ifrs update event 2015 highlighting the key issues · pdf file• iasb’s public forum...

TRANSCRIPT

Groenekan, 19 November 2015

Highlighting the key issues

IFRS Update Event 2015

© 2015 Deloitte Accountants B.V.

Peter Bommel

CEO Deloitte Nederland

© 2015 Deloitte Accountants B.V.

Ralph ter Hoeven

Partner IFRS Centre Deloitte Nederland

Dingeman Manschot

Director IFRS Centre Deloitte Nederland

© 2015 Deloitte Accountants B.V.

Agenda

• IFRS Developments; Ralph’s Top 10

Break

• IFRS 9 Financial instruments

• IFRS 15 Revenue from contracts with customers

• Other platform changes

• Draft IFRIC Interpretations

• Attention points for 2015 FSs

© 2008 Deloitte Global Services Limited

IFRS Developments Ralph’s Top 10

© 2015 Deloitte Accountants B.V.

Ralph’s Top 10

1. Disclosure initiative

2. IFRS 15 Input TRG

3. Insurance contracts

4. IFRS 9 & Insurance industry

5. Leases

6. Conceptual framework

7. Post-implementation reviews IFRS 3 & IFRS 8

8. Rate-regulated activities

9. Accounting for dynamic risk management

10. Implementation issues

© 2008 Deloitte Global Services Limited

1.Disclosure initiative

© 2015 Deloitte Accountants B.V.

Disclosure problem

• Cutting the clutter (Financial Reporting Council, 2011)

• Losing the excess baggage - reducing disclosures in financial statements

to what’s important (The Institute of Chartered Accountants of Scotland &

New Zealand, 2011)

• IASB’s public forum to discuss disclosure overload (28 January 2013) &

IASB’s Feedback Statement of this Forum (May 2013)

Too much irrelevant

information

Not enough relevant

information

© 2015 Deloitte Accountants B.V.

Breaking the boilerplate

1. Clarify in IAS 1 the materiality principle

2. Clarify that a materiality assessment applies to the whole of the financial

statements, including the notes

3. If a Standard is relevant, it does not automatically follow that every disclosure

requirement is material

4. Remove prescriptive language from IAS 1

5. Flexibility about where they disclose accounting policies in the financial

statements

6. Consider adding a net-debt reconciliation requirement

7. Look into the creation general application guidance on materiality

8. Less prescriptive wordings for disclosure requirements when developing new

standards

9. Create a new disclosure framework (fundamental review of IAS 1, 7 & 8)

10. Undertake a general review of disclosure requirements in existing Standards

10-point plan to make financial reporting disclosure

more effective

Hans Hoogervorst

IFRS Foundation conference

Amsterdam, 27th June 2013

© 2015 Deloitte Accountants B.V.

Projects

Disclosure initiative activities

Completed

projects

Amendments

to IAS 1

Ongoing

activities

Digital

reporting

Implementation projects Research projects

Proposed

amendments

to IAS 7

(reconciliation

of liabilities

from financing

activities)

Distinction

between a

change in

accounting

policy and

estimate

Materiality

Practice

Statement

Principles of

disclosures

(Fundamental

review of

IAS 1 & IAS 8)

Standards

level review

of

disclosures

© 2015 Deloitte Accountants B.V.

Disclosure initiative activities

Materiality

• Not obscure useful information by aggregating or disaggregating

information.

• Materiality considerations apply to the primary statements, notes,

and specific disclosure requirements.

Disaggregation

and subtotals

• Specific line items can be disaggregated and aggregated as

relevant.

• Additional guidance on the presentation of subtotals.

Notes structure • Flexibility when designing the structure of the notes..

Other • Presentation of OCI items

Pre

se

nta

tio

n

2016

Amendments to IAS 1

© 2015 Deloitte Accountants B.V.

IFRS Practice Statement Application of Materiality to Financial Statements

Overview of ED

• Characteristics of materiality

• How to apply the concept when

presenting and disclosing information in

the financial statements

• Omissions and misstatements

• Will not be promoted to formal IFRS

(non-mandatory)

Objective

To help management apply the

concept of materiality when preparing

general purpose financial statements

in accordance with IFRS

ED

© 2015 Deloitte Accountants B.V.

Focus is on reviewing the general disclosure guidance in IAS 1 and IAS 8

Principles of disclosure (PoD) project

A Disclosure Standard that

improves and brings together the

principles for determining the basic

structure and content of the

financial statements, in particular

the notes.

