information brief

TRANSCRIPT

INFORMATION BRIEF

1

LEAD MANAGERS & ARRANGERS

BOOK RUNNER

All communication, inquires and requests for information relating to the IPO of Hascol Petroleum Limited should be addressed to:

Umair Aijaz, FCCA Liaquat Ali, FCA SVP / Head Partner Investment Banking Avais Hyder Liaquat Nauman Chartered Accountants AKD Securities Limited Tel: +92-21-35655975 Tel: +92-21-35863512 Fax: +92-21-35655977 Fax: +92-21-35867992 E-mail: [email protected] E-mail: [email protected]

Mohammad Yasir Khan Syed Saquib Moiz Senior Associate Assistant Manager Investment Banking Avais Hyder Liaquat Nauman Chartered Accountants AKD Securities Limited Tel: +92-21-35655976 Tel: +92-21-35371303 Fax: +92-21-35655977 Fax: +92-21-35867992 E-mail: [email protected] E-mail: [email protected]

INFORMATION BRIEF

2

DISCLAIMER

This Information Brief (“IB”) has been prepared by AKD Securities Limited (“AKDS”) Avais Hyder Liaquat

Nauman Chartered Accountants (“AHLN”) (hereinafter referred to as Joint Lead Managers & Arrangers).

The information provided and opinions herein have been compiled or arrived at based upon information

obtained from Hascol Petroleum Limited (“HPL” or the “Company”) documents and / or

communications and / or other sources believed to reliable in good faith. Although, the information has

been verified, to the extent possible, we make no expressed or implied representation or warranty as to

its accuracy, completeness or correctness.

The information is not meant to be a substitute for the recipients’ personal judgment. All such

information, representation and opinions contained in these documents assume certain economic

conditions and industry developments and constitute only current scenarios. The recipient of this

information is cautioned to exercise his / her own independent judgment and analysis at all times.

This IB includes certain statements, estimates, analysis and projections with respect to the anticipated

future performance of HPL. Such statement, estimates and analysis reflect certain assumptions

concerning the anticipated result, which assumption and / or anticipated results may or may not prove

to be correct. Neither the Joint Lead Managers, nor any of their affiliates have independently verified

these estimates, analysis and projections and accordingly they do not express any opinion or provide

any form of assurance with regard to such estimates, analysis and projections.

The Joint Lead Managers expressly disclaim any and all liability that may be based on any errors or

omissions from, or mistake in assumptions with respect to any information, estimates, analysis or

projections contained in this IB or any other written or oral communication transmitted to any potential

investor in the course of its evaluation of the possible investment.

INFORMATION BRIEF

3

Table of Contents

Serial Contents Page #

1 Transaction Overview 04

2 OMC Sector Dynamics 06

3 Hascol Petroleum Limited 10 4 Profile of Directors 20

5 Investment Rationale 24 6 Management Projections & Valuation 29

INFORMATION BRIEF

4

SECTION I

TRANSACTION OVERVIEW

INFORMATION BRIEF

5

Transaction Overview

The purpose of this Information Brief (“IB”) is to solicit the interest of potential institutional and

individual investors for participation in the Initial Public Offering of Hascol Petroleum Limited (“HPL” or

the “Company”).

The Company intends to issue 25 million Ordinary Shares (27.59% of post-IPO Paid-up Capital) through

an Initial Public Offering via the Book Building process at a Floor Price of PKR 20.00 per share. Moreover,

a total of 18.75 million Ordinary Shares (75% of the Issue) will be issued in the Book Building portion and

subsequently 6.25 million Ordinary Shares (25% of the Issue) will be issued in the General Public portion

at the Strike Price determined via Book Building.

HPL was incorporated in Pakistan as a Private Limited Company on March 28, 2001 and was converted in

to a Public Unlisted Company on September 12, 2007. The principal business of HPL is distribution and

marketing of petroleum products along with blending and marketing of foreign branded lubricants

"FUCHS". The Company obtained its oil marketing license from the Ministry of Petroleum & Natural

Resources in 2005 while the commercial operations were initiated in September 2005.

The purpose of this Initial Public Offering is to utilize the raised proceeds in completion of a storage

facility at Machike in the province of Punjab. Further to this, the proceeds would also be used for the

construction and commissioning of 50 retail fuel outlets.

It is also pertinent to highlight that prior to the IPO a pool of strategic investors have purchased

3,875,000 Ordinary Shares of HPL (5.91% of the existing total paid-up capital) from a few existing

shareholders of HPL at PKR 25.00 per share that is at a 25% premium over the floor price of PKR 20.00

per share. This clearly portrays the level of confidence that investors have on HPL’s growth trajectory.

HPL Flagship Site - Sharah-e-Faisal, Karachi

INFORMATION BRIEF

6

SECTION II

OMC SECTOR DYNAMICS

INFORMATION BRIEF

7

Domestic Oil Marketing Industry Overview

There are thirteen Oil Marketing Companies (“OMC”) operating in Pakistan including foreign and

domestic players. That said, close to 90% of the market is dominated by four oil marketing companies

with state-owned PSO having the largest market share at 63%. Among these thirteen OMCs there are

two relatively new companies, namely Total Parco Pakistan Limited and Hascol Petroleum Limited that

have emerged as active players and are rapidly gaining further market share.

Following are the current market shares of all OMCs operating in Pakistan:

Company Market

Share (%) Listing Status

No. of Retail Outlets

Market Price*

Pakistan State Oil 63.30 Listed 3,760 PKR 345

Shell Pakistan Ltd 9.90 Listed 798 PKR 210

Attock Petroleum Ltd. 9.50 Listed 362 PKR 508

Chevron Pakistan Ltd. 4.40 Branch Office 518 -

Total-Parco Pakistan Ltd. 3.80 Non Listed 260 -

Hascol Petroleum Ltd. 2.40 Under Listing 210 N / A

Byco Petroleum Ltd. 1.60 Listed 219 PKR 9

Bakri Trading Co. Pakistan (Pvt.) Ltd. 1.60 Pvt. Limited 47 -

Askari Oil Services (Pvt.) Ltd. 0.14 Pvt. Limited 294 -

Overseas Oil Trading Co. (Pvt.) Ltd. 0.10 Pvt. Limited 109 -

Zoom Petroleum (Pvt.) Ltd. 0.10 Pvt. Limited 12 -

Admore Gas (Pvt.) Ltd. 0.00 Pvt. Limited 442 -

Pearl Parco (Pvt.) Ltd. 3.16 Pvt. Limited (Non OMC)

0 -

(Source: OCAC Oil Report Oct- 2013)

*Price quoted as at January 16, 2014

Oil marketing companies have three primary drivers of earnings which include product inventory and

resulting inventory Net Realizable Value (“NRV”) adjustments, marketing margins and overall sales

volumes. While marketing margins are regulated and NRV adjustments on inventory are a function of

international oil prices, OMC strategy to increase core earnings focuses on increasing volume and

expanding market share.

