indian auto industry analysis

TRANSCRIPT

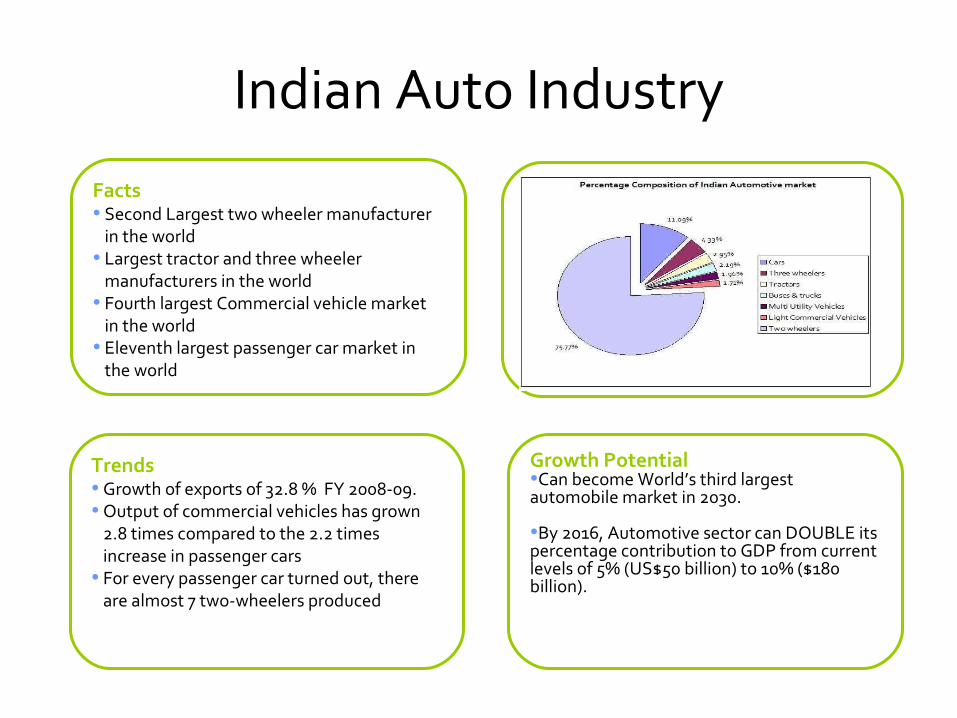

Indian Auto Industry

Facts• Second Largest two wheeler manufacturer

in the world• Largest tractor and three wheeler

manufacturers in the world• Fourth largest Commercial vehicle market

in the world• Eleventh largest passenger car market in

the world

Growth Potential•Can become World’s third largest automobile market in 2030.

•By 2016, Automotive sector can DOUBLE its percentage contribution to GDP from current levels of 5% (US$50 billion) to 10% ($180 billion).

Trends• Growth of exports of 32.8 % FY 2008-09. • Output of commercial vehicles has grown

2.8 times compared to the 2.2 times increase in passenger cars

• For every passenger car turned out, there are almost 7 two-wheelers produced

The Growth JourneyPre 1983 1983-1993 1993-2007

Era of globalisation and

evolution of India as a global

manufacturing hub

Closed market

• Growth of market limited by supply

• Outdated models

Players

• Hindustan Motors

• Premier

• Telco

• Ashok Leyland

• Mahindra & Mahindra

Japanisation - GOI- Suzuki joint venture to form Maruti Udyog• Joint ventures with companies in commercial vehicles and componentsPlayers• Maruti Udyog• Hindustan Motors• Premier• Telco• Ashok Leyland• Mahindra & Mahindra

Delicensing of sector in 1993

• Global major OEMs start assembly in India (Toyota, GM, Ford, Honda, Hyundai)

• Imports allowed from April 2001; alignment of duty on components and parts to ASEAN levels

• Implementation of VAT

Automotive Companies in IndiaMajor Multi-national companiesMajor Indian Companies