Objective

© 2015 Deloitte Accountants B.V.

Review of existing disclosure requirements

Standards level review of disclosures project

To review disclosures in existing

Standards to identify targeted

improvements and to develop a

drafting guide.

Objective

This project will be informed by the

principles being developed in the

Principles of Disclosure (PoD)

project.

© 2015 Deloitte Accountants B.V.

Good Practice: Sligro Food Group Financial Statements 2014

© 2008 Deloitte Global Services Limited

2.IFRS 15 Input TRG

© 2015 Deloitte Accountants B.V.

FASB/IASB Transition Resource Group for Revenue Recognition

IFRS 15 TRG

US

influence

© 2008 Deloitte Global Services Limited

3.Insurance contracts

© 2015 Deloitte Accountants B.V.

Types of contracts

Insurance contracts

Non-participating contracts Participating contracts

Insurance contracts without

participation features.

Insurance contracts with participation

features.

The participation feature gives rise to

payments to the policyholder, paid out

from a distinct share of surpluses, after

providing the guaranteed benefits.

© 2015 Deloitte Accountants B.V.

Measurement & allocation of contractual service margin

Insurance contracts

Contractual service margin

‘Fulfilment cash flows’

Future cash flows: expected cash flows from

premiums and claims and benefits

Risk adjustment: an assessment of the uncertainty

about the amount of the future cash flows

Discounting

© 2015 Deloitte Accountants B.V.

Other matters

• An optional simplified measurement approach for simpler

insurance contracts, based on the unearned premium reserve

approach used in many jurisdictions

• Accounting requirements for reinsurance contracts that an entity

holds, based on the general model

• Accounting requirements for investment contracts with

discretionary participating features

Insurance contracts

© 2008 Deloitte Global Services Limited

4.IFRS 9 & Insurance industry

© 2015 Deloitte Accountants B.V.

Addressing the consequences of different effective dates of IFRS 9 and the new

insurance contracts standard

IFRS 9 & New insurance contracts standard

IFRS 9 Financial Instruments

1 January 2018 1 January 202X?

Solution 1: Overlay approach (effects in mismatch in OCI)

IFRS XX Insurance Contracts

Solution 2: Deferral approach (deferral of IFRS 9 for insurance industry)

Consequences

EU endorsement?

© 2008 Deloitte Global Services Limited

5.Leases

© 2015 Deloitte Accountants B.V.

Leases

The IASB has completed its decision making for the Leases project

The IASB plans to issue the new standard before the end of 2015

The new Leases standard will be effective from 1 January 2019

© 2008 Deloitte Global Services Limited

6.Conceptual framework

© 2015 Deloitte Accountants B.V.

Conceptual framework

1 The objective of general purpose financial reporting

2 Qualitative characteristics of useful financial information

3 Financial statements and the reporting entity

4 The elements of financial statements

5 Recognition and derecognition

6 Measurement

7 Presentation and disclosure

8 Concepts of capital and capital maintenance

ED – Chapters

© 2015 Deloitte Accountants B.V.

ED – Objective and qualitative characteristics

Conceptual framework

The objective of general purpose financial reporting is to provide useful financial

information

Fundamental characteristic 1

Relevance

Fundamental characteristic 2

Faithful representation

Relevant financial information is

capable of making a difference in

decisions made by users

• Representation of relevant

economic phenomena and faithful

representation of the phenomena

that it purports to represent

• Complete, neutral and free from

error

Enhancing characteristics

Comparability – Verifiability – Timeliness – Understandability

Cost constraint

© 2015 Deloitte Accountants B.V.