While OMC volumes have increased at tepid 5-year CAGR of 1.6%, earnings have posted a volatile trend

with a CAGR of 2.3%. Earnings volatility is largely due to: 1) NRV adjustments on inventory due to

changes in crude oil and refined product prices, 2) PKR depreciation with SBP rebuffing FX cover for oil

marketing companies since 2009, 3) higher financial charges due to working capital requirements to

finance circular debt and buildup in receivables and 4) interest income/expense on delayed payments

due to circular debt.

Pakistan's oil & gas landscape is divided between up, mid and downstream sectors within the regulatory

ambit of the Ministry of Petroleum and Natural Resources. Pakistan's oil marketing and distribution

INFORMATION BRIEF

8

however is undergoing a deregulation phase within the backdrop of increasing volume demand and

higher reliance on imported products. Consumption of petroleum products has increased at a 1% CAGR

over the last 10 years, led by expanding rural incomes and per-capita incomes. This is despite

cannibalization with the trend in shift to Compressed Natural Gas (“CNG”) as a transport fuel up till

FY12, which has reversed of late with a severe shortage of natural gas in the country.

Pakistan's oil demand is expected to rise by approximately 7% during the current fiscal year (2013-14)

ending June 30, 2014 on year-on-year basis. The demand would touch 21 million tons against 19 to 20

million tons, on the back of closure of CNG stations and resolution of circular debt problem.

Over the last few years, POL products demand rose by an average 3%to4% per year, but if the country's

growth rate managed to remain between 5% - 6% during this year along with the closure of CNG

stations in Punjab then the subsequent increase in demand of petroleum products is likely increase

rapidly.

The country is a huge oil guzzler as more than 80% of the total demand is either imported in the form of

Crude or Refined products. The product slate is dominated by 9 million tons of Fuel Oil (including 4.5

million tons produced locally) followed by High Speed Diesel with total consumption of 7.5 million tons

(including 4 million tons of imported products). With the shortage of CNG in the market the Motor

Gasoline (Petrol) market has almost doubled from 1.2 million tons to 2 million tons.

With domestic refining capacity at 13.15mn tons per annum, Pakistan produces approximately 9.5mn

tons while annual consumption is close to 20mn tons per year. The deficit is primarily for fuel oil, high

speed diesel and more recently motor gasoline.

At present there are 6 major oil refineries operating in the country:

UNIT: M. Tons

Oil Refineries Capacity Production

Pak Arab Refinery Limited ("PARCO") 4,500,000 3,216,416

National Refinery Limited ("NRL") 2,710,500 1,834,845

Attock Refinery Limited ("ARL") 1,916,500 1,710,000

Byco Petroleum Pakistan Limited ("BPPL") 1,740,500 120,332

Byco Oil Pakistan Limited ("BOPL") – Under Commissioning 5,800,000 -

Pakistan Refinery Limited ("PRL") 2,298,500 941,272

Regulatory Landscape for OMCs:

Over the last decade, oil marketing and distribution has been semi-regulated with marketing margins set

by the Government of Pakistan (“GoP”) while price setting at the forecourt retail level has moved back

and forth from regulatory ambit. In 2000 the market for residual fuel oil and industrial products mainly

used for power generation was completely de-regulated which was followed by GoP’s reforms across

key areas of the economy. While marketing margins remain regulated, OMCs in Pakistan focus on

INFORMATION BRIEF

9

increasing core earnings by volumetric growth that eventually boasts their respective market share and

profitability.

In order to stimulate foreign investment, marketing margins for OMCs were revised from an initial

0.51%-2.17% to 3% for all regulated products. Margins were further enhanced to 3.5% in July 2002 and

Pakistan's 2nd largest volume generating product HSD (accounts for 35% of total petroleum products

consumption today) was de-regulated at the principal stage in view of the domestic production deficit.

OMCs were allowed to import HSD and set the retail level price of the product with prices uniform

across the country through a system known as Inland Freight Equalization Margin (IFEM) evenly

spreading the distribution and transport costs of the products across the country onto end retail prices.

During 2002 to 2008, petroleum product pricing included ex-refinery prices based on import parity, with

dealer and distributor margins and taxes taking prices to the ex-depot level. Prices were independently

regulated by the Oil and Gas Regulatory Authority (“OGRA”). Post 2008, within the backdrop of firmly

high oil prices, the GoP reinstated the reform process to further deregulate the sector.

Marketing margins were changed from a percentage to an absolute basis in 2010 leading to a reduction

in product distribution margins by 20%-25% across the regulated product range. In 2011, the GoP

revised upwards margins on premium motor gasoline and HSD by 32% and 30%, respectively, to

improve core profitability of downstream marketing within the backdrop of circular debt exposure and

PkR depreciation. Imports of premium motor gasoline were deregulated at the principal stage i.e.

allowing OMCs to set the ex-refinery and ex-depot price based on actual product imports excluding

gallop tenders while the GoP continued to monitor HSD prices at the ex-refinery level for refiners. In

2012, the GoP for the first time deregulated HSD prices at the ex-refinery level bringing them in-line

with actual OMC import prices as set by Pakistan State Oil Company Limited (state owned and is the

largest oil marketing company in Pakistan). Currently, margins on HSD and MS are being considered for

an upward revision by the GoP given inflationary pressures amid repeated requests by the industry.

