implementing should-be costing - procureforce.co · implementing should-be costing ... a recording...

TRANSCRIPT

Implementing Should-Be Costing September 14, 2016

2

Attendees will be in listen only mode

A recording of this presentation and the slides will be available on the APD Website

Webinar attendees who complete the webinar feedback survey will receive the slides by email

Welcome to the Webinar

3

We make purchasing a competitive advantage

We lever a network of >10,000

supply chain professionals,

and have both onshore and

offshore delivery capabilities

Our solutions are empowered

by a purpose built, proprietary

technology platform

We have a database of >1,000

cost elements based of >850

cost blueprints.

All of our solutions are provided on a modular, as-a-service, basis.

People Tools &

Technology Intelligence

4

Today’s Presenter:

Jeoff Burris Principal, Advanced Purchasing Dynamics

▸ >20 years manufacturing purchasing experience

▸ Founded APD in 2004

▸ Helps clients make their investment in purchasing a competitive advantage

5

Today’s Presenter:

Steve Haburne Business Solutions Specialist, Advanced Purchasing Dynamics

▸ Project Management Leadership for Consulting and ProcureForce Implementation

▸ 3 years with APD’s ProcureForce Technology Platform

▸ Helps clients make their investment in purchasing a competitive advantage

On Demand Webinars and White Papers

Visit the APD Knowledge Center

http://www.apurchasingd.com/knowledge-center/

7

Webinar: October 19 – 10:00 EST

Adding Value on

New Programs

58% of the CEO’s we surveyed questioned the value

their purchasing organizations drop to the bottom

line. An often cited statistic is that 70-80% of a

products cost structure is determined during the time it

is being developed.

This webinar will identify the practices leading

purchasing organizations employ to add value during

the design phase and how APD’s ProcureForce

software supports those practices.

8

Webinar: October 26 – 10:00 EST

Recruiting – and Retaining – Purchasing Superheroes The market for purchasing talent is very hot. Join us to learn what it takes to land highly sought after purchasing professionals, and what you can do to retain your top performers. We’ll share insights from our recent survey of nearly 200 purchasing professionals, as well as strategies we’ve seen work in this highly competitive marketplace.

9

Purpose

Identify the savings potential of should be

costing tools.

Overview the steps companies are taking

to implement cost tools.

Demonstrate how ProcureForce helps

them achieve the savings.

10

Agenda

APD Intro

Introduction to the cost and collaboration curve

Attribute models

Optimizing detailed cost breakdowns

Statistical should be models

Wrap up

11

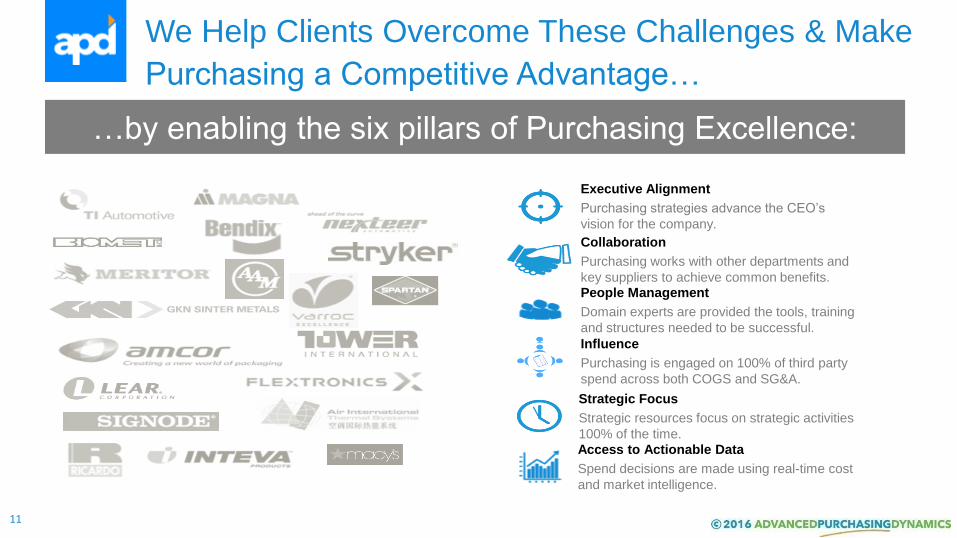

…by enabling the six pillars of Purchasing Excellence:

We Help Clients Overcome These Challenges & Make

Purchasing a Competitive Advantage…

Executive Alignment

Purchasing strategies advance the CEO’s

vision for the company.

Collaboration

Purchasing works with other departments and

key suppliers to achieve common benefits. People Management

Domain experts are provided the tools, training

and structures needed to be successful.

Strategic Focus

Strategic resources focus on strategic activities

100% of the time.

Influence

Purchasing is engaged on 100% of third party

spend across both COGS and SG&A.

Access to Actionable Data

Spend decisions are made using real-time cost

and market intelligence.

12

Introducing APD

We have 12 years of experience in empowering Purchasing

teams to focus on what they do best.

