iia east region enhancing our influence – dr ian peters (chief executive) iia east – agm 2015...

TRANSCRIPT

IIA East Region

Enhancing Our Influence – Dr Ian Peters (Chief Executive)

IIA East – AGM 2015

The Power of Persuasion – Dale Carnegie Training

21 July 2015

haysmacintyre26 Red Lion Square, London WC1R 4AG, United Kingdom

Enhancing our influence

Dr Ian PetersChief Executive

Tuesday 21st July, 2015

IIA East

Meeting Expectations

• Challenges and opportunities

• The Institute’s response

• Enhancing our influence

• Questions

Challenges for the Public Sector

• Lord Browne’s 2013/14 annual report highlighted the nature of change within government and the implications for the management of risk :-

• “ [ The role of government ] has increasingly become a commissioning body, buying and managing a range of complex services and commercial relationships against an economic backdrop requiring efficiencies and cost savings. As a result it needs to be the smartest buyer in the nation, with much more effective management of risk”.

Source : The Government’s Lead Non-Executive’s Annual Report, 2013-14

Challenges for the private sector

The revised UK Corporate Governance Code raises the bar for Boards in four key areas :

•Going concern, risk management and internal control•Culture and tone at the top•Remuneration•Shareholder engagement

“The changes to the Code are designed to strengthen the focus of companies and investors on the longer term and the sustainability of value creation.”

Stephen Haddrill, CEO, Financial Reporting Council, September 2014

Bad behaviour: a recurring problem

• Banks

• Supermarkets

• Health service

• Local government (child abuse)

• Pharmaceuticals

Boards’ accountability redefined?

The Prudential Regulation Authority is now consulting on plans to outline the collective and individual responsibilities of board members in

regulated firms in the areas of:

•Culture

•Risk appetite and risk management

•The respective roles of executive and non-executive directors

•Knowledge and experience of non-executive directors

•Board committees

Key themes

Higher expectations of organisations amongst their key stakeholders including the public and the media :

• Stronger ethical behaviour throughout organisations and their suppliers

• Better conduct in relation to consumers

• Reliable, accessible and transparent public reporting

Shifting the focus for internal audit

Hence, there are greater expectations of internal audit to assess:

• Tone at the top

• Culture

• Business strategy / management information

• Public reporting (e.g. Annual Reports, Strategic Reports, Integrated Reports)

These expectations raise a number of issues for internal audit, in particular:

• Its Independence and authority

• Its scope and priorities

Key initiative: Financial Services Code

• Response to the regulators

• As much for executives and non-executives as internal audit

• Relevance beyond financial services

• Has put internal audit firmly on the agenda

Independence and authority of internal audit

• The primary reporting line for the Chief Internal Auditor should be to the Chairman of the Audit Committee.

• The Audit Committee should be responsible for the Chief Internal Auditor’s:o appointment/removalo performance, objectives setting and remuneration

• The Chief Internal Auditor should be at a senior enough level within the organisation to give him or her the appropriate standing, access and authority to challenge the Executiveo normally Executive Committee level

• “Internal Audit should have the right to attend and observe all or part of Executive Committee meetings and any other key management decision making fora.”

Scope and priorities of Internal Audit

• Internal Audit’s scope should be unrestricted

• A risk based approach should be taken in setting priorities:

o ” Internal Audit should make a risk-based decision as to which areas within its scope should be included in the audit

plan – it does not necessarily have to cover all of the potential scope areas every year.“

• Risk assessments and prioritisation of Internal Audit work:

o “In setting its scope, Internal Audit should take into account business strategy and should form an independent view of

whether the key risks to the organisation have been identified and how effectively they are being managed.”

Scope should include:

• Internal governance

• Information for strategic and operational decision-making

• Setting of, and adherence to, risk appetite

• The risk and control culture of the organisation

• Poor customer treatment, conduct and reputational risk

• Key corporate events (e.g.. M&A)