INFORMATION BRIEF

10

SECTION III

HASCOL PETROLEUM LIMITED

INFORMATION BRIEF

11

Hascol Petroleum Limited

HPL was incorporated in 2001 under the Companies

Ordinance, 1984 primarily to take advantage of the

petroleum sector deregulation and undertake a program for

owning, leasing and renting oil storage facilities as well as

importing petroleum products for its own account.

In February 2005 HPL was granted a full marketing license by

the Government of Pakistan and since then, HPL has been

engaged in developing a retail network and storage facilities

under the Hascol brand and by 31st December 2013 the

Company had commissioned approximately 210 retail outlets

across Pakistan and this number is expected to reach 291 by

the end of 2016.

The Directors and sponsors of the company have decades of

multinational companies experience in Oil Trading, Retail

Management, Marketing & Supply Chain Management.

HPL management team comprises of well experienced staff

from each segment of the oil industry who have worked in

local and multinational oil companies for many years and

have ability to do things right.

Pattern of shareholding of HPL as at 31st December 2013 is as follows:

Serial Name of Shareholder Shares %

1 Mr. Mumtaz Hasan Khan - Chairman & CEO 34,387,567 52.42

2 Fossil Energy (Private) Limited 12,175,713 18.56

3 Marshal Gas (Private) Limited 8,500,396 12.96

4 Other Shareholders 10,536,324 16.06

Total Shares 65,600,000 100.00

As at December 31, 2013 HPL’s investment in its fixed assets amounted to PKR 2,315 million while the

Company operates through 210 retail fuel stations wide-spread across Pakistan. Further to this, HPL has

constructed and commissioned a state of the art storage installation at Shikarpur while another purpose

built installation is currently being constructed at Machike.

HPL’s product mix includes petroleum products such as Motor Spirits (“MS”), Furnace Oil (“HSFO”), High

Speed Diesel (“HSD”), Jet A-1, Liquid Petroleum Gas (“LPG”), Super Kerosene Oil (“SKO”) and Lubricants.

The Company is currently offering Petrol, Diesel under the Company’s own brand name as “Tiger Super”

and “Rocket Diesel” and lubricants under the brand name of FUCHS.

INFORMATION BRIEF

12

The Code of Corporate Governance applicable to listed companies is fully in place at the Company and

the following Management Committees and Board Committees actively function towards the

sustainability and growth of HPL:

Product Line:

HPL’s product mix includes petroleum products such as Motor Spirits (“MS”), Furnace Oil (“HSFO”), High

Speed Diesel (“HSD”), Jet A-1, Liquid Petroleum Gas (“LPG”), Super Kerosene Oil (“SKO”) and Lubricants.

The success of an OMC is dependent on how well its supply chain has been established. The presence of

storage facility at each discharge point of Pak Arab Pipe Line Company System is a necessity. HPL has

very successfully developed supply depots, either through its own sources or through third party

arrangements.

Supply chain is a lifeline of any industry throughout the world. It plays an essential role in ensuring that

the right products are available at the right places at all times; specially, in the country like Pakistan

where the gap between supply and demand is continuously widening.

Storage Facilities:

HPL has developed state-of-the-art storage facilities at

strategic locations that fully cover its retail network. Out of

the 5 functional facilities, the Shikarpur storage facility is fully

owned and operated by HPL while Machike storage facility

would be the second facility to be owned by HPL.

INFORMATION BRIEF

13

The existing storage facilities currently operating under the banner of HPL including the under

construction Machike Facility are as follows: Unit in MT

Serial Facility Ownership Capacity

1 Port Qasim Long-term agreement - VTT Port Qasim (Pvt.) Ltd. 32,400

2 Kemari Long-term agreement - Al-Raheem Trading 12,150

3 Kemari Import Terminal Long Term Lease Agreement with Al-Abbas Group 15,000

4 Shikarpur HPL Owned 6,500

5 Machike HPL Owned (Under Construction) 6,500

6 Amangarh Long-term lease agreement - an option to buy 1,500

In order to further enhance its capacity the Company is in the process of acquiring a land at Mehmood

Kot, Punjab adjacent to Pak-Arab Refinery Limited. This will facilitate the Company to cover its supply in

the Southern Punjab envelope.

INFORMATION BRIEF

14

Efficient Logistics Network:

HPL’s logistics network provides the Company with an

efficient value chain that drives the Logistics department is

the backbone of an oil marketing and distribution company.

Hascol Petroleum Limited does not compromise on quality

and quantity of petroleum products.

HPL is maintaining its logistics policy wherein we ensure the

deliveries of safe and sound condition to the valued

customers. Tank Lorries registered with HPL are duly

calibrated by weights & measures, and designed as per rules

required by 'OGRA' and 'Ministry of Petroleum and Natural

Resources'.

HPL has got 19 registered contractors maintaining a fleet of

1,300 Tank Lorries for Black Oil and 350 Tank Lorries for

White Oil.

HPL all the tank lorries are registered in HPL state of the art

ERP system JD Edwards to control the logistics data and

product movement and time log, as well. The cartage

contractors have to provide the tank lorries as per demand

of HPL Cartage Agreements.

IT Infrastructure:

In 2013 HPL successfully implemented JD Edwards ERP software

which is an integrated system comprising of the following six

modules:

Financial

Procure to Pay

Order to Cash

Inventory Management

Transportation

Advance Pricing

Now all Hascol Installations, depots and warehouses are

connected with the Hascol Head Office in Karachi enabling

Hascol real time information for business controls efficient

customer service and structured MIS of management decisions.

INFORMATION BRIEF

15

All of HPL regional offices, Installations & depots are connected online for the Video Conferencing with

HPL management at Head office.

Hascol has built its own state-of-the-art data center for the centralized and safe storage of Company's

valuable data with inside and outside firewalls to ensure data security and safety.

Retail Outlets:

HPL has a large network of retail outlets in all corners of the country. With over 210 retail outlets in all

four provinces of the country HPL has invested more than PKR 2 billion in their expansion venture

through dealers and its own investment.

