informal credit markets an overview ...shodhganga.inflibnet.ac.in/bitstream/10603/79/18/08...chapter...

TRANSCRIPT

CHAPTER I1

INFORMAL CREDIT MARKETS - AN OVERVIEW

The informal credit market is an important part of the financial system of the

developing countries. They play a decisive role in channeling credit to small and poor

borrowers i n both urban and rural areas. They also constitute an important source of

working capital of all sizes and serve generally to ameliorate inefficiencies in the

allocation of formal sector credit.

There are two views concerning the importance of the informal credit markets

viz. Tradit~onal view and Modern view. The traditional view is quite sceptical about

the usefulness of the informal credit market in financial intermediation, saving

mobilisation, efficient and equitable use of funds in LDCs (Less Developed

Countries). Informal finance was often thought to be anti-developmental, exploitative,

and prone to consumption rather than investment behaviour and incapable of

expanding to provide an appropriate volume and range of financial services (Pischke

et.al., 19831.

However, of late the typically sceptical view of the traditional view has came

to be quest~oned. UNDP (1997) study made it clear that informal credit market works

directly in the community and had simplified application procedures, quickness in

extending credit, focus on the local market, providing larger loans based on successful

repayments, charge high rate of Interest, addressing the need of the poor clients and

consider reputation in the community as more important than collateral. This view

looked more sympathetic than the traditional one. Chandavarkar (1986) pointed out

that the ger~eral stance of policy towards the informal credit markets, in developing

countries can best be described as an amalgam of benign neglect and prejudice, which

is unwi~rranted considering that its scope and persistence testify, if anything to its

basic economic rationale deriving from its capacity to satisfy the needs which were

not met by the formal sector. Rather it supported the case for a positive and coherent

policy towards the informal financial sector. Platteau et.al. (1985) through a seminal

study of informal credit market in some villages in Kerala found that the demand for

credit in the rural area is apt to be a function of the degree of commercialisation and

modernisation of agriculture, investment opportunities etc. The efficiency and

resource rnobilisation aspects of informal credit markets are most relevant in the

present contcxl.

Konig and Koch (1990) held the view that unorganised financial market could

be seen as rcstorlrlg part of the social welfare lost due to the imperfection in formal

credit market and distributing income in favour of the small scale informal sector

which suifer!, disproportionately from uncertainty and high transaction cost. Rahman

(1992) was of the view that informal credit markets needed to be supported and

nurt~~reil lor justaining efficient and egalitarian development. Nair (1997) asserted a

linear relationship between credit and economic welfare. To her credit is just a

f.acilitation hctor in poverty reduction and economic welfare. Credit is potentially a

prime weapo~~ against rural and urban poverty.

Nisber (1067) and Holst (1985) found that informal credit markets knew their

custome~-s well and closely monitored their business payment records vis-i-vis formal

lenders and overall prosperity, integrity and cash position of their customers. Donald

(1976) al'f~rmed that convenient location, a minimum of red tapism, availability of

credit at ,my rime of the year, flexible term structure, flexible loan security

I-equil-cnler~ts were the merits of ICM. Besides there were no application forms to fill

out, reference to submit and line to stand in. The lender accepted or rejected the

request immediately. Roe (1979) and Timberg and Aiyar (1980) held the view that

informal c~edi t markets provided valuable services that were not adequately met by

moctern financial corporations.

Bhat (1986) viewed that informal credit markets operated largely on the basis

of personal intimate information and knowledge and they were in a better position to

identify new opportunities in financial transactions. Bouman (1989) asserted that

informal credit markets responded quickly or remarkably well to short term financing

opportunities, and allowed low income people access to service, not available to them

elsewhere ,ind ar relatively low cost. Another advantage was that informal credit

markets wvre made loans quickly (Ghate, 1992). Besides, informal credit markets

were not .subjected to interest rate regulation, credit allocation guarantee or

requlremenrs to maintain specified liquidity ratio. They do not incur legal expenses

and their cost of lending and deposit taking tend to be lower than that of modern

financial institutions.

Despite the growing body of literature upholding the merits of informal credit

markets, there are many who have remarked the negative side of the picture. With

regard to satery and liquidity of their customer's deposits, indigenous banks showed a

remarkably good performance although occasionally they mismatched maturities and

had liq~iidity problems. The risk diversification of indigenous bank was not good as

they provided unsecured loans (Nayar, 1982). Most of these unsecured loans were of

short duration. Thus it did not satisfy long term credit needs of the borrowers (Donald,

1976, Srivasiava, 1992).

Schrader (1992) explained that the literature of Sociology of development

labeled moneylenders with two stereotypes for the most part. The first one considered

them as "loan sharks" who sucked the poor and innocent peasants. The other

stereotype teflected the dominant opinion in development that moneylenders were

traditional torces, which prohibited progress and had to be eliminated for the sake of

rural development and replaced by banks and other formal savings and credit

institutions Boll1 stereotypes neglected the function of moneylenders in the supra

local socicl-econornic context. The positive aspects of low transaction costs and

efficient operation in informal credit markets was totally dominated by the emphasis

on the evil aspect of ICMs. Wai (1977) one of the first writers on lCMs estimated

that tnfornial loans were unproductive.

Many other researchers endorsed the view that informal credit markets

provided 1l1ost of their money for consumption or non-productive purposes. They add

nothing to their ability but at the same time they put borrowers in debt (Pischke et.al. ,

(1983)). According to Madhur and Nayar (1987) providing loans for consumption and

unproduct~ve purposes were not in the best interest of the capital scarce economies.

2.1 MOIIELS OF INFORMAL CREDIT MARKETS - A REVIEW

T l ~ e formal credit is often rationed with bank lending rate typically fixed by

authorities 1 government and the unresponsiveness to excess demand for credit. As a

consequence of this "financial repression", unorganised money market had tended to

develop ,~nd had become an essential part of the financial intermediation process.

lntere\t tart,\ 111 these markets were being determined by market forces of demand and

sll[>ply

Mc Kinnon-Shaw School used the term 'financial repression' for the first time

to describe such characteristics, loomed large in the domain of developing country

financial markets. This provided the intellectual underpinnings for a recent movement

towards fi~lancial liberelisation in many parts of the third world. Both Mc Kinnon

(1973) and Shaw (1973) assumed that capital markets in LDCs were imperfect and

fragtriented in the sense that there existed discrepancies among rates of return on

cap~tal ant1 financial assets. But the topic fragmentation of the credit market was not

expl~citly on side red in their analytical framework. Both of them recognized the

existence o i markets outside the formal credit markets.

The low administratively determined interest rates on bank loans ensure that

credlr will l)e rationed by non-price means, artificially depressing the aggregate rate of

retul-11 on invesunent. Thus financial repression reduced both the quantity and quality

ol'rlcw investments thereby economy's rate of growth (Peter, 1989).

'1'111. cretlit gap resulting l'rom the financial repression supposed to be filled by

infolmal cretlir rliarkets was exemplified by Mc Kinnon-Shaw Models. But these

markets were perceived as inefficient and not incorporated into the formal analytical

framewol-k The policy prescriptions that followed from the Mc Kinnon-Shaw

Mypothesi!, was that interest rate should be freed from administrative restrictions

along with easing restrictions on bank lending.

The informal, unorganised or unregulated loan markets were incorporated in

economic n~odels in the works of Winbergen (1982 & 1983). Taylor (1983), Buffie

(1984). Kotrsaka (1984), Cho et.a1.(1992), Lim (1987), Liang (1988), Shabin (1990),

etc. These studies known as Neo-Structuralist ones were largely developed to

examine the impact of liberalisation policies and some stabilisation measures on

economic activity when informal loan markets were incorporated in economic

~nodels.

