ibex global solutions plc · operations with ibm, convergys, 3com corporation, modus media, and...

TRANSCRIPT

ANNUAL REPORT

2016IBEX GLOBAL SOLUTIONS PLC

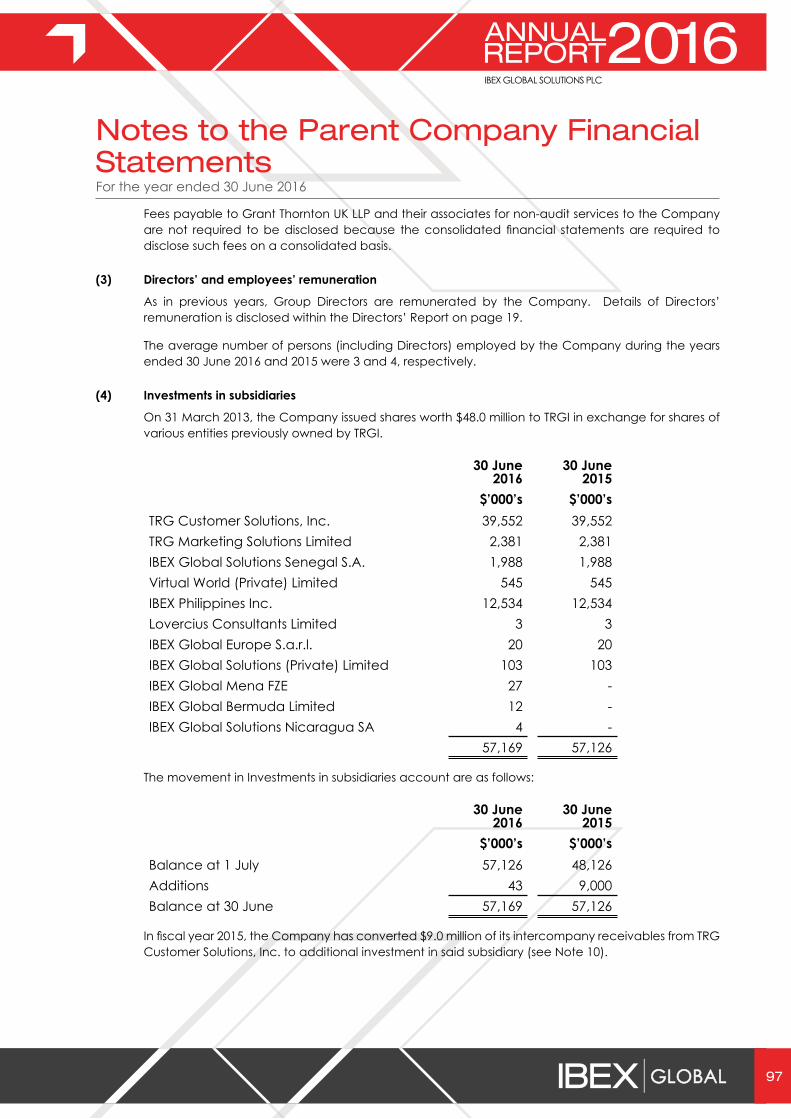

RESPECT | INTEGRITY | TRANSPARENCY | EXCELLENCE

Table of Contents

Company Information 1

Board of Directors 2

Chairman’s Statement 4

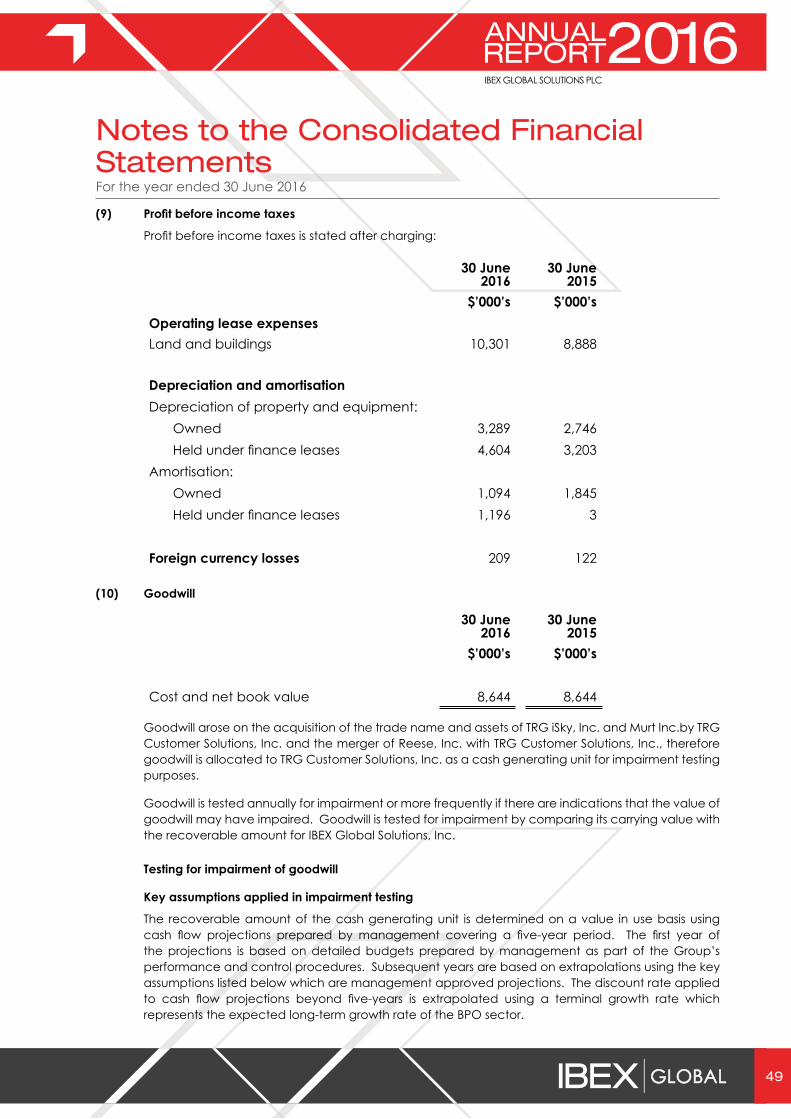

Strategic Report 6

Directors’ Report 17

Corporate Governance Report 24

Statement of Directors’ Responsibilities 26

Independent Auditors’ Report on Group Financial Statements 27

Consolidated Statement of Comprehensive Income 29

Consolidated Statement of Financial Position 30

Consolidated Statement of Changes in Equity 32

Consolidated Statement of Cash Flows 33

Notes to the Consolidated Financial Statements 34

Independent Auditors’ Report on Parent Company Financial Statements 89

Parent Company Statement of Financial Position 91

Parent Company Statement of Changes in Equity 92

Parent Company Statement of Cash Flows 93

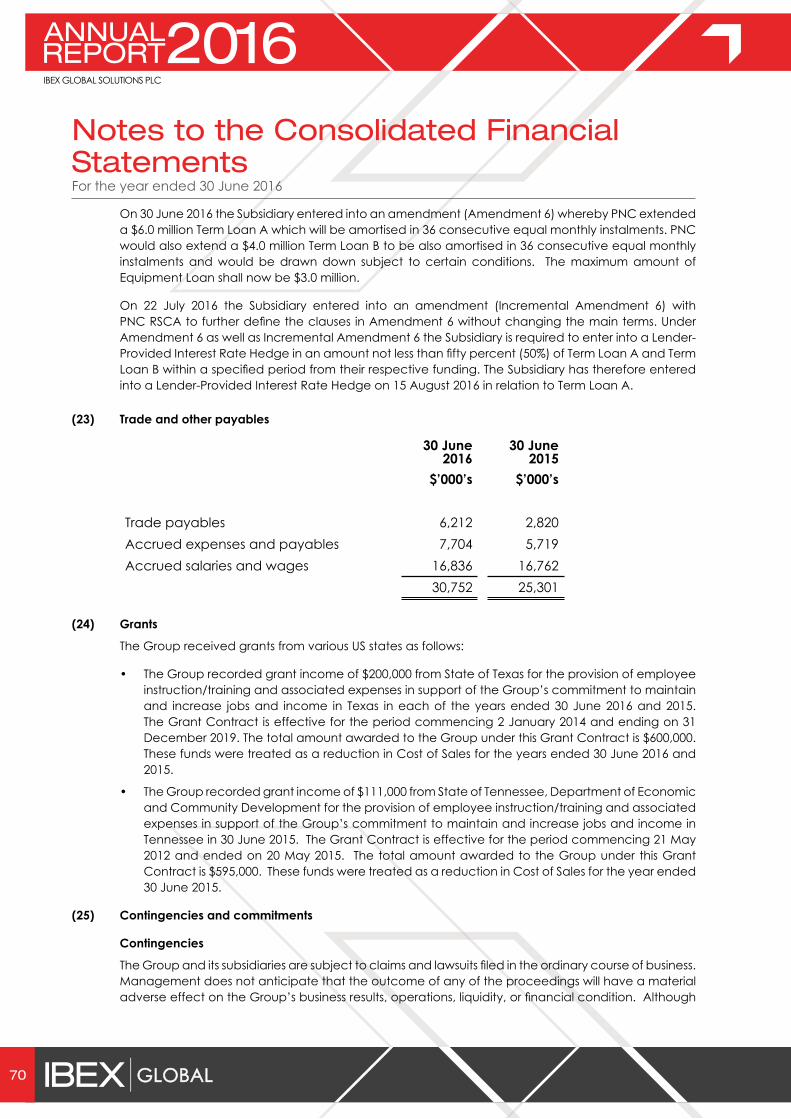

Notes to the Parent Company Financial Statements 94

4

4 1

Directors Muhammad Ziaullah Khan (“Zia”) Chishti (Non-executive Chairman)Robert Dechant (Chief Executive Officer)Karl Gabel (Chief Financial Officer)Mohammedullah (“Mohammed”) Khaishgi (Non-executive Director)John Leone (Non-executive Director)Gerhard Johannes (“Gerard”) Kleisterlee (Independent Non-executive Director)Joel Wyler (Independent Non-executive Director)

Corporate Secretary Deena Williamson

Registered Office 3rd Floor5 Lloyds AvenueLondonEC3N 3AE

Registered Number 08462510

Nominated Advisor and Joint Broker

Liberum Capital LimitedRopemaker Place, Level 1225 Ropemaker StreetLondon EC2Y 9LY

Joint Broker Cenkos Securities Plc6.7.8 Tokenhouse YardLondonEC2R 7AS

Legal Advisers to IBEX Global Solutions Plc and subsidiaries (IBEX, IBEX Global, IBEX Group or the Group)

Eversheds LLP1 Wood StreetLondonEC2V 7WS

Auditor to the Group Grant Thornton UK LLPGrant Thornton HouseMelton StreetEuston SquareLondonNW1 2EP

Reporting Accountant Grant Thornton UK LLP30 Finsbury SquareLondonEC2P 2YU

Registrar Capita Registrars LimitedThe Registry34 Beckenham RoadBeckenhamKentBR3 4TU

Public Relations Adviser to the Group

Alma PR Limited37 Dempster RoadLondonSW18 1AS

Website www.ibexglobal.com

Company InformationFor the year ended 30 June 2016

2

For the year ended 30 June 2016

Zia Chishti – Non-executive Chairman

Zia is the Chief Executive Officer (CEO) and Chairman of The Resource Group International (TRGI). He represents TRGI’s 71 percent interest in IBEX Global Solutions Plc (IBEX Global, the Company, the Holding Company or the Parent Company). Zia has served as the Chairman and CEO of Align Technology (NASDAQ: ALGN) which he led from inception to a more than $500 million public valuation. Zia has worked at Morgan Stanley and McKinsey and serves on multiple corporate and non-profit boards. Zia is a graduate of Columbia University and earned an MBA from Stanford Graduate School of Business.

