insurance in the obama era: the road ahead in the post-crisis world ncci annual issues symposium...

TRANSCRIPT

Insurance in the Obama Era: The Road Ahead in the

Post-Crisis World

NCCI Annual Issues SymposiumOrlando, FLMay 6, 2010

Robert P. Hartwig, Ph.D., CPCU, President & EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Reasons for Optimism in the Overall P/C Insurance Industry & Workers Comp Line

Economic Recovery is Self-Sustaining: No Double Dip Recession

Era of Mass Exposure Destruction Has Ended, Including WC Payroll Loss

No Secondary Spike in Unemployment or Swoon in Payrolls/WC Exposure But wage growth remains sluggish

Exposure Growth Will Begin in Earnest in 2nd Half 2010, Accelerate in 2011

Increase in Demand for Commercial Insurance is in its Earliest Stages and Will Accelerate in 2011, Including Workers Compensation

P/C Insurance Industry Will See Growth in 2011 for the First Time Since 2006

Investment Environment Is/Remains Much More Favorable Volatility, however, will persist and yields remain low

Both are critical issues in long-tailed lines like workers comp

P/C Insurance Industry Capacity as of 3/31/10 Has Recovered 100%+ of the Capital Lost During the Financial Crisis As of 12/31/09 capacity was within 2% of pre-crisis high

Financial Strength & Ratings of Global (Re)Insurance Industries Remained Strong Throughout the Financial Crisis in Sharp Contrast With Banks

Insurers Have Avoided (So Far) the Most Draconian Outcomes in Financial Services Reform Legislation

Source: Insurance Information Institute.

3

The Economic Storm

What the Financial Crisis and Recession Mean for the Industry’s

Exposure Base, Growth and Profitability

4

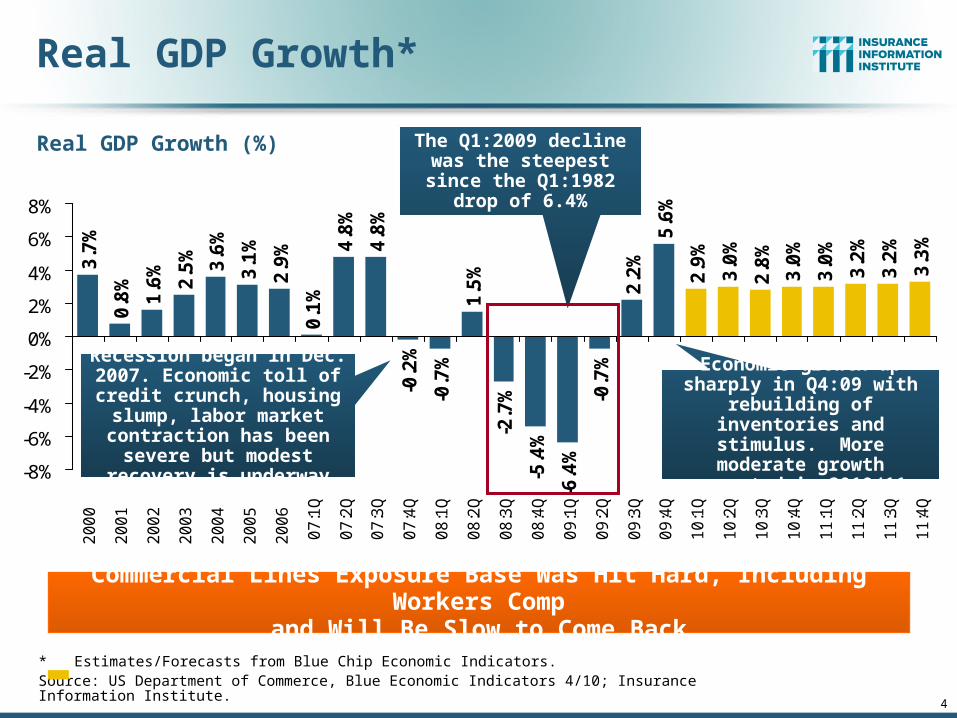

Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 4/10; Insurance Information Institute.

2.9

%

0.1

%

4.8

%

4.8

%

-0.2

%

-0.7

%

1.5

%

-2.7

%

-5.4

%

-6.4

%

-0.7

%

2.2

%

5.6

%

2.9

%

3.0

%

2.8

%

3.0

%

3.0

%

3.2

%

3.2

%

3.3

%

3.7

%

0.8

%

1.6

%

2.5

% 3.6

%

3.1

%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

Commercial Lines Exposure Base Was Hit Hard, Including Workers Compand Will Be Slow to Come Back

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit

crunch, housing slump, labor market contraction has

been severe but modest recovery is underway

The Q1:2009 decline was the steepest since the Q1:1982 drop of 6.4%

Economic growth up sharply in Q4:09 with rebuilding of inventories and stimulus.

