inflation insight_oct 2011

TRANSCRIPT

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 1/9

October 2011

Analytical contact

Dharmakirti Joshi - Chief Economist

Vidya Mahambare - Senior Economist

Dipti Saletore - Economist

Economy Insights

u M a n u f a c t r i n g

I N F LA T I O N INFLATION

F o o d

e Fu l

R a t e

h i k e

Persistent inflation makes rate hike imperative

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 2/9

Persistent inflation makes rate hike imperativeBy CRISIL Centre for Economic Research (C-CER)

C-CER Team

Dharmakirti Joshi Chief Economist

Vidya Mahambare Senior Economist

Dipti Saletore Economist

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 3/9

1

Persistent inflation makes rate hike imperative

Key Points

• The persistent nature of inflation, we believe, makes another repo rate hike imperative if inflation is to be

brought down to around 5 per cent and maintained at around that level.

• As of September 2011, inflation, as measured by changes in the wholesale price index, has stayed above 9 per

cent for the past 20 months1; above 8 per cent for 28 months and above the RBI’s comfort zone of 5 per cent,

for 48 out of 66 months since April 2006.

• While monetary policy can lower inflation and its expectations, the short term trade-off between growth and

inflation will continue to rise, unless the supply potential of the economy is raised and wages and income

transfers are linked to productivity.

• Persistent and stubborn inflation India in recent years is largely due to near simultaneous occurrence of shocks, many of which are linked to the fiscal policy, and have tended to be permanent in nature.

Policy coordination is critical for achieving low inflation

• The Reserve Bank of India (RBI) is responsible for maintaining low and stable inflation. It does so by

bringing down demand for goods and services, in line with supply. Fiscal policy can support the objective of

low inflation, either by expanding supply potential and/or by not creating excessive upward pressure on

demand. However, an expansionary fiscal policy which contradicts the monetary policy actions by raising

overall demand without sufficiently increasing supply potential of the economy defeats the objective of

inflation control.

• This phenomenon has been experienced in India in recent years. Sustained fiscal push in terms of a near

simultaneous increase in wages and income transfers across most income groups, and not linked to

productivity, has kept demand persistently surging ahead of supply. This has constantly raised inflation and

inflation expectations, leading to higher demand for wages, in turn bringing persistence to inflation. In this

situation, monetary policy cannot maintain low and stable inflation, without a sledgehammer of high interest

rates and credit squeeze, to bring down demand sharply.

• To lower inflation and maintain high growth rates, government policy must simultaneously work towards

expanding the supply potential of the economy, which could complement the central bank’s efforts to contain

excess demand and inflation.

Inflation and inflationary expectations have become persistent

• Inflation, as measured by the annual change in the wholesale price index, is not just high, but has become

more persistent in nature in the past 5 years. Inflation has, since April 2006, remained higher than Reserve

Bank of India’s comfort level of inflation at about 5 per cent. In the 66 months beginning April 2006 to

September 2011, WPI inflation has remained -

o above 5 per cent in 48 months,

o above 6 per cent in 44 months,

o above 7 per cent in 34 months and

o above 8 per cent in 28 months

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 4/9

2

• In fact, inflation has remained for above 9 per cent in the last 20 months1. Even core inflation (non-food

manufacturing inflation, which indicates demand side pressures) has remained at or above 5 per cent in 5 out

of last 7 years (See Table 1), much above RBI’s threshold level. This has in turn fuelled expectations that

inflation will remain high going forward.

• CRISIL Research therefore believes that given this recent trend, for inflation to permanently move to around

5 per cent, it will not only have to fall, but will also have to stay low for a considerable period of time.

Without sustained low inflation, inflationary expectations cannot be anchored. For this, monetary policy must

continue with its tightening stance – at least until core inflation consistently starts showing signs of

moderation.

Table 1: Inflation above 5 per cent is not a new phenomenon

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Overall7.1 3.6 3.4 5.5 6.5

4.4 6.6 4.7 8.1 3.9 9.6 9.6

Food0.4 2 3 4.1 3.5

5.4 9.6 7.1 9.1 15.2 15.8 8.9

Fuelgroup

28.4 9.3 5.5 6.4 10.113.6 6.6 0.1 11.7 -1.7 12.3 12.9

Core4.7 2.2 2.2 5 6.5

2.6 5.7 5 5.7 0.2 6.1 7.4

Note: Green indicates inflation ≤ 4%, Orange indicates inflation between 4% and 5%, Red indicates inflation ≥ 5%.