People

Supply strategies should be built

and implemented by domain

experts who spend 100% of their

time on value added activities

Intelligence Tools & Tech

Sourcing and pricing decisions

should be made based on a

detailed understanding of cost

drivers and market intelligence

Customized solutions; There is no one size fits all approach.

The execution of market leading

supply strategies should be

expedited by the use of built-for-

purpose technology and

processes

➤ Find purchasing professionals

(direct hire or contract)

➤ Low cost purchasing support

services Center of Excellence

➤ Buyer skill development

training

➤ Open-book cost models

➤ Real-time analysis of supplier

price quotes

➤ Identification of capable

suppliers

➤ Benchmark cost models

➤ Cloud based, SaaS tool for

Sourcing with Should Be

Costing

➤ Library of over 850 cost

models to determine “should-

cost” pricing

➤ Sourcing blueprints that cover

all major spend areas

13

USA

Leadership, Program

Management and

Governance

India

Purchasing Support &

Analytics Center of

Excellence

Plymouth, MI

Chennai, India

Delivered by a Distributed Global Model

APD’s leadership team has over 10 years of experience in delivering

purchasing support and analytics services from Chennai.

14

“we spend so much time on administrative tasks that my team cannot

focus on the value added work they need to perform to succeed”

We Frequently Hear these Challenges from

Purchasing Leaders

“we collect so much data from our suppliers, but we do not

have a good way of turning that into actionable intelligence”

“we do not have a strong understanding of what products or

services should cost, and so we rely on the market or our

suppliers to tell us” Purchasing Leader

15

Multiple Tool Approach

2-5 %

3-6 %

3-7 %

Price Focused

Knowledge Based

Collaborative

GOAL

16

Difficulty and Benefit of Moving up the Curve

Easy with High Return

Easy with Low Return

Difficult with High Return

Difficult with Low Return

17

Single Tool Approach to Pricing

18

Multiple Tool Approach

19

Where are your commodities now?

20

Results of survey

Used on 80-100% of spend

Used on 60-79% of spend

Used on 40-59% of spend

Used on 20-39% of spend

Used on 1-19% of spend

Not Used

Piece Price is the only Tool Used

11% 22% 11%

Detailed Cost Breakdowns

44% 11% 11% 22%

Cost Models Using

Information from Detailed Cost Breakdowns

11% 11% 33%

Regression Models

11% 33%

E-auctions 11% 22%

Cost Estimates Developed By a Cost Estimating Group of Person

11% 11% 22%

21

How APD Customers Have Progressed

Value

Alignment

Open Book - through market testing

new or existing components

Knowledge Based Quote Model - through market testing new or existing components

Attribute Based Quote Model development through market

testing or analysis of existing pricing

Variance Analysis of existing quote history

Cost Breakdown improvement

22

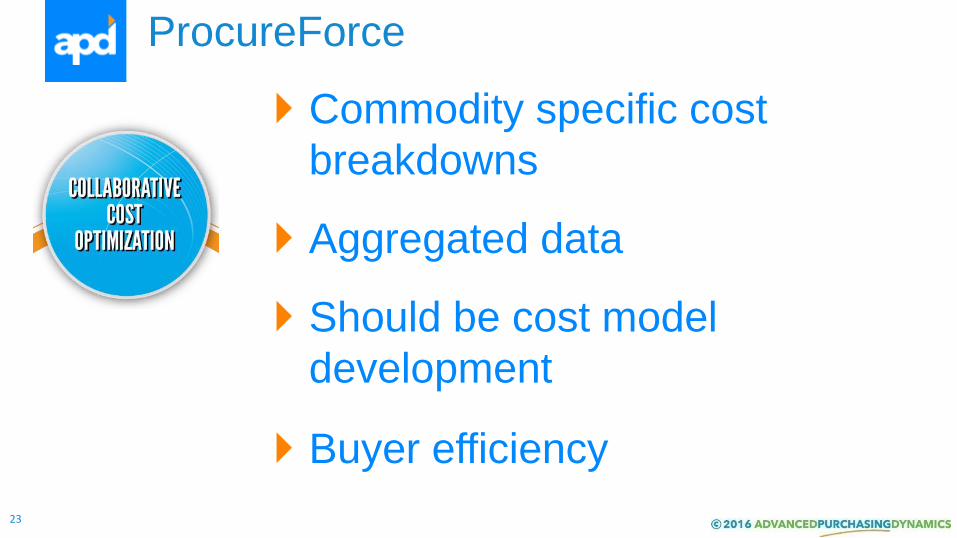

ProcureForce is a technology platform

that optimizes the way manufacturers

deliver savings and manage direct

material purchases.

