ©

17

11

25

2

7

17

19

-1

-5 0 5 10 15 20 25 30

Group

Royalties

Retail

Wholesale

fx adjusted

in euro Sales growth by channel, y-o-y 9M 2012

(in %)

5

16

23

-5

0

16

15

-9

-10 -5 0 5 10 15 20 25

Group

Royalties

Retail

Wholesale

fx adjusted

in euro Sales growth by channel, y-o-y Q3 2012

(in %)

January 2013 60 / 67

Sales by region

HUGO BOSS Investor Meeting Presentation HUGO BOSS ©

*incl. Middle East and Africa

11

16

22

7

7

5

13

6

0 5 10 15 20 25

Group

Asia/Pacific

Americas

Europe*

fx adjusted

in euro Sales growth by region, y-o-y 9M 2012

(in %)

13

5

13

25

-3

0

0

-4

-5 0 5 10 15 20 25 30

Group

Asia/Pacific

Americas

Europe*

fx adjusted

in euro Sales growth by region, y-o-y Q3 2012

(in %)

January 2013 61 / 67

Trade net working capital

HUGO BOSS Investor Meeting Presentation HUGO BOSS ©

0

5

10

15

20

25

30

Q4 2011

19.9

Q3 2011

19.6

Q2 2011

19.3

Q1 2011

19.1

Q4 2010

19.2

Q3 2010

19.9

Q2 2010

20.9

Q1 2010 Q3 2009

27.2

Q2 2009

28.5

Q1 2009

29.7

22.7 +1.4pp

Q3 2012

21.0

Q2 2012

20.8

Q1 2012

20.2

24.6

Q4 2009

Average trade net working capital as a

percentage of sales by quarter (in %)

January 2013 62 / 67

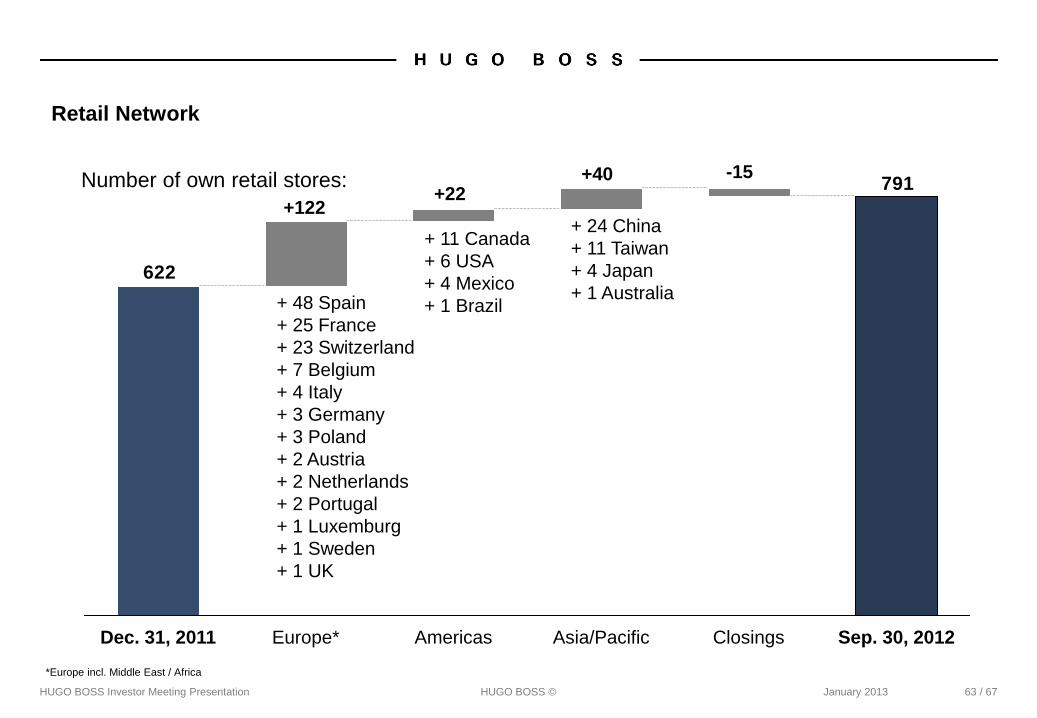

Retail Network

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013

*Europe incl. Middle East / Africa

63 / 67

Number of own retail stores: 791

622

Sep. 30, 2012 Closings Asia/Pacific Americas Europe* Dec. 31, 2011

+122 +22

+40 -15

+ 48 Spain

+ 25 France

+ 23 Switzerland

+ 7 Belgium

+ 4 Italy

+ 3 Germany

+ 3 Poland

+ 2 Austria

+ 2 Netherlands

+ 2 Portugal

+ 1 Luxemburg

+ 1 Sweden

+ 1 UK

+ 11 Canada

+ 6 USA

+ 4 Mexico

+ 1 Brazil

+ 24 China

+ 11 Taiwan

+ 4 Japan

+ 1 Australia

Level I ADR program to launched in January 2013

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 64 / 67

ADR Details Benefits of ADRs for

U.S. investors

■ Clear and settle according to normal U.S.