Source: Ministry of Industry, CRISIL Research

• Expectations about future inflation influence household decisions about how much they consume today

versus how much they hope to consume in the future. If households expect inflation to go up, there is an

incentive to buy now before prices begin to rise faster. Similarly, inflation expectations also influence how

companies set prices and how wages are negotiated. If people believe high inflation is here to stay, they

would demand higher wages. This in turn raises demand in the economy, leading to a wage-price spiral.

Firms are willing to pay higher wages, since they believe they can pass on higher wage costs to consumers in

the form of higher prices.

Figure 1: Average Inflation and growth forecast for the next five years

5.0

6.3

5.5

7.0

8.0

8.5

Q12008-09 Q3 2008-09 Q12009-10 Q3 2009-10 Q12010-11 Q3 2010 -11 Q12011-12

WP I CP I GDP

Source: Professional forecasters’ survey, RBI

1Except in November 2010 when it was recorded at 8.2 per cent.

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 5/9

3

• The RBI’s Professional Forecasters’ Survey suggests that participants have upwardly revised their medium-

term (next 5 years) outlook on WPI inflation, consistently since the third quarter of 2008-09. The latest

forecast results released in August 2011 place medium-term inflation outlook at 6.3 per cent. (Figure 1).

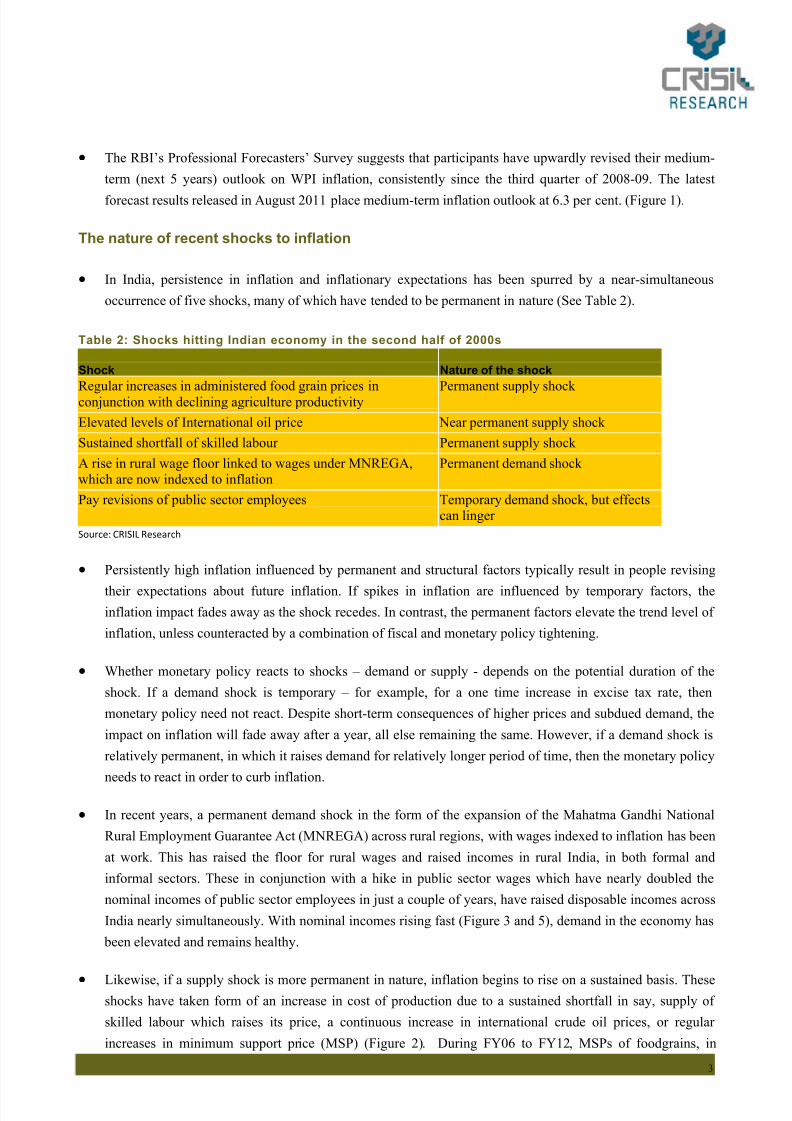

The nature of recent shocks to inflation

• In India, persistence in inflation and inflationary expectations has been spurred by a near-simultaneous

occurrence of five shocks, many of which have tended to be permanent in nature (See Table 2).