Robert Dechant – Chief Executive Officer

Mr. Robert Dechant is a proven executive in the business process outsourcing and technology industries. He has over 25 years of leadership experience in strategic sales, marketing, client management and operations with IBM, Convergys, 3Com Corporation, Modus Media, and Stream Global Services, Inc.

Prior to joining IBEX Global, Mr. Dechant was the Chief Sales, Marketing and Client Relations Officer at Qualfon Inc., a global business process outsourcing (BPO) provider. In this role, he diversified the client portfolio, implemented new sales and go-to-market processes and established viable nearshore markets, transforming the business into a rapidly growing player in the BPO industry. He also served as the Executive Vice President for Sales, Marketing and Client Services for Stream Global Services, an $850.0 million revenue per year global BPO provider.

Karl Gabel – Chief Financial Officer

Karl joined IBEX Global at the time of its acquisition of Telespectrum Worldwide, Inc. in 2004, where he was Vice President of Finance and was instrumental in the financial restructuring of Telespectrum Worldwide, Inc. prior to its sale. Karl has over 19 years of experience in the contact centre industry, commencing with his first role as Director of Revenue at Telespectrum in 1997. Karl has a B.S. in Accounting from Penn State University and MBA from St. Joseph’s University.

Board of Directors

2 3

For the year ended 30 June 2016

Mohammed Khaishgi – Non-executive Director

Mohammed is Chief Operating Officer of TRGI. He along with Zia Chishti, as Board Directors of TRGI, represent TRGI’s 71 percent interest in the Company. Prior to joining TRGI in 2003, Mohammed was a Senior Director at Align Technology, where he managed Align’s offshore contact centre and back office services operations. He was previously a Senior Investment Officer at the International Finance Corporation (private sector investment arm of the World Bank) where he was responsible for investments in the Asian telecommunications and technology sectors. Mohammed has a B.S. degree in Electrical Engineering from University of Engineering and Technology in Lahore, Pakistan, a B.A. degree in Philosophy, Politics and Economics from the University of Oxford where he was a Rhodes Scholar and MBA from Harvard Business School.

John Leone – Non-executive Director

John Leone is a Non-executive Director of the Company. John Leone is the Managing Director of PineBridge Investments, an investor in TRGI. John works on sourcing, negotiating and executing private equity transactions in Europe, Latin America, the Middle East and Africa. Prior to this role, John was General Counsel of PineBridge Investments’ Emerging Markets Private Equity operations. Earlier in his career, John was an attorney at Kirkland & Ellis LLP where he focused on advising private equity clients. John earned a Juris Doctor, with High Honours, from The George Washington University Law School where he was a member of the Law Review, and a Bachelor of Arts, Magna Cum Laude, from the State University of New York at Binghamton.

Gerard Kleisterlee – Independent Non-executive Director

Gerard Kleisterlee is an Independent Non-executive Director of the Company. He is Chairman of Vodafone Group Plc. A Non-executive Director and member of the Audit Committee and Chair of the Remuneration Committee of Royal Dutch Shell and Chairman of the Supervisory Board of Dutch Technology Company ASML A former member of the Supervisory Board of Daimler AG, and of the Board of Directors of Dell Inc. He was President, CEO and Chairman of Royal Philips Electronics from 2001 to 2011.

Joel Wyler – Independent Non-executive Director

Joel Wyler is an Independent Non-executive Director of the Company and, currently, he is the Chairman of Granaria Holdings, a global investment company. He is an entrepreneur with a broad range of knowledge and experience in operating, manufacturing, trading, shipping and logistics companies internationally. He is a director of Rainbow Medical Ltd, and Aegate Holdings, Ltd. Joel is a partner of ACPI Investments, Ltd, member of the Advisory Board of SatMap, Inc. d/b/a Afiniti, and a Board Member of Cocon Vastgoed B.V. Joel was appointed Officer of the Order of Orange Nassau in 2000 and Chevalier de la Legion d’honneur in 2009.

Board of Directors

4

For the year ended 30 June 2016

Dear fellow shareholders,

I am pleased to announce this set of strong results, which marks the first full year under Bob Dechant’s stewardship, and shows excellent progress in all key metrics across the Group as we continue to deliver efficiently against our growth strategy announced in February 2016. Our financial performance reflects not only very encouraging growth in volumes with existing clients, but also, importantly, an expansion in our client base. This success has been delivered through a combination of continued investment in front line call centre agents and new facilities, as well as the hard work and dedication of all our employees.

Financial Results

Revenues in the year to 30 June 2016 were $255.5 million, representing strong improvement compared with the previous year (2015: $238.8 million) and adjusted EBITDA (excluding share-based payment, exceptional items and other income) was $17.9 million (2015: $16.6 million), reflecting growth of 7.0% and 7.8%, respectively. Profit before tax was $7.1 million (2015: $7.2 million).

Operationally, previous investment in the Group’s infrastructure continues to deliver improved efficiencies and capabilities which allow us to provide, we believe, world-class services to our growing client base. The Group performed well in each of its chosen geographies with a strong improvement in our Offshore operations in the Philippines. We also expanded our business into the Nearshore regions of Nicaragua and Jamaica launched mid-year and then took the strategic decision to invest further in our Jamaica facility, following greater than expected client demand. Whilst this investment resulted in an increase in capex and impacted negatively on EBITDA, the investment should lead to increased revenues and margins in fiscal year 2017 and beyond. A further pleasing trend, now consistently represented across reporting periods, has been the winning of new blue chip clients. We believe this highlights IBEX’s growing presence as the provider of choice amongst the most successful class of global businesses.

Dividend

The Board hereby indicates its intent to pay final a dividend of 6.6 cents per share, representing a total dividend for the year of 11.7 cents per share. The final dividend will be declared ahead of the Annual General Meeting, and expected to be paid before the end of the calendar year, in line with previous periods.

Share Buyback

In accordance with the terms of the general authority to make market purchases of the Company’s own shares granted to it by shareholders of the Company on 20 November 2015, and the announcement made by the Company on 24 August 2015 to extend the period for making purchases of its own shares until such time as the Board shall choose to terminate for a total up to $1.0 million, the Company acquired for cash in the market 39,082 ordinary shares in the capital of the Company for treasury from 19 March 2015 to 30 June 2016 at a price of 72 to 130 pence per share. IBEX will continue to make additional purchases of its own shares in line with the above general authority where the Board considers that it is appropriate to do so. The buyback affirms the Board’s confidence in the Group’s prospects and market position.

Chairman’s Statement

4 5

For the year ended 30 June 2016

Management and Staff

Given the nature of our business, IBEX’s success depends on the continued dedication and hard work of its employees at all levels across the Group, from the Board to our contact centre workers who provide excellent service to our client’s end customers. I would like to thank all IBEX employees for their continuing commitment to our ethos and congratulate them on their collective achievement as we continue to drive our business forward.

Corporate Governance

The Board remains focused on strong corporate governance, including nurturing a culture in which our people behave in accordance with our values, which is fundamental to building a business that can deliver sustainable, profitable growth. I believe that our continued commitment to business integrity, sustainability and governance is important to our business.

The Company’s statement on corporate governance can be found in the Corporate Governance Report on pages 24 to 25.

IBEX is well-positioned to continue on its successful path and deliver world-class services for clients, opportunity for employees and growing shareholder value and returns. We look forward to the future with confidence.

Best regards,

Muhammad Ziaullah Khan ChishtiChairmanDate: 27 September 2016

Chairman’s Statement

6

For the year ended 30 June 2016

IBEX Group (“IBEX Global”, “IBEX”, “we”, or “our”) is a global provider of customer interaction solutions with facilities in the United States, Philippines, the United Kingdom, Pakistan, United Arab Emirates, Senegal, Jamaica and Nicaragua servicing Fortune 1000 and industry-leading companies around the world. Its service offerings include business and consumer customer care support, inbound and outbound telesales and technical support services. The Company provides these across an Omni Channel medium including voice, chat, email, SMS and social media. IBEX Group also offers enabling technology solutions including Intelligent Call Routing powered by Afiniti,Interactive Voice Response (IVR) and a suite of outbound dialers.

Business and Financial Review

IBEX delivered a strong performance, both operationally and financially, during the fiscal year 2016. Operational improvements and strategic investment not only helped us to achieve significant increases in both revenues and profitability for the year under review but have also placed us in a strong position for further, continued growth in the years to come. The Group’s organic growth, consistently delivered over successive periods, has continued to outperform industry averages and reflects the advantages of our business model. As a Group we are focused on enhancing IBEX’s position as preferred BPO provider verses our larger competitors by delivering superior services to our clients and maintaining high levels of client satisfaction. We repay the confidence they show in us by helping them to better service their own end customers. This approach not only grows volumes with existing clients but also provides the Group with a steady stream of new client wins.

Key Financial Performance Indicators (KPIs)

The principal KPIs used by the Board in measuring the performance of the Group continue to be Revenue, Cost of Sales, Selling, General & Administrative (SG&A) expenses, Adjusted EBITDA, Net Income and Net Debt.

It is important to note that the comparative figures for 2015 included considerable one-off project revenues of $5.2 million. Therefore, we have also included the comparative figures excluding those revenues in the proforma column below to provide an illustration of the ongoing, repeatable business of the period against 2015.

Strategic Report

6 7

For the year ended 30 June 2016

Proforma*

30 June 2016 30 June 2015 30 June 2015Continuing Operations $’000s $’000s $’000sRevenue 255,510 238,806 233,590Cost of sales 213,225 200,027 200,027Less depreciation and amortisation (9,080) (6,946) (6,946) 204,145 193,081 193,081

Adjusted gross profit 51,365 45,725 40,509Adjusted gross profit margin 20.1% 19.1% 17.3%

SG&A 34,539 30,017 30,017Less depreciation and amortisation (1,103) (851) (851) 33,436 29,166 29,166Adjusted EBITDA 17,929 16,559 11,343Adjusted EBITDA margin 7.0% 6.9% 4.9%Depreciation and amortisation,

exceptional items, finance costs, share based payment, income tax and other income 11,443 10,146

Net income 6,486 6,413Net income margin 2.5% 2.7%* excluding $5.2 million one-off project revenue relating to expansion of one of major clients

