iab pwc: online adspend study 2007, uk

TRANSCRIPT

2007 UK online adspend study

1. Introduction

Agenda

1. Introduction

2. Study methodology

3. Market background and trends

4. UK online adspend – headline results

5. Online in context

6. The digital media mix

7. Industry categories

8. Summary

9. Looking ahead…

10. Questions

Background

• Census of all major UK online media owners

• Official Advertising Association figures since 1997

• Information collected each half year

• Analysis available by

‒ Format

‒ Industry category

2. Methodology

• The IAB has been working with PwC since 1997 to survey the value of the online advertising market

• We have run projects in Europe and North America to assess the size of the interactive media markets

• These figures have become the industry standard for measuring advertising spend

• 118 companies have participated in the survey

• Reported figures are not adjusted to account for other organisations that have not participated

• Total advertising revenue is reported on a gross basis

• The figures are drawn up on the basis of site declaration

• They cover thousands of UK websites, but by no means all

A brief history…

Research participants

Acxiom Ad2-one Adept Scientific Adlink Ad Revenue AdSales4U Advertising.com Adviva AOL Affiliate Window Ask Associated Northcliffe Digital Autotrader BBC Worldwide

Bloomberg Blue Lithium BMJ Bolt Blue Bounty BSkyB Buy Association Buy.at (Perfiliate) Channel 4 Chinwag Chrysalis Radio Classic FM CNET Conde Nast Confetti Dennis

Interactive DGM Dixons Double Fusion E-circle Economist EDR EMAP E-Type Euroclick Everyclick Faversham House Group Financial Times Find.co.uk Findaproperty Fish4 Five

Friends Reunited Future Publishing GCap Radio Google Guardian Habbo Hachette Fillpacchi Handbag Haymarket Hello IDG Independent I.E.T (Institute of Engineering and Technology) IPC Media IPT i-Points ITN ITV iVillage Jetix Jobs.ac.uk Jobsite Johnston Press Loot Lycos Manchester Online Media Brokers Memedia Miva Monetise Moneyextra Monster MSN My

Space National Magazines Net Communities Netrecruit News International Orange Oridian Overture Pigsback Prime Location Property Finder Real Media Reed Business Information Reuters Right Move Scotland Online Sift Simply Media TV SRH Skupe Teamtalk Telegraph

Tesco Tiscali TMN Media Tradedoubler UK Net Guides UKTV Unanimis Upmystreet U Target Valueclick Viacom Brand Solutions Virgin Radio WME Workthing Yahoo! Yell

…Plus further recruitment sites, courtesy of WARC

Representing thousands of UK websites

3. Market background

and trends

At the height of the “boom” online was worth £166m!

19.4

153.1

165.7

51.0

0

20

40

60

80

100

120

140

160

180

1998 1999 2000 2001

£ m

illio

ns

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

Where were we this time last year?..

• Online broke through the £2bn barrier in 2006

• The medium grew by 41% from £1.4bn in 2005

• Online overtook National Press• Our initial forecast for 2007 was £2.6bn…

• …but we revised that up to £2.75bn (and Prayed!)

3.6mJune 96

Source: Gfk NOP World, To July 2007

Have you used the Internet in the last 12 months?