But the notion of informality embedded in the Neo-Structuralist view of these

markers wah rather restrictive. Their view of informal credit markets was that of

competitive markets existing parallel to the formal credit markets with flexible market

clearing prices. In these markets there were no impediments to movement of

borrowers from one market to another nor the flow of funds across the markets. This

version of informal credit markets is referred to as curb markets the term used by

Neo-Structuralists.

But in dii.ect contrast to the curb markets, an alternative view of informal

credit tr;~nsai:tions recognises their traditional structure and the'underdeveloped nature

of these in;~rkets. Such conceptualisation finds considerable support in recent

empirical studies (ADB, 1985). The bulk of the evidence suggested that informal

credit markets were a far cry from the competitive, flex-price curb markets. They are

usually fragmented, non no pol is tic and inclined to be characterised by sluggish prices.

(Srivastava, 1992).

Thert: are two types of informal credit market viz., reactive and autonomous.

The lorrnei- may be reactive to the formal sector regulations. So informal credit

transactions ore not ever1 loans from professional moneylenders, But borrowings from

friends and relatives also. In stark contrast to the neo-structuralist view, where

informal crcdit markets was viewed as curb markets and was integrated with the

regulated . tornial credit markets, the current stream of thinking considers informal

credit marke~s as the traditional and underdeveloped markets (Srivastava, 1992).

2.2 SIZH OF INFORMAI, CREDIT MARKETS

'l'herc IS llttle information particularly a detailed quantitative information

available on inlorrnal credit markets in developing countries. The main reason is the

reluctance o:i the part of the lenders to divulge the details regarding their functions.

This 1s being done in order to maintain informational advantages and to perform

heterogeneous functions in the sector (Peter, 1989). The available data on informal

credit niarkets are fragmentary and relying on desperate and non-comparable sources

across countl-ic. I3ut the size of the informal credit markets in many developing

countries 1s hy no means negligible. The fragmentary evidences available puts the

size o f iniortnal credit markets anywhere between 33 per cent and 93 per cent of the

total tinanci.11 inarket. Bangladesh Bureau of Statistics (1989) provided that about

63.7 per c e n ~ of the total credit i.e. 14.1 billion Taka was transacted in the informal

credit marker i n the year 1986 in Bangladesh.

The hize of the Informal Credit Market may be detected from two main points

according to Prabovo (1987). The first one is on the number of people borrowing or

lending o n informal basis. The second is the amount of loans transacted. But he was

01- the vlew tI1;1t both the factors cannot be precisely determined. So, how much is the

size ot ~nlbl-mal credit market is not precisely known. Ghate (1992) viewed that

though ICM is largely inscrutable, i t is almost important in aggregative terms.

111 the: Philippines lion-institutional credit was estimated to have provided 64-

78 per cent C I S ttre total credit granted to agriculture in the late 1970s (IBRD, 1983).

l'hc data on Kore;~ at the household level estimated that 50 per cent of the total loans

were obta~nzd t1oi11 informal sources (IBRD, 1984). Cole and Park (1983) found that

ill Korea thc. size of the curb market was about 15 per cent of the total in 1978 and i t

decl~ned to 7 per cent in 1982. The figure for Thailand is 52 per cent in regard to the

new loans extended to the agricultural sector

Wai (1977) estimated that the value of total loans outstanding in organised

rnoney inal kets went up in most developing countries in the 1950s and 1960s. It was

found that in ilnorganlsed markets also value of total loans outstanding showed an

upward rre~lci in a number of countries including Thailand and the Philippines.

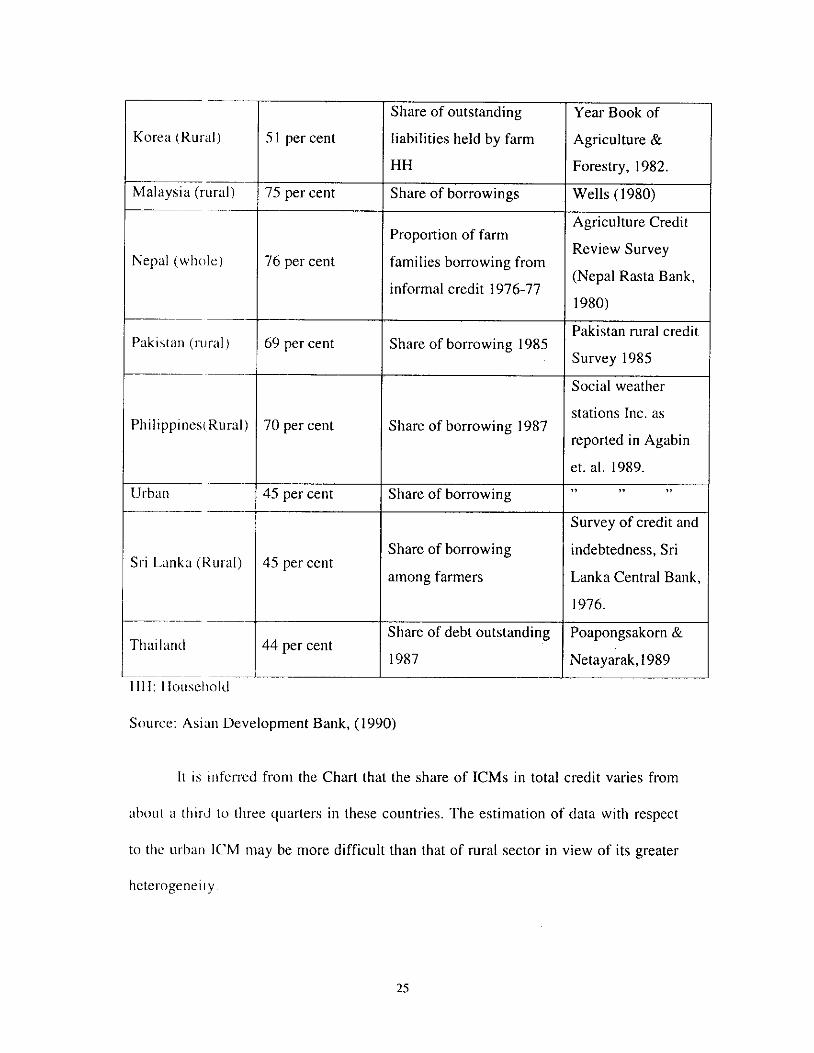

'I'ht. Chart 2.1 shows some recent estimates of the size of informal credit

market\ 111 \elected developing countries

Chart 2.1 Size of lCMs in Selected Developing Countries

r - .- - - -.

Country

India (ruri11)

Informal Credit

113 - 213

113 - 213

Source

Share of total volume of

borrowings

Share of borrowing mid

1980 s

38 per cent

Rahman, Chowdary

& Murshid (1989);

Hussian (1983), and

Rural credit Survey,

1987. (Bangladesh

Bureau of Statistics:

Various studies

Share of outstanding HH

debt owed to ICM 1982

reviewed by Feder

et.al. (1989)

All India Debt and

Investment Survey,

1982-83 (RBI,

(Continued)

I I I Share of outstanding I Year Book of 1 Korea (Rural) 1 5 1 per cent I liabilities held by farm 1 Agriculture d 1 I-.-- Malaysia (rural)

75 per cent

Nepal (whole) 76 per cent

Urban

HH

Share of borrowings

--

Sri [ a k a (liural)

Forestry, 1982.