Attached to the retail outlets HPL is also operating a network of convenient store with a brand name

"Hasmart". HPL have 42 Hasmart, 40 Tyre - Care and 15 Express Wash nationwide to cater the needs of

its customers.

Automax LPG (Liquefied Petroleum Gas) is an economical,

safe and environment friendly alternate to CNG, Petrol

and Diesel. HPL is the first oil marketing company to

develop LPG auto station and started dispensing LPG

through its Flagship retail outlet at Sharah-e-Faisal with a

brand name AUTOMAX. At present 15 AUTOMAX stations

are in various stages of approval with the Government of

Pakistan.

INFORMATION BRIEF

16

The detail of current retail outlets with respect to location is as follows:

Province Retail Outlets %

Sindh 72 34.30%

Baluchistan 7 3.30%

Punjab 98 46.70%

Khyber Pakhtun Khua 30 14.30%

Azad Jamu & Kashmir 3 1.40%

Total 210 100.00%

FUCHS – HPL’s Lubricants:

HPL has a sole strategic agreement with FUCHS international to manufactures/import, distribute and sell

FUCHS branded lubricating oils and greases in Pakistan. A company that combines tradition with

progress is best poised to meet the challenges of the future.

HPL is the only local company with International Lubricant Brand

.i.e. FUCHS Germany that gives a great strength to HPL's lubricants

product line. In addition to its strong sales through 210 retail

outlets, HPL also operates in high street market, commercial and

industrial sector. It is also the market leader for supplies to

Pakistan Army with sales well over PKR 1 billion (2.5 million liters).

HPL has the proprietary product rights to cater for lubricant for

Pakistan Army's indigenous tank, Al-Khalid.

INFORMATION BRIEF

17

Historical Financials of HPL (2011 – 2013):

(PKR in millions)

Description 2013 2012 2011

Fixed Assets 2,286 1,724 877

Current Assets 6,707 2,595 1,136

Equity (Including Revaluation Surplus) 1,444 1,065 460

Current Liabilities 7,630 3,067 1,686

Sales (in Thousand Liters) 619,923 341,738 259,910

Sales 57,441 29,775 19,584

Gross Margin 1,320 996 699

Operating Profit / (Loss) 548 393 257

Finance Cost 110 101 202

Profit Before Tax 438 292 43

Profit After Tax 392 218 82

Earnings per Share 5.97 3.33 1.94

Break-up Value per share (with Revaluation) 22.02 16.24 7.01

Break-up Value per share (w/o Revaluation) 16.55 10.20 6.71

Current Ratio 0.88:1 0.85:1 0.67:1

*Financial Year – January to December

INFORMATION BRIEF

18

Key Agreements:

1. Currently HPL has fuel supply arrangements with all

refineries in Pakistan.

2. HPL has hospitality agreement with PSO for the storage

and handling of products at, Machike, Chakpirana and

Sihala.

3. HPL is engaged in a sole strategic agreement with

FUCHS International for the manufacture, import

distribution and sale of their products in Pakistan.

4. HPL is in contract with OOPL as it blending partner for

lubricants in Pakistan.

5. HPL is in contract with Sui Sothern Gas Company (“SSGC”) for the supply of LPG.

6. HPL is in contract with Marshal Gas (Pvt.) Limited for the supply of LPG.

7. HPL has signed a Technical Services Agreement (“TSA”) with an International Operator, to start

aircraft refueling services in Karachi.

Principal Purpose of the IPO:

The principal purpose of the Issue is to inject additional equity into the Company mainly for utilization in

the completion of Machike Storage Facility in Punjab and for setting up new retail outlets all across

Pakistan. As per the Company’s plans, out of the total equity raised via issuance of 25 million shares at

PKR 20/- per share:

PKR 200mn will be utilized for capital expenditure on the completion of Machike Storage

Facility which includes purchase of pipelines, gensets, pumps, electrical equipment etc.

PKR 100mn will be utilized for the setting up and commissioning of new / under

construction retail fuel stations

The remaining proceeds will be utilized for working capital requirements of the Company

Future Prospects:

Pakistan economy is in a growth mode and energy is a very essential ingredient, more trucks will move

across the country for trade and there will be more cars and motorcycles on the road.

The expected growth rate of the of the economy is between 3% to 4% and the in efficiency of state

owned OMC will create a space for new market entrant with thin cost structure, efficient supply chain

management and good corporate governance.

HPL has doubled its sales volume and profitability on year to year basis. During the last three years this

growth has resulted in a market share from 1% to 2.4% up to October 2013 (Source OCAC Report), from

2014 and onwards within 2 years the company has a target to achieve a volumes of 1,000,000 MT with a

market share of 5%.

INFORMATION BRIEF

19

This growth will be achieved by HPL backed by the following strategic steps:

Completion of Machike Storage Facility

Development of a Storage Facility at Mehmood Kot

Depots at Sahiwal and Shershah

Increase in retail outlets from 210 to 291 by the end of 2016

Development of Aircraft Refueling Station (JET-A1) at Karachi Airport. After PSO, HPL is the only

OMC that has a TSA with an International Operator to sell Jet A-1 to airlines

Development of a Lubricants and Grease Plant by end of 2016

INFORMATION BRIEF

20

SECTION IV

PROFILE OF DIRECTORS

INFORMATION BRIEF

21

Profile of Directors

Mr. Mumtaz Hasan Khan– Chairman & C.E.O

Mr. Mumtaz Hasan Khan has over 50 year of experience within

the oil industry. He started his career with Burmah Shell Oil

Storage and Distribution Company in May 1963. In January

1976 Mr.Mumtaz resigned from the post of International Sales

Manager to join Pakistan Services Limited as Managing

Director. Pakistan Services Limited was the owning company of

four Intercontinental Hotel (now known as Pearl Continental

Hotel) in Pakistan at that time. In 1980 Mr. Mumtaz left

Pakistan Services Limited and moved to London.

He established Hascombe Limited, which started trading in Crude Oil and Petroleum Products.

Hascombe bought petroleum product from Middle Eastern sources and sold to international trading

companies like Shell and Elf. Hascombe was also a major supplier of petroleum products to Pakistan

during 1991 till 1996.