32.5mJuly 07

Meanwhile the audience is still growing

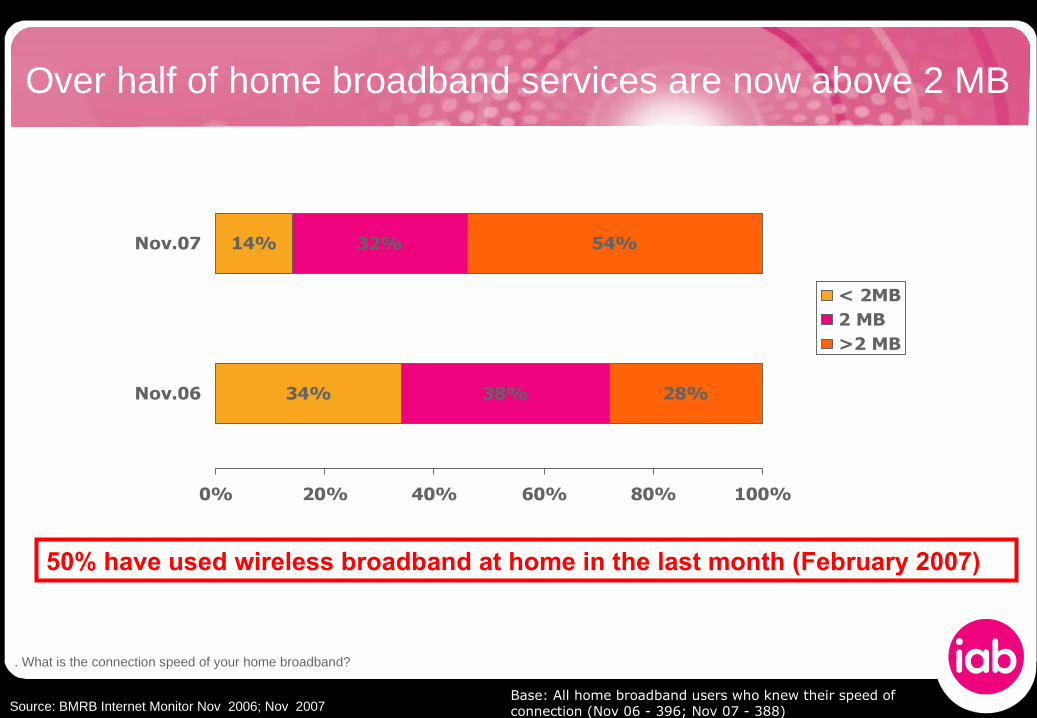

Over half of home broadband services are now above 2 MB

34%

14%

38%

32% 54%

28%

0% 20% 40% 60% 80% 100%

Nov.06

Nov.07

< 2MB2 MB>2 MB

Base: All home broadband users who knew their speed of connection (Nov 06 - 396; Nov 07 - 388)Source: BMRB Internet Monitor Nov 2006; Nov 2007

50% have used wireless broadband at home in the last month (February 2007)

Q. What is the connection speed of your home broadband?

Young women take over…

Women 25-34 now spend more time online than men in

the same age group.

Source: Ofcom Communications Report 2007

Empty nesters go surfing…

One quarter of all Britons online are over 50 and 30% of total time spent on the internet is by the over 50’s

Source: Ofcom Communications Report 2007

It’s never been easier to get online

£4.50

Toshiba Tecra 8100£250 inc VAT

$100 Wind Up

50p per hour

Free at libraries

Bars, Hotels,Coffee shops, parks…

4. UK Online Adspend Study

Results for the full year of 2007Prepared by PricewaterhouseCoopers for the IAB

Have I got news for you…?

