ifma's world workplace: perspectives on the fm market development

TRANSCRIPT

TITLE (MAIN)Title (sub)

Perspectives on the FM Market Development

Glenn Hodge, Vice President – Client Solutions, ISS Facilities Services, Inc.Peter Ankerstjerne, CMO, ISS World Services A/S

CEUs & CFM® Maintenance PointsYou are eligible to receive Continuing Education Units and Certified Facility Manager® maintenance points for attending sessions at IFMA’s World Workplace.To receive CEU points, you must add the US$15 processing fee to your registration. (Full Event PLUS! registration includes the CEU processing fee.)

To Receive 20 CFM Maintenance PointsRecord your attendance for the three-day conference on your CFM Recertification Form in CAMP.At re-certification time, submit your completed CFM Recertification Form.

Managing CEUs:• Log into the Attendee Service Center. http://tinyurl.com/p6y4fxb

Your log-in information was sent to you when you registered for the conference.• Click “Start CEU Process” on the left-hand side.• Click “Start” next to the session you attended.• Complete the session evaluation.• Click “Start Test” next to the session.

After passing the test, your certificate will be available for download.

**If you wish to receive CEUs or LUs from other organizations, you must contact those organizations for instructions on reporting credit hours.

2

TITLE (MAIN)Title (sub)

Your Feedback is Valued!

Please take the time to Evaluate Sessions

Log into the Attendee Service Centerhttp://tinyurl.com/p6y4fxb

4

• TITLE (MAIN)• Title (sub)

Peter Ankerstjerne

Chief Marketing Officer of ISS World Services A/S since 2007

With ISS since June 1994

Based in Copenhagen, Denmark

Chair of the IFS Steering Group (Key Business Development Initiative)

Member of IAOP's Strategic Advisory Board, Fellow of RICS and former Trustee of IFMA Foundation

VP Clients Solutions, ISS Facility Services Inc

With ISS since 2011

Based in Phoenix, Arizona

ISS sponsor for IFMA – FMCC Council

28 years of experience in Engineering, Operations and Finance roles both in manufacturing and facilities

Glenn Hodge

Review Session Learning Objectives

The purpose of this session is to discuss the;

