initial public offeringinitial public offering€¦ · · 2012-03-09initial public...

TRANSCRIPT

Initial Public OfferingInitial Public Offering

February 2012February 2012

Forward Looking Statements

GSE Holding Inc has filed a registration statement (including a prospectus) with the SEC for the offering to which thisGSE Holding, Inc. has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GSE Holding, Inc. has filed with the SEC for more complete information about GSE Holding, Inc. and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov.

These slides and the accompanying oral presentation contain forward-looking statements and information. The use of words such “ ” “ i ht” “ ill” “ h ld” “ t” “ l ” “ ti i t ” “b li ” “ ti t ” “ j t” “i t d” “f t ” “ t ti l”as “may”, “might”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “estimate”, “project”, “intend”, “future”, “potential” or

“continued”, and other similar expressions are intended to identify forward-looking statements.

Certain statements in this presentation and responses to various questions may constitute forward-looking statements, including statements regarding the Company’s financial position, business strategy and plans and objectives of management for future operations. These statements, which contain words such as "believe,” “expect,” “anticipate,” “intends,” “estimate,” “forecast,”operations. These statements, which contain words such as believe, expect, anticipate, intends, estimate, forecast, “project,” “will,” “may,” “should” and similar expressions, reflect the beliefs and expectations of the Company and are subject to risks and uncertainties, including those described under “Risk Factors” in the registration statement, that may cause actual results to differ materially. These risks and uncertainties include, among other factors, the achievement of the anticipated levels of profitability, growth, the timely development and acceptance of new products, the impact of competitive pricing, the ability to obtain necessary regulatory approvals, and the impact of general business and global economic conditions. These and other factors could adverselyaffect the outcome and financial effects of the plans and events described herein.affect the outcome and financial effects of the plans and events described herein.

The trademarks included herein are the property of the owners thereof and are used for reference purposes only. Such use should not be construed as an endorsement of the products or services of GSE Holding, Inc. or this offering.

Neither the Company, nor any of its respective agents, employees or advisors intend or have any duty or obligation to supplement, p y, y p g , p y y y g pp ,amend, update or revise any of the forward-looking statements contained in this presentation.

The information and opinions contained in this document are provided as at the date of this presentation and are subject to change without notice. This document has not been approved by any competent regulatory or supervisory authority.

THE PIONEER OF GEOSYNTHETICS 1

This document will not be left behind after this presentation and by accepting this document and attending the presentation you agree to be bound by the foregoing limitations.

Offering Summary

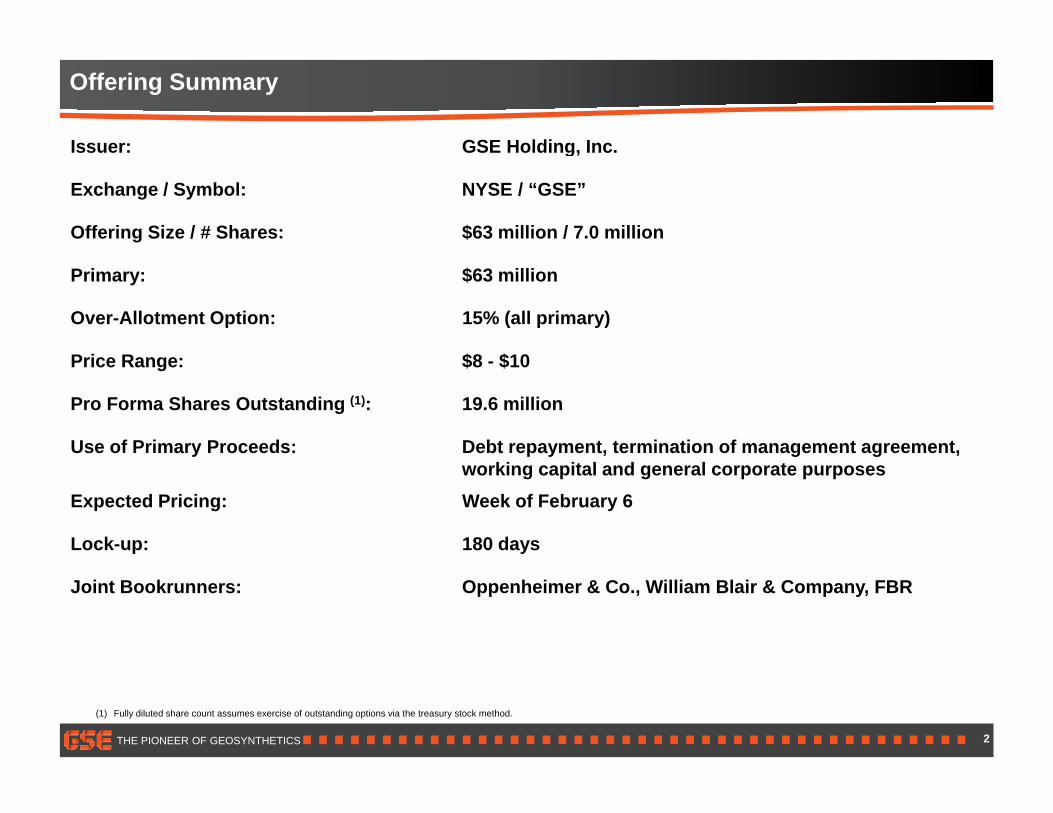

Issuer: GSE Holding, Inc.Issuer: GSE Holding, Inc.

Exchange / Symbol: NYSE / “GSE”

Offering Size / # Shares: $63 million / 7.0 million

Primary: $63 million

Over-Allotment Option: 15% (all primary)

P i R $8 $10Price Range: $8 - $10

Pro Forma Shares Outstanding (1): 19.6 million

Use of Primary Proceeds: Debt repayment, termination of management agreement, working capital and general corporate purposes

Expected Pricing: Week of February 6

Lock-up: 180 days

Joint Bookrunners: Oppenheimer & Co., William Blair & Company, FBR

THE PIONEER OF GEOSYNTHETICS 2

(1) Fully diluted share count assumes exercise of outstanding options via the treasury stock method.

Presentation Team

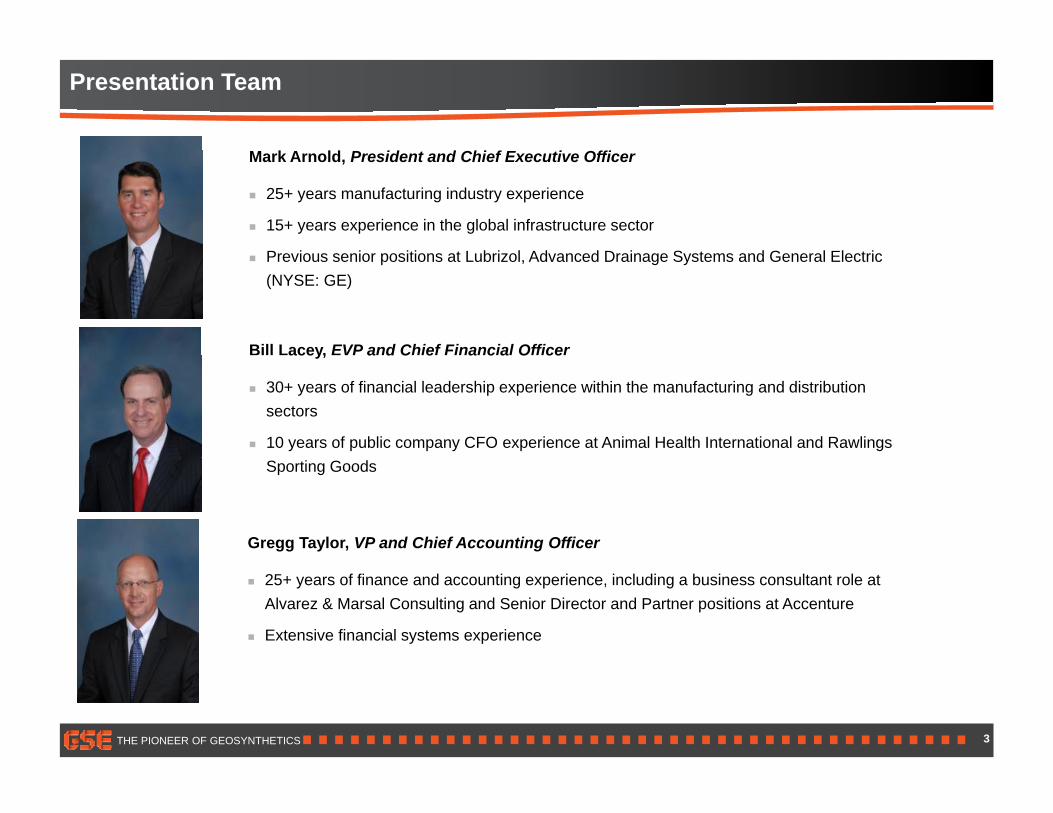

C f OffMark Arnold, President and Chief Executive Officer

25+ years manufacturing industry experience

15+ years experience in the global infrastructure sector

P i i iti t L b i l Ad d D i S t d G l El t i

Bill Lacey, EVP and Chief Financial Officer

Previous senior positions at Lubrizol, Advanced Drainage Systems and General Electric (NYSE: GE)

acey, a d C e a c a O ce

30+ years of financial leadership experience within the manufacturing and distribution sectors