£2,812.6mmarket in 2007

An increase of £797m year-on-year

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

38% increase

New contributions in 2007 represented £64.9m

2007 vs. 2006

on a like for like basis

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

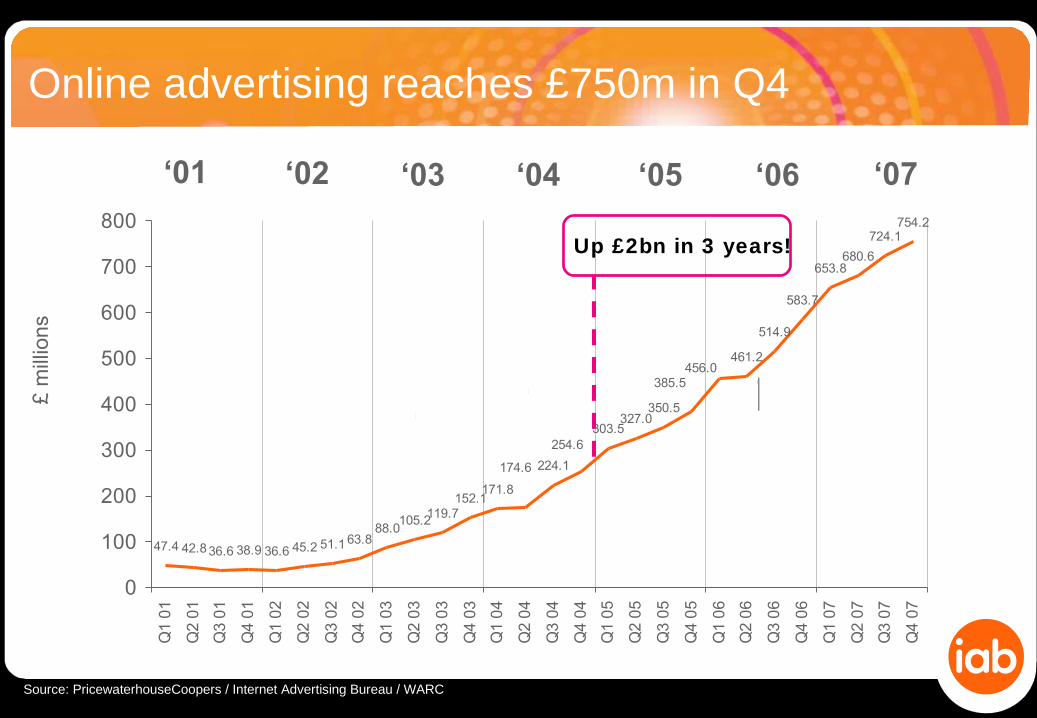

Online advertising reaches £750m in Q4

47.4 42.836.6 38.9 36.6 45.2 51.1 63.888.0

105.2119.7152.1

171.8

224.1

303.5327.0

350.5

461.2

514.9

583.7

653.8680.6

724.1754.2

385.5456.0

174.6

254.6

0

100

200

300

400

500

600

700

800

Q1

01

Q2

01

Q3

01

Q4

01

Q1

02

Q2

02

Q3

02

Q4

02

Q1

03

Q2

03

Q3

03

Q4

03

Q1

04

Q2

04

Q3

04

Q4

04

Q1

05

Q2

05

Q3

05

Q4

05

Q1

06

Q2

06

Q3

06

Q4

06

Q1

07

Q2

07

Q3

07

Q4

07

£ m

illio

ns

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

‘01 ‘03‘02 ‘04 ‘05 ‘06 ‘07

Up £2bn in 3 years!

5. Online in context…Breaking market trends in the UK ad industry

21.8%

15.3%

11.8% 5.3%

3.3%

0.9%6.7%

15.1%

19.9%

Television

Press - Display

Internet

Press - Classified

Direct Mail

Directories

Outdoor

Radio

Cinema

2007 market share 15.3% (11.4% in 2006)

% share of revenues for January to December 2007

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

IAB estimates for actual ad spend by format are based on samples of categorised revenue from key IAB members provided by PwC. Data excludes unclassified figures.

Total advertisingmarket

£18.4bn

-3.2%

4.0% 4.6%

9.9%

-0.3%

2.3% 2.8%

-6.5%

38%

Direct

Press

Clas

sified

Press

Disp

lay TVRad

io

Direct

ories

Outdo

or

Cinem

a

Inte

rnet

Source: PricewaterhouseCoopers / Internet Advertising Bureau, The Advertising Association / WARC: WARC estimate for directories.

