innovation in audit tools & techniques - wirc in audit tools... · • it department was unable...

TRANSCRIPT

Innovation in Audit Tools & Techniques

TT

Tools & Techniques

CA Smita Gune

Agenda

Tools and Techniques

• Testing of controls

• Sampling

• Audit Reporting

• Reporting Frequency

• Audit Frequency

• Control validation

• Coordination

• Google Alert

TNovember 2011 © Anil Ashok & Associates.2

• Google Alert

• Case Studies

• Last Thoughts

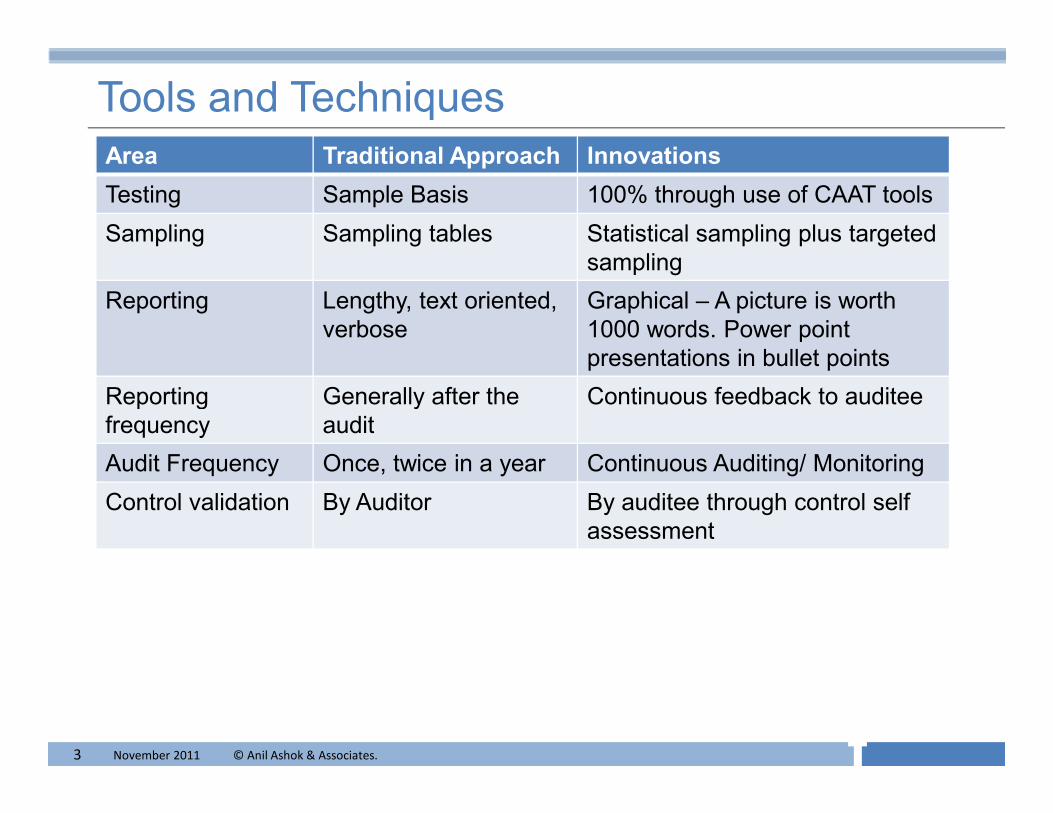

Tools and Techniques

Area Traditional Approach Innovations

Testing Sample Basis 100% through use of CAAT tools

Sampling Sampling tables Statistical sampling plus targeted

sampling

Reporting Lengthy, text oriented,

verbose

Graphical – A picture is worth

1000 words. Power point

presentations in bullet points

Reporting Generally after the Continuous feedback to auditee

TNovember 2011 © Anil Ashok & Associates.3

Reporting

frequency

Generally after the

audit

Continuous feedback to auditee

Audit Frequency Once, twice in a year Continuous Auditing/ Monitoring

Control validation By Auditor By auditee through control self

assessment

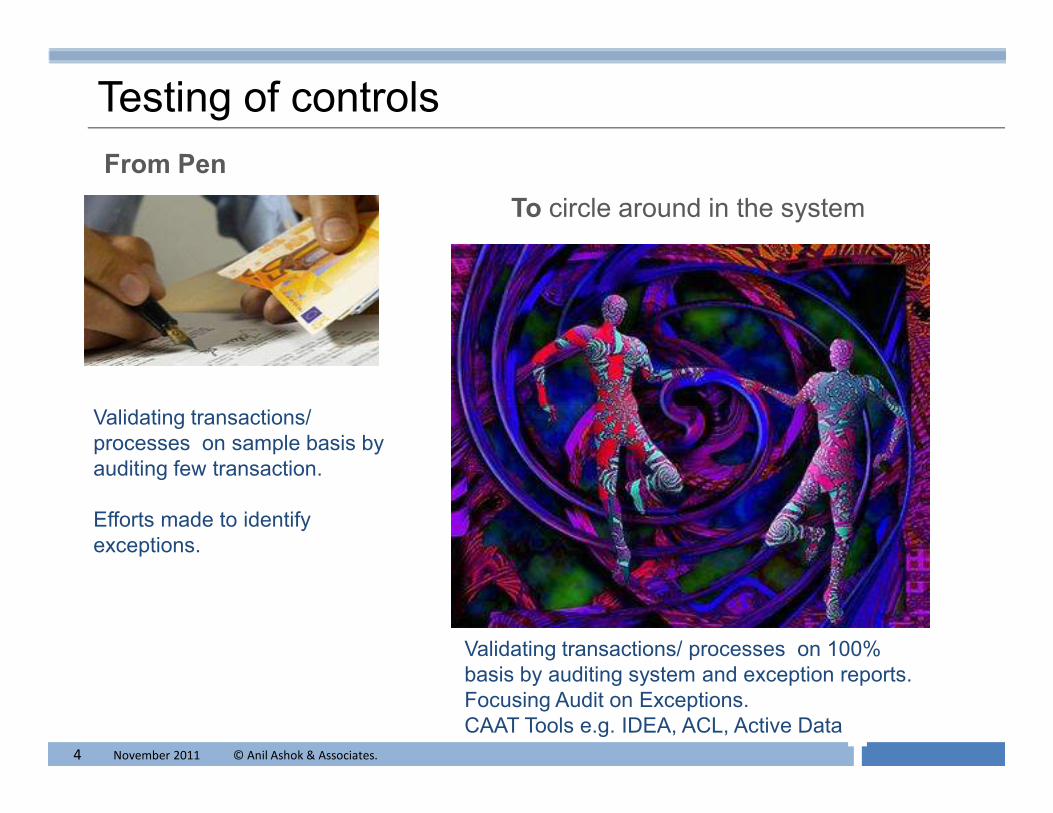

Testing of controls

From Pen

To circle around in the system