Wells (1980)

Proportion of farm

families borrowing from

informal credit 1976-77

Thailand

Agriculture Credit

Review Survey

(Nepal Rasta Bank,

1980)

Share of borrowing 1985 Pakistan rural credit

Survey 1985

Social weather

70 per cent

45 per cent

Share of borrowing 1987

45 per cent

Source: Asia11 Development Bank, (1990)

stations Inc. as

reported in Agabin

Share of borrowing

44 per cent

11 is inferred from the Chart that the share of ICMs in total credit varies from

et. al. 1989. 3 , 2. ,,

Survey of credit and

Share of borrowing

among farmers

ahout n thir8.I lo three quarters in these countries. The estimation of data with respect

indebtedness, Sri

Lanka Central Bank,

Share of debt outstanding

1987

to thc urbei~ ICM may he more difficult than that of rural sector in view of its greater

Poapongsakorn &

Netayarak, 1989

2.3 SIZE OF INFORMAL CREDIT MARKETS IN INDIA

'l'he .,ystern of indigenous banking dates back to ancient time in India. Until

the middle c ~ f the nineteenth century indigenous banks were the central part of the

financial system and loans were even provided to the government also. The advent of

the British drsturbed the monopoly of these markets and in its place European bankers

enjoyed the state patronage. As a result indigenous bankers were gradually pushed

out. But these European bankers were concentrated only in urban centres and this

helped the irldigenous banks to maintain an important position in rural areas. But with

the progressive expansion of commercial banks the share of the indigenous banks

started diminishing. (Govt. of India, 1972). Today, indigenous banks play a limited

role, but they still enjoy a significant role in the Indian Financial System (Holst,

1985 1.

The Indian Financial System broadly consists of two segments. Formal and

Informal credit sector. But the line of demarcation between the formal and informal

sector i \ 1101 watertight. The informal credit market in India is highly Institutionalised

in terms 01' organisational structure. It covers institutions both in corporate and non-

corporate tit-ms (Pishke, 1991). Nayar (1982) found that in India besides the

organised financial intermediaries there is also a sizable unorganized sector, which

includes a bariety of small institutions.

Most of the studies on lCMs in India concentrated on rural sector. But recently

a few stud~es had been conducted on urban sectors of the economy. According to

AIDIS figure (1981-82) the proportion of the household outstanding debt owed to

informal sector was 38.79 per cent for rural areas and 40.05 per cent for urban areas.

The survey indicated that there has been a sharp decline in the share of informal rural

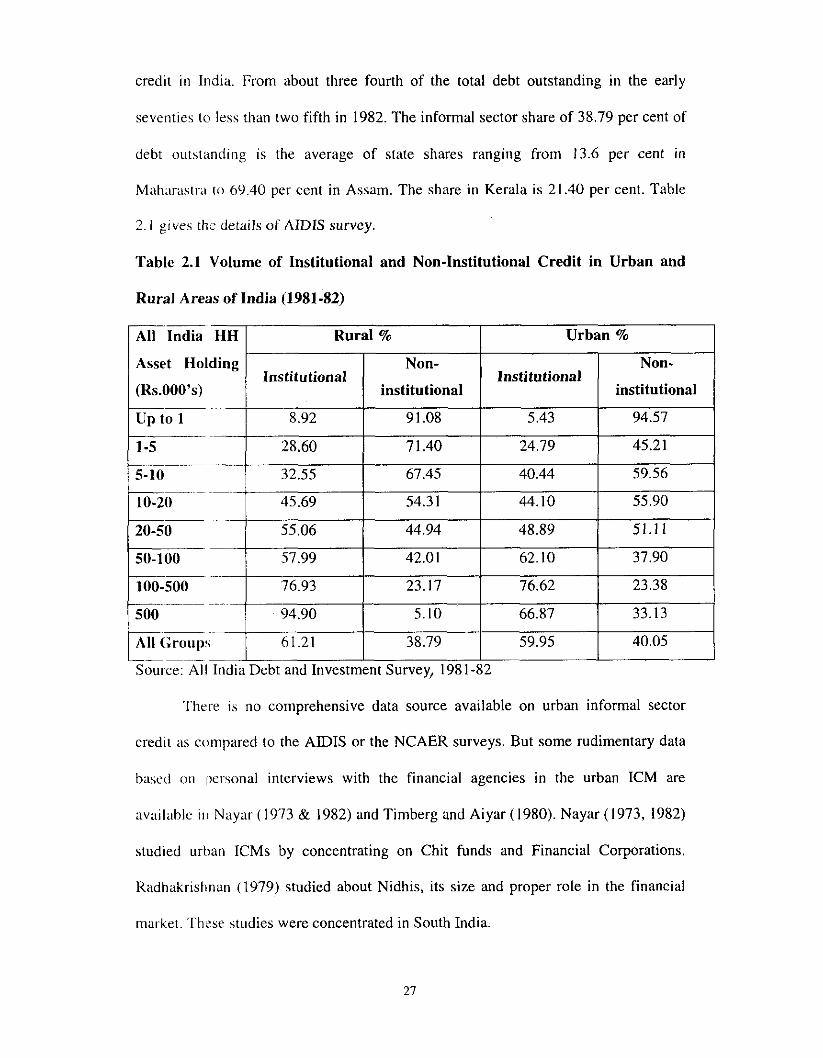

credit in India. From about three fourth of the total debt outstanding in the early

seventies to less than two fifth in 1982. The informal sector share of 38.79 per cent of

debt outstanding is the average of state shares ranging from 13.6 per cent in

Mahar.ast~-a to 69.40 per cent in Assam. The share in Kerala is 21.40 per cent. Table

2.1 gtves the details of AIDIS survey

Table 2.1 Volume of Institutional and Non-Institutional Credit in Urban and

Rural Areas of lndia (1981-82)

Asset Holding Non- Non- Institutional

(Rs.000'~) institutional institutional

91.08 5.43 94.57

p i r l n d i a v Rural %

I I I I

Sou~ce: All India Debt and Investment Survey, 198 1-82

Urban %

There is no comprehensive data source available on urban informal sector

credit as compared to the AIDIS or the NCAER surveys. But some rudimentary data

basctl O I I perwnal interviews with the financial agencies in the urban ICM are

av;~~lablc 1 1 1 Nayar (19'73 & 1982) and Timberg and Aiyar (1980). Nayar (1973, 1982)

studied urhan ICMs by concentrating on Chit funds and Financial Corporations

Radhakrishnan (1979) studied about Nidhis, its size and proper role in the financial

market. These studies were concentrated in South India.

Table 2.2 shows the destination of informal credit market funds in percentage of loans

Table 2.2 Percentage of Loan Outstanding

1 Small I Large

Source I Trade / Exports I Scale ( Scale

1 1 I Industries I Industries -- I I I I Shikarpuri Financiers

I I I I

-- - Rastogi Bankers-Uttar

55 12 Pradesh

Gujarati Bankers

Chettiar Financiers-Tamil

Nadu

- -- -- Cheltiar Pawn Brokers -

22 5 Tamil Nadu

- Finance Companies

40 8 (Trichy and Karur)

32

-- Source Dat,~ gathered by C.V Aiyar, 1979

60

45

Others

25

15

20

Sr~vastavc~ (1992) in his study presented the estimate of a group of

10

10

intern~edinrir:~ namely indigenous bankers and commercial financiers. Since a

16

number of othel- types of lenders are excluded these figures can be viewed as severely

7

5

5

biased. Tc~blt 2.3 shows the estimate of credit extended by selected informal lenders

10

10

Table 2.4 Estimates of Credit Extended by Selected Informal Lenders

-- - - - -- Name Number of firms I Credit extended (billion Rs.)