In 2005 Hascol was granted an oil marketing license by the government of Pakistan in Pakistan. Hascol

has established a network of 200 Petrol Pumps all across Pakistan including Azad Jamu and Kashmir.

Mr. Mumtaz Hasan Khan is currently also serving as Chairman of Sigma Motors (Sole distributor of Land

Rover vehicles in Pakistan).He is a Trustee of the Foundation of Museum of Modern Art (FOMMA)

located in Karachi and the member of the Expert Energy Group which prepared Pakistan’s first

Integrated Energy Plan in 2009.

INFORMATION BRIEF

22

Dr. Akhtar Hasan Khan – Director

Dr Akhtar Hasan Khan is a former civil servant. He retired as Secretary Planning for the Government of

Pakistan. Dr. Akhtar holds a Masters in Public Administration from the University of Harvard and a PHD

in economics from the TUFFs University in USA. Dr. Akhtar served as Secretary Education, Additional

Secretary Finance, Additional Secretary Commerce and additional secretary ministry of production. Dr.

Akhtar has served on the board of public organization such as Pakistan International Airline, National

Development Finance Corporation, Pakistan Automobile Corporation and Chairman of the Pakistan

Ghee Corporation. Dr Akhtar is the author of several publications; his recent book was called “the

impact of privatization in Pakistan”. He is a Director of Sigma Motors Limited.

Mr. Najmus Saquib Hameed – Director

Mr. Najmus Saquib Hameed is the honorary Vice Chairman and C.E.O of Layton Rahmatullah Benevolent

Trust (LRBT). LRBT is one of the largest charitable organizations in Pakistan providing free eye care to

over 2 million patients through a network of 17 hospitals annually. He has over 47 year of experience in

Senior Management position with multinational organization such as Unilever and Pakistan Tobacco

where he retired as Chairman of the Company. Mr. Najmus Saquib holds a Master in International

Relations and was a gold medalist at Institute of Business Administration (IBA). He has served as

Chairman of the Cigarette Manufacturers Association and past Chairman Board of Governor at the Indus

Valley School of Art and Architecture, Karachi. Mr. Najmus Saquib Hameed is currently serving on the

board of NIB Bank Limited and Sigma Motors Limited.

Mr. Farooq Rahmatullah – Director

Mr. Rahmatullah is law graduate from the University of Peshawar. He joined Burmah Shell and Oil

Distribution Company in 1968. Mr. Rahmatullah worked in various capacities with the organization i.e.

Chemical, Human Resource, Marketing, Supply, Distribution and Retail. In 1994 Mr. Rahmatullah was

transferred to Shell International London as Manager Business Strategy Division. He looked after various

portfolios covering 140 countries. In 1998 he was transferred back to Pakistan as Head of Operations

Shell Pakistan. Mr. Rahmatullah was also looking after Middle East and South Asia (MESA).In 2001 he

was appointed managing director Shell Pakistan Limited a post he retired from in June 2006.

Mr. Rahmatullah is credited with being the founding member of PAPCO (Pak Arab Pipeline Company

limited). He has also served as the Director General of Civil Aviation Authority, Chairman of the Oil and

Gas Development Authority, Chairman of LEADs. Since 2005 he has been chairman of the Pakistan

Refinery Limited. He is currently serving on the Board of Director of Faysal Bank Limited, Society of

Sustainable Development, and Resource Development Committee for the Agha Khan Hospital. He is also

the Group Founding Member of the Pakistan Human Development Fund and a member of National

Commission of Government Reform and Member of the Pakistan stone Development Company. He is

the Chairman of Pakistan Refinery Limited and Non-Executive Director of Faysal Bank Limited.

INFORMATION BRIEF

23

Mr. Liaquat Ali – Director

Mr. Liaquat Ali is a Chartered Accountant by profession and a fellow member of the Institute of Charted

Accountantsof Pakistan (ICAP). He has over 18 years of experience in leasing and investment banking

field and has completed numerous transactions including restructuring of companies, merger and

Acquisition.

Mr. Liaquat Ali is a member of one of the leading Chartered Accountant firm Avais Hyder Liaquat

Nauman Chartered Accountants (AHLN). AHLN is a member of RSM international which is the 7th largest

network of accounting and consulting firms in the world[1]. AHLN has offices in Lahore, Karachi,

Peshawar, Faislabad, Islamabad, Quetta and Kabul (Afghanistan). He is also a member of the benevolent

fund committee of ICAP.

Mr. Sohail Hasan – Director

Mr. Sohail is a Chartered Accountant and a member of the Institute of Chartered Accountants in England

and Wales and the Institute of Chartered Accountants of Pakistan. He was a partner in a leading

accounting firm A.F.Ferguson & Co for over 35 years and has also served as its senior partner. He has

served as the member of the Provisional Financial Commission Punjab and is currently a member of the

Corporate Law Review Commission of Pakistan. He is a Non-Executive Director of Habib Metropolitan

Bank Limited.

Mr. Saleem Butt – Chief Operating Officer& Executive Director

Mr. Saleem Butt has achieved a diversified 22 year career in Finance, Corporate Affairs, Supply Chain,

Sales, Management, Human Resource, I.T and ERP implementation. Mr. Butt started to work as a

Chartered Accountant for a firm which is now a part of Price Waterhouse Coopers. He then worked with

various Shell Group of companies in Pakistan and overseas for 14 years. He was then offered a position

with Emaar Pakistan a subsidiary of Emaar PJSC, U.A.E as Chief Operating Officer (COO).

Mr. Butt is a Chartered Accountant and holds a Bachelor Degree in Commerce from the University of

Karachi. He received his fellowship from the Institute of Chartered Accountants of Pakistan in 2004. He

also serves as non-executive director on the boards of Pakistan Refinery Limited, TRG Pakistan Limited

and Sigma Motors Limited.

INFORMATION BRIEF

24

SECTION V

INVESTMENT RATIONALE

INFORMATION BRIEF

25

Investment Rationale

Growth Story: HPL has taken a time span of approximately 8 years to turn itself into a fully developed

OMC. The sponsors of the Company have mostly invested the capital from their own resources and have

now made the company capable running as a profitable and sustainable entity which can clearly be seen

through the financial highlights of the Company.