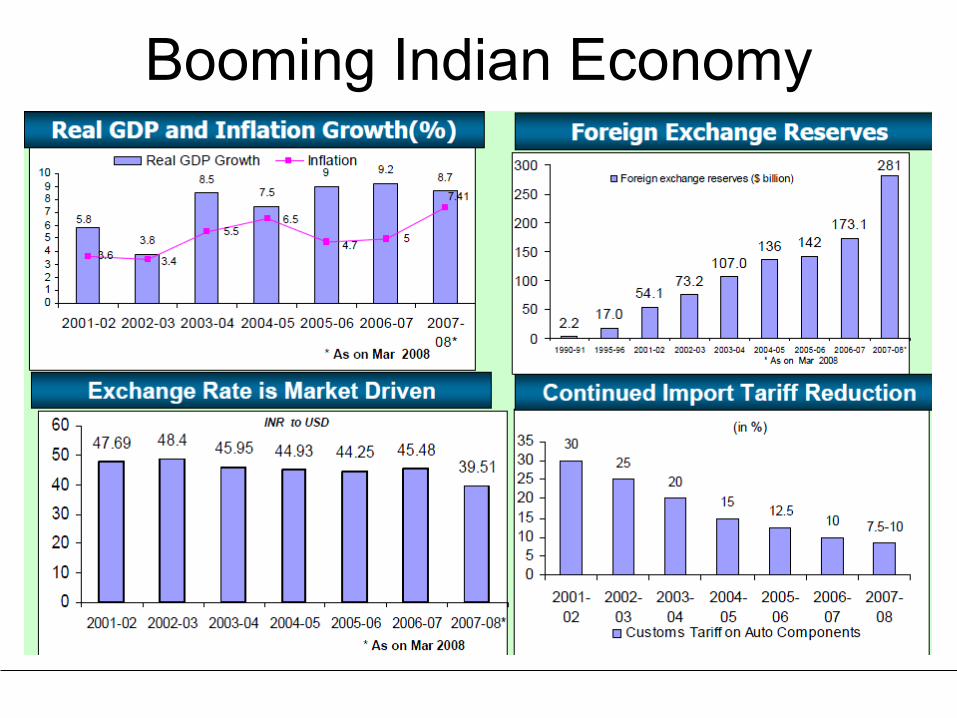

Booming Indian Economy

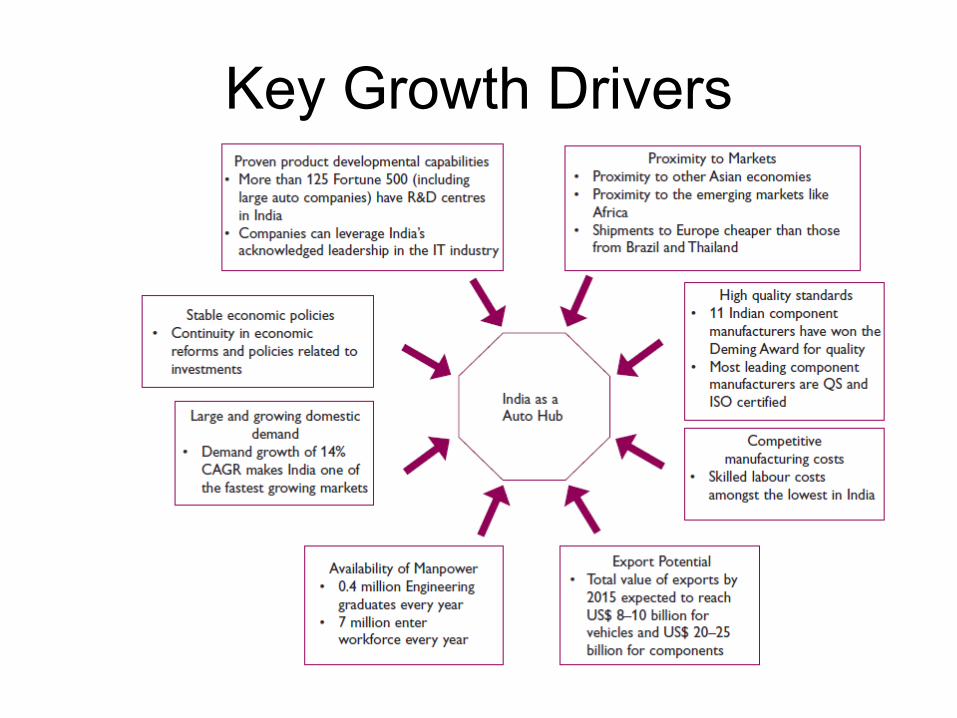

Key Growth Drivers

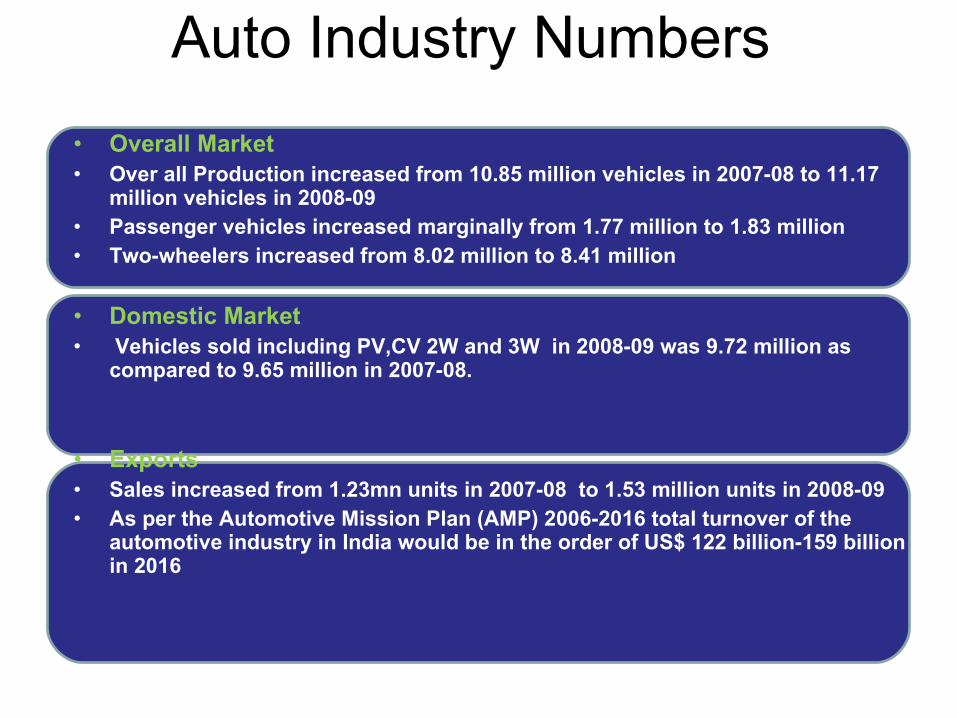

Auto Industry Numbers

• Overall Market• Over all Production increased from 10.85 million vehicles in 2007-08 to 11.17

million vehicles in 2008-09• Passenger vehicles increased marginally from 1.77 million to 1.83 million • Two-wheelers increased from 8.02 million to 8.41 million

• Domestic Market • Vehicles sold including PV,CV 2W and 3W in 2008-09 was 9.72 million as

compared to 9.65 million in 2007-08.

• Exports• Sales increased from 1.23mn units in 2007-08 to 1.53 million units in 2008-09• As per the Automotive Mission Plan (AMP) 2006-2016 total turnover of the

automotive industry in India would be in the order of US$ 122 billion-159 billion in 2016