I I -- - -- - - Gujarati Bankers 2,000 7.5

Rastogi Ijankers 500 1 .O .. . -- --

Chettiar i3anlcers 2,500 3.8 I .... -

Shikarpuri Bankers 7 2,955 3.8

'l'irnberg and Aiyar (1984) estimated that there were 25,000 Chettiars pawn

brokers firms in 1978-79 with credit extending to Rs. 12.5 Billion. Banking

commission of 1981 reported that indigenous-style bankers provided one-twelth to

one hall ot a11 credit to different categories of industrial units. The amount ranged

from all average of Rs.300 for units of under Rs.25.000 capitilisation and increased to

Rs.35,000 ibr those with over Rs.75.000 capitilisation (Timberg and Aiyar ,1984).

Madhur and Nayar (1987) showed the volume of lending by both corporate

segment and non-corporate segment of the informal credit markets. Table 2.4 shows

the total lending by both corporate and non-corporate sector of informal credit

markets. ('orporate sector includes Investment companies, Loan companies, Hire

purchase companies, Housing finance companies, Mutual benefit funds, Chit funds

and non-cc~rporate sector includes Finance corporations, Indigenous bankers, Pawn

brokel-s ctc

Table 2.4 Total Lending by Corporate and Non-Corporate Segment of ICM I Total lending by corporate sector

Year (Rs. in Crores)

.

1975 240.4 ~ ~ P ~ , -~ . .. ~~p

1976 298.9 p~ ~ .

1977 351.5 - ' 1978 399.2

-~ .-- 1979 450.0 p P ~ ~ -~ ~

1980 658.4 ~ ~- , ~~ ~~ -

1981 751.2 p~~ ~. ~ , 1982 9 19.6 -- . .

1983 3 ~- 11 17.4 1984 j ....-

1295.9

1985 1817.9 - - -. -

Total lending by non-corporate sector (Rs. in Crores)

-

3437.9

3535.2

3632.5

3744.0

3672.8

4020.3

4190.2

Source : S Madhur and C P S Nayar (1987)

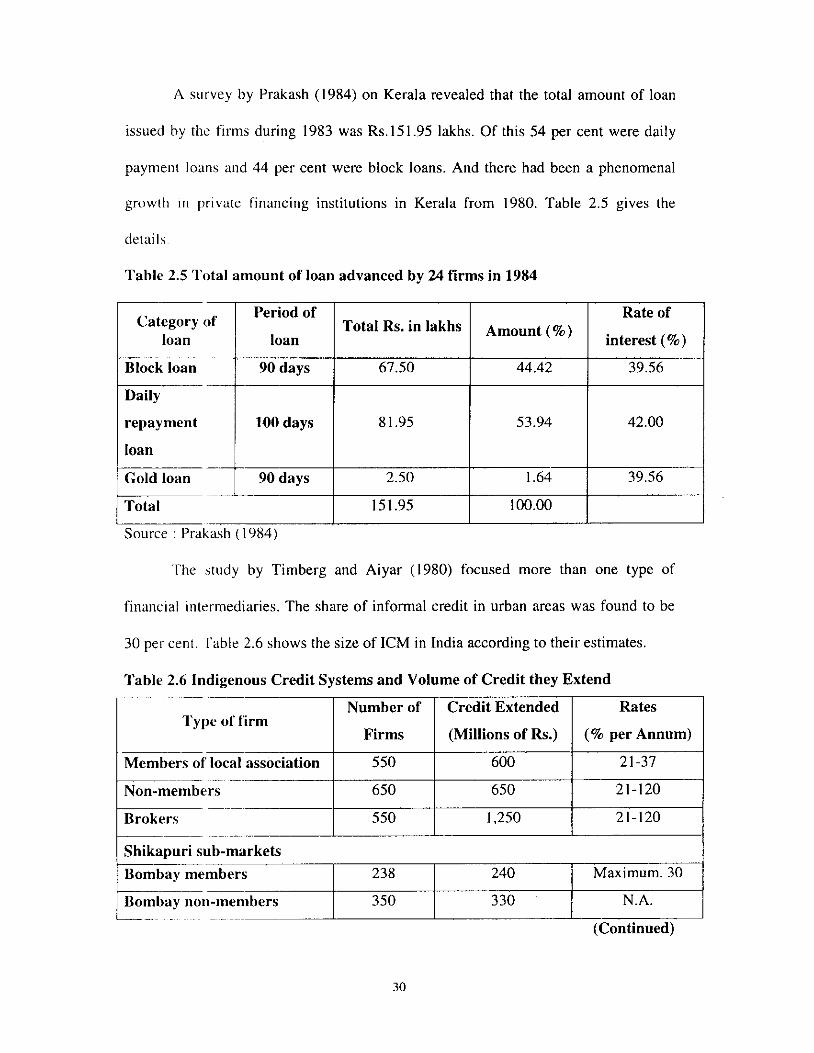

A survey by Prakash (1984) on Kerala revealed that the total amount of loan

issued by the f~ rms during 1983 was Rs.151.95 lakhs. Of this 54 per cent were daily

payment loans and 44 per cent were block loans. And there had been a phenomenal

growth in private financing institutions in Kerala from 1980. Table 2.5 gives the