• Evolution of the FM industry from the 80’s to present

• Identify the drivers for growth in the FM industry

• Changes in FM delivery models

• Changing demands require a new way of thinking

5

EVOLUTION OF THE FM INDUSTRY

6

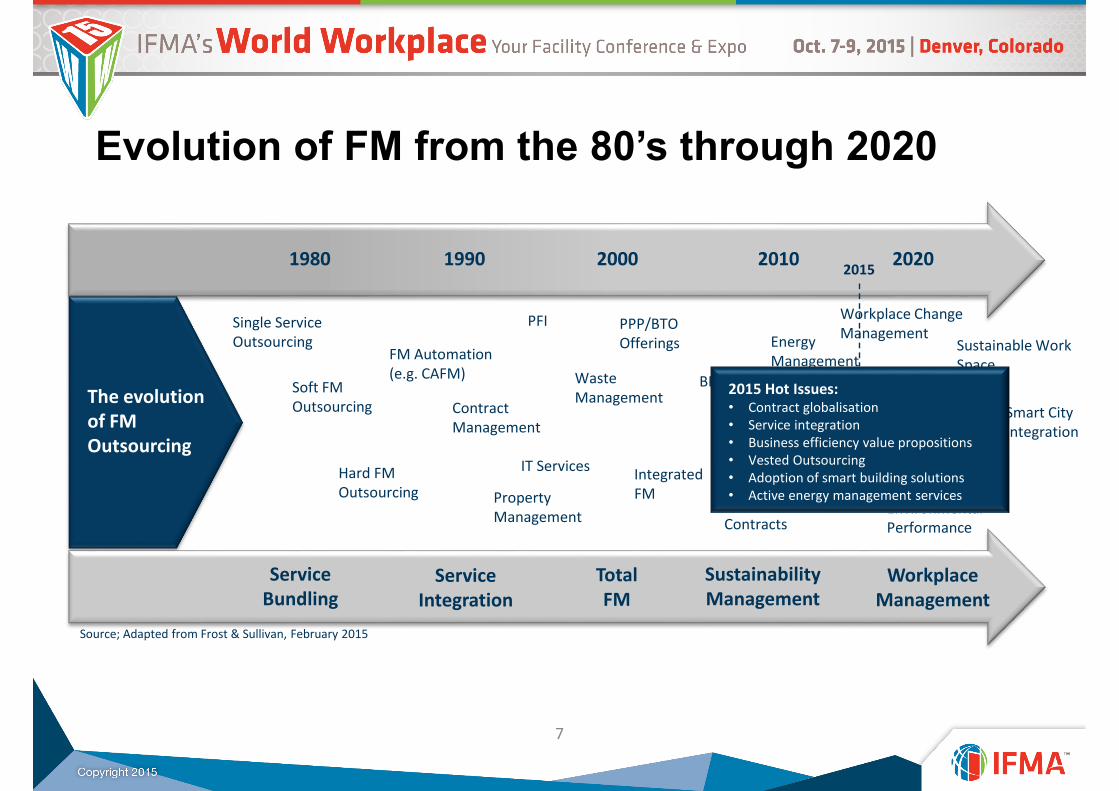

Evolution of FM from the 80’s through 2020

7

Copyright © 2014 IAOP. All Rights Reserved.

1980 1990 2000 2010 2020

Single ServiceOutsourcing

Soft FMOutsourcing

Hard FMOutsourcing

FM Automation(e.g. CAFM)

ContractManagement

PropertyManagement

EnergyManagement

IT Services

PFI PPP/BTOOfferings

Waste Management

Value DrivenDesign

Regional/GlobalContracts

BPO

Workplace ChangeManagement

EnvironmentalPerformance

Sustainable WorkSpace

Source; Adapted from Frost & Sullivan, February 2015

The evolution of FM Outsourcing

ServiceBundling

ServiceIntegration

TotalFM

SustainabilityManagement

WorkplaceManagement

Managing IntelligentBuildings

Integrated FM

Smart CityIntegration

Business Productivity

2015

2015 Hot Issues:• Contract globalisation• Service integration• Business efficiency value propositions• Vested Outsourcing• Adoption of smart building solutions• Active energy management services

Shift from in house delivery to service provider

• Large shift from in house to service supplier• Service model moved from single to bundled service delivery• Integrated service delivery will take more market share in the

future• WMS (Workplace Management Solutions) and “office hotelling”

