industry 4.0 and minas gerais4rvaesbr.com.br/aes/wp-content/uploads/rb-industry-40-and... ·...

TRANSCRIPT

Apresentação

Belo Horizonte, June 7th 2018

Industry 4.0 and opportunities for Minas Gerais

2 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation.

It may not be passed on and/or may not be made available to third parties without prior written consent from .

© Roland Berger

Contents Page

A. Roland Berger at a glimpse and our topic references 3

B. Industry 4.0 as a productivity lever 11

C. Business opportunities for Minas Gerais due to technological advancements 23

D. What this means to the industries in Minas Gerais and how we can help 37

A. Roland Berger at a glimpse and our topic references

4 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Exp

erie

nce

Our team has deep expertise in mining and the applications of Industry 4.0 in this sector

Team expertise

> 20 years of industry (Automotive industry executive) and consulting experience (9 years)

> Led over 100 projects in the industrial landscape on the last couple of years

> Projects involving growth strategies (organic and M&A) and new technologies, as well as restructuring and operational efficiency among others

> Mechanical engineer (Unicamp) and MBA (IE Business School, Madrid)

Rodrigo Custódio

Principal

> 29 years of industry experience (Embraer and Arcelor Mittal) and strategy consulting

> Key areas of expertise include Competitive Intelligence, Strategic Alliances, Corporate Strategy and Business Development

> Led several projects of Intelligence and market entry for multinational companies

> Economist by UFMG, Master in Business from FDC and specialization in Global Strategic Management from Harvard

Paulo Franklin

Senior Advisor

Source: Roland Berger

5 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

5

Roland Berger is a German consulting firm with over 50 years of history worldwide and in Brazil since 1976

Our profile

Founded in 1967 in Germany by Roland Berger

About 220 RB Partners currently serving

~1,000 international clients

50 offices in 36 countries with around 2,400 employees

Present in Brazil since 1976 (41 years)

Over 500 successful projects across Latam since 2000

Experienced team in São Paulo leveraging

our global network know-how

Source: Roland Berger

6 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

6

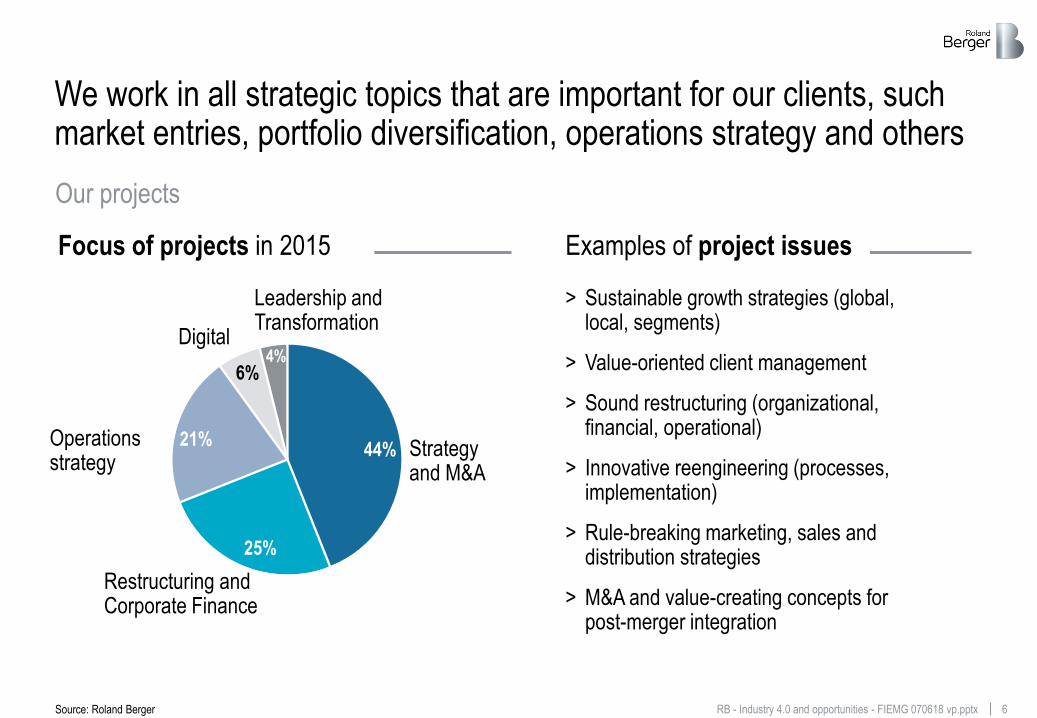

We work in all strategic topics that are important for our clients, such market entries, portfolio diversification, operations strategy and others

Focus of projects in 2015

> Sustainable growth strategies (global, local, segments)

> Value-oriented client management

> Sound restructuring (organizational, financial, operational)

> Innovative reengineering (processes, implementation)

> Rule-breaking marketing, sales and distribution strategies

> M&A and value-creating concepts for post-merger integration

Digital

Leadership and Transformation

Strategy and M&A

Restructuring and Corporate Finance

Operations strategy

44%

25%

6%

21%

4%

Source: Roland Berger

Examples of project issues

Our projects

7 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

7

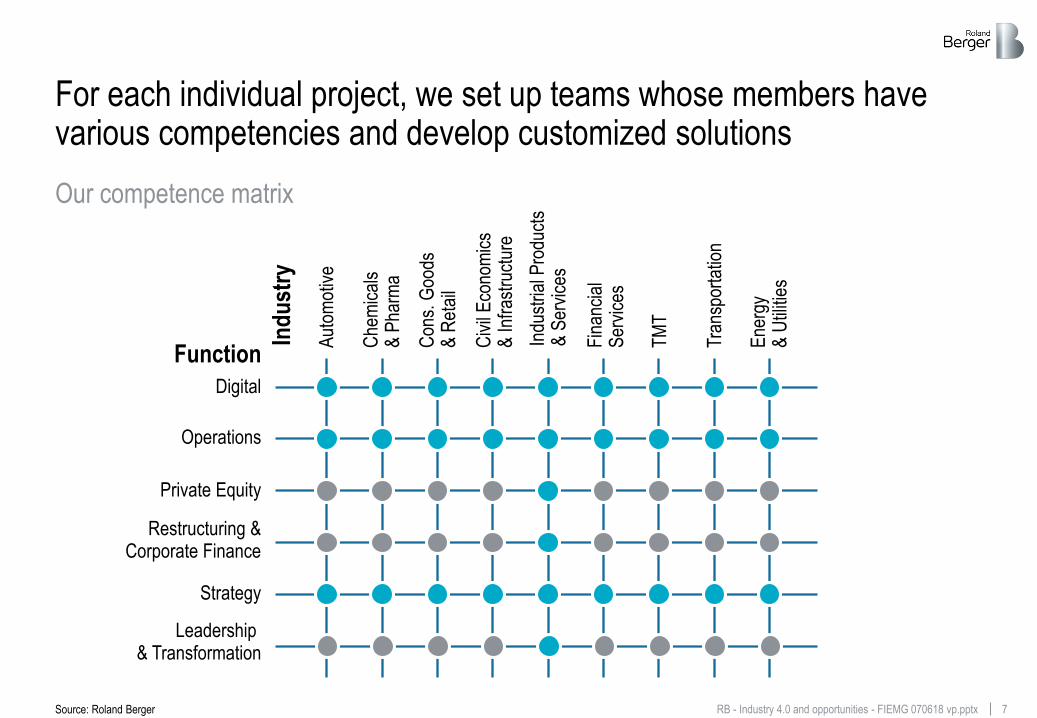

For each individual project, we set up teams whose members have various competencies and develop customized solutions

Function

Ind

ust

ry

Con

s. G

oods

&

Ret

ail

Indu

stria

l Pro

duct

s

& S

ervi

ces

Ene

rgy

&

Util

ities

Digital

Operations

Private Equity

Restructuring & Corporate Finance

Strategy

Aut

omot

ive

Che

mic

als

&

Pha

rma

Fin

anci

al

Ser

vice

s

TM

T

Tra

nspo

rtat

ion

Civ

il E

cono

mic

s &

Infr

astr

uctu

re

Leadership & Transformation

Source: Roland Berger

Our competence matrix

8 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

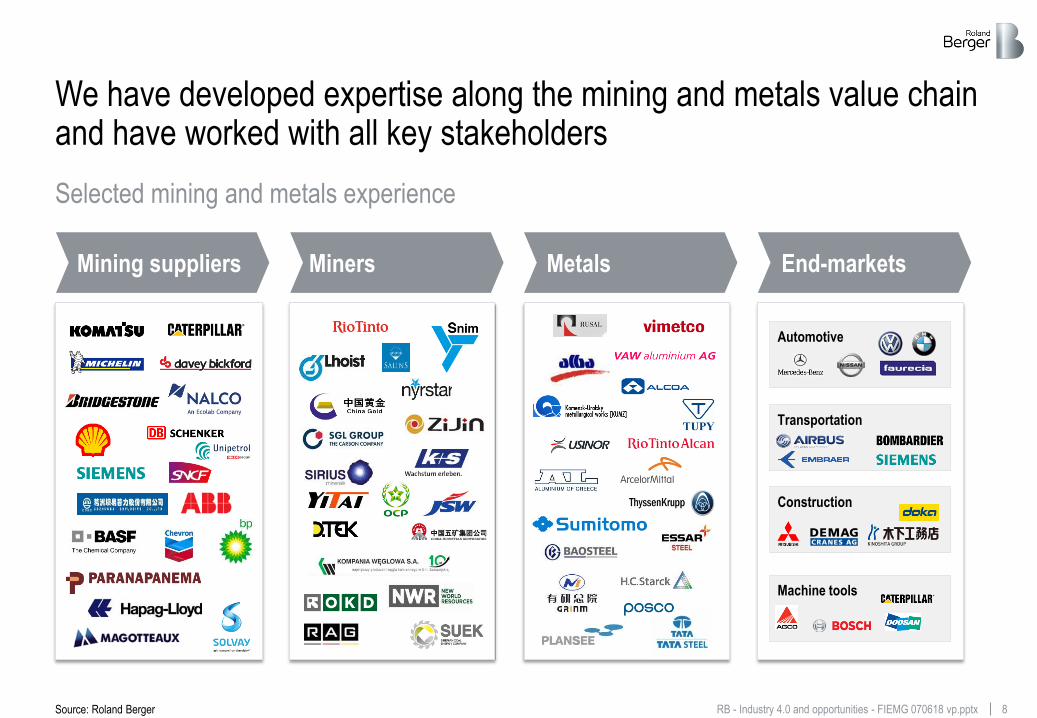

We have developed expertise along the mining and metals value chain and have worked with all key stakeholders

