indonesia coal industry update 2016

TRANSCRIPT

Indonesia Coal Industry Update 2016

JOGMEC Coal Investment SeminarTokyo, 27 January 2016

CONTENTS

Indonesia Coal Industry1

Coal as Key to Increase Electrification Ratio2

Future Energy Mix3

CONTENTS

Indonesia Coal Industry1

Coal as Key to Increase Electrification Ratio2

Future Energy Mix3

Coal Contribution to Indonesia Economy

Sources: Badan Pusat Statistik

Other then being the most economical source of energy for electricity, coal mining industry plays an important role in supporting Indonesia’s economy

65105

131160

195

254

333

398

462483 480

3.1%

4.3%4.4%

4.5%4.4%

4.9%

5.2%

5.4%

5.6%

5.3%

4.8%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

0

50

100

150

200

250

300

350

400

450

500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Trillion Rp.

GDP from Non Oil & Gas Mining

PDB Tambang Non-Migas % dari Total PDB

2.74.3

6.1 6.7

10.5

13.8

18.5

27.2 26.224.5

20.8

3.8%

5.1%

6.0%5.8%

7.6%

11.9%11.7%

13.4%13.8%

13.4%

11.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Billion US$Coal Export

Export batubara (US$ Billion) % dari Total Ekspor

Historical Indonesian Coal Production 2009 – Oct 2015

Sources: Directorate General Mineral & Coal, MEMR

254 275

353

412

474 458

322.5

198210

287

345

402382

215

56 65 66 67 72 76 62

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

0

50

100

150

200

250

300

350

400

450

500

2009 2010 2011 2012 2013 2014 2015Production (Million Tons) as Per October 2015

Export (Million Tons) as Per October 2015

Domestic Sales (Million Tons) as Per October 2015

Average of Coal Price based on HBA USD/MT as Per December 2015

Estimated Domestic Coal Consumption - 2016

81%

2%

2% 12%

2% 1% 0%

2016 DMO Composition (%)

Coal fired power plant Metallurgy

Fertilizer Cement

Textile Paper

Briquette

Domestic Consumption (MT)

Coal fired power plant 82

Metallurgy 2

Fertilizer 2

Cement 12

Textile 2

Paper 1

Briquette 0

TOTAL 101

Sources: Directorate General Mineral & Coal, MEMR

Currently, Indonesia is still dependent on coal exports as domestic consumption can only absorb a small portion of total coal production.

Depressed Coal Price has affected CAPEX Coal Mining

Company

*source: Bloomberg, internal analysis

Companies included: ABMM, ADRO, ARII, BORN, BRAU, BSSR, BUMI, BYAN, GEMS, GTBO, HRUM, INDY, ITMG, KKGI, MBAP, PTBA, TKGA, TOBA

• CAPEX of publicly listed coal mining company has been down significantly by 80% since 2012 as a result of significant lower coal price

• Most of the Companies cutting back on expansion and exploration. Low investment made will result no new reserves identified over last three years

• Total accumulated CAPEX for the last 5 years reach US$5.6 bn

0

0.5

1

1.5

2

2.5

2011 2012 2013 2014 Ann. 2015

in billion USD

CAPEX Coal Mining Listed Co –Last 5 Years

1.931.83

0.93

0.52

0.40

Total

CAPEX:

US$5.6 bln

20

40

60

80

100

120

140

01 J

an 2

011

01 A

pr

2011

01 J

ul 2011

01 O

ct 2011

01 J

an 2

012

01 A

pr

2012

01 J

ul 2012

01 O

ct 2012

01 J

an 2

013

01 A

pr

2013

01 J

ul 2013

01 O

ct 2013

01 J

an 2

014

01 A

pr

2014

01 J

ul 2014

01 O

ct 2014

01 J

an 2

015

01 A

pr

2015

01 J

ul 2015

01 O

ct 2015

NEWC Evolution 2011 – Jan 2016 (6,322 GAR)

Jan 2011

US$130/ton

Jan 2016

US$49/ton

• Global Coal Index NEWC declined by 62% fromthe highest level US$130/ton in January 2011 toUS$49/ton di January 2016