Online drives the whole market

Total advertising market growth = 4.3%

Year on year growth for 2007

Mar

ket

Sha

reOnline’s share growth accelerates to 16%

Source: PricewaterhouseCoopers / Advertising Association / Internet Advertising Bureau / WARC

2.5%3.3%

4.2%5.5%

7.3%8.4%

10.4%

12.4%

14.7%15.9%

H12003

H22003

H12004

H22004

H12005

H22005

H12006

H22006

H12007

H22007

0

200

400

600

800

1000

1200

Q198

Q298

Q398

Q498

Q199

Q299

Q399

Q499

Q100

Q200

Q300

Q400

Q101

Q201

Q301

Q401

Q102

Q202

Q302

Q402

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Online slices through the media market£

mill

ions

Source: PricewaterhouseCoopers / Internet Advertising Bureau / Advertising Association / Radio Advertising Bureau / WARC

N.B. WARC Recruitment data included from 2003

Radio

Outdoor

Internet

Press - Display

Television

Press - Classified

Direct Mail

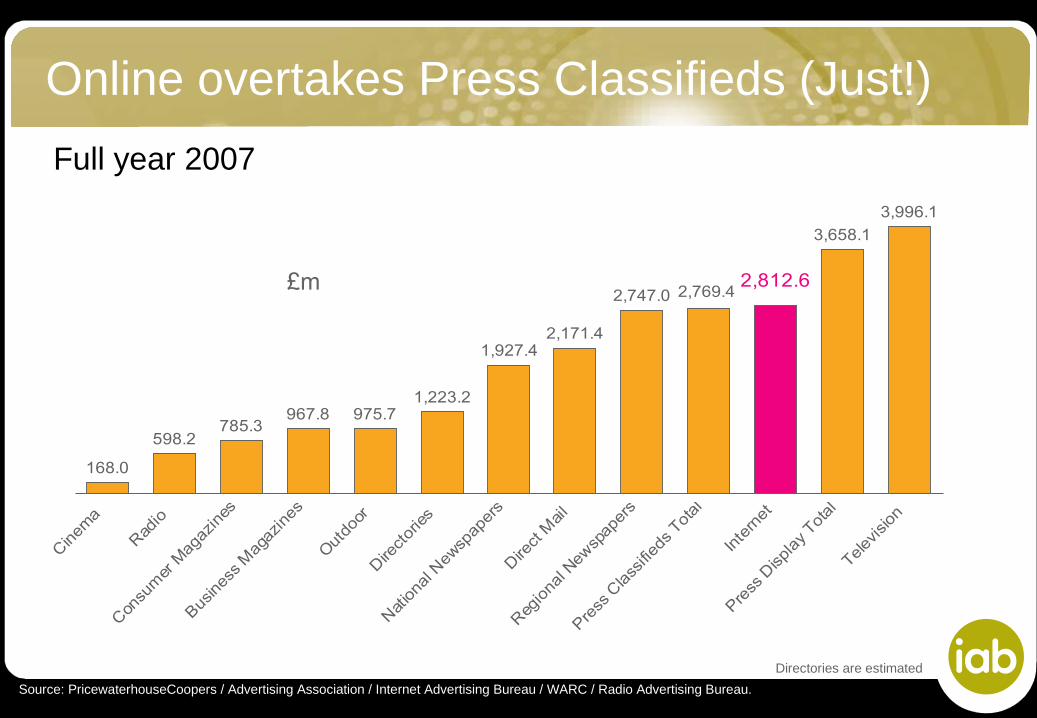

Online overtakes Press Classifieds (Just!)

168.0

598.2785.3

967.8 975.71,223.2

1,927.42,171.4

2,747.0

3,658.1

3,996.1

2,769.42,812.6

Cinem

a

Rad

io

Con

sum

er M

agaz

ines

Busines

s M

agaz

ines

Out

door

Dire

ctor

ies

Nat

iona

l New

spap

ers

Dire

ct M

ail

Reg

iona

l New

spap

ers

Press

Class

ified

s Tot

al

Inte

rnet

Press

Disp

lay Tot

al

Telev

ision

£m

Source: PricewaterhouseCoopers / Advertising Association / Internet Advertising Bureau / WARC / Radio Advertising Bureau.