10 years of public company CFO experience at Animal Health International and Rawlings Sporting Goods

Gregg Taylor, VP and Chief Accounting Officer

25+ years of finance and accounting experience, including a business consultant role at Alvarez & Marsal Consulting and Senior Director and Partner positions at Accenture

Extensive financial systems experience

THE PIONEER OF GEOSYNTHETICS 3

Who We Are

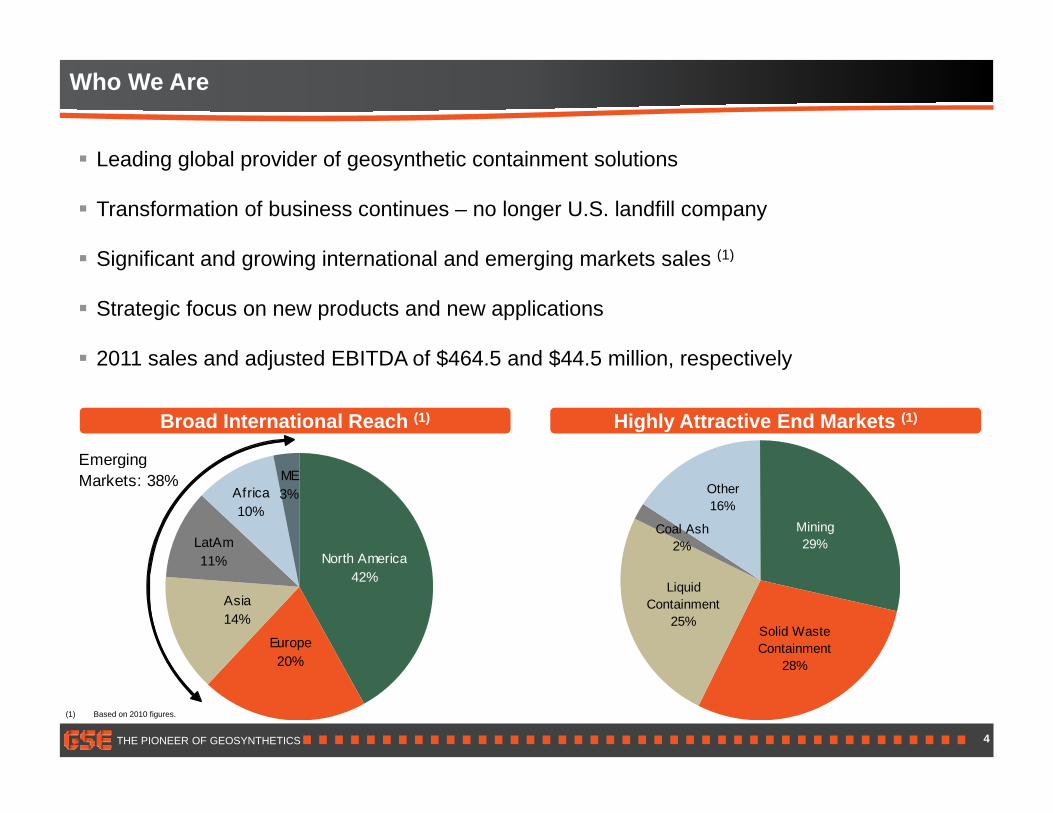

Leading global provider of geosynthetic containment solutions

Transformation of business continues – no longer U.S. landfill company

Si ifi t d i i t ti l d i k t l (1) Significant and growing international and emerging markets sales (1)

Strategic focus on new products and new applications

2011 sales and adjusted EBITDA of $464 5 and $44 5 million respectively 2011 sales and adjusted EBITDA of $464.5 and $44.5 million, respectively

Emerging

Broad International Reach (1) Highly Attractive End Markets (1)

Coal Ash2%

Other16%

Mining29%

ME3%Africa

10%

LatAm11% North America

EmergingMarkets: 38%

Solid Waste Containment

28%

Liquid Containment

25%

11%

Asia14%

Europe20%

North America42%

THE PIONEER OF GEOSYNTHETICS

28%20%

4

(1) Based on 2010 figures.

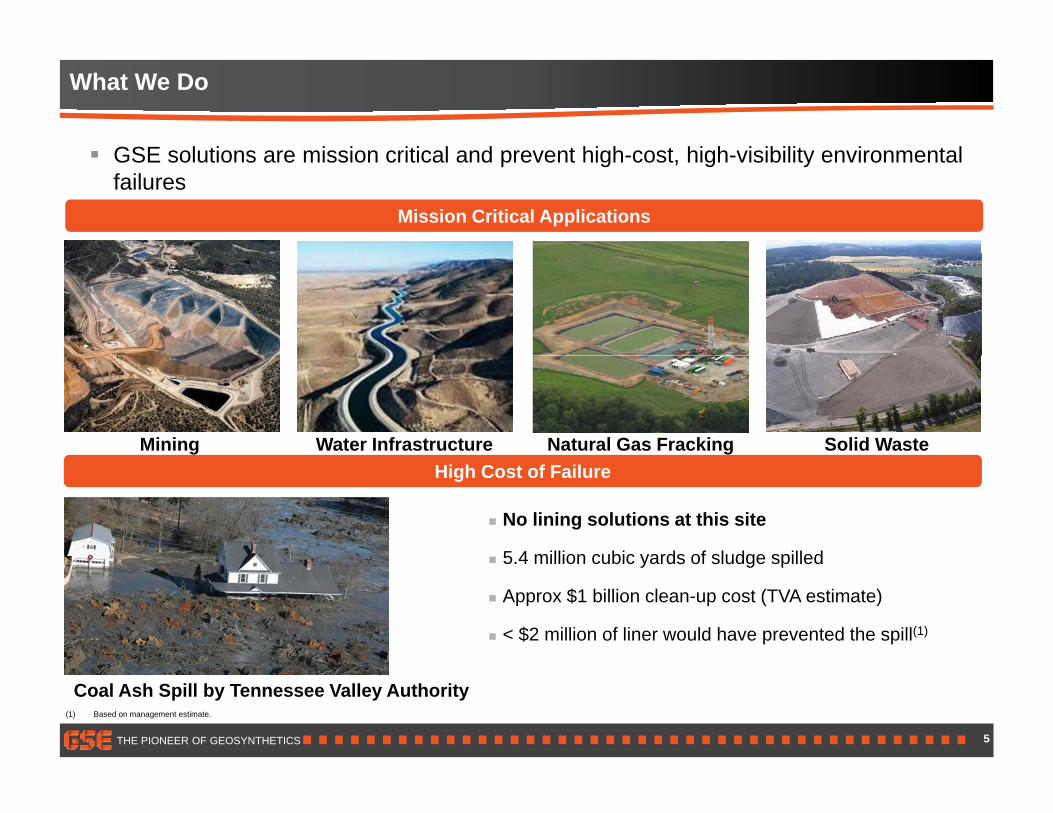

What We Do

GSE l ti i i iti l d t hi h t hi h i ibilit i t l

Mission Critical Applications

GSE solutions are mission critical and prevent high-cost, high-visibility environmental failures

Mining Water Infrastructure Natural Gas Fracking Solid Waste

No lining solutions at this site

5 4 million cubic yards of sludge spilled

High Cost of Failure

5.4 million cubic yards of sludge spilled

Approx $1 billion clean-up cost (TVA estimate)

< $2 million of liner would have prevented the spill(1)

THE PIONEER OF GEOSYNTHETICS

Coal Ash Spill by Tennessee Valley Authority(1) Based on management estimate.

5

Our Attractive End Markets Have Secular Growth Trends

Gl b l Mi i S l Emerging Markets Waste Liquid Containment –Global Mining Supercycle Emerging Markets Waste Containment

Liquid Containment Waterways

Coal AshLiquid Containment – Oil and Gas FrackingCoal AshAcquaculture Oil and Gas Fracking

THE PIONEER OF GEOSYNTHETICS 6

Our Strategy

Leverage global infrastructure to expand our leading market share in high growth geographies and end markets

Focus sales on higher value proprietary products and continued operational improvement to significantly expand marginsp g y p g

Accelerate development of new proprietary products Accelerate development of new proprietary products

C ti t d l d k t d li ti f d t Continue to develop new end markets and new applications for our products

THE PIONEER OF GEOSYNTHETICS

Selectively pursue investment and acquisition opportunities

7

Recent Developments

2011 Fi i l P f 2011 Financial Performance Revenues – $465 mm; 36% YoY increase from 2010

Gross profit – $71 mm; 61% YoY increase from 2010

Gross margin – 15.9% in 4Q11 vs 15.3% in 4Q10

EBITDA – $44.5 mm; 58% YoY increase from 2010

N t bl Hi h M i P j t S D i J 2012 Notable High Margin Project Successes During January 2012 Mining – new orders in Middle East region

Coal Ash – new impoundment with proprietary products; $7 mm orders ($8 mm sales in all of 2011)

Shale – three new customers in U.S. generate > $6 mm orders ($11 mm sales in all of 2011)

China – multiple wins generate $8 mm orders ($27 mm orders in all of 2011)

THE PIONEER OF GEOSYNTHETICS 8

Recent Developments (Cont’d)