The construction of back-end (storages) and front-end (retail outlets) facilities has been a game changer

for HPL as the functionality of these facilities have brought the Company’s sales volumes at an optimum

level and further volumes can be generated as well. In addition to this, the local and the international

brands such as FUCHS AG attached to the Company now carries significant business value and today HPL

is known for its quality products and services.

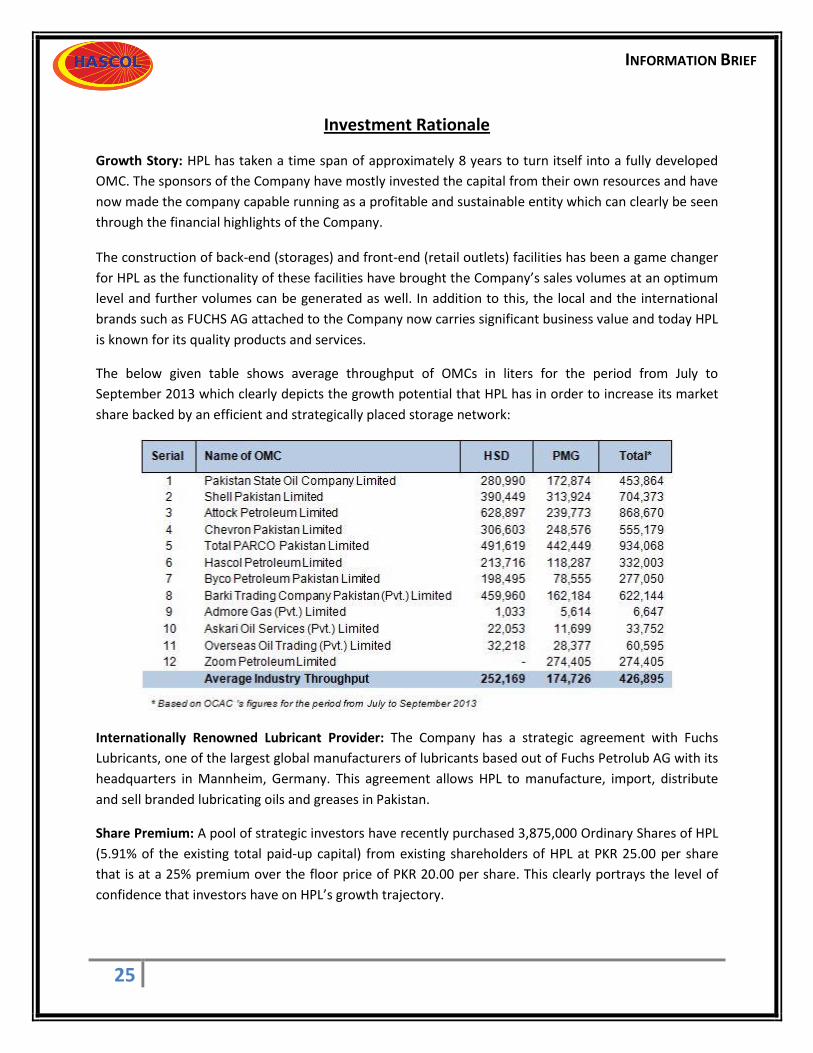

The below given table shows average throughput of OMCs in liters for the period from July to

September 2013 which clearly depicts the growth potential that HPL has in order to increase its market

share backed by an efficient and strategically placed storage network:

Internationally Renowned Lubricant Provider: The Company has a strategic agreement with Fuchs

Lubricants, one of the largest global manufacturers of lubricants based out of Fuchs Petrolub AG with its

headquarters in Mannheim, Germany. This agreement allows HPL to manufacture, import, distribute

and sell branded lubricating oils and greases in Pakistan.

Share Premium: A pool of strategic investors have recently purchased 3,875,000 Ordinary Shares of HPL

(5.91% of the existing total paid-up capital) from existing shareholders of HPL at PKR 25.00 per share

that is at a 25% premium over the floor price of PKR 20.00 per share. This clearly portrays the level of

confidence that investors have on HPL’s growth trajectory.

INFORMATION BRIEF

26

Fuel Supply Arrangements: HPL has established fuel supply arrangements, with all domestic refineries

including Pak-Arab Refinery, Attock Refinery, Pakistan Refinery Limited, Byco Petroleum Pakistan

Limited and National Refinery. Apart from the fuel supply arrangements, HPL has developed a well-

managed supply chain structure through which its products are transferred to all parts of the country.

The Company has also entered into the import market and has imported 3 cargos of Fuel Oil and Motor

Gasoline during the current year. The Company has also set up a fully integrated import supply chain at

both Kemari and Port Qasim.

Shield Against Circular Debt: HPL has carried a very defensive commercial sales strategy during the past

3 years due to the rising issue of circular debt pertaining to the Oil & Gas and Power sectors of Pakistan.

As an antidote to this risk, HPL has always secured its receivables from commercial sales to IPPs and

other debt burdened institutions through irrevocable financial instruments. As a result of these prudent

measures HPL has remained unharmed by the risk of circular debt and the resultant liquidity crunch

faced by most OMCs.

Strategically Placed Storage Facilities: The Company, under agreements with other OMCs, uses 5

different storage facilities that are strategically located in different oil supply hubs of the country. Apart

from this, HPL has recently commissioned its own storage Facility in Shikarpur, Sindh which is currently

being fully utilized by the Company while HPL will also commission another storage facility at Machike in

Punjab this year. The operational support of these purpose built state-of-the-art storage facilities will

provide significant volumetric growth in the sales of High Speed Diesel & Motor Spirit. With the shortage

of CNG in the country during the last 3 years the country-wide volume of Motor Gasoline has doubled.

HPL has hired a storage facility at Kemari on long-term basis to manage the imported products and

imported its first cargo in December 2013. The import facilities for fuel oil, motor gasoline and High

Speed Diesel have placed the Company strategically in a very strong position for the security of its

supplies.