ProcureForce.co

ProcureForce

23

ProcureForce

Commodity specific cost

breakdowns

Aggregated data

Should be cost model

development

Buyer efficiency

24

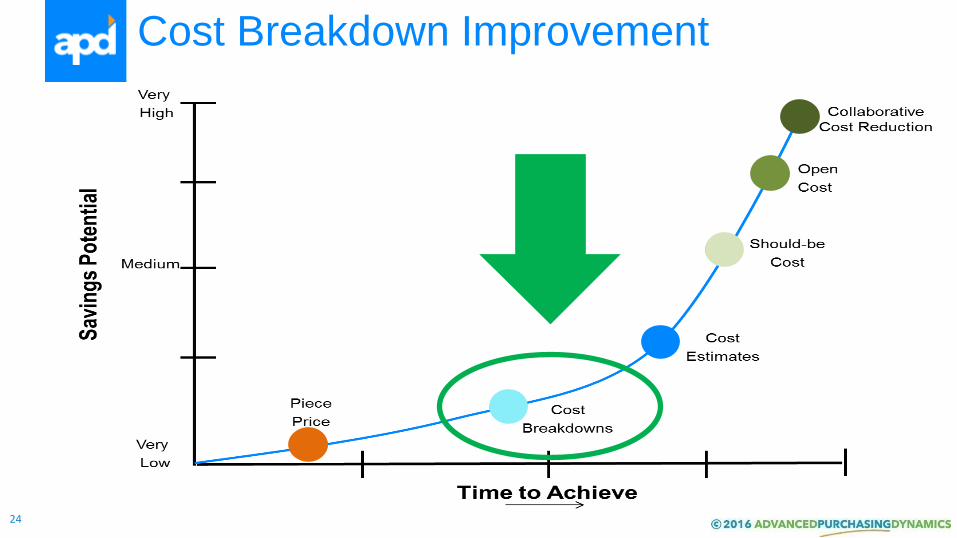

Cost Breakdown Improvement

25

The Case for Cost Breakdowns

Provides buyers and managers with actionable data to

improve purchased material cost.

Provides information required to understand global

sourcing opportunities.

Improves negotiation results regardless of the negotiating

model.

Can form the basis for more collaborative supplier

relationships based upon cost models and tools to reduce

waste and cost.

26

Benefits to Buyers

Data driven approach, used consistently makes issue resolution easier.

Can change the tenor of negotiations from positional (win/lose) to less stressful, more collaborative, partnership based.

Increases buyers knowledge of operations as well as cost accounting thus providing more ability for lateral and promotional organization moves.

27

Benefits to Suppliers

More objective and equitable quoting process.

Provide supplier feedback on cost competitiveness.

Ensures pricing is tied to cost.

Common understanding of cost structure provides supplier and customer with the basis for a collaborative relationship.