standards

■ Offer the convenience of stock quotes and

dividend payments in U.S. dollars

■ Can be purchased/sold in the same way as

other U.S. stocks via a U.S. broker

■ Provide a cost-effective means of

international portfolio diversification

Market OTC

Symbol BOSSY

CUSIP 444560106

Ratio 5 : 1

Country Germany

Effective Date Jan 18, 2013

Underlying SEDOL B88MHC4

Underlying ISIN DE000A1PHFF7

Depositary BNY Mellon

Hong Kong

Joe Oakenfold

email: [email protected]

Tel: +852 2840 9717

New York

Ravi Davis

email: [email protected]

Tel: +1 212 815 4245

London

Mark Lewis

email: [email protected]

Tel: +44 (0)20 7964 6089

For questions about creating HUGO BOSS ADRs, please contact BNY Mellon:

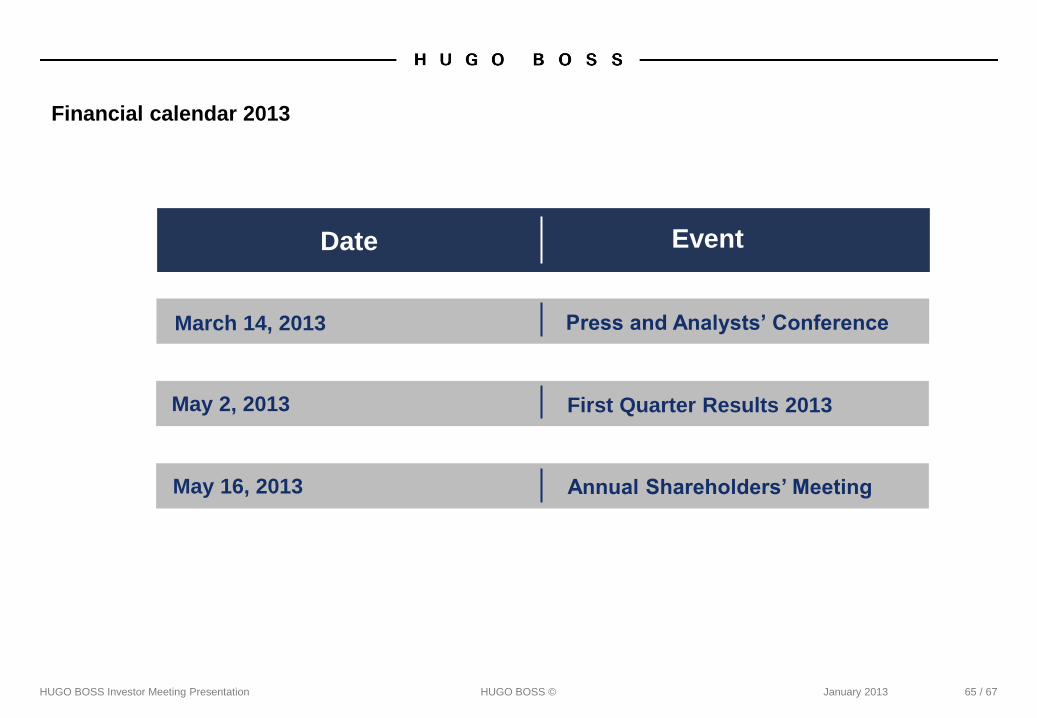

Financial calendar 2013

HUGO BOSS Investor Meeting Presentation HUGO BOSS ©

Date Event

March 14, 2013 Press and Analysts’ Conference

May 2, 2013 First Quarter Results 2013

May 16, 2013 Annual Shareholders’ Meeting

January 2013 65 / 67

Forward looking statements contain risks

HUGO BOSS Investor Meeting Presentation HUGO BOSS © January 2013 66 / 67

This document contains forward-looking statements that reflect management's current views with

respect to future events. The words "anticipate ", "assume ", "believe", "estimate", "expect",

"intend", "may", "plan", "project", "should", and similar expressions identify forward-looking

statements. Such statements are subject to risks and uncertainties. If any of these or other risks

and uncertainties occur, or if the assumptions underlying any of these statements prove incorrect,

then actual results may be materially different from those expressed or implied by such statements.

We do not intend or assume any obligation to update any forward-looking statement, which speaks

only as of the date on which it is made.