Mining suppliers Miners Metals End-markets

Automotive

Transportation

Construction

Machine tools

Source: Roland Berger

Selected mining and metals experience

9 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

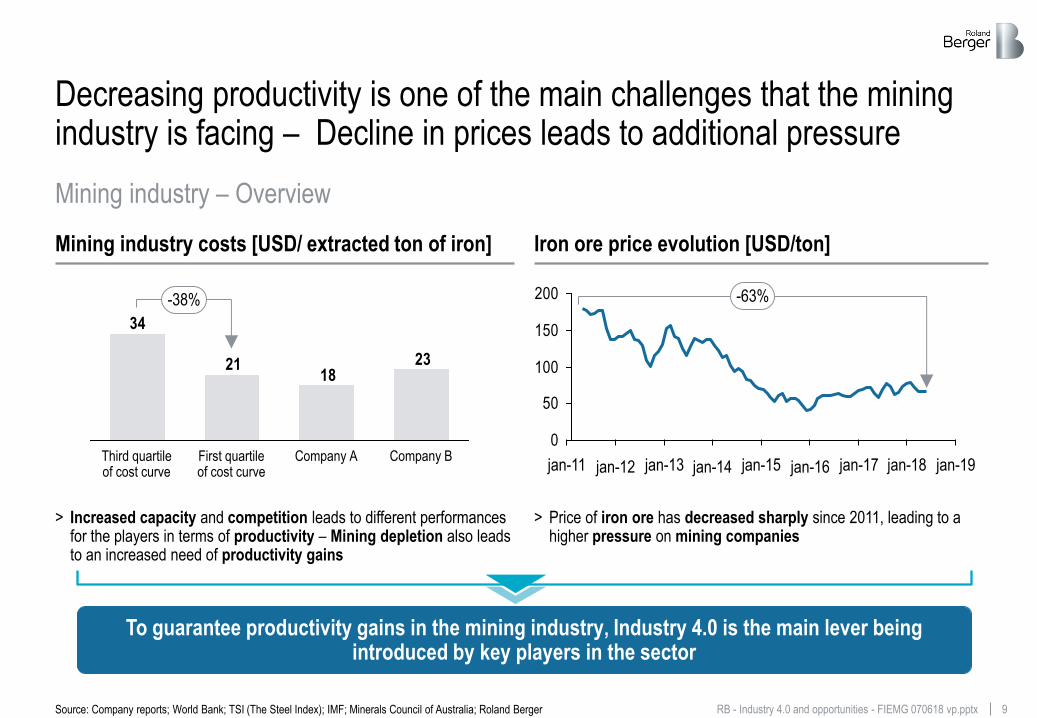

Decreasing productivity is one of the main challenges that the mining industry is facing – Decline in prices leads to additional pressure

Mining industry costs [USD/ extracted ton of iron] Iron ore price evolution [USD/ton]

0

50

100

150

200

jan-11 jan-13 jan-17 jan-15 jan-14 jan-16 jan-19 jan-18 jan-12

-63%

Source: Company reports; World Bank; TSI (The Steel Index); IMF; Minerals Council of Australia; Roland Berger

Mining industry – Overview

2318

21

34

First quartile of cost curve

Third quartile of cost curve

Company A

-38%

Company B

To guarantee productivity gains in the mining industry, Industry 4.0 is the main lever being introduced by key players in the sector

> Price of iron ore has decreased sharply since 2011, leading to a higher pressure on mining companies

> Increased capacity and competition leads to different performances for the players in terms of productivity – Mining depletion also leads to an increased need of productivity gains

10 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

As mineral production value in Brazil decreases, companies must adapt and find new opportunities in the mining sector

Business opportunities in the mining sector

> With the decline in the value of mineral production in Brazil in recent years, companies have started to look for additional business opportunities

> There are new technologies emerging, such as additive manufacturing and batteries for electric vehicles and energy storage

252426

4044

4853

39

0

10

20

30

40

50

60

2015 2016

-52,8%

2017 2011 2010 2012 2013 2014

Iron ore Pellets Slab Laminated steel

Mineral Production in Brazil [USD billions]

Source: IBRAM; Roland Berger

Example of Value chain – Iron Ore

New business opportunities for mining

companies

B. Industry 4.0 as a productivity lever

12 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Software

Computing Hardware > Data storage hardware > Embedded systems > High-performance computing > In-Memory computing > LCD / touch interfaces > Micro computing

> Real- time data processing > Business process software > Database management systems > Cloud computing > Real-time image processing (e.g. OCR) > Advanced algorithms > Machine learning

Interfaces

Production Hardware > Robotics > New joining technologies > Traditional Machinery > Automation equipment

> Visual sensors > RFID > Biometrics > Magnetic stripes > Camera & imaging systems > Semiconductor based sensors > Traditional sensors

Connec-tivity

> High speed mobile broadband (e.g. 3G / 4G) > Industrial Ethernet > Internet protocols (IPv6) > Local broadband (e.g. WIFI) > Short range/low power transmissions (e.g. Bluetooth, NFC)

Industry 4.0 integrates technologies leading to higher productivity and new possibilities

Base Technologies Potential solutions

Cyber world Physical world Self-reconfiguring machines

Logistics automation 4.0

Smart storage bin

Modularized production

Additive manufacturing

Self-diagnosing machines

Smart products

Unitary, RFID-based parts tracking

Autonomous vehicles

Smart environment recognition

Interactive robotics

Predictive Maintenance

Demand-response energy management systems

Predictive quality / Enhanced Throughput

Smart handbooks and process documentation

Virtual process optimization

User-friendly operations dashboards

Digital Prototyping

Mobile device based machine control

Demand driven provision of material and tools

Centralized machinery planning

Self-learning robots

Self-optimizing system

Cobotics Intelligent rush/new order management

Augmented Reality

Virtual work preparation Customer triggered lot-size 1 production

Source: Roland Berger

Industry 4.0 technologies and solutions

13 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

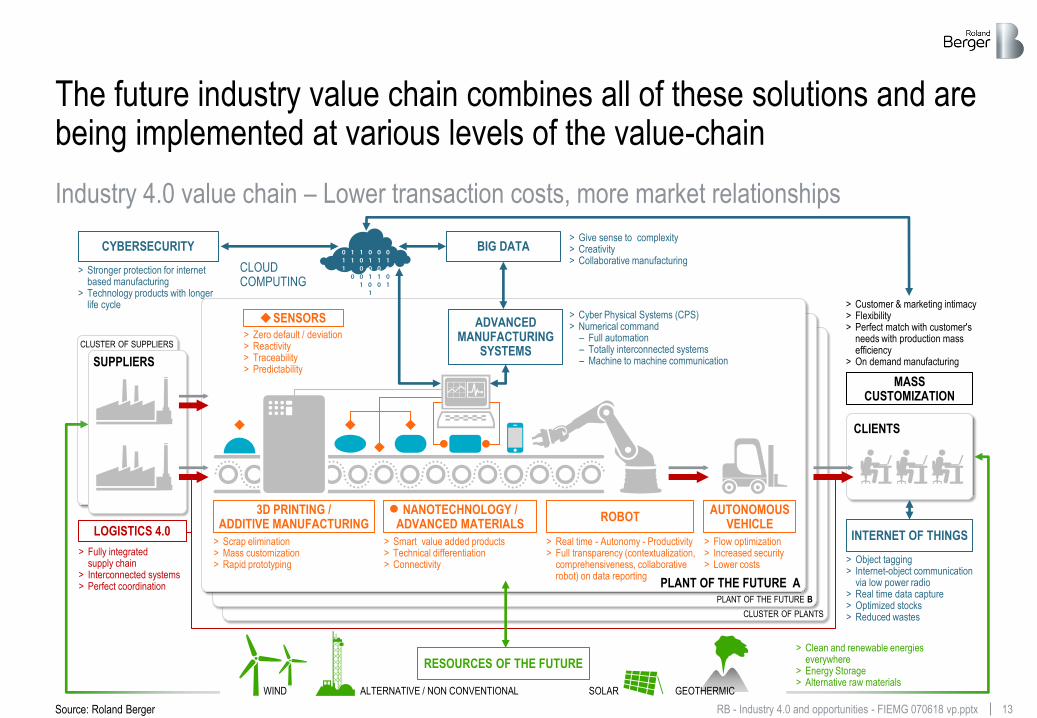

CLUSTER OF PLANTS

PLANT OF THE FUTURE B

CLIENTS

> Customer & marketing intimacy > Flexibility > Perfect match with customer's

needs with production mass efficiency

> On demand manufacturing

MASS CUSTOMIZATION

INTERNET OF THINGS

> Object tagging > Internet-object communication

via low power radio > Real time data capture > Optimized stocks > Reduced wastes

The future industry value chain combines all of these solutions and are being implemented at various levels of the value-chain