APBI-ICMA INTERNAL SURVEY

*Survey result as of May 6th, 2015

43%

18%

39%

Coal Price Forecast

Decrease

Increase

Flat

10%

69%

21%

CapEx Policy

Increase

Decrease

Flat

29%

26%

45%

Production Volume Policy

Increase

Decrease

Flat51%

24%

24%

Employee Rationalization

Not rationalizing

<10%

>10%

CHALLENGES: GOVERNMENT POLICIES

1. Significant rate increase

2. Upfront payment upon permit approval instead of upon usage

1. Additional costs during distressed coal market condition

2. Potential cash flow management disruption

3. Creating confusion due to lack of technical guidelines

1. Additional costs related to logistics and infrastructure use

2. Ports designation may not be transparent

1. Increasing unemployment because of mine closures

2. Not necessarily increasing government revenue

3. Potential disruption in government’s 35 GW plan

Letter of Credit requirement for export activities

Non-tax state revenue from land use of forest areas

Plan of limiting coal shipment from 14 designated ports

Royalty increase plan

1. Supplies and contractor rates are already in US$

2. Potential hedging costs

Requirement of Rupiah as the only currency for domestic transactions

CONTENTS

Indonesia Coal Industry1

Coal as Key to Increase Indonesia Electrification Ratio2

Future Energy Mix3

6.0% 4.6% 6.2% 6.5% 6.3% 5.7% 5.1%

129.0 134.2147.3

158.0174.0

187.5197.3

0

50

100

150

200

250

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2008 2009 2010 2011 2012 2013* 2014**

TW

hGDP Growth (%) Electricity Sales (TWh)

Economic growth needs to be supported by sufficient Electrification Ratio (ER)

Installed Capacity in Indonesia is always below the energy demand

Current Economic and Electricity Condition

Indonesia Economic & Electricity Growth

Sources: PLN, IEA World Energy Outlook 2014 (for ER), Badan Pusat Statistik, RUPTL 2015, MEMR Presentation Sept 2014**Estimated by PLN & BPS

CAGR 7.3%

0

200

400

600

800

1,000

1,200

0

50

100

150

200

250

300

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

Existing Capacity (GW) Additional Power Needs (GW)

Peak Load (GW) Electricity Needs (TWh)

GW TWh

Installed Capacity vs Electricity Needs

Indonesia Electricity Overview

22 GW

13 GW

4 GW

3 GW

1 GW

- 5 10 15 20 25

Coal-fired

Gas-fired

Hydro

Diesel

Others

Installed Capacity* 43 GW

Coal and gas are the largest sources of energy for electricity generation with highest total

installed capacity and at the most economical price

Power plant investments must be focused towards developing Coal-fired and Gas-fired Power Plants

Sources: RUPTL 2015-2024, Buku Statistik PLN 2014

Coal is still the cheapest and most abundant energy source for power

generation

* Per December 2014, excluding rental from 3rd party sources ~4 GW

Energy Source Costs (per KWh)

0

0.05

0.1

0.15

0.2

0.25

0.3

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Cost (Rp/KWh) Cost (US$/KWh)*

* Exchange rate Rp 13,500/USD

3841

4548

5155

6064

0

10

20

30

40

50

60

70

2015 2016 2017 2018 2019 2020 2021 2022

in G

W

Peak Load (in GW)

Sources: PLN Investor Presentation May 2015, RUPTL 2015-2024, MEMR, World Bank

Projected Growth in Peak LoadTarget 2019: >95%

Growing Power Demand

ASEAN Electrification Ratio Comparable

As government pushes for infrastructure & industrial development, low electricity

consumption and installed capacity levels create significant increase in electricity demand

Government aims to achieve >95% electrification rate by 2019, hence PLN Programs such as Fast Track and IPP are enforced to attract Private Sector to enter into Electricity Sector

Power Generation Overview

2639

57 60 6

8

3344

2010 2014 2019 2024

PLN IPP

Indonesia projected additional 50-60 GW until 2024 to achieve electrification ratio of >95%

To accelerate the needs of Electricity, Government of Indonesia initiated 35 GW

Program from 2015-2019 and to follow up on several delayed projects from FTP 1 & 2 to

increase Electrification Ratio to >95%

PLN IPP

Size: 25 GWTransmission: 360 kms

Size: 18 GWTransmission: 50k kmsSubstation: 743 loc.