Full year 2007

Directories are estimated

Summary – Full year 2007

• Online advertising driving growth of the entire media market

• Internet advertising reaches £2,812.6m in 2007

• Online achieved a share of 15.3%, up nearly 4 points from 2006 (11.4%)

• The market grew on a like for like basis by 38% year-on-year, maintaining the strong growth of previous waves

• Online overtakes Regional Newspapers and press classifieds (15% and 15.1% respectively)

Summary – H2 2007

• In the second half of the year, online advertising was worth £1,478.2m

• The internet’s share of all advertising expenditure actually reached 15.9%

• Revenues for Q4 over £750m

6. The digital media mixThe developing mix of ad products

21.0%

57.6%

0.6%

20.8%

DisplayClassifiedsPaid for searchSolus Email

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

IAB estimates for actual ad spend by format are based on samples of categorised revenue from key IAB members provided by PwC. Data excludes unclassified figures.

Full year total

£2,812.6m

% share of revenues for the full year 2007

The digital media mix

335.9262.2

768.3

453.7379.0

1165.6

592.0 585.3

1619.1

Display Classifieds Paid for search

2005 2006 2007

£ m

illio

ns

+31% +54%

+39%

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

IAB estimates for actual ad spend by format are based on samples of categorised revenue from key IAB members provided by PwC. Data excludes unclassified figures.

The digital media mix

All online formats have experienced strong growth

10.2%

16.6%

10.5%

57.6%

1,6%

Banners / Embedded

Sponsorships

Interruptive formats

Display ads on email

Tenancies

Other display

Solus Email

Recruitment classifieds

Consumer classifieds

B2B Classified

Paid-for search listings

The digital media mix

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

IAB estimates for actual ad spend by format are based on samples of categorised revenue from key IAB members provided by PwC. Data excludes unclassified figures.

Full year total

£2,812.6m

£467.1m

£23.1m

£15.1m

£23.4m

£44.1m

£19.2m

£16.2m

£286.8m

£296.5m

£1.9m

£1,619.1m

% share of revenues for the full year 2007

The digital media mix£

mill

ions

IAB estimates for actual ad spend by format are based on samples of categorised revenue from key IAB members provided by PwC. Data excludes unclassified figures.

14.0

17.5

15.8

20.1

9.1

15.1

16.2

19.2

23.1

23.4

44.1

298.4

467.1

1619.1

73.2

215.2

163.8

321.5

1165.6

286.8

Interruptive formats

Solus Email

Other display

Sponsorships

Display ads on email

Tenancies

Recruitment classifieds

Further classifieds

Banners / Embedded

Paid-for search listings

2007

2006

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

Year on year comparison

Strong growth of Search continues

181.2248.5

337.0

431.4

531.3

634.3

762.3

856.8

H1 2004 H2 2004 H1 2005 H2 2005 H1 2006 H2 2006 H1 2007 H2 2007

£m

Source: Internet Advertising Bureau / PricewaterhouseCoopers

Almost 90% use search every month

Source: Nielsen Online, MegaView Search UK, January 2008, Home and Work, Netview January 2008, IAB/PwC Online Ad Spend H2 2007

• In January 2008, 29m people visited a search engine and 27.7m of these clicked through onto a site.

• This equates to 89% of the internet population visiting a search engine and 84% clicking through.

• There were 1.7bn search queries carried out in the UK in January 2008.

• On average, there are 3.4 click throughs per search session.

• PPC Search revenues in 2007 reached £1,619.1m. In H2 2007 this was £856.8

53.8 67.494.4 87.6 102.8 112.3

142.0 144.814.3

26.0

37.0 43.359.3

104.5

135.6162.8

0

50

100

150

200

250

300

350

H1 2004 H2 2004 H1 2005 H2 2005 H1 2006 H2 2006 H1 2007 H2 2007

Recruiment classifieds Further classifieds

£m

Source: Internet Advertising Bureau / PricewaterhouseCoopers

Growth in further classifieds

Classifieds led by key players

Display: formats dominated by banners & rich media

73.2 91.4 105.4 119.0 138.9182.7

203.6

263.5

305.0287.1

237.9215.9

173.8162.1

136.2

96.7

0

50

100

150

200

250

300

350

H1 2004 H2 2004 H1 2005 H2 2005 H1 2006 H2 2006 H1 2007 H2 2007

Banners / Embedded Sponsorships Interruptive formats

Display ads on email Tenancies Other display

£m

Source: Internet Advertising Bureau / PricewaterhouseCoopers

Embedded formats up over 100% in the last two years£

mill

ions

IAB estimates for actual ad spend by format are based on samples of categorised revenue from key IAB members provided by PwC. Data excludes unclassified figures.