Industry 4.0 value chain – Lower transaction costs, more market relationships

PLANT OF THE FUTURE A

ROBOT

> Real time - Autonomy - Productivity > Full transparency (contextualization,

comprehensiveness, collaborative robot) on data reporting

> Cyber Physical Systems (CPS) > Numerical command

– Full automation – Totally interconnected systems – Machine to machine communication

ADVANCED MANUFACTURING

SYSTEMS

SENSORS

> Zero default / deviation > Reactivity > Traceability > Predictability

CLOUD COMPUTING

> Stronger protection for internet based manufacturing

> Technology products with longer life cycle

CYBERSECURITY > Give sense to complexity > Creativity > Collaborative manufacturing

BIG DATA

AUTONOMOUS VEHICLE

> Flow optimization > Increased security > Lower costs

3D PRINTING / ADDITIVE MANUFACTURING

NANOTECHNOLOGY / ADVANCED MATERIALS

> Scrap elimination > Mass customization > Rapid prototyping

> Smart value added products > Technical differentiation > Connectivity

CLUSTER OF SUPPLIERS

LOGISTICS 4.0

> Fully integrated supply chain

> Interconnected systems > Perfect coordination

SUPPLIERS

RESOURCES OF THE FUTURE

WIND ALTERNATIVE / NON CONVENTIONAL SOLAR GEOTHERMIC

> Clean and renewable energies everywhere

> Energy Storage > Alternative raw materials

Source: Roland Berger

14 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Schematic

The value chain from the mining industry, from the extraction until distribution offers numerous opportunities for digitalization

Production management and supply chain integration 3

Digitization of production equipment 2 Digital sales & distribution 4

Digital in Application Engineering 5

Process automation in indirect areas using AI based RPA

7 Digital culture and organization

> Autonomous intra-logistics

> Autonomous factories

> Conditional & predictive maintenance

> AI based optimization of power consumption

> Automated error processing using machine learning

> User friendly operations dashboards (e.g. error handling)

> Direct sales via online "shop"

> Real time order tracking

> Optimized stocks

> Pricing analytics

> Flexible order reprioritization

> Real–time tracking

> Robotic process automation of routine knowledge work such as invoicing or order processing

> Digital mindset

> Open and co-innovation

> Corporate venture capital approach

> Simulation of metallurgic properties

> Simulation of production processes

> Image recognition in quality control

Supported operators 8

De-salination plant

Customer

Distributor

Direct sales

Ore Logistics & warehouse

Outbound logistics

Transp.

Transp.

Transp.

Transp.

Power supplier

Platform

6

Mine

Refinery Refined ore

Smelter Casting Metal

Carbon plant

> Digital harbor logistics

Digitization clusters and potential initiatives along the value chain

Source: Roland Berger

Quality control 9

Mining efficiency 1

15 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Mining efficiency can be greatly increased with technologies such as vehicular automation, cameras and sensors

Use cases at a glance

Remote control center and Internet-of-Things sensors > Real time data is utilized to optimize mine and logistics scheduling, leading to smart decision

support

> Alerts of notifications of interruptions in any kind of device

> Employees can take immediate action and solve issues collaboratively, preventing failures and maximizing productivity

1 Mining efficiency

Source: Roland Berger

Vehicle automation > Autonomous trucks, drills, and trains are used for mining, reducing the need for employees

> This technology reduces the total FTE used to execute the mining operation

> These vehicles are also capable of harvesting ore from hard-to-reach places

Precision mining technology > High tech cameras are capable of detecting the best areas for ore extraction

> As a result there is considerable time saving when compared to traditional exploration

> Additionally, the quality of the harvested ore increases as cameras detect the best deposits

16 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

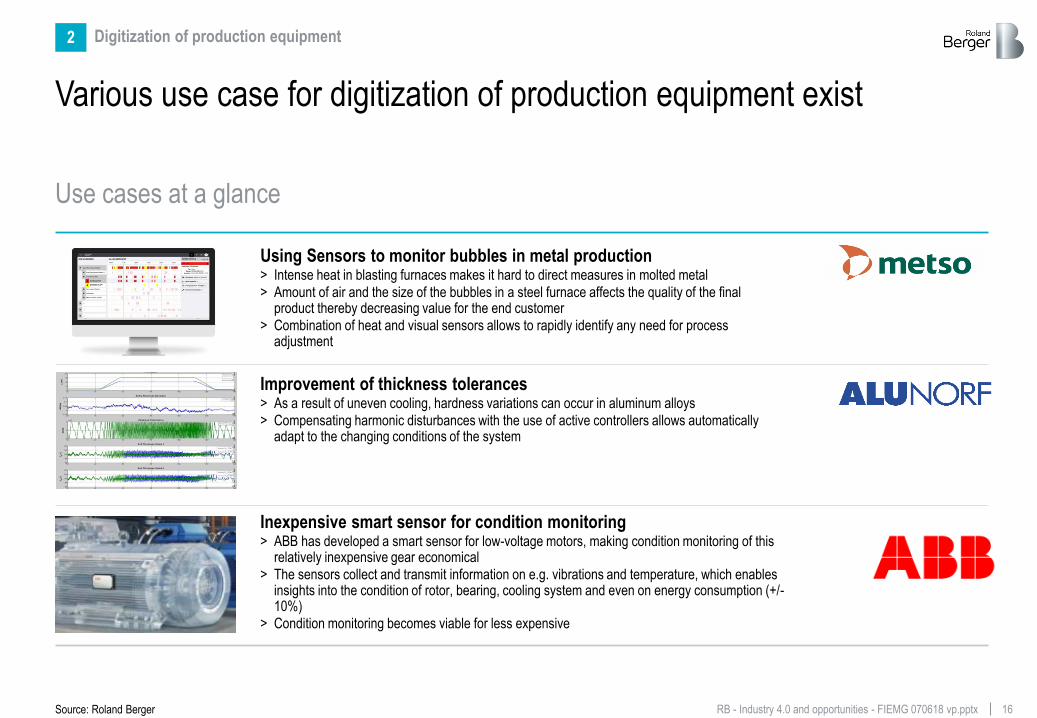

Various use case for digitization of production equipment exist

2 Digitization of production equipment

Using Sensors to monitor bubbles in metal production > Intense heat in blasting furnaces makes it hard to direct measures in molted metal

> Amount of air and the size of the bubbles in a steel furnace affects the quality of the final product thereby decreasing value for the end customer

> Combination of heat and visual sensors allows to rapidly identify any need for process adjustment

Improvement of thickness tolerances > As a result of uneven cooling, hardness variations can occur in aluminum alloys

> Compensating harmonic disturbances with the use of active controllers allows automatically adapt to the changing conditions of the system

Inexpensive smart sensor for condition monitoring > ABB has developed a smart sensor for low-voltage motors, making condition monitoring of this

relatively inexpensive gear economical

> The sensors collect and transmit information on e.g. vibrations and temperature, which enables insights into the condition of rotor, bearing, cooling system and even on energy consumption (+/- 10%)

> Condition monitoring becomes viable for less expensive

Source: Roland Berger

Use cases at a glance

17 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Various use case for digitization of production equipment exist

2 Digitization of production equipment

Additive Manufacturing to produce spare parts & tools on-site > Process of making physical objects from a digital CAD model using a printer

> Improved supply chain effectiveness leading to cost and time savings

> Instead of replacing a large section of the machine only the damaged connector that removes liquid mist from gas was milled off and replaced

> Less material and time required for repair (60 hours to print the connector in Amsterdam)

Big data analytics tool for predictive maintenance and cost savings > Ready-to-use big data analytics tool that integrates with existing process historian

> Makes use of collected process and systems data to visualize patterns, trends and interrelations

> 75% elimination of breakdowns by energy companies that have implemented predictive maintenance programs and 50% maintenance cost savings possible

Source: Roland Berger

Use cases at a glance

Smart corrosion sensors > Smart ultrasonic corrosion and temperature sensors can deliver real time wall thickness and temperature

measurements to a centralized monitoring platform

> Sensors wired to range extender antennas can be tracked from distances of up to 40 km

> Low necessary sampling rate of two measurements per day enables operation for years without need for battery change

> Variety of other examples for smart sensors including wear monitoring of pumps, leak sensors etc.

18 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Some players have digitalized the supply chain to optimize output and/or margins

Use cases at a glance

Source: Roland Berger

Production management and supply chain integration & Digital sales & distribution 4 3

Information exchange between supplier and customer on plant system > Thyssenkrupp's steel mill Hoesch Hohenlimburg leverages digitization to improve output

> Suppliers and customers are integrated into the plant's IT systems to enable the exchange of information on orders, logistics and production processes

> Customers can easily adjust their orders short notice

> A 30% output increase was realized within two years – Ongoing efficiency improvements expected to provide further double-digit productivity gains

Online platform for steel purchasing and studies > Online platform for industrial steel purchasing through bundling of steel traders; integration into IT

systems possible

> Comparison of offers, prices and delivery times

> Publishing of studies and online blogging on steel trading and Industry 4.0 topics

Implementation of Revenue Management to increase margin > VDM Metals supplies high-performance nickel alloys, cobalt alloys, and stainless-steel products

> VDM Metals' business is ~100% Make-to-Order (MTO) – The process is a combination of process and discrete production, with sheet finishing as the key bottleneck

> VDM Metals chose to implement Revenue Management (RM) on its sheet business

> Improvement of order acceptance decisions and increase of overall contributive margin (+13%)

20 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Robotic process automation (RPA) and artificial intelligence (AI) play a major role in the automation of indirect areas

Confidential

Source: Roland Berger

Use cases at a glance

6 Process automation in indirect areas

Encourage involvement of business users using BRM > Business Rules Management (BRM) software provides the ability for non-technical business

users to get involved directly in business rules management, leading to flexible decision automation for applications which are subject to complex and evolving business rules

> Easy accommodation of future changes to production requirements (production method, special treatments, special conditions to be respected, etc.)