More moderate growth expected in 2010/11

5

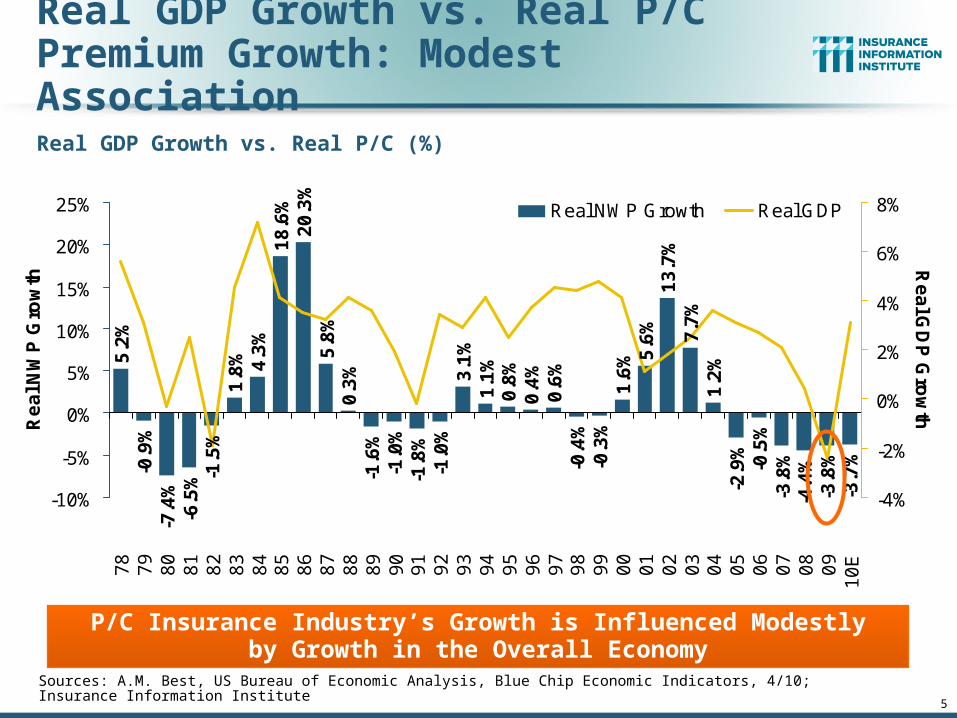

Real GDP Growth vs. Real P/CPremium Growth: Modest Association

Sources: A.M. Best, US Bureau of Economic Analysis, Blue Chip Economic Indicators, 4/10; Insurance Information Institute

4.3

%1

8.6

%2

0.3

%5

.8%

0.3

%-1

.6%

-1.0

%-1

.8%

-1.0

%3

.1%

1.1

%0

.8%

0.4

%0

.6%

-0.4

%-0

.3%

1.6

% 5.6

%1

3.7

%7

.7%

1.2

%-2

.9%

-0.5

%-3

.8%

-4.4

%-3

.8%

-3.7

%

5.2

%-0

.9%

-7.4

%-6

.5% -1

.5%

1.8

%

-10%

-5%

0%

5%

10%

15%

20%

25%

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

E

Re

al N

WP

Gro

wth

-4%

-2%

0%

2%

4%

6%

8%

Re

al G

DP

Gro

wth

Real NWP Growth Real GDP

P/C Insurance Industry’s Growth is Influenced Modestlyby Growth in the Overall Economy

Real GDP Growth vs. Real P/C (%)

6

Regional Differences Will Significantly Impact P/C Markets and Growth Opportunities in WC