Sponsor Profile & Management Prowess: The main sponsor of HPL, Mr. Mumtaz Hasan Khan, has an

experience of over 50 years in the Oil industry and has been associated with reputable brand names

such as Burmah Shell. Over the years HPL has gathered a team of well experienced team of individuals

who have significant expertise in the oil industry. The Company has a strong emphasis on recruiting and

retaining the best professionals who play the pivotal role in this business model. The Management has a

cumulative experience of 175 years pertaining to the Oil Marketing industry.

Recent Growth Track-Record: From 2010 onwards the Company has roughly doubled its sales volumes

at year on year basis. This growth has resulted in an increase of market share from 1.00% to 2.50% up to

October 2013. (Source: OCAC Oil Report)

Year Sales of HPL

2010 PKR 9,202,000,000

2011 PKR 19,583,000,000

2012 PKR 29,775,000,000

2013 PKR 57,441,000,000

INFORMATION BRIEF

27

The current network of the Company has the capacity to further enhance the sales volumes after

completion of the Machike Storage Facility based in Punjab.

Growing Retail Network: The Company has a wide-spread network of 210 retail outlets across Pakistan

through which POL products are sold. The company plans to add 50 more retail outlets by the end of

this year, moreover the Company plans to add 91 fuel stations by the end of 2016 which would further

boast HPL’s sales of HSD and MS. The province-wise break-up of HPL’s 210 operational retail outlets is as

follows:

Province No. of Sites Motor Fuels

Avg. Monthly Sale / Site

Quantity (Liters)

Punjab 101 111,619,392 92,095.21

Sindh 70 130,574,793 155,446.18

Khyber Pakhtun Khua 26 4,833,402 15,491.67

Baluchistan 07 3,596,000 42,809.52

Azad Jammu Kashmir 06 914,000 12,694.44

210 251,537,587 318,537

Attractive Floor Price: The floor price of PKR 20.00 per share represents an attractive discount of

64.70% on CY13 P/E Multiple of HPL i.e. 3.35 times versus the P/E Multiple of KSE-100 Index i.e. 9.49

times (Source: Bloomberg).

Moreover, we have also undertaken relative valuation based on comparison of HPL with leading oil

marketing companies of the country. For relative valuation we have considered Attock Petroleum

Limited, Pakistan State Oil & Shell Pakistan Limited. The following table highlights the financial highlights

and trading multiples of the above mentioned OMCs in comparison with HPL:

Indicators PSO SHELL APL HPL

Retail Outlets 3,760 798 362 210

Sales (PKR in 000') 1,294,503,247 244,316,875 191,181,800 57,441,365

PAT/ (LAT) (PKR in 000') 12,557,945 (2,082,531) 3,906,534 391,407

Shares (No. of shares) 246,987,217 85,609,886 69,120,000 65,600,000

EPS (PKR per share) 50.84 (24.33) 56.52 5.97

Market Price (As at 31-Dec-13) 333.22 190.43 499.69 20*

Shareholder's Equity (PKR in 000') 61,887,604 6,175,590 14,043,457 1,443,695

Book Value (PKR per share) 250.57 72.14 203.18 22.01

P/ E Ratio 6.55 N/A 8.84 3.35

P/ B Ratio 1.33 2.64 2.46 0.91

Financial Data Reporting Date 30-Jun-13 31-Dec-12 30-Jun-13 31-Dec-13

* Book Building - Floor Price

INFORMATION BRIEF

28

The floor price of PKR 20.00 per share represents an attractive discount of 56.49% based on CY13 P/E

Multiple of HPL of 3.35 times versus the Average P/E Multiple of the above mentioned OMCs of 7.70

times. Based on the above given peer comparison, HPL has an estimated value of PKR 45.94 when

viewed in line with the average P/E of 7.70x for PSO & APL.

Furthermore, when comparing the CY13 P/B Multiple of HPL of 0.91 times with the Average P/B Multiple

of the above mentioned OMCs of 2.14 times, the P/B Multiple presents a discount of 57.48%. Based on

the average P/B of 2.14x for the above mentioned OMCs the projected value of HPL is estimated to be

PKR 47.17.

Multiples Average Multiple

HPL (CY13) HPL’s Projected

Price

P/E 7.70x EPS PKR 5.97 PKR 45.94

P/B 2.14x BVPS PKR 22.01 PKR 47.17

INFORMATION BRIEF

29

SECTION VI

MANAGEMENT PROJECTIONS

&

VALUATIONS

INFORMATION BRIEF

30

Management Projections

2013 (A) 2014 (E) 2015 (E) 2016 (E) 2017 (E) 2018 (E)

Non Current Assets

Property, plant and equipment 2,308,238 2,587,971 2,922,970 3,193,316 3,119,369 3,026,241

Intangible assets 7,054 5,643 4,515 3,612 2,889 2,311

Long term deposits 32,372 25,898 20,718 16,574 13,260 10,608

Long term investment - - - - - -

Deferred taxation - net 354,491 319,042 287,138 258,424 232,582 209,323

2,702,155 2,938,554 3,235,340 3,471,927 3,368,099 3,248,484

Current Assets

Stock-in-trade 3,177,692 3,578,063 4,674,853 5,846,939 6,001,056 8,298,955

Trade debts 2,088,097 2,736,166 3,739,883 4,872,449 5,648,053 7,054,112

Loans and advances 464,647 441,415 419,344 398,377 378,458 359,535

Trade deposits and short term prepayments 40,585 44,644 49,108 58,929 70,715 84,858

Sales tax receivable 54 - - - - -

Other receivables 35,674 41,025 47,179 54,256 62,394 71,753

Bank balances 864,680 1,264,161 1,131,186 1,540,853 2,818,562 3,398,769

6,671,429 8,105,473 10,061,552 12,771,802 14,979,239 19,267,982

TOTAL ASSETS 9,373,584 11,044,027 13,296,892 16,243,729 18,347,339 22,516,466

Non Current Liabilities

Liability against assets subject to Finance Lease 73,685 - 20,520 18,399 16,813 4,508