derails

Table 2.5 Total amount of loan advanced by 24 firms in 1984

Block loan *days / I I

67.50 44.42 39.56 1

T:: of Category of

loan

loan i I I I

Total Rs. in lakhs

Daily

repayment 100 days

~~~~~t (%)

81.95

- - t y d a y s j I I

I - I I I

Source : Prakash ( 1984)

Rate of

interest (%)

Gold loan 2.50 I I I

'The study by Timberg and Aiyar (1980) focused more than one type of

53.94

Total

financ~al inttxmediaries. The share of informal credit in urban areas was found to be

42.00

1.64

30 pet- cent. I'able 2.6 shows the size of ICM in India according to their estimates.

39.56

151.95 100.00

/Bornbaymembers 238 240 / Maximum. 30

Table 2.6 Indigenous Credit Systems and Volume of Credit they Extend

Rates

(% per Annum)

21-37

21-120

21-120

- .- ~ ---

Type of firm

Members of local association ~

Nan-members ~p --- -

Brokers

I I I

Number of

Firms

550

650

550

N.A. 350

Credit Extended

(Millions of Rs.)

600

650

1,250

(Continued)

330

I\<. $

j e ~ e e r s ' $ p 5 IS0 ' 1 Maximum, 37 I ,%.. .,

l=~n-n~embers 200 I 160 I N.A.

I I I 10 N.A. N.A.

I I I 12 N.A. N.A.

Bangalore nlembers

Bangalore non-members N.A. N.A.

N.A. 30 N.A. I I I

N.A. 45 N.A. I I I

N.A. 10 N.A.

100 104 N.A. similar work.

Gujarati Indigenous-style bankers

2,000 7,460 18

N.A. N.A. 18 Agents

Chettiars bankers

I -- I I IZastogi hankers 500 1,000 18-24 up to 36

-~ - . ~~~ ~ ~~~ ~~ -- - Soul.ct. : I h t n gathered by C.V. Aiyar, 1979

Chettiar bankers

- - 1 2 5 , 0 0 0 I I

N i ~ c : ,ill i;11c5 ere approximate ; the interest rates and numher of firms figure trlorc solid tlnn ~hc est i~~~atcs 01' cred~t extended. Shikapuris receive Rs.30-Rs.60 m i l l i o l~ in bank refinance and havc Rs.75 n i i l l ~on i n deposits. Chettiars have perhaps Rs.2.500 million i n deposits. Rastogis have approxinialrly Rc.550 million in deposits.

Chettiar pa~nbrokers

2,500

12,500

3,800

18-30+

18-30

2.4 SEGMENTATION IN INFORMAL CREDIT MARKETS

I t was found that ICM consisted of many sub-markets depending on the type

and nature of collateral, types of borrowers, need for credit and the like. There was a

visible difference among different categories of these sub-markets within the informal

credit markets. Cole and Park (1983) in a study on Korean ICM classified into five

sub-sectors or- sub-markets in terms of characteristics of intermediaries, borrowers and

lenders in each market. These were Private Credit Markets, the Kye market, Curb

market, Private financial companies and Informal bill market.

Vo~~gpradip (1985) described the existence of four sub-markets in urban

infol-ma1 credit market in Thailand. These were Personal Rosca, Business Rosca,

Trade crcd~t and Cheque discounting operations. In India Timberg and Aiyar (1980 &

1984) class~fied intermediaries into four types on functional lines. These were

( i ) Those accepting deposits such as Gujaratis, Indigenous banks and finance

cotnp;lnies ( i i ) Commercial financiers employing mostly their own funds but availing

of discount~ng facilities with the commercial banks such as Shikapuri financiers (iii)

Brokers who worked for both the first and second category (iv) Commercial paper

financiers.

Lan.~berte (1987) classified ICMs into mainly five sub-sectors: Rosca, landlord

moneylendcrs, tradedmiller moneylenders, farmer lenders and professional

moneylendcrs. Kwack et.al. (1981) classified the rural credit markets into friends,

relatives and neighbours, fanners, landlords, input dealers, output dealers,

profcssiona money lenders, pawn shops and Rosca. Probovo (1987) classified ICM

according to the motives for moneylending into two types: commercial and non-

commc~-cinl. I'he commercial lenders included stores, itinerant traders etc. Non-

con~nlercial lenders included friends, relatives and patrons etc.

The characteristics of intermediaries in classifying informal credit markets are

referred to a \ the conventional criteria according to Mauri (1987). The instruments

used in transactions in ICM were also used as basis for better understanding of

segmentatiol~ 111 informal credit markets. Instruments are important because informal

interest r a t e vary with types of instruments used in transactions in informal credit

markets.

Ghatc ( 1986) in a study conducted for the ADB stated that there was no such

thing as informal credit markets. But there were a number of informal credit market

segments by locality, lender size, the trade, industry or service being financed whether

lcgnl (11- illci:al and so on. Correlated with these variables would be others such as

soul-ces of funds and uses of funds i.e., fixed or working capital, interest charged,

doc~~mer~tary instruments used, source of information on borrowers and ability to

impose debr-service disciplines etc. He asserted that direction of lending was the

identifying factor for finding out different segments in the economy.

Madhur and Nayar (1987) argued that the segmentation in informal credit

market was due to wide dispersion in interest rates between markets and the difficulty

or limitalic~n of the customers to get finance from particular markets. This

specialisation was due to the asymmetric information about borrowers. Nisbet (1967)

supported the above view and opined that moneylenders had limited credit markets

area i.e., thuir radius of action in which credit demand was rather inelastic with regard

to changes of interest rates. Iqbal (1988) also found that segmentation and information

aspecls wclc illiitiiately related.

Swan~~nathan (1991) opined that understanding the reason for the

seg~nentatlon was important both for the theory of informal credit markets and for

developlrig policies. The type of collateral accepted as security by lenders and the

purpose llr~derlying ihe demand for credit were the two important determinants of

segnientatit~n according to her.

Schlxder (199'2) found that informal credit markets revealed a very

heterogeneous and imperfect structure. Owing to this heterogeneous and segmented

market structure informal credit markets were not integrated. Rahman (1992)

explained scgmentation in ICM as rigidly defined boundaries in terms of the lenders

and bol-rowers and more importantly in terms of the forces, operating to determine the

I-ate ut' IIIIL'I.I:SI within each segment.

' I ' l l i Icatls to a question whether lCMs are segmented or specialiscd. The key

dit'ference between the two being that segmentation implies a certain degree of

inefficiency itrising from non-optimal allocation of resources, whereas specialisation

connotes cff~ciency through optimal allocation of resources. Ghate (1992) found that

segrnentaiioll could be thought of as the existence of several sub-markets and an

increase in ihe ;~vailabil~ty of funds in one segment did not immediately increase the

availability ~.)1- reduce the price of credit in another, although some funds flowed

between segnlentb. The segments were in the sense of relatively homogeneous

hot-rower grclups or borrowing purposes or what might be termed as vertical segments

wet-e however themselves segmented horizontally into a sort of cellular structure. The

borl-owers wcre relatively homogeneous across horizontal cells but not across vertical

segmenth. Segmen~ation was more than just a division of the market by lender type,

since seve,ral types of lenders often made the same type of loan to the same group of

borrowers

Meyer and Nagarajan (1997) found that the matching of informal lenders with

borrowers based on their occupational specialisation led to market segmentation. The

segrnentati~~n limited the effective functioning of a particular type of lender outside

his or he) specialised field due to the lack of adequate borrower screening

tcchr~ologics and contract enforcement mechanism. Gupta (1997) explained

