improve domestic payment “h infrastructure and … · improve domestic payment ... broadening the...

TRANSCRIPT

Remittances in ACP Countries: Key Challenges and Ways ForwardInforming Discussions of the ACP-EU Dialogue on Migration and Development

improve domestic payment infrastructure and access to new technologies

Improving domestic payment infrastructure and access to new technologies begins by broadening the typology of formal remittance channels.Developing multiple pathways to send and receive remittances addresses several challenges that impact directly the lives of migrants. The use of technologies such as mobile phones, postal networks, and other relevant operators can address barriers like high sending remittance

costs and the lack of access to formal remittance services. However significant obstacles remain. For example, evidence indicates that cross-border mobile services are well used only when consumers are already using mobile payments for their everyday domestic financial needs. It follows that, until significant domestic use of mobile payments and cross-border mobile services are in place, costs will remain high for service providers creating barriers

to the facilitation of international remittance flows.

This ‘How to’ piece is drawn directly from ACP-EU Migration publication “Remittances in ACP countries: Key Challenges and Ways Forward” and will explore potential approaches to improving domestic payment infrastructure and migrant access to new technologies.

Background

“How to”

legislation

alternative Banking options

infrastructure and technology

Establishing an enabling regulatory framework for new technology at the domestic level entails striking a balance between facilitating remittance flows and assessing individual transfers and the risks associated with them. Particularly those associated to Anti-Money Laundering (AML) and Counter-Financing of Terrorism (CFT) ! .

Increasing telephone network coverage is of critical importance, particularly in key target areas which currently lack access to financial institutions;

Initiatives to achieve interoperability between different product providers should be considered, as many mobile-based services operate on a closed loop basis, which means that payments can only be made to another individual on the same network. Stakeholder consultation and coordination is essential to cope with the associated concerns, both from a market risk and a commercial perspective;

Support the introduction of digital acceptance terminals, particularly in isolated areas where infrastructure is currently lacking ! and the ability of Remittance Service Providers (RSPs) to offer digital payment services is hence limited. Support could include tax incentives, subsidiaries and grants for setting up non-cash payment services outside of urban areas, data collection to demonstrate business potential in these areas and well as assistance with agent and consumer education.

Support Remittance Service Providers (RSPs) onboarding of and managing of agents (entities which distribute remittance transfers on behalf of a RSP). This support could include: clear procedures for appointing agents; investment in technology, particularly the development of interfaces between the agent and the money transfer operator or bank systems and; staff training for banks in how to manage agents.

Support access to “bricks and mortar” financial services. These are small and medium sized businesses and non-banking institutions acting as Remittance Service Providers (RSPs). A good example is the promotion of (rural) post offices as RSPs and the establishment of a link between remittances and postal-account based services.

education and awareness

Support nationwide education and awareness raising campaigns to ensure usage of remittance services by receivers of remittances whose financial literacy levels might be limited. Specifically, campaigns targeting the senders of remittances, given their critical role as the initiator of the transaction.

“Remittances in ACP countries: Key Challenges and Ways Forward” | ACP-EU Migration Action

Remittances in ACP Countries: Key Challenges and Ways ForwardInforming Discussions of the ACP-EU Dialogue on Migration and Development