224.4

55.6

20.5 8.8 15.7

321.5

73.2

20.1 9.1 14.0 15.8

467.1

44.123.1 23.4 15.1 19.210.9

Banners /Embedded

Tenancies Sponsorships Display ads onemail

Interruptive formats Other display

2005

2006

2007

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

+45%

+8%+15% +22%+159%-40%

IASH sales houses represent thousands of sites

Source: Internet Advertising Bureau

40% of display spend through networks

Formats summary – 2007

• Revenues increased across all formats, except for tenancies and solus e-mail

• With revenues of £1619.1m in 2007, search maintained its dominant position

• YoY, display was up 31% to £592m while search increased by 39% and classifieds were up by 54% to £585.3m

• Core “embedded” display rose 45% YOY

• Classifieds: recruitment increased by 33% to £286.8m and other classifieds grew by 82% to £298.4m

Source: Internet Advertising Bureau / PricewaterhouseCoopers

7. Industry categories

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

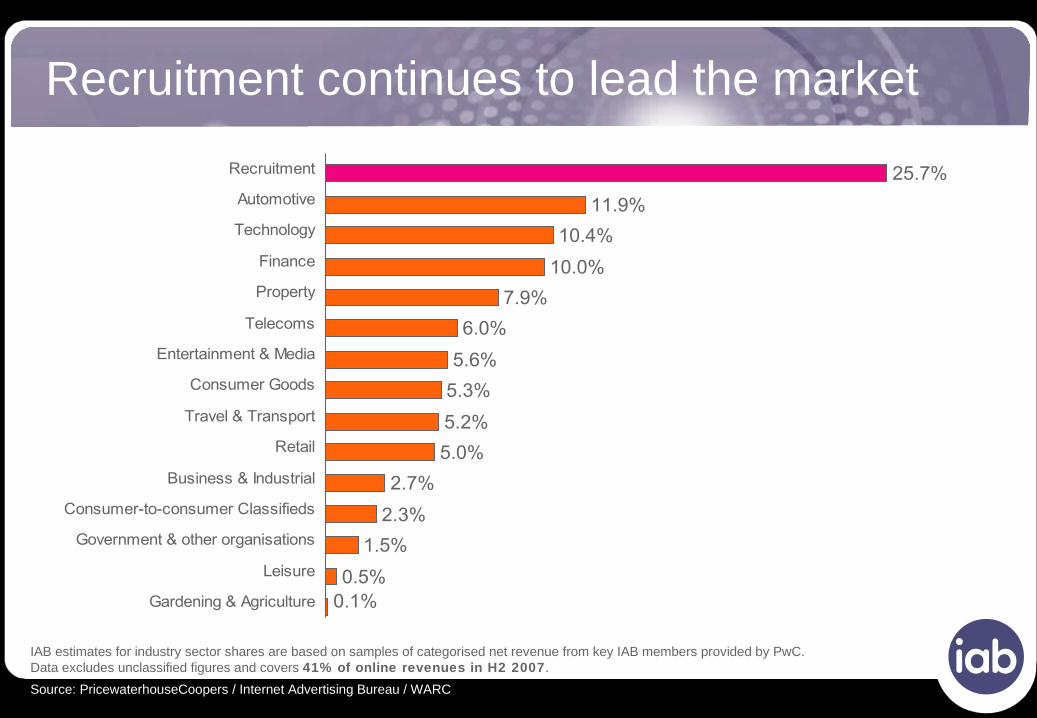

IAB estimates for industry sector shares are based on samples of categorised net revenue from key IAB members provided by PwC. Data excludes unclassified figures and covers 41% of online revenues in H2 2007.