28

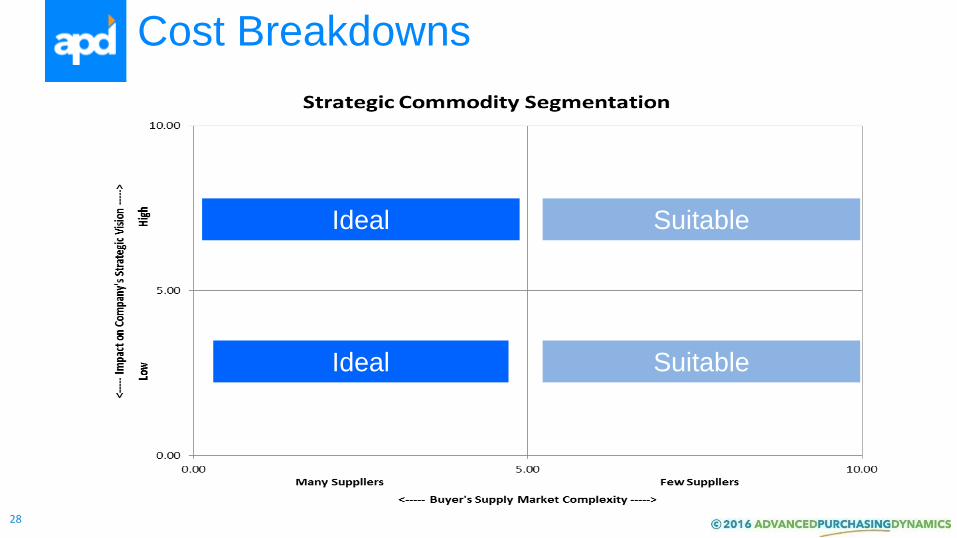

Cost Breakdowns

Ideal

Suitable Ideal

Suitable

29

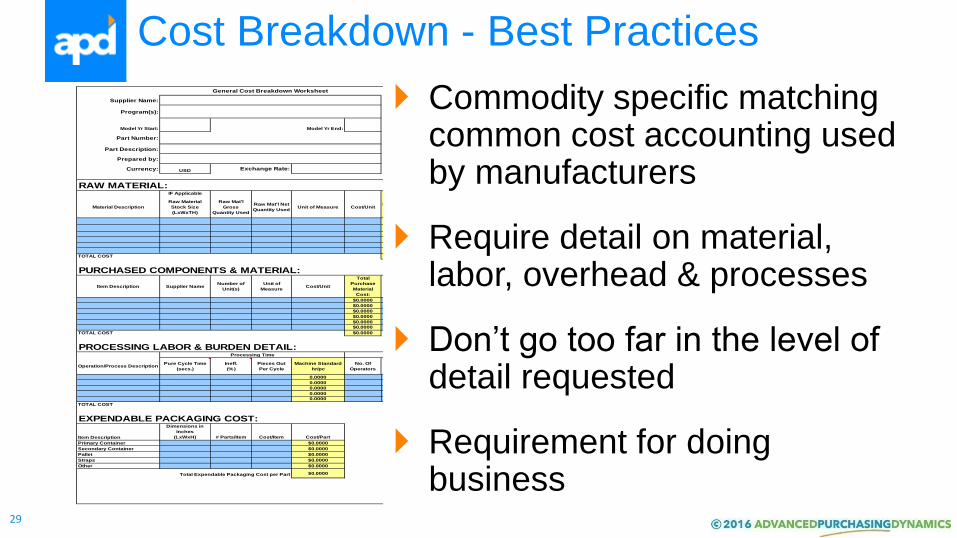

Cost Breakdown - Best Practices

Supplier Name: Date: Annual Volume Quoted:

Program(s): PCRN #Supplier Mfg. Location:

Model Yr Start: Model Yr End:RFQ

Supplier Shipping Location:

Part Number: REV LEVELCustomer Ship To Location:

Part Description: Tooling Capacity:

Prepared by:

Currency: USD

RAW MATERIAL:IF Applicable

Material Description

Raw Material

Stock Size

(LxWxTH)

Raw Mat'l

Gross

Quantity Used

Raw Mat'l Net

Quantity UsedUnit of Measure Cost/Unit

Gross Raw

Material Cost

Total

$

Scrap Weight

Scrap

Resale

Cost/Unit

Eng. Scrap

Credit

$

Raw Material

Cost:

Process Scrap

%

Process Scrap

$

Raw Mat'l

SG&A

Markup %

Raw Mat'l

Profit Markup

%

Markup Total

$

Total Raw

Material Cost:

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

TOTAL COST $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

PURCHASED COMPONENTS & MATERIAL:

Item Description Supplier NameNumber of

Unit(s)

Unit of

MeasureCost/Unit

Total

Purchase

Material

Cost:

Process

Scrap %

Process

Scrap $

Purch.

Comp.

SG&A

Markup %

Purch. Comp.

Profit Markup

%

Markup Total

$

Total

Purchase

Material Cost

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

TOTAL COST $0.0000 $0.0000 $0.0000 $0.0000

PROCESSING LABOR & BURDEN DETAIL:

Operation/Process DescriptionPure Cycle Time

(secs.)

Ineff.

(%)

Pieces Out

Per Cycle

Machine Standard

hr/pc

No. Of

Operators

Direct Labor

Rate

($/hr)

Labor Fringe

Rate

($/hr)

Labor Cost

($)

Equipment

TypeBurden Rate

Burden/Overh

ead Cost

Total Labor &

Burden Cost

Process

Scrap %

Process

Scrap $

Processing

SG&A

Markup %

Processing

Profit Markup

%

Markup Total

$

Total

Processing

Cost

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

TOTAL COST $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

Item Description

Dimensions in

Inches

(LxWxH) # Parts/Item Cost/Item Cost/Part $0.0000

Primary Container $0.0000 $0.0000

Secondary Container $0.0000 $0.0000

Pallet $0.0000 % of TMC #DIV/0! $0.0000

Straps $0.0000 $0.0000

Other $0.0000 $0.0000

Total Expendable Packaging Cost per Part $0.0000 $0.0000

$0.0000

EXPENDABLE PACKAGING COST: FREIGHT COST: PRICE SUMMARY:

General Cost Breakdown Worksheet

Note: YELLOW CELLS are

automatically calculated: BLUE

CELLS are inputted by supplierExchange Rate:

Processing Time Direct Labor Cost Manufacturing Burden/Overhead Cost

Terms Quoted

(Input Ex-Works or

Delivered) Ex-Works Total Raw Mat'l and Purch. Component Cost

Title Transfer Point Total Labor & Burden Processing Costs

Grand Total Proposed Piece Price w/Freight

Supplier Mfg. Location Total Manufacturing Cost (TMC)

Mfg. Location Total SG&A and Profit Cost

Freight Cost per Part Packaging Cost

Freight

Grand Total Proposed Piece Price w/o Freight

0.0% 0.0% 0.0% 0.0% 0.0% 0.0%0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Raw Mat'l Purchase Mat'l Labor & Burden SG&A & Profit Packaging Freight

% o

f To

tal P

ropo

sed

Pie

ce P

rice

Category

% Breakout Comparison to Grand Total Proposed Piece Price

Commodity specific matching common cost accounting used by manufacturers

Require detail on material, labor, overhead & processes

Don’t go too far in the level of detail requested

Requirement for doing business

30

Cost Breakdown - Best Practices

Supplier Name: Date: Annual Volume Quoted:

Program(s): PCRN #Supplier Mfg. Location:

Model Yr Start: Model Yr End:RFQ

Supplier Shipping Location:

Part Number: REV LEVELCustomer Ship To Location:

Part Description: Tooling Capacity:

Prepared by:

Currency: USD

RAW MATERIAL:IF Applicable

Material Description

Raw Material

Stock Size

(LxWxTH)

Raw Mat'l

Gross

Quantity Used

Raw Mat'l Net

Quantity UsedUnit of Measure Cost/Unit

Gross Raw

Material Cost

Total

$

Scrap Weight

Scrap

Resale

Cost/Unit

Eng. Scrap

Credit

$

Raw Material

Cost:

Process Scrap

%

Process Scrap

$

Raw Mat'l

SG&A

Markup %

Raw Mat'l

Profit Markup

%

Markup Total

$

Total Raw

Material Cost:

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

$0.0000 0.00 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

TOTAL COST $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

PURCHASED COMPONENTS & MATERIAL:

Item Description Supplier NameNumber of

Unit(s)

Unit of

MeasureCost/Unit

Total

Purchase

Material

Cost:

Process

Scrap %

Process

Scrap $

Purch.

Comp.

SG&A

Markup %

Purch. Comp.

Profit Markup

%

Markup Total

$

Total

Purchase

Material Cost

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

$0.0000 $0.0000 $0.0000 $0.0000

TOTAL COST $0.0000 $0.0000 $0.0000 $0.0000

PROCESSING LABOR & BURDEN DETAIL:

Operation/Process DescriptionPure Cycle Time

(secs.)

Ineff.

(%)

Pieces Out

Per Cycle

Machine Standard

hr/pc

No. Of

Operators

Direct Labor

Rate

($/hr)

Labor Fringe

Rate

($/hr)

Labor Cost

($)

Equipment

TypeBurden Rate

Burden/Overh

ead Cost

Total Labor &

Burden Cost

Process

Scrap %

Process

Scrap $

Processing

SG&A

Markup %

Processing

Profit Markup

%

Markup Total

$

Total

Processing

Cost

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

TOTAL COST $0.0000 $0.0000 $0.0000 $0.0000 $0.0000 $0.0000

Item Description

Dimensions in

Inches

(LxWxH) # Parts/Item Cost/Item Cost/Part $0.0000

Primary Container $0.0000 $0.0000

Secondary Container $0.0000 $0.0000

Pallet $0.0000 % of TMC #DIV/0! $0.0000

Straps $0.0000 $0.0000

Other $0.0000 $0.0000

Total Expendable Packaging Cost per Part $0.0000 $0.0000

$0.0000

EXPENDABLE PACKAGING COST: FREIGHT COST: PRICE SUMMARY:

General Cost Breakdown Worksheet

Note: YELLOW CELLS are

automatically calculated: BLUE

CELLS are inputted by supplierExchange Rate:

Processing Time Direct Labor Cost Manufacturing Burden/Overhead Cost

Terms Quoted

(Input Ex-Works or

Delivered) Ex-Works Total Raw Mat'l and Purch. Component Cost

Title Transfer Point Total Labor & Burden Processing Costs

Grand Total Proposed Piece Price w/Freight

Supplier Mfg. Location Total Manufacturing Cost (TMC)

Mfg. Location Total SG&A and Profit Cost

Freight Cost per Part Packaging Cost

Freight

Grand Total Proposed Piece Price w/o Freight

0.0% 0.0% 0.0% 0.0% 0.0% 0.0%0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Raw Mat'l Purchase Mat'l Labor & Burden SG&A & Profit Packaging Freight