30 June 2016 30 June 2016$’000s $’000s

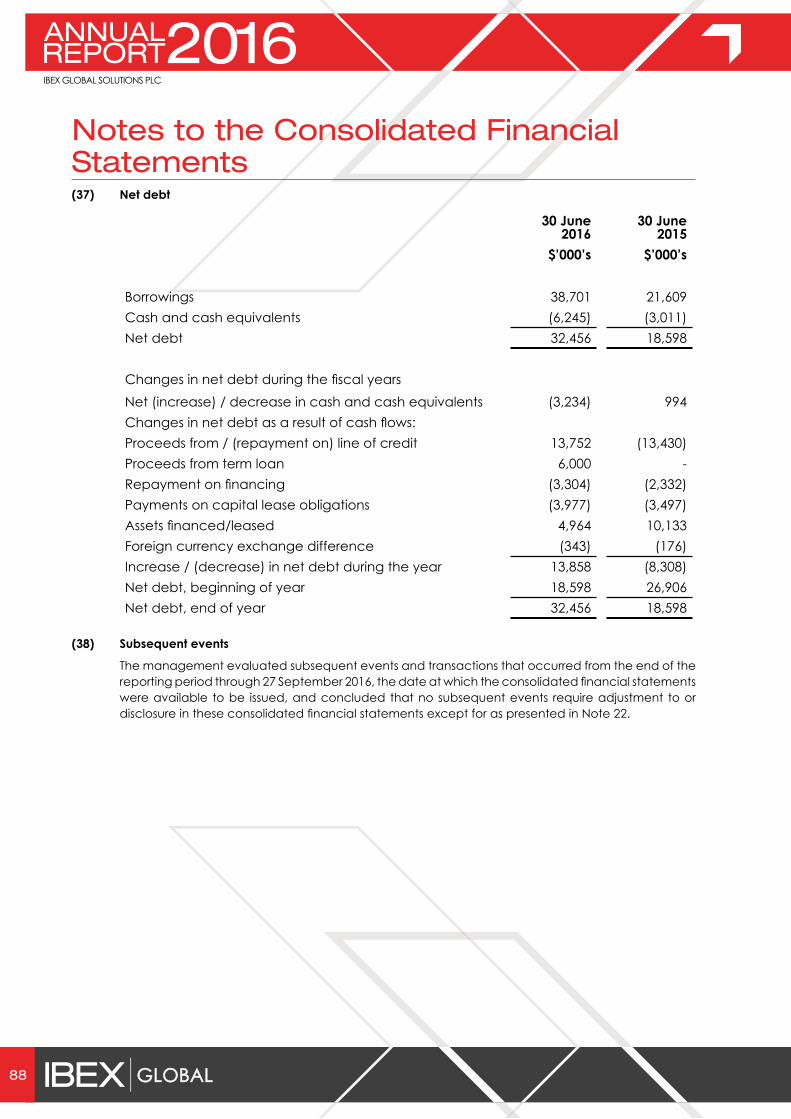

Borrowings 38,701 21,609Cash and cash equivalents (6,245) (3,011)Net debt 32,456 18,598

The Income Statement KPIs above are in line with the Board’s expectations.

Revenue for the year grew 7.0% to $255.5 million (2015: $238.8 million), or by 9.4% when excluding one-off items in the prior year (2015: $233.6 million). Whilst the growth in revenues was driven primarily by increasing business from our existing client base, of which our top four clients grew at 5%, the overall percentage of revenue contributed by them decreased slightly, a trend that we will look to continue as we attract further clients across various geographical and industrial verticals.

Adjusted EBITDA was 7.8% ahead of last year at $17.9 million (2015: $16.6 million). The main reason for this is the delivery against the Group’s strategic objectives which has resulted in improved operations, driving greater efficiencies and also in concentrating on higher margin areas of growth. The Company sees the expansion of its presence in both the Offshore and Nearshore markets as a key part of its strategy to achieve double digit Adjusted EBITDA margins and will look to build a greater proportion of business in its Offshore and Nearshore markets.

Strategic Report

8

For the year ended 30 June 2016

As announced on 14 July 2016, Adjusted EBITDA was impacted by two factors, the Group’s strategic decision to build its own facility in Jamaica in the fourth quarter to cater for excess client demand, and separately a merger between two existing clients which created higher than anticipated operating costs while we converted to a new integrated delivery model in the US region in the second half of the year. The Group expects to benefit from the Jamaica investment from the current period onwards, whilst the costs relating to the merger were a one-off event.

Profit before tax for the year slightly declined to $7.1 million; however on a proforma basis excluding one-off items, increased 255% (2015: $7.2 million) with earnings per share slightly higher than the prior year at 16.37 cents (2015: 16.19 cents). Net debt (third party borrowings less cash and cash equivalents of $6.2 million) at the end of the year increased to $32.5 million (2015: $18.6 million), primarily through greater utilisation of line of credit due to decelerated receivables towards the close of financial year.

Operational Review

The Company has stated its target of achieving double digit EBITDA margins while developing the Company into a more repeatable and predictable business. I am pleased to report that we have made solid progress on these fronts. Importantly, as well as delivering improved financial performance for the year under review we believe we have made strategic investments in the business which will continue to provide further improvements to both the top and bottom line in the years to come.

In particular, the Group has had great success in improving and expanding its Offshore and Nearshore operations with over 1600 seats of new capacity, both of which contribute higher margin. Our sales and client facing teams have had great success in selling over 75% of this new capacity.

Nearshore operations were successfully established in the year in both Jamaica and Nicaragua with two blue chip clients launching in each of these territories with over 1100 seats of new capacity. Our Jamaica operations were initially established in conjunction with a partner. However, it soon became evident that the opportunity in that geography was significant enough to warrant further investment. As such, the Group took the strategic decision to exit its partnership relationship with a local Jamaican operator and build its own 720 seat facility which became operational on 1 July 2016. Whilst this had an impact on the year’s EBITDA performance as a result of paying higher fees to the partner for the early exit and the associated costs for the buildout of our new facility, we believe it will prove of great benefit over the coming years. The facility provides IBEX with additional capacity to look after additional client operations in the current period and beyond with minimal additional capex required. Our Nicaragua business operations, with 450 seats of capacity, extends our capabilities to provide very good bilingual English and Spanish services (a key offering to clients providing goods or services to the Hispanic population) and has gone through successful launches whilst having ample capacity for growth for FY17.

In total, revenues from the Offshore and Nearshore operations totalled 39% of Group revenue compared with 28% in 2015. In order to achieve our target of double digit EBITDA margins, the Group will look to further increase the proportion of Group revenue that comes from Offshore and Nearshore operations, both through increasing the volume of work executed and clients in those geographies but also through maximising the efficiency and output of our US operations.

Our International business made good strides as well. In the second half of the fiscal year, we began efforts in transforming our Senegal operations to be a new, low cost alternative to support the French market. We believe this market to be a viable alternative to the Tunisia and Moroccan geographies with competitive labour rates, great French speaking skills, and limited competition. Investments were also made in improving and expanding our facilities in Pakistan. These investments paid off quickly as we were able to win significant business with a major mobile/telco operator in Pakistan at the end of the period which we expect to make a positive impact in the current period.

Strategic Report

8 9

For the year ended 30 June 2016

The Company also made great strides in improving important operational KPI’s across the Group. Our agent employee satisfaction – the key driver for success – for FY16 measured at 92% companywide with the Philippines leading the way at 96% satisfied. This stronger focus on employee engagement in particular at our Offshore operations in the Philippines helped to greatly improve our agent retention rates, which naturally resulted in a much better performance. We believe that during the course of this year we have been able to build our Philippines operations into being best-in-class and we are confident that we will continue to see a strong performance in the coming years.

As the Group continues to grow and expand the vertical and geographical markets which we serve, it is important that we continue to invest into the business and get the right experience and talent in place. I am therefore delighted that on 17 August 2016 Bruce Dawson was appointed as our Chief Sales and Client Services Officer. Bruce joined us from Atento, one of the major global players in our industry, where he was Director of Nearshore and US. Bruce’s experience will help us to build an industry best sales engine and client management model whilst our ability to attract somebody of his calibre also underlines our growing standing in the market place. This key appointment will enable Julie Casteel to focus on Strategic Client Relationships and Marketing for the Company as we continue to define our unique position in the market.

Analysis of our revenue growth by clients shows a pleasing mix of additional work by our existing client base, which we believe reflects their growing confidence in our abilities, as well as a number of new clients, which will support our growth and performance beyond the current reporting period and enable us to become less dependent on our top few clients.

With regards our existing client base, revenue growth was underpinned by:

• A global telecommunications provider where we were able to expand geographically into the Philippines and Nicaragua as well as expand Line of Businesses (LOBs) support. The result was a near threefold increase in volume and agents and was pursuant to a series of acquisitions by our client.

• A leading client in the television services and broadband internet industry expanded its business sourced from IBEX by adding a supplemental line of business serviced by the Group’s US and Philippines sites as well as launching in its new Jamaica site.

Of note within the new customer wins, contracts were signed with four large companies, spanning the insurance, home solutions and transportation services industries. Several of these new clients have already expanded with us into new geographies. These wins continue to highlight our value proposition of delivering great performance for our clients across many different markets at competitive price points. We remain committed to our investment in new business development across a diversified set of verticals and we will look to grow our base of new clients in the coming quarters.

More widely, IBEX’s remains committed to its business model - what we call the virtuous cycle. This is the sourcing of front-line agents of unparalleled quality, delivering superior performance in our service offering and therefore growing the delivery volumes with the existing client base. IBEX also invests in an on-going, robust business development effort in order to win a regular stream of new clients and we aim to repeat this cycle, year-on-year.

IBEX benefits from a lean, efficient operating overhead structure. Our SG&A adjusted for depreciation is at 13.1% of revenues, which is generally lower than the 15-28% expected from our competitors. Consequently, IBEX has a strong operating leverage associated with its business model. This, coupled with a focus on the excellence of our operational execution, means that clients entrust greater portions of their outsourcing spend to IBEX.

Strategic Report

10

For the year ended 30 June 2016

Our Marketplace and Outlook

The customer contact management industry is highly fragmented. The size of the outsourced portion of the customer contact management industry worldwide was estimated at approximately $64.0 billion in 2014, according to International Data Corporation (“IDC”), an industry research firm. IDC also estimates that the outsourced portion of the customer contact industry is expected to grow to approximately $81.0 billion by 2018, a compound annual growth rate of 6.1% from 2014 to 2018. According to Ovum, an industry research firm, it is estimated that no single outsourcer has more than five percent of the total agent positions worldwide.

The Board believes that IBEX provides the ideal alternative to the largest providers in the industry with our extensive footprint, robust offerings, exceptional service delivery model, complemented with speed and flexibility. As a result over the last several years, IBEX has consistently achieved greater than market growth and we anticipate this year will provide further opportunities. Our core clients continue to deliver growing volumes and additional services to us and we remain confident that our sales and client teams will deliver new client wins which will diversify our revenue streams, in line with our strategy.

The improvement in our Philippine operations has been pleasing and we are excited by the opportunities available at our Nearshore operations. Additionally, our International operations should benefit further in the current fiscal year from the launch with a major mobile/telco client in Pakistan which took place in June 2016. The increased capex investment this year should benefit the Group in the coming years as we fill the additional capacity it has created. Whilst we would expect capex spend to be lower in the current fiscal year, the Board will continue to take advantage of strategic opportunities which present themselves, such as our decision to build our own facility in Jamaica, to maximise the benefit for all stakeholders in the coming years.

We have a positive trajectory as we move into the new fiscal year. The success that we had in engineering a stronger business and management team is positioning us for success in fiscal year 2017. Whilst our clients continue to refine their strategies and their geographies within which they choose to operate, we believe that the overall business is on a good footing to meet our client requirements. We anticipate the majority of our growth to be driven in our Offshore and Nearshore regions, and the investments we have made to strengthen our sales team are seeing early positive returns. In early August, we launched in the Philippines with a new strategic client who is a leader in the Television and Media services. Additionally, we are gearing up for a major launch in our Jamaica centre with a Fortune 25 client in late September. Whilst these are new relationships, it is reinforcement that our value proposition is strong, our reputation is growing, and our future is very bright.

The Board of IBEX recognises that changes to the macro-backdrop can quickly affect the business. Whilst regulatory and legislative issues, the 2016 U.S. Presidential election, and various new minimum wage statutes at state and federal levels may impact on the US economy, we are confident in our business and our team’s ability to successfully deal with any challenges we encounter and continue to build upon our business.

Our goal is to continue to grow faster than the market whilst improving our bottom line performance. We firmly believe we can deliver on this. The Group has begun the new fiscal year well and with our focus on people, product and execution, the Board looks forward to the future with confidence.