Recovery in Some Areas Will Begin Years Ahead of Others

and Speed of Recovery Will Differ by Orders of Magnitude

7

State Economic Growth Varied Tremendously in 2008

US Bureau of Economic Analysis

Highest Quintile

Fourth Quintile

Third Quintile

Second Quintile

Lowest Quintile

Far West0.6

Rocky Mountain2.2

Southwest1.7

Plains2.0 Great Lakes

-0.4

New England1.0

Mideast1.3

Southeast0.0

US = 0.7

WA2.0

OR1.6

CA0.4

NV-0.6

ID0.0

MT1.8

WY4.4

UT1.4 CO

2.9

AZ-0.6 NM

2.0

TX2.0

OK2.7

KS2.2

NE1.3

SD3.5

ND7.3 MN

2.0

IA2.1

MO1.3

WI0.7

IL0.3

MI-1.5

IN-0.6

OH-0.7

NY1.6

PA1.1

NJ0.6

MD1.3

DE-1.6

DC3.0VA

1.3

WV2.5

KY-0.1

NC0.1

SC0.6

TN0.5

AR0.7

LA0.3

MS1.7

AL0.7

GA-0.6

FL-1.6

AK-2.0

HI0.7

ME1.4

NH1.8

VT1.7 MA

1.9

RI-0.9CT

-0.4

Mountain, Plains States Growing the Fastest

Percent Change in Real GDP by State, 2007–2008

8

Fastest Growing States in 2008:Plains, Mountain States Lead

2.1% 2.0%

7.3%

4.4%

3.5%2.9% 2.7% 2.5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

ND WY SD CO OK WV IA TX, MN,NM, WA

Source: US Bureau of Economic Analysis; Insurance Information Institute.

Real State GDP Growth (%)

Natural Resource and Agricultural States Have Done Better Than Most Others Recently, Helping Insurance Exposure in Those Areas

9

Slowest Growing States in 2008: Diversity of States Suffering

Source: US Bureau of Economic Analysis; Insurance Information Institute.

States in the North, South, East and West All Represented Among Hardest Hit, But for Differing Reasons

Real State GDP Growth (%)

-0.9%

-1.5%-1.6% -1.6%

-1.7%

-2.0%

-0.1%

-0.4%-0.6% -0.6% -0.6% -0.6%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%KY CT AZ GA IN NV RI MI DE FL OH AK

10

Labor Market Trends

Massive Job Losses Sapped the Workers Comp Exposure Base, but Improvements Are on the Horizon

11

Unemployment and UnderemploymentRates: Beginning to Improve in 2010

2

4

6

8

10

12

14

16

18

Jan 00 Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10

Traditional Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

Mar10

10.1% Oct 2009 unemployment rate (U-3) was

the highest monthly rate since 1983.

Peak rate in the last 30 years: 10.8% in Nov -

Dec 1982

Stood at 9.7% in Mar. 2010.

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in Oct 2009; Stood at 16.9% in Mar.

2010

January 2000 through March 2010, Seasonally Adjusted (%)

