indian river county impact fee update … river county impact fee update workshop ... waste, public...

TRANSCRIPT

INDIAN RIVER COUNTY IMPACT FEE UPDATE WORKSHOP

Indian River County will be conducting an impact fee workshop at the date, time, and location shown below. The purpose of this workshop is to discuss a draft impact fee update report covering the following impact fee categories: Correctional Facilities, Solid Waste, Public Education, Libraries, Fire/Emergency Services, Law Enforcement, Public Buildings, Parks, and Traffic. All interested parties are welcome.

THURSDAY, MAY 24, 2007 1:30 P.M.

COMMISSION CHAMBERS COUNTY ADMINISTRATION BUILDING

1840 25TH STREET, VERO BEACH, FL 32960

The Impact Fee Update Report will be available after May 18, 2007. Please visit the County’s website at www.ircgov.com to download a copy or contact Rachel Clyne, Planner, Long Range Planning at 772-226-1923 or [email protected]. Anyone who needs a special accommodation for this meeting must contact the County’s Americans with Disabilities Act Coordinator at (772) 226-1223, at least 48 hours in advance of the meeting.

IImmppaacctt FFeeee UUppddaattee IInnddiiaann RRiivveerr CCoouunnttyy,, FFlloorriiddaa

TTeecchhnniiccaall MMeemmoorraanndduumm ##33 ((FFiinnaall))

in association with

Dr. James C. Nicholas Thomas G. Wright, Esq.

___________________________

April 30, 2007

Table of Contents EXECUTIVE SUMMARY................................................................................................................1 INTRODUCTION.............................................................................................................................3

Legal Framework .............................................................................................................................3 Level of Service................................................................................................................................6 Service Areas ....................................................................................................................................8

TRAFFIC ..............................................................................................................................................9 Major Roadway System.................................................................................................................10 Current Level of Service...............................................................................................................10 Cost per Service Unit ....................................................................................................................12 Revenue Credits .............................................................................................................................17 Travel Demand ..............................................................................................................................24 Updated Fee Schedule ..................................................................................................................27 Revenue Projections......................................................................................................................31

SCHOOLS..........................................................................................................................................32 Current Level of Service...............................................................................................................32 Cost Component ...........................................................................................................................37 Revenue Credits .............................................................................................................................40 Student Generation Rate ..............................................................................................................43 Updated Impact Fee Schedule.....................................................................................................46 Revenue Projections......................................................................................................................46

PARKS ................................................................................................................................................48 Current Level of Service...............................................................................................................49 Revenue Credits .............................................................................................................................53 Updated Impact Fee Schedule.....................................................................................................56 Revenue Projections......................................................................................................................57

LIBRARIES........................................................................................................................................58 Current Level of Service...............................................................................................................58 Revenue Credits .............................................................................................................................60 Updated Impact Fee Schedule.....................................................................................................64 Revenue Projections......................................................................................................................64

FIRE RESCUE ..................................................................................................................................65 Current Level of Service...............................................................................................................66 Revenue Credits .............................................................................................................................68 Updated Impact Fee Schedule.....................................................................................................71 Revenue Projections......................................................................................................................74

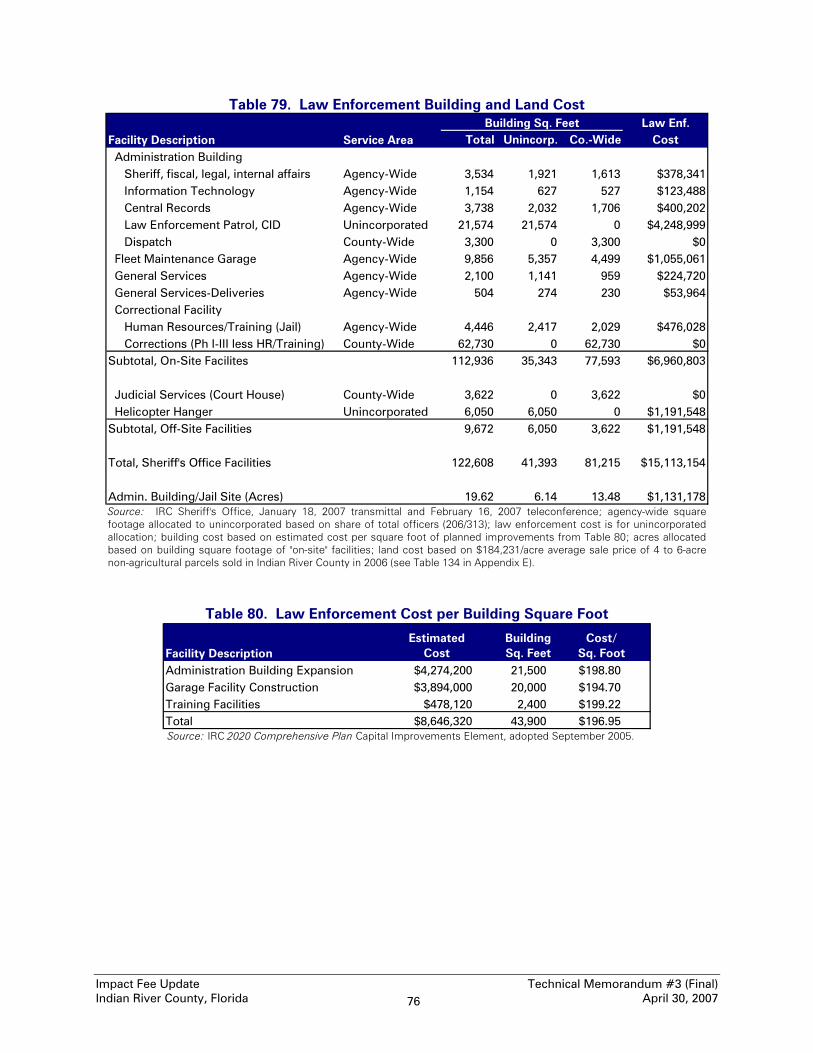

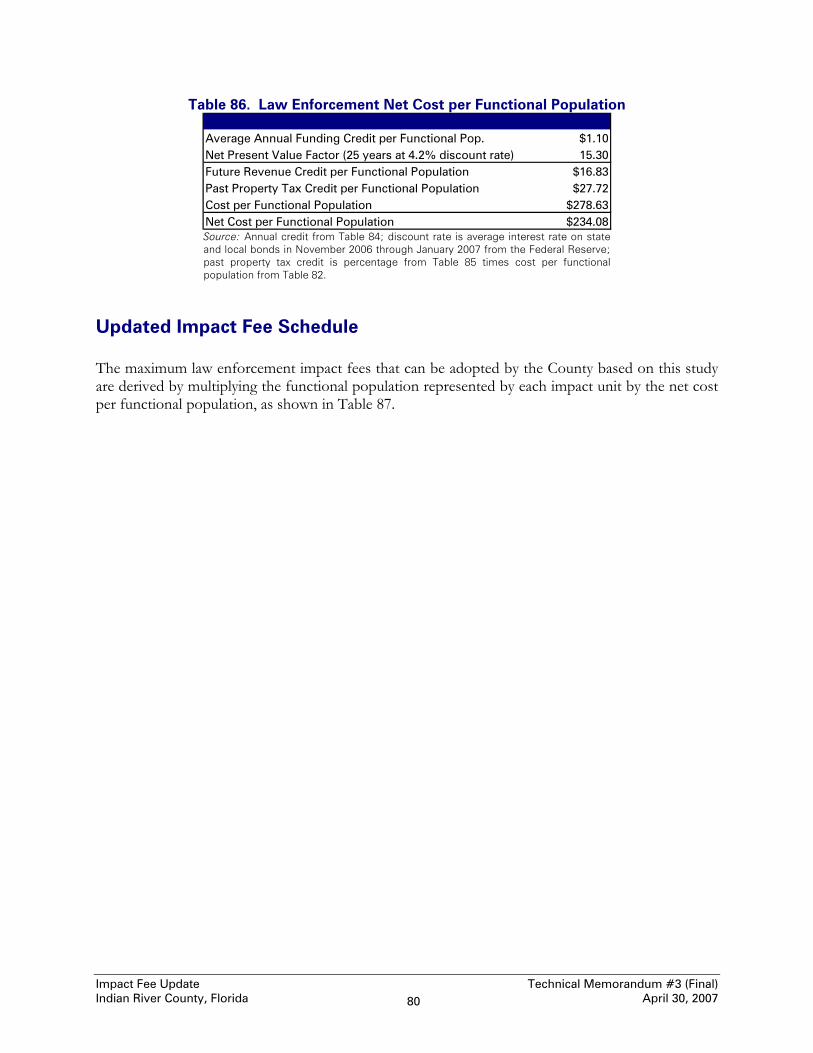

LAW ENFORCEMENT .................................................................................................................75 Current Level of Service...............................................................................................................75 Revenue Credits .............................................................................................................................77 Updated Impact Fee Schedule.....................................................................................................80 Revenue Projections......................................................................................................................84