ED – Objective and qualitative characteristics

Conceptual framework

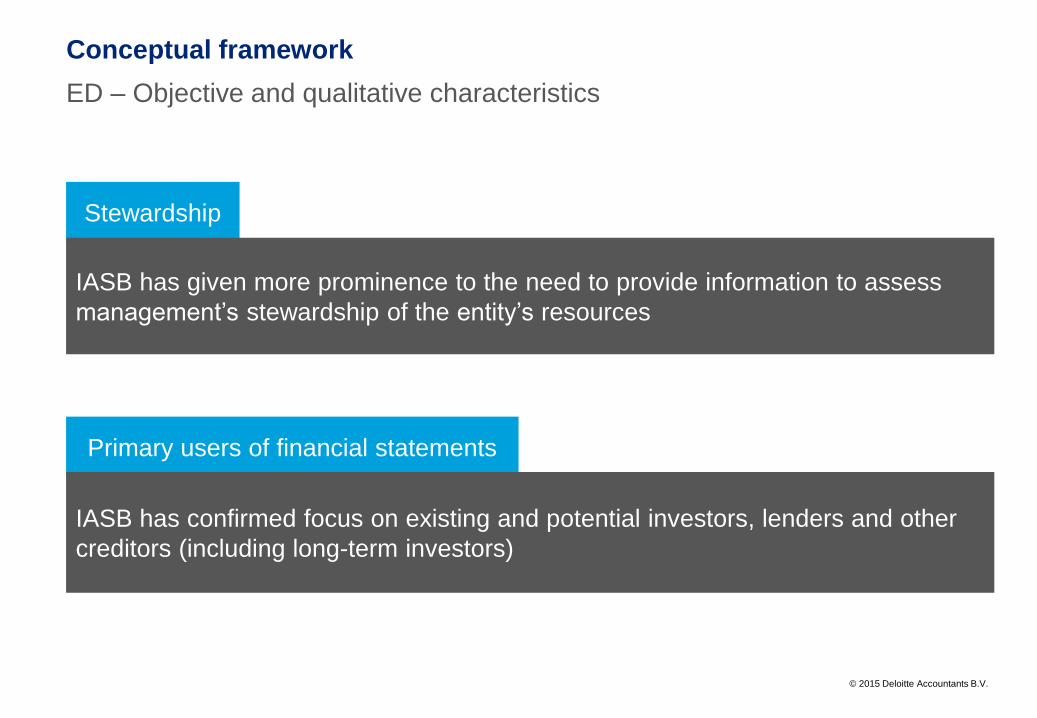

Stewardship

Primary users of financial statements

IASB has given more prominence to the need to provide information to assess

management’s stewardship of the entity’s resources

IASB has confirmed focus on existing and potential investors, lenders and other

creditors (including long-term investors)

© 2015 Deloitte Accountants B.V.

ED – Objective and qualitative characteristics

Conceptual framework

Prudence

Measurement uncertainty

• IASB has reintroduced an explicit reference to the notion of prudence

(exercise of caution when making decisions under conditions of uncertainty)

• No overstatement or understatement of assets, liabilities, income or expenses

(ie neutral)

• If an estimate is too uncertain, it might not provide relevant information

• Trade-off against other factors that affect relevance

Substance over form

IASB has reintroduced explicit reference to substance over form within

description of faithful representation

© 2015 Deloitte Accountants B.V.

ED – Definitions of assets and liabilities

Conceptual framework

Asset

Liability

A resource controlled by the

entity as a result of past events

and from which future economic

benefits are expected to flow to

the entity

A present obligation of the entity

arising from past events, the

settlement of which is expected

to result in an outflow from the

entity of resources embodying

economic benefits

A present economic resource

controlled by the entity as a

result of past events

A present obligation of the

entity to transfer an

economic resource of a

result of past events

Economic

resourceNot defined

A right that has the potential

to produce economic benefits

EDCurrent

© 2015 Deloitte Accountants B.V.

ED – Present obligation

An entity has a present obligation to transfer an economic resource if both:

• the entity has no practical ability to avoid the transfer; and

• the obligation has arisen from past events, ie the entity has received the

economic benefits, or conducted the activities, that establish the extent of

its obligation.

• Consequence for IAS 37 Provisions / IFRIC 21 Levies

Conceptual framework

© 2015 Deloitte Accountants B.V.

Conceptual framework

Income OCI

ED – Performance reporting

Income or expenses could be reported outside income only if:

• the income or expenses relate to assets or liabilities measured at current

values; and

• excluding those items from the statement of profit or loss would enhance

the relevance of the information in the statement of profit or loss for the

period.

© 2008 Deloitte Global Services Limited

7.Post-implementation reviews IFRS 8 & IFRS 3

© 2015 Deloitte Accountants B.V.

Post-implementation reviews

IFRS 8

&

IFRS 3

© 2015 Deloitte Accountants B.V.

IFRS 8

• Consistent description of the entity across presentations to investors, the

management commentary and operating segments disclosures

• CODM is a function that makes operating decisions

• Disclosure of the nature of the entity’s CODM

• Extend the number of examples of similar economic characteristics

• Additional guidance about the type of information that is most useful to

investors (e.g. non-cash expenses, non-recurring items)

Post-implementation reviews

© 2015 Deloitte Accountants B.V.