Recession ended in

November 2001

Unemployment kept rising for

19 more months

Recession began in

December 2007

12

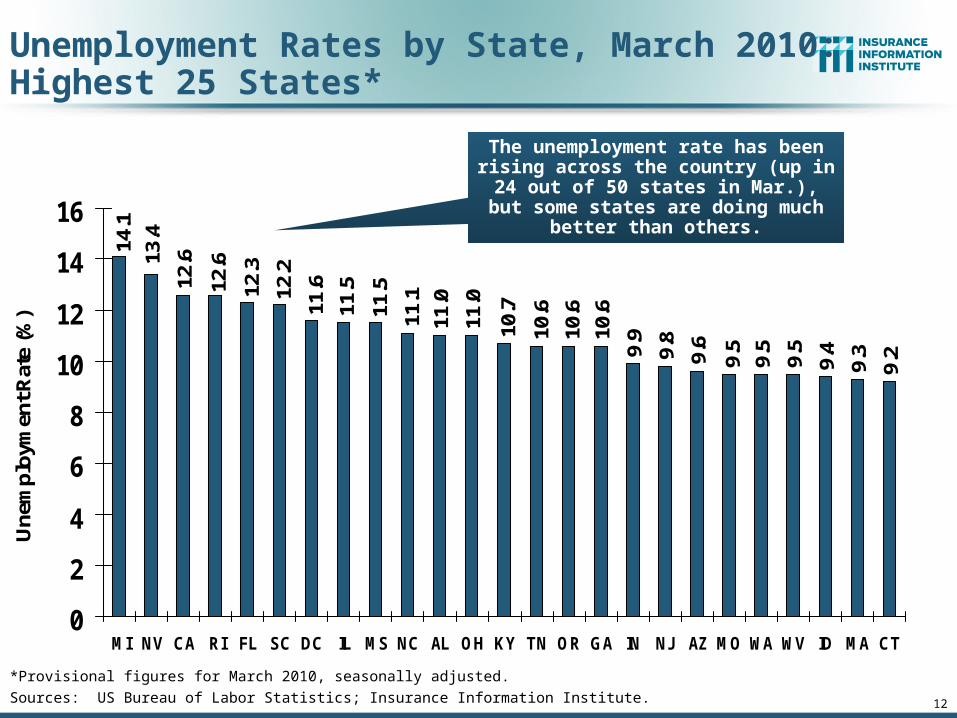

Unemployment Rates by State, March 2010:Highest 25 States*

10.6

9.911

.0

10.6

10.6

10.7

9.5

9.5

9.5

9.29.6

9.3

9.49.8

11.612

.3

11.0

11.1

11.5

11.512

.2

13.4

12.6

12.6

14.1

0

2

4

6

8

10

12

14

16

MI NV CA RI FL SC DC IL MS NC AL OH KY TN OR GA IN NJ AZ MO WA WV ID MA CT

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for March 2010, seasonally adjusted.

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

The unemployment rate has been rising across the country (up in 24 out of 50 states in Mar.), but some states are

doing much better than others.

13

6.9

6.8

6.6

6.57.

07.17.

47.

4

4.85.0

6.57.

27.3

4.0

6.9

8.28.

7

7.7

7.8

7.98.

28.69.

0

8.8

8.89.

2

0

2

4

6

8

10

DE PA NM WI NY AK ME TX CO AR MD MN VA WY UT MT NH LA HI IA OK VT KS NE SD ND

Une

mpl

oym

ent R

ate

(%)

Unemployment Rates By State, March 2010: Lowest 25 States*

*Provisional figures for March 2010, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

The unemployment rate has been rising across the country (up in 24 out of 50 states in Mar.), but some states are

doing much better than others.

14

US Unemployment Rate

4.5

%

4.5

%

4.6

%

4.8

%

4.9

% 5.4

% 6.1

%

6.9

%

8.1

%

9.3

%

9.6

% 10

.0%

9.7

%

9.7

%

9.6

%

9.3

%

9.1

%

8.9

%

8.6

%

9.4

%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

:Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

Rising unemployment eroded payrolls

and workers comp’s exposure base.

Unemployment likely peaked at 10% in late 2009.

* = actual; = forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (4/10); Insurance Information Institute

2007:Q1 to 2011:Q4F*

Unemployment forecasts are being

revised downward for the first time in years

15

Monthly Change Employment*-7

2

-14

4

-12

2

-16

0

-13

7

-16

1

-12

8

-17

5

-32

1

-38

0

-59

7

-68

1

-77

9

-72

6

-75

3

-52

8 -38

7

-51

5 -34

6 -21

2

-22

5

-22

4

64

-10

9

14

-14

16

2

-1,000

-800

-600

-400

-200

0

200

400

Jan

08

Fe

b 0

8

Ma

r 0

8

Ap

r 0

8

Ma

y 0

8

Jun

08

Jul 0

8

Au

g 0

8

Se

p 0

8

Oct

08

No

v 0

8

De

c 0

8

Jan

09

Fe

b 0

9

Ma

r 0

9

Ap

r 0

9

Ma

y 0

9

Jun

09

Jul 0

9

Au

g 0

9

Se

p 0

9

Oct

09

No

v 0

9

De

c 0

9

Jan

10

Fe

b 1

0

Ma

r 1

0

Monthly Losses in Dec–May Were the

Largest in the Post-WW II Period

.Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Job Losses Since the Recession Began in Dec. 2007 Total 8.4 Million; 14.9 Million People are Now Defined as Unemployed

January 2008 through March 2010 (Thousands)

March’s gain of 162,000 jobs was the best in 3 years;

Labor market recoveries are often erratic.

Estimated Effect of Recessions* on Payroll (Workers Comp Exposure)

*Data represent maximum recorded decline over 12-month period using annualized quarterly wage and salary accrual dataSource: Insurance Information Institute research; Federal Reserve Bank of St. Louis (wage and salary data); National Bureau of Economic Research (recession dates).

-4.4%

-2.0%-1.1%

1.1%

3.7%4.6%

8.5%

3.5%

2.1%

-0.5%

-3.6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1948-1949

1953-1954

1957-1958

1960-1961

1969-1970

1973-1975

1980 1981-1982

1990-1991

2001 2007-2009

Recessions in the 1970s and 1980s saw smaller exposure impacts

because of continued wage inflation, a factor not present

during the 2007-2009 recession

The Dec. 2007 to mid-2009 recession

caused the largest impact on WC

exposure in 60 years

(Percent Change)

(All Post WWII Recessions)

Recession Dates (Beginning/Ending Years)

17