Artificial Intelligence bot to take care of customer service > Amelia is an artificial intelligence solution used in call centers

> She understands written and spoken language including contextual information, she is able to understand the user's mood and learns from live interactions

> In an IT service desk, Amelia learned to take 64% of the incoming calls through observational learning, reducing staffing requirements by half and increasing meant time to resolve an issue to less than one third

Automation of reporting process using RPA > Reporting process of a client involved mostly manual interventions performed by personnel

> In a digital project, a pilot was launched to automate reporting process via RPA, i.e. replacing manual interventions with robotic interventions

> As a result, cost savings realized (80% of process automated) and quality, e.g. on-time delivery, improved

22 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

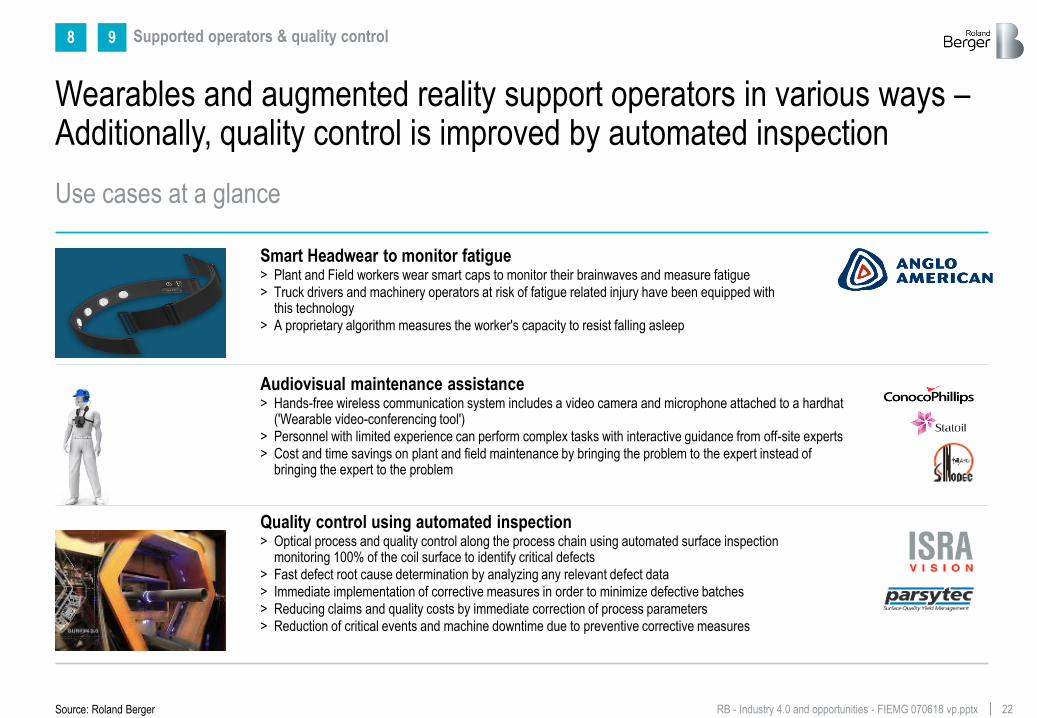

Wearables and augmented reality support operators in various ways – Additionally, quality control is improved by automated inspection

8

Use cases at a glance

Source: Roland Berger

Supported operators & quality control 9

Smart Headwear to monitor fatigue > Plant and Field workers wear smart caps to monitor their brainwaves and measure fatigue

> Truck drivers and machinery operators at risk of fatigue related injury have been equipped with this technology

> A proprietary algorithm measures the worker's capacity to resist falling asleep

Quality control using automated inspection > Optical process and quality control along the process chain using automated surface inspection

monitoring 100% of the coil surface to identify critical defects

> Fast defect root cause determination by analyzing any relevant defect data

> Immediate implementation of corrective measures in order to minimize defective batches

> Reducing claims and quality costs by immediate correction of process parameters

> Reduction of critical events and machine downtime due to preventive corrective measures

Audiovisual maintenance assistance > Hands-free wireless communication system includes a video camera and microphone attached to a hardhat

('Wearable video-conferencing tool')

> Personnel with limited experience can perform complex tasks with interactive guidance from off-site experts

> Cost and time savings on plant and field maintenance by bringing the problem to the expert instead of bringing the expert to the problem

C. Business opportunities for Minas Gerais due to technological advancements

24 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

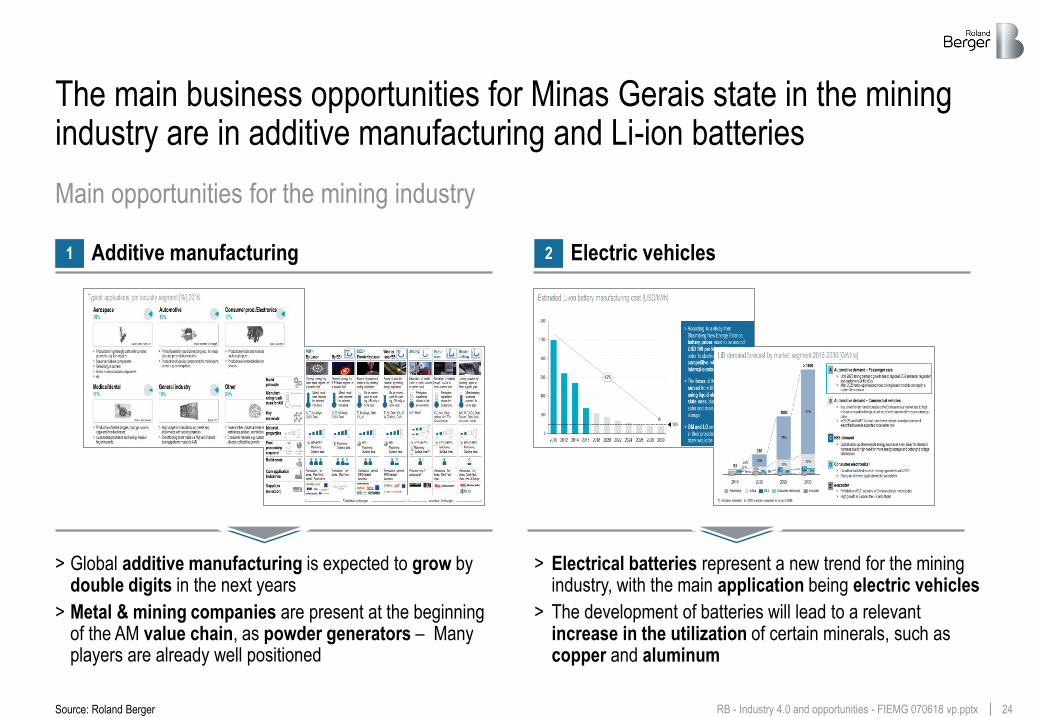

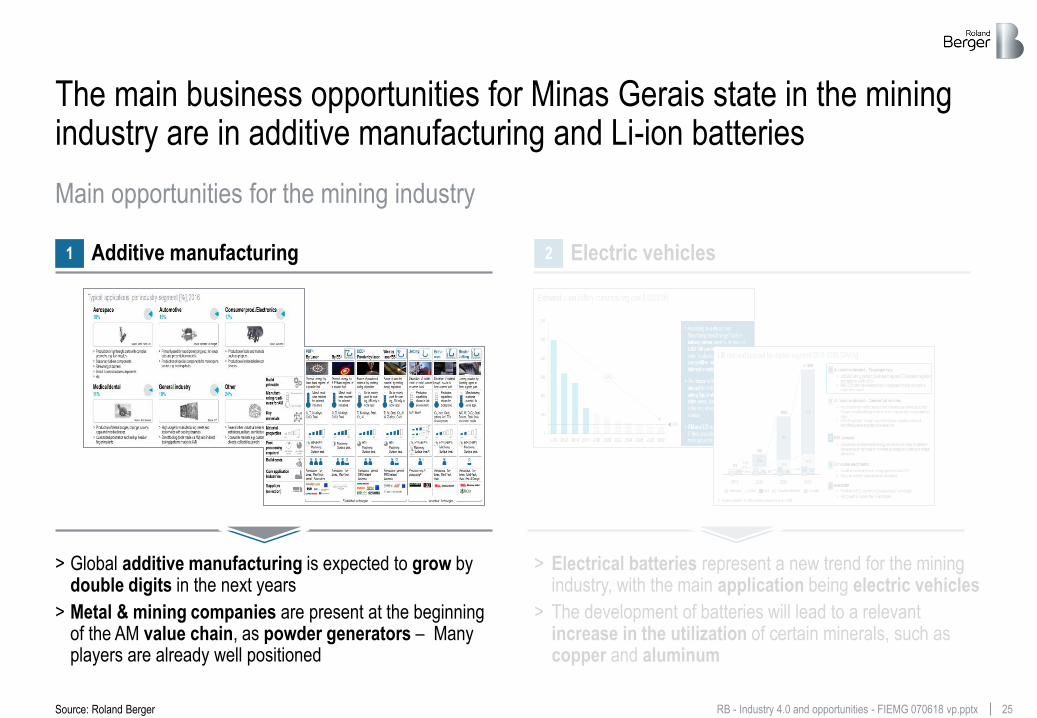

The main business opportunities for Minas Gerais state in the mining industry are in additive manufacturing and Li-ion batteries

Main opportunities for the mining industry

Source: Roland Berger

> Global additive manufacturing is expected to grow by double digits in the next years

> Metal & mining companies are present at the beginning of the AM value chain, as powder generators – Many players are already well positioned

Additive manufacturing 1 Electric vehicles 2

> Electrical batteries represent a new trend for the mining industry, with the main application being electric vehicles

> The development of batteries will lead to a relevant increase in the utilization of certain minerals, such as copper and aluminum

25 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

The main business opportunities for Minas Gerais state in the mining industry are in additive manufacturing and Li-ion batteries

Main opportunities for the mining industry

Source: Roland Berger

> Global additive manufacturing is expected to grow by double digits in the next years

> Metal & mining companies are present at the beginning of the AM value chain, as powder generators – Many players are already well positioned

Additive manufacturing 1 Electric vehicles 2

> Electrical batteries represent a new trend for the mining industry, with the main application being electric vehicles

> The development of batteries will lead to a relevant increase in the utilization of certain minerals, such as copper and aluminum

26 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Using additive manufacturing technology, three-dimensional solid objects of virtually any shape can be made from a digital model

> Additive manufacturing (AM) is a process of

making a three-dimensional solid object

of virtually any shape from a digital model

> AM uses an additive process, where

materials are applied in successive layers

> AM is distinguished from traditional

subtractive machining techniques that rely

on the removal of material by methods such

as cutting or milling

> The capacity to make metal objects

relevant to the engineered products and high

tech industries has been around since 1995

Additive manufacturing 1

Definition

Source: Direct Manufacturing Research Center (DMRC); Roland Berger

27 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

AM is an industry that can serve various applications, from Aerospace and Medical devices to the Automotive industry

Typical applications per industry segment [%], 2016

Source: Rennteam Uni Stuttgart Source: Morris Techn. Inc.