IFRS 3

• The effectiveness and complexity of testing goodwill for impairment

• The subsequent accounting for goodwill

• Challenges in applying the definition of a business

• Identification and fair value measurement of intangible assets such as

customer relationships and brand names

Post-implementation reviews

© 2008 Deloitte Global Services Limited

8.Rate-regulated activities

© 2015 Deloitte Accountants B.V.

Discussion Paper published in September 2014

• What information is needed to help investors understand the financial

effects of rate regulation?

• Definition of ‘rate regulation’?

• How does rate regulation affect the amount, timing and certainty of

revenue, profit and cash flows?

• How should IFRS be amended, if at all, to provide relevant information to

investors through IFRS financial statements?

Rate-regulated activities

© 2008 Deloitte Global Services Limited

9.Accounting for dynamic risk management

© 2015 Deloitte Accountants B.V.

Macro hedging

Accounting for dynamic risk management

© 2008 Deloitte Global Services Limited

10.Implementation issues

© 2015 Deloitte Accountants B.V.

• Annual Improvements cycle 2014-2016

• Annual Improvements cycle 2015-2017

• IFRS 13 Fair Value Measurement: unit of account

• IAS 12 Income Taxes: Recognition of deferred tax assets for

unrealised losses

• IAS 40 Investment Property: Transfers of investment property

Narrow scope amendments

Selection projects

Break

© 2008 Deloitte Global Services Limited

IFRS 9 Financial instruments

© 2015 Deloitte Accountants B.V.

Classification & Measurement

IAS

39 C

lassific

ation Rule-Based

Complex and difficult to apply

Own credit gains and losses recognized in P&L for fair

value option (FVO) liabilities

Complicated reclassification rules IF

RS

9 C

lassific

ation

Principle-based

Classification based on business model and nature of cash flows

Own credit gains and losses recognized in OCI

for FVO liabilities

Business model-driven classification

What are the differences?

© 2015 Deloitte Accountants B.V.

Classification & Measurement

Financial assets

Are the cash flows

considered to be solely

principal and interest

(“SPPI”)?

What is the business

model?

What is the

measurement category?

Are alternative options

available?

New

Certain modifications

of the relationship

between principal and

interest are

permissible

No FVTPL

FVOCI option for

equity investments

(dividends in P&L)

Yes

Hold to collect

contractual cash flows

Hold to collect

contractual cash flows

AND to sell

All other strategies

Amortized Cost

FVTOCI

FVTPL

FVTPL option

(in case of acc.

mismatch)

FVTPL Option

(in case of acc.

mismatch)New

© 2015 Deloitte Accountants B.V.

Impairment

Reduce reliance on identifying

“incurred loss” triggers

Financial crisis–

delayed recognition

of credit losses

Incurred loss model–

earnings management–

reduce the cliff effect

Reduce complexity of

multiple impairment

measures

Enhance

comparability

Why have changes been made to the impairment model?

© 2015 Deloitte Accountants B.V.

AC FVTOCI

FVTPL/FVTOCI Option

for certain equity

instruments

Within the scope of the impairment model

Outside the scope of

the impairment model

Financial assets in the scope of IFRS 9

Loan

commit-

ments

(unless @

FVTPL)

Financial

guarantees

(unless @

FVTPL)

Lease

receivables

Contract

assets

(IFRS 15)

Impairment

Subsequent measurement …

Scope of impairment provisions of IFRS 9

© 2015 Deloitte Accountants B.V.

Expected credit loss (ECL) model

Stage 1

No significant

increase in credit risk

12-month expected

credit losses

interest calculated

on gross carrying

amount

Stage 2

lifetime expected

credit losses

Significant increase in credit

risk and greater than low credit

risk but no objective evidence

of impairment

interest calculated

on gross carrying

amount

Stage 3

Objective evidence

of impairment

lifetime expected

credit losses

interest calculated

on net carrying

amount

• Low credit risk model

• Purchased or originated credit-impaired financial assets

• Trade receivables and contract assets

Simplifications

and exceptions:

General impairment model

© 2015 Deloitte Accountants B.V.

Measurement of expected credit losses

Measurement on

individual instrument

or on portfolio level.

Collective

assessment

Discounted to the

reporting date using the

effective interest rate at

initial recognition or an

approximation thereof.

Time value of moneyThe estimate shall always reflect:

• the possibility that a credit loss occurs; and

• the possibility that no credit loss occurs.