Our workforce continues to be our most critical asset in delivering outstanding results for our clients. Our success depends on our growing network of associates, which currently numbers more than 15,500 across the world, and we thank them all for their passion in delivering exceptional services. IBEX will continue to invest in the talents and skill sets of our world-class workforce and provide employees with the best opportunities to reach their ambitious professional goals. We believe that a commitment to our people is a commitment to performing extremely well for our clients.

Strategic Report

10 11

For the year ended 30 June 2016

Principal Risks and Uncertainties

The Group cannot be certain that its business strategy will be successful or that it will successfully address these or other risks that may become material. The Group’s failure to address any of the risks described below could have an adverse effect on its business.

Client Concentration

The Group’s business relies on relationships with a limited number of clients and any deterioration of the Group’s relationship with any particular client could have a material adverse effect on the Group’s performance. Furthermore, mergers and acquisitions associated with IBEX Group’s client base could have a material adverse effect on the Group’s performance. Our relationships with our largest clients have multiple engagements, span many geographies and sites and across several lines of business. The contracts we have typically have different termination dates. That being said, although we have a good track record of contract extensions and evergreening, there can be no assurances this will continue.

As such, the Company has made client diversification one of its most important platforms. The Company’s executive management and Board continually monitors the progress of new client wins and the performance and health of the relationships with its largest clients.

Tax

IBEX enjoys an overall effective tax rate of 9-16 percent, given a tax-efficient corporate and legal structure. There is a risk that amounts paid or received under intra-group arrangements in the past or in the future could be deemed for tax purposes to be lower or higher, as the case may be, or be disregarded for the purposes of calculating tax, which may increase the Group’s taxable income or decrease the amount of relief available to the Group with a consequential material negative effect on its financial and operating results.

Following the UK’s decision to exit the European Union (EU), management is in the process of evaluating the overall tax impact for the Group. There is some uncertainty as the UK still has two years to finalise the details and negotiate its trade agreements before it withdraws from the EU. At this stage, management does not expect a significant increase in overall tax rate subsequent to the UK’s exit from the EU.

Operations in International Markets

As the Group has its operations in overseas territories, the Group has and expects to become increasingly subject to diverse local legal and regulatory requirements. Violations of these laws and regulations could result in fines and/or criminal sanctions against the Group, its officers and employees, as well as challenges to its ability to conduct its business and its ability to offer products and services in one or more countries. Such challenges could delay or prevent potential acquisitions and materially damage the Group’s reputation, brand, international expansion efforts, ability to attract and retain employees and operating results.

The Group’s success depends, in part, on its ability to anticipate these risks and manage these difficulties.

The Group is also subject to a variety of other risks and challenges in operating in various countries, including but not limited to: challenges caused by distance, language and cultural differences; general economic conditions in each country or region; fluctuations in currency exchange rates; regulatory changes; political unrest, terrorism and the potential for other hostilities; longer payment cycles and difficulties in collecting debts; overlapping tax regimes; the ability to repatriate funds held by international subsidiaries at favourable tax rates; difficulties in transferring funds from certain countries; and reduced protection for intellectual property rights in some countries. If the Group is unable to manage the international aspects of its business, its operating results and overall business may be significantly and adversely affected.

Strategic Report

12

For the year ended 30 June 2016

As such, the Group continues to monitor the relevant regulatory, geopolitical and other risk factors related to our operations outside of the United States. Additionally, we work closely with our clients to de-risk this by placing business across multiple regions, markets, and sites. However, we cannot assess with certainty what impact such risks are likely to have over time on business and can provide no assurance that we will always be able to mitigate these risks successfully and avoid material impact to our business and results of operations.

Ability to Recruit, Compensate and Retain Skilled Personnel

The Group’s performance is dependent on the talents and efforts of its agents; therefore the ability to compete effectively in the Group’s business and expand into new businesses and geographic areas depends on the ability to attract new talent and retain and motivate existing employees. Factors that can affect the Group’s ability to attract and retain employees include the compensation and benefits offered to employees as well as its reputation as a successful business in fairly treating and motivating its employees. Competition in the call centre industry and in the geographies where the Group’s call centre businesses are located can be intense. Although the Group believes that it has appropriate incentive structures and employee engagement to attract and retain the calibre of employees necessary to ensure the efficient management and development of the Group; any difficulties encountered in hiring and retaining appropriate employees may have a detrimental effect on the trading performance of the Group.

Changes in federal, state, local and international laws or failure to comply with certain laws could increase costs, reduce margins and lower sales.

The Group’s business is subject to laws and regulations in the United States and other countries in which it operates. Significant workforce-related legislative changes could increase expenses and adversely affect operations. In addition, the Group’s failure to comply with applicable laws and regulations including wage and hour laws, data security, the Foreign Corrupt Practices Act and local anti-bribery laws, could subject the Group’s business to legal risk including government enforcement and class action civil litigation, which could adversely affect operations by increasing costs, reducing margins and lowering sales. Changes in U.S. federal, state and international laws relating to outsourcing of jobs to foreign countries may adversely impact our ability to provide services from these locations. The Group’s compliance group and outside advisors monitor the changing laws, where possible.

Rapid growth

In order to manage the further expansion of the Group’s business and the growth of its operations and personnel, the Group may need to expand and enhance its infrastructure and technology, and improve its operational and financial systems and procedures and controls from time to time in order to be able to match that expansion, as well as procure working capital financing. There can be no assurance that the Group’s current and planned personnel, infrastructure, systems, procedures and controls will be adequate to support its expanding operations in the future or that the Group will be able to source the working capital financing required for further growth. If the Group fails to manage its expansion effectively, its business, operations and prospects may be materially and adversely affected. As such the Company will be moving its infrastructure to a hardened, commercial grade co-location facility that will provide significant expandability and 99.999 uptime.

Technological changes and advances

The industry has a history of technological advances to improve the customer experience or costs associated with providing services. Technological advancements in voice recognition software, web-based help, chatbots, and call avoidance technologies, have the potential to adversely impact call volume. As these technologies come to market for simple customer transactions, this will place requirements on us to provide more complex services and will require us to provide adequately training personnel.

Strategic Report

12 13

For the year ended 30 June 2016

Competition

Current and potential competitors of the Group may have substantially greater financial, technical and marketing resources, longer operating histories, larger customer bases, greater name recognition and more established relationships than the Group and so may be better able to compete in the Group’s target markets.

Risks Relating to Data Security and Potential Cyber Attacks

The Group’s operations depend on a complex combination of technology networks and systems, comprising hardware, software, and telecommunications including dependency on third-party systems and services. Internal or external cyber attacks on any the Group and/or any third party network and/or system could disrupt call centre operations and adversely affect the Group’s ability to meet key performance standards, which could result in liability under its client service agreements or in loss of clients. Moreover, the Group’s business involves use, storage and transmission of data about clients, customers of clients, and employees. In addition, laws governing data privacy are continually evolving and sometimes conflict among various jurisdictions where the Group operates. Negligent or intentional breach of data security controls, or misuse or misappropriation of confidential data, or failure to comply with applicable law, could result in damages, fines, penalties or criminal prosecution. Any such breach, misuse or misappropriation could also result in negative publicity and damage to reputation, loss of clients, or other material adverse effects. The Group has a security platform protecting its systems and confidential data, and it updates the platform periodically. The platform includes compliance with the PCI Data Security standard in the Group’s call centres locations. However, it is possible that the security platform may not prevent improper access to or disclosure of confidential data including over the internet. The Group maintains cyber insurance coverage, and reviews and updates the coverage at least annually. There can be no assurance, however, that available insurance will be adequate to cover losses that may occur.

In March 2015, IBEX US received a notice from one of its major clients of a claim for indemnification under applicable client service agreements. This notice resulted from a data security breach that occurred during late 2014 at one of the Group’s call centres. IBEX and the client had cooperated to investigate the problem and take appropriate remedial action. There was no evidence of any financial loss to any customer of the client. Taking into account the facts and circumstances known at this point, together with applicable insurance coverage, IBEX US believes that this potential indemnity claim should fall within the applicable insurance policy limitations.

Stock Price Volatility

IBEX’s share price has fluctuated in the past and may continue as such in the future in response to various factors. These factors, in addition to reported results of our operations, may include changes in economic, political, social or environmental fabrics of the countries we are situated in, which may or may not be directly related to our business; general or industry-specific market conditions; volatility in major financial markets; revision in trends of risk assumption; fundamental analysis of geographical diversity of our business and segments thereof; regulatory announcements by us or competitors about developments in current business or prospects; projections or speculation about our business or that of competitors by the press or investment analysts; and our ability to generate distributable cash flow to return to our shareholders in the form of dividend at historical or expected levels.

Third Party Service and Outsource Providers

The Group depends on third-party suppliers and outsourcers for a variety of services including our telecommunications and data network. If these third party services were interrupted in the provision of supplies and/or services, it could impact our ability to meet client demand, damage our reputation and client relationships and adversely affect our revenue and profitability.

Strategic Report

14

For the year ended 30 June 2016

Financial Risks

The Group’s activities expose it to a variety of financial risks:

• Interest rate risk

• Foreign currency risk

• Credit risk

• Liquidity risk

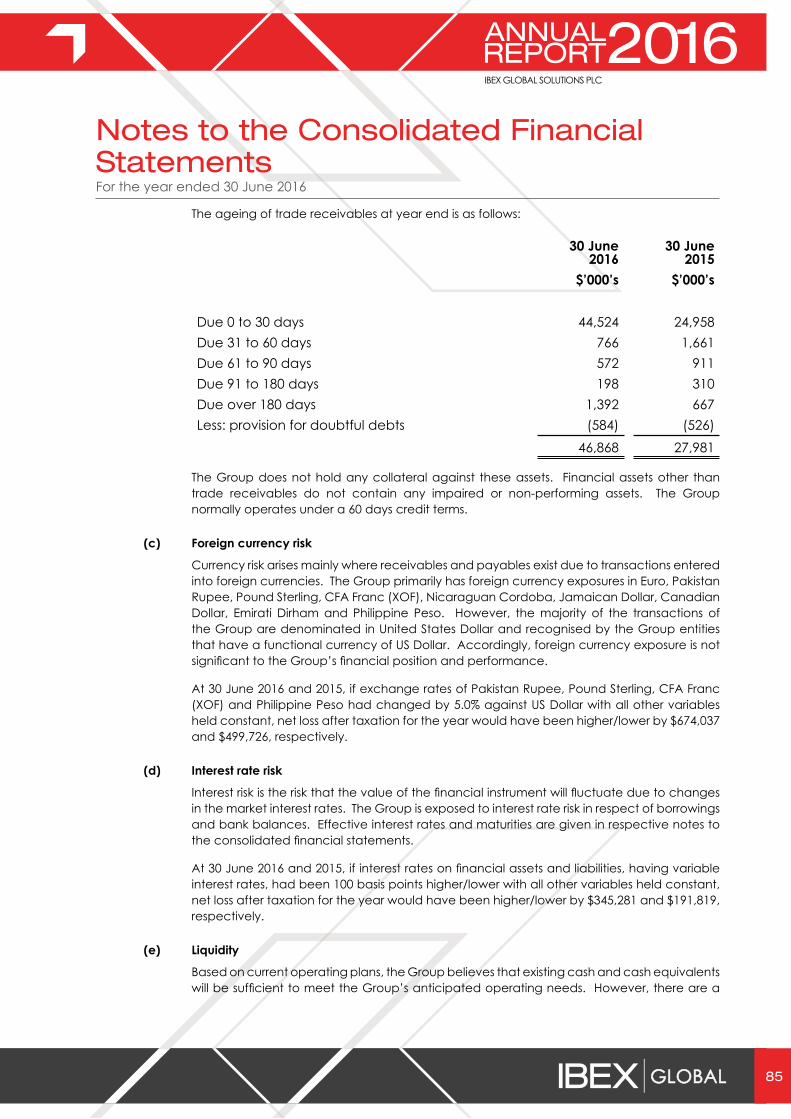

Interest rate risk

Interest risk is the risk that the value of the financial instrument will fluctuate due to changes in the market interest rates. The Group is exposed to interest rate risk in respect of borrowings and bank balances. Effective interest rates and maturities are given in applicable notes to the consolidated financial statements.