Source: CPM Source: FIT Source: SLM Solutions

Source: Kuhn-Stoff

> Production of tools and manufacturing equipment such as grippers

> Production of embedded electronics, e.g. RFID devices

> Primarily used for rapid prototyping esp. for visual aids and presentation models

> Production of special components for motorsports sector, e.g. cooling ducts

> Production of lightweight parts with complex geometry, e.g. fuel nozzles

> Stationary turbine components > Reworking of burners

> Small Ti aerostructure components > etc

Other 24%

> Several other industrial areas such as academic institutions, military, architectural, oil & gas, space

> Consumer markets, e.g. customized design objects, collectibles, jewelry

General industry 19%

> High usage for manufacturing inserts and tools/molds with cooling channels

> Direct tooling (tools made via AM) and indirect tooling (patterns made via AM)

Medical/dental 11%

> Production of dental bridges, copings, crowns, caps and invisible braces

> Customized prosthetics such as hip, head or finger implants

Consumer prod./Electronics 17%

Automotive 15%

Aerospace 18%

Additive manufacturing 1

Source: Wohlers; interviews with market participants; Roland Berger

28 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

There are various technologies available, with different maturity levels and various metals used

1) Powder Bed Fusion 2) Electron Beam 3) Direct Energy Deposition 4) Heat treatment 5) Hot isostatic pressing 6) might not be needed for X-Jet process 7) Cost effectiveness potential by claim, so far no proof in industrial context 8) VADER process (Magnetojetting) 9) X-jet process (Nanoparticle Jetting)

Manufact-uring readi-ness for AM

Key materials

Post processing required

Build costs

Core application Industries

Suppliers (selection)

High degree required

Material properties

Low degree required

Low High

Full rate production

Proof of concept

Build principle

HT4)/HIP5) Machining Surface treat.

Al, Ti, Ni-alloys, CoCr, Steel

Aerospace, Tur-bines, Med-Tech, dental, Automotive

Machining Surface treat.

Al, Ti, Ni-alloys, CoCr, Steel

Ti, Ni-alloys, Steel, Co, Al

HT4) Machining Surface treat.

Ti, Ni, Steel, Co, Al, W, Zr-alloy, CuNi

AL8), Steel9)

HT4) (/HIP5)) Machining Surface treat.

Cu, Inco, Steel, (others incl. Ti in development)

HT4) (/HIP5)) Machining Surface treat.

WC, W, CoCr, Steel/ Bronze, Steel, Inco, non-metal molds

Low High

X-Jet

Manuf. readi-ness reached for selected industries

Aerospace, Tur-bines, Med-Tech

Aerospace, general MRO related business

Aerospace, general MRO related business

Precision eng.9), prototyping8)

Aerospace, Tur-bines, Med-Tech, Auto

Aerospace, Tur-bines, Med-Tech, Auto, Arts & Design

HT4) (/HIP5))

Machining Surface treat.6)

7)

HT4) Machining Surface treat.

Vader

9)

8)

Low Low High Low Low Low Low High High High High High

Manuf. readi-ness reached for selected industries

So far mainly used for coat-ing, AM only in niche appl.

So far mainly used for coat-ing, AM only in niche appl.

Production capabilities shown in lab-environment

Production capabilities shown for prototyping

Manufacturing readiness reached for niche appl.

Thermal energy by laser fuses regions of a powder bed

Thermal energy by EB2) fuses regions of a powder bed

Fusion of powdered material by melting during deposition

Fusion of wire fed material by melting during deposition

Deposition of molten metal or metal powder in carrier liquid

Dispense of material through nozzle to form a green part

Joining powder by bonding agent to form a green part

Established technologies Incumbent technologies

Additive manufacturing 1

Source: Company information; Expert interviews; Roland Berger

Binder Jetting

Extru- sion

PBF1) DED3)

By Laser By EB2) Powder by laser Wire by laser/EB

Jetting

29 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

The market is still under development and there are various players establishing themselves

Powder generation

Engineering (Software) Production (Hardware)

CAD Optimization Preparation Additive Manufact.

Tempering Metal cutting Quality control

1)

Support structure1)

Surface treatment

Additive manufacturing 1

AM Value Chain (generic)

1) Removing support structure: Mostly manually as of today, atomization concepts in development

Source: Roland Berger

30 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

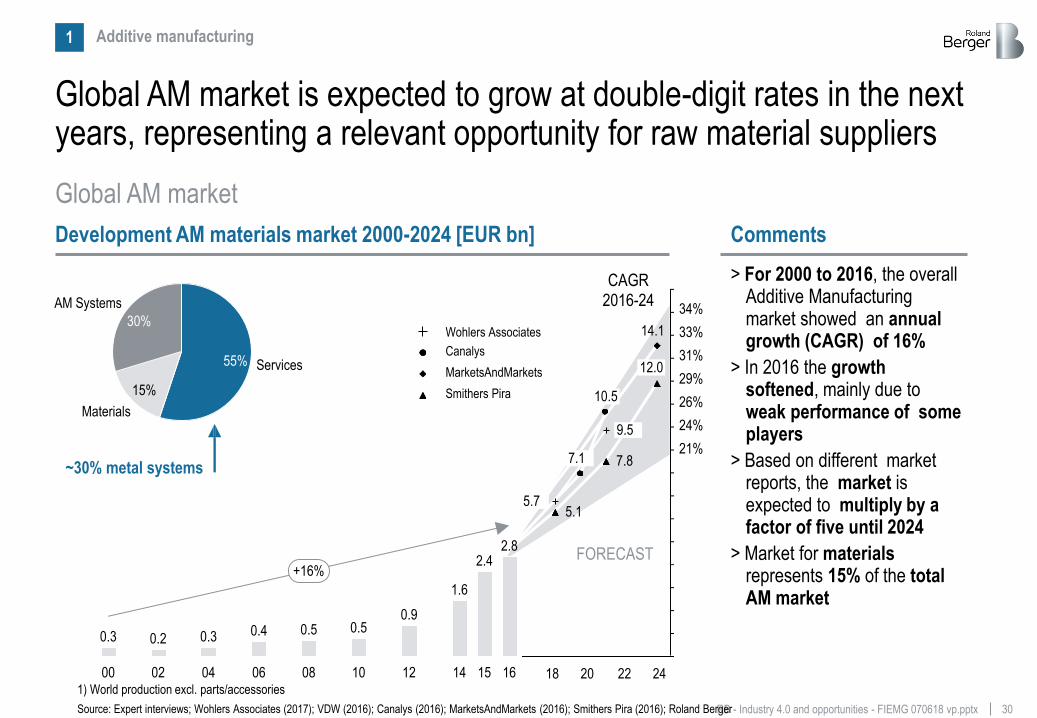

Global AM market is expected to grow at double-digit rates in the next years, representing a relevant opportunity for raw material suppliers

Global AM market

Source: Expert interviews; Wohlers Associates (2017); VDW (2016); Canalys (2016); MarketsAndMarkets (2016); Smithers Pira (2016); Roland Berger

1) World production excl. parts/accessories

> For 2000 to 2016, the overall Additive Manufacturing market showed an annual growth (CAGR) of 16%

> In 2016 the growth softened, mainly due to weak performance of some players

> Based on different market reports, the market is expected to multiply by a factor of five until 2024

> Market for materials represents 15% of the total AM market

Comments Development AM materials market 2000-2024 [EUR bn]

FORECAST

5.7 5.1

7.1 7.8

10.5

12.0

9.5

Wohlers Associates

Canalys

MarketsAndMarkets

Smithers Pira

CAGR 2016-24

Additive manufacturing 1

Services

15%

55%

Materials

30%

AM Systems

18 20 22 24

34%

33%

31%

29%

26%

24%

21%

14.1

14 00 12 10

0.3

06

0.5

2.4

04

+16%

0.4 0.3 0.5

2.8

08 16

0.2

02

0.9

1.6

15

~30% metal systems

31 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

The main business opportunities for Minas Gerais state in the mining industry are in additive manufacturing and Li-ion batteries

Main opportunities for the mining industry

Source: Roland Berger

> Global additive manufacturing is expected to grow by double digits in the next years

> Metal & mining companies are present at the beginning of the AM value chain, as powder generators – Many players are already well positioned

Additive manufacturing 1 Electric vehicles 2

> Electrical batteries represent a new trend for the mining industry, with the main application being electric vehicles

> The development of batteries will lead to a relevant increase in the utilization of certain minerals, such as copper and aluminum