N P i t P d t I iti ti New Proprietary Product Initiatives High performance liner – launched in international markets in December; three purchase

orders in January 2012

Conductive liner three recent international orders; first time sales in emerging markets Conductive liner – three recent international orders; first time sales in emerging markets

Coal ash – proprietary system designed into 2012 projects

Mine drain demonstration projects – commencing in emerging markets

Other Business Developments Egypt plant gains CE certification – lowest cost plant now able to serve European market

Expanded supplier base – new suppliers include Borealis and Equistar Sabic and IneosExpanded supplier base new suppliers include Borealis and Equistar, Sabic and Ineos, and Q-Chem

Conductive Liner CE Certified Egypt Plant High Density PE

THE PIONEER OF GEOSYNTHETICS 9

Recent Developments (Cont’d)

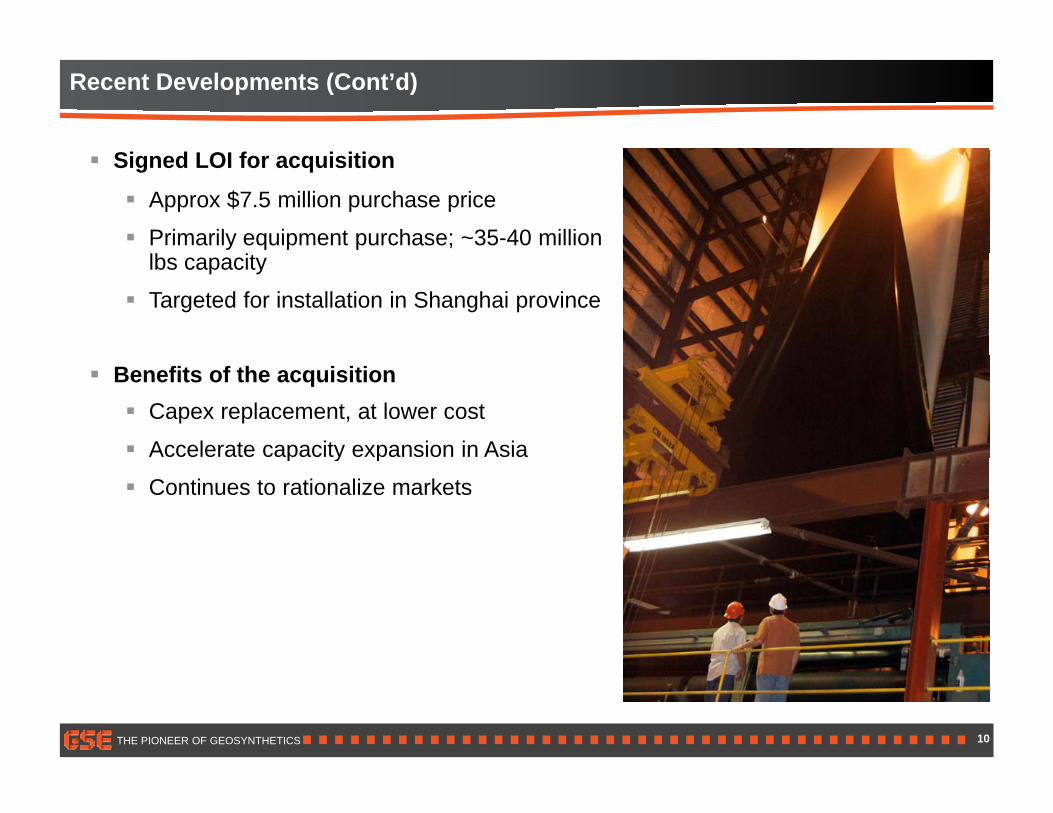

Signed LOI for acquisition Approx $7.5 million purchase price

Primarily equipment purchase; ~35-40 million lbs capacity

Targeted for installation in Shanghai province

Benefits of the acquisition Capex replacement, at lower cost

Accelerate capacity expansion in Asiap y p

Continues to rationalize markets

THE PIONEER OF GEOSYNTHETICS 10

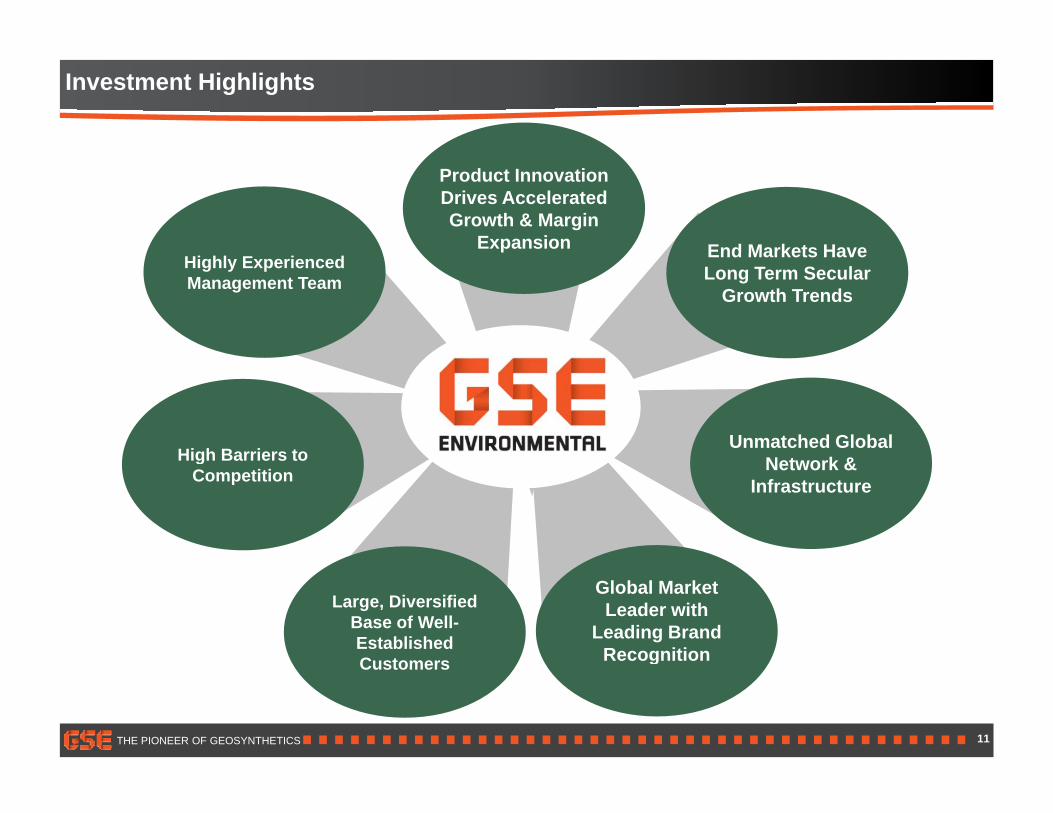

Investment Highlights

Product Innovation Drives Accelerated Growth & Margin

Expansion End Markets HaveEnd Markets Have Long Term Secular

Growth Trends

Highly Experienced Management Team

Unmatched Global N t k &High Barriers to Network &

InfrastructureHigh Barriers to

Competition

Global Market Leader with

Leading Brand Recognition

Large, Diversified Base of Well-Established Customers

THE PIONEER OF GEOSYNTHETICS 11

gCustomers

Product Innovation – Re-Engineered Core Products

Utili i l i t t 3 ti d t t t l h d d f

T t G M i2011

Utilizing polymer science to create 3-tier product strategy, launched end of 2011 and fully operational globally in mid-2012