Validating transactions/

TNovember 2011 © Anil Ashok & Associates.4

Validating transactions/

processes on sample basis by

auditing few transaction.

Efforts made to identify

exceptions.

Validating transactions/ processes on 100%

basis by auditing system and exception reports.

Focusing Audit on Exceptions.

CAAT Tools e.g. IDEA, ACL, Active Data

Reporting

From Ocean of Text

To Graphical, Audio Visual

TNovember 2011 © Anil Ashok & Associates.5

To Graphical, Audio Visual

Amounts deemed to be doubtful are provided

by payroll department.

• Provision of Rs. 47.37 million is provided on

Nov. 30, 2010 – “Staff Settlement

Receivables” (net of notice period pay) of

Rs.20.87 million outstanding as of 30-Nov-

2010. The provision is therefore in excess by

Rs. 26.50 million

Balance as on November 30, 2010. (Rs. In million)

A. Staff Receivable (incl. Notice Pay

receivable)

163.56

B. Notice Pay Receivable ((amount accrued

in Nov 2010)

142.69

C. (A-B) Net Staff Receivable excl. Notice

Pay

20.87

D. Provision for Staff receivable 47.37

E. (D-C) Excess Provision 26.50

Reporting

• Efficient Audit Reporting

• Focus report on key objectives,

• Use visuals –photos, charts, maps, sketches to explain

• Cut verbosity.

