indonesian lng challenges aheadlng-world.com/lng_bali2014/slides/lng bali - day 1 pdf/skk...

TRANSCRIPT

SPECIAL TASK FORCE FOR UPSTREAM OIL AND GAS

BUSINESS ACTIVITIES

(SKK MIGAS)

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

Indonesian LNG – Challenges Ahead

Widhyawan Prawiraatmadja Deputy Chairman for Commercial Management Special Task Force for Upstream Oil & Gas Business Activities (SKK Migas) Bali, 19th May 2014

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

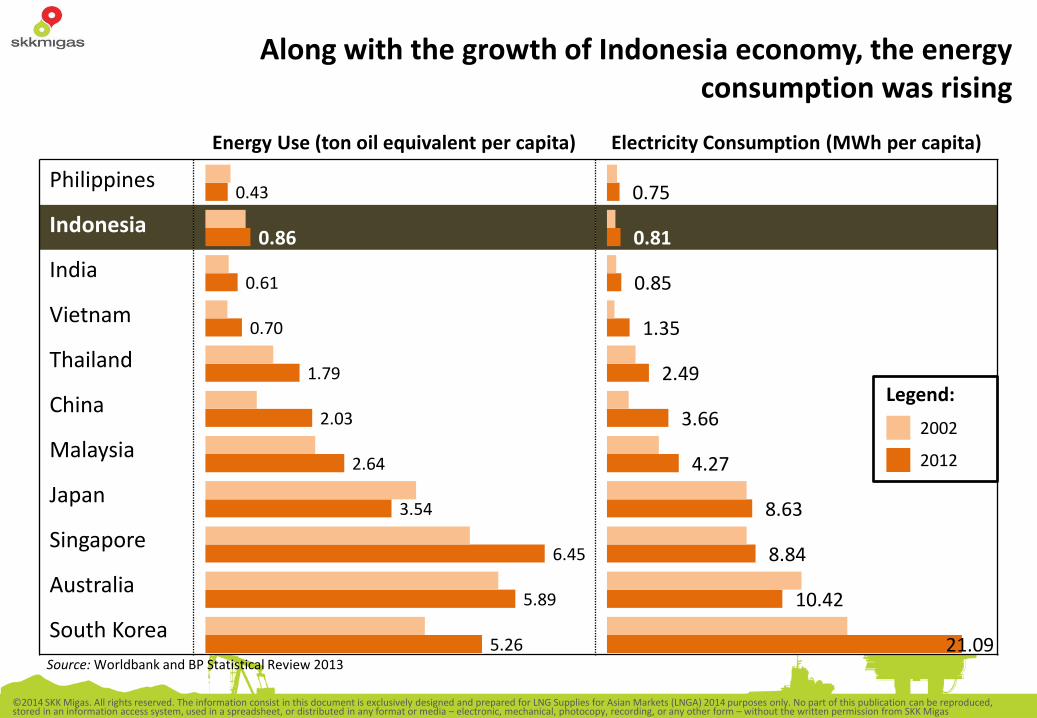

Indonesia macroeconomic has performed impressively over the past decade and been predicted still growing over next decades

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

Philippines

Indonesia

India

Vietnam

Thailand

China

Malaysia

Japan

Singapore

Australia

South Korea

Along with the growth of Indonesia economy, the energy consumption was rising

5.26

5.89

6.45

3.54

2.64

2.03

1.79

0.70

0.61

0.86

0.43

21.09

10.42

8.84

8.63

4.27

3.66

2.49

1.35

0.85

0.81

0.75

Energy Use (ton oil equivalent per capita) Electricity Consumption (MWh per capita)

2002

2012

Legend:

Source: Worldbank and BP Statistical Review 2013

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

As a key economic driver, Indonesia upstream industry is one of major players in Asia that experiences the shifting from oil into gas

dominance

Peak 1977 Peak 1995

Starting 2002, upstream energy in Indonesia is dominated by gas and this trend will continue in the future.

Indonesia still have several major gas projects that will be on stream in the near future.