High Performance

Target Gross Margins2011Gross Margin

EPA Spec Liner

gLiner

(“Best”)25 – 29%

~14%EPA Spec Liner(Impacting 70%

2011 Sales)

Re-EngineeredEPA Spec Liner

(“Better”)15 – 17%

300 – 400 bps gross margin improvement

Fit-For-Purpose Liner

(“Good”)17 – 21%

THE PIONEER OF GEOSYNTHETICS 12

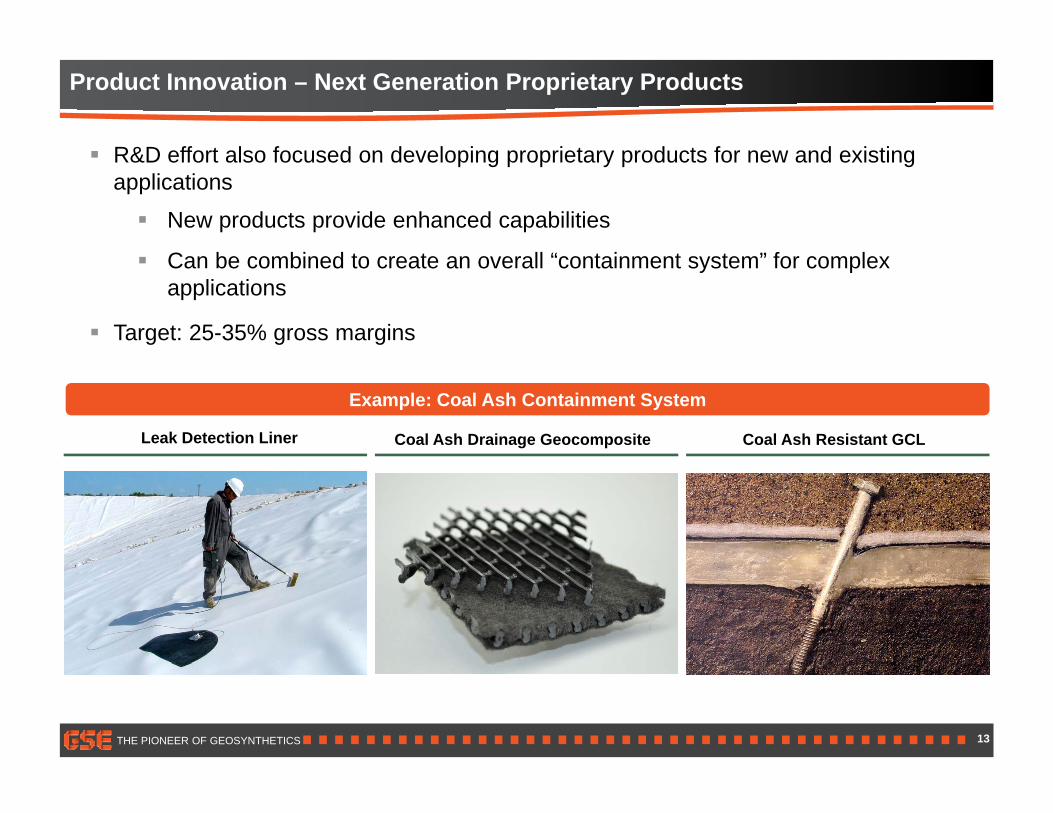

Product Innovation – Next Generation Proprietary Products

R&D ff t l f d d l i i t d t f d i ti R&D effort also focused on developing proprietary products for new and existing applications

New products provide enhanced capabilities

C b bi d t t ll “ t i t t ” f l Can be combined to create an overall “containment system” for complex applications

Target: 25-35% gross margins

Example: Coal Ash Containment System

Leak Detection Liner Coal Ash Drainage Geocomposite Coal Ash Resistant GCL

THE PIONEER OF GEOSYNTHETICS 13

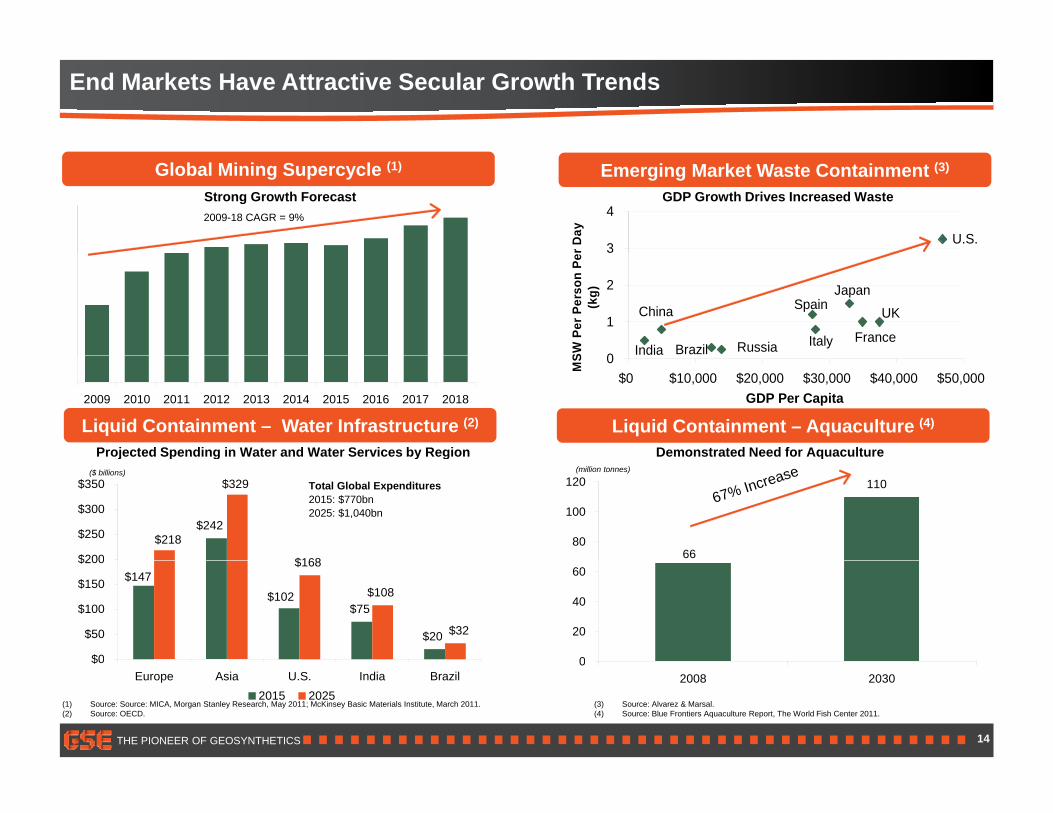

End Markets Have Attractive Secular Growth Trends

U.S.3

4

r Day

Global Mining Supercycle (1) Emerging Market Waste Containment (3)

GDP Growth Drives Increased Waste Strong Growth Forecast 2009-18 CAGR = 9%

India

China

Brazil Russia

Spain

Italy

Japan

France

UK

0

1

2

SW P

er P

erso

n Pe

(kg)

79113

132 138 141 142 140 147 160 168

0$0 $10,000 $20,000 $30,000 $40,000 $50,000

GDP Per Capita

MS

Demonstrated Need for Aquaculture

Liquid Containment – Aquaculture (4)Liquid Containment – Water Infrastructure (2)

Projected Spending in Water and Water Services by Region

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

67% Increase

66

110

80

100

120

q

$329

$168

$242$218

$200

$250

$300

$350 Total Global Expenditures2015: $770bn2025: $1,040bn

(million tonnes)($ billions)

j p g y g

0

20

40

60

$75

$20

$168

$108$147

$102

$32

$0

$50

$100

$150

$200

THE PIONEER OF GEOSYNTHETICS

02008 2030

$0Europe Asia U.S. India Brazil

2015 2025

14

(1) Source: Source: MICA, Morgan Stanley Research, May 2011; McKinsey Basic Materials Institute, March 2011. (2) Source: OECD.

(3) Source: Alvarez & Marsal.(4) Source: Blue Frontiers Aquaculture Report, The World Fish Center 2011.

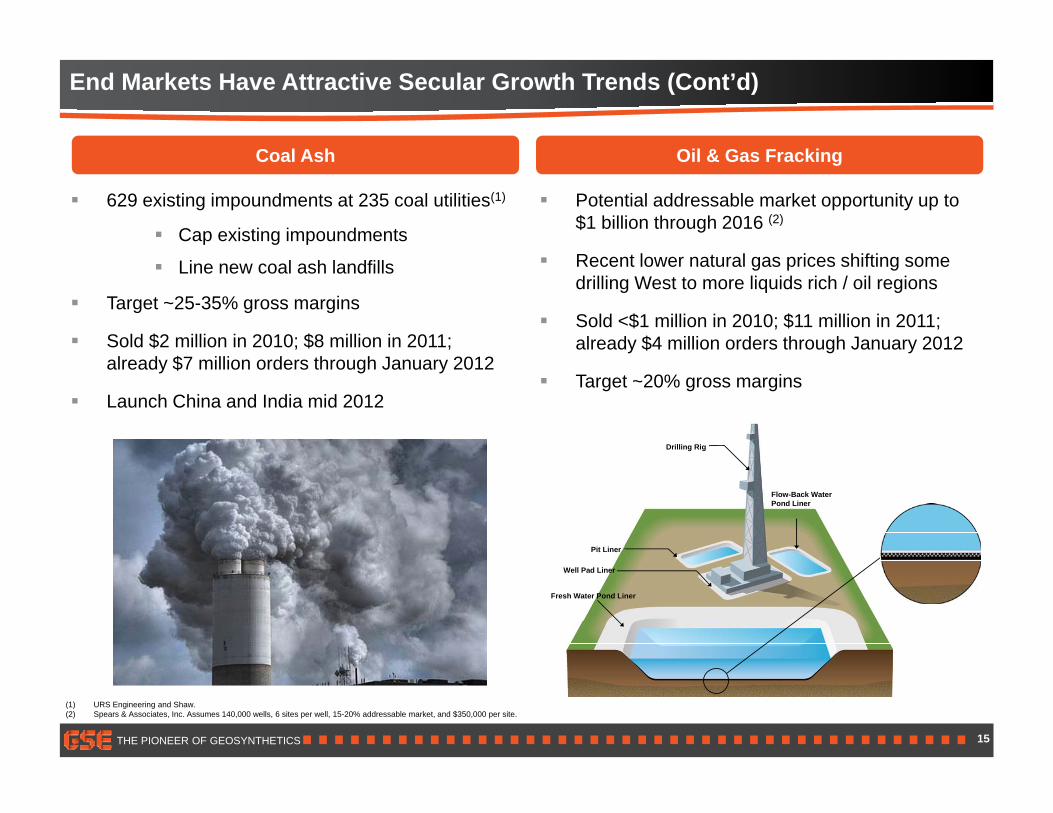

End Markets Have Attractive Secular Growth Trends (Cont’d)

Oil & G F kiC l A h Oil & Gas Fracking

629 existing impoundments at 235 coal utilities(1)

Cap existing impoundments

Potential addressable market opportunity up to $1 billion through 2016 (2)

Coal Ash

Line new coal ash landfills

Target ~25-35% gross margins

Sold $2 million in 2010; $8 million in 2011; $

Recent lower natural gas prices shifting some drilling West to more liquids rich / oil regions

Sold <$1 million in 2010; $11 million in 2011; already $4 million orders through January 2012

already $7 million orders through January 2012

Launch China and India mid 2012 Target ~20% gross margins

Drilling Rig

Flow-Back Water Pond Liner

Pit Liner

Fresh Water Pond Liner

Well Pad Liner

THE PIONEER OF GEOSYNTHETICS 15

(1) URS Engineering and Shaw.(2) Spears & Associates, Inc. Assumes 140,000 wells, 6 sites per well, 15-20% addressable market, and $350,000 per site.