Category wise numbers

Two Wheeler

Passenger Vehicles

Commercial Vehicles

Three Wheeler

Dominated by Motorcycles 80% , Scooters 14% Mopeds 6%

Domestic - 7.25mn units . Hero Honda 42% & Bajaj 27% share CAGR – 9.5%

Exports 819000 units (07-08) . Bajaj Auto 59% TVS 17% share CAGR – 41%

Dominated by Cars 78% , MUV/SUV 22%

Domestic – 1.5mn units Maruti-46% Tata-15% Hyundai 14% CAGR -14.8%

Exports - 217000 units (07-08) Maruti 66% Hyundai 24% CAGR – 26%

Dominated by M&HCV – Goods 48% Passenger 38% , Rest by LCV -14%

Domestic – 487 thousand units , Tata-62% Ashok Leyland -15% CAGR- 22%

Exports – 59 thousand units, Tata 67% Ashok Leyland 12% CAGR -30.6%

Dominated by Passenger Carriers with 64% share , Goods Carrier -36%

Domestic – 365 thousand units , Bajaj -42% Piaggio-41% CAGR- 10.5%

Export – 141 thousand units , Bajaj -97% CAGR -44.5%

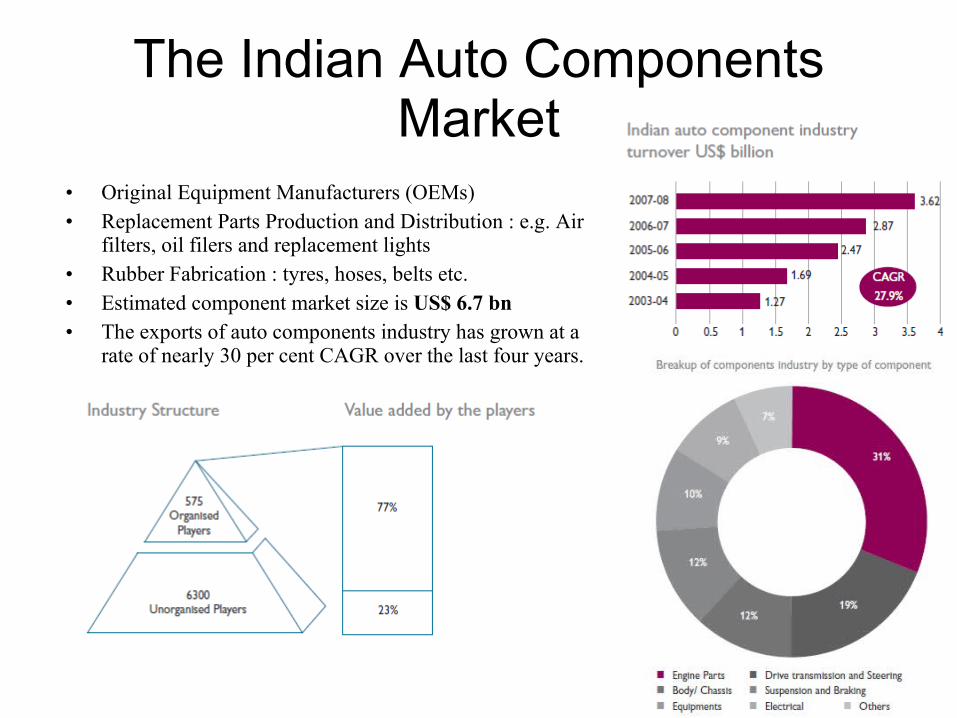

The Indian Auto Components Market

• Original Equipment Manufacturers (OEMs)• Replacement Parts Production and Distribution : e.g. Air

filters, oil filers and replacement lights • Rubber Fabrication : tyres, hoses, belts etc.• Estimated component market size is US$ 6.7 bn • The exports of auto components industry has grown at a

rate of nearly 30 per cent CAGR over the last four years.

Second Hand Automobile Market

• Used car market demand : 1.4 million cars annually• Market Structure :

– Organized : 10%– Unorganized : 90%

• Vendor Based – 30%• Direct Dealings – 70%

• Certified used car dealers in India are – Maruti TrueValue, Honda Auto Terrace, Ford Assured, Toyota U Trust, Hyundai Advantage, Mahindra and Mahindra’s First Choice, General Motors - Chevrolet-OK

• Unorganized market lacks services like -warranties, OEM equipments, insurance and taxes

• Second hand market expected to grow at 12-15 per cent in the next five years to touch a robust 2.5 million units and a turnover of Rs 50 thousand crore

• Estimations are that 50 percent of the used cars sales will be brought under organized car market by 2013