• Whether outcomes match objectives of policies and processes

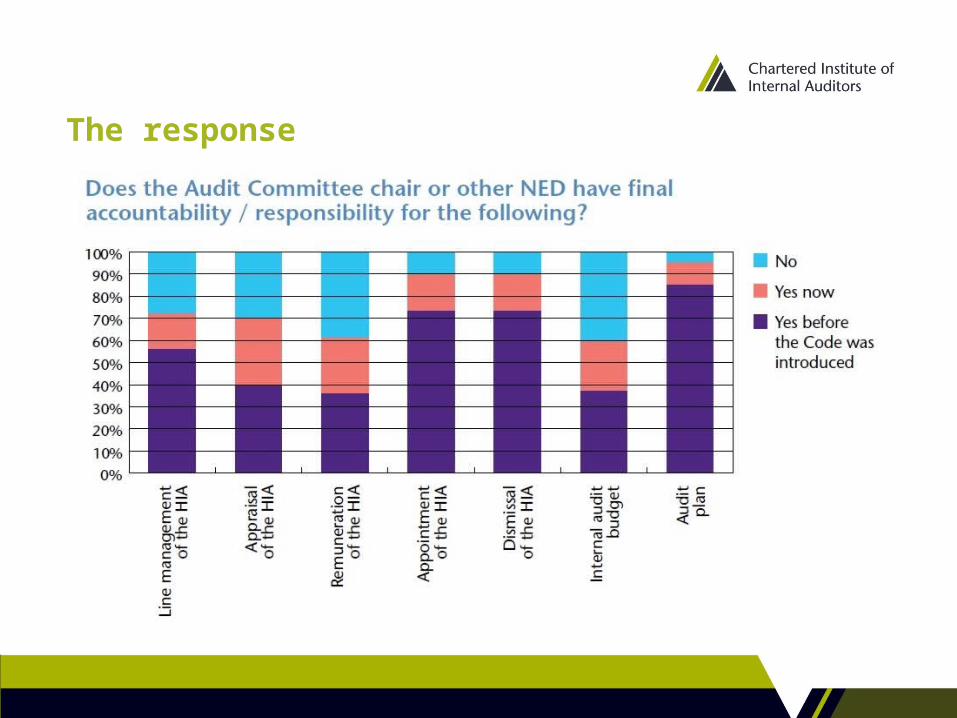

The response

The response

Key Initiative: Auditing Culture

“Internal audit… can provide confidence that there is a strong commitment to good conduct and that it is actually being translated into everyday behaviours, but also, more importantly, where it is not.” Sir Winfried Bischoff , Chair, FRC.

Some key points from our report on auditing culture:

• Corporate culture must be analysed, defined and disseminated by the board (what is expected must be explicit)

• There must be appetite and support from the top of the organisation• Internal audit must be given a clear mandate (in the Audit Charter)

Auditing Culture

Key points from our report continued:

• Internal audit will need to use qualitative as well as quantitative methods and will need to be willing to move out of it’s comfort zone into subjective judgements

• There must be a relationship of trust between AC Chair and the HIA to allow for informal discussion about subjective judgements (gut feel)

• Internal audit must be well regarded in the organisation and hold non-adversarial relationships with clients. It must have the confidence of management

Challenges for boards, audit committees and internal audit

• Relationships and trust are key

• Internal Audit must have the right position and standing in the organisation

• Promoting objectivity and independence

• Access and engagement (e.g. Executive Committee)

• Value of “gut feel” – a willingness to listen to the HIA’s view, not just the ‘hard evidence’

• Appointing people with credibility

Enhancing our influence

• Identifying key issues in relation to good governance

• Focussing on internal audit’s relevance

• Engaging with key stakeholders

• Adding value to the debate

• Offering solutions

Questions

Page 21

Presented by:

The Power of Persuasion: Enhancing our Influence with Critical Stakeholders

Mark SharrattDale Carnegie Training

Page 22

Agenda

Influence: “the power or capacity of a person to be a compelling force on the actions, behaviour, opinions of others”

Define the attributes and qualities of key individuals of influence

Apply principles for engaging with and influencing even the most difficult stakeholders across the business

Raise the profile and effectiveness of Internal Audit within the business

Commitments

Page 23

Introductions

Who We Are

What We Do

Share a Personal Experience:

Who is your ‘Most Challenging Stakeholder’?

What got/gets in the way of the relationship?

What would be the benefit of winning them round more easily?

Page 24

Becoming a Key Person of Influence

Influence: “the power or capacity of a person to be a compelling force on the actions, behaviour, opinions of others”

Think of a person you have known that you have known that you would consider to be persuasive & influential

Now consider, what was it about them that caused them to be so influential?

Page 26

What qualities, traits, and attributes do we need to possess to becomea Key Person of Influence in our organisation?