Expected value

Shortfalls of principal and

interest as well as late

payment without

compensation.

Cash shortfalls

Maximum contractual period

under consideration of

extension options.

Period

All reasonable and

supportable information,

which is available without

undue cost or effort

including information

about past events, current

conditions, and forecasts

of future economic

conditions.

Information

© 2015 Deloitte Accountants B.V.

Assessment of a significant increase in credit risk

Assessment of the

increase in credit risk

Relativeassessment–

compareinception and reporting date

Acc. policy choice: assume no increase if low credit risk at the reporting

date

Use reasonable and supportable forward-looking information that is available without undue cost/effort

Rebuttable presumption when more

than 30 days past due

May assess credit risk

increases on a collective

basis

Significant increase normally occurs

before credit-impairment

© 2015 Deloitte Accountants B.V.

Exemptions to the general impairment model

Special provisions

•No loss allowance on initial recognition

•Apply a credit-adjusted effective

interest rate (based on the

expected cash flows at inception

including expected credit losses)

Stage 3

General model

Stage 2 Stage 3Stage 1

• Trade receivables with a

significant financing

component

• Contract assets with a

significant financing

component

• Lease receivablesPolicy

choice

• Trade receivables without a

significant financing

component

• Contract assets without

significant financing

component

Simplified model

Stage 2 Stage 3

Purchased or originated

credit-impaired financial

assets

© 2015 Deloitte Accountants B.V.

Purchased or originated credit-impaired financial assets

On initial recognition,

measure at FV

Calculate a credit-adjusted EIR, incorporating

expected lifetime credit losses

Subsequently measure the asset

by applying the credit-adjusted

EIR to its amortized cost

Recognize cumulative

changes in the lifetime ECLs as an impairment

gain/loss in P&L

Even if lifetime ECLs have

decreased since initial

recognition

Purchased or originated credit-impaired financial assets are those that at the date of initial

recognition are credit-impaired.

A financial asset is considered to be credit-impaired when one or more events that have a

detrimental impact on the estimated future cash flows of that financial asset have occurred.

© 2015 Deloitte Accountants B.V.

Hedge accounting

New

effectiveness

requirements

(removal of

80%-125%)

Disclosures(IFRS 7 amendments)

Treatment of the

time value of

options, forward

elements of

forward

contracts,

foreign currency

basis spread

Extension of

FV option when

managing

credit risks +

own use

contract

Concept of

rebalancing

Eligibility of

hedged items

and hedging

instruments Closer

alignment of the

hedge

accounting

model with risk

management

Changes compared to IAS 39

© 2015 Deloitte Accountants B.V.

Effective date of transition for IFRS 9 (2014)

Effective for

annual periods

beginning on or

after January 1,

2018• Early application permitted.

• Concurrent application of all

requirements with certain

exceptions.

Retrospective application, with a

number of practical elections and

expedients available at transition.

Date of Initial Application–date when an entity first applies IFRS 9 (2014)

Choice of whether to

restate

comparatives, but

restatement not

allowed if this

requires use of

hindsight.

If an entity with a Dec 31 YE does not early adopt, DIA = January 1, 2018

IFRS 9:7.2.22: hedge

accounting

requirements will

generally be applied

prospectively

© 2008 Deloitte Global Services Limited

IFRS 15

Revenue from contracts with

customers

© 2015 Deloitte Accountants B.V.

Overview

Identify the contract with a

customer

(Step 1)

Identify the performance obligations in the contract

(Step 2)

Determine the

transaction price

(Step 3)

Allocate the transaction price to the

performance obligations

(Step 4)

Recogniserevenue when

each performance obligation is

satisfied

(Step 5)

Control approach (differs from the risks and rewards approach under IAS 18)

Recognise revenue to depict the transfer of goods or services to customers in an

amount that reflects the consideration to which the entity expects to be entitled in

exchange for those goods or services.

Five-step model to apply the core principle:

The core principle

© 2015 Deloitte Accountants B.V.

Step 1: Identifying the contract

A legally enforceable contract (incl. oral or implied) must meet all of the following requirements:

A contract is outside the scope if:

Commercial substance.

Contracts are approved and the

parties are committed to perform.

Each party’s rights can be

identified.

Payment terms can be identified.

The contract is wholly unperformedEach party can unilaterally terminate the

contract without compensation

Step 1 Step 2 Step 3 Step 4 Step 5

It is probable that the entity will

collect the consideration to which

it will be entitled.