Foreign currency risk

Currency risk arises mainly where receivables and payables exist due to transactions entered into foreign currencies. The Group primarily has foreign currency exposures in Pakistan Rupee, Pound Sterling, CFA Franc (XOF), Philippine Peso, Jamaican Dollar and Nicaraguan Cordoba. However, the majority of the transactions of the Group are denominated in United States Dollar (US$) and recognised by Group entities that have a functional currency of US$. Accordingly, foreign currency exposure is not significant to the Group’s financial position and performance.

Concentration of credit risk

Financial instruments which potentially expose the Group to concentrations of credit risk consist primarily of cash and cash equivalents and accounts receivable. The Group’s cash and cash equivalents are held with US and foreign commercial banks. The balance at times may exceed insured limits.

Liquidity risk

The Group leverages the Revolving Line of Credit with PNC Bank, National Association to fund its working capital cycle as necessary. This credit, together with cash generated through operations, enable the Group to meet its working capital needs. In addition, the Group’s receivables financing agreement with Citibank, N.A. has enabled it to accelerate cash collections from a major client during financial year 2016. However, the Group’s operating plan for financial year 2016-17 incorporates a number of business assumptions which may not materialise as expected. As a result, the Group may take necessary measures including seeking additional financing or implementing a reduced spending plan to fund its continued operations.

Risk Management System

The risk management objective of IBEX is to identify, minimize, mitigate and prevent risks within the business (both externally and internally) and within the Company’s various departments such as operations, finance, technology and human resources. The risk practices seek to enhance long-term competitive advantage to the Group and to protect the business and its customers.

Indemnities, Commitments and Guarantees

From time to time, during the normal course of business, the Company may make certain indemnities, commitments and guarantees under which it may be required to make payments in relation to certain transactions. These include, but are not limited to: (i) indemnities to clients, vendors and service providers pertaining to claims based on negligence or wilful misconduct of the Company and (ii) indemnities involving breach of contract, failure of service, data breaches; the accuracy of representations and warranties

Strategic Report

14 15

For the year ended 30 June 2016

of the Company, or other liabilities assumed by the Company in certain contracts including SLA service failures. In addition, the Company has agreements whereby it will indemnify certain officers and directors for certain events or occurrences while the officer or director is, or was, serving at the Company’s request in such capacity. The indemnification period covers all pertinent events and occurrences during the officer’s or director’s lifetime. The maximum potential amount of future payments the Company could be required to make under these indemnification agreements is unlimited; however, the Company has director and officer insurance coverage that limits its exposure and enables it to recover a portion of any future amounts paid subject to standard insurance exclusions. The Company believes the applicable insurance coverage is generally adequate to cover any estimated potential liability under these indemnification agreements. The majority of these indemnities, commitments and guarantees do not provide for any limitation of the maximum potential for future payments the Company could be obligated to make. The Company has not recorded any liability for these indemnities, commitments and guarantees. In addition, the Company has some client contracts that do not contain contractual provisions for the limitation of liability of different types of damages, and other client contracts that contain agreed upon exceptions to limitation of liability. The Company has not recorded any liability with respect to any client contracts under which the Company has or may have unlimited liability.

Incentivising Key Staff

Traditionally, staff churn is a challenge for operators in our industry because the training of staff to make them effective can be both costly and time-consuming. For a BPO solution to be competitive, the staff involved in dealing with customers’ needs must know their business extremely well and be able to deliver our clients’ aspirations for customer service to very high standards, every time.

IBEX understands that the retention and motivation of staff are absolutely crucial to our success. Attrition has a disproportionate impact on Group profitability, both through the cost of replacement training and through foregone margin associated with a departing employee. The Directors believe that employees with longer tenures are more likely to perform better, thereby improving client metrics and more easily growing the Group’s share of the client’s outsourcing spend.

To this end, the salaries we pay are sometimes above the industry average in each country in which we have operations. Additionally, our employees are afforded opportunities to progress their careers as we grow the business. We believe employee career development is inextricably linked to the success of the Group. In order to further enhance these principles, IBEX used the Alternative Investment Market (AIM) admission to offer an equity incentivisation plan. The IBEX equity reward scheme is therefore not limited to the Board and senior management, but is also offered to nearly all manager-level individuals in the organisation. This represents a significant point of differentiation in the BPO marketplace and the overall incentivisation package IBEX Group provides, which will help safeguard the services we offer to our clients.

Customer Service

We are acutely aware that our clients entrust IBEX with key customer support functions, thereby outsourcing mission-critical parts of their business operations. Given the impact we have on our client’s reputation, we know that customer service is a key differentiator in the marketplace, and represents a key aspect of how we manage our business. We are also aware that merely performing against our client’s requirements is the bare minimum of what we can achieve on each client’s behalf.

Therefore, after taking care of our workforce, we turn our attention to outperforming against client requirements. It is this approach, consistently applied, which differentiates us from the competition, and means that household names use us to protect and cultivate their relationships with their end customers. Overall, we want our clients to know that IBEX is dedicated to generating the best outcomes of customer satisfaction on their behalf. In each case, the metrics by which clients measure the value we add to their operations are examined almost daily. We are diligent when it comes to ensuring client satisfaction and the business is set up to improve constantly on our already proven success.

Strategic Report

16

For the year ended 30 June 2016

Technology

IBEX uses state-of-the-art systems to service our clients’ needs and deliver the best possible service for each of them. We have continually improved our infrastructure through investment to make sure that we run as efficiently as possible and provide the exceptionally high levels of service which our clients have come to expect.

The world of technology and connectivity moves very quickly. To that end, IBEX sees the improvement of its systems as an on-going priority for the Group. By applying the latest technology developments available to us, we can continually ensure that our system capability is world class. We not only make sure that we are operating existing technology as efficiently as possible, but we are always looking for ways in which we can innovate within our client delivery models. This provides us with a strategic advantage over our rivals and keeps us competitive in the market.We would like to thank our shareholders, clients, employees and Board members for your confidence and support.

The strategic report was approved by the Board of IBEX Global Solutions Plc and signed on its behalf by:

Robert Dechant Karl GabelChief Executive Officer Chief Financial OfficerDate: 27 September 2016 Date: 27 September 2016

Strategic Report

16 17

For the year ended 30 June 2016

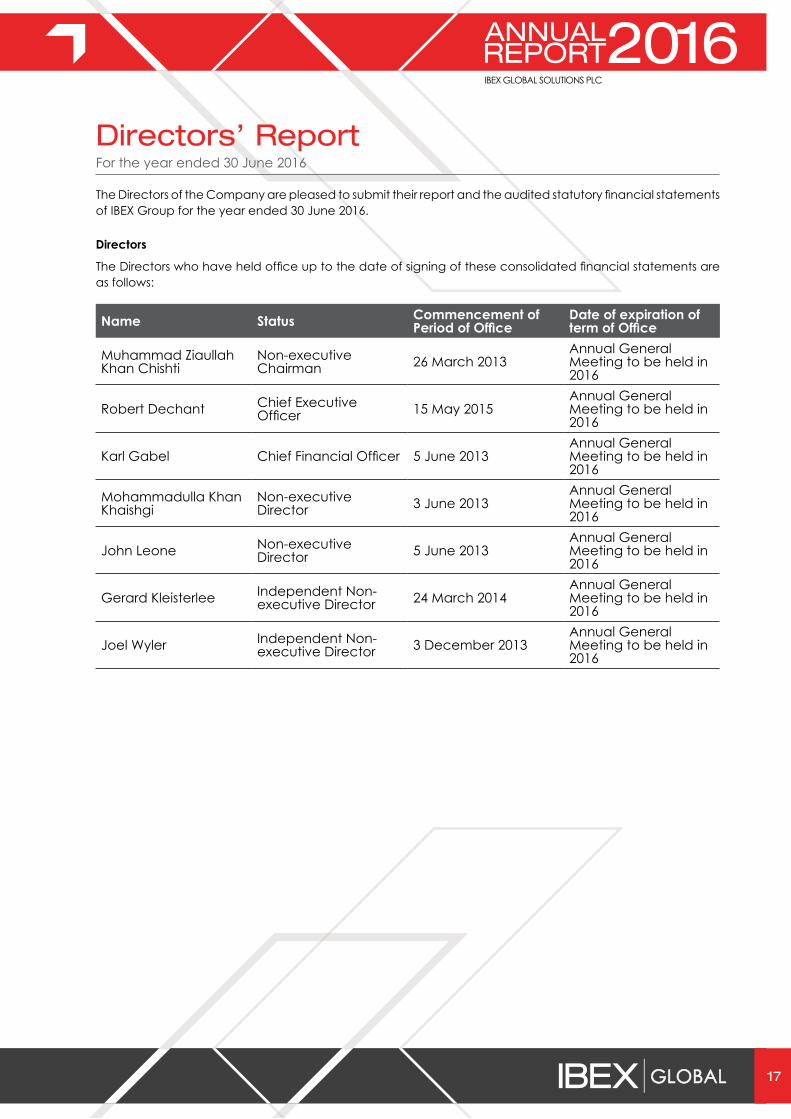

The Directors of the Company are pleased to submit their report and the audited statutory financial statements of IBEX Group for the year ended 30 June 2016.

Directors

The Directors who have held office up to the date of signing of these consolidated financial statements are as follows:

Name Status Commencement of Period of Office

Date of expiration of term of Office

Muhammad Ziaullah Khan Chishti

Non-executive Chairman 26 March 2013

Annual General Meeting to be held in 2016

Robert Dechant Chief Executive Officer 15 May 2015

Annual General Meeting to be held in 2016

Karl Gabel Chief Financial Officer 5 June 2013Annual General Meeting to be held in 2016

Mohammadulla Khan Khaishgi

Non-executive Director 3 June 2013

Annual General Meeting to be held in 2016

John Leone Non-executive Director 5 June 2013

Annual General Meeting to be held in 2016

Gerard Kleisterlee Independent Non-executive Director 24 March 2014

Annual General Meeting to be held in 2016

Joel Wyler Independent Non-executive Director 3 December 2013

Annual General Meeting to be held in 2016

Directors’ Report

18

For the year ended 30 June 2016

As at the date of this document, the following options have been granted to Directors of the Company under the Company Stock Plan 2013:

NameNumber of share options

Percent of enlarged

share capital at 30 June

2016

Vesting schedule Exercise period (from)

Exercise Price

Robert Dechant 700,000 1.8%

175,000 options vested on 11 May 2016; 14,584 stock

options vesting monthly until 11 May 2019

11 May 2015 $1.88

Karl Gabel 442,307 1.1% 442,307 options vested on 30 June 2015 05 June 2013 $1.55