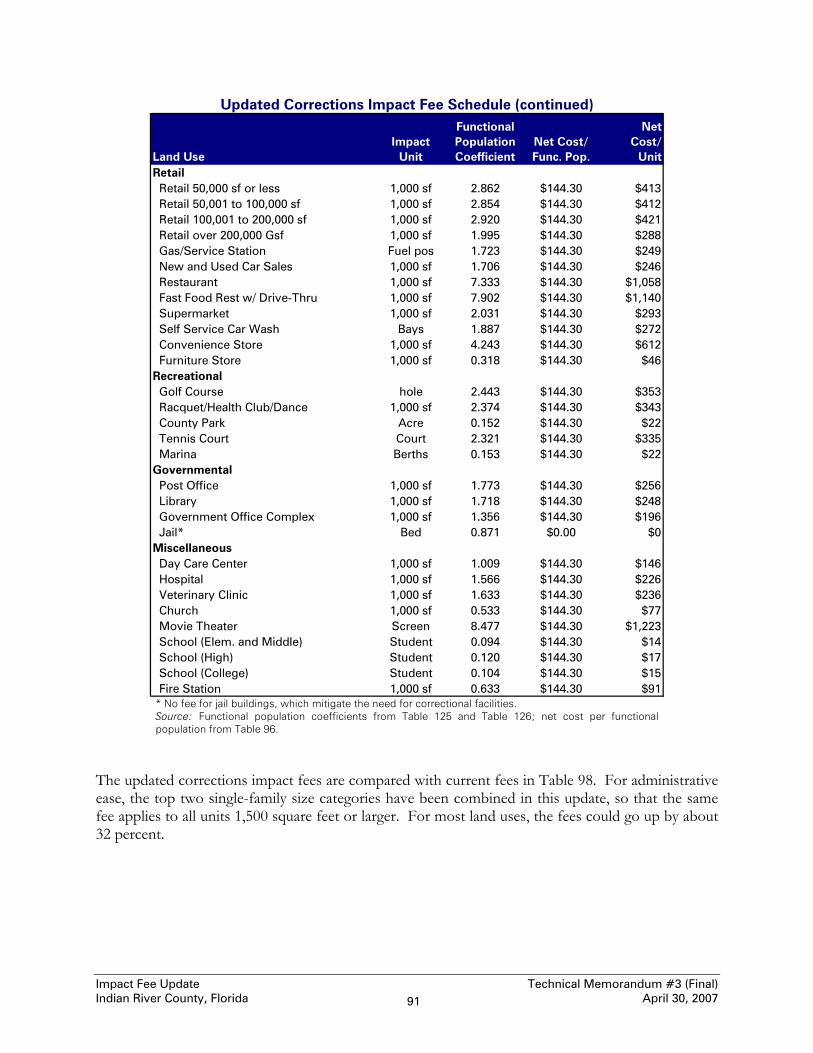

CORRECTIONS...............................................................................................................................85 Current Level of Service...............................................................................................................85 Revenue Credits .............................................................................................................................87 Updated Impact Fee Schedule.....................................................................................................90 Revenue Projections......................................................................................................................93

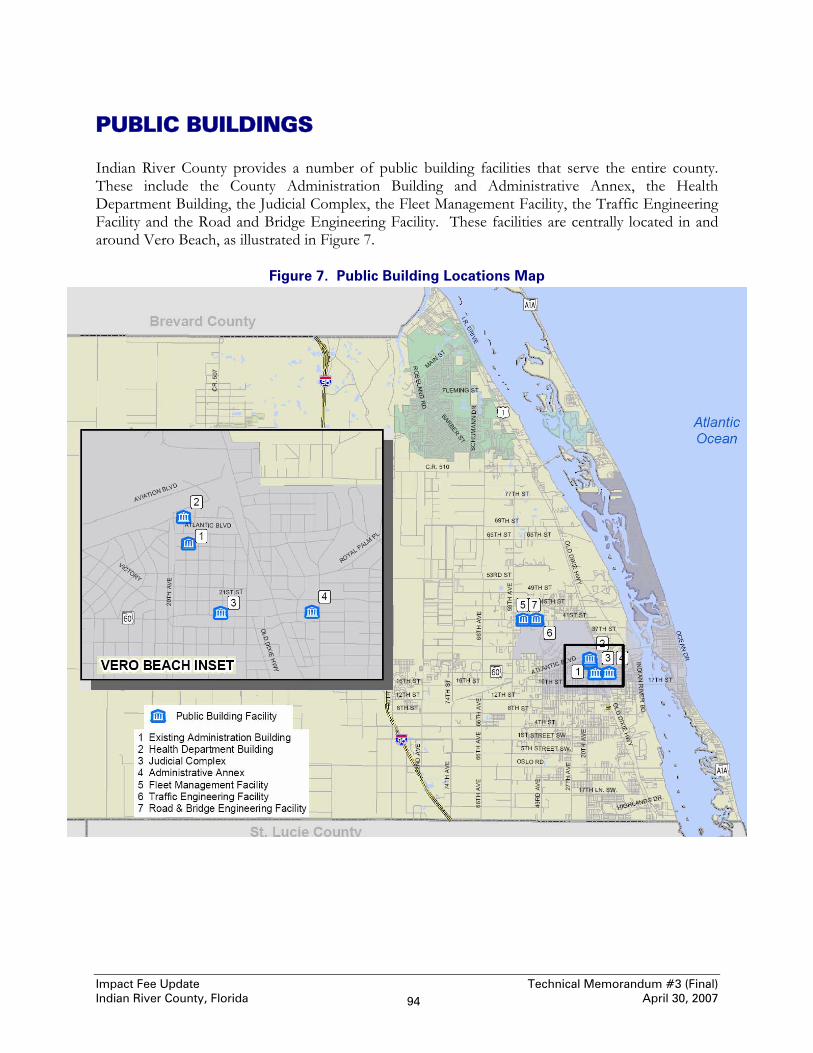

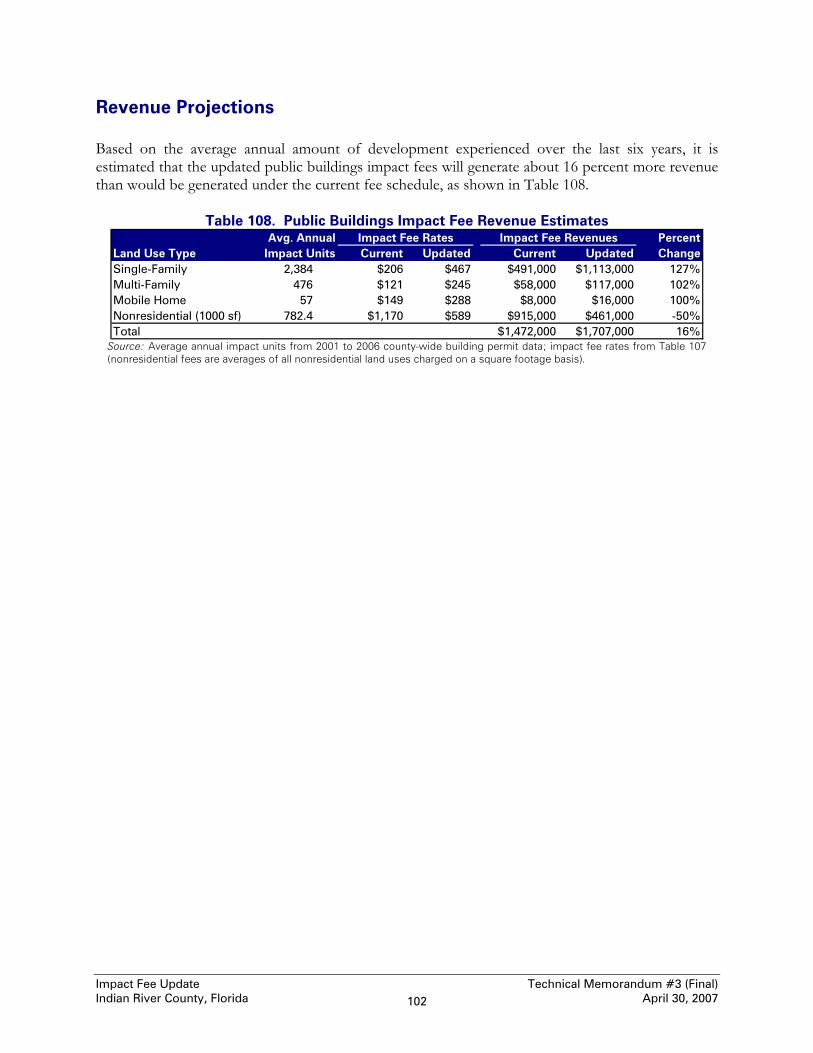

PUBLIC BUILDINGS .....................................................................................................................94 Current Level of Service...............................................................................................................94 Current Level of Service...............................................................................................................95 Revenue Credits .............................................................................................................................96 Updated Impact Fee Schedule.....................................................................................................99 Revenue Projections....................................................................................................................102

SOLID WASTE...............................................................................................................................103 Service Unit ..................................................................................................................................104 Current Level of Service.............................................................................................................106 Revenue Credits ...........................................................................................................................112 Updated Impact Fee Schedule...................................................................................................113 Revenue Potential ........................................................................................................................116

APPENDIX A: POPULATION AND DEMOGRAPHICS..................................................117 APPENDIX B: FUNCTIONAL POPULATION....................................................................120 APPENDIX C: MAJOR ROADWAY INVENTORY ............................................................125 APPENDIX D: PARK INVENTORY.......................................................................................131 APPENDIX E: AVERAGE LAND COSTS .............................................................................135

List of Tables Table 1. Impact Fee Update Summary ............................................................................................2 Table 2. Existing Major Roadway System Level of Service........................................................11 Table 3. Planned Improvement Costs ...........................................................................................14 Table 4 Weighted Average Cost per Lane-Mile ...........................................................................15 Table 5. Capacity Added by Planned Road Improvements........................................................16 Table 6. Road Cost per Service Unit..............................................................................................17 Table 7. Fuel Tax Distribution per Penny per Gallon, FY 2006-07..........................................17 Table 8. Historic Local Option Gas Tax Funding, FY 2002-2007............................................18 Table 9. Historic Optional Sales Tax Funding, FY 2002-2007 ..................................................19 Table 10. Future Local Option Gas Tax Funding, FY 2008-2012 ............................................19 Table 11. Future Optional Sales Tax Funding, FY 2008-2012 ..................................................20 Table 12. Local Funding Credit per Gallon ..................................................................................20 Table 13. FDOT Work Program, FY 2001-2006.........................................................................21 Table 14. FDOT Work Program, FY 2007-2012.........................................................................22 Table 15. State Road Projects in 2030 LRTP, FY 2013 to 2030................................................22 Table 16. Federal/State Gas Tax Funding Credit per Gallon....................................................23 Table 17. Road Credit per Gallon ..................................................................................................23 Table 18. Vehicle-Miles of Travel on Major Roadway System ..................................................25 Table 19. Expected Local Vehicle-Miles of Travel ......................................................................26 Table 20. Trip Length Calibration Factor .....................................................................................26 Table 21. Updated Traffic Impact Fee Schedule..........................................................................28 Table 22. Comparison of Current and Updated Traffic Impact Fees.......................................29 Table 23. Traffic Impact Fee Revenue Estimates ........................................................................31 Table 24. Inventory of Public Schools, 2007................................................................................34 Table 25. Public School Enrollment and Capacity, 2007-2011..................................................35 Table 26. Recent School Construction Costs ...............................................................................37