concepts are gaining new ground

8

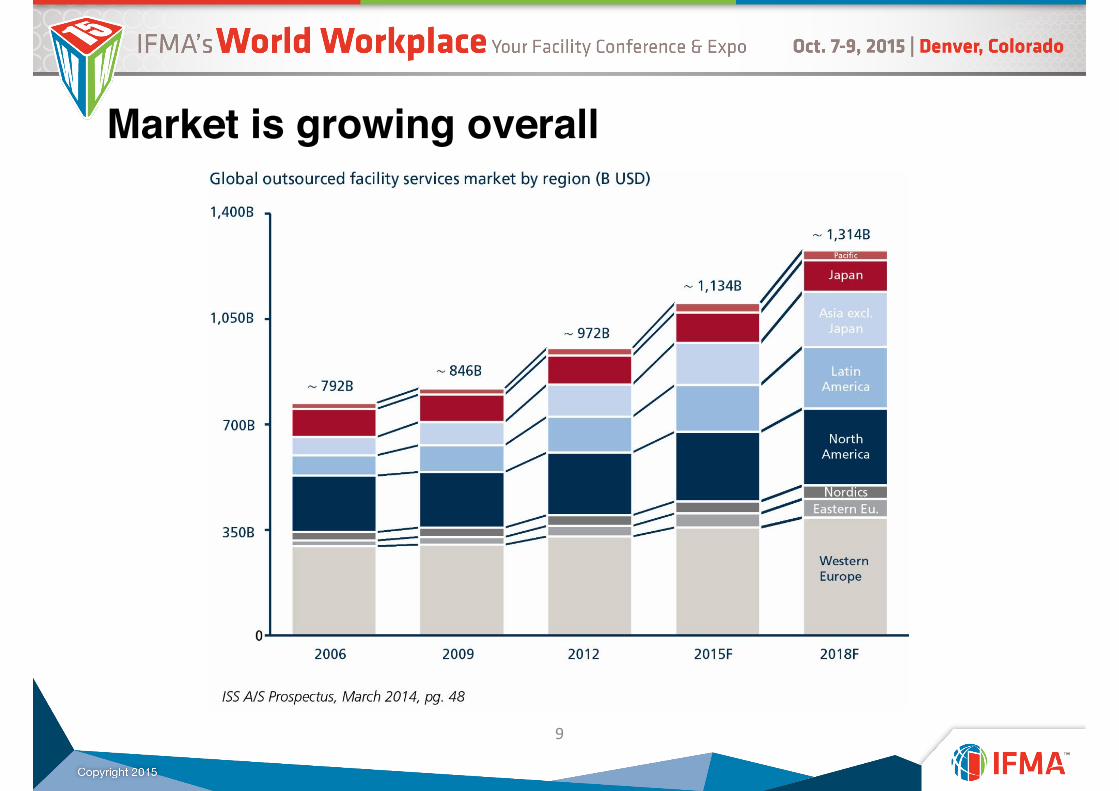

Market is growing overall

9

IFM as a portion of total FM market

10

IFS vs IFM

• IFS: Integrated Facility Services• IFM: Integrated Facility Management

For the purpose of this presentation:

IFS = IFM

11

IFS will continue to outgrow the market

12

• From the customer perspective – Integration provides one point

of contact– Increased transparency

through dealing with fewer vendors

– Reduced points of accountability

“It’s not part of our core business to take care of services such as cleaning and security. That is why we choose to outsource them. It’s also more flexible to do so than to have these services in- house.”- Nordic purchasing manager, Pharmaceutical Co, Sweden