Gerard Kleisterlee

50,000 0.1%

12,500 options vested on 01 December 2014; 1,042 stock

options vesting monthly through 30 November

2017; 1,030 options vest 31 December 2017

01 December

2013$1.55

50,000 0.1%

12,500 options vest on 22 December 2016

with 1,042 stock options vesting monthly through 22 November 2019; 1,030

options vest 22 December 2019

22 December

2015$1.64

Joel Wyler

50,000 0.1%

12,500 options vested on 01 December 2014; 1,042 stock

options vesting monthly through 01 November

2017; 1,030 options vest 01 December 2017

01 December

2013$1.55

50,000 0.1%

12,500 options vest on 22 December 2016

with 1,042 stock options vesting monthly through 22 November 2019; 1030

options vest 22 December 2019

22 December

2015$1.64

Directors’ Report

18 19

For the year ended 30 June 2016

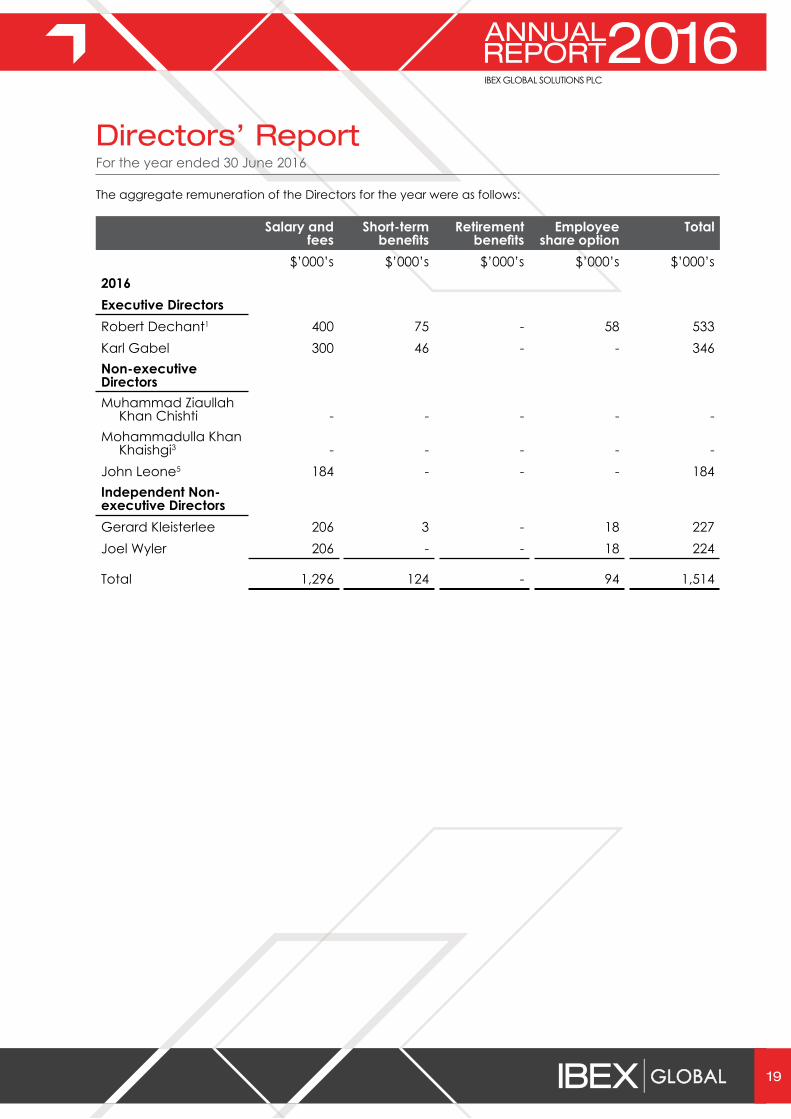

The aggregate remuneration of the Directors for the year were as follows:

Salary and fees

Short-term benefits

Retirement benefits

Employee share option

Total

$’000’s $’000’s $’000’s $’000’s $’000’s2016Executive DirectorsRobert Dechant1 400 75 - 58 533Karl Gabel 300 46 - - 346Non-executive DirectorsMuhammad Ziaullah

Khan Chishti - - - - -Mohammadulla Khan

Khaishgi3 - - - - -John Leone5 184 - - - 184Independent Non-executive DirectorsGerard Kleisterlee 206 3 - 18 227Joel Wyler 206 - - 18 224

Total 1,296 124 - 94 1,514

Directors’ Report

20

For the year ended 30 June 2016

Salary and fees

Short-term benefits

Retirement benefits

Employee share option

Total

$’000’s $’000’s $’000’s $’000’s $’000’s2015Executive DirectorsRobert Dechant1 58 136 - 8 202Karl Gabel 300 45 - 4 349Steve Kezirian2 699 792 - 46 1,537Mohammadulla Khan

Khaishgi (as Interim CEO)3 150 - - - 150

Non-executive DirectorsMuhammad Ziaullah Khan

Chishti - - - - -Mohammadulla Khan

Khaishgi3 - - - - -Tim Kelly4 62 - - 3 65John Leone5 120 - - - 120Independent Non-executive DirectorsGerard Kleisterlee 150 5 - 69 224Joel Wyler 225 - - 69 294

Total 1,764 978 - 199 2,941

1Appointed 15 May 20152Left his post as Director effective 7 October 20143Interim CEO from 3 November 2014 to 30 April 20154Left his post as Director effective 13 October 20145Remuneration of John Leone paid to Pine Bridge

Stephen M. Kezirian resigned as CEO and left his post as Executive Director effective 7 October 2014, and by agreement provided transition assistance through to 31 December 2014. The financial terms of the aforementioned agreement have been reflected in the disclosure above. Mr. Kezirian’s options continued vesting until the day after the first anniversary of resignation date, and Mr. Kezirian’s vested options were exercisable up until 30 April 2016 at which time the options expired. Mohammed Khaishgi, a Non-executive Director, succeeded Mr. Kezirian as interim CEO. Robert T. Dechant became CEO and an Executive Director on 1 May 2015. Mr. Khaishgi continues as a Non-executive Director.

Employment of Disabled Persons

The Group’s policy is to comply with applicable laws regarding recruitment and employment of disabled workers. Arrangements are made, wherever possible, for making reasonable accommodations for employees who become disabled.

Directors’ Report

20 21

For the year ended 30 June 2016

Political Donations

No political donations were made by the Parent Company or the Group during the fiscal year 2016 (2015: nil).

Going Concern

The Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. Thus they continue to adopt the going concern basis of accounting in preparing the annual consolidated financial statements. If for any reason the Group is unable to continue as a going concern, it could have an impact on the Group’s ability to realise assets at their recognised values and to extinguish liabilities in the normal course of business at the amounts stated in the consolidated financial statements.

Financial Instruments

The Group’s financial instruments comprise cash and cash equivalents, bank loans, finance leases and financing arrangements together with various items such as receivables and payables that arise directly from operations. As mentioned in the Strategic Report on page 14, the Group’s activities expose it to a variety of financial risks: market risk (including interest rate risk and foreign currency risk), credit risk and liquidity risk. Additional information on financial instruments is included in Note 35 to the consolidated financial statements.

Purchase of Treasury Shares

In accordance with the terms of the general authority to make market purchases of Holding Company’s own shares granted to it by shareholders of the Company on 20 November 2015, and the announcement made by the Holding Company on 24 August 2015 to extend the period for making purchases of its own shares until such time as the Board shall choose to terminate for a total up to $1.0 million, the Holding Company acquired for cash in the market a total of 39,082 ordinary shares as of 30 June 2016. The acquired shares were held in treasury.

Directors’ Report

22

For the year ended 30 June 2016

Below are the details of treasury shares as of the year ended 30 June 2016.

Acquisition date No. of Shares Price per share (in

US$)

Total price (in US$)

19 March 2015 13,888 1.08 14,93028 May 2015 749 1.24 92829 May 2015 700 1.31 9173 June 2015 725 1.56 1,1319 June 2015 745 1.80 1,34230 June 2015 725 1.98 1,4363 July 2015 725 2.00 1,44824 July 2015 725 1.96 1,4245 November 2015 725 2.00 1,45210 November 2015 740 1.96 1,45112 November 2015 735 1.97 1,44919 November 2015 730 1.91 1,39624 November 2015 700 1.91 1,3371 December 2015 745 1.92 1,4308 December 2015 725 1.66 1,20311 December 2015 1,000 1.67 1,66914 December 2015 2,000 1.67 3,35015 December 2015 2,000 1.67 3,33716 December 2015 2,000 1.68 3,36517 December 2015 2,000 1.68 3,36718 December 2015 2,000 1.64 3,28621 December 2015 2,000 1.56 3,12722 December 2015 2,000 1.67 3,338Total 39,082 58,113

Auditors

A resolution proposing the re-appointment of Grant Thornton UK LLP will be put to the shareholders at the forthcoming Annual General Meeting.

Directors’ Report

22 23

For the year ended 30 June 2016

Statement of Disclosure to Auditors

Each of the persons who is a Director at the date of approval of this report confirms that:

a. So far as they are aware, there is no relevant audit information of which the Company’s auditors are unaware; and

b. They have taken all the steps that they ought to have taken as Directors in order to make themselves aware of any relevant audit information and to establish that the Company’s auditors are aware of that information.

IBEX owes its continuing success not just to the management team but also to our employees across all roles within the Group. The quality and dedication of our staff is what differentiates us from the competition and delivers the best, most well informed and professional service for our client base. I would therefore like to thank every member of the IBEX team for their on-going support and efforts. Galvanised by our successful initial public offering on AIM, we remain true to our core values (Integrity, Transparency, Excellence and Respect) and look forward to a bright future for the entire IBEX family.

By order of the Board

Robert Dechant Karl GabelChief Executive Officer Chief Financial OfficerDate: 27 September 2016 Date: 27 September 2016

Directors’ Report

24

For the year ended 30 June 2016Corporate Governance Report

Financial Aspects of Corporate Governance

The Directors recognise the importance of sound corporate governance and confirm that they intend to comply in all material respects with the Corporate Governance Guidelines (as devised by the Quoted Companies Alliance or QCA in consultation with a number of significant institutional small company investors), to the extent appropriate for a company of its nature and size. We do not fully comply with the QCA Code, however; and the Board is encouraging, where possible and practicable, for the Company to follow the material recommendations on corporate governance of the QCA for companies with shares traded on AIM.

This approach to corporate governance was proposed by the QCA, as it considers the UK Corporate Governance Code to be inappropriate to many AIM companies. The Corporate Governance Guidelines state that, “The purpose of good corporate governance is to ensure that the company is managed in an efficient, effective and entrepreneurial manner for the benefit of all shareholders over the longer term.” We do not comply with the UK Corporate Governance Code. However, we have reported on our Corporate Governance arrangements by drawing upon best practice available, including those aspects of the UK Corporate Governance Code we consider to be relevant and material to the Group and best practice.

The Board meets at least four times per year to review, formulate and approve the Group’s strategy, budgets, and corporate actions and oversee the Group’s progress towards its goals. It has established audit, nomination and remuneration committees with formally delegated duties and responsibilities and with written terms of reference. From time to time, separate committees may be set up by the Board to consider specific issues when the need arises.

Audit Committee

The audit committee will meet formally at least four times a year and otherwise as required. It will be responsible for ensuring that the financial performance of the Group is properly reported on and monitored, including reviews of the annual and interim accounts, results announcements, internal control systems and procedures and accounting policies, reviewing and monitoring the extent of the non-audit services undertaken by the external auditors and advising on the appointment of external auditors.

The audit committee has undertaken vital tasks throughout the year and safeguards independent oversight of both management and external auditors were exercised.