Recruitment continues to lead the market

0.1%0.5%

1.5%

2.3%

2.7%

5.0%

5.2%

5.3%

5.6%

6.0%

7.9%

10.0%

10.4%

11.9%

25.7%

Gardening & Agriculture

Leisure

Government & other organisations

Consumer-to-consumer Classifieds

Business & Industrial

Retail

Travel & Transport

Consumer Goods

Entertainment & Media

Telecoms

Property

Finance

Technology

Automotive

Recruitment

Sector Market Shares

0.9%

0.3%

1.2%

1.0%

0.6%

3.3%

5.8%

8.0%

0.1%

0.5%

1.5%

2.3%

2.7%

5.0%

5.2%

5.3%

5.6%

6.0%

7.9%

10.0%

10.4%

11.9%

25.7%

4.4%

13.8%

13.4%

24.8%

12.6%

4.6%

5.3%

Gardening & Agriculture

Leisure

Government & other organisations

Consumer-to-consumer Classifieds

Business & Industrial

Retail

Travel & Transport

Consumer Goods

Entertainment & Media

Telecoms

Property

Finance

Technology

Automotive

Recruitment

H2 2007

H2 2006

IAB estimates for industry sector shares are based on samples of categorised net revenue from key IAB members provided by PwC. Data excludes unclassified figures and covers 41% of online revenues in H2 2007.

*

• Technology overtakes Finance

• Property enters top 5

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

Sector Market Shares

0.9%

0.3%

1.2%

1.0%

0.6%

3.3%

5.8%

8.0%

0.1%

0.5%

1.5%

2.3%

2.7%

5.0%

5.2%

5.3%

5.6%

6.0%

7.9%

10.0%

10.4%

11.9%

25.7%

4.4%

13.8%

13.4%

24.8%

12.6%

4.6%

5.3%

Gardening & Agriculture

Leisure

Government & other organisations

Consumer-to-consumer Classifieds

Business & Industrial

Retail

Travel & Transport

Consumer Goods

Entertainment & Media

Telecoms

Property

Finance

Technology

Automotive

Recruitment

H2 2007

H2 2006

IAB estimates for industry sector shares are based on samples of categorised net revenue from key IAB members provided by PwC. Data excludes unclassified figures and covers 41% of online revenues in H2 2007.

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

Retail gains share

!

Spotlight on Retail

• Online spend beginning to grow, reflecting a buoyant and competitive e-commerce market (46.6bn 2007)

• 46.6bn ecommerce spend up 54% on the £30.2bn recorded for 2006

Are Finance and travel maturing?

0.2%

0.5%

0.7%

0.9%

1.4%

3.5%

4.2%

5.7%

6.2%

9.3%

10.5%

11.2%

21.6%

24.0%

Gardening & Agriculture

Leisure

Government & other organisations

Consumer-to-consumer Classifieds

Property

Retail

Business & Industrial

Consumer Goods

Entertainment & Media

Technology

Automotive

Travel & Transport

Recruitment

Finance

0.1%0.5%

1.5%

2.3%

2.7%

5.0%

5.2%

5.3%

5.6%

6.0%

7.9%

10.0%

10.4%

11.9%

25.7%

Gardening & Agriculture

Leisure

Government & other organisations

Consumer-to-consumer Classifieds

Business & Industrial

Retail

Travel & Transport

Consumer Goods

Entertainment & Media

Telecoms

Property

Finance

Technology

Automotive

Recruitment

*

Finance and Travel spend has increased

over time,

but share of categories has declined

H2 2007

H2 2004

• Property is the share point winner (+3.3 points) however, recruitment retains the pole position and Technology overtakes Finance for the first time to take the third spot.

• Retail (+1.7), Business and Industrial (+2.1) and Telecoms (+0.7 points) strengthened their positions whilst Finance (-3.8 points) and Technology (-3 points) continued to showed a decline.

• Share for Consumer Goods, though remains mid tier, increased by 0.9 point - there is still room for growth in this sector.