AND

© 2015 Deloitte Accountants B.V.

Identify all (incl. implicit) promised goods/services in the contract

Step 2: Identifying performance obligations

Is the good/service distinct?

Can the customer benefit

from the good or service

on its own or together with

other readily available

resources?

Is the good or service

separately identifiable from

other promises in the

contract?

Account for as a separate

performance obligation

Combine two or more

promised goods or

services

YES NO

CAPABLE OF BEING

DISTINCT

DISTINCT IN CONTEXT

OF CONTRACT

Step 1 Step 2 Step 3 Step 4 Step 5

AND

© 2015 Deloitte Accountants B.V.

Transaction price

The transaction price would

not be reduced for the

effects of customer credit

risk.

Excluding credit risk

Variable considerationConsideration amount to which an entity

expects to be entitled in exchange for

transferring promised goods or services to

a customer.

Definition

The amount is fixed and not

contingent on the outcome of

future events.

Fixed consideration

• Consideration in a form other than

cash

• Shall be measured at FV

Non-cash consideration

Significant benefit of financing

• Estimated and

potentially constrained

• e.g., discounts, rebates,

refunds, etc.

Step 3: Determining the transaction price Step 1 Step 2 Step 3 Step 4 Step 5

Consideration payable

to customers

• If identified, leads to adjustment in

transaction price.

• Practical expedient available.

Reduces transaction

price unless payment is

made for a distinct

good/service.

What is the transaction price? What does it include?

© 2015 Deloitte Accountants B.V.

Determine standalone selling price

• Estimate the price if unobservable

• Acceptable methods: Adjusted market assessment approach Expected cost plus a margin approach Residual approach (under conditions)

Allocate the transaction

price

• Allocate the transaction price to each performance obligation on a relative stand-alone selling price basis.

• Allocate discounts proportionally to all performance obligations unless certain criteria are met.

• Allocate variable consideration and changes in transaction price to allperformance obligations unless two criteria are both met.

• Do not reallocate changes in standalone selling price after inception.

Step 4: Allocating the transaction price Step 1 Step 2 Step 3 Step 4 Step 5

Maximize the

use of

observable

inputs and

apply

consistently

© 2015 Deloitte Accountants B.V.

Step 5: Recognising revenue

The seller’s

performance creates or

enhances an asset

controlled by the

customer.

Performance satisfied over time = Revenue recognised over time

The seller creates an

asset that does not

have an alternative

use to the seller and

the seller has the right

to be paid for

performance to date.

OR

Revenue recognised at a point in time

The customer

simultaneously

receives and

consumes the benefit

of the seller’s

performance as the

seller performs.

IF NOT

Step 1 Step 2 Step 3 Step 4 Step 5

OR

© 2015 Deloitte Accountants B.V.

Key impact on revenue recognition

Identify the contract with a customer

Identify the performance obligations in the contract

Determine the transaction price

Allocate the transaction price to performance obligations

Recogniserevenue when each performance obligation is satisfiedStep 1

Step 2

Step 3

Step 4

Step 5

Collectability

Healthcare

Technology

Unbundling of contracts

Telecom

Software

Automotive

Uncertain revenue or contingent revenue

Life Science

Consumer & Industrial Products

Allocation of total revenue to the unbundled parts

Telecom

Recognition of revenue at a point in time or over timeContract Manufacturer

Real estate

© 2015 Deloitte Accountants B.V.

Disclosures

• Description of significant judgments applied/transaction price, allocation methods and assumptions

Significant judgments

• Disaggregation of revenue

• Contract balances (including reconciliation)

• Information about performance obligations

• Remaining performance obligations

• Practical expedients

Contracts with customers

• Policy decisions –time value of money and cost to obtain a contract

• Contract costs

Others

Enable users to understand the amount, timing, and uncertainty of revenue and

cash flows

© 2015 Deloitte Accountants B.V.

Transition to IFRS 15

Adjust opening

balance of

equity as at

date of initial

application

Current GAAP IFRS 15

All restated under IFRS 15

Option 1:

Modified

Retrospective

Option 2:

Fully

Retrospective

Initial

application

Jan

2014

Jan

2020

Jan

2018

© 2015 Deloitte Accountants B.V.

• Determining when a good or service is ‘separately identifiable’

• Determining whether an entity is a principal or an agent

• Determining the nature of an entity’s promise in granting a licence

• Application of the exemption for sales- and usage-based royalties

• Practical expedients upon transition

Clarifications to IFRS 15 (ED/2015/6)

© 2008 Deloitte Global Services Limited

Other platform changes

© 2015 Deloitte Accountants B.V.