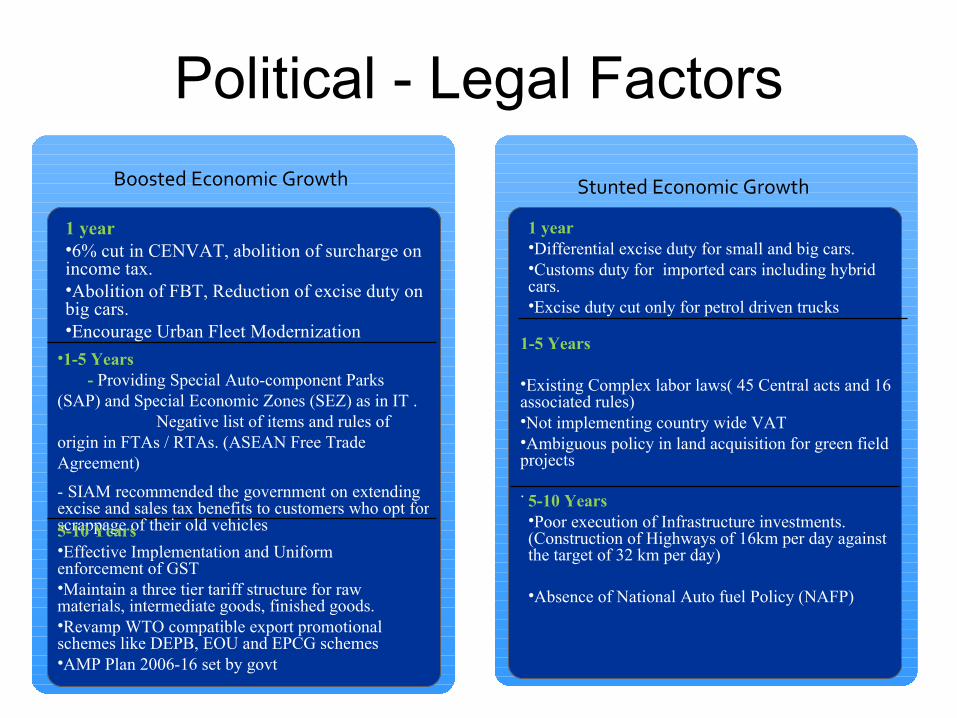

Political - Legal Factors

Boosted Economic Growth

1 year •6% cut in CENVAT, abolition of surcharge on income tax.•Abolition of FBT, Reduction of excise duty on big cars.•Encourage Urban Fleet Modernization

•1-5 Years - Providing Special Auto-component Parks (SAP) and Special Economic Zones (SEZ) as in IT . Negative list of items and rules of origin in FTAs / RTAs. (ASEAN Free Trade Agreement)

- SIAM recommended the government on extending excise and sales tax benefits to customers who opt for scrappage of their old vehicles5-10 Years•Effective Implementation and Uniform enforcement of GST •Maintain a three tier tariff structure for raw materials, intermediate goods, finished goods.•Revamp WTO compatible export promotional schemes like DEPB, EOU and EPCG schemes •AMP Plan 2006-16 set by govt

Stunted Economic Growth

1 year •Differential excise duty for small and big cars.•Customs duty for imported cars including hybrid cars.•Excise duty cut only for petrol driven trucks

1-5 Years •Existing Complex labor laws( 45 Central acts and 16 associated rules)•Not implementing country wide VAT•Ambiguous policy in land acquisition for green field projects

. 5-10 Years•Poor execution of Infrastructure investments. (Construction of Highways of 16km per day against the target of 32 km per day)

•Absence of National Auto fuel Policy (NAFP)

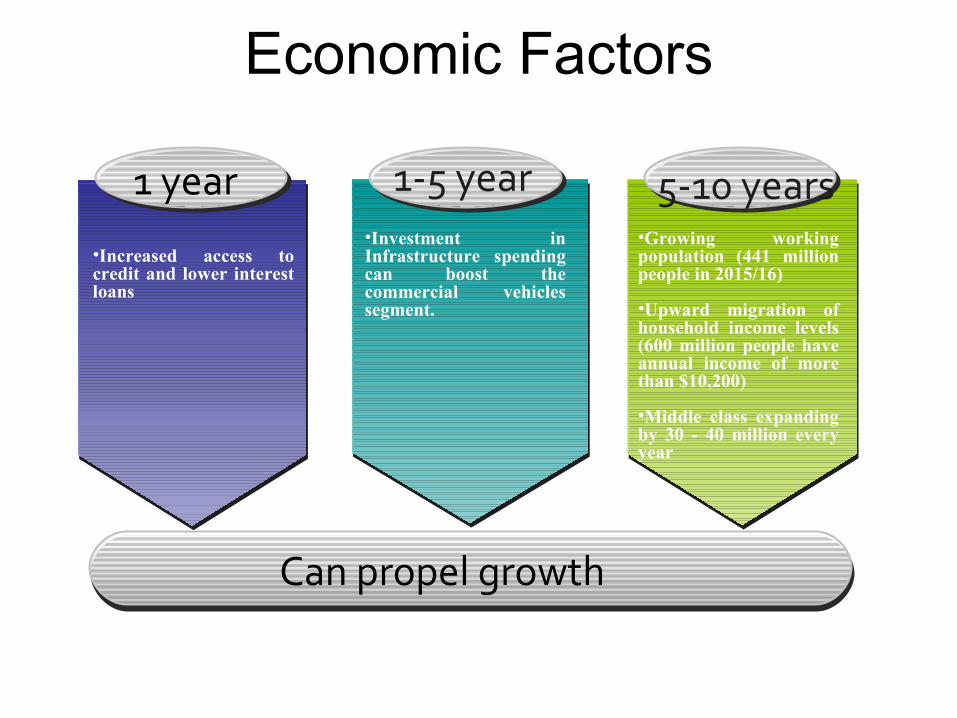

1 year 1-5 year 5-10 years•Increased access to credit and lower interest loans

•Investment in Infrastructure spending can boost the commercial vehicles segment.