32 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

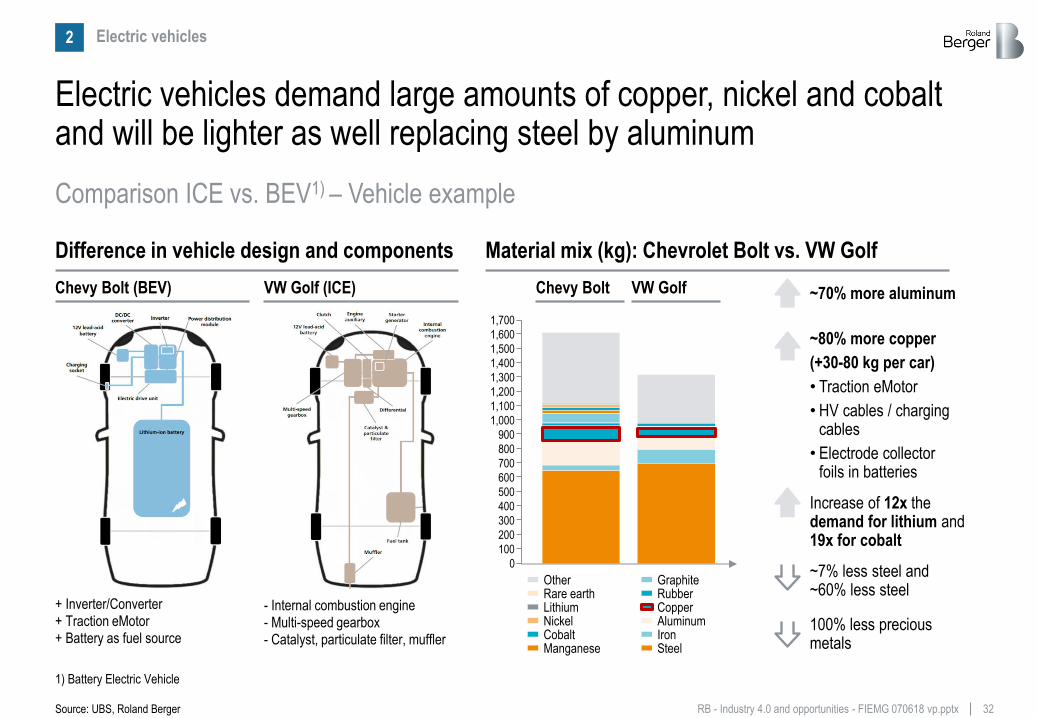

Electric vehicles demand large amounts of copper, nickel and cobalt and will be lighter as well replacing steel by aluminum

Source: UBS, Roland Berger

Comparison ICE vs. BEV1) – Vehicle example

1) Battery Electric Vehicle

Other Rare earth Lithium Nickel Cobalt Manganese

Graphite Rubber Copper Aluminum Iron Steel

1,700

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

+ Inverter/Converter + Traction eMotor + Battery as fuel source

- Internal combustion engine - Multi-speed gearbox - Catalyst, particulate filter, muffler

Material mix (kg): Chevrolet Bolt vs. VW Golf Difference in vehicle design and components

Chevy Bolt (BEV) VW Golf (ICE) Chevy Bolt VW Golf

~7% less steel and ~60% less steel

100% less precious metals

~70% more aluminum

~80% more copper

(+30-80 kg per car)

• Traction eMotor

• HV cables / charging cables

• Electrode collector foils in batteries

Increase of 12x the demand for lithium and 19x for cobalt

Electric vehicles 2

33 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx Source: Roland Berger

Legislative actions and customer pull drive the xEV-market growth, but are constrained by some factors such as availability of raw materials

Overview of key triggers and challenges for the xEV market (status quo)

Expected market

develop- ment for EVs and PHEVs Stake-

holders

Market triggers1) Market challenges

Customer

Prices too high vs ICE and offer still limited

Infrastructure

Auto-Industry / Politics

Local employment dependent on traditional

ICE technologies

Resource Push

End Customer

Making EVs and PHEVs attractive for end customers by fulfilling customer needs for…

CO2

NO x

CO2 and toxic emission regulations

OEMs

Forcing OEMs to supply a significant number of EVs and PHEVs with…

§

> (City) access limitations (e.g. London, Paris)

> ICE registration bans (e.g. Norway, Netherlands)

1) Both dimensions exist in all three regions, however, with different emphasis; 2) Push is dominating factor in CARB Section 177 States;

Pull2)

Technology

and re-

sources Lack of grids,

charging poles

Lack of rare resources

& production capacities

Electric vehicles 2

34 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

0

200

400

600

800

1.000

1.200

2028

-12%

2012 2014 2010 2016 2024 2018 2026

100

2030 2020 2022

Source: Energy Storage World Forum; Bloomberg New Energy Finance; Roland Berger

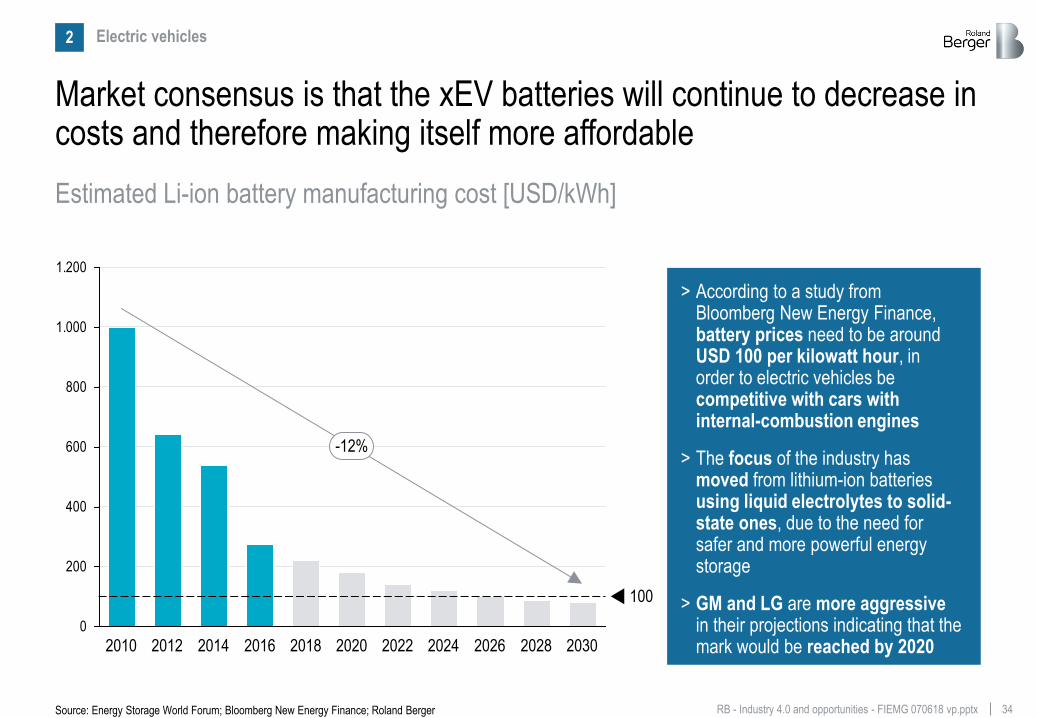

Market consensus is that the xEV batteries will continue to decrease in costs and therefore making itself more affordable

Estimated Li-ion battery manufacturing cost [USD/kWh]

> According to a study from Bloomberg New Energy Finance, battery prices need to be around USD 100 per kilowatt hour, in order to electric vehicles be competitive with cars with internal-combustion engines

> The focus of the industry has moved from lithium-ion batteries using liquid electrolytes to solid-state ones, due to the need for safer and more powerful energy storage

> GM and LG are more aggressive in their projections indicating that the mark would be reached by 2020

Electric vehicles 2

35 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

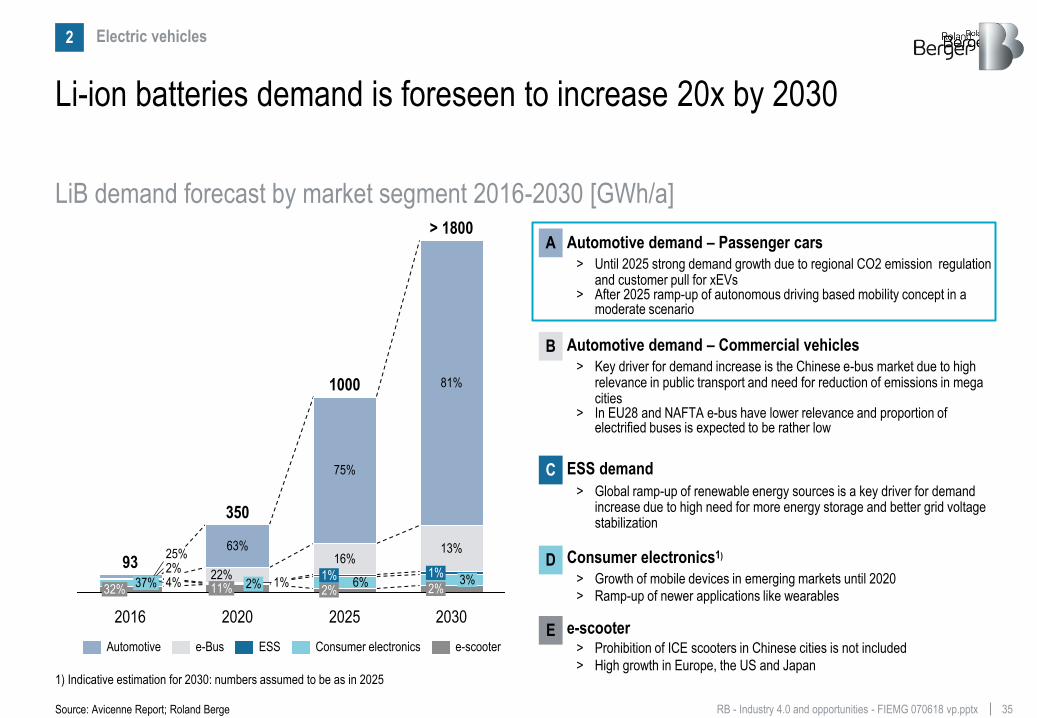

Li-ion batteries demand is foreseen to increase 20x by 2030

Automotive demand – Passenger cars

> Until 2025 strong demand growth due to regional CO2 emission regulation and customer pull for xEVs