Table 27. Estimated Local School Building Costs per Square Foot..........................................38 Table 28. School Bus Cost per Student .........................................................................................39 Table 29. School Capital Cost per Student ...................................................................................40 Table 30. Planned School Capital Expenditures and Revenues, 2007-2011 ............................41 Table 31. School State Revenue Credit..........................................................................................42 Table 32. School Capital Improvements Tax Revenue Credit ...................................................42 Table 33. School Past Property Tax Credit Percentage...............................................................43 Table 34. School Net Cost per Student .........................................................................................43 Table 35. Uncalibrated Student Generation Rates, 2000 ............................................................44 Table 36. Calibrated Student Generation Rates, 2007.................................................................44 Table 37. Comparison of Student Generation Rates...................................................................45 Table 38. Updated School Impact Fee Schedule..........................................................................46 Table 39. Comparative School Impact Fees .................................................................................46 Table 40. School Demand and Cost Analysis, 2007-2025 ..........................................................46 Table 41. School Impact Fee Revenue Estimates ........................................................................47 Table 42. Current Parks and Recreation Level of Service ..........................................................49 Table 43. Landscaping and Site Improvements Cost per Acre..................................................50 Table 44. Utilities and Paving Cost per Acre................................................................................50 Table 45. Total Land Cost per Developed Acre ..........................................................................51 Table 46. Parks Facility Replacement Cost ...................................................................................52 Table 47. Total Park Cost per Person............................................................................................53 Table 48. Historical Park Improvements, 2002-2007..................................................................54 Table 49. Planned Park Improvements, 2008-2012.....................................................................55 Table 50. Park Annual Revenue Credit per Person .....................................................................55 Table 51. Park Past Property Tax Percentage...............................................................................56 Table 52. Park Net Cost per Person ..............................................................................................56 Table 53. Updated Park Impact Fee Schedule..............................................................................57 Table 54. Comparative Park Impact Fees .....................................................................................57 Table 55. Park Impact Fee Revenue Estimates ............................................................................57 Table 56. Library Building and Land Replacement Cost ............................................................59 Table 57. Library Building Cost per Square Foot ........................................................................59 Table 58. Library Land Cost per Acre ...........................................................................................59 Table 59. Library Collections Replacement Cost .........................................................................60 Table 60. Library Cost per Person..................................................................................................60 Table 61. Historical Library Improvements, 2002-2007 .............................................................61 Table 62. Library Annual Revenue Credit per Person ................................................................62 Table 63. Library Past Property Tax Percentage ..........................................................................63 Table 64. Library Net Cost per Person..........................................................................................63 Table 65. Updated Library Impact Fee Schedule.........................................................................64 Table 66. Comparative Library Impact Fees.................................................................................64 Table 67. Library Impact Fee Revenue Estimates .......................................................................64 Table 68. Fire Rescue Building and Land Cost ............................................................................66 Table 69. Fire Rescue Vehicle Cost................................................................................................66 Table 70. Fire Rescue Capital Equipment Cost............................................................................67 Table 71. Fire Rescue Cost per Functional Population...............................................................67 Table 72. Historical Fire Rescue Improvements, 2002-2007 .....................................................69 Table 73. Planned Fire Rescue Improvements, 2008-2012 ........................................................70 Table 74. Fire Rescue Annual Credit per Functional Population..............................................70

Table 75. Fire Rescue Net Cost per Functional Population.......................................................71 Table 76. Updated Fire Rescue Net Cost Schedule .....................................................................71 Table 77. Comparative Fire Rescue Impact Fees.........................................................................73 Table 78. Fire Rescue Impact Fee Revenue Estimates ...............................................................74 Table 79. Law Enforcement Building and Land Cost.................................................................76 Table 80. Law Enforcement Cost per Building Square Foot .....................................................76 Table 81. Law Enforcement Vehicle and Equipment Cost........................................................77 Table 82. Law Enforcement Cost per Functional Population ...................................................77 Table 83. Historical Law Enforcement Improvements, 2002-2007..........................................78 Table 84. Law Enforcement Annual Credit per Functional Population ..................................79 Table 85. Law Enforcement Past Property Tax Percentage.......................................................79 Table 86. Law Enforcement Net Cost per Functional Population ...........................................80 Table 87. Updated Law Enforcement Impact Fee Schedule......................................................81 Table 88. Comparative Law Enforcement Impact Fees .............................................................83 Table 89. Law Enforcement Impact Fee Revenue Estimates ....................................................84 Table 90. Corrections Building and Land Cost ............................................................................86 Table 91. Corrections Vehicle and Equipment Cost ...................................................................86 Table 92. Corrections Cost per Functional Population...............................................................87 Table 93. Historical Corrections Improvements, 2002-2007 .....................................................88 Table 94. Corrections Annual Credit per Functional Population..............................................89 Table 95. Corrections Past Property Tax Percentage ..................................................................89 Table 96. Corrections Net Cost per Functional Population.......................................................90 Table 97. Updated Corrections Impact Fee Schedule.................................................................90 Table 98. Comparative Corrections Impact Fees.........................................................................92 Table 99. Corrections Impact Fee Revenue Estimates ...............................................................93 Table 100. Public Buildings Facility and Land Cost ....................................................................95 Table 101. Public Buildings Cost per Functional Population ....................................................96 Table 102. Historical Public Buildings Improvements, 2002-2007 ...........................................97 Table 103. Public Buildings Annual Credit per Functional Population....................................98 Table 104. Public Buildings Past Property Tax Percentage........................................................98 Table 105. Public Buildings Net Cost per Functional Population.............................................99 Table 106. Updated Public Buildings Impact Fee Schedule.......................................................99 Table 107. Comparative Public Buildings Impact Fees.............................................................101 Table 108. Public Buildings Impact Fee Revenue Estimates ...................................................102 Table 109. Waste Generation Units by Land Use Type............................................................104 Table 110. Total Existing Waste Generation Units ...................................................................106 Table 111. Convenience Center Cost per Residential WGU ...................................................107 Table 112. Recycling Cost per WGU...........................................................................................108 Table 113. Landfill Acreage and Capacity ...................................................................................110 Table 114. Landfill Land and Vehicle Cost.................................................................................111 Table 115. Landfill Class I Recoupment Cost per WGU .........................................................112 Table 116. Solid Waste Cost Summary per WGU .....................................................................112 Table 117. Updated Solid Waste Impact Fee Schedule.............................................................113 Table 118. Comparative Solid Waste Impact Fees ....................................................................115 Table 119. Solid Waste Impact Fee Revenue Estimates ...........................................................116 Table 120. Persons per Unit, 2000 ...............................................................................................117 Table 121. Person per Single-Family Unit by Size, U.S. 2003..................................................118 Table 122. Persons per Unit, with Single-Family Tiering .........................................................118

Table 123. Existing Housing Units and Population, 2007........................................................118 Table 124. Permanent, Year-Round Population, 2007-2025....................................................119 Table 125. Functional Population per Unit for Residential Land Uses ..................................121 Table 126. Functional Population per Unit for Nonresidential Land Uses ...........................122 Table 127. Total Functional Population by Service Area, 2007...............................................123 Table 128. Functional Population, 2007-2025............................................................................124 Table 129. Existing Major Roadway Inventory – Principal Arterial Roads ...........................125 Table 130. Existing Major Roadway Inventory – Minor Arterial Roads ................................126 Table 131. Existing Major Roadway Inventory – Collector Roads .........................................128 Table 132. Existing Park Inventory..............................................................................................131 Table 133. Average Land Cost, 40-to-160-Acre Parcels, 2006.................................................135 Table 134. Average Land Cost, 4-to-6-Acre Parcels, 2006.......................................................135

List of Figures Figure 1. Population Growth, 2000-2025........................................................................................3 Figure 2. Indian River County 2030 Planned Roadway Improvements ...................................13 Figure 3. Locations of Existing Public Schools............................................................................33 Figure 4. Location of Existing County Parks ...............................................................................48 Figure 5. Locations of Existing Library Facilities ........................................................................58 Figure 6. Fire Station Locations......................................................................................................65 Figure 7. Public Building Locations Map ......................................................................................94 Figure 8. Solid Waste Locations ...................................................................................................103 Figure 9. Layout of the Existing Landfill Site.............................................................................109 Figure 10. Nonresidential Functional Population Formula......................................................121