32 GW

47 GW

90 GW

104 GW

Projected Installed Capacity

Sources: PLN Investor Presentation 2015, RUPTL 2015-2024

GOVERNMENT 35 GW PROGRAM

*source: Internal calculations; RUPTL 2015-2024

35 GW Power Project

Coal Fired Power Plant

Gas & Steam Power Others

~20 GW ~12GW ~3GW

PLN

2 GW

IPP

18 GW

Project CostsUS$28 – 35 bln

57% 34% 9%

DEBT (Proj. Financing)

US$20 – 25 bln

EQUITYUS$8 – 11 bln

Sources: RUPTL 2015-2024, APBI CEO Gathering

Administration under President Jokowi has committed to add 35 GW power to existing installed capacity of 47 GW (until Dec 2014)

55-60% of total 35 GW power projects will come from coal-fired power plants and require significant participation from private (IPP)

Total project cost to be borne by private sector / IPP : US$ 28 – 35 bln

Total IPP Projects

TenderedIPP Projects

Soon to be Tendered

IPP Projects

Existing IPP Projects*

35.59 GW

Capacity Project CostMax

Potential Revenue p.a.

Max EBITDA p.a.**

16.92 GW

11.04 GW

7.63 GW

US$ 68.5 Bn

US$ 31.1 Bn

US$ 19.3 Bn

US$ 18.1 Bn

US$ 18.3 Bn US$ 8.2-9.2 Bn

US$ 8.1 bn US$ 3.6-4.1 Bn

US$ 5.5 Bn US$ 2.5-2.7 Bn

US$ 4.7 Bn US$ 2.1-2.4 Bn

*Per Dec 2014, using the same assumptions as new IPP Projects** EBITDA = 45-50% of Revenues

IPP market of 36 GW is projected to be approximately US$ 70 billion market opportunity Out of 70 GW, ~60% will come from coal-based Wide-open opportunities to becoming main player in non-coal energy segment

Sources: RUPTL 2015-2024, PLN Market Sounding 2015, US EIA Report 2013, internal data analysis, APLSI

35 GW Program Open Participation of Private

Sector

35 GW Electricity Program and Industrial Development

Will Increase Electricity Demand dan Domestic Coal

Consumption

• As the government pushes infrastructure and industrial development, the demand for electricity will increase and subsequently domestic coal consumption for electricity generation will increase.

• Assuming 5%-6% economic growth in 2015-2017, and 7% onward, coal consumption for electricity will increase by 10% CAGR in 2015-2024.