Deferred Liability - Gratuity 50,174 57,700 66,355 76,308 87,755 100,918

Long Term Loan - Summit Bank (150) - - - - - -

Long Term Loan - PAIR (100) 58,333 25,000 - - - -

Long Term Loan FWBL - (200) 163,636 90,909 (0) - - -

Long Term Loan - PAIR (150) - 139,286 85,714 42,857 - -

Long Term Deposits 90,872 99,959 109,955 120,951 133,046 146,350

436,701 412,854 282,545 258,515 237,613 251,776

Current Liabilities

Current Portion of Liabilities Against Assets Subject to Finance Lease 46,987 31,482 - - - -

Finance Under Mark-up Arrangements 493,013 197,205 138,044 96,631 67,641 47,349

PAIR - (100) 41,667 - - - - -

HBL - (70) 70,000 - - - - -

PAIR - (350) - 145,833 145,833 175,000 175,000 175,000

Commercial Paper (75) 75,000 - - - - -

Commercial Paper (150) - 150,000 150,000 150,000 150,000 150,000

Trade & Other Payables 6,368,590 7,126,809 8,595,955 10,457,467 11,363,365 14,088,308

Accrued Interest 16,569 18,226 20,048 22,053 24,259 26,685

Sales Tax Payable - - - - - -

Provision for Taxation 381,362 407,479 455,107 379,015 337,495 368,977

Total Current Liabilities 7,493,188 8,077,035 9,504,988 11,280,166 12,117,761 14,856,318

TOTAL LIABILITIES 7,929,889 8,489,889 9,787,532 11,538,681 12,355,374 15,108,094

NET ASSETS 1,443,695 2,554,138 3,509,360 4,705,048 5,991,964 7,408,372

Shareholders' Equity

Share Capital 656,000 656,000 906,000 906,000 906,000 906,000

Further issue at Rs 10/ share (25m shares) - 250,000

Share premium - Old 3,300 3,300 3,300 3,300 3,300 3,300

Share premium of Rs 10/ share (25 m shares) - 250,000 250,000 250,000 250,000 250,000

Accumulated profits 426,019 1,038,712 1,996,185 3,194,123 4,483,290 5,901,949

Surplus on revaluation on fixed assets 358,376 356,125 353,875 351,624 349,374 347,123

1,443,695 2,554,138 3,509,360 4,705,048 5,991,964 7,408,372

HASCOL PETROLEUM LIMITED

PROJECTED BALANCE SHEETS

Balance Sheets

Amount in PKR '000

INFORMATION BRIEF

31

Description 2014 (E) 2015 (E) 2016 (E) 2017 (E) 2018 (E)

Sales - Gross 76,823,122 97,504,087 118,562,926 128,846,213 151,455,929

Sales - Net of Sales Tax 66,597,535 84,525,748 102,781,537 111,696,061 131,296,298

Cost of Sales (65,032,134) (82,566,407) (100,446,724) (109,148,115) (128,555,807)

Gross Profit 1,565,401 1,959,341 2,334,814 2,547,946 2,740,492

Selling & Distribution Expenses (621,784) (639,705) (705,548) (763,697) (797,313)

Administrative Expenses (229,706) (249,201) (275,858) (306,121) (340,398)

Operating Profit 713,910 1,070,435 1,353,407 1,478,128 1,602,781

Finance Cost (106,795) (101,692) (125,652) (154,395) (132,036)

Other Income 94,631 101,756 107,621 114,792 123,481

Profit Before Taxation 701,747 1,070,499 1,335,377 1,438,525 1,594,226

Taxation 89,053 113,027 137,438 149,358 175,568

Profit After Taxation 612,693 957,473 1,197,939 1,289,167 1,418,659

EPS 6.76 10.57 13.22 14.23 15.66

Profit & Loss Accounts

Amount in PKR '000

HASCOL PETROLEUM LIMITED

PROJECTED PROFIT & LOSS ACCOUNTS

GP Margin 2.35% 2.32% 2.27% 2.28% 2.09%

NP Margin 0.80% 0.98% 1.01% 1.00% 0.94%

Current Ratio 1.00 1.06 1.13 1.24 1.30

Breakup Value with Revlauation 28.19 38.73 51.93 66.14 81.77

Breakup Value w/o Revlauation 24.26 34.83 48.05 62.28 77.94

INFORMATION BRIEF

32

Valuation Snapshot

Risk Free Rate 11.50% 5 - Year PIB Rate

Market Risk Premium 6.00% Standard Convention by Consensus Analyst

Beta 1.07 Average OMC Beta (PSO & SHELL)

Cost of Equity 17.92% Ke = Rf + (Rm-Rf)Beta

Terminal Growth Rate 2.00% Sustainable Growth Rate

Tax Rate 35.00% Corporate Tax Rate

Cost of Debt 13.50% 1 - Year KIBOR + 3.00%

Debt to Equity 21.67% Debt to Equity Ratio

WACC 15.94% Weighted Average Cost of Capital

Weighted Average Cost of Capital

(Amount in PKR '000) FY14F FY15F FY16F FY17F FY18F Terminal Yr.

Profit After Tax 612,693 957,473 1,197,939 1,289,167 1,418,659

Add: Depreciation 106,913 96,752 129,323 148,349 137,529

Working Capital Changes (276,344) (619,909) (439,070) (23,829) (983,594)

Add: Interest Expense (Net of Tax) 69,416 66,099 81,674 100,357 85,823

Less: Capital Expenditure (386,646) (431,751) (399,670) (74,402) (44,402)

Free Cash Flow 126,033 68,665 570,195 1,439,643 614,015 626,296

NPV of Free Cash Flow 108,751 51,104 365,883 796,795 293,119

Free Cash Flow

Terminal Growth Rate 2.00%

Terminal WACC 15.94%

Estimated Terminal Free Cash Flow (PKR) 626,296

Terminal Value (FY2018) (PKR) 4,493,335

Terminal Value (Current) (PKR) 2,145,032

Terminal Value

NPV of Forecasts (PKR) 1,615,652

NPV of Terminal Value (PKR) 2,145,032

Enterprise Value / Cashflow Generated 3,760,684

Less: Net Debt (Net Cash as at December 31, 2013) (157,642)

Equity Value (PKR) 3,603,042

No of Shares 90,600,000

Per Share Equity Value (PKR) 39.77

DCF Valuation