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 1

EXECUTIVE SUMMARY This report updates Indian River County’s traffic, schools, parks, libraries, fire rescue, law enforcement, corrections, public buildings and solid waste impact fees. With the exception of the traffic impact fee, which the County has had for some time and which was updated a year earlier, the current fees were adopted in 2005 based on Tindale-Oliver & Associates, Indian River County Impact Fee Study, May 2005 (referred to here as the “previous study”). The current traffic impact fee was adopted in 2004 based on Tindale-Oliver & Associates, Update of the Traffic Impact Fee Ordinance, February 2004. Several deviations from the methodology used in the previous study were made to simplify the impact fee system. The first major change was to base all of the updated fees at or below the existing level of service. The previous study had based several of the fees on the higher level of service anticipated to be provided in five years. In this study, the corrections and public buildings fees are based on a future level of service that is somewhat lower than the current level of service, in recognition of the fact that the current major jail and public building expansions to be completed this year will not be repeated in the near future. Another major deviation from the methodology employed in the previous study for four of the facilities addressed in this report (fire rescue, law enforcement, corrections and public buildings) is a significant simplification of the “functional population” calculations. For the most part, this change has little effect on the resulting impact fees. The one exception is the fee for public buildings. The previous study used an 11-hours-per-day, 5-days-per-week functional population for public buildings, rather than the 24-hours-per-day, 7-days-per-week functional population used for the other three facilities. This had the effect of putting most of the burden of public building costs on nonresidential development, since few people are home during the daylight weekday hours when public buildings are open. In this update, the 24-hours-per-day functional population approach has been used for all four facilities. This change results in higher public building impact fees for residential land uses and lower fees for nonresidential land uses, although overall revenues will increase significantly. Major changes are also proposed for the solid waste fee methodology. The previous study based the fees on the percent of the cost of incremental landfill improvements (such as creating new disposal cells) attributable to the disposal of waste from new development, and attributed convenience center costs to all development. This study recoups the cost of upfront landfill investments (land and heavy machinery) that will be consumed by new development, and allocates convenience center costs only to residential development. This latter change has the effect of significantly reducing solid waste fees for nonresidential land uses. In addition, overall fee revenues will decline somewhat, even if growth continues as in the recent past. In Table 1 below, the current and updated amounts for all of the County’s impact fees are shown for five typical land uses (2,000-square-foot single-family unit, multi-family unit, 1,000 square feet of retail in a 100,000 square-foot shopping center, 1,000 square feet of office in a 100,000 square-foot office building, and 1,000 square feet of industrial). Residential fees increase more than nonresidential fees, due primarily to significant increases in school and park fees, which are paid only by residential development

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 2

Table 1. Impact Fee Update Summary

Impact Fee/Land Use TypeImpact

Unit Proposed CurrentIncrease/Decrease

PercentChange

Traffic Dwelling $7,927 $5,202 $2,725 52%Schools Dwelling $4,411 $1,756 $2,655 151%Parks Dwelling $2,546 $1,463 $1,083 74%Libraries Dwelling $563 $483 $80 17%Fire/Rescue Dwelling $339 $278 $61 22%Law Enforcement Dwelling $362 $245 $117 48%Corrections Dwelling $223 $170 $53 31%Public Buildings Dwelling $467 $206 $261 127%Solid Waste Dwelling $82 $75 $7 9%Total, Single-Family (2,000 sf) Dwelling $16,838 $9,803 $7,035 72%

Traffic Dwelling $4,329 $2,842 $1,487 52%Schools Dwelling $1,079 $500 $579 116%Parks Dwelling $1,336 $884 $452 51%Libraries Dwelling $295 $285 $10 4%Fire/Rescue Dwelling $178 $176 $2 1%Law Enforcement Dwelling $190 $148 $42 28%Corrections Dwelling $117 $100 $17 17%Public Buildings Dwelling $245 $121 $124 102%Solid Waste Dwelling $62 $57 $5 9%Total, Multi-Family Dwelling $7,769 $5,056 $2,713 54%

Traffic 1,000 sf $12,005 $7,813 $4,192 54%Fire/Rescue 1,000 sf $626 $502 $124 25%Law Enforcement 1,000 sf $668 $439 $229 52%Corrections 1,000 sf $412 $312 $100 32%Public Buildings 1,000 sf $863 $1,527 -$664 -43%Solid Waste 1,000 sf $41 $236 -$195 -83%Total, Retail (100,000 sf) 1,000 sf $14,574 $10,593 $3,981 38%

Traffic 1,000 sf $8,115 $5,326 $2,789 52%Fire/Rescue 1,000 sf $162 $130 $32 25%Law Enforcement 1,000 sf $173 $114 $59 52%Corrections 1,000 sf $107 $81 $26 32%Public Buildings 1,000 sf $224 $555 -$331 -60%Solid Waste 1,000 sf $16 $94 -$78 -83%Total, Office (100,000 sf) 1,000 sf $8,557 $5,651 $2,575 51%

Traffic 1,000 sf $4,263 $2,797 $1,466 52%Fire/Rescue 1,000 sf $150 $120 $30 25%Law Enforcement 1,000 sf $160 $105 $55 52%Corrections 1,000 sf $99 $75 $24 32%Public Buildings 1,000 sf $207 $512 -$305 -60%Solid Waste 1,000 sf $41 $236 -$195 -83%Total, General Industrial 1,000 sf $4,879 $3,609 $1,270 35% Source: Traffic, schools, parks, libraries, fire rescue, law enforcement, corrections, public buildings, and solid waste fees from Table 21, Table 38, Table 53, Table 65, Table 76, Table 87, Table 97, Table 106 and Table 117, respectively; fees do not include administrative charge.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 3

INTRODUCTION Figure 1. Population Growth, 2000-2025

Impact fees are most appropriate for jurisdictions experiencing rapid growth. Indian River County (IRC) has been experiencing significant growth over the past two decades, and this growth is projected to continue. The population of the county increased by 51 percent in the 1980s and by 24 percent in the 1990s. The population is projected to increase by another 70 percent from 2000 to 2025 (see Figure 1). This section provides a legal background, general information about impact fee principles and a description of the role of level of service in impact fee analysis. Assumptions and resulting population estimates for 2007 and projections through the year 2025 (in five-year increments) are presented and summarized in Appendix A for use, as appropriate, within each of the impact fee program areas. Functional population estimates and projections, as well as a discussion of what functional population is, are provided in Appendix B.

Legal Framework Impact fees are a way for local governments to require new developments to pay a proportionate share of the infrastructure costs they impose on the community. In contrast to traditional “negotiated” developer exactions, impact fees are charges that are assessed on new development using a standard formula based on objective characteristics, such as the number and type of dwelling units constructed. The fees are one-time, up-front charges, with the payment usually made at the time of building permit issuance. Essentially, impact fees require that each new development project pay its pro-rata share of the cost of new capital facilities required to serve that development. Since impact fees were pioneered in states like Florida that lacked specific enabling legislation, such fees have generally been legally defended as an exercise of local government’s broad “police power” to regulate land development in order to protect the health, safety and welfare of the community. The courts have developed guidelines for constitutionally-valid impact fees, based on “rational nexus” standards. The standards essentially require that the fees must be proportional to the need for additional infrastructure created by the new development, and must be spent in such a way as to provide that same type of infrastructure to benefit new development. A Florida district court of appeals described the dual rational nexus test in 1983 as follows, and this language was quoted and followed by the Florida Supreme Court in its 1991 St. Johns County decision:

In order to satisfy these requirements, the local government must demonstrate a reasonable connection, or rational nexus, between the need for additional capital facilities and the growth in population generated by the subdivision. In addition, the government must show a reasonable connection, or rational nexus, between the expenditures of the funds collected and the benefits

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 4

accruing to the subdivision. In order to satisfy this latter requirement, the ordinance must specifically earmark the funds collected for use in acquiring capital facilities to benefit the new residents.

Florida Statutes The 2006 Florida Legislature passed Senate Bill 1194, which establishes certain requirements for impact fees in Florida. The bill, which became effective on June 14, 2006, created a new Section 163.31801, Florida Statutes, which reads as follows: 163.31801 Impact fees; short title; intent; definitions; ordinances levying impact fees.-- (1) This section may be cited as the "Florida Impact Fee Act."

(2) The Legislature finds that impact fees are an important source of revenue for a local government to use in funding the infrastructure necessitated by new growth. The Legislature further finds that impact fees are an outgrowth of the home rule power of a local government to provide certain services within its jurisdiction. Due to the growth of impact fee collections and local governments' reliance on impact fees, it is the intent of the Legislature to ensure that, when a county or municipality adopts an impact fee by ordinance or a special district adopts an impact fee by resolution, the governing authority complies with this section.

(3) An impact fee adopted by ordinance of a county or municipality or by resolution of a special district must, at minimum:

(a) Require that the calculation of the impact fee be based on the most recent and localized data.

(b) Provide for accounting and reporting of impact fee collections and expenditures. If a local governmental entity imposes an impact fee to address its infrastructure needs, the entity shall account for the revenues and expenditures of such impact fee in a separate accounting fund.

(c) Limit administrative charges for the collection of impact fees to actual costs.

(d) Require that notice be provided no less than 90 days before the effective date of an ordinance or resolution imposing a new or amended impact fee.

(4) Audits of financial statements of local governmental entities and district school boards which are performed by a certified public accountant pursuant to s. 218.39 and submitted to the Auditor General must include an affidavit signed by the chief financial officer of the local governmental entity or district school board stating that the local governmental entity or district school board has complied with this section.

Other provisions relating to impact fees are scattered about in the Florida Statutes. Section 163.2517(3)(j) requires that urban infill and redevelopment area plans contain a package of financial incentives, one of which could be “lower transportation impact fees for development which encourages more use of public transit, pedestrian and bicycle modes of transportation.” School concurrency provisions in Section 163.3180(13)(e)2 state that if developers make proportionate-

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 5

share mitigation contributions, “the local government shall credit such a contribution, construction, expansion, or payment toward any other impact fee or exaction imposed by local ordinance for the same need, on a dollar-for-dollar basis at fair market value.” Transportation concurrency provisions relating to multi-modal transportation districts provide in Section 163.3180(15)(d) that “local governments may reduce impact fees or local access fees for development within multi-modal transportation districts based on the reduction of vehicle trips per household or vehicle miles of travel expected from the development pattern planned for the district.” Transportation concurrency management provisions provide in Section 163.3180(16)(b)2 that “proportionate fair-share mitigation shall be applied as a credit against impact fees to the extent that all or a portion of the proportionate fair-share mitigation is used to address the same capital infrastructure improvements contemplated by the local government's impact fee ordinance.” The boards of independent special fire control districts are authorized to establish fire impact fees in Section 191.009(4). Section 290.0057(1)(e) authorizes “impact fee abatement or reduction” as part of a package of incentives that must be put in place for enterprise zones. Developments of regional impact must be given credit for any capital contributions required as a condition of development approval, pursuant to Section 380.06(16). Local governments are encouraged to establish affordable housing incentive strategies, which may include the “modification of impact-fee requirements, including reduction or waiver of fees and alternative methods of fee payment for affordable housing,” according to Section 420.9076(4)(b). Public schools are exempted from the payment of impact fees in Section 1013.371(1)(a).