% o

f To

tal P

ropo

sed

Pie

ce P

rice

Category

% Breakout Comparison to Grand Total Proposed Piece Price

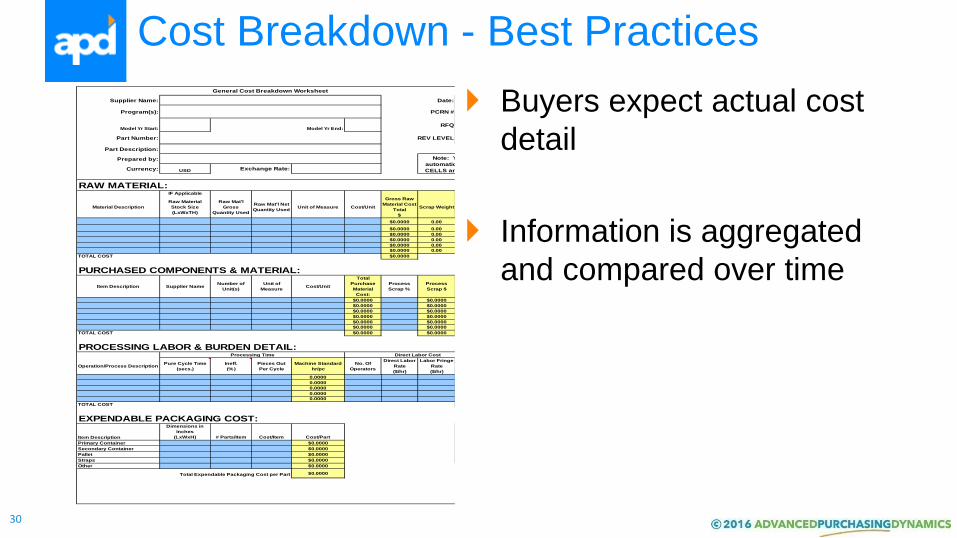

Buyers expect actual cost

detail

Information is aggregated

and compared over time

31

Variance Analysis

Analysis of multiple detailed cost

breakdowns

Identify savings opportunities

32

Step 1

Extract & consolidate the cost elements from quotation history.

Step 2

Identify the cost variances across material, labor, burden, cycle time, SG&A and packaging.

Step 3

Identify areas for investigation.