Becoming a Key Person of Influence

Page 27

Triangle of Success

Page 28

Win People to Your Way of Thinking

Page 29

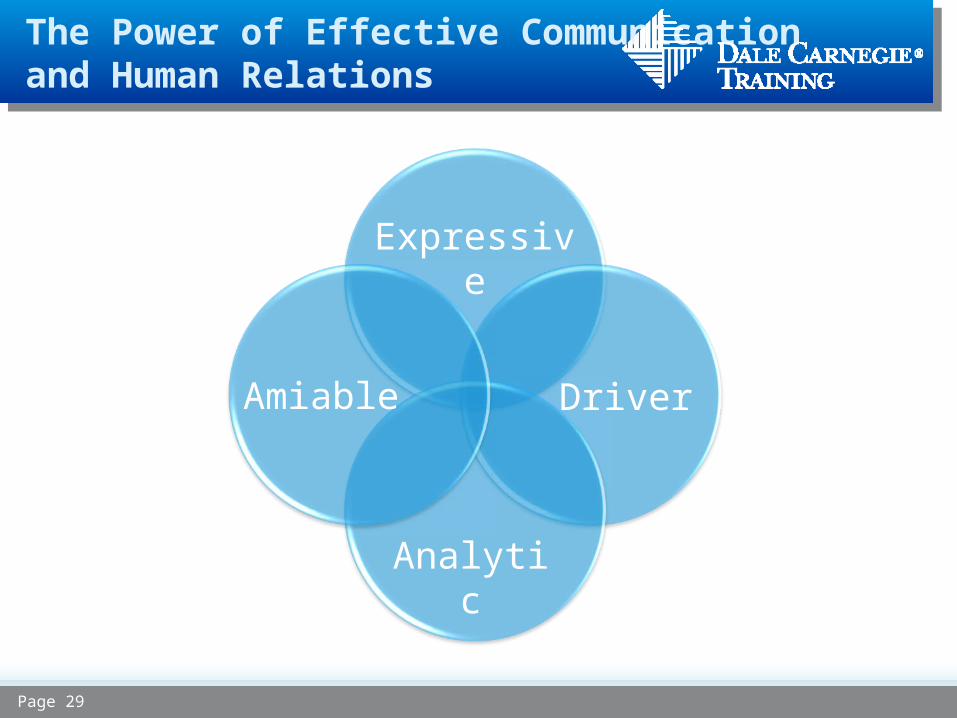

The Power of Effective Communicationand Human Relations

Amiable Driver

Expressive

Analytic

Page 30

Understand Our Own Style

Page 31

Relating with Different Styles

Page 32

Commit to Influence Others

Page 33

Agenda

Influence: “the power or capacity of a person to be a compelling force on the actions, behaviour, opinions of others”

Define the attributes and qualities of key individuals of influence

Apply principles for engaging with and influencing even the most difficult stakeholders across the business

Raise the profile and effectiveness of Internal Audit within the business

Commitments

Page 34

Presented by:

The Power of Persuasion: Enhancing our Influence with Critical Stakeholders

Mark SharrattDale Carnegie Training

Page 35

[ADD TITLE]

Bullet 1

Sub-bullet 1 Sub-bullet 2 Sub-bullet 3

Bullet 2

Sub-bullet 1 Sub-bullet 2 Sub-bullet 3

IIA East RegionAGM 2015

21 July 2015

haysmacintyre26 Red Lion Square, London WC1R 4AG, United Kingdom

IIA East Region - AGM 2015Your Committee

• Chairman Chris Brookes (Rexam PLC)• Deputy Chairman/ Louise Woodward (Royal Bank of

Scotland) Secretary• Treasurer Mark Leckie (haysmacintyre)

IIA East Region - AGM 2015Your Committee

• Comm’ee Member David Alexander (Consultant)

• Richard Clarke (RGP)• Sissel Heiberg (Deutsche Bank)• Xina Li (Starr Underwriters)• Pirjo Shaer (Govt IA Agency)• Joanne Stanley (HMRC)

IIA East Region - AGM 2015Annual Report 2014-15• Events held in 2014-15:

- Student (Pre-Exam) Training (KPMG) April 2014 - Auditing Fraud, Bribery & Corruption (Kirkland Ellis) May 2014- AGM and Speed Networking (haysmacintyre) June 2014- Cyber risks (BDO) October 2014

• Other activity- Worked very closely with South region to help ensure events were shared in London and get them off the ground- Support with IIA International Conference in July 2014- Recruiting new Committee members to support the Region’s members

April 2014 - March 2015– Income £2,890*– Expenditure £(2,144)**– Surplus £746

* From 4 events held (1 free networking event)