General Impact Fee Principles One of the most fundamental principles of impact fees, rooted in both case law and norms of equity, is that impact fees should not charge new development for a higher level of service than is provided to existing development. While impact fees can be based on a higher level of service than the one existing at the time of the adoption of the fees, two things are required if this is done. First, another source of funding other than impact fees must be identified and committed to fund the capacity deficiency created by the higher level of service. Second, the impact fees must generally be reduced to ensure that new development does not pay twice for the same level of service, once through impact fees and again through general taxes that are used to remedy the capacity deficiency for existing development. In order to avoid these complications, the general practice is to base the impact fees on the existing level of service. A corollary principle is that new development should not have to pay more than its proportionate share when multiple sources of payment are considered. As noted above, if impact fees are based on a higher-than-existing level of service, the fees should be reduced by a credit that accounts for the contribution of new development toward remedying the existing deficiencies. A similar situation arises when the existing level of service has not been fully paid for. Outstanding debt on existing facilities that are counted in the existing level of service will be retired, in part, by revenues generated from new development. Given that new development will pay impact fees to provide the existing level of service for itself, the fact that new development may also be paying for the facilities that provide that level of service for existing development could amount to paying for more than its proportionate share. Consequently, impact fees should be reduced to account for future payments that will retire outstanding debt on existing facilities. The issue is less clear-cut when it comes to other types of revenue that may be used to make capacity-expanding capital improvements of the same type being funded by impact fees. Arguably,

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 6

no credit is warranted in most cases, since, while new development may contribute toward such funding, so does existing development, and both existing and new development benefit from the higher level of service that the additional funding makes possible. Impact fee studies in Florida, however, have traditionally given credit for the portion of dedicated revenues, such as gasoline taxes, that are used for capacity-expanding improvements. This study will provide revenue credits for these types of dedicated revenues. Credit has also sometimes been provided for outstanding grants for capacity improvements that can reasonably be anticipated in the future. In addition to the argument presented above (i.e., grants raise the level of service and benefit new development as well as existing development), two additional arguments can be made against applying credit for grants. First, new development in a community does not directly pay for State and Federal grants in the same way they pay local gasoline and property taxes. Second, future grant funding is far more uncertain than dedicated revenue streams. On the other hand, local governments have less discretion about whether to spend grant funding on capacity-expanding capital improvements. In this study, credit will be provided for anticipated future Federal and State grant funding based on recent grant funding history. For the most part, impact fee studies in Florida do not give credit for past property tax payments from vacant land that is now being developed, or for future general fund expenditures for capacity-expanding improvements. However, the previous study did give credit for these types of expenditures, and this study will continue to provide such revenue credits.

Level of Service The role of level of service (LOS) in impact fee analysis is central, but often misunderstood. The previous discussion makes clear the fundamental importance of the concept of level of service in impact fee analysis. However, it is possible to address these issues without specifying a LOS standard in terms of an explicit ratio, such as acres of parkland per 1,000 residents. In reality, the LOS is a set of capital facilities, including land, buildings and equipment, that provides service to a given amount of development. Explicit LOS standards inevitably over-simplify this complex relationship by emphasizing one element of the capital facilities, such as acres of land for parks or square feet of library buildings (or, in some cases a characteristic that is not directly related to capital facilities, such as officers for law enforcement). An alternative is to calculate the level of service in terms of the replacement cost of the capital facilities provided per unit of development served. In fact, this is what impact fee calculations generally do. The choice of an explicit LOS standard to represent this relationship is generally unnecessary, and can create undesirable policy outcomes. For example, a parks and recreation system represents a capital investment in land, buildings and other improvements that provides service to residents. Reducing this relationship to a simple ratio of acres of land to population does provide a concrete, measurable indicator. However, it may unintentionally put undue emphasis on the acquisition of park land, at the expense of the provision of recreational facilities and improvements. The expansion of a park system may involve periods of extensive land acquisition, followed by periods that focus on the development of land with park improvements. Adoption of a LOS standard expressed in acres implies that only additional land acquisition can enhance the level of service. In reality, the level of service provided by a park system can be enhanced by improvements to existing land as well as by acquisition of additional land.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 7

In this impact fee update, the fees are based, for the most part, on the existing levels of service. However, the levels of service do not need to be expressed in the form of simplistic ratios. Nor do explicit LOS standards need to be incorporated into the Comprehensive Plan in order for the impact fees to be consistent with the Plan. It is recommended that the specific LOS standards incorporated into the Comprehensive Plan after the previous impact fee study for non-concurrency facilities (fire rescue, law enforcement, corrections, public buildings and libraries) be replaced with a more general statement along the following lines:

Impact fees shall be based on a level of service for new development that does not exceed the level of service provided to existing development.

Of the facilities under consideration in this study, traffic, schools, parks and solid waste are subject to State concurrency requirements. The County’s adopted level of service for transportation concurrency purposes is set forth in the Capital Improvements Element of the 2020 Comprehensive Plan:

Level-of-Service “D” during peak hour, peak season, peak direction conditions, on all TRIP grant funded roads as well as all freeway, arterial, and collector roadways, with the exception of the following two, which will operate at level of service “E” plus 20%. 27th Ave – South County Line to SR 60 43rd Ave – Oslo Road to 16th Street For SIS/Florida Intrastate Highway System roadways, level of service “B” is adopted for rural areas, and level of service “C” is adopted for urban areas.

According to County staff, the two exception roads have been improved and the “E plus 20%” standard is no longer necessary. Otherwise, the concurrency LOS standard for roads should remain as it is. The traffic impact fees are based on a standard that is different from, but not inconsistent with, the adopted standard. The adopted concurrency standard is focused on individual roadway facilities and utilizes peak hour traffic. The impact fees are based on average daily traffic and focus on the system-wide ratio of capacity to demand. The County’s adopted level of service for schools is expressed in terms of building square feet per student station. These LOS standards were adopted to be consistent with the previous impact fee study, not for concurrency purposes (concurrency was not required for schools at the time). The draft interlocal agreement between the School District, the County and the municipalities for school concurrency, as approved by the School Board on February 13, 2007, establishes the following standard (the “School Service Areas” are defined as elementary, middle and high school attendance zones):

The adopted level of service for each year of the five year planning period and through the long term planning period for each School Service Area will be 100% of the FISH permanent capacity.

The proposed standard is consistent with the school impact fee analysis, which bases the fees on a district-wide ratio of one permanent FISH student capacity per enrolled regular (non-charter school) student.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 8

The adopted concurrency level of service for parks is based on the previous impact fee study. The adopted LOS in the 2020 Comprehensive Plan is “6.61 recreation acres/1,000 permanent plus weighted peak seasonal population” county-wide. The County may wish to consider modifying its adopted LOS for concurrency purposes to base it on the ratio of developed park acres owned or operated by the County to the permanent population residing in unincorporated areas of the county. If the County wanted the concurrency standard to be consistent with the updated impact fees, the acreage would include State-owned land that is leased to the County on a long-term basis for a nominal rate, and would exclude enterprise facilities such as golf courses. On this basis, the current actual LOS for parks is 6.26 acres per 1,000 residents (see park impact fee analysis for detailed calculations). This LOS is based on regional, community and neighborhood parks that are currently available to residents in the unincorporated county. However, it might be prudent for the County to make the concurrency standard somewhat lower than the existing ratio. Regardless of what LOS is established for concurrency purposes, the updated park impact fees will be based on the current actual ratio of the replacement cost of existing park land and facilities to the unincorporated area residents served by these facilities. The adopted level of service for solid waste is also based on the previous impact fee study. The adopted LOS is “2.2 tons or 3.67 cubic yards per capita for permanent plus weighted peak seasonal population per year.” This update uses a “waste generation unit,” or WGU, which is equivalent to one ton per year (a single-family dwelling is estimated to generate 1.6 tons per year), as the service unit, rather than permanent plus weighted peak seasonal population. An alternative concurrency LOS service standard that is consistent with the updated impact fee service unit would be “0.77 cubic yards of class I solid waste per waste generation unit.”

Service Areas The nine types of facilities covered in this report provide service to three different service areas: county-wide, unincorporated areas only and county-wide with an exception. Traffic, schools, libraries, corrections, public buildings and solid waste facilities provide services county-wide. Parks and law enforcement (Sherriff’s Office patrol) facilities provide service to unincorporated areas only. County fire rescue service is provided to development county-wide, with the exception of Indian River Shores, which provides its own municipal fire rescue service.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 9

TRAFFIC The purpose of this section of the report is to assist Indian River County in updating its existing traffic impact fee program. This traffic impact fee update maintains the current traffic impact fee (TIF) formula and local trip characteristics. The calculations in this report are based on the methodology utilized by Tindale-Oliver & Associates in their 2004 update of the traffic impact fee.1 However, one change from the methodology used in the previous study is that the trip lengths were calibrated to reflect actual travel on the major roadway system. The updated impact fee schedule is based on the most recent road cost data from the Metropolitan Planning Organization’s (MPO’s) Long Range Transportation Plan (LRTP) and the County’s adopted Capital Improvement Program (CIP), and the cost of providing additional roadway capacity on those projects. The resulting revised cost per lane-mile is then used to update the impact fee formula cost component and resulting impact fee rate schedule. The credit component update is based on an analysis of revenues that local governments and the Florida Department of Transportation (FDOT) use to construct new and expanded roads in Indian River County. This is determined by updating the number of pennies per gallon of gas tax that return to the community for non-Interstate capital improvements for State, County and municipal road improvements. The work activities accomplished as part of this effort are summarized below:

• Prepared an inventory of the major roadway system. The inventory is used to calibrate trip lengths by land use from the previous study to match existing vehicle-miles of travel (VMT) on the major roadway system. It is also used to demonstrate that there are no existing deficiencies on a system-wide basis.