24 25

For the year ended 30 June 2016

Remuneration Committee

The remuneration committee is expected to meet at such times as required, and not less than twice a year. Executive Directors may attend meetings at the committee’s invitation. The remuneration committee has responsibility for determining, within agreed terms of reference, the Group’s policy on the remuneration packages of senior executives and specific remuneration packages for Executive Directors. This includes agreeing with the Board the framework for remuneration of the CEO, all other Executive Directors, the Corporate Secretary and such other members of the executive management of the Group as it is designated to consider. It is furthermore responsible for determining the total individual remuneration packages of each Director including, where appropriate, bonuses, incentives, pension rights and compensation payments. It is also responsible for making recommendations for grants of options under the Share Option Plans.

The remuneration of Non-executive Directors is a matter for the Board. No Director may be involved in any discussions as to their own remuneration. From time to time, the remuneration committee may consult with shareholders on remuneration matters, regardless of any regulatory requirement or governance guideline recommendation to do so.

The remuneration committee ensures the Group’s remuneration policy and practice align with the Group’s strategy.

Nomination Committee

The Nomination Committee will be an ad hoc committee constituted by the Board as and when required. When constituted it will be chaired by an independent member of the Board. It will have responsibility for reviewing the balance of the Board including its skills and experience, the state of the business and its leadership needs, and give full consideration to succession planning. It will also have responsibility for recommending new appointments to the Board.

Relations with Shareholders

Communication with shareholders is given a high priority by the Board and the Directors are available to enter into dialogue with shareholders. All shareholders are encouraged to attend and vote at the Annual General Meeting during which the Board is available to discuss issues affecting the Company.

The shareholders or potential shareholders of the Company may also request information about the Company through the website www.ibexglobal.com.

Corporate Governance Report

2626

For the year ended 30 June 2016

Directors’ Responsibilities

The Directors are responsible for preparing the Directors’ Report and Strategic Report along with consolidated financial statements of the Group and separate financial statements of the Parent Company in accordance with applicable law and regulations.

Companies law requires the Directors to prepare financial statements for each fiscal year. Under that law, the Directors have elected to prepare consolidated financial statements of the Group and separate financial statements of the Parent Company in accordance with International Financial Reporting Standards (lFRS) as adopted by the European Union. Under UK Companies Law, the Directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Group and the Parent Company and of the profit or loss of the Group and the Parent Company for that period.

In preparing these financial statements, the Directors are required to:

• Select suitable accounting policies and then apply them consistently;

• Make judgments and accounting estimates that are reasonable and prudent;

• State whether applicable accounting standards have been followed subject to any material departures disclosed and explained in the financial statements; and

• Prepare the financial statements on a going concern basis unless it is inappropriate to presume that the Group and the Parent Company will continue in business.

The Directors are responsible for keeping adequate accounting records that are sufficient to show and explain the Parent Company’s and Group’s transactions and which disclose with reasonable accuracy at any time the financial position of the Parent Company and the Group and enable them to ensure that the financial statements comply with the Companies Act 2006. The Directors are also responsible for safeguarding the assets of the Parent Company and the Group and, hence, for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Website Publication

The Directors are responsible for the maintenance and integrity of the corporate and financial information included on the Group’s website. The work carried out by the auditors does not involve consideration of these matters and, accordingly, the auditors accept no responsibility for any changes that may have occurred to the financial statements since they were initially presented on the website. Legislation in the United Kingdom governing the preparation and dissemination of the financial statements may differ from legislation in other jurisdictions.

Statement of Directors’ Responsibilities

26 2726

Independent Auditors’ Report on Group Financial Statements

We have audited the Group financial statements of IBEX Global Solutions Plc for the year ended 30 June 2016 which comprise the consolidated statement of comprehensive income, the consolidated statement of financial position, the consolidated statement of changes in equity, the consolidated statement of cash flows and the related notes. The financial reporting framework that has been applied in their preparation is applicable law and International Financial Reporting Standards (IFRSs) as adopted by the European Union.

This report is made solely to the Company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditor

As explained more fully in the Directors’ Responsibilities Statement set out on page 26, the Directors are responsible for the preparation of the Group financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the Group financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the financial statements

A description of the scope of an audit of financial statements is provided on the Financial Reporting Council’s website at www.frc.org.uk/auditscopeukprivate.

Opinion on financial statements

In our opinion the Group financial statements:

• give a true and fair view of the state of the Group’s affairs as at 30 June 2016 and of its profit for the year then ended;

• have been properly prepared in accordance with IFRSs as adopted by the European Union;

• have been prepared in accordance with the requirements of the Companies Act 2006.

2828

Opinion on other matter prescribed by the Companies Act 2006

In our opinion the information given in the Strategic Report and Directors’ Report for the financial year for which the Group financial statements are prepared is consistent with the Group financial statements.

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

• certain disclosures of Directors’ remuneration specified by law are not made; or

• we have not received all the information and explanations we require for our audit.

Other matter

We have reported separately on the parent company financial statements of IBEX Global Solutions Plc for the year ended 30 June 2016.

Marc SummersSenior Statutory Auditorfor and on behalf of Grant Thornton UK LLPStatutory Auditor, Chartered AccountantsLondonDate: 27 September 2016

Independent Auditors’ Report on Group Financial Statements

28 29

For the year ended 30 June 2016

28

Consolidated Statement of Comprehensive Income

2016 2015Continuing operations Notes $’000’s $’000’sRevenue 5 255,510 238,806Cost of sales 6 (213,225) (200,027)Gross profit 42,285 38,779

Selling, general and administrative Expenses (34,539) (30,017)Share-based payment (90) 162Exceptional item 8 - (1,375)Other income 20 1,255 1,298 Total selling, general and administrative expenses 6 (33,374) (29,932)

Operating profit 8,911 8,847Other expenses

Finance costs 7, 20 (1,767) (1,604)

Income before taxation 9 7,144 7,243

Income tax expense 30 (658) (830)Net income for the year attributable to the equity

holders of the parent 6,486 6,413Other comprehensive incomeItem that will not be subsequently reclassified to profit or

loss -Actuarial gain/(loss) on retirement benefits 132 (225)

Item that will be subsequently reclassified to profit or lossForeign currency translation adjustment (45) (86)

87 (311) Total comprehensive income attributable to equity

holders of the parent 6,573 6,102

Earnings per share attributable to equity holders of the

parent Basic earnings per share (in US$) 31 0.164 0.162

Diluted earnings per share (in US$) 31 0.164 0.162

The accompanying notes are an integral part of these financial statements.

30

For the year ended 30 June 2016

Consolidated Statement of Financial Position

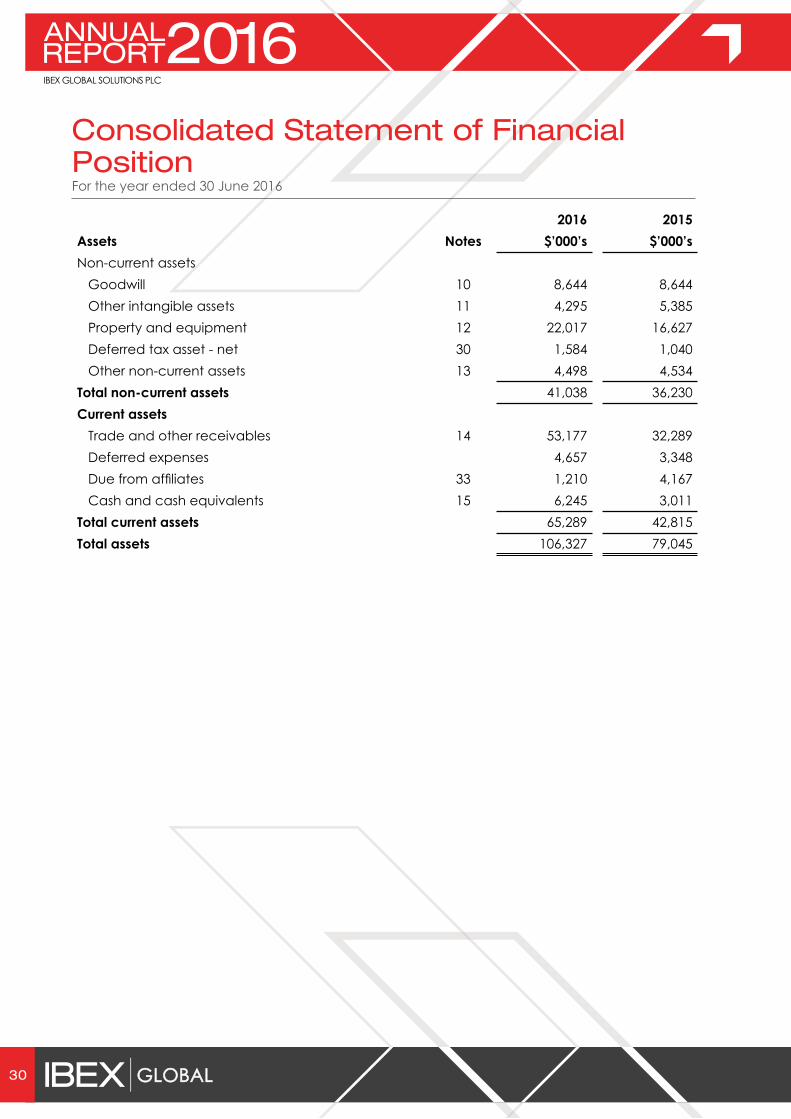

2016 2015Assets Notes $’000’s $’000’sNon-current assets Goodwill 10 8,644 8,644 Other intangible assets 11 4,295 5,385 Property and equipment 12 22,017 16,627 Deferred tax asset - net 30 1,584 1,040 Other non-current assets 13 4,498 4,534 Total non-current assets 41,038 36,230Current assets Trade and other receivables 14 53,177 32,289 Deferred expenses 4,657 3,348 Due from affiliates 33 1,210 4,167 Cash and cash equivalents 15 6,245 3,011Total current assets 65,289 42,815Total assets 106,327 79,045

30 31

For the year ended 30 June 2016

Consolidated Statement of Financial Position

2016 2015Equity and liabilities Notes $’000’s $’000’sEquity attributable to owners of the parent Share capital 16 602 602 Share premium 14,479 14,479 Capital redemption reserve 17 48,530 48,530 Treasury shares (58) (19) Other reserves 1,230 918 Deficit (37,207) (38,986)Total equity 27,576 25,524 Non-current liabilities Deferred revenue 1,376 1,196 Obligation under finance lease 19 6,090 7,159 Long-term financing 20 2,115 4,251Term loan 22 4,000 -Other 21 1,095 1,304 Total non-current liabilities 14,676 13,910 Current liabilities Line of credit 22 17,025 3,273 Obligation under finance lease 19 3,579 3,730 Current portion of financing 20 3,892 3,196 Term loan 22 2,000 - Trade and other payables 23 30,752 25,301 Deferred revenue 6,622 4,066 Due to affiliates 33 205 45 Total current liabilities 64,075 39,611 Total liabilities 78,751 53,521 Total equity and liabilities 106,327 79,045

The accompanying notes are an integral part of these consolidated financial statements.

