implementation and consequential risks of a solar-based...

TRANSCRIPT

Transitions Pathways and Risk Analysis for Climate Change

Mitigation and Adaptation Strategies

Decarbonising our Energy System

Transformation pathways, policies and markets: spotlight on Greece

16 November 2018

Alexandros Nikas

Management & Decision Support Systems Lab

National Technical University of Athens (NTUA)

Implementation and consequential risks of a

solar-based transition pathway in Greece:

Insights from a stakeholder-driven analysis

CONTEXT

Motivation

Understanding the dynamics of a solar-based low-carbon transition of the Greek power

sector

Research questions

• What are the potential barriers to and consequences of such a transition?

• Can they be quantified, in terms of impact?

• How can science respond to actual policy demand?

• Can we bridge the infamous science-policy interface?

Carried out by

NTUA UPRC/TEES IBS

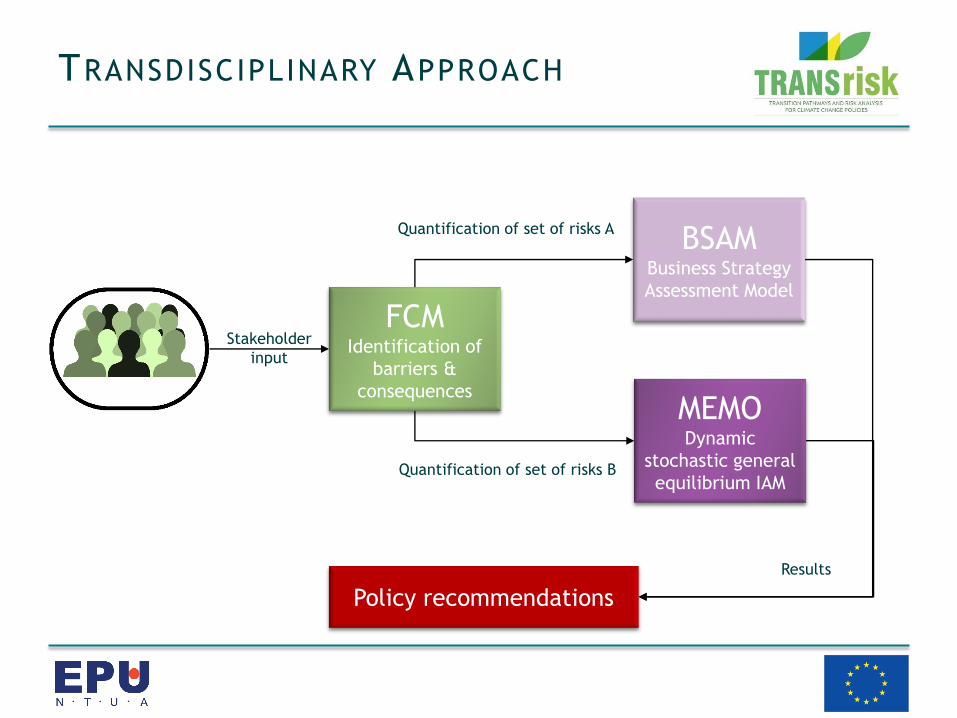

TRANSDISCIPLINARY APPROACH

BSAMBusiness Strategy

Assessment Model

MEMODynamic

stochastic general

equilibrium IAM

FCMIdentification of

barriers &

consequences

Policy recommendations

Stakeholder

input

Quantification of set of risks A

Quantification of set of risks B

Results

UNDERSTANDING BARRIERS

IMPLEMENTATION RISKS

• B1. Ongoing recession

• B2. Poor public acceptance

• B3. Unstable regulatory

framework

• B4. High technological costs

• B5. Poor political prioritisation

B1. Ongoingeconomic recession

B2. Publicacceptance

B3. Regulatoryframeworkinstability

B4. Technologicalcosts

B5. Poor politicalprioritisation

SCENARIOS

IDENTIFY ING POTENTIAL CONSEQUENCES

CONSEQUENTIAL RISKS

• C1. Costs for end users

• C2. Poor economic growth

• C3. Investments

• C4. Unemployment

• C5. Tariff deficits (again)

• A prosuming-oriented strategy perceived to have positive socioeconomic impacts

along the envisaged transition. Especially in a high adaptation challenges scenario.