Part NumberAnnual

Volume

Supplier

Pricing

Variance as a

Service

Per Piece

Difference% Opportunity

Annual

Opportunity

Part 1 330,810 $1.3676 $1.0767 ($0.2909) -27.02% $96,226

Part 2 307,000 $1.3841 $1.3304 ($0.0538) -4.04% $16,506

Part 3 237,000 $1.1758 $1.1758 $0.0000 0.00% $0

Part 4 156,600 $1.3230 $1.0489 ($0.2740) -26.12% $42,914

Part 5 116,000 $1.1693 $0.9422 ($0.2271) -24.11% $26,349

Part 6 107,000 $1.2599 $1.0271 ($0.2328) -22.66% $24,906

Part 7 175,000 $1.2731 $1.0546 ($0.2185) -20.72% $38,239

$1,856,427 $1,611,287 ($245,140) -13% $245,140Totals

Variance as a Service

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

Part 1 Part 2 Part 3 Part 4 Part 5 Part 6 Part 7

Supplier Quote vs. Variance as a Service Price

Supplier Pricing

Variance as aService

Variance Analysis

ProcureForce Demo

34

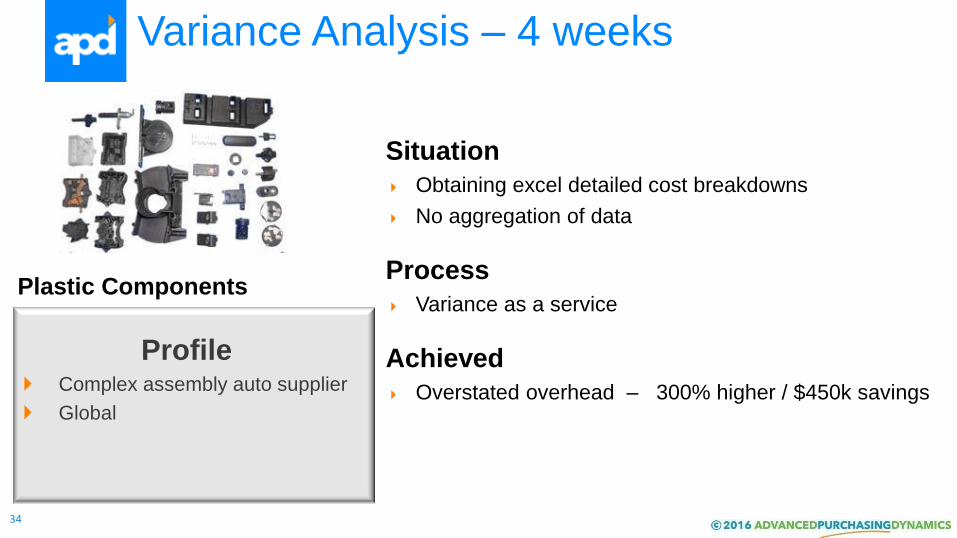

Profile Complex assembly auto supplier

Global

Variance Analysis – 4 weeks

Situation

Obtaining excel detailed cost breakdowns

No aggregation of data

Process

Variance as a service

Achieved

Overstated overhead – 300% higher / $450k savings

Plastic Components

35

Profile Interior Systems Automotive

Supplier

Global

Variance Analysis & Benchmarking – 12 weeks

Situation

Obtaining excel detailed cost breakdowns

No aggregation of data

Process

Variance as a service combined with benchmarking

Achieved

Identified $4.1 mil of savings on $34 mil of spend

Same purchased component 40% higher price -- $294 k savings

Complex Assemblies

36

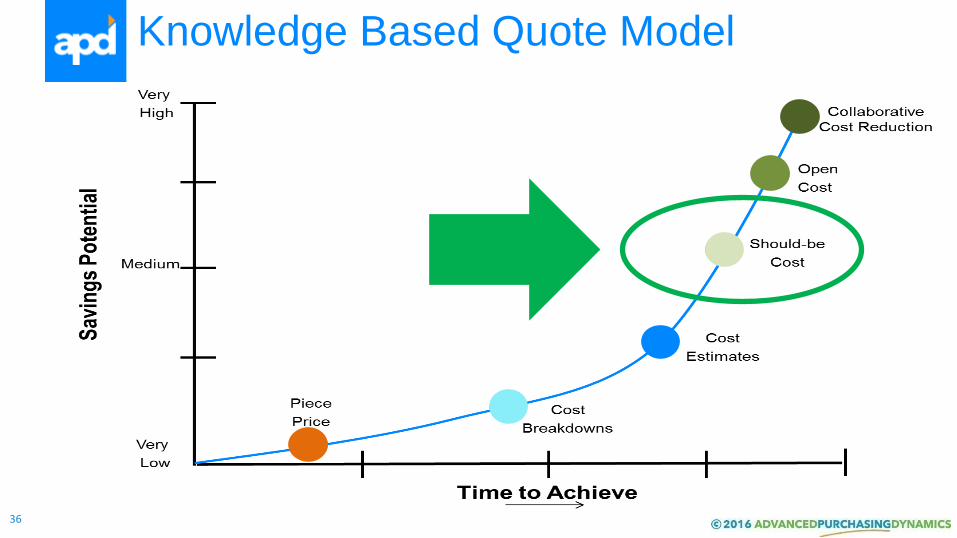

Knowledge Based Quote Model

37

Knowledge Based Quote Model

Statistic based developed using data

gathered through knowledge based quote

activity with a high degree of accuracy and

competitive pressure.

38

Would it be beneficial to know?

That a suppliers labor rate is in the top 10% in competitiveness?

The likelihood that a supplier in Mexico would have an overhead rate of $100?

What quote should be if all the cost drivers are of average value?

What quote should be if all cost drivers were in the top 25%?

39

Statistical Analysis

Statistical Analysis provides us with the ability to analyze cost data from a large number of detailed cost breakdowns to: Determine the relative competitiveness of

suppliers cost structures.

Provide credible feedback to suppliers on their cost competitiveness.

Develop knowledge based cost models.

40

Ideal

Suitable Ideal

Suitable

Knowledge Based Quote Model

41

Building a Statistical Model

Step 1

Extract & consolidate the cost elements from quotation history.

Step 2

Create a statistical model.

Step 3

Compare supplier quotes to the model.

ProcureForce Demo

43

Profile Complex assembly powertrain

manufacturer

Refocusing business to core

and non-core processes

From No Price to Statistical Model – 22 Weeks

Situation

PM production viewed as non-strategic

100 components to source

No supply Base

No history of detailed cost breakdowns.

Limited review of cost competiveness on 30% of spend

Process

Utilized multi round market test in awardable lots

Engaged 22 suppliers in first round

Achieved

Achieved $182k/10% reduction

Identified low cost supply base

Developed statistical model for US

Powdered Metal Components

44

Profile Specialty vehicle OEM

Highly customized

From Price to Statistical Model – 14 Weeks

Situation

12 suppliers – US and Mexico

Short lead times on 30% of spend leaving no time for competitive sourcing

No history of detailed cost breakdowns

Process

Utilized multi round market test of 10% of total spend

Achieved

$220k/16% savings

Obtained and verified detailed cost breakdowns

Identified 4 low cost producers

Developed statistical models for Mexico and US

Wire Harnesses

45

Attribute Cost Models

46

Attribute Based Quote Models

Developed based upon regression performed using cost drivers such as physical part attributes.

Usually developed when suppliers will not provide detailed cost breakdowns.

Best if done when pricing has been established with competitive pressure.

47

Attribute Based Quote Models

Does not require supplier participation.

Easy to develop.

Less accurate – used mostly to identify “outliers” for investigation.

Used for Bearings, Seals, Motors…..

Easily combined with a benchmarking center

48

Attribute Models

Suitable

Ideal

Suitable

Suitable

49

Building a Regression Model

Step 1

Brainstorm Possible Cost Drivers

Step 2

Collect Data

Step 3

Use Excel to run Regression Analysis and Generate Regression Model

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.998329266

R Square 0.996661324

Adjusted R Square 0.995910121

Standard Error 0.157570411

Observations 50

ANOVA

df SS MS F Significance F

Regression 9 296.4712646 32.94125163 1326.755088 1.30381E-46

Residual 40 0.993137375 0.024828434

Total 49 297.464402

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 0.667731785 0.101002613 6.611034742 6.55205E-08 0.463597889 0.871865681 0.463597889 0.871865681

Length of Tube (ft) 0.210507973 0.038580536 5.45632578 2.74035E-06 0.132533801 0.288482144 0.132533801 0.288482144

Diameter of Tube (in) 0.401705199 0.087802546 4.575097391 4.53525E-05 0.224249634 0.579160764 0.224249634 0.579160764