Industry sectors summary – H2 2007

8. Summary

Have I got news for you…

Summary

• Online ad spend leaps by 38% year-on-year (on a

like-for-like basis) to reach £2,812.6m in 2007

• Online achieved a share of 15.3%, up 3.9 points from 2006 (11.4%)

• Online overtakes Press Classifieds and Regional Newspapers Online has grown

by £2bn in just

3 years

Summary

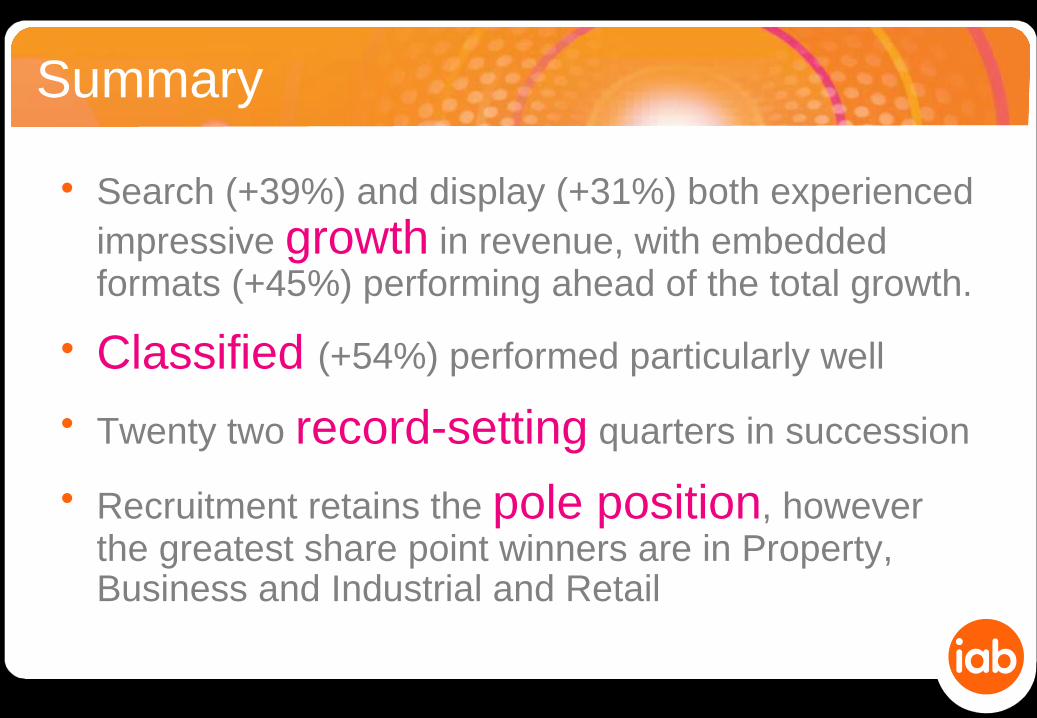

• Search (+39%) and display (+31%) both experienced impressive growth in revenue, with embedded formats (+45%) performing ahead of the total growth.

• Classified (+54%) performed particularly well

• Twenty two record-setting quarters in succession

• Recruitment retains the pole position, however the greatest share point winners are in Property, Business and Industrial and Retail

9. Looking ahead

Online poised to draw level with total Press display

0

200

400

600

800

1000

1200

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Internet Press Display

£m

Source: PricewaterhouseCoopers / Advertising Association / Internet Advertising Bureau / WARC

Could online overtake TV next year?

0

200

400

600

800

1000

1200

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Internet TV

£m

Source: PricewaterhouseCoopers / Advertising Association / Internet Advertising Bureau / WARC

…And be the single biggest medium!?

YOU BET!

!

£

Our current forecast for 2008 is…

£3.6 billion

All of the 118 companies taking part, representing thousands of websites

and to

Our thanks to…

Nicki Lynas, Senior Manager and

Paul Pilkington, Director

Colin Macleod, Research Director