Economic Factors

•Growing working population (441 million people in 2015/16)

•Upward migration of household income levels (600 million people have annual income of more than $10,200)

•Middle class expanding by 30 - 40 million every year

Can propel growth

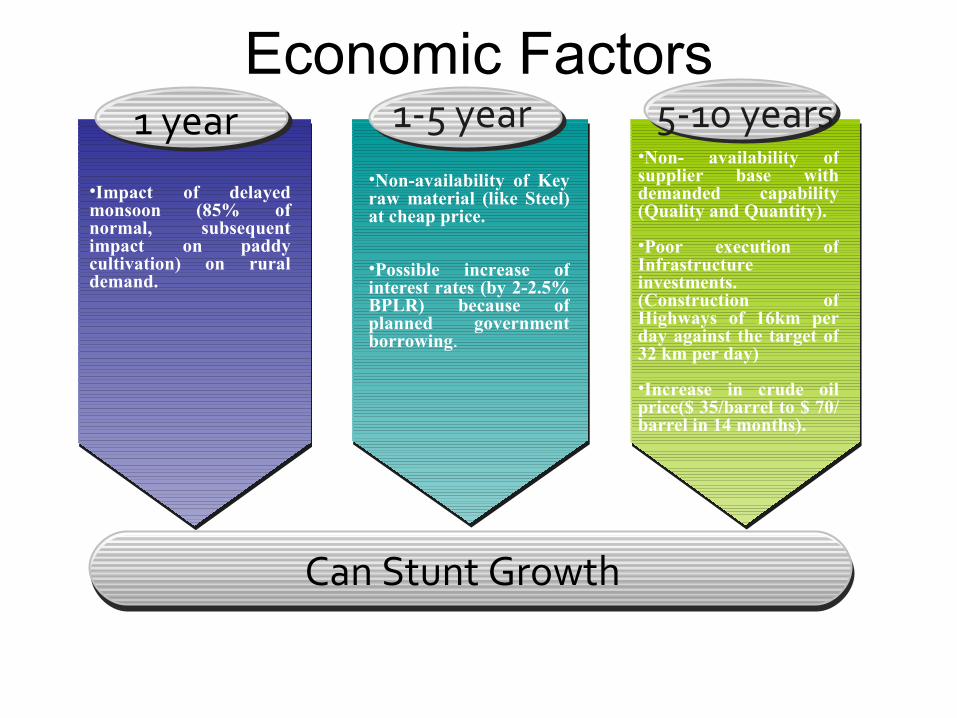

1 year 1-5 year 5-10 years

•Impact of delayed monsoon (85% of normal, subsequent impact on paddy cultivation) on rural demand.

•Non-availability of Key raw material (like Steel) at cheap price.

•Possible increase of interest rates (by 2-2.5% BPLR) because of planned government borrowing.

Economic Factors

•Non- availability of supplier base with demanded capability (Quality and Quantity).

•Poor execution of Infrastructure investments. (Construction of Highways of 16km per day against the target of 32 km per day)

•Increase in crude oil price($ 35/barrel to $ 70/ barrel in 14 months).