• Think ‘Movie-making’ and ‘audit-making’ - Packaging and timing of products vs.

timing of fieldwork

TNovember 2011 © Anil Ashok & Associates.6

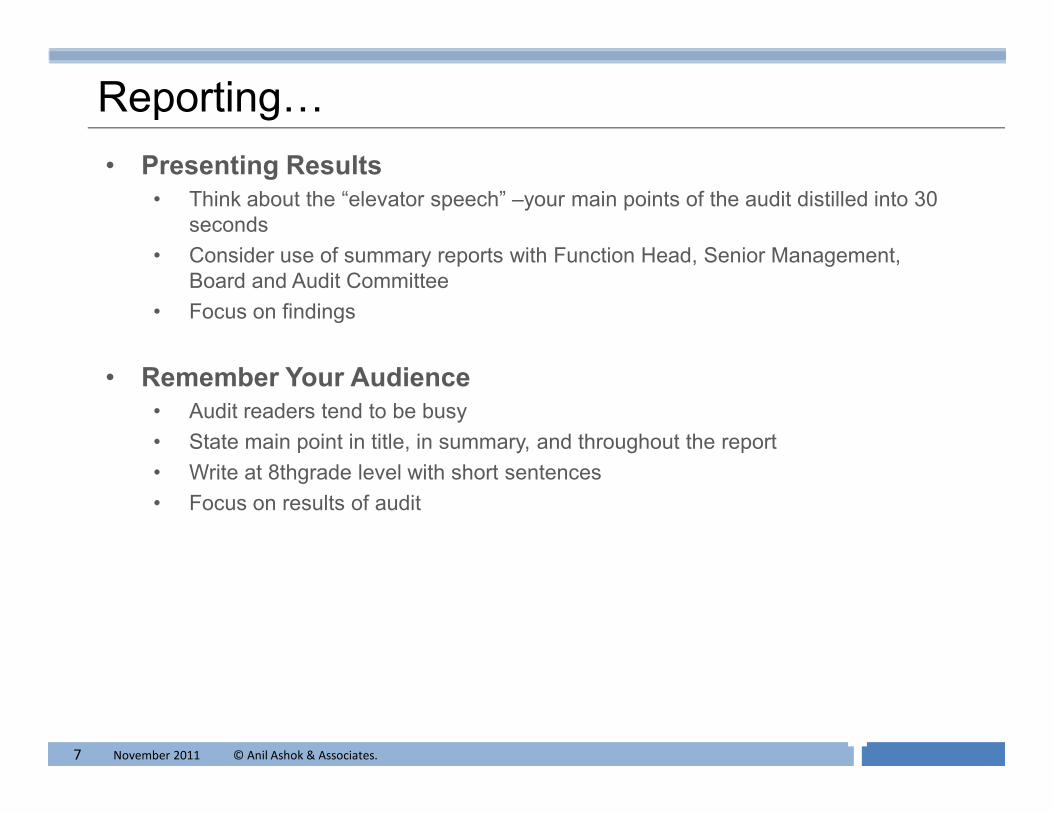

Reporting…

• Presenting Results

• Think about the “elevator speech” –your main points of the audit distilled into 30