13

Tactical Management

Operational Management

Strategic Management

Serv

ices

& O

rgan

izat

ions

Stan

dard

s &

Lang

uage

Proc

esse

s &

Proc

edur

es

Mgm

t Too

ls &

Sys

tem

s

Integration is (still) at the top of the agenda

FM and CRE

Increased Integration

14

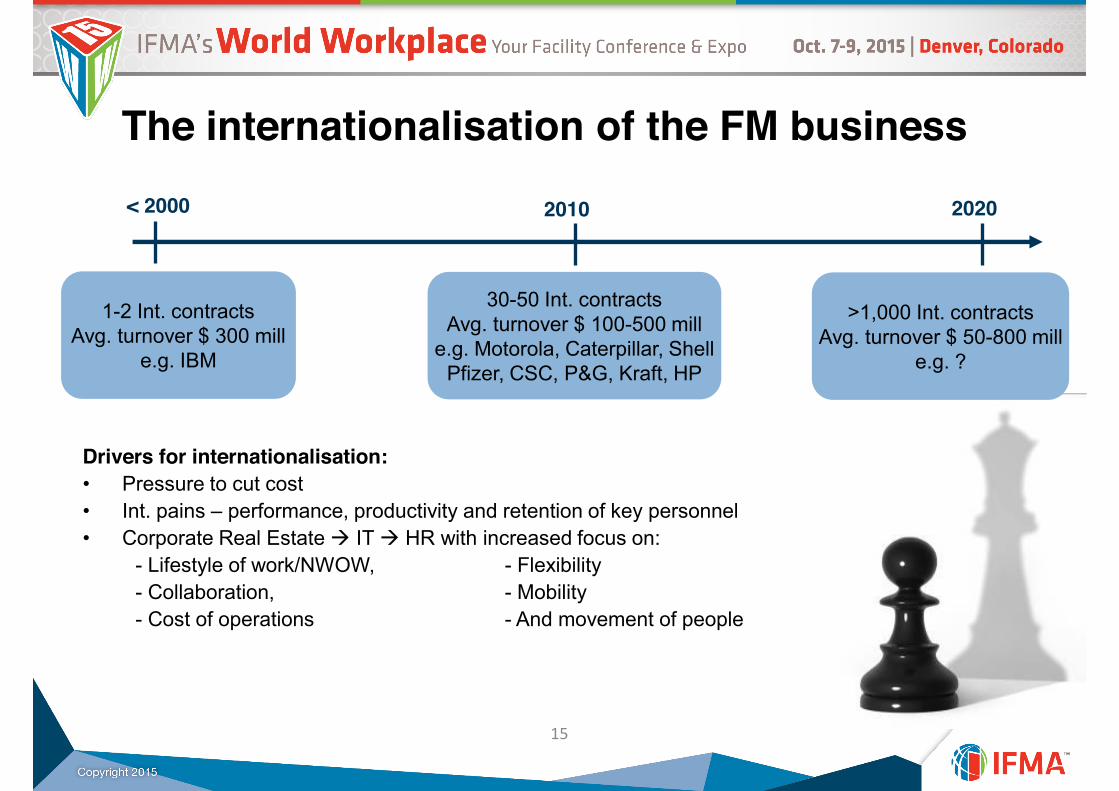

The internationalisation of the FM business

Drivers for internationalisation:• Pressure to cut cost• Int. pains – performance, productivity and retention of key personnel• Corporate Real Estate Æ IT Æ HR with increased focus on:

- Lifestyle of work/NWOW, - Flexibility - Collaboration, - Mobility - Cost of operations - And movement of people

< 2000 2010

30-50 Int. contractsAvg. turnover $ 100-500 mill

e.g. Motorola, Caterpillar, ShellPfizer, CSC, P&G, Kraft, HP

2020

>1,000 Int. contractsAvg. turnover $ 50-800 mill

e.g. ?

1-2 Int. contractsAvg. turnover $ 300 mill

e.g. IBM

15

Market demand for value added services

16

• Generate greater Value• Retain employees• Drive the organizations whole

ecosystem –– Social– Environmental– Economical

The market leaders are able to provide the client efficiency gains above mere outsourcing… innovation is becoming key, and that requires scale.”- Director General, Facilities Management Association

Regulatory changes influence customer behaviour

Cen15221 – 1-7

ISO/TC 267

17

DRIVERS FOR GROWTH IN THE INDUSTRY

18

Economic and environmental demands

Feeling the pressure:

• Economic pressures and competition are pushing companies to evaluate how they do business

• Higher scrutiny after financial scandals

• Broader environmental requirements

• Increasing focus on Corporate Social Responsibility

Looking for:

• Companies that are vested in the corporations success

• Facility Leaders to maximize the value of their corporate assets

• Innovators to deliver new ways of providing service (increased value)

• Trustees that will take care of their employees as their own

19

Nationalization and internationalization of purchasing

20

• Cost pressures• Drive for increased quality• Demand for simplification and

standardization of services• Reduction of internal soft costs

(procurement and finance) estimated at 5-7%

Increased appetite for outsourcing

• Expected growth is 4-5%• Outsourcing is growing across

– Regions– Service lines

• Companies focus on core activities

• Simplification and cost savings are key drivers

21

“I would prefer moving to an integrated set-up with a single provider. It seems so much more convenient than our current solution.”- Purchasing manager, Pharmaceutical Co, India

22

Value Add through outsourcingA transparent and streamlined value chain makes management more efficient and creates value:

Drive for efficiency – price, cost, performance and service level dynamics

Doubled-up functions are easily eliminated

A single point of contact shortens and optimises lines of communication

Risks are eliminated by transferring them to a (reliable and sound) partner

Someone who mitigates these risks

Someone who protects the brand you are building

22

Market’s demand for increased value added

• The decision to outsource is moving beyond the traditional core vs. non-core and cost reduction parameters

• Customer’s are demanding providers with e.g.– knowledge and competencies to address the customer’s specific needs– the ability to comply with CR and health, safety and environment standards– (credible) risk transfer – the ability to deliver a uniform set of services internationally– The ability to integrate facility services

23

24

Key points when outsourcing

• Finding partners who can provide support in achieving strategic goals and reaching overall success criteria

• Transfer financial and operational risks

• Strive for Management and Operational Excellence by outsourcing processes and not only tasks