Global Regulatory Climate Continues to Favor GSE Containment Solutions

United States China

Europe

Oil and gas fracking regulation – top priority among member states

Environmental protection –top priority

$28 billion for urban waste disposal (2011-2015)

Poland and UK –developing mandate of strict fracking controls

Increased regulation of groundwater activity

Coal ash management

Shale gas / fracking

Mine work tailings Middle East

Water contamination – strong regulatory framework

South America

Brazil – First national waste management law (2010)

Chil E i t l

India

Urbanization leads to increased solid waste generation

Africa Chile – Environmental

regulations and sustainability as priority

generation

Foreign investment driving increased environmental awareness

Ground water protection and consumption – top priority

Mining activities – increased environmental control

THE PIONEER OF GEOSYNTHETICS. 16

Solid waste – increased regulation

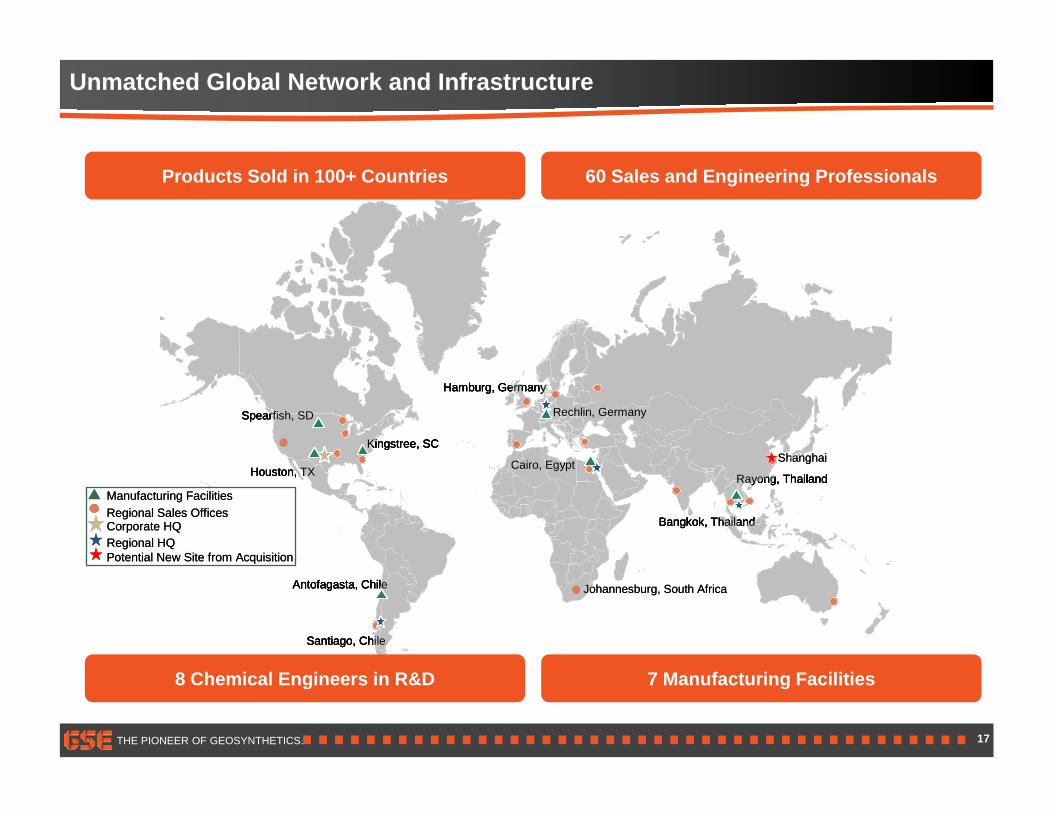

Unmatched Global Network and Infrastructure

60 Sales and Engineering ProfessionalsProducts Sold in 100+ Countries

Kingstree, SC

Spearfish, SD

Hamburg, Germany

Rechlin, Germany

Kingstree, SC

Spearfish, SD

Hamburg, Germany

Rechlin, Germany

ShanghaiKingstree, SC

Spearfish, SD

Hamburg, Germany

Rechlin, Germany

Kingstree, SC

Spearfish, SD

Hamburg, Germany

Rechlin, Germany

ShanghaiHouston, TX Cairo, Egypt

Bangkok, Thailand

Rayong, ThailandHouston, TX Cairo, Egypt

Bangkok, Thailand

Rayong, Thailand

ShanghaiHouston, TX Cairo, Egypt

Bangkok, Thailand

Rayong, ThailandHouston, TX Cairo, Egypt

Bangkok, Thailand

Rayong, Thailand

Shanghai

Corporate HQRegional HQ

Manufacturing FacilitiesRegional Sales Offices

Potential New Site from Acquisition

Corporate HQRegional HQ

Manufacturing FacilitiesRegional Sales Offices

Potential New Site from Acquisition

Antofagasta, Chile

Santiago, Chile

Antofagasta, Chile

Santiago, Chile

Johannesburg, South Africa Antofagasta, Chile

Santiago, Chile

Antofagasta, Chile

Santiago, Chile

Johannesburg, South Africa

Potential New Site from AcquisitionPotential New Site from Acquisition

THE PIONEER OF GEOSYNTHETICS.

7 Manufacturing Facilities8 Chemical Engineers in R&D

17

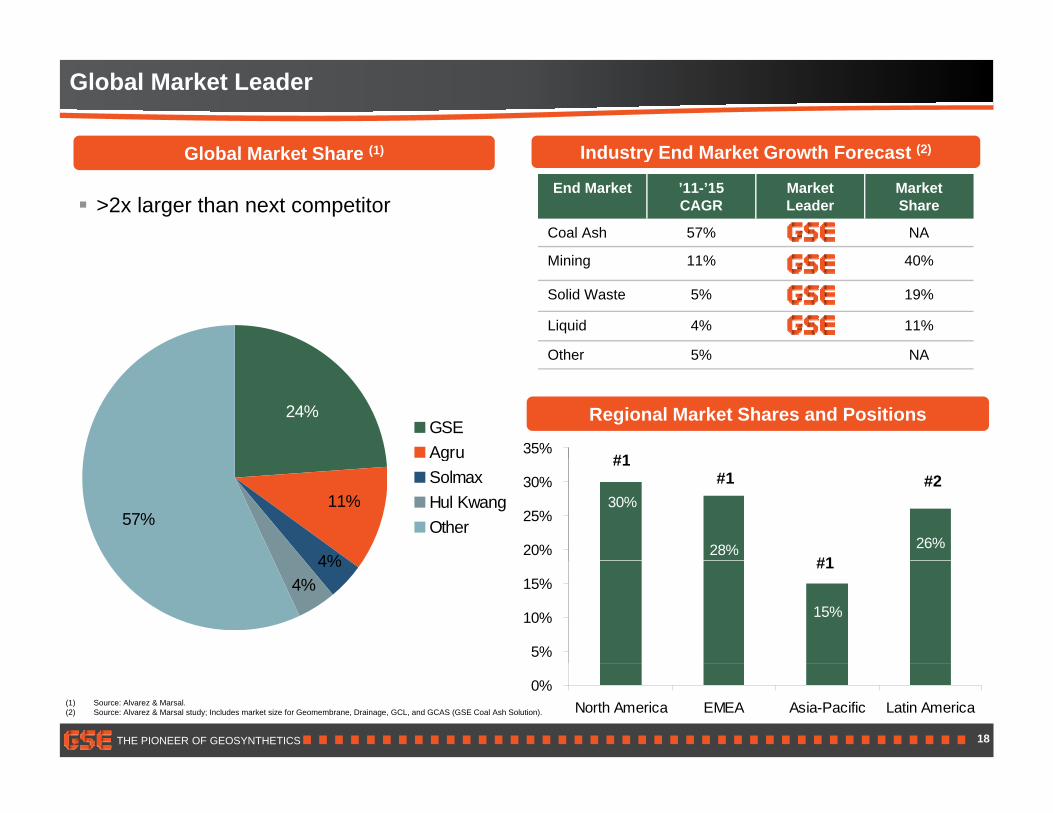

Global Market Leader

Global Market Share (1) Industry End Market Growth Forecast (2)Global Market Share (1)

>2x larger than next competitor

Industry End Market Growth Forecast (2)

End Market ’11-’15 CAGR

Market Leader

Market Share

Coal Ash 57% NA

Mining 11% 40%

Solid Waste 5% 19%

Liquid 4% 11%

Other 5% NA

Regional Market Shares and Positions24%GSEAgru 35%

#1

Other 5% NA

57%

4%

11%

g uSolmaxHul KwangOther

26%28%

30%

20%

25%

30%#1

#1

#1

#2

4%4%

15%

5%

10%

15%#1

THE PIONEER OF GEOSYNTHETICS 18

(1) Source: Alvarez & Marsal.(2) Source: Alvarez & Marsal study; Includes market size for Geomembrane, Drainage, GCL, and GCAS (GSE Coal Ash Solution).