OIL

GAS

Dominated By GAS

Dominated By OIL

Source: SKK Migas Source: SKK Migas

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

Indonesia has been a LNG producer for more than 35 years with 3 major LNG Plants

1972 First discovery of Arun Gas Field

1971 First discovery of Badak Gas Field

1977 First shipment of LNG loaded

1982 World record for safety awarded to PT. Badak

1994 First discover of Wiriagar Deep Gas

2002 • Gas sales purchase

agreement with Fujian, China

• Tangguh became the third LNG center in Indonesia

2004 Gas sales purchase agreement with: • POSCO, Korea • K-Power, Korea • Sempra, US • Tohoku

2010 Gas sales purchase agreement with Chubu Electric Power, Japan

2016 Chevron IDD Bangka Field on stream

2018 • Chevron IDD Gehem • Inpex Masela

2019 • Train 3 BP

LNG Tangguh • VICO CBM

2009 1st LNG Shipment from BP Tangguh

2012 1st LNG Shipment from Badak to West Java FSRU

2017 • ENI Muara Bakau • Chevron IDD Gendalo

Started since 1977 from two LNG plants in Arun (Aceh) and Bontang (Kalimantan), and their capacities are gradually increased to 12.3 MTPA and 22.2 MTPA respectively. Both plants reached its peak production at 29 MTPA in 1999, and had declined to 11.5 MTPA in 2013.

The third LNG center called as Tangguh is established in Papua since 2004 and started its production at the end of 2009, and produce 7.12 MTPA in 2013, approaching its capacity production of 7.6 MTPA.

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013

M T

P A

BONTANG

Production Trend of 3 LNG Plants in Indonesia (2005-2013)

Source: SKK Migas

Source: SKK Migas

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

To fulfill domestic energy demand, Indonesia LNG industry is facing many challenges

Energy Domestic Fulfillment Technical

• Moving to Eastern Indonesia

• Lack of infrastructure

Economic

• Maintaining Contractor Profitability

• Domestic gas price issue

Socio-Political

• Demanding more national interests

• 2014 Election

Regulatory • Land acquisition • Sectoral

regulations, etc.

The Challenges

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

Government of Indonesia have been showing commitment to improve regulatory management in the upstream industry

Regulatory

There is a concerted effort to transform the licensing process into one door licensing system within related institutions. In the upstream oil and gas, the current progress is to simplify all permits into 8 type of licenses:

Government Effort

• land acquisition license • forest area utilization • foreign ship utilization • dry docking FSO/FPSO

• drilling waste dumping • licenses by province government • licenses by regency government • license for land intersection with

train

On process to create good investment climate by: 1. Exploration incentives 2. Provide good data for exploration area 3. Implement tax free on using shared facilities

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

Government of Indonesia have been trying to maintain an optimal profit margin (GOI and Contractor) even though high cost

of the exploration and exploitation Economic

0

5

10

15

20

25

0 2 4 6 8 10 12 14

Economics of Gas Field Development

*The bubble scales are representing the field gas reserves based on POD approval.

Gas Price (US$/MSCF)

IRR

(%

)

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

Current LNG Prices for Indonesian Domestic Contracts have become closer to that of exports Economic

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

LNG

Pri

ce (

$/M

MB

TU)