• Reviewed Cost Feasible Plan of the MPO’s adopted 2030 Long Range Transportation Plan, the

five-year Transportation Improvement Program and the FDOT 2008-2012 Work Program to determine the status of which projects have been completed or are under construction.

• Updated the 2005 total cost estimates for the 2030 Cost Feasible Plan improvements based on

the construction cost inflation index published by Engineering News-Record, as well as updated cost estimates provided by the County Public Works Department.

• Calculated an updated average cost per lane-mile and per vehicle-mile of capacity (VMC)

added to the transportation network based on the adjusted cost of capacity-adding road projects in the 2030 Cost Feasible Plan.

• Identified and reviewed revenue sources used for transportation purposes; determined the

appropriate present value factor to use based on current Federal Reserve interest rate data for state and local bonds; assessed credit components of the current impact fee formula; and determined the credit amount to be applied in the impact fee formula.

1 Tindale-Oliver & Associates, Inc., Update of the Traffic Impact Fee Ordinance – Cost Estimate Variable, Indian River County, February, 2004.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 10

• Prepared an updated impact fee schedule for Indian River County, based on the updated cost and credit components.

The remainder of this section reviews and summarizes the results of the work activities identified above.

Major Roadway System A traffic impact fee program should include a clear definition of the major roadway system that is to be funded with impact fees. The County’s current road impact fee system (i.e., the previous study and current ordinance) does not clearly define the major roadway system. In this update, a definition of the major road system is proposed that includes all collectors, minor arterials and major arterial roads in the county, except for I-95. The Interstate is excluded because a significant portion of the traffic on that facility is likely to be attributable to through traffic that is unrelated to new development in Indian River County. An inventory of the existing major roadway system was compiled from Table 4.7.1 of the Transportation Element of the 2020 Indian River County Comprehensive Plan. The inventory is presented in Table 129, Table 130 and Table 131 in Appendix C. The major purpose of the inventory is to ensure that the travel demand factors for individual land uses in the fee schedule are calibrated to the actual system-wide travel observed on the major roadway system. A secondary purpose is to ensure that the level of service (LOS) implicit in the standard consumption-based road impact fee methodology does not exceed the actual LOS on the major roadway system. The implicit LOS in the standard consumption-based methodology is a system-wide ratio of 1.0 between vehicle-miles of capacity (VMC) and vehicle-miles of travel (VMT) on the major roadway system.

Current Level of Service The secondary purpose for compiling the existing major roadway inventory is to determine the current level of service for impact fee purposes. Oftentimes this is taken to be a segment-specific level of service, such as “all roadway segments shall operate at LOS D or better.” This is in fact the type of level-of-service standard that Indian River County has adopted for concurrency purposes. According to the Capital Improvements Element of the 2020 Comprehensive Plan, the adopted traffic circulation level-of-service standard is:

Level-of-Service “D” during peak hour, peak season, peak direction conditions, on all TRIP grant funded roads as well as all freeway, arterial, and collector roadways, with the exception of the following two, which will operate at level of service “E” plus 20%. 27th Ave – South County Line to SR 60 43rd Ave – Oslo Road to 16th Street For SIS/Florida Intrastate Highway System roadways, level of service “B” is adopted for rural areas, and level of service “C” is adopted for urban areas.

According to the County, the two road segments that are currently allowed to function at LOS E plus 20 percent have been upgraded to four lanes and no longer require a special standard. The level

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 11

of service for concurrency purposes, however, is not necessarily appropriate as the level of service for impact fees. Most road impact fee systems in Florida are not really designed to provide sufficient funding to achieve or maintain such a segment-specific standard. Most road impact fees in Florida, including Indian River County’s, use the standard consumption-based methodology. This methodology essentially charges new development, for every VMT generated, the cost to add a VMC. In other words, the cost per VMT equals the cost per VMC, which implies a one-to-one ratio of VMC to VMT (cost/VMT = cost/VMC times VMC/VMT, where VMC/VMT = 1). This is conservative, because most roadway systems have more than one VMC for every VMT on a system-wide basis. However, even if capacity were to be measured using LOS D, and even if the system-wide level of service were to be set at the existing VMC/VMT ratio, and the fees were based on this level of service, it would still not necessarily be sufficient to ensure that every roadway segment would function at LOS D. A segment-specific level of service standard is simply not appropriate for impact fees calculated using a consumption-based methodology. Why then use a consumption-based methodology? One advantage is that one avoids the problem of segment-specific existing deficiencies. An improvements-based methodology based on all segments functioning at LOS D or better would inevitably create a number of existing deficiencies that could not be remedied with impact fee funds. In addition, some of the non-impact fee funds that are used to remedy the deficiency would be generated by new development, which would need to have its impact fees reduced by a deficiency credit to avoid double payment issues. With the consumption-based methodology, in contrast, there are no deficiencies as long as the system-wide ratio on which the fees are based is no higher than the actual existing VMC/VMT ratio. Another important advantage is the flexibility provided by a consumption-based system. An improvements-based methodology is tied to a specific list of planned improvements determined by a transportation plan to be needed to maintain segment-specific LOS in the face of anticipated growth. Revenues from a consumption-based fee, on the other hand, can be used on any capacity-expanding improvement. As in the prior impact fee study, capacities were based on average annual daily capacity at LOS D. There are no existing deficiencies on the existing major roadway system as a whole, as evidenced by a VMC/VMT ratio significantly greater than one.

Table 2. Existing Major Roadway System Level of Service Road Classification VMC Total VMT RatioPrincipal Arterial 1,660,554 1,116,356 1.49Minor Arterial 1,250,775 934,226 1.34Collector 1,809,904 935,285 1.94Total 4,721,233 2,985,867 1.58 Source: VMC from Table 129, Table 130 and Table 131 in Appendix C; VMT from Table 18.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 12

Cost per Service Unit Expanding the capacity of the County’s major roadway system is primarily accomplished by widening existing roadway cross-sections to accommodate additional through lanes and by building new roads. The traffic impact fee is designed to cover the cost of adding capacity to the roadway system. All of the normal components of a roadway expansion project are eligible for impact fee funding, including engineering and design, right-of-way acquisition, construction of new lanes, reconstruction of existing lanes and relocation of utilities where necessary as part of a widening project, and installation of sidewalks, street lighting and landscaping as part of an improvement project.

Cost per Lane-Mile The previous impact fee update developed detailed road cost estimates for the County’s capacity-adding road projects in the 2025 Cost Feasible Plan. The road cost estimates included separate analysis of right-of-way acquisition costs for planned roads, construction cost estimates and design costs. This update is based on the local average cost to add roadway capacity to the County’s major roadway system based on the most recent cost data. The most recent and comprehensive road construction cost data were developed for Indian River County’s 2030 Cost Feasible Plan in 2005. The locations of these projects are illustrated in Figure 2. The current Cost Feasible Plan includes improvements to I-95, SR 60 and US 1. Including State road improvements in the impact fee calculation is reasonable, because the County increasingly participates in the cost of State road improvements and motor fuel tax credits are provided for the portion of gasoline taxes that are used to fund State road improvements. The improvements to I-95 are excluded from this update, since the County does not participate in construction of interstate highways, and much of the travel on such roads is through traffic unrelated to development in Indian River County. Given the array of projects in the 2030 Cost Feasible Plan and their locations throughout the County, these planned projects are representative of the current average cost to add capacity to the County’s major roadway system. For this study, the 2005 cost estimates have been inflated to 2007 values to reflect the total cost increase since the original estimates were developed. In addition, updated cost estimates have been provided for some projects by the County Public Works Department. The project costs included in Table 3 represent the updated cost of implementing all of the as-yet unconstructed 2030 Cost Feasible Plan roadway capacity improvements. The project costs utilized in updating the impact fee schedule exclude the interstate highway widening on I-95 in order to be consistent with the existing impact fee schedule and trip length methodology.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 13

Figure 2. Indian River County 2030 Planned Roadway Improvements

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 14

Table 3. Planned Improvement Costs

Street From To82nd Ave 26th St CR 510 $28,174,165 1.056 $29,751,918 2 7.05 14.10SR 60 98th Ave I-95 $2,543,842 1.056 $2,686,297 2 0.66 1.32SR 60 I-95 82nd Ave $8,119,445 NA $21,289,000 2 1.34 2.68SR 60 82nd Ave 66th Ave - NA $33,344,000 2 2.00 4.00SR 60 6th Ave Indian River $1,864,758 NA $4,000,000 2 0.30 0.60US 1 S Co. Line Oslo Rd $12,064,823 NA $54,009,000 2 2.16 4.32US 1 Aviation Blvd Old Dixie Hwy $44,372,047 1.056 $46,856,882 2 6.70 13.40US 1 Roseland Rd N Co. Line $5,255,518 1.056 $5,549,827 2 1.00 2.00