Table 2: Shocks hitting Indian economy in the second half of 2000s

Shock Nature of the shock

Regular increases in administered food grain prices inconjunction with declining agriculture productivity Permanent supply shock

Elevated levels of International oil price Near permanent supply shock

Sustained shortfall of skilled labour Permanent supply shock

A rise in rural wage floor linked to wages under MNREGA,which are now indexed to inflation

Permanent demand shock

Pay revisions of public sector employees Temporary demand shock, but effectscan linger

Source: CRISIL Research

• Persistently high inflation influenced by permanent and structural factors typically result in people revising

their expectations about future inflation. If spikes in inflation are influenced by temporary factors, the

inflation impact fades away as the shock recedes. In contrast, the permanent factors elevate the trend level of

inflation, unless counteracted by a combination of fiscal and monetary policy tightening.

• Whether monetary policy reacts to shocks – demand or supply - depends on the potential duration of the

shock. If a demand shock is temporary – for example, for a one time increase in excise tax rate, then

monetary policy need not react. Despite short-term consequences of higher prices and subdued demand, the

impact on inflation will fade away after a year, all else remaining the same. However, if a demand shock is

relatively permanent, in which it raises demand for relatively longer period of time, then the monetary policy

needs to react in order to curb inflation.

• In recent years, a permanent demand shock in the form of the expansion of the Mahatma Gandhi National

Rural Employment Guarantee Act (MNREGA) across rural regions, with wages indexed to inflation has been

at work. This has raised the floor for rural wages and raised incomes in rural India, in both formal and

informal sectors. These in conjunction with a hike in public sector wages which have nearly doubled the

nominal incomes of public sector employees in just a couple of years, have raised disposable incomes across

India nearly simultaneously. With nominal incomes rising fast (Figure 3 and 5), demand in the economy has

been elevated and remains healthy.

• Likewise, if a supply shock is more permanent in nature, inflation begins to rise on a sustained basis. Theseshocks have taken form of an increase in cost of production due to a sustained shortfall in say, supply of

skilled labour which raises its price, a continuous increase in international crude oil prices, or regular

increases in minimum support price (MSP) (Figure 2). During FY06 to FY12, MSPs of foodgrains, in

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 6/9

4

particular, have risen by an average of 11.7 per cent compared to a 5.7 per cent during FY00 to FY05. This

has consistently raised the floor for the market price of these commodities and has contributed to the

stickiness in food inflation. A failure to raise agricultural supply potential has further aggravated the

situation. (Figures 3). Similarly, the shortfall of skilled labour (Annexure 1) has increased skill premium and

has tended to sharply raise their wages.

Low agriculture output growth coupled with rising minimum support price pushes up inflation

Figure 2: Minimum Support Price hikes Figure 3: Agri Price and Output Movements

193 190

204

230

248

Paddy Jowar, Bajra

Maize

Ragi Arhur (Tur) Moong

2004-05=100

2004-05 2011-12

50.0

100.0

150.0

200.0

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Price Output

Note: (2004-05=100)

Source: Ministry of Agriculture, CRISIL Research

Note: (2004-05=100)Source: CSO, Ministry of Industry, CRISIL Research

• Upward momentum in international crude oil prices has also taken the shape of a near-permanent shock to

inflation due to its sticky nature. Barring the global recession in 2009, crude oil prices have consistently

exerted higher cost pressures on the corporate sector. While it is necessary to pass on international oil price

increases to domestic consumers, the ad-hoc nature of increases in administered fuel prices raises the element

of unanticipated inflation, thus interrupting the impact of monetary policy decisions.

• In recent months, a transitory risk to inflation has emerged in terms of depreciating rupee. Despite some

softening of global crude oil prices in recent months, a depreciating rupee is pushing up import costs, thus

raising inflation in domestic fuel prices, which are linked to international prices. However, the second-round

pass-through of exchange rate depreciation into retail prices would be limited as firms would find it difficult

to raise prices because of slowing private consumption growth.

Policy co-ordination

While the interaction between demand and supply determines the level of prices, the role of monetary policy is

restricted to influencing the level of demand in the economy. The expansion of supply potential is determined by

the quantity and quality of factors of production, namely labour and capital, and to a large extent, influenced by

government policies. In addition, fiscal policy also influences demand pressure via both direct government

spending and changes to household income through changes in public sector wages and minimum income

guarantee. Government policies related to education and enhancement of skills, and capital spending determine

the availability and cost of labour as well as infrastructure. Monetary policy will face the perennial pressure to

trade off economic growth for controlling inflation in the near future, if the fiscal policy is not supportive to the

objective of inflation control.