Contract Signing Year

Indonesian Domestic LNG Contract

Domestic Price

Export Price

Indonesia LNG Prices

Source: SKK Migas

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

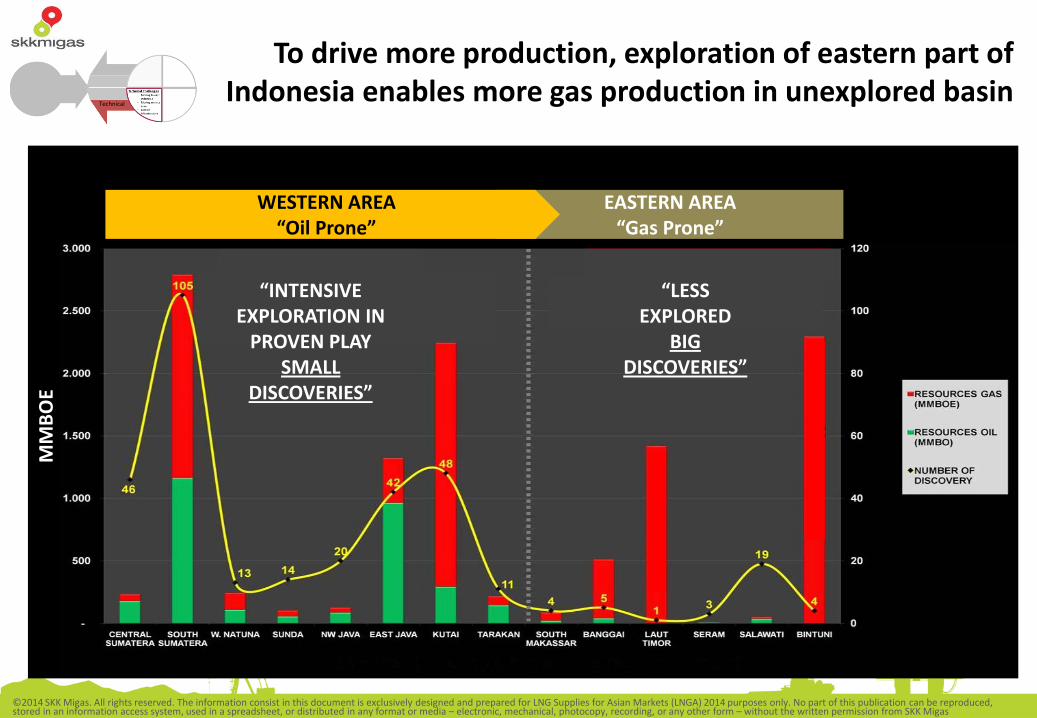

EASTERN AREA “Gas Prone”

To drive more production, exploration of eastern part of Indonesia enables more gas production in unexplored basin

MM

BO

E

“INTENSIVE EXPLORATION IN

PROVEN PLAY SMALL

DISCOVERIES”

“LESS EXPLORED

BIG DISCOVERIES”

WESTERN AREA “Oil Prone”

Technical

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

In addition to the existing gas infrastructures, new gas pipelines and FSRUs are being constructed and planned to support the

domestic demand

11 11 11

Technical

FSRU Nusantara Regas Capacity: 3 MTPA On stream Mid of 2012 Allocation in 2014: 27 cargoes (Bontang & Tangguh)

Planned LNG Receiving Terminal

Existing Pipeline

Planned Pipeline

CNG Plant

LNG Plant

Existing

Project

Potential

Gas Supply: Gas Demand:

Contracted

Commited

Potential

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

The rising energy demand as consequence of rapid economic growth will make Indonesia more focus in supplying its domestic

needs. However, exports will be maintained for existing contracts as well as to support new project developments. As domestic

demand will grow in gradual manner, there is a need to implement more interruptible mid-terms contracts to create the

flexibility in domestic and export supply.

While exports are being maintained, most of additional gas supply now goes to the domestic market

4,3

97

4,4

16

4,2

02

4,0

08

3,8

20

3,7

75

3,6

81

4,3

36

4,0

78

3,6

31

3,4

02

3,4

04

1,4

80

1,4

66

1,5

13

2,3

41

2,5

27

2,9

13

3,3

23

3,3

79

3,2

67

3,5

50

3,7

74

4,5

60

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013* 2014

BB

TUD

Export Domestic

*

Source: SKK Migas * Projection

©2014 SKK Migas. All rights reserved. The information consist in this document is exclusively designed and prepared for LNG Supplies for Asian Markets (LNGA) 2014 purposes only. No part of this publication can be reproduced, stored in an information access system, used in a spreadsheet, or distributed in any format or media – electronic, mechanical, photocopy, recording, or any other form – without the written permission from SKK Migas

End Remarks

• In meeting growing Indonesia’s gas demand, Increasing LNG use for domestic consumption is unavoidable. Gas infrastructure will be key in facilitating the consumption growth.

• Indonesia used to be a net-oil exporter but shifted to a net-oil importer in 2003, nonetheless Indonesia still exports crude oil until today. If it is done optimally, there is nothing wrong to import gas for domestic use. Pertamina has already secured volumes from US LNG.

• The existence of growing domestic demand and export contracts create an opportunity to supply gas in a portfolio basis.

• Significant gas base load demand can be created, as replacement of fuel base consumption, especially since gasoil use is still spread out. Once the base demand and infrastructure are in place, gas consumption will proliferate, hence creating Indonesia not only as importance LNG producers but also as LNG consumers.

• The big question is “Can Indonesia create a good investment climate so that continuing natural gas exploration and production as well as its infrastructure development can be a sustainable business proposition?”

HEAD OFFICE Wisma Mulia LG, 21, 22, 23, 27, 28, 29, 30, 31, 33, 35, 36, 37, 38, 39, 40 Jalan Jenderal Gatot Subroto Kav. 42, Jakarta 12710, INDONESIA

PO BOX 4775 Telephone : +62 21 2924 1607

Facsimile : +62 21 2924 9999

SPECIAL TASK FORCE FOR UPSTREAM OIL AND GAS BUSINESS ACTIVITIES (SKK Migas)

14