$102,394,598 $197,486,924 21.21 42.42

12th St 90th Ave 82nd Ave $3,781,786 1.056 $3,993,566 2 1.00 2.0012th St 43rd Ave 27th Ave $2,854,618 1.056 $3,014,477 1* 1.00 1.0013th St SW 66th Ave 58th Ave $4,041,388 1.056 $4,267,706 2 1.00 2.0013th St SW 43rd Ave 34th Ave $1,560,899 1.056 $1,648,309 2 0.56 1.1213th St SW 34th Ave 27th Ave $3,359,684 1.056 $3,547,826 2 0.44 0.8813th St SW 27th Ave 20th Ave $1,922,225 1.056 $2,029,870 2 0.45 0.9017th St SW 66th Ave 58th Ave $4,019,519 1.056 $4,244,612 2 1.00 2.0026th St 66th Ave 43rd Ave $13,006,154 NA $16,006,154 2 2.00 4.0026th St 82nd Ave 74th Ave $3,850,481 1.056 $4,066,108 2 1.00 2.0027th Ave S Co. Line Oslo Rd $9,560,909 1.056 $10,096,320 2 2.00 4.0027th Ave Oslo Rd SR 60 $12,330,699 NA $24,000,000 2 3.50 7.0043rd Ave Oslo Rd 8th St $8,311,058 NA $13,000,000 2 2.00 4.0043rd Ave S Co. Line Oslo Rd $12,974,563 1.056 $13,701,139 2 2.00 4.004th St 98th Ave 66th Ave $16,262,035 1.056 $17,172,709 2 4.00 8.0053rd St 82nd Ave 66th Ave $9,599,620 1.056 $10,137,199 2 2.00 4.0066th Ave S Co. Line Oslo Rd $8,562,423 1.056 $9,041,919 2 2.00 4.0066th Ave Oslo Rd 4th St $8,887,466 1.056 $9,385,164 2 1.50 3.0066th Ave 4th St SR 60 $8,853,565 NA $15,886,425 2 2.03 4.0666th Ave SR 60 CR 510 $36,173,489 NA $84,385,664 2 7.53 15.0682nd Ave S Co. Line Oslo Rd $7,302,941 1.056 $7,711,906 2 2.00 4.008th St 82nd Ave 74th Ave $3,955,196 1.056 $4,176,687 2 1.00 2.00CR 510 CR 512 US 1 $36,369,280 NA $73,400,478 2 5.82 11.64CR 510 US 1 ICWW $3,718,539 1.056 $3,926,777 2 0.70 1.40CR 512 Fellsmere City I-95 $19,192,929 1.056 $20,267,733 2 3.10 6.20CR 512 I-95 CR 510 $13,317,010 1.056 $14,062,763 2 2.45 4.90CR 512 CR 510 Roseland $6,674,370 NA $15,100,000 2 1.30 2.60Indian Rvr Bvd Royal Palm 37th St $8,678,255 NA $11,000,000 2 1.00 2.00Laconia St CR 510 Concha Dr $11,076,344 1.056 $11,696,619 2 0.55 1.10Oslo Rd I-95 58th Ave $19,484,669 1.056 $20,575,810 2 3.25 6.50Roseland Rd CR 512 US 1 $12,847,897 1.056 $13,567,379 1* 4.70 4.70Schumann Dr CR 510 Barber St $3,974,335 1.056 $4,196,898 2 0.82 1.64

$316,504,346 $449,308,217 63.70 121.70

Aviation Blvd 43rd Ave US 1 $8,537,828 NA $18,000,000 2 1.93 3.86Aviation Blvd US 1 Indian River $14,387,771 NA $30,000,000 4 1.06 4.24Barber St Schumann Dr US 1 $3,621,587 1.056 $3,824,396 1* 1.30 1.30Barber St CR 512 Schumann Dr $7,596,306 1.056 $8,021,699 1* 2.70 2.70Fleming St Easy St US 1 $4,838,861 1.056 $5,109,837 2 1.20 2.40

$38,982,353 $64,955,932 8.19 14.50

Total $457,881,297 $711,751,073 93.10 178.62

Subtotal, FDOT Projects

Subtotal, County Projects

Subtotal, City Projects

Lane-miles

Project Limits Total Cost (2007)

Added Lanes Miles

Total Cost (2005)

Cost Factor

* No new traffic lanes (capacity enhanced by adding a median and turn lanes to an existing two-lane road) Source: Indian River County Metropolitan Planning Organization, 2006 Priority Projects Report, 2006, Table A-9; miles scaled by Duncan Associates; cost factor is Engineering News-Record Construction Cost Index, annual 2005 to April 2007 (NA indicates updated costs provided by IRC Public Works Department, February 28, March 9 and March 21, 2007).

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 15

One of the key inputs into the road impact fee formula is the cost per lane-mile to construct new roadway capacity. The current impact fee methodology is based on the consumption-based approach, in which roadway construction costs are entered into the formula as an average cost for providing new roadway capacity. This average unit cost reflects the relationship between the total project costs and the total number of lane-miles that is to be constructed. As shown in Table 4, the weighted average cost per lane-mile is approximately $4.0 million.

Table 4 Weighted Average Cost per Lane-Mile

Source Total CostLane-Mi.

AddedCost per

Lane-MileIndian River County Projects $449,308,217 121.70 $3,691,933FDOT Projects $197,486,924 42.42 $4,655,514City Projects $64,955,932 14.50 $4,479,719Total $711,751,073 178.62 $3,984,722 Source: Total cost and lane-miles from Table 3.

Roadway Capacity Cost In order to determine the cost of new capacity added by planned road improvements, the consultant reviewed existing and planned roadway characteristics and determined the amount of capacity added by each road project. As in the prior impact fee study, the analysis of the capacity of Indian River County’s road improvements is based on the generalized planning capacity estimates promulgated by the Florida Department of Transportation (FDOT). These capacity estimates are based on Highway Capacity Manual procedures and take into consideration roadway cross-sections, left turn bays at intersections, the spacing of signalized intersections and the characteristics of the area (i.e., rural, rural developed, transitioning to urban and urbanized). As in the prior impact fee study, capacities were based on average annual daily capacity at LOS D. The average capacity per new lane-mile is determined based on the same set of improvements used to determine the average cost per lane-mile. Table 5 shows the total vehicle-miles of capacity added by planned improvements. As noted earlier, these improvements exclude Interstate projects in Indian River County, such as the widening of I-95.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 16

Table 5. Capacity Added by Planned Road Improvements

Street From To Before After NewSR 60 98th Ave I-95 0.66 2 1.32 35,700 53,500 17,800 11,748SR 60 I-95 82nd Ave 1.34 2 2.68 35,700 53,500 17,800 23,852SR 60 82nd Ave 66th Ave 2.00 2 4.00 35,700 53,500 17,800 35,600SR 60 6th Ave Indian River Blvd 0.30 2 0.60 32,700 49,200 16,500 4,950US 1 S. County Line Oslo Rd 2.16 2 4.32 35,700 53,500 17,800 38,448US 1 Aviation Blvd Old Dixie Hwy 6.70 2 13.40 32,700 49,200 16,500 110,550US 1 Roseland Rd N. County Line 1.00 2 2.00 35,700 53,500 17,800 17,800Subtotal, FDOT Projects 13.50 27.00 231,200

12th St 90th Ave 82nd Ave 1.00 2 2.00 0 14,600 14,600 14,60012th St 43rd Ave 27th Ave 1.00 1* 1.00 11,680 15,330 3,650 3,65013th St SW 66th Ave 58th Ave 1.00 2 2.00 0 14,600 14,600 14,60013th St SW 43rd Ave 34th Ave 0.56 2 1.12 0 14,600 14,600 8,17613th St SW 34th Ave 27th Ave 0.44 2 0.88 0 14,600 14,600 6,42413th St SW 27th Ave 20th Ave 0.45 2 0.90 0 14,600 14,600 6,57017th St SW 66th Ave 58th Ave 1.00 2 2.00 0 14,600 14,600 14,60026th St 66th Ave 43rd Ave 2.00 2 4.00 14,600 31,100 16,500 33,00026th St 82nd Ave 74th Ave 1.00 2 2.00 0 14,600 14,600 14,60027th Ave S. County Line Oslo Rd 2.00 2 4.00 11,680 31,100 19,420 38,84027th Ave Oslo Rd SR 60 3.50 2 7.00 14,600 31,100 16,500 57,75043rd Ave Oslo Rd 8th St 2.00 2 4.00 14,600 31,100 16,500 33,00043rd Ave S County Line Oslo Rd 2.00 2 4.00 11,680 31,100 19,420 38,8404th St 98th Ave 66th Ave 4.00 2 8.00 7,600 14,600 7,000 28,00053rd St 82nd Ave 66th Ave 2.00 2 4.00 0 14,600 14,600 29,20066th Ave S County Line Oslo Rd 2.00 2 4.00 0 14,600 14,600 29,20066th Ave Oslo Rd 4th St 1.50 2 3.00 11,680 31,100 19,420 29,13066th Ave 4th St SR 60 2.03 2 4.06 15,330 31,100 15,770 32,01366th Ave SR 60 CR 510 7.53 2 15.06 11,680 31,100 19,420 146,23382nd Ave S County Line Oslo Rd 2.00 2 4.00 0 14,600 14,600 29,20082nd Ave 26th St CR 510 7.05 2 14.10 7,600 14,600 7,000 49,3508th St 82nd Ave 74th Ave 1.00 2 2.00 7,600 14,600 7,000 7,000Aviation Blvd 43rd Ave US 1 1.93 2 3.86 14,600 31,100 16,500 31,845Aviation Blvd US 1 Indian River Blvd 1.06 4 4.24 0 31,100 31,100 32,966CR 510 CR 512 US 1 5.82 2 11.64 14,600 31,100 16,500 96,030CR 510 US 1 ICWW 0.70 2 1.40 14,600 31,100 16,500 11,550CR 512 Fellsmere City I-95 3.10 2 6.20 11,680 31,100 19,420 60,202CR 512 I-95 CR 510 2.45 2 4.90 31,100 46,800 15,700 38,465CR 512 CR 510 Roseland 1.30 2 2.60 31,100 46,800 15,700 20,410Indian River Blvd Royal Palm 37th St 1.00 2 2.00 31,100 46,800 15,700 15,700Laconia St CR 510 Concha Dr 0.55 2 1.10 0 14,600 14,600 8,030Oslo Rd I-95 58th Ave 3.25 2 6.50 11,680 31,100 19,420 63,115Roseland Rd CR 512 US 1 4.70 1* 4.70 11,680 15,330 3,650 17,155Schumann Dr CR 510 Barber St 0.82 2 1.64 11,680 31,100 19,420 15,924Subtotal, County 73.74 143.90 1,075,368

Barber St Schumann Dr US 1 1.30 1* 1.30 11,680 15,330 3,650 4,745Barber St CR 512 Schumann Dr 2.70 1* 2.70 11,680 15,330 3,650 9,855Fleming St Easy St US 1 1.20 2 2.40 0 14,600 14,600 17,520Subtotal, City 5.20 6.40 32,120

Total 92.44 177.30 1,338,688

New Daily VMC

Project Limits Average Daily CapacityMiles

New Lns

New Ln-Mi

* No new lanes added, capacity enhanced by creating a median and turn lanes on existing 2-lane road. Source: Project descriptions, segment lengths, added lanes from Table 3; average daily capacity based on LOS D, from Florida Department of Transportation, 2002 Quality/Level of Service Handbook, 2002, Table 4-1: Generalized Annual Average Daily Volumes for Florida’s Urbanized Area and Table 4-2: Generalized Annual Average Daily Volumes for Florida’s Areas Transitioning into Urbanized Areas.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 17

The average cost per service unit is determined by dividing the total cost of planned improvements by the VMC added by the improvement, as shown in Table 6. The table also shows the average capacity per lane, although this is not an integral part of the impact fee calculations.