Accounting for acquisitions of interests in joint operations that

constitute a business

Does the activity of the

JO constitute a

business under IFRS 3?

• Fair value measurement of

identifiable assets and liabilities

• Recognize goodwill, deferred tax

assets, and liabilities

• Expense acquisition-related costs

Allocate the total cost of the

acquisition on the basis of relative

fair value of the assets and

liabilities of JO

Investor

acquires an

interest in a JO

Apply the business combinations

principles under IFRS 3 and

other IFRSs

Account for as the

acquisition of assets

YesNo

New guidance on the

accounting for acquisitions

of interests in JO, in which

the activity constitutes a

business

Apply the principles under

IFRS 3 and other relevant

IFRSs if the JO activity

meets the definition of

business under IFRS 3

2016

© 2015 Deloitte Accountants B.V.

Simplified measurement of bearer plants 2016

Apples at fair

value less costs

to sell

(IAS 41)

Tree at cost

(IAS 16)

© 2008 Deloitte Global Services Limited

Draft IFRIC Interpretations

© 2015 Deloitte Accountants B.V.

Draft Interpretation Uncertain tax positions

If an entity concludes that it is probable that the taxation authority will

accept an uncertain tax treatment, or group of uncertain tax treatments, it

shall determine the taxable profit (tax loss), tax bases, unused tax losses,

unused tax credits or tax rates consistently with the tax treatment used or

planned to be used in its income tax filings.

> 50%

© 2015 Deloitte Accountants B.V.

Draft Interpretation Uncertain tax positions

Reflect the effect of uncertainty in determining the related taxable profit (tax

loss), tax bases, unused tax losses, unused tax credits or tax rates. It shall

reflect the effect by using one of the following methods:

≤ 50%

The most likely amount The expected value

Apply approach which will provide the better prediction of the

resolution of the uncertainty

© 2015 Deloitte Accountants B.V.

How to determine the date of transaction and thus the

exchange rate to use to translate the asset, expense or

income on initial recognition?

If non-monetary prepayment asset or non-monetary

deferred income liability is recognised in advance of

the related asset, expense or income

Draft Interpretation Foreign currency transactions and advance

consideration

© 2015 Deloitte Accountants B.V.

Draft Interpretation Foreign currency transactions and advance

consideration

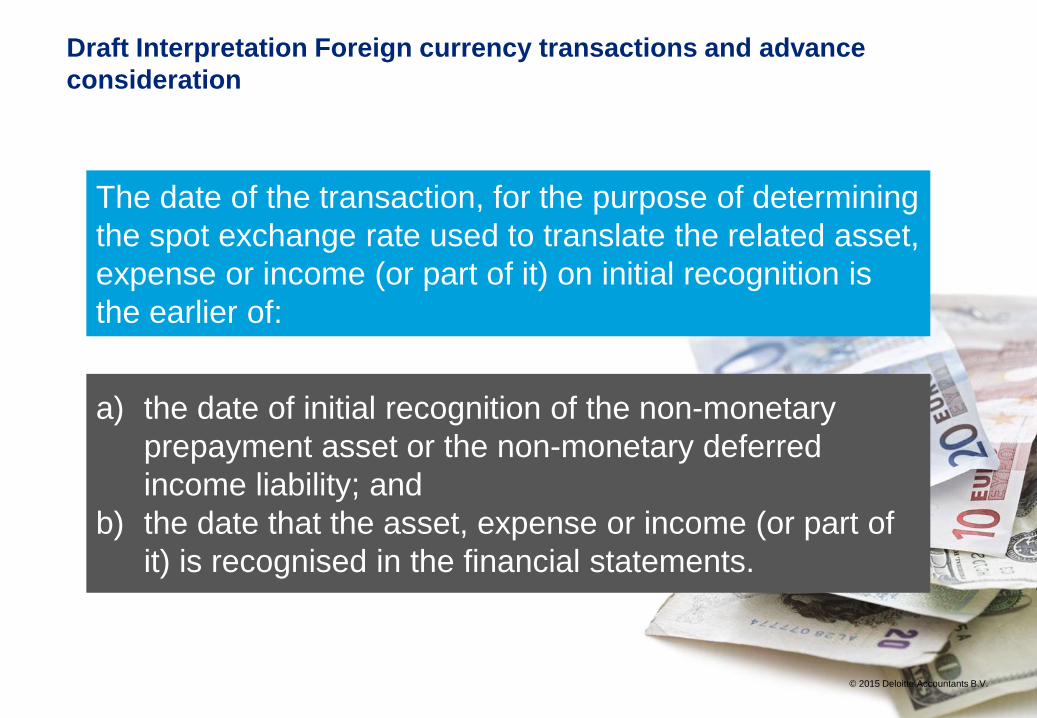

a) the date of initial recognition of the non-monetary

prepayment asset or the non-monetary deferred

income liability; and

b) the date that the asset, expense or income (or part of

it) is recognised in the financial statements.