resources and good Practices

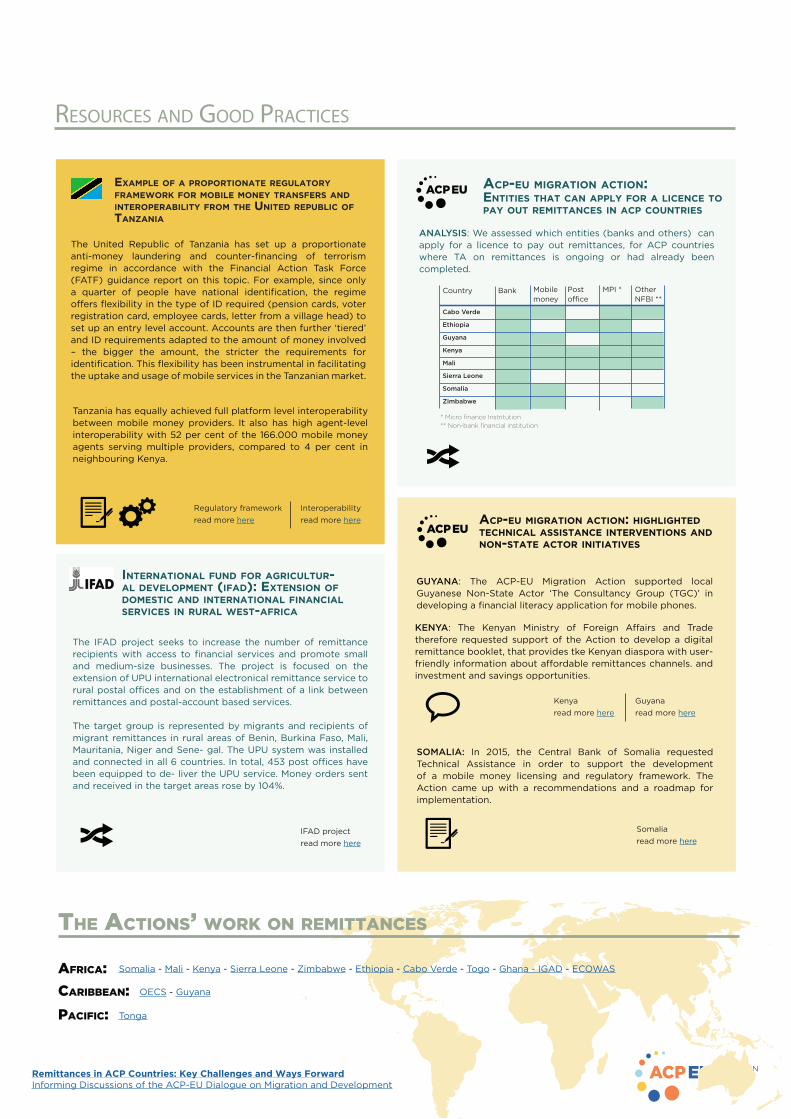

example of a proportionate regulatory framework for moBile money transfers and interoperaBility from the united repuBlic of tanzania

international fund for agricultur-al development (ifad): extension of domestic and international financial services in rural west-africa

The United Republic of Tanzania has set up a proportionate anti-money laundering and counter-financing of terrorism regime in accordance with the Financial Action Task Force (FATF) guidance report on this topic. For example, since only a quarter of people have national identification, the regime offers flexibility in the type of ID required (pension cards, voter registration card, employee cards, letter from a village head) to set up an entry level account. Accounts are then further ‘tiered’ and ID requirements adapted to the amount of money involved – the bigger the amount, the stricter the requirements for identification. This flexibility has been instrumental in facilitating the uptake and usage of mobile services in the Tanzanian market.

Tanzania has equally achieved full platform level interoperability between mobile money providers. It also has high agent-level interoperability with 52 per cent of the 166.000 mobile money agents serving multiple providers, compared to 4 per cent in neighbouring Kenya.

The IFAD project seeks to increase the number of remittance recipients with access to financial services and promote small and medium-size businesses. The project is focused on the extension of UPU international electronical remittance service to rural postal offices and on the establishment of a link between remittances and postal-account based services.

The target group is represented by migrants and recipients of migrant remittances in rural areas of Benin, Burkina Faso, Mali, Mauritania, Niger and Sene- gal. The UPU system was installed and connected in all 6 countries. In total, 453 post offices have been equipped to de- liver the UPU service. Money orders sent and received in the target areas rose by 104%.

acp-eu migration action: entities that can apply for a licence to pay out remittances in acp countries

Interoperability read more here

ANALYSIS: We assessed which entities (banks and others) can apply for a licence to pay out remittances, for ACP countries where TA on remittances is ongoing or had already been completed.

IFAD project read more here

Cabo Verde

Ethiopia

Guyana

Kenya

Mali

Sierra Leone

Somalia

Zimbabwe

* Micro finance Instritution** Non-bank financial institution

Bank Mobilemoney

Postoffice

MPI * Other NFBI **

Country

Regulatory frameworkread more here

The AcTions’ work on remiTTAnces

GUYANA: The ACP-EU Migration Action supported local Guyanese Non-State Actor ‘The Consultancy Group (TGC)’ in developing a financial literacy application for mobile phones.

KENYA: The Kenyan Ministry of Foreign Affairs and Trade therefore requested support of the Action to develop a digital remittance booklet, that provides tke Kenyan diaspora with user-friendly information about affordable remittances channels. and investment and savings opportunities.

SOMALIA: In 2015, the Central Bank of Somalia requested Technical Assistance in order to support the development of a mobile money licensing and regulatory framework. The Action came up with a recommendations and a roadmap for implementation.

acp-eu migration action: highlighted technical assistance interventions and non-state actor initiatives

cAribbeAn:

AfricA:

PAcific:

Somalia - Mali - Kenya - Sierra Leone - Zimbabwe - Ethiopia - Cabo Verde - Togo - Ghana - IGAD - ECOWAS

OECS - Guyana

Tonga

Guyana read more here

Kenyaread more here

Somalia read more here