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 7/9

5

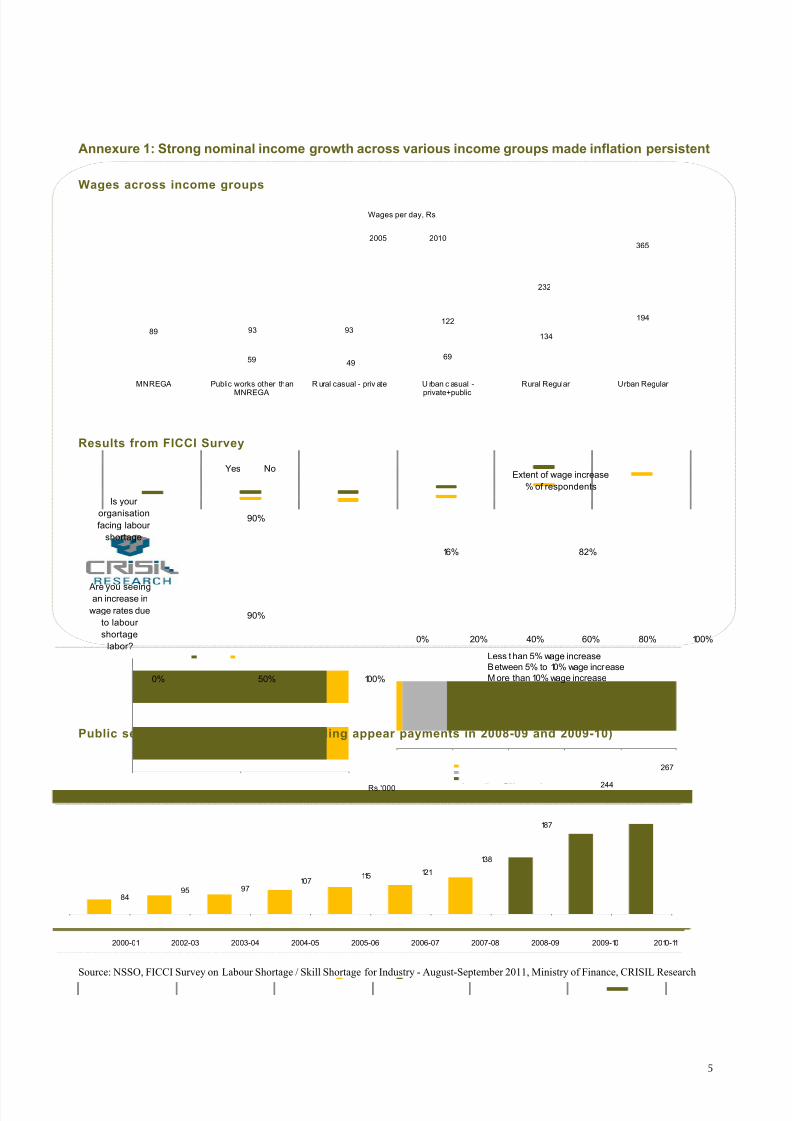

Annexure 1: Strong nominal income growth across various income groups made inflation persistent

Wages across income groups

59 4969

134

194

89 93 93122

232

365

MNREGA Public works other than

MNREGA

R ural casual - priv ate U rban c asual -

private+public

Rural Regular Urban Regular

Wages per day, Rs

2005 2010

Results from FICCI Survey

90%

90%

0% 50% 100%

Are you seeingan increase in

wage rates due

to labour

shortage

labor?

Is your

organisation

facing labour

shortage

Yes NoExtent of wage increase

% of respondents

16% 82%

0% 20% 40% 60% 80% 100%

Less t han 5% wage increase

Between 5% to 10% wage increase

M ore than 10% wage increase

Public sector wages per person (excluding appear payments in 2008-09 and 2009-10)

8495 97

107115 121

138

187

244

267

2000-01 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Rs.'000

Source: NSSO, FICCI Survey on Labour Shortage / Skill Shortage for Industry - August-September 2011, Ministry of Finance, CRISIL Research

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 8/9

CRISIL Centre for Economic Research (C-CER)

Macroeconomics:

Financial Economics:

Public Finance:

Environmental Economics:

“CRISIL EcoView”.

The Centre for Economic Research is a division of CRISIL. Set up in April 2002, C-CER reflects CRISIL’s

commitment to provide an integrated research offering to help corporates and policy makers take

more informed business decisions.

C-CER applies sound economic principles to real world applications, creating conceptual and

contextual linkages that are unique to CRISIL. C-CER also supports Standard & Poor’s Asia Pacific by

analysing and forecasting macroeconomic variables for 14 countries in the region.