seconds

• Consider use of summary reports with Function Head, Senior Management,

Board and Audit Committee

• Focus on findings

• Remember Your Audience

• Audit readers tend to be busy

TNovember 2011 © Anil Ashok & Associates.7

• Audit readers tend to be busy

• State main point in title, in summary, and throughout the report

• Write at 8thgrade level with short sentences

• Focus on results of audit

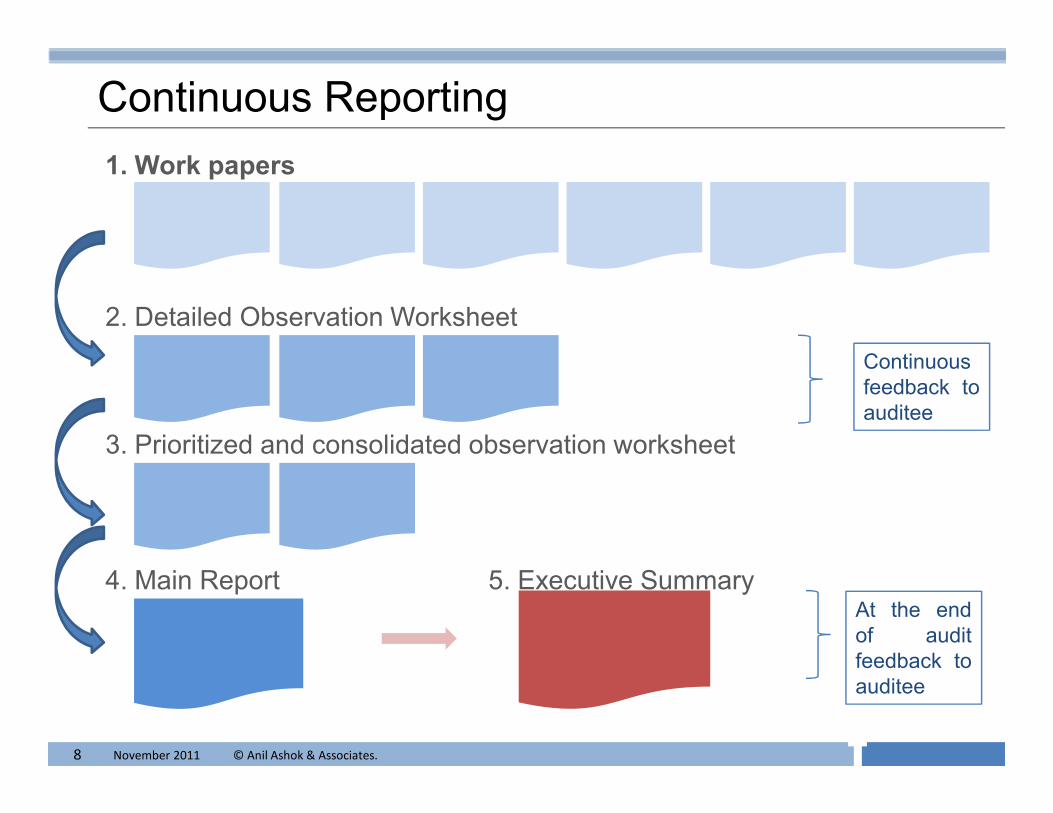

Continuous Reporting

1. Work papers

2. Detailed Observation Worksheet

Continuous

feedback to

auditee

TNovember 2011 © Anil Ashok & Associates.8

3. Prioritized and consolidated observation worksheet

4. Main Report 5. Executive Summary

auditee

At the end

of audit

feedback to

auditee

Audit Frequency

Audit calendar

24 x 7 continuous audit

TNovember 2011 © Anil Ashok & Associates.9

Creating Awareness

From holding a mirror

To Control Self Assessment

TNovember 2011 © Anil Ashok & Associates.10

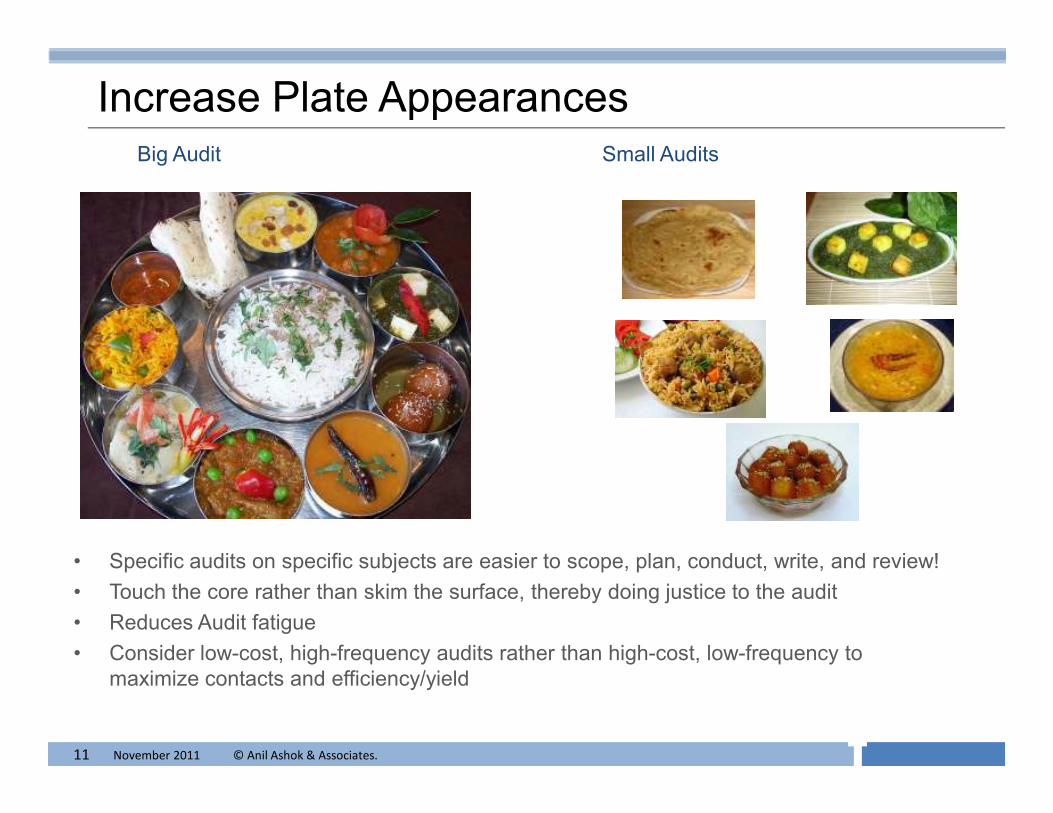

Increase Plate AppearancesBig Audit Small Audits

TNovember 2011 © Anil Ashok & Associates.11

• Specific audits on specific subjects are easier to scope, plan, conduct, write, and review!

• Touch the core rather than skim the surface, thereby doing justice to the audit

• Reduces Audit fatigue

• Consider low-cost, high-frequency audits rather than high-cost, low-frequency to

maximize contacts and efficiency/yield

Google Alert

• Google Alert

• Google offers an ‘Alert” facility based on your interest. You can define what you

want to be alerted and frequency and Google will send you alerts.

TNovember 2011 © Anil Ashok & Associates.12

Case Study 1• Risk Assessment to Risk Management

• IAD of an organisation was concerned with quality of their branch audit.

• CAE developed reports (SQL queries) based on the audit objective and started

giving these reports to branch auditors.

• Having exception reports reduced the time of the branch auditors substantially.

• As the next step, CAE provided access to these reports to branches themselves

TNovember 2011 © Anil Ashok & Associates.13

• Risk awareness in the entire organisation has increased.