• A centralised generation-based pathway perceived to have negligible socioeconomic

benefits, unless our future’s trends do not shift from historical patterns.

More importantly:

• Potential impact of energy storage and demand flexibility on wholesale electricity

prices and, in turn, electricity costs for end users.

• Potential impact of a wide-scale RES deployment on socioeconomic indices

(economic growth, investments, employment).

KEY STAKEHOLDER F IND INGS

R ISK QUANTIFICATION

BSAMBusiness Strategy

Assessment Model

MEMODynamic

stochastic general

equilibrium IAM

• Energy storage

• Wholesale electricity prices

• Wide-scale RES deployment

• Technological costs

• Economic growth

• Investments

• Employment

ECONOMIC R I SKS (BSAM)

-12

-9

-6

-3

0

3

6

9

12

1 2 3 4 5 6 7 8 9 10 11 12

Pri

ce d

iffe

rence

(€

/mw

h)

Month

Storage market share of 5%

SC01 SC11 SC21

-12

-9

-6

-3

0

3

6

9

12

1 2 3 4 5 6 7 8 9 10 11 12Pri

ce d

iffe

rence

(€

/mw

h)

Month

Storage market share of 10%

SC02 SC12 SC22

• Self-consumption favours

prosumers: they offset the

energy produced with energy

consumed at different times

(abolishing the grid’s role).

• Combined with the limited

flexibility of the Greek power

system, increasing self-

consumption could “force”

generators to bid higher.

• Increasing self-consumption

will increase, for some

months of the year, the price

that everybody else pays.

ECONOMIC R I SKS (MEMO)

• Across all scenarios, the

impact of RES-E deployment

on the Greek economy

becomes positive by 2040.

• In 2050, the Greek economy

would be 1.8% larger in the

RES scenario than in the BAU

scenario; GDP loss never

larger than 0.6% (-1% in high

technological costs scenario)

• Investment goods fuelled by

inflow of labour and capital.

-1,5%

-1,0%

-0,5%

0,0%

0,5%

1,0%

1,5%

2,0%

2017Q

12018Q

12019Q

12020Q

12021Q

12022Q

12023Q

12024Q

12025Q

12026Q

12027Q

12028Q

12029Q

12030Q

12031Q

12032Q

12033Q

12034Q

12035Q

12036Q

12037Q

12038Q

12039Q

12040Q

12041Q

12042Q

12043Q

12044Q

12045Q

12046Q

12047Q

12048Q

12049Q

12050Q

1

% o

f base

line G

DP

Effect of RES Deployment on GDP

-0,1%

0,0%

0,1%

0,2%

0,3%

0,4%

0,5%

0,6%

0,7%

2017Q

12018Q

12019Q

12020Q

12021Q

12022Q

12023Q

12024Q

12025Q

12026Q

12027Q

12028Q

12029Q

12030Q

12031Q

12032Q

12033Q

12034Q

12035Q

12036Q

12037Q

12038Q

12039Q

12040Q

12041Q

12042Q

12043Q

12044Q

12045Q

12046Q

12047Q

12048Q

12049Q

12050Q

1

% b

ase

line G

DP

Effect of RES Deployment on Investment

high tech costs expected tech costs low tech costs

SOCIAL R I SKS (MEMO)

• Larger wages and better job

finding rates encourage

activity and a miners’ shift to

other sectors.

• Increase in demand for goods,

greater real revenue for firms,

increases in real wages,

increases in the number of job

vacancies and higher chances

of unemployed finding a job.

• Temporary decrease in labour

productivity. Size and length

depend on investments/costs.