0%North America EMEA Asia-Pacific Latin America

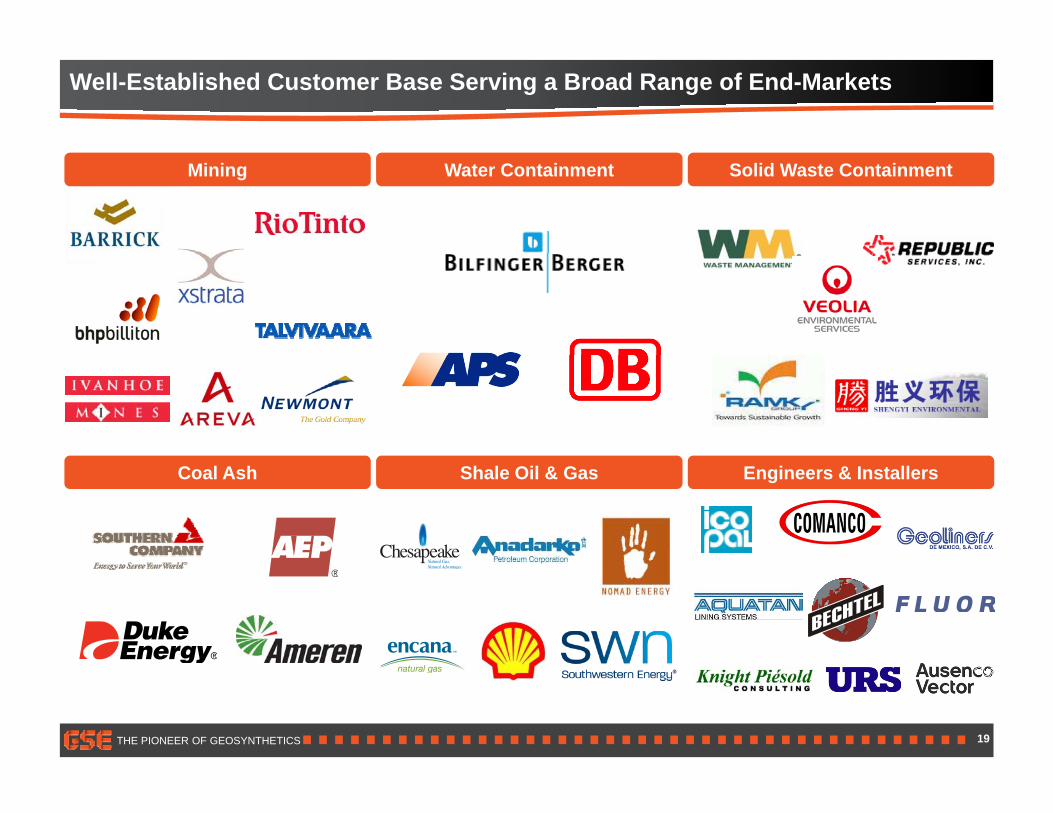

Well-Established Customer Base Serving a Broad Range of End-Markets

Mining Water Containment Solid Waste Containment

Coal Ash Shale Oil & Gas Engineers & Installers

THE PIONEER OF GEOSYNTHETICS 19

Financial Highlights

Revenue growth driven by attractive end markets, regions and regulatory mandates

High revenue visibility

Margin expansion driven by operational improvements and new products

Strong free cash flow generation

Financial flexibility to pursue growth opportunities and capacity expansion

THE PIONEER OF GEOSYNTHETICS 20

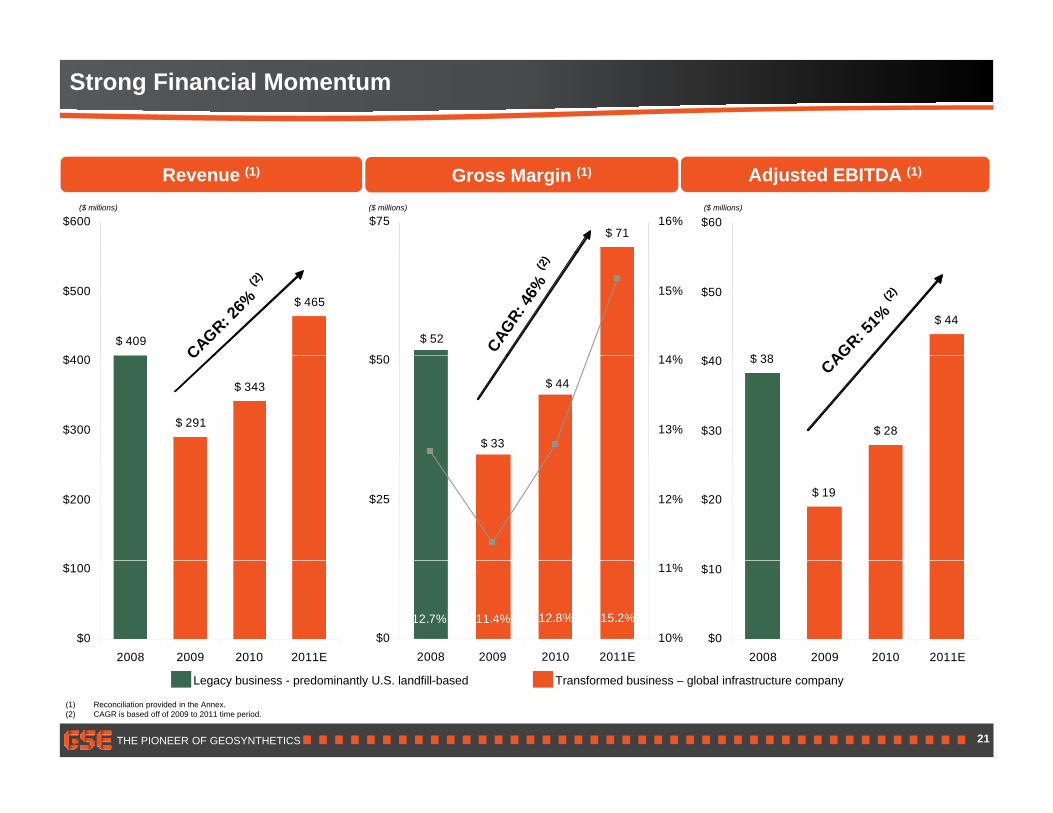

Strong Financial Momentum

Revenue (1) Adjusted EBITDA (1)Gross Margin (1)

($ millions) ($ millions) ($ millions)

$600$ 71

$75 16% $60

CAGR: 26%

(2)

$ 409

$ 465

$400

$500

CAGR:

46%

(2)

$ 52

$50 14%

15%

AGR: 51%

(2)

$ 38

$ 44

$

$50

C

$ 291

$ 343

$300

$400

$ 44

$ 33

$50

13%

14%

CAG$ 38

$ 28$30

$40

$200 $25 12% $ 19$20

$0

$100

2008 2009 2010 2011E

15.2%12.8%11.4%12.7%$0

2008 2009 2010 2011E10%

11%

$0

$10

2008 2009 2010 2011E

THE PIONEER OF GEOSYNTHETICS 21

(1) Reconciliation provided in the Annex.(2) CAGR is based off of 2009 to 2011 time period.

Legacy business - predominantly U.S. landfill-based Transformed business – global infrastructure company

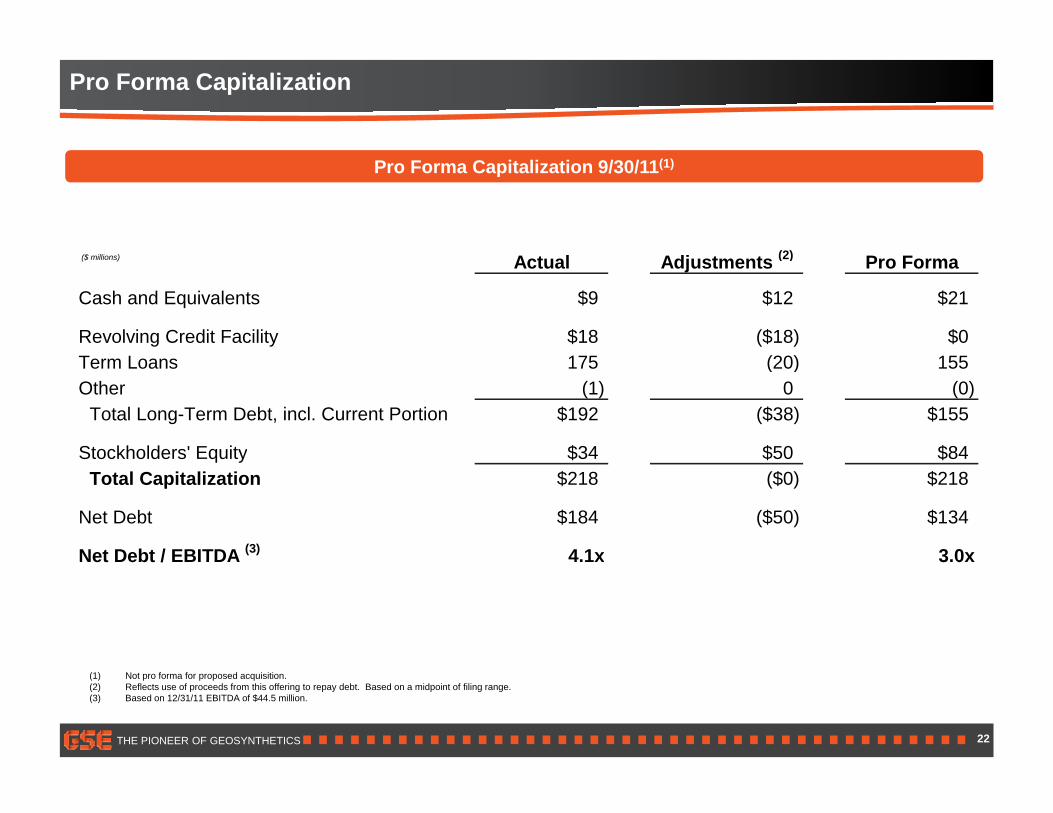

Pro Forma Capitalization

Pro Forma Capitalization 9/30/11(1)