segmentatioll in ICMs i n terms of exclusive sets of borrowers and lack of fluidity of

loa~iable fullds i~cross segments made the market inefficient and high rate of interest

and differer~t rates in different segments manifested both inefficiency and monopoly

power ol' lenders vis-i-vis the economically weak borrowers and resulted in an

inadequate xonomic order through appropriation of collateral and surplus of the

borrower iiy the lenders. Gill and Singh (1997) explained the credit market

segrnentatio~~ between formal and informal credit sectors rather than segmentation

within informal credit market. They cited some reasons for the segmentation between

(hrm:rl u11d ~nli)rniaal sectors. The main one among was that the inability of some

borrowel-s to offer Sully marketable collateral.

7'0 conclude segmentation connotes different implications to different

researchers. I'hey have used different concepts to explain segmentation in informal

cretlit nlarkcts. Most of the studies reviewed above emphatically proved the existence

of segrnent;~~~o~l ill inSol-ma1 credit markets. It is argued that there exists different

categories ul lnoncylenders lintermediaries in informal credit market. The activities

may be dil-feient form one category to another and it is the basis of segmentation in

lCMs lo a group of researchers. Another argument is that there are various collateral

instruments used in informal credit transactions and it is a guiding factor according to

some researchers to define segmentation in ICM since there exists different interest

rates. Again another view is that due to the presence of asymmetry of information on

borrowers, lenders in ICM seemed to have specilised in some kind of activities and

their activity is confined to a limited area. When each lender specialises in one type of

lending anti restricts himself to a certain type of activity this forms another type of

segrne~itatii)n.

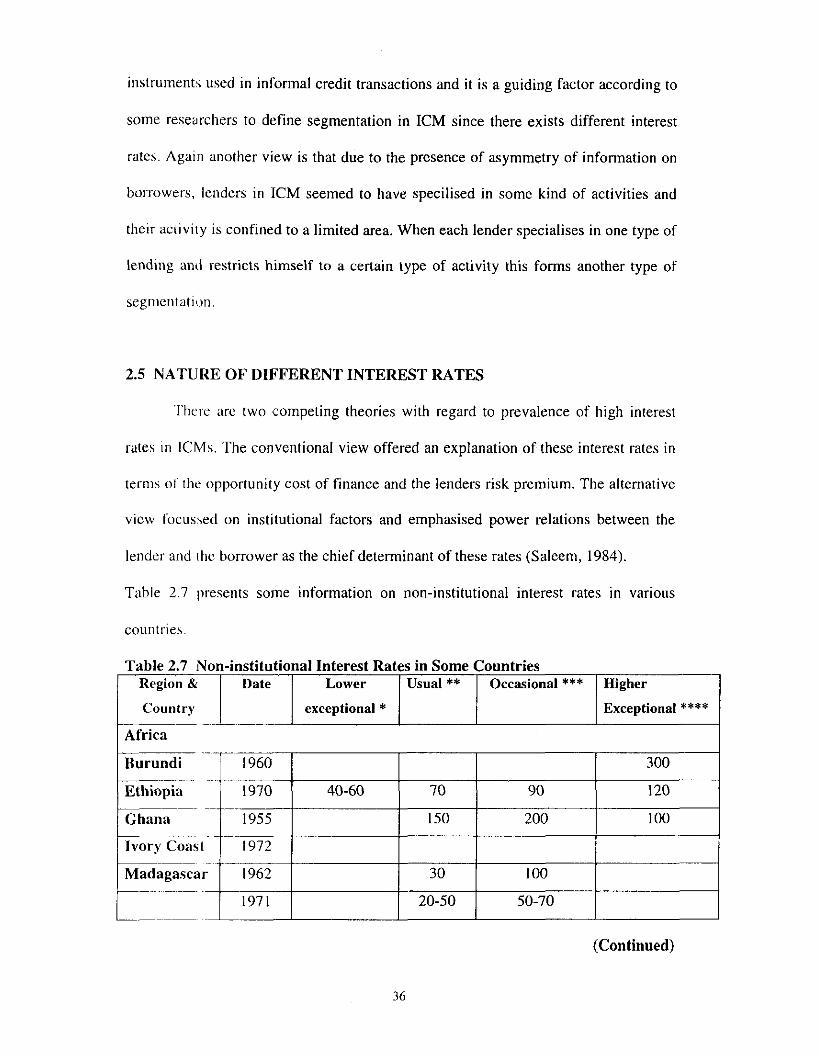

2.5 NATURE OF DIFFERENT INTEREST RATES

'I'hel-e arc two competing theories with regard to prevalence of high interest

rates in ICMs. The conventional view offered an explanation of these interest rates in

terms of rhc opportunity cost of finance and the lenders risk premium. The alternative

view focus-,etl on institutional factors and emphasised power relations between the

lender and the borrower as the chief determinant of these rates (Saleem, 1984).

Table 2.7 presents some information on non-institutional interest rates in various

countries

Table 2.7 Non-institutional Interest Rates in Some Countries

. -.

(Continued)

60 130

200 --

Asia

Latin America

Brazil - 1 15 I I I

1 29-40 1 80

I I I ~-

Colombia t - ~ 24 60 95

120 Bolivia 11961 1 48 98

I I

Costa Rica t -1969 I

(Continued)

12 1 18-24 1 35

Ecuador 1965-66 2

El Salvador.

1971 - ~ -- --

Mexico

Paraguay 1972 18

Above 100

20-27

25

40

36-72

24-30

50

144

36

80

300

60

Source: [ I Tun Wal ( 1 980)

18

7

10

Inforllti~l interest rates were generally discussed in terms of transaction costs,

r~sk prenl~um, cos l of funds, non no pol is tic or oligopolistic profits, asymmetric

* ** Most frequently reported rate *** Rates between the usual and the highest **** Highest rates

3 3

35

18-24

20

16-20

information, demand and supply factors, nature of collateral etc. Leite (1982) argued

that the nominal lending rates should represent the moneylender cost of making

50

30

25-36

capital available The lending rates covered transaction cost is . , cost related to default

48

risk plus administration cost as well as the opportunity cost of capital.

Meyer and Nagarjan (1997) in a study on rural economy found that interest

rates was high ertough to cover lender costs defaults risk and inflation premium. It is

justified that by charging high rates can only lending institutions become viable and

self-sufficient. Mrak (1989) asserted that moneylender's rates of interest not only

covered transactit~n cost of capital but also included an extra profit resulting from

their monopoly power. It is argued that ICM handled high-risk loans thus require a

high prernlum to cover up repayment default (Wai, 1956, Bottomley, 1963, Bhaduri,

Aleem (1990) found that high informal rates reflected high cost of gathering

information on the part of moneylenders about loan applicants. Similar views were

held by Siaruwalla et. al. (1990). Floro and Yotopoulose (1991), Chandavarkar,

(1987) arid Wclls (1980). They found that high interest rates were not totally usurious

or monopoly rents but due to high transaction, administration and opportunity cost

they were hrced to lend at high rates. [Also in Bottomely (1963,1975)l. Plattaeu et.

al. (1985) did not support the above view. They mentioned that opportunity cost of the

lender's time and risks factors were the major reasons behind high rates.

Cihate (1986) did not support the view that interest rates in the ICMs were

decided by mor~opoly power. To him i t is depended on higher risk premium and loan

administration costs. The following is a hypothetical cost structure of formal and

informal credit markets loans in percentages given by Ghate (1992). It showed the

cost components of formal and informal loans to borrowers in two categories before

and after competition.

Chart 2.2 Cost Components of Type of Loans

Formal Loan lnformal Loan (Before competition) Informal Loan (After competition) Informal Loan to high risk borrower (Before competition) Formal Loan to high risk borrower (After competition) Informal loan to high risk borrower (After competition) Transaction Cost Risk Premium Opportunity Cost of funds Monopoly Profit Efficiency Rent

Source : CiI~'i[c( I002 I

Rahman r 1992) did not support the premise that the high interest rates in the

ICMs imply exploitation of the borrower by the lender. He connected interest rates

with that of rate o l return. If the rate return was more than the rate of interest the

borrower gets the borrower was said to be in a better position. Wellington (1955) also

supported [hi5 arpuinent. Stiglitz and Weiss (1981) made it clear that high interest rate

was due tc) 111gh-I-isk PI-oblems or asymmetric information. Iqbal (1981) pointed out

tI1;it there w ; ~ a iclonc~poly surcharge in the informal interest rates. Bottomely (1964),

Pischke (1983). Holst (1985), Lelart (1982), Bouman (1989). Wai (1977). IBRD

(1983) and Mujumdar (1991) supported the monopolistic character in informal

interest rates.

The nature of collateral is another factor, which influences the rate of interest

in the ICM. Mc Leod (1991) inferred that the exact rate of interest chosen reflected

the nature and value of assets offered as security and banks' evaluation of the

borrowers' char;tctcr and ability. Sarap (1987) found that rate of interest charged

decreased as the qu~ility of the collateral and status of borrowers rose. The purpose of

borrowing is another factor influencing rate of interest in the ICM.

Swaminathan(l991) claimed that high rate of interest in ICM was due to the inelastic

demand for inforrnal credit.

Nayar (1982) compared the prevailing rate of interest in formal and informal

credit markets. He showed that formal bank credit was not attractive since it was

difficult to gel loans from them. The borrower had to make several trips to a bank in

order to secure a lo;ui. These involved substantial cost of transport and other expenses

as well 21s loss of working time. If these were added to the nominal rate of interest

charged on bank loam, the difference between the two might not be large.

Srivastava (1992) found that there was remarkable consensus across the

different respontlents about the perceived value of a reference rate of interest, and it

showetl 110 signil~cant intertemporal variation over substantial period of time.