The date of the transaction, for the purpose of determining

the spot exchange rate used to translate the related asset,

expense or income (or part of it) on initial recognition is

the earlier of:

© 2015 Deloitte Accountants B.V.

© 2015 Deloitte Accountants B.V.

Example: Foreign currency and advance consideration

1 April

Date of

transaction

• An entity enters into a contract with a supplier on 1 March to purchase a

machine for use in its business.

• The entity pays the supplier a non-refundable fixed purchase price of

USD 1000 on 1 April.

• On 15 April the entity takes delivery of the machine.

• The functional currency of the entity is the Euro.

1 March 15 April

ED

© 2008 Deloitte Global Services Limited

Attention points for 2015 FSs

© 2015 Deloitte Accountants B.V.

• Impacts of the financial markets on the financial statements

• Statement of cash flows and related disclosures

• Fair value measurement and related disclosures

ESMA – European enforcement priorities for 2015 financial statements

© 2015 Deloitte Accountants B.V.

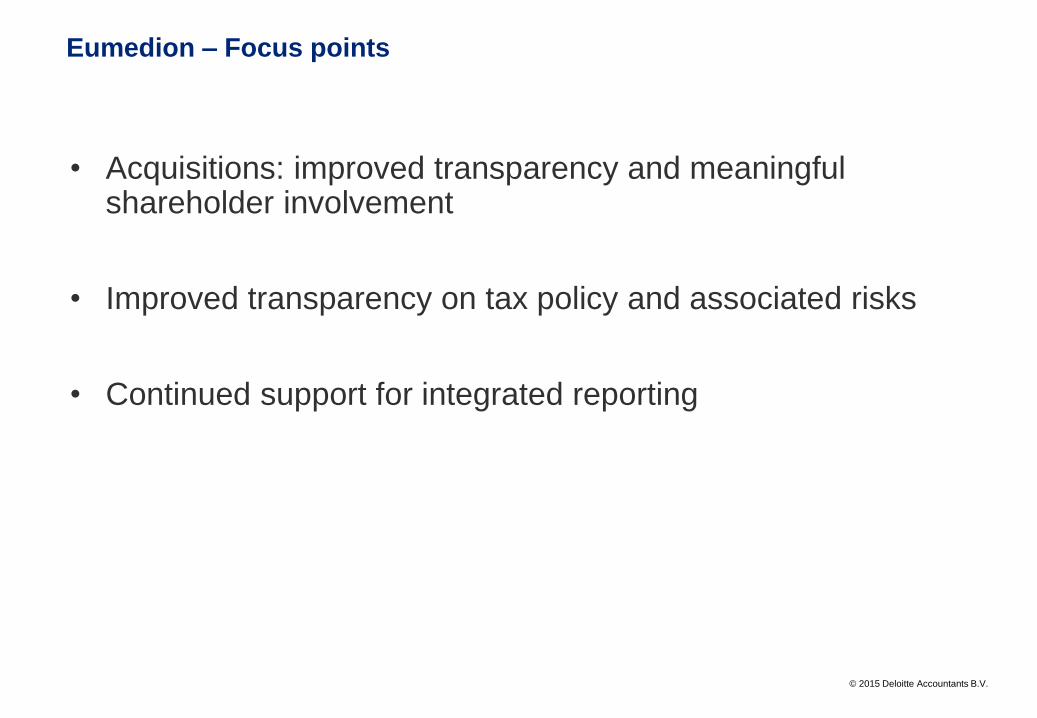

• Acquisitions: improved transparency and meaningful shareholder involvement

• Improved transparency on tax policy and associated risks

• Continued support for integrated reporting

Eumedion – Focus points

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.nl/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally

connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights

they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte

network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained

by any person who relies on this communication.

© 2015 Deloitte Accountants B.V.