> After 2025 ramp-up of autonomous driving based mobility concept in a moderate scenario

A

Automotive demand – Commercial vehicles

> Key driver for demand increase is the Chinese e-bus market due to high relevance in public transport and need for reduction of emissions in mega cities

> In EU28 and NAFTA e-bus have lower relevance and proportion of electrified buses is expected to be rather low

B

ESS demand

> Global ramp-up of renewable energy sources is a key driver for demand increase due to high need for more energy storage and better grid voltage stabilization

C

Consumer electronics1)

> Growth of mobile devices in emerging markets until 2020

> Ramp-up of newer applications like wearables

D

e-scooter > Prohibition of ICE scooters in Chinese cities is not included

> High growth in Europe, the US and Japan

E

LiB demand forecast by market segment 2016-2030 [GWh/a]

2030

> 1800

25%

350

11% 2% 1% 22%

63%

2016

93

32% 37% 4%

2%

2% 3%

1%

13%

81%

2025

1000

2% 6%

1%

16%

75%

2020

e-scooter Consumer electronics Automotive e-Bus ESS

Source: Avicenne Report; Roland Berge

1) Indicative estimation for 2030: numbers assumed to be as in 2025

Electric vehicles 2

36 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

The relevance of metals will change due to the demand for EV batteries, so some companies will have to adapt their current strategy

Projections for key metals in EV batteries (thousand metric tons)

Source: Bloomberg New Energy Finance; Roland Berger

> With the adoption of electric vehicles, there will be a huge increase in demand for metals such as Lithium, Manganese, Cobalt, Copper, Aluminum and Nickel

> Mining companies focused on iron will have to diversify their production, or they will face an increasingly difficult competitive situation

0 50 100 150 200 250 300 350

Lithium

Manganese

Cobalt

Copper

Aluminum

Nickel

12x

19x

24x

27x

31x

32x

2016 2030 2020 2025

Electric vehicles 2

D. What this means to the industries in Minas Gerais and how we can help

38 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

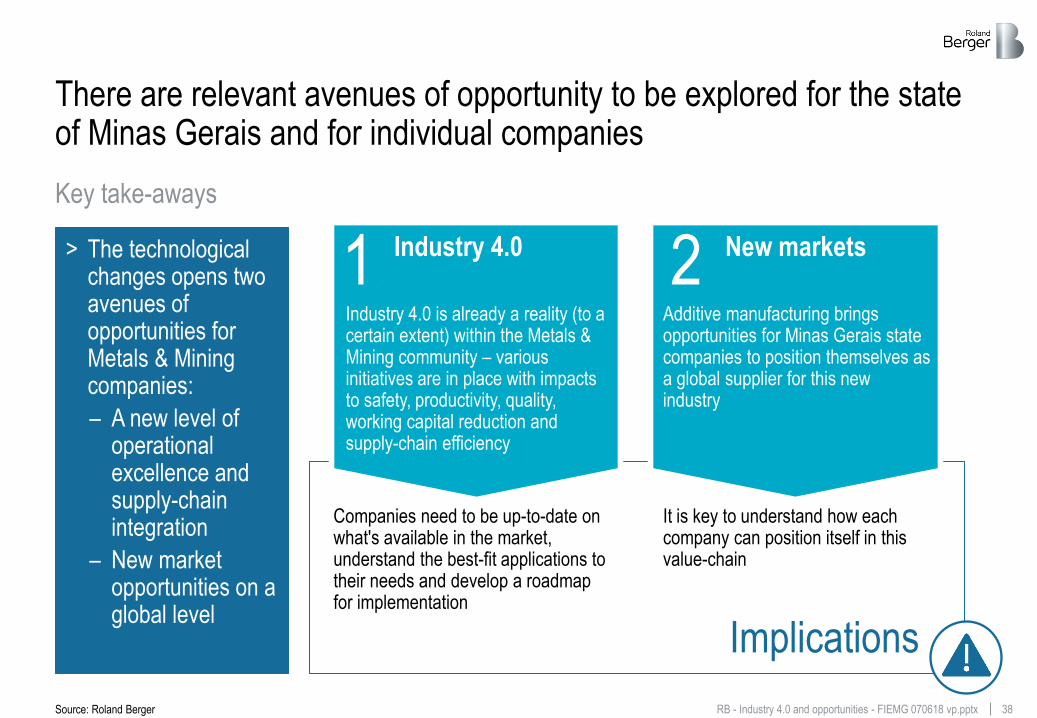

There are relevant avenues of opportunity to be explored for the state of Minas Gerais and for individual companies

Key take-aways

> The technological changes opens two avenues of opportunities for Metals & Mining companies:

– A new level of operational excellence and supply-chain integration

– New market opportunities on a global level

Source: Roland Berger

Implications

Industry 4.0 1 Industry 4.0 is already a reality (to a certain extent) within the Metals & Mining community – various initiatives are in place with impacts to safety, productivity, quality, working capital reduction and supply-chain efficiency

It is key to understand how each company can position itself in this value-chain

Companies need to be up-to-date on what's available in the market, understand the best-fit applications to their needs and develop a roadmap for implementation

2 New markets

Additive manufacturing brings opportunities for Minas Gerais state companies to position themselves as a global supplier for this new industry

39 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

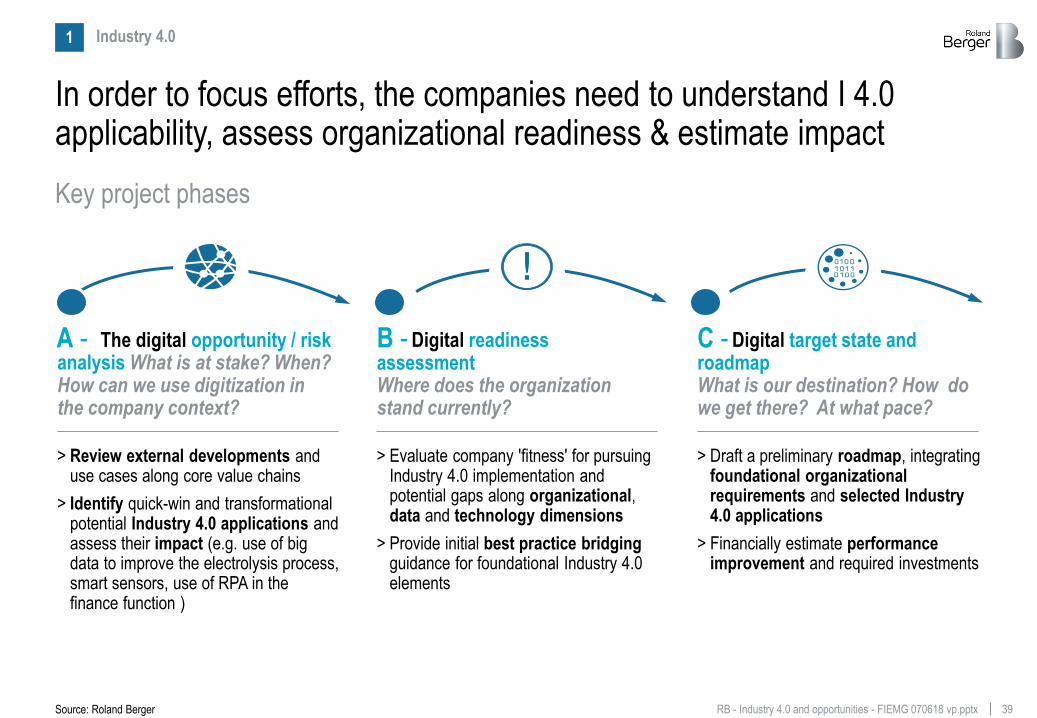

In order to focus efforts, the companies need to understand I 4.0 applicability, assess organizational readiness & estimate impact

Digital target state and roadmap What is our destination? How do we get there? At what pace?

Digital readiness assessment Where does the organization stand currently?

> Evaluate company 'fitness' for pursuing Industry 4.0 implementation and potential gaps along organizational, data and technology dimensions

> Provide initial best practice bridging guidance for foundational Industry 4.0 elements

The digital opportunity / risk analysis What is at stake? When? How can we use digitization in the company context?