These consolidated financial statements were approved for issue by the Board of Directors on 27 September 2016 and were signed on its behalf by

Robert Dechant Karl GabelChief Executive Officer Chief Financial Officer

32

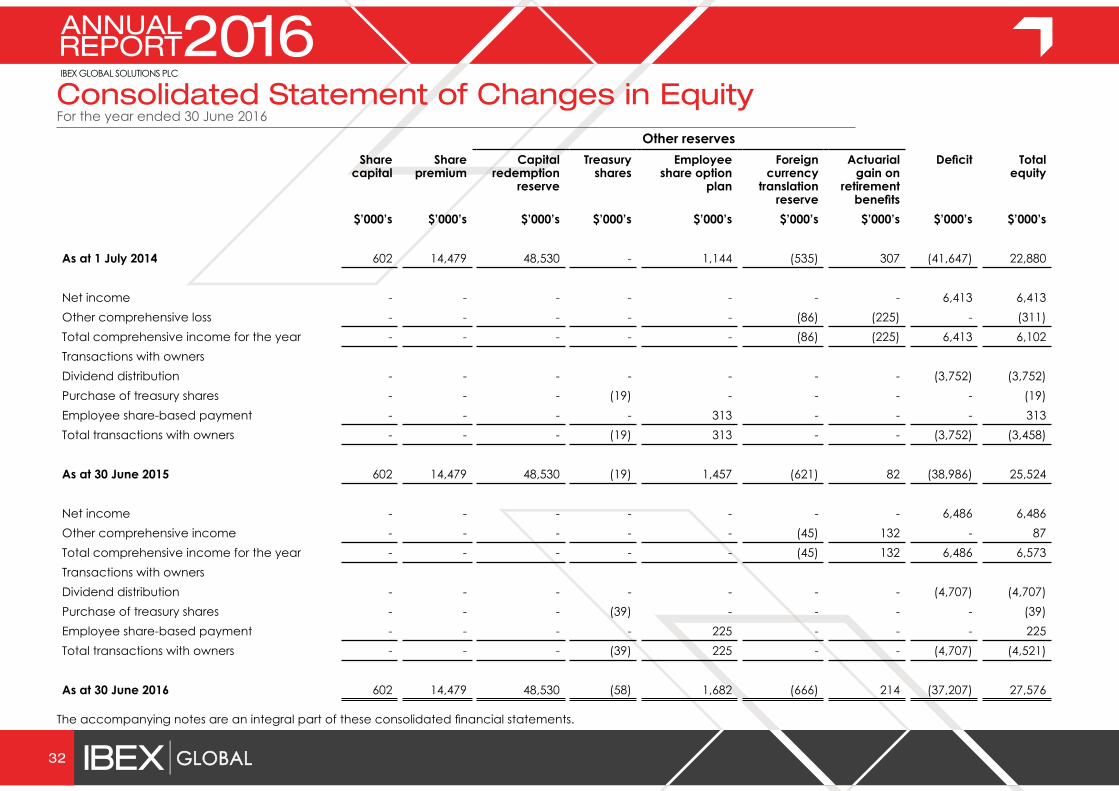

For the year ended 30 June 2016Consolidated Statement of Changes in Equity Other reserves

Share capital

Share premium

Capital redemption

reserve

Treasury shares

Employee share option

plan

Foreign currency

translation reserve

Actuarial gain on

retirement benefits

Deficit Total equity

$’000’s $’000’s $’000’s $’000’s $’000’s $’000’s $’000’s $’000’s $’000’s

As at 1 July 2014 602 14,479 48,530 - 1,144 (535) 307 (41,647) 22,880

Net income - - - - - - - 6,413 6,413Other comprehensive loss - - - - - (86) (225) - (311) Total comprehensive income for the year - - - - - (86) (225) 6,413 6,102Transactions with ownersDividend distribution - - - - - - - (3,752) (3,752) Purchase of treasury shares - - - (19) - - - - (19)Employee share-based payment - - - - 313 - - - 313Total transactions with owners - - - (19) 313 - - (3,752) (3,458)

As at 30 June 2015 602 14,479 48,530 (19) 1,457 (621) 82 (38,986) 25,524

Net income - - - - - - - 6,486 6,486Other comprehensive income - - - - - (45) 132 - 87Total comprehensive income for the year - - - - - (45) 132 6,486 6,573Transactions with ownersDividend distribution - - - - - - - (4,707) (4,707)Purchase of treasury shares - - - (39) - - - - (39)Employee share-based payment - - - - 225 - - - 225Total transactions with owners - - - (39) 225 - - (4,707) (4,521)

As at 30 June 2016 602 14,479 48,530 (58) 1,682 (666) 214 (37,207) 27,576

The accompanying notes are an integral part of these consolidated financial statements.

32

33

For the year ended 30 June 2016Consolidated Statement of Cash Flows

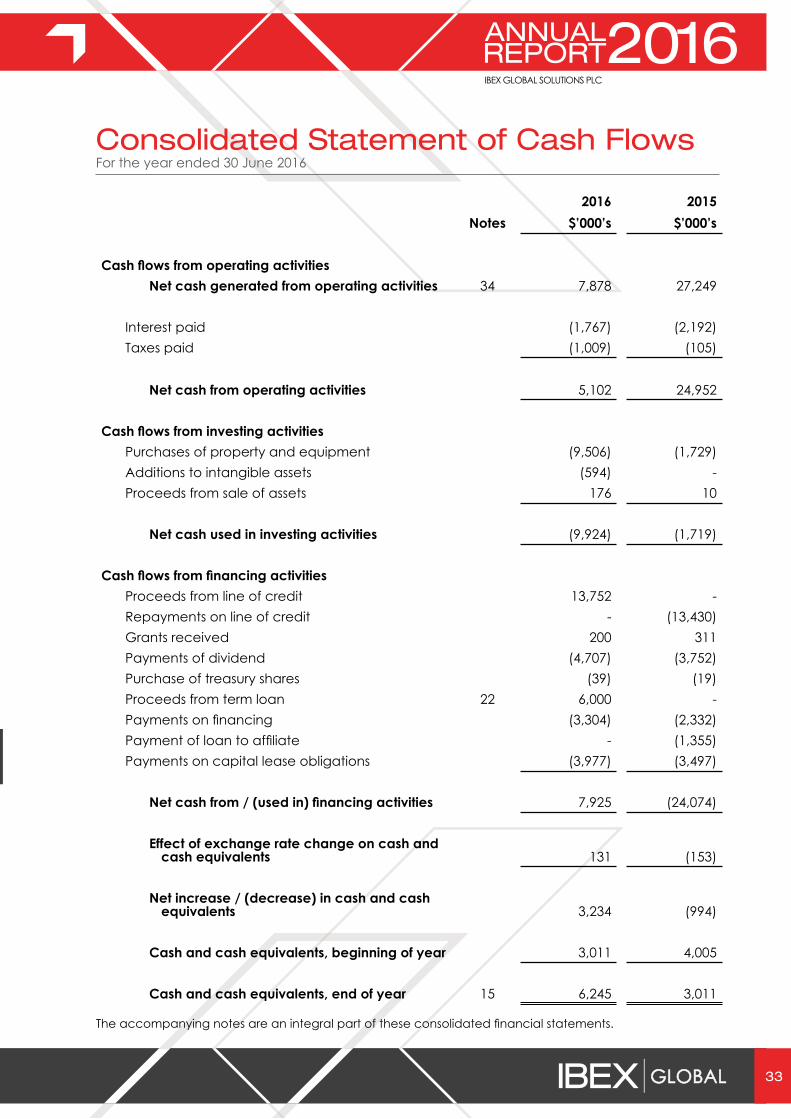

2016 2015Notes $’000’s $’000’s

Cash flows from operating activities

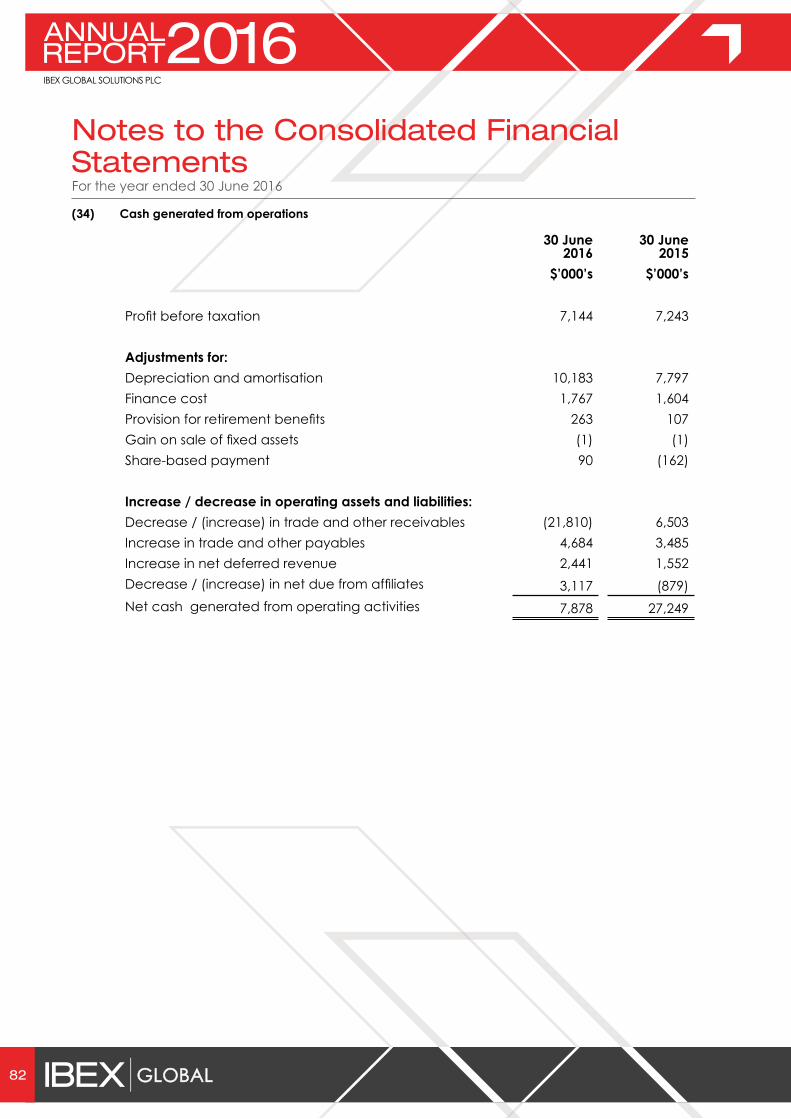

Net cash generated from operating activities 34 7,878 27,249

Interest paid (1,767) (2,192)Taxes paid (1,009) (105)

Net cash from operating activities 5,102 24,952

Cash flows from investing activitiesPurchases of property and equipment (9,506) (1,729)Additions to intangible assets (594) -Proceeds from sale of assets 176 10

Net cash used in investing activities (9,924) (1,719)

Cash flows from financing activitiesProceeds from line of credit 13,752 - Repayments on line of credit - (13,430)Grants received 200 311Payments of dividend (4,707) (3,752)Purchase of treasury shares (39) (19)Proceeds from term loan 22 6,000 -Payments on financing (3,304) (2,332)Payment of loan to affiliate - (1,355)Payments on capital lease obligations (3,977) (3,497)

Net cash from / (used in) financing activities 7,925 (24,074)

Effect of exchange rate change on cash and cash equivalents 131 (153)

Net increase / (decrease) in cash and cash equivalents 3,234 (994)

Cash and cash equivalents, beginning of year 3,011 4,005

Cash and cash equivalents, end of year 15 6,245 3,011

The accompanying notes are an integral part of these consolidated financial statements.

34

For the year ended 30 June 2016

Notes to the Consolidated Financial Statements

(1) Nature of the business

IBEX Global Solutions Plc (the Holding Company or the Parent Company) was incorporated on 26 March 2013 as IBEX Global Solutions Limited and was re-registered as a public limited company on 4 June 2013. Its registered office is 3rd Floor, 5 Lloyds Avenue, London EC3N 3AE. The Holding Company was incorporated under the Companies Act 2006 with a fiscal year end of 30 June. On 28 June 2013, the Holding Company was admitted to trade on the Alternative Investment Market (AIM), a market operated by the London Stock Exchange Group Plc.