(2)Actual Adjustments (2) Pro Forma

Cash and Equivalents $9 $12 $21

Revolving Credit Facility $18 ($18) $0T L 175 (20) 155

($ millions)

Term Loans 175 (20) 155Other (1) 0 (0)

Total Long-Term Debt, incl. Current Portion $192 ($38) $155

Stockholders' Equity $34 $50 $84Stockholders Equity $34 $50 $84Total Capitalization $218 ($0) $218

Net Debt $184 ($50) $134

Net Debt / EBITDA (3) 4.1x 3.0xNet Debt / EBITDA 4.1x 3.0x

THE PIONEER OF GEOSYNTHETICS 22

(1) Not pro forma for proposed acquisition.(2) Reflects use of proceeds from this offering to repay debt. Based on a midpoint of filing range.(3) Based on 12/31/11 EBITDA of $44.5 million.

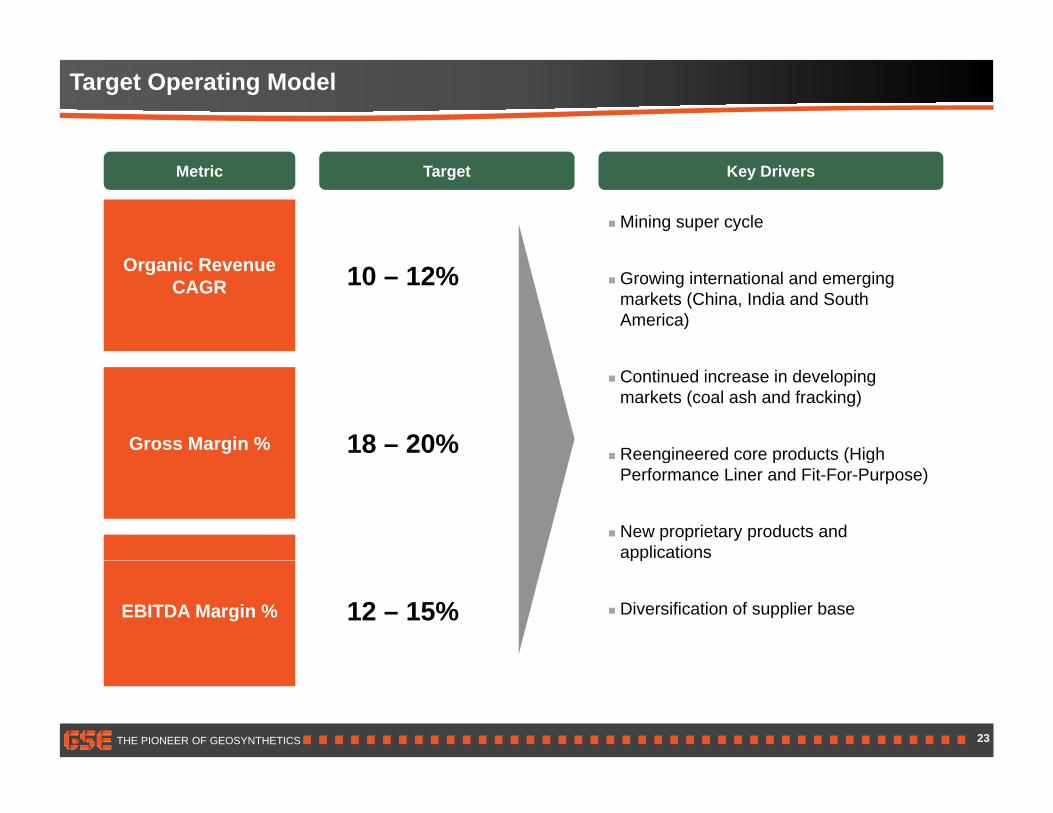

Target Operating Model

Key Drivers

Mining super cycle

Metric Target

Organic RevenueCAGR Growing international and emerging

markets (China, India and South America)

10 – 12%

Gross Margin %

Continued increase in developing markets (coal ash and fracking)

Reengineered core products (High18 – 20% Reengineered core products (High

Performance Liner and Fit-For-Purpose)

New proprietary products and applications

EBITDA Margin %

pp

Diversification of supplier base12 – 15%

THE PIONEER OF GEOSYNTHETICS 23

Y E d d D b 31Nine Months Ended

S t b 30

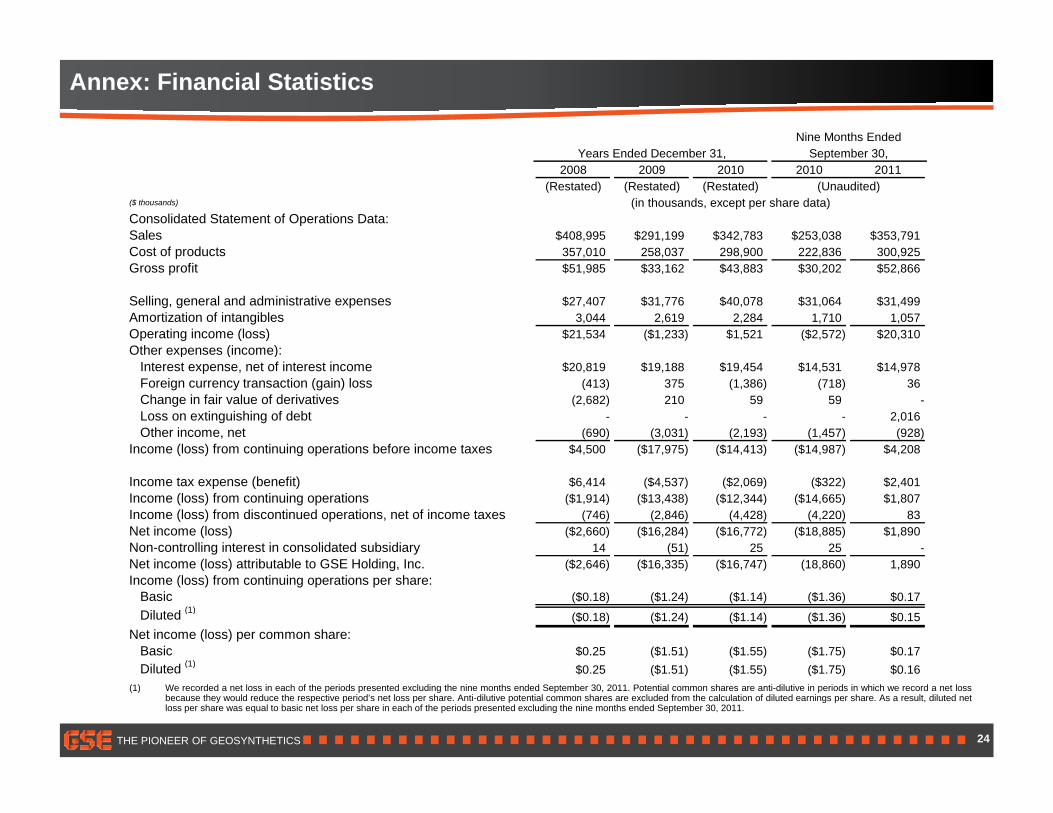

Annex: Financial Statistics

2008 2009 2010 2010 2011(Restated) (Restated) (Restated)

Consolidated Statement of Operations Data:Sales $408,995 $291,199 $342,783 $253,038 $353,791Cost of products 357 010 258 037 298 900 222 836 300 925

(in thousands, except per share data)(Unaudited)

Years Ended December 31, September 30,

($ thousands)

Cost of products 357,010 258,037 298,900 222,836 300,925Gross profit $51,985 $33,162 $43,883 $30,202 $52,866

Selling, general and administrative expenses $27,407 $31,776 $40,078 $31,064 $31,499Amortization of intangibles 3,044 2,619 2,284 1,710 1,057Operating income (loss) $21,534 ($1,233) $1,521 ($2,572) $20,310Other expenses (income):p ( )