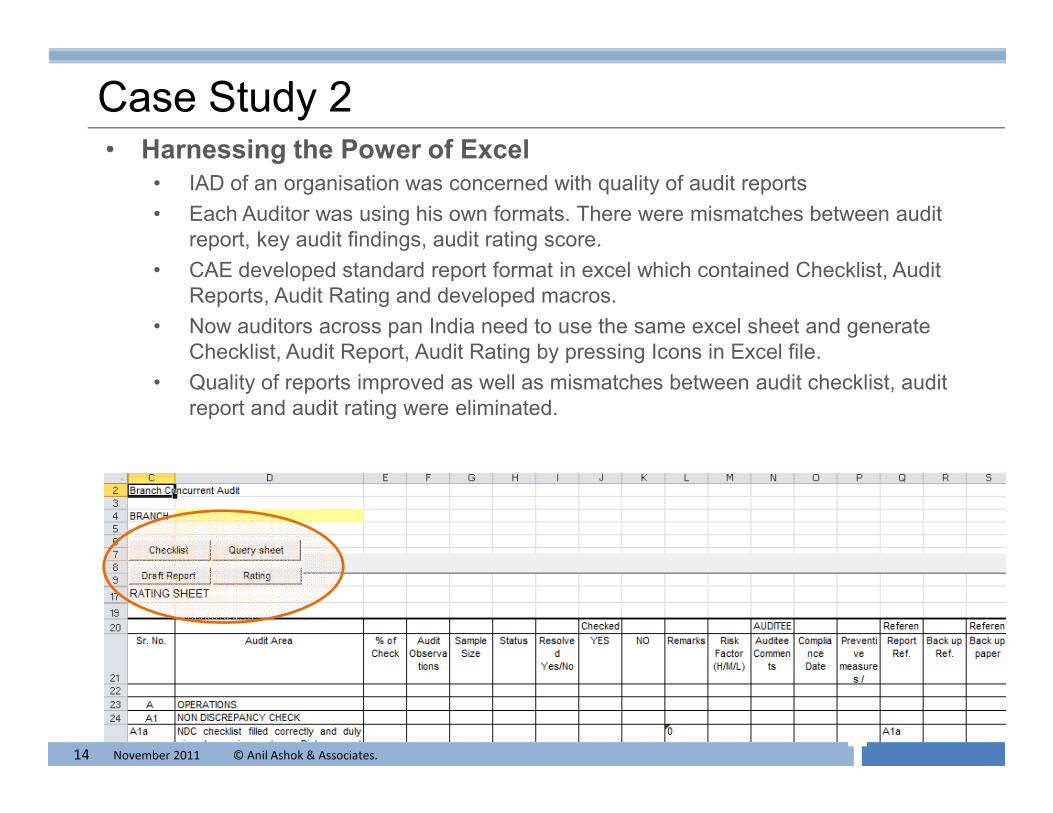

Case Study 2• Harnessing the Power of Excel

• IAD of an organisation was concerned with quality of audit reports

• Each Auditor was using his own formats. There were mismatches between audit

report, key audit findings, audit rating score.

• CAE developed standard report format in excel which contained Checklist, Audit

Reports, Audit Rating and developed macros.

• Now auditors across pan India need to use the same excel sheet and generate

Checklist, Audit Report, Audit Rating by pressing Icons in Excel file.

• Quality of reports improved as well as mismatches between audit checklist, audit

report and audit rating were eliminated.

TNovember 2011 © Anil Ashok & Associates.14

report and audit rating were eliminated.

Case Study 3• Harnessing the Power of Software

• A large organisation has over 10000 servers.

• IT department was unable to change passwords every 3 months across all

servers, fixing accountability of changes made on servers, keeping a track of

changes, costs etc.

• IT department deployed a software which now manages entire change

management aspects including password changes with complete audit trail, thus

ensuring 100% compliant with organisation polices .

TNovember 2011 © Anil Ashok & Associates.15

ensuring 100% compliant with organisation polices .

Case Study 4

• Harnessing the Power of Software

• TRAI mandates Metering and Billing System Audit (MBSA) for all telecom

service providers

• MBSA requires an external auditor to validate the accuracy of bills based on the

call information and plan opted by a consumer (called rating of call data

record(CDR).

• Software was developed to check the accuracy thereby reducing the manpower.

TNovember 2011 © Anil Ashok & Associates.16

• Software was developed to check the accuracy thereby reducing the manpower.

Quality Assurance - Looking into mirror

• ISO 9001

• Peer Review (ICAI)

• Quality assurance (IIA)

TNovember 2011 © Anil Ashok & Associates.17

An external assessment ensures that IA processes are:

1. Documented

2. Standardized

3. Work papers are in order.

4. Quality and depth of audit

TNovember 2011 © Anil Ashok & Associates.18

TNovember 2011 © Anil Ashok & Associates.19

Thank You