Can Stunt Growth

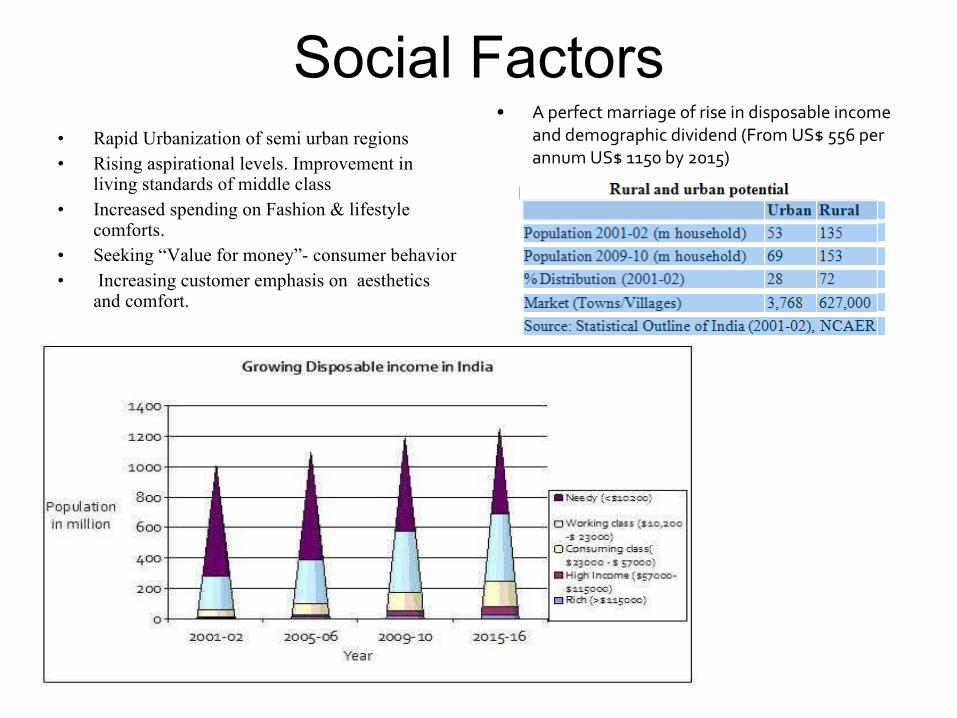

Social Factors• Rapid Urbanization of semi urban regions • Rising aspirational levels. Improvement in

living standards of middle class• Increased spending on Fashion & lifestyle

comforts.• Seeking “Value for money”- consumer behavior• Increasing customer emphasis on aesthetics

and comfort.

• A perfect marriage of rise in disposable income and demographic dividend (From US$ 556 per annum US$ 1150 by 2015)