Interest expense, net of interest income $20,819 $19,188 $19,454 $14,531 $14,978Foreign currency transaction (gain) loss (413) 375 (1,386) (718) 36Change in fair value of derivatives (2,682) 210 59 59 -Loss on extinguishing of debt - - - - 2,016Other income, net (690) (3,031) (2,193) (1,457) (928)

Income (loss) from continuing operations before income taxes $4,500 ($17,975) ($14,413) ($14,987) $4,208

Income tax expense (benefit) $6,414 ($4,537) ($2,069) ($322) $2,401Income (loss) from continuing operations ($1,914) ($13,438) ($12,344) ($14,665) $1,807Income (loss) from discontinued operations, net of income taxes (746) (2,846) (4,428) (4,220) 83Net income (loss) ($2,660) ($16,284) ($16,772) ($18,885) $1,890Non-controlling interest in consolidated subsidiary 14 (51) 25 25 -N t i (l ) tt ib t bl t GSE H ldi I ($2 646) ($16 335) ($16 747) (18 860) 1 890Net income (loss) attributable to GSE Holding, Inc. ($2,646) ($16,335) ($16,747) (18,860) 1,890Income (loss) from continuing operations per share:

Basic ($0.18) ($1.24) ($1.14) ($1.36) $0.17Diluted (1)

($0.18) ($1.24) ($1.14) ($1.36) $0.15Net income (loss) per common share:

Basic $0.25 ($1.51) ($1.55) ($1.75) $0.17(1)

THE PIONEER OF GEOSYNTHETICS

Diluted (1) $0.25 ($1.51) ($1.55) ($1.75) $0.16

24

(1) We recorded a net loss in each of the periods presented excluding the nine months ended September 30, 2011. Potential common shares are anti-dilutive in periods in which we record a net lossbecause they would reduce the respective period’s net loss per share. Anti-dilutive potential common shares are excluded from the calculation of diluted earnings per share. As a result, diluted netloss per share was equal to basic net loss per share in each of the periods presented excluding the nine months ended September 30, 2011.

Nine Months EndedY E d d D b 31 S t b 30

Annex: Financial Statistics (Cont’d)

Years Ended December 31, September 30,2008 2009 2010 2010 2011

(Restated) (Restated) (Restated)Net income (loss) attributable to GSE Holding, Inc. ($2,646) ($16,335) ($16,747) ($18,860) $1,890(Income) loss from discontinued operations, net of income taxes 746 2,846 4,428 4,220 (83)Interest expense, net of interest rate swap 20,398 18,005 18,935 14,025 14,983Income tax expense (benefit) 6 414 (4 537) (2 069) (322) 2 401

($ thousands)

Income tax expense (benefit) 6,414 (4,537) (2,069) (322) 2,401Depreciation and amortization expense 13,219 12,703 12,700 9,486 9,340Change in the fair value of derivatives (a) (2,682) 210 59 59 -Foreign currency transaction (gain) loss (b) (413) 375 (1,386) (718) 36Restructuring expense (c) - 1,444 1,096 1,183 381Professional fees (d) 262 1,436 8,904 8,462 3,143St k b d ti (e)Stock-based compensation expense (e) 450 28 67 14 75Management fees (f) 2,004 2,004 2,019 1,519 1,520Loss on extinguishment of debt (g) - - - - 2,016Other (h) 647 972 58 59 8Adjusted EBITDA $38,399 $19,151 $28,064 $19,127 $35,710

(a) Represents the mark-to-market change in the value of three interest rate swaps, including one entered into in July 2010 in connection with our German revolving credit facility, one entered into in January2005 and one in June 2009 each as a mechanism to convert $75 0 million of fixed rate debt to variable rate debt2005 and one in June 2009, each as a mechanism to convert $75.0 million of fixed rate debt to variable rate debt.

(b) Primarily related to gains and losses incurred on purchases, sales, intercompany loans and dividends denominated in non-functional currencies.

(c) Represents severance costs primarily related to the restructuring and productivity improvement programs we adopted during the fourth quarter of 2009.

(d) Represents consulting and other advisory fees related to recruiting a new chief executive officer in 2008 and 2009 and the restructuring and productivity improvement programs adopted by us during thefourth quarter of 2009, which primarily consists of fees related to the engagement of an independent consulting firm that specializes in performance improvements for portfolio companies of privateequity firms.

(e) Represents the compensation expense attributable to each respective period based on the calculated value of employee stock options.

(f) Represents management fees that will terminate in connection with this offering. See ‘‘Certain Relationships and Related Party Transactions – Management Agreement.’’

THE PIONEER OF GEOSYNTHETICS 25

(g) Represents the loss recognized in connection with the refinancing of our Senior Notes as described in ‘‘Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidityand Capital Resources – The Refinancing Transactions; Description of Long Term Indebtedness.’’

(h) 2008 and 2009 include $0.6 million of disaster recovery expense associated with Hurricane Ike and $1.0 million of death benefits paid to the estate of our former President and Chief Executive Officer,respectively. Otherwise, relates to gains and losses on asset sales.

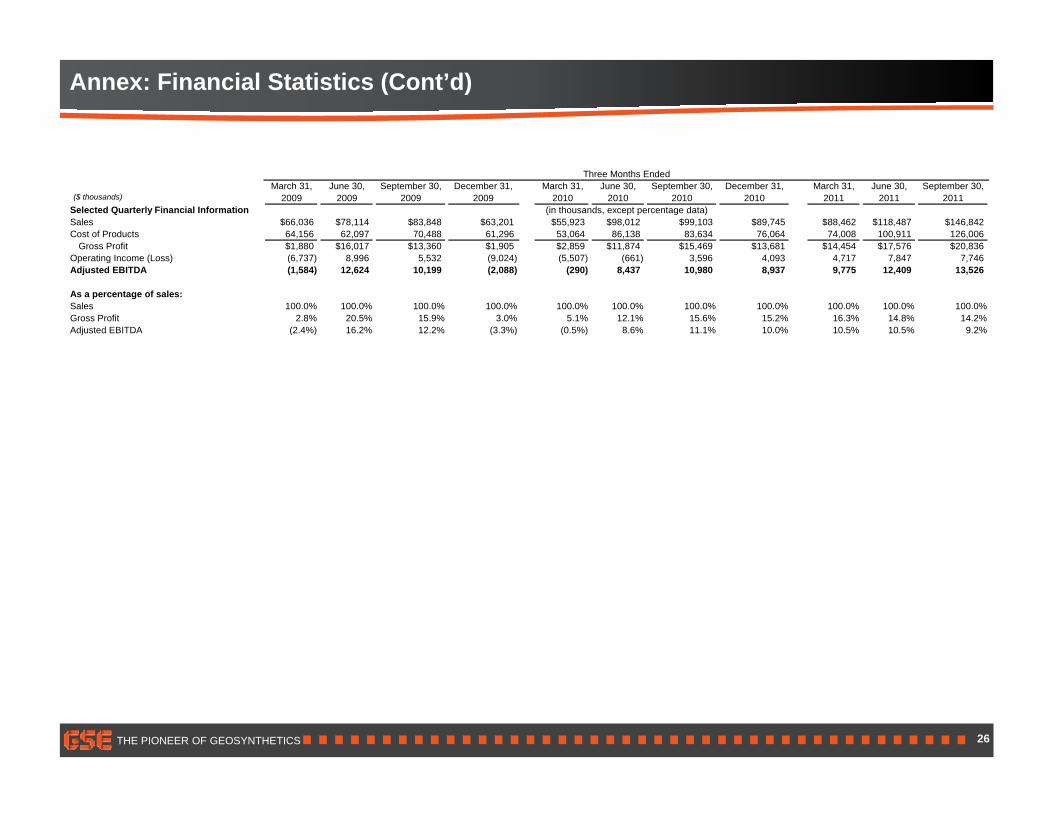

Annex: Financial Statistics (Cont’d)

($ thousands)

Three Months EndedMarch 31, June 30, September 30, December 31, March 31, June 30, September 30, December 31, March 31, June 30, September 30,

2009 2009 2009 2009 2010 2010 2010 2010 2011 2011 2011Selected Quarterly Financial Information (in thousands, except percentage data)Sales $66,036 $78,114 $83,848 $63,201 $55,923 $98,012 $99,103 $89,745 $88,462 $118,487 $146,842Cost of Products 64,156 62,097 70,488 61,296 53,064 86,138 83,634 76,064 74,008 100,911 126,006

Gross Profit $1,880 $16,017 $13,360 $1,905 $2,859 $11,874 $15,469 $13,681 $14,454 $17,576 $20,836Operating Income (Loss) (6,737) 8,996 5,532 (9,024) (5,507) (661) 3,596 4,093 4,717 7,847 7,746Adjusted EBITDA (1,584) 12,624 10,199 (2,088) (290) 8,437 10,980 8,937 9,775 12,409 13,526

As a percentage of sales:Sales 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%Gross Profit 2.8% 20.5% 15.9% 3.0% 5.1% 12.1% 15.6% 15.2% 16.3% 14.8% 14.2%Adjusted EBITDA (2.4%) 16.2% 12.2% (3.3%) (0.5%) 8.6% 11.1% 10.0% 10.5% 10.5% 9.2%

THE PIONEER OF GEOSYNTHETICS 26