Alnlost all studies have firmly proved the prevalence of high rate of interest in

the inforn~al credit market. But the factor influencing this high rate of interest differ in

different studies There are differences in the factors, which influence the high rate of

interest in urba~i and rural informal credit markets. The monopolistic character of

lenders IS onc o l the factors, which is said to influence the high rate of interest. But

this may not he possible when there is a case of competition. We cannot expect fall in

the rate of interest in the informal credit markets when monopoly of lenders is

shattered. Opportunity cost of finance, default risk premium, transaction cost, demand

and supply factors, asymmetry information on borrowers are some other important

factors influe~~cing the high rate of interest in informal credit markets. The quality of

collateral and purpose of borrowing are said to influence the high rate of interest. It is

concluded that i f the quality or marketability of collateral is high rate of interest

charged will be low.

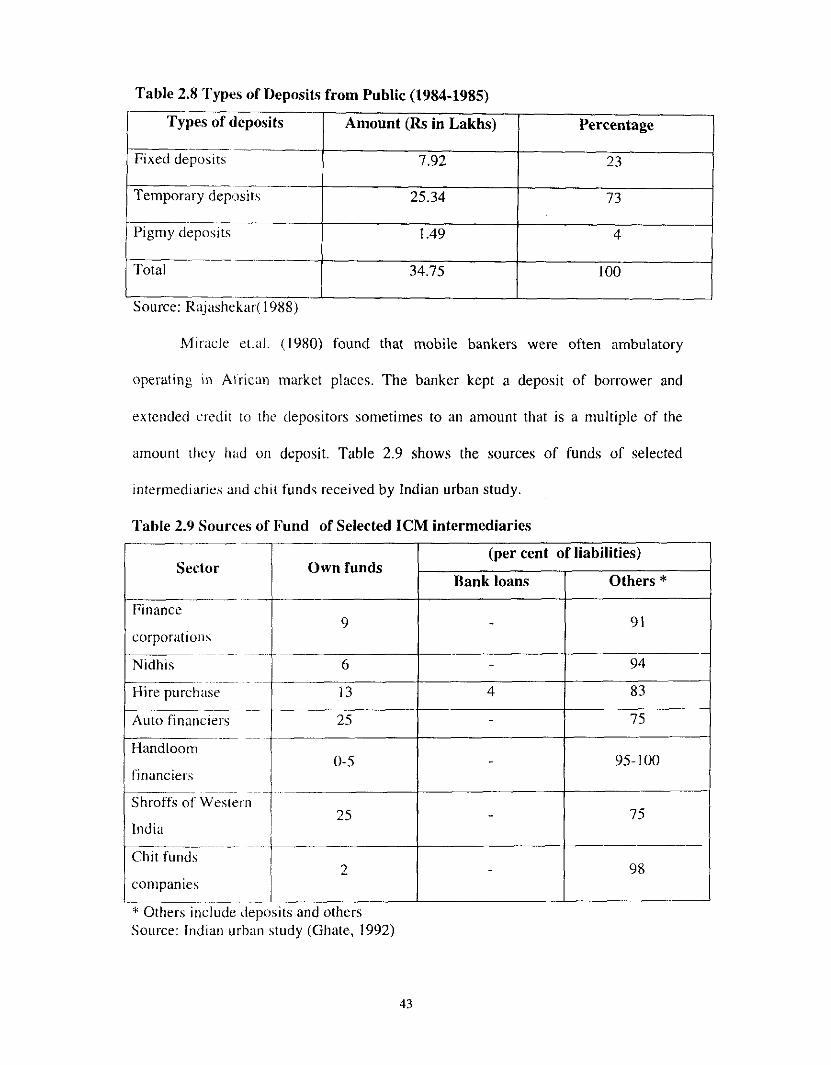

2.6 DEPOSI'I' MOBILISATION

Depos~ts can be regarded as the main raw material in the banking industry. It

can be a powel-fill rneans of creating debt capacity and lenders are benefited out of

deposit mobil~sation to improve their performance. Institutions providing only credit

may incl-ease their services by offering deposits accounts facilities in order to further

broadening their business ( Pischke, 1991). Chandavarkar (1965) observed that rural

moneylenders did not generally accept deposits but they lend out their own funds. But

urban moneylenders accept deposits and lend money.

Kr~shnan (1979) argued that the lending and deposit taking activities of ICMs

were generally evidenced by legally enforceable formal commitments. These formal

commitments were however confined to the minimum. Rajashekar (1988) gave an

account of the types of credit form the public, in the year 1984-85 in Karnataka.

Table 2.8 Types of Deposits from Public (1984-1985)

~ ~ d ~ o s i ts Amount (Rs in Lakhs) Percentage 1

-- I Total 34.75

I Source: Rajashekal-( 1988)

I

Miracle et.al. (1980) found that mobile bankers were often ambulatory

operating in African market places. The banker kept a deposit of borrower and

extended cl-ctiil to the depositors sometimes to an amount that is a multiple of the

amount they hird on deposit. Table 2.9 shows the sources of funds of selected

ir~termediaries arid chit funds received by Indian urban study.

13 4 83

Auto financiel-s 25 . 75

Table 2.9 Sources of Fund of Selected ICM intermediaries

Handloom 95- 100

financiers

funds Sector

Finance 9

corporation\

P m p a n i e s i 1 " Others include deposits and others Source: Indian urban study ((;hate, 1992)

(per cent of liabilities)

. - ~

Shroffs of Western 1 India 1 25

Bank loans

-

Others *

9 1

- 75

k Nayar ( 1980) argued that deposits were also mobilised by'the partners through

their influence ant1 not through interest rate competition. He clarified that savings

deposits with i~tdigenous banks tended to be more risky than those in formal banks

because risk di,gersification of informal sector was not usually good as that of the

formal banks. Madhur (1987) found that ICMs offered attractive deposits rates and

savers were allowed to withdraw even term deposits without much difficulties. Ghate

(1986) op~ned that solution to restrict the increasing activity of the ICM was to restrict

deposit-accepting act~vities. It virtually helped them to multiply their stronghold on

the economy

To surn up deposits are said to be the basic ground for creating loans by

informal c~edit ilarket intermediaries, Short-term or temporary deposits is the main

type of deposits in the informal credit markets. More about deposit mobilising

activities are explained in fifth chapter.

2.7 RELA'rION BE'I'WEEN FORMAL AND INFORMAL CREDIT MARKET

Many stt-dies have explicitly made it clear that there is an inter-relation

between forinal ;tnd informal credit rparkets. Kurup (1976) found that moneylenders

In a village i n Ker-ala lend money on the security of gold, replenished their funds by

pledging iheir gold with the forinal banks. Acharya and Madhur (1983) developed a

simple model ot the interaction between t& fqrmal and the informal credit markets

and found that a restrictive credit policy in the formal sector created excess demand

for funds 111 the i~il'ol-~nal sector. Thus the Mgng(gy and Credit Policy has a significant

effect oli the 1nl;ol-mill credit market.

Chandavarkar (1986) agreed with Acharya and Madhur (1983) that ICMs were

not insulated from impacl of aggressive credit controls and it was likely to be stronger

on the availability rather than on the price of informal credit. Larson (1988) surveyed

in the Philippines found that 70 per cent of the sample traders obtained 60 per cent of

their funds from formal sector banks. Jwa (1986) described how commercial banks in

Korea becamt: increasingly involved in channeling funds from lenders by seeking

deposits from them and using the deposits to make a loan to a borrower designated by

the informal sector.

'There were some debates on whether the formal and informal sectors-

substitutes and complements, or whether the growth of one sector was at the expense

of the other. A well known complementation was described by Cole and Park (1983)

relating to Korea in the 1960s and 1970s when large scale industry met its fixed

investment requirements from the formal sector but borrowed part of its working

capital requirernents from the informal sector.

The substitution relationship between formal and informal sectors had a major

implication on the efficiency of monetary and credit policy. Onchan (1985) observed

that when credrt was restricted during the financial crisis of the mid-1980s, interest

rates in the intormal sectors was showing an increasing trend. But Sundaram and

Pandit (1975) argued that the presence of highly elastic supplies of black liquidity in

the Indian economy swamped a weak upward pressure on interest rates transmitted

from the formal sector. Rahman (1992) was of the view that absolute growth and even

the relative growth of the informal financial sector overtime was due to the growth of

the formal sector. Alan1 (1989) found that significant part of the loans extended in the

formal sector found its way to the informal sector through on lending by the formal

sector borrowers.

Vongpradip (1985) claimed that in Thailand the source of 48 per cent of the

subscriptions in business Roscas was the formal sector itself, with participants

borrowing from the banks to finance their subscriptions. Geron (1988) and TBAC

(1981) study revealed that, informal lenders used formal sector funds in most of the

lending programmes. Bouman and Houtman (1988) obtained data to support the claim

that unregistered pawnbrokers obtained refinancing from registered pawnshops by

repledging articles with them. One of the best examples of flow of flows from the

formal to the informal sector in urban credit was the refinancing of the operations of

Shikapul-i (Multani), Shroffs (indigenous) in India through the rediscounting of the

operations of thzil- bills by the co~nmercial banks. (Ghate, 1992).

There is a complen~entary and substitute role between formal and informal

credit markets. The borrowers who have acquired loans from the formal sector also

acquire loan frorn informal sector. On the other hand borrowers who find difficulty in

getting credit from formal may be getting easy access to the informal sector thus plays

a complementary role. The informal credit markets acquire funds from formal sector

and many intermediaries acquired loans or funds by repledging their security with the

formal banks.

2.8 TRANSACI'ION COST ADVANTAGES