-0,4

-0,2

0

0,2

0,4

0,6

0,8

2017Q

1

2017Q

6

2017Q

11

2017Q

16

2017Q

21

2017Q

26

2017Q

31

2017Q

36

2017Q

41

2017Q

46

2017Q

51

2017Q

56

2017Q

61

2017Q

66

2017Q

71

2017Q

76

2017Q

81

2017Q

86

2017Q

91

2017Q

96

2017Q

101

2017Q

106

2017Q

111

2017Q

116

2017Q

121

2017Q

126

2017Q

131

2017Q

136

%

Effect of RES Deployment on the Activity Rate

-0,5

-0,4

-0,3

-0,2

-0,1

0

0,1

0,2

0,3

2017Q

1

2018Q

1

2019Q

1

2020Q

1

2021Q

1

2022Q

1

2023Q

1

2024Q

1

2025Q

1

2026Q

1

2027Q

1

2028Q

1

2029Q

1

2030Q

1

2031Q

1

2032Q

1

2033Q

1

2034Q

1

2035Q

1

2036Q

1

2037Q

1

2038Q

1

2039Q

1

2040Q

1

2041Q

1

2042Q

1

2043Q

1

2044Q

1

2045Q

1

2046Q

1

2047Q

1

2048Q

1

2049Q

1

2050Q

1

%

Effect of RES Deployment on the Unemployment Rate

high tech costs expected tech costs low tech costs

CONCLUS IONS

Renewables can facilitate the country’s economic recovery.

Optimising self-consumption is not always beneficial

(if optimality means decreasing the price that consumers without it must pay)

Self-consumption with storage must be evaluated with decreasing costs for storage, new

business models and regulatory frameworks (fair allocation of benefits among all actors)

Acknowledging the limitations of modelling activities

Assumptions outdated or unrealistic (e.g. fresh 2030 RES targets for Greece)

Unit commitment problem, grid inflexibility and technical aspects

Rigidity of wages (sectoral level), barriers of entry, structural changes’ effect to R&D

D I SCUSS ION/QUESTIONS

D I SCUSS ION/QUESTIONS

Appendix

(modelling assumptions)

SCENARIO A SSUMPTIONS

• Installed PV Capacity: {2016: 2,611 MWp}, {2025: 3,900 MWp}, {2035: 5,900 MWp}

• 3 energy storage (in small-scale PV) market share scenarios: 0%, 5%, and 10%

• Large-scale PV 6 : 1 small-scale

• Ceteris paribus (total power demand, fossil fuel prices, water reservoir levels, etc.)

• Elastic job search intensity (small wage changes many workers joining market)

• Electricity demand: linear trend {2020: 53 TWh} {2030: 58.5 TWh}

COST A SSUMPTIONS

• For one 1 MW installation (large-scale solar projects): The average annual

capacity factor is taken to be 22% and the annual efficiency decrease 0.5%.

Furthermore, the operating and maintenance cost is assumed to be equal to

1% of the total investment cost per annum. Investment cost is 1 €/W.

• For small roof-mounted PV systems: The operating and maintenance cost is

assumed to be equal to 2% of the total investment cost per annum. The

average annual capacity factor for rooftop PV installations is 15%. The

annual efficiency decrease has been assumed to be 0.5%. Investment cost is

1.3 €/W.

• The capital cost for onshore wind power systems in Greece is 1.2 €/W. The

average annual capacity factor for interconnected wind RES-E farms is 25%.

A SSUMPTIONS FOR PV/W IND CAPACITY

Year PV Capacity (MW) Wind Capacity (MW)

2016 2,443 1,987

2020 2,900 2,831

2025 3,900 3,675

2030 4,900 4,519

2035 5,900 5,363

2040 6,900 6,207

2045 7,900 7,051

2050 8,900 7,900

A SSUMPTIONS FOR OTHER TECHNOLOGIES

Generation mix for residual demand (%)

Year Lignite Natural gas Hydro

2016 32 41 27

2020 25 45 30

2025 26 44 30

2030 25 42 32

2035 26 41 33

2040 28 37 35

2045 15 47 38

2050 9 53 38