# of Bends 0.133159068 0.034831856 3.822910476 0.000451453 0.062761261 0.203556875 0.062761261 0.203556875

Part Weight (grams) 0.019965735 0.007787591 2.563788456 0.014216609 0.004226427 0.035705043 0.004226427 0.035705043

mm of MIG 0.097684007 0.038584272 2.531705335 0.015382746 0.019702285 0.175665729 0.019702285 0.175665729

# of Attachments -0.16129352 0.079039874 -2.04066017 0.047922823 -0.321039068 -0.00154798 -0.321039068 -0.001547978

Type of Tube (Fuel/Water) -0.01499527 0.047278441 -0.31716931 0.752764762 -0.110548565 0.080558024 -0.110548565 0.080558024

# of Critical Characteristics -0.01801595 0.017651663 -1.02063773 0.313559654 -0.053691296 0.017659389 -0.053691296 0.017659389

Contains Fixed Label 0.028842843 0.04916095 0.586702306 0.560700514 -0.070515143 0.128200829 -0.070515143 0.128200829

R Square is called the coefficient of determination. It compares estimated and actual y-values, and ranges in value

from 0 to 1. If it is 1, there is a perfect correlation in the sample — there is no difference between the estimated y-

value and the actual y-value. At the other end if it is 0 there is no correlation between the estimated y-value and

actual y-value.

In the example here the Piece Price is a function of Length of Tube, Diameter of Tube, # of Bends, Part Weight, mm of

MIG, # of attachments, Type of Tube, # of Critical Characteristics and Fixed Label, with an R Square value of = .9966. It

can be interpreted as "99.66% of the total variation of piece price is explained by Length of Tube, Diameter of Tube, #

of Bends, Part Weight, mm of MIG, # of attachments, Type of Tube, # of Critical Characteristics and Fixed Label, and

the remaining 0.34% is accounted for by something other than these attributes.

Formula = Intercept + (Length of Tube coefficient * ft of Tube) + (Diameter of Tube coefficient * diameter of tube) + (# of Bends coefficient * # of Bends) + (Part Weight coefficient *

part weight) + (mm of MIG coefficient * mm of MIG) + (# of Attachments coefficient * # of Attachments) + (Type of Tube coefficient * Type of Tube) + (# of Critical Characteristics

coefficient * # of Critical Characteristics) + (Contains Fixed Label coefficient * Contains Fixed Label) = Estimated output value (y)

ProcureForce Demo

51

Profile Complex assembly auto supplier

Regional buyer in global

company

Regression Analysis – 2 weeks

Situation

Obtaining excel detailed cost breakdowns

No aggregation of data

Process

Buyer performed multi-variable regression

Identified outliers

Review historical cost breakdowns on outliers and conforming

Achieved

$275k savings

Purchased Components

52

Open Book

53

Open Book Cost Models

Developed on a supplier by supplier basis based upon manufacturing cost studies on supplier shop floor – Each stamping supplier would have a unique cost model.

54

Open Book Cost Models

Highly credible and accurate

Time intensive to develop

Requires detailed supplier participation

Used for Stampings, injection molding, fabrication, fasteners

55

Open Book Costing

Suitable

Suitable Ideal

56

Profile Specialty vehicle OEM

Invested in metal fabrication

when key supplier went out of

business

From Limited Cost to Open Book – 20 Weeks

Situation

CEO questioned competitiveness of in-house mfg

12 fabrication suppliers

Limited detail on cost breakdowns

Process

Utilized multi round market test verified with open book costing of most cost competitive suppliers (6)

Utilized Strategic Sourcing Process

Achieved

Savings of $1.4 mils / 12%

Established cost models to use with all fabrication suppliers to manage ongoing pricing for new and revised parts

Reduced supply base from 12 to 4-5 BIC suppliers while closing internal manufacturing

Metal Fabrications

57

Multiple Tool Approach

2-5 %

3-6 %

3-7 %

Price Focused

Knowledge Based

Collaborative

GOAL

58

Collaboration is Key

Open and honest dialogue about costs

Collaboration to reduce costs

59

Available in the APD

Knowledge Center

Cost Models White Paper:

60

How APD Customers Have Progressed

Value

Alignment

Open Book - through market testing

new or existing components

Knowledge Based Quote Model - through market testing new or existing components

Attribute Based Quote Model development through market

testing or analysis of existing pricing

Variance Analysis of existing quote history

Cost Breakdown improvement

61

Summary

Significant savings opportunities and buyer workload reduction exist using cost knowledge and collaboration.

Using the right approach results can be achieved in weeks.

62

Next Steps

Thank you for your time.

To continue the conversation, your key APD points of contact are:

Mike Wynn

Sr. Director

Advanced Purchasing Dynamics

+1 734 927 0836 ext.106 | [email protected]

Jeoff Burris

Principal

Advanced Purchasing Dynamics

+1 734 748 0542| [email protected]