** Includes IIA central admin charge of £2,093

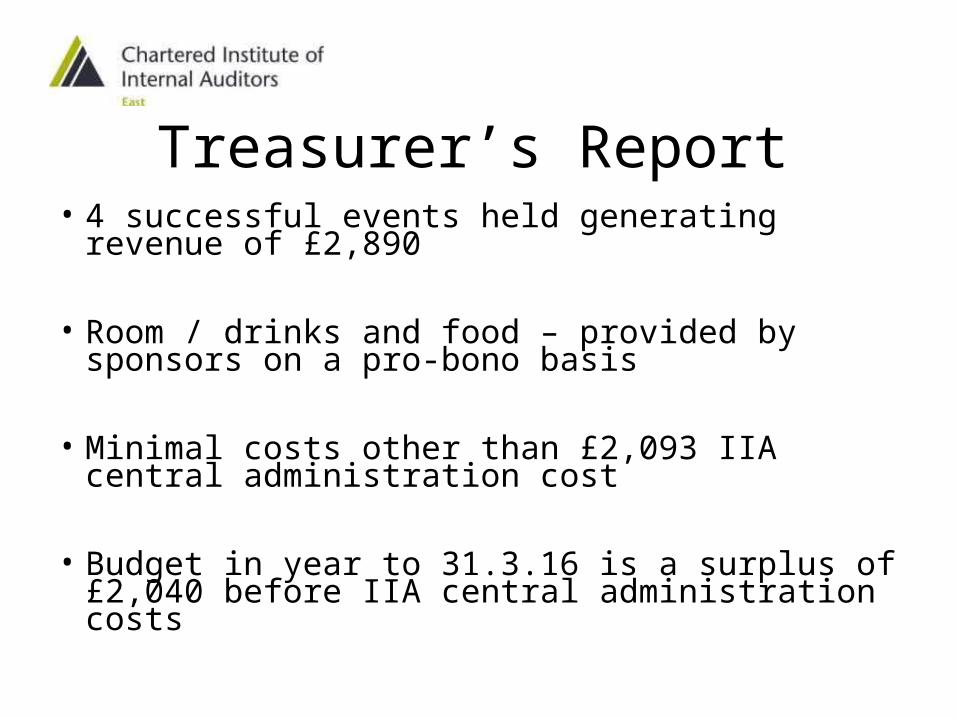

Treasurer’s Report

• 4 successful events held generating revenue of £2,890

• Room / drinks and food – provided by sponsors on a pro-bono basis

• Minimal costs other than £2,093 IIA central administration cost

• Budget in year to 31.3.16 is a surplus of £2,040 before IIA central administration costs

Treasurer’s Report

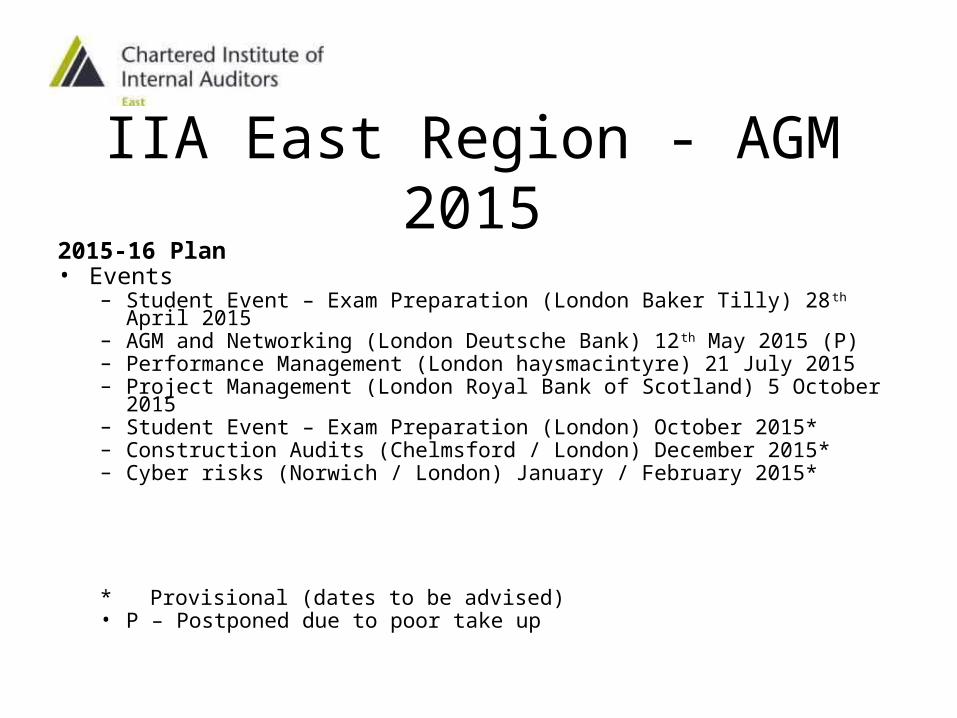

IIA East Region - AGM 20152015-16 Plan• Events

– Student Event – Exam Preparation (London Baker Tilly) 28th April 2015– AGM and Networking (London Deutsche Bank) 12th May 2015 (P)– Performance Management (London haysmacintyre) 21 July 2015– Project Management (London Royal Bank of Scotland) 5 October 2015– Student Event – Exam Preparation (London) October 2015*– Construction Audits (Chelmsford / London) December 2015*– Cyber risks (Norwich / London) January / February 2015*

* Provisional (dates to be advised)• P – Postponed due to poor take up

IIA East / South Mentor SchemeWhat is it?•Provides IIA East & South Members with access to a volunteer mentor•Advice and support in relation to professional Internal Audit development

Benefits for the person being mentored?•enhanced training and career development •influence in their attitudes and professional outlook •guide them round major decisions

Benefits for the Mentors?•satisfaction from helping others and seeing them progress •deeper and broader knowledge of their own and other organisations •job enrichment and the chance to build wider networks