• Performance based on balancing quality & cost

• Ultimately striving for a Vested Partner

24

24

26

12345

Quality Reputation Price Range Nationalcoverage

Internationalcoverage

Companies with > 354.1M USD in revenue Companies with < 354.1M USD in revenue

Source: Global customer interview program undertaken by a third party

Large customers care as much about

reputation as they do about price

Reputation is a more important parameter for large customers than it is for small

customers

How important is each of the following criteria when purchasing facility services? (1-5)

4,6 4,4 4,3 4,3 4,2 4,1

1

2

3

4

5

Matchinggeographic

scope

HSE/CSRreputation

Price Ability to self-deliver

Quality Matchingrange ofservices

IFS buyers rate self-delivery criteria highly

How important are the following criteria in purchasing IFS for Multinational companies?

Service range

Key drivers of outsourcing

CHANGES IN FM DELIVERY MODELS

27

Move from service delivery to service performance

• Integrated vs Independent delivery

• Self delivery vs sub contracted

• People & process vs supply-chain

– Managing service

– Output vs input specifications

• Value vs cost

28

Focus for Industries• Focus on the key market drivers

• Determine what are your core competencies

• Determine what makes you successful

• Determine what is core to your products and services

– what is a prerequisite for you to be competitive in your market

• Liberate resources by outsourcing of “non-core” services

29

30

The competitive landscape is changing

The FM/CRE market is big and continues to growCompetition comes from many places and continue to drive the development

Everybody is fighting for the same market

Strong need to develop the market and a shared interest to define the industry

New entrants are re-defining the marketNWOW as a disruptive technology?

WeWorkLiquid SpaceRegus2’nd Home

Project Management

New Waysof Working

Assets (CRE)Management

TechnicalManagement

ServiceManagement

IntegratedFacility

Management

30

CHANGING DEMANDS

REQUIRE A NEW WAY OF THINKING

31

Service Management 3.0

• Fostering a culture of Service

• Creating a sense of purpose within the organization

• Engaging employees

• Leading instead of managing

32

33

0%

20%

40%

60%

80%

100%

Time

Wo

rklo

ad

Actual Workload

“Staffing to Peak Demand”

Efficient base organization

“Service on Demand”

PotentialSynergies

Services must become significantly more efficientEfficient base organization

From “staffing to peak demand” to “service on demand” at the same quality level or better!

Efficient base organization (on-site)

Self-delivery is a fundamental requirement:Ability to integrate services and multi-task employees

Ability to take-over outsourced staff as new core employees

Going from input to output specificationsEmpowering front-line employees and provide them with more responsibility

Become more purpose-oriented and empower the frontline to deliver CUSTOMER EXCELLENCE

Demand for increased ”service” experience

33

34

Optimizing the Service Delivery System

Service delivery must be based on….

• What value the customer is getting from the service

• How total quality is perceived in customer relationships to facilitate value creation

• How an organization will be able to deliver the perceived quality

• How the service delivery system should be developed and managed

• Empowering frontliners to meet customer value expectations

35

Excellent Service = Customer Perception minus Customer Expectation

Understanding Workplace Management

0 20 40 60 80 100

Hospitality servicesInternal signage

Leisure facilities onsite or nearbyHealth and safety provisionsMail and post-room services

Reception areasAtriums and communal areas

Access (e.g. lifts, stairways, ramps etc.)Security

Parking (car, mororbike, bicycle)General tidiness

Restaurant/ canteenWashroom facilities/ showers

General cleanlinessTea, coffee and other refreshment facilities

% of respondents 'very satisfied' % variance vs. 'Top 15 average'

Workplace Facilities Satisfaction Survey

Source: Leesman

Supporting customersto win their war on

talent

Assisting to drive up productivity and

efficiency

Supporting the brand and reputation of the

customer……all at the right cost

36

TITLE (MAIN)Title (sub)

THANK YOU!For download of white papers/books;

http://www.issworld.com/en/about-iss/learning-zone

Follow us: www.servicefutures.com

Be sure to evaluate the session online at the Attendee Service Center

http://tinyurl.com/p6y4fxb