'Tr;,n.;action costs are athnission tickets to financial markets. They are the costs

of establish~ng .~nd conducting financial relationship. They include costs on

rr~lbrmation gathering, security arrangements, to protect cash documents and other

data recording ,iystern for transactions, processing cost of funds and bad debts. There

are three kinds ~ol'costs, which increase the total transaction costs.

(i) non-interest charges (ii) loan application procedures (iii) travel expenses and time

for promoting and following up the application . These overall costs of formal

borrowing made informal credit more attractive to many small borrowers (Shajahan,

1968). Miracle (1973) revealed that costs in the commercial segment of the informal

capital market were low because it was extremely decentralised system of dispensing

credit.

Madhur and Nayar (1987) and Kotwal (1989) brought out that transaction cost

in the ICM was lower than that of formal banks. Mujumdar (1991) found that degree

of decentralisation in procedures of sanctioning loans through cutting down the tiers

of hierarchy of sanctioning authorities also contributed to such reduction in cost. The

transaction cost provided plausible explanation for difference in lending patterns by

formal and informal banks (Bhat 1978, Bhat and Roe 1979, Saito and Willaueva

1978, Mampilly 1980 and Pischke 1991) made it clear that administration costs i n

ICM were generally small. The incremental cost of gathering information and

collection of debts was also small. Schrader (1992) observed that banks had no local

advantages with regard to sub-branches on the local level and lack of information on

locale. This makes the difference between formal and informal in regard to their

transaction cosl

To sum up, informal credit markets are at an advantageous position in lending

out money by making least cost. Borrowers approach the ICM due to the speedy

disposal of their- loan application, even though they charge high rate of interest.

Besides, LCM have localised advantages with regard to information on nature of

borrowers.

2.9 INFORMAL CREDIT MARKETS AND URBAN INFORMAL SECTOR

Most of the studies on informal sector proved that the most important

constraint faced by the entrepreneurs in the informal sector activity was the non-

availability o l capital. (Patrick, 1999) The formal sector banks may not extend credit

facilities to them since they are not meeting the basic requirements to get credit

facilities. They lend money on the basis of collateral. Since informal sector have no

such collateral to offer and they find out alternative sources of credit, to meet their

working capical as well as their daily needs. It is estimated that informal sector

depended mainly on informal credit market funds. They extend types of credit

facilities depending on the need and they need to satisfy little requirements compared

to that of formal sector. The main advantage was the rapidity with which it can

provide money with little or no collateral (Timberg and Aiyar, 1984).

Rahman (1992) observed that the size of the ICM in urban areas was partly

depended on how much amount each informal sector participant bought unsecured

without tying up their stocks as collateral. A study conducted in Dhaka showed that

the percentage of informal sector borrowing to finance the purchase of raw materials

was anywhere between 50 per cent and 100 per cent . Of late, the informal credit

market is gaining a commanding position and unprecedented growth due to the

uniqueness in extending credit facilities Lo the needy. This topic is dealt in detail in

lhe fifth chapter.

2.10 RESTRICTIVE MEASURES AND INFORMAL CREDIT MARKETS

There are a number of restrictive measures suggested by researchers to control

and regulate [he activities of the informal credit markets, as it seems to endanger the

working of the financial system as a whole. Their actual nature of working and the

volume of business are still unexplored due to the unaccounted nature of their

activities.

Holst i 1985) suggestkd three approaches to bring informal and formal sectors

close together. The first approach was called the traditional approach and it was

intended to formalise the informal credit markets. The second approach was called

the socio-economic approach and it accepted ICMs and tried to retain its strong role in

the economy. Middle-of-the-road approach suggested the co-existence of both

financial sectors and recognised the role played by the ICM in a country's financial

sector.

The mere lack of official regulation is often considered to be a merit to the

undesirable and unaccounted nature of their activity. Efforts are therefore put into

considering legislative and other means of reducing or eliminating informal activity

rather than underslanding the growth and implications of the existence of these

markets. These markets are regarded as a necessary evil and ought to be controlled

according to many policy makers. Attempts to control these ICMs have not achieved

the desil-ed effect and sometimes i t served only to encourage further innovation in

such markets. (hnsequently overtime there has been a growing acceptance of the

need to understand the economic significance of the markets.

Nathan (1980) asserted that economists had generally criticised these

regulations as i t is detrimental to low income consumers because financial institutions

under binding Interest rates tended to allocate credit to most credit worthy borrowers,

who generally belonged to middle or high income groups.

Virmani (1982) made it clear that to eliminate imperfection in the capital

market the government should extend interest and lump sum subsidies to the banking

sector and it would help reduce collateral requirements and are able to improve

efficiency in the capital market. Ghate (1986) was of the view that much of the

informal activrty resulted from regulation in the formal markets. Fry (1988) opined

that it was natural to expect that the informal sector would shrink with financial

liberation or deregulation. Madhur and Nayar (1987) suggest that the role of informal

credit markets should be cut down by extending the services of formal sector to areas

which are hither to be served by informal credit agencies and simultaneously bringing

more and more informal wedit agencies under government rules.

Pischke (1983) opined that the quality and prices of ICMs could be improved

through increased competition between formal and informal sector. In this connection

Mujumdar (1991) asserted that formal sector had to graft the virtues of an informal

credit system such as simplicity, flexibility and low cost profile. It is also argued that

ICMs were not competitive or that they would become less and less important as

formal credit market develop. Gill and Singh (1997) were of the opinion that access to

credit should be made easier even at higher rate of interest by formal sources and

l'orrnal sector should shift from land to crop as collateral. But since the activities of

lCMs are secret and unaccounted the suppression or regulation of moneylenders may

riot bring much success.

2.11 CONCLUSION

An overview of informal credit markets given above makes it clear that size

and structure of informal credit markets seems differently in different countries. It is

proved in the context of the analysis of segmentation that the classification of

informal credit market into sub-markets was done according to the financial structure

of each country. In other words what has been the classification in one particular

market is not quite same in the other. Hence the need to give a working definition of

informal cred~t market in the study area is essential. The conceptual framework and

working definition will explain various segments in informal credit markets, both

legal and illegal.