Table 6. Road Cost per Service Unit

SourceVMC

AddedLn-Mi.Added

Avg. Capacity per Lane Cost

Cost per VMC

FDOT Projects 231,200 27.00 8,563 $197,486,924 $854Indian River County Projects 1,075,368 143.90 7,473 $449,308,217 $418City Projects 32,120 6.40 5,019 $64,955,932 $2,022Total 1,338,688 177.30 7,550 $711,751,073 $532

Source: Project costs from Table 3; lane-miles added and vehicle-miles of capacity added from Table 5.

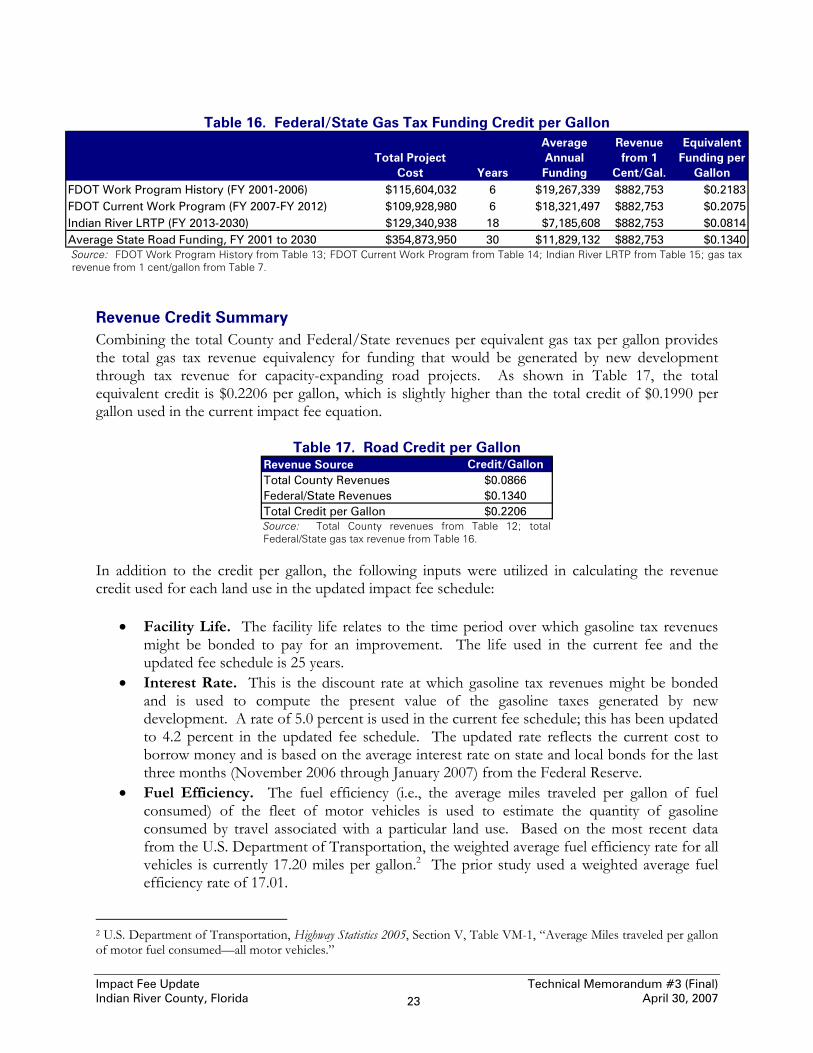

Revenue Credits This section of the report updates the credit calculation to account for revenue generated by new development that will be used to pay for capacity-related capital improvements through motor fuel taxes and sales taxes. To update this credit, the consultant reviewed Indian River County historical expenditures and future appropriations for roadway projects that expand the capacity of the road system. The County primarily utilizes the Local Optional Sales Tax and Local Option Gas Tax in funding road improvements. A credit for State and Federal funding recognizes the Florida Department of Transportation expenditures on State roads in Indian River County. FDOT funding sources include Federal and State gas tax and State general revenue in the form of legislative Transportation Regional Incentive Program (TRIP) appropriations.

Penny per Gallon Gas Tax Equivalent Since the total cost per unit for each land use is developed using vehicle-miles of travel, the credit calculation is also developed using vehicle-miles of travel. To make this calculation, it is necessary to convert the average annual sales tax into an equivalent number of pennies of gas tax. This is accomplished by determining how much revenue is generated from the one penny of the County’s six-cent 1st Local Option Gas Tax based the total revenue distributed to the County. Since all municipalities participate in the traffic impact fee and assess their impact fees based on the County’s impact fee schedule, this study bases the distribution per penny on the county-wide distribution of the 1st Local Option Gas Tax rather than on the amount distributed to the unincorporated area of the County. As shown in Table 7, the value per penny (per gallon of fuel) that is used to calculate the equivalent pennies for all credits is $882,753 per penny.

Table 7. Fuel Tax Distribution per Penny per Gallon, FY 2006-07

1st Local Option Tax (1-6 Cents) Revenue, FY 2007 $5,296,518Amount of Levy per Gallon $0.0600Distribution per Penny $882,753

Source: Total gas tax revenue for FY 2007 from Florida Legislative Committee on Intergovernmental Relations, http://www.floridalcir.gov/reports/ localoptfuel07.pdf.

Impact Fee Update Technical Memorandum #3 (Final) Indian River County, Florida April 30, 2007 18

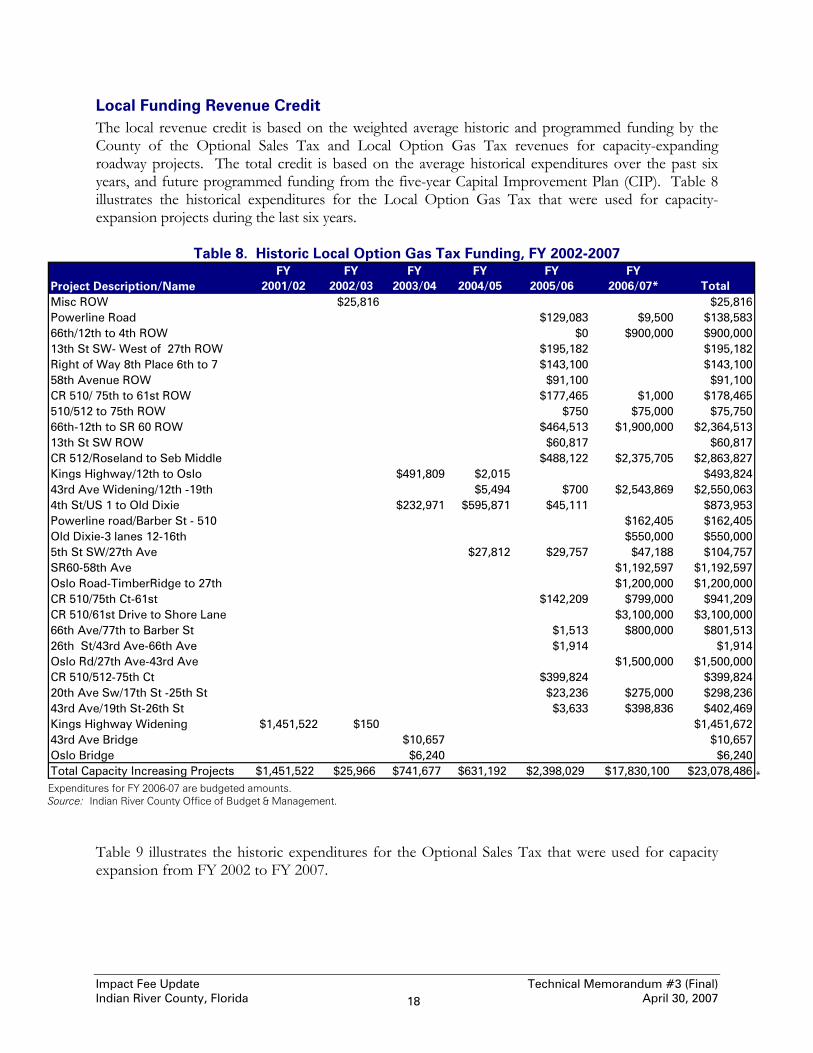

Local Funding Revenue Credit The local revenue credit is based on the weighted average historic and programmed funding by the County of the Optional Sales Tax and Local Option Gas Tax revenues for capacity-expanding roadway projects. The total credit is based on the average historical expenditures over the past six years, and future programmed funding from the five-year Capital Improvement Plan (CIP). Table 8 illustrates the historical expenditures for the Local Option Gas Tax that were used for capacity-expansion projects during the last six years.

Table 8. Historic Local Option Gas Tax Funding, FY 2002-2007

Project Description/NameFY

2001/02FY

2002/03FY

2003/04FY

2004/05FY

2005/06FY