C-CER’s core strengths emerge from a strong understanding of and capabilities in the following

areas:

l

Regular monitoring and forecasting of macroeconomic indicators,assessment of domestic and global events, and analysis of long-term structural changes in the

economy

l Analysis and forecasting of interest rates and exchange rates.

l Analysis and forecasting of central and state government revenues,

expenditures and borrowing requirements.

l Analysis of Indian firms’ impact on environmental, social and

governance parameters.

C-CER reviews developments in the Indian economy on a monthly basis and provides its outlook on

the economy through a dedicated publication CRISIL EcoView is used by CEOs,CFOs, economists, corporate strategy teams, marketing teams, treasuries and knowledge

management teams of various corporates and management consultancy firms to make appropriate

strategy level decisions.

The C-CER team comprises senior economists with over a decade’s experience of working with

premier research institutes.

8/3/2019 Inflation Insight_Oct 2011

http://slidepdf.com/reader/full/inflation-insightoct-2011 9/9www crisil com

Head office

Regional offices in India

CRISIL HouseCentral Avenue,Hiranandani Business Park Powai, Mumbai - 400 076Phone : 91-22-3342 3000Fax : 91-22-3342 3001

AhmedabadUnit No.706, 7th Floor,

Venus Atlantis, Near Reliance Petrol Pump,Prahladnagar, Ahmedabad 380 015.Phone: 91-79-4024 4500Fax: 91-79-2755 9863

Bengaluru W-101, Sunrise Chambers,22, Ulsoor Road,Bengaluru - 560 042Phone: 91 (80) 2558 0899, 2559 4802

Fax: 91 (80) 2559 4801

Chennai Thapar House,43/44, Montieth Road,Egmore, Chennai - 600 008Phone: 91-44-2854 6205 - 06, 2854 6093Fax: 91-44-2854 7531

New Delhi The Mira, G-1, 1st Floor, Plot No. 1 & 2Ishwar Nagar, Mathura Road,New Delhi - 110 065, India

Phone: +91 (11) 4250 5100, 2693 0117-121Fax: +91 (11) 2684 2212/ 13

Hyderabad3rd Floor, Uma ChambersPlot No. 9&10, Nagarjuna Hills,(Near Punjagutta Cross Road)Hyderabad - 500 482Phone: 91-40-2335 8103 - 05Fax: 91-40-2335 7507

KolkataHorizon, Block 'B', 4th Floor

57 Chowringhee RoadKolkata - 700 071Phone: 91-33-2289 1949-50, 5529 4501Fax: 91-33-2283 0597 Pune1187/17, Ghole Road,Shivaji Nagar,Pune - 411 005Phone: 91-20-2553 9064 - 67Fax: 91-20-4018 1930

Disclaimer CRISIL Research, a division of CRISIL Limited (CRISIL) has taken due care and caution in preparing this Report

based on the information obtained by CRISIL from sources which it considers reliable (Data). However, CRISIL does

not guarantee the accuracy, adequacy or completeness of the Data / Report and is not responsible for any errors or

omissions or for the results obtained from the use of Data / Report. This Report is not a recommendation to invest /

disinvest in any company covered in the Report. CRISIL especially states that it has no financial liability whatsoever tothe subscribers/ users/ transmitters/ distributors of this Report. CRISIL Research operates independently of, and

does not have access to information obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions

Limited (CRIS), which may, in their regular operations, obtain information of a confidential nature. The views

expressed in this Report are that of CRISIL Research and not of CRISIL’s Ratings Division / CRIS. No part of this

Report may be published / reproduced in any form without CRISIL’s prior written approval.

About CRISIL Limited

About CRISIL Research

CRISIL Privacy Notice

CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India's leading ratings agency. We are also the foremostprovider of high-end research to the world's largest banks and leading corporations.

CRISIL Research is the country’s largest independent and integrated research house with strong domain expertise on Indian economy, industries and capital markets. Weleverage our unique research platform and capabilities to deliver superiorperspectives and insights to over 1200 domestic and global clients, through a range of research reports, analytical tools, subscription products and customised solutions.

CRISIL respects your privacy. We use your contact information, such as your name,address, and email id, to fulfill your request and service your account and to provide

you with additional information from CRISIL and other parts of The McGraw-HillCompanies, Inc. you may find of interest.

For further information, or to let us know your preferences with respect to receiving marketing materials, please visit www.crisil.com/privacy.

You can view McGraw-Hill’s Customer Privacy Policy at http://www.mcgrawhill.com/site/tools/privacy/privacy_english.