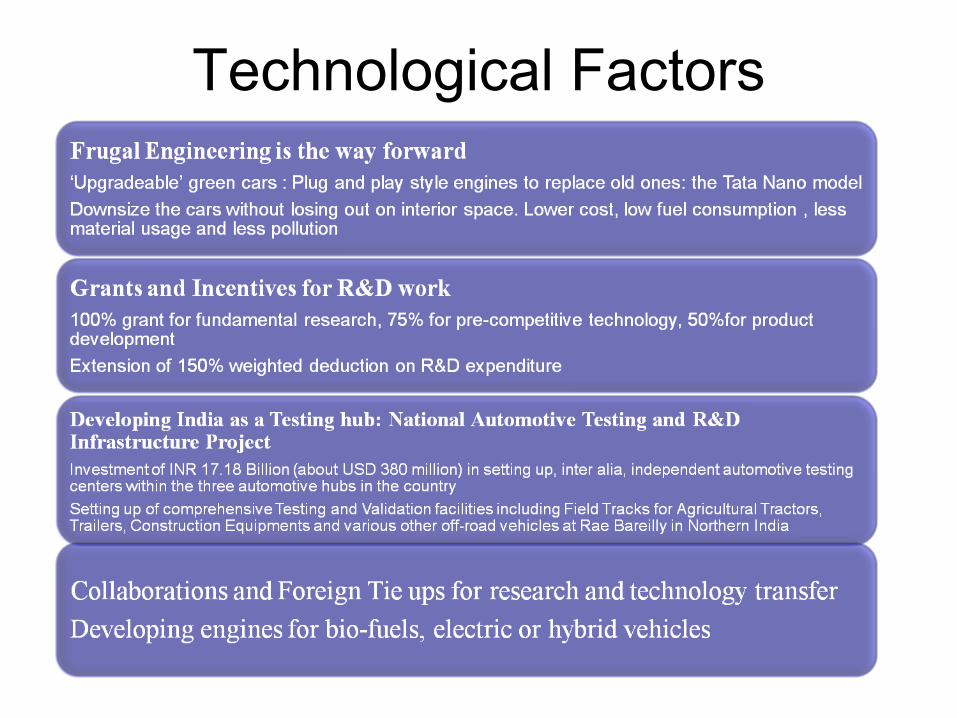

Technological Factors

India as a Testing Hub : NATRIP

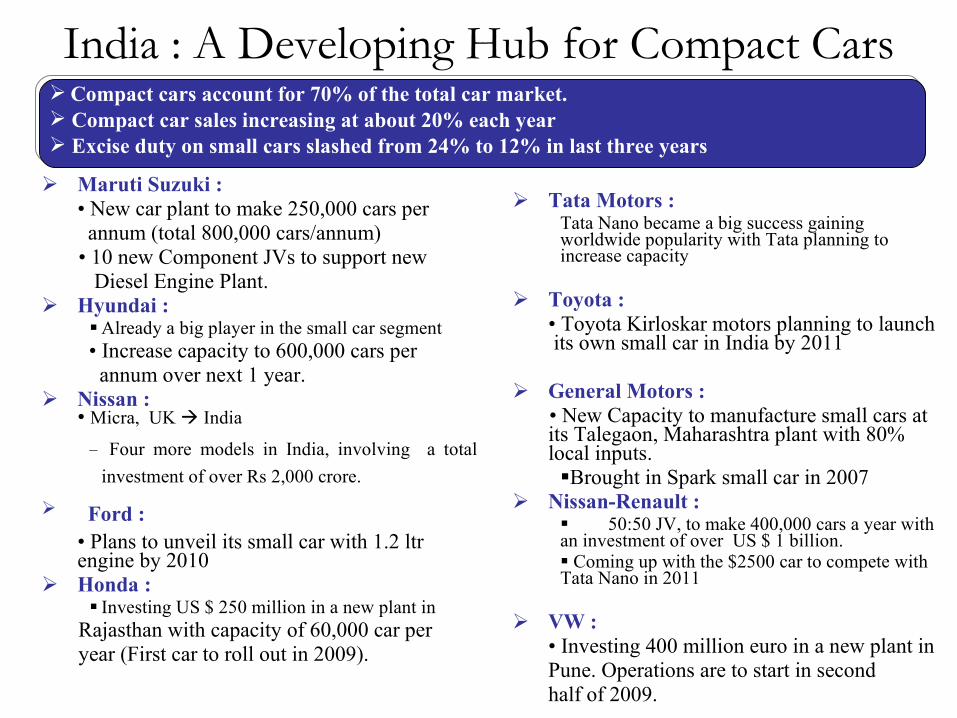

India : A Developing Hub for Compact Cars

Maruti Suzuki :• New car plant to make 250,000 cars per annum (total 800,000 cars/annum)

• 10 new Component JVs to support new Diesel Engine Plant. Hyundai :

Already a big player in the small car segment • Increase capacity to 600,000 cars per annum over next 1 year. Nissan :

• Micra, UK India

– Four more models in India, involving a total

investment of over Rs 2,000 crore. Ford :

• Plans to unveil its small car with 1.2 ltr engine by 2010

Honda : Investing US $ 250 million in a new plant in

Rajasthan with capacity of 60,000 car per year (First car to roll out in 2009).

Tata Motors :Tata Nano became a big success gaining worldwide popularity with Tata planning to increase capacity

Toyota :• Toyota Kirloskar motors planning to launch its own small car in India by 2011

General Motors : • New Capacity to manufacture small cars at

its Talegaon, Maharashtra plant with 80% local inputs.Brought in Spark small car in 2007

Nissan-Renault : 50:50 JV, to make 400,000 cars a year with an investment of over US $ 1 billion. Coming up with the $2500 car to compete with Tata Nano in 2011

VW :• Investing 400 million euro in a new plant inPune. Operations are to start in secondhalf of 2009.

Compact cars account for 70% of the total car market. Compact car sales increasing at about 20% each year Excise duty on small cars slashed from 24% to 12% in last three years

•India will be a Automotive hub, led by small cars and auto component domains

•Export of automotive components to ASEAN,BRIC,EU and USA for OEMs as well as Aftermarket

•Booming Automobiles (Particularly cars) second sales and remodeling

•Increased deployment of IT-enabled Automobile support systems like GPS,ABS,ASR and Safety systems.

•Quality Certification (Deming, Six Sigma,TQM,TS16949) amongst suppliers have attained critical mass and the entire market will follow to get quality certifications.

•Will be a hub for optimal cost, high quality vehicular testing and terrain data acquisition services

•Alternate fuel (Bio fuel, electricity) and environment friendly green engines (Bharat emission norms)

Break through future trends

References

• www.acmainfo.com• www.wikipedia.org• www.siamindia.com• www.ibef.org• Ernst & Young Auto Track• www.economywatch.com• www.business-standard.com• The Economic Times• Hindu Business Line• www.automobileindia.com• automobiles.mapsofindia.com