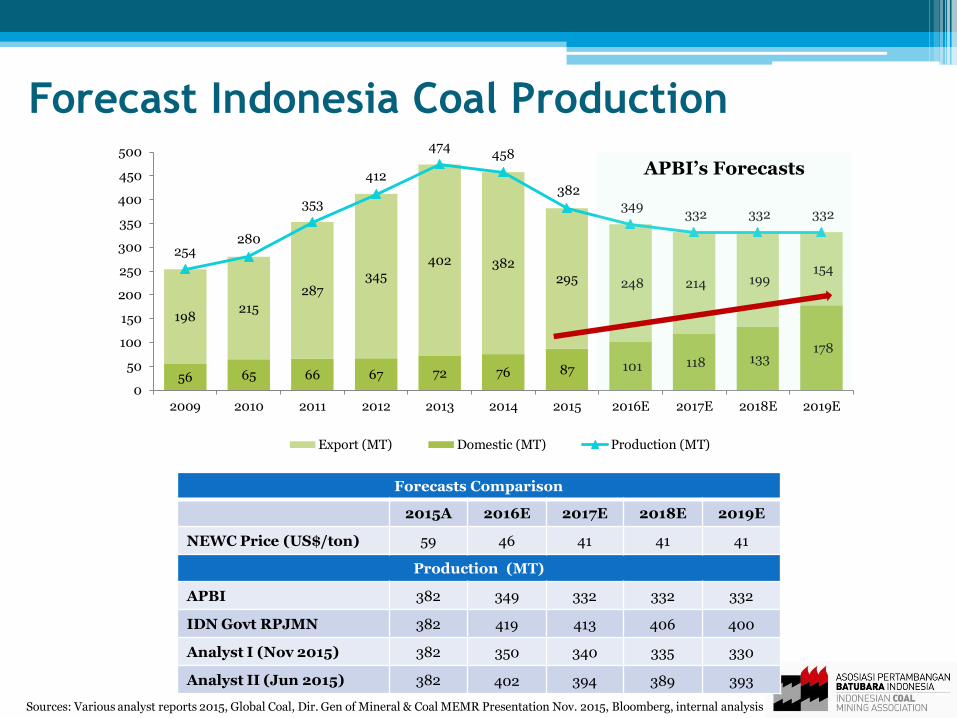

56 65 66 67 72 76 87 101 118 133 178

198215

287345

402 382295 248 214 199

154

254280

353

412

474458

382 349

332 332 332

0

50

100

150

200

250

300

350

400

450

500

2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Export (MT) Domestic (MT) Production (MT)

APBI’s Forecasts

Forecast Indonesia Coal Production

Sources: Various analyst reports 2015, Global Coal, Dir. Gen of Mineral & Coal MEMR Presentation Nov. 2015, Bloomberg, internal analysis

Forecasts Comparison

2015A 2016E 2017E 2018E 2019E

NEWC Price (US$/ton) 59 46 41 41 41

Production (MT)

APBI 382 349 332 332 332

IDN Govt RPJMN 382 419 413 406 400

Analyst I (Nov 2015) 382 350 340 335 330

Analyst II (Jun 2015) 382 402 394 389 393

Coal Requirements post Realization of 35 GW

Existing Coal Fired

PP (30 Sept 2014)

Estimated Under 35

GW

Total

22 MW

20 MW

42 MW

CapacityCoal

Cons p.a

76 mln

~75 mln

~150 mln

Coal TypeReserves

(billion ton)

Low 9.5

Medium 20.1

High 1.8

Total 31.4

1 Jan 2013 Now

NEWC

PriceUS$ 94/MT US$ 52/MT

Reserve 31 bln MT-25 ~ 30

%

As of 1 January 2013

Coal Requirement – Next 5 years Coal Reserves

Domestic

Export 300 – 350 mln ton

Total 456 – 506 mln ton

WITH COAL PRICE KEEP GOING DOWN, THE AMOUNT OF RESERVE WE HAVE IS GETTING SMALLER.

Sources: Bloomberg, APBI internal calculation, Handbook of Energy and statistics of Indonesia 2014

CONTENTS

Indonesia Coal Industry1

Coal as Key to Increase Electrification Ratio2

Future Energy Mix3

Coal61%

Gas16%

New and Renewable

Energy22%

2025

ENERGY MIX LANDSCAPE

Sources: PLN Investor Presentation, May 2015; Indonesia’s National Energy Council’s Energy Outlook 2014; RUPTL 2015-2024

Coal50%

Gas27%

Hydro8%

Geothermal3%

Oil12%

2014

Coal66%

Gas 18%

New and Renewable

Energy16%

2050Government Initial Energy Mix Target

• By 2025, Indonesia plans to no longer use oil as power generation source and convert to other renewable energy sources

• Renewable energy such as solar and hydro power technology is rapidly developing, resulting in falling cost curves and more competitive investment costs

• Renewables as energy source were initially planned to rise from ~11% in 2014 to ~ 22% in 2025

CONCLUSION

Continued decreasing coal demand from China still causes market oversupply and therefore, further weakens coal prices, which affects production outputs of Indonesian miners

From 2014 to 2015, domestic coal demands increased 14% y-o-y from 76 MT to 87 MT and is expected to continue to increase. Though currently, Indonesia still needs to rely on exports as domestic usage of coal only absorbs a small portion of total Indonesia production

The 35 GW Program provides investment opportunities and is expected to revive the coal industry through their high installed capacity projections of coal fired power plants. In 2019, Indonesian domestic consumption of coal is expected to more than double 2015 consumption and overpass exports

In addition to utilizing the country’s cheapest energy source (coal), the government also increases opportunities towards growing renewable energy portion for power generation sources