> Review external developments and use cases along core value chains

> Identify quick-win and transformational potential Industry 4.0 applications and assess their impact (e.g. use of big data to improve the electrolysis process, smart sensors, use of RPA in the finance function )

> Draft a preliminary roadmap, integrating foundational organizational requirements and selected Industry 4.0 applications

> Financially estimate performance improvement and required investments

A - B - C -

Key project phases

Source: Roland Berger

Industry 4.0 1

40 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Two parallel streams could allow to build an integrated transformation roadmap and estimate financial impact

Industry 4.0 tools selection, prioritization & modelling A -

Industry 4.0 Readiness Assessment B -

Integrated 4.0 tools and organizational requirements transformation roadmap

Financial uplift estimations and associated required investments

Final outputs

Diagnose gaps across organizational, data and technology dimensions

Identify key principles required to bridge major deficits

Define a minimum 'Industry 4.0-viability' threshold along selected dimensions

Design minimum target state and foundational requirements roadmap

Understand activity /value chains and Industry 4.0 ‘hot spots'

Enrich list of potential Industry 4.0 tools that could be used

Prioritize tools based on needs, implementation ease and benefits

Deep-dive on MVP, risks and potential impact for each app

C -

Two parallel streams form the basis for the integrated roadmap

Source: Roland Berger

Industry 4.0 1

41 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

A successful digitalization of mine operations is expected to generate ~15%-20% of gains on overall cost base

> Remote excellence & operations centers with access

to real-time data to operate the mine and define

operational improvements

> Day planning based on 3D display, data analytics

> Predictive maintenance reducing unexpected failures

> On-site spare part replacement

Main Applications

> Autonomous Fleet Management System operating

drillers, shovels, haulers

> Workers equipped with mobile diagnosis tools, FitBit

health systems and receiving personalized tasks

> Real-time geo-tracking of resources

> Mine environment, health, load… monitoring with smart

sensors to detect anomalies and reduce incidents

> Optimized mineral recovery process (e.g. Oxygen

flow optimization in gold leaching process)

> Process flow optimization

Plan & optimize

Maintain

Operate

Monitor

Process

Explore & build > Optimized construction plans leveraging 3D

modelling systems

> Mine configuration simulations for optimal mineral recovery

Share of overall cost impact

Limited share of overall gains High share of overall gains Source: Roland Berger

Industry 4.0 1

42 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

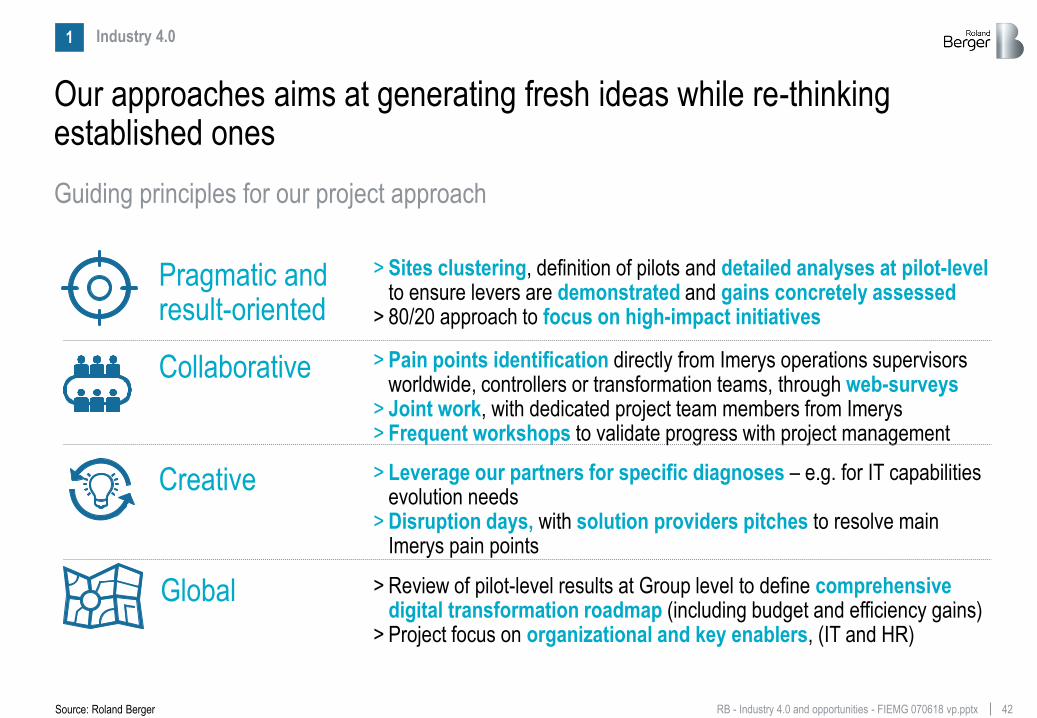

Our approaches aims at generating fresh ideas while re-thinking established ones

Pragmatic and result-oriented

> Sites clustering, definition of pilots and detailed analyses at pilot-level to ensure levers are demonstrated and gains concretely assessed

> 80/20 approach to focus on high-impact initiatives

Collaborative > Pain points identification directly from Imerys operations supervisors worldwide, controllers or transformation teams, through web-surveys

> Joint work, with dedicated project team members from Imerys > Frequent workshops to validate progress with project management

Creative > Leverage our partners for specific diagnoses – e.g. for IT capabilities evolution needs

> Disruption days, with solution providers pitches to resolve main Imerys pain points

Global > Review of pilot-level results at Group level to define comprehensive digital transformation roadmap (including budget and efficiency gains)

> Project focus on organizational and key enablers, (IT and HR)

Guiding principles for our project approach

Source: Roland Berger

Industry 4.0 1

43 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

Our approach is designed to go beyond the conventional and to explore transformational growth opportunities

Cluster opportunities for growth & filter to short list

Assess attractiveness, fit, risk & feasibility of shortlisted opportunities

Synthesize the new opportunities into themes

> Outline a roadmap with strategic options

> Identify potential targets

> Establish PMO

> Help understand trends & their implications

> Facilitate ideation of growth opportunities

> Investigate competitive dynamics & market conduct

> Analyze core business under scenarios

Current portfolio evaluation

New growth areas > Establish guiding

principles for growth

> Define your Business Essence1)

Internal

External

Establishing the baseline

1 Opportunity filtering

2 Deep-dive assessment

3 Strategic direction

4 Execution planning

5

Determine the strategic direction of the company

Evaluate endgame strategies for current businesses (e.g., divest, consolidate, defend niche, harvest)

Source: Roland Berger

Roland Berger approach to transformational portfolio strategy

New markets 2

44 RB - Industry 4.0 and opportunities - FIEMG 070618 vp.pptx

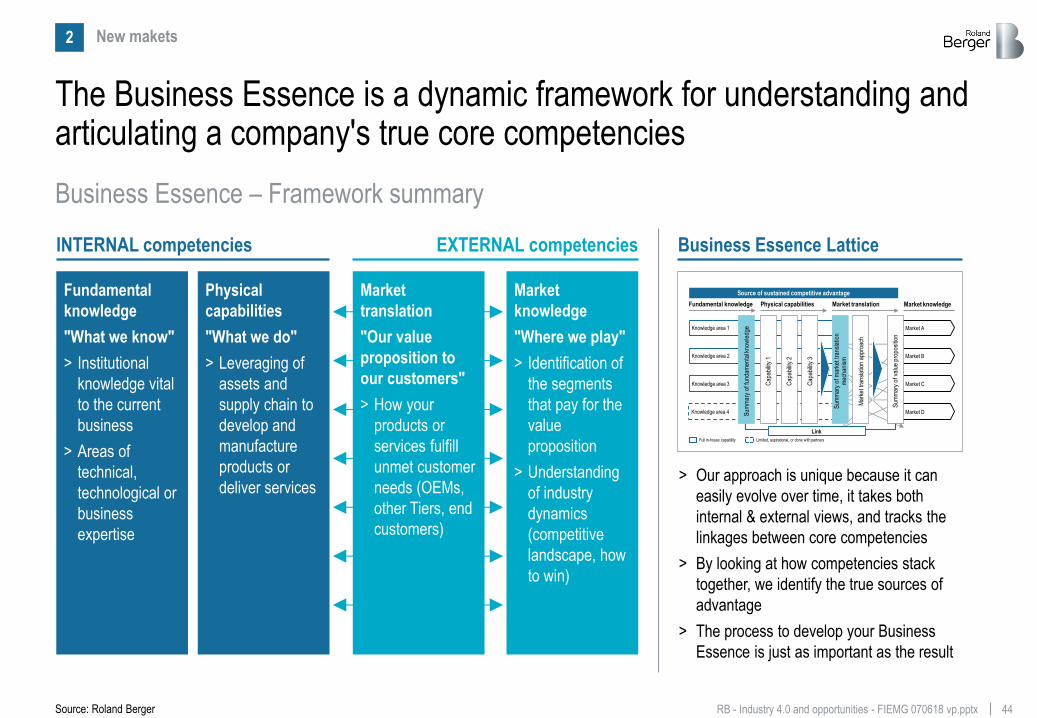

The Business Essence is a dynamic framework for understanding and articulating a company's true core competencies

> Our approach is unique because it can

easily evolve over time, it takes both

internal & external views, and tracks the

linkages between core competencies

> By looking at how competencies stack

together, we identify the true sources of

advantage

> The process to develop your Business

Essence is just as important as the result

INTERNAL competencies EXTERNAL competencies

Fundamental

knowledge

"What we know"

> Institutional

knowledge vital

to the current

business

> Areas of

technical,

technological or

business

expertise

Physical

capabilities

"What we do"

> Leveraging of

assets and

supply chain to

develop and

manufacture

products or

deliver services

Market

translation

"Our value

proposition to

our customers"

> How your

products or

services fulfill

unmet customer

needs (OEMs,

other Tiers, end

customers)

Market

knowledge

"Where we play"

> Identification of

the segments

that pay for the

value

proposition

> Understanding

of industry

dynamics

(competitive

landscape, how

to win)

Knowledge area 1

Knowledge area 2

Knowledge area 3

Knowledge area 4

Market A

Market B

Market C

Market D

Full in-house capability Limited, aspirational, or done with partners

Ca

pa

bili

ty 1

Ca

pa

bili

ty 3

Ca

pa

bili

ty 2

Fundamental knowledge Physical capabilities Market translation Market knowledge

Source of sustained competitive advantage

Link

Su

mm

ary

of

valu

e p

rop

osi

tion

Su

mm

ary

of

ma

rke

t tr

an

sla

tion

m

ech

an

ism

Ma

rke

t tr

an

sla

tion

ap

pro

ach

Su

mm

ary

of

fun

da

me

nta

l kn

ow

led

ge

Business Essence Lattice

Source: Roland Berger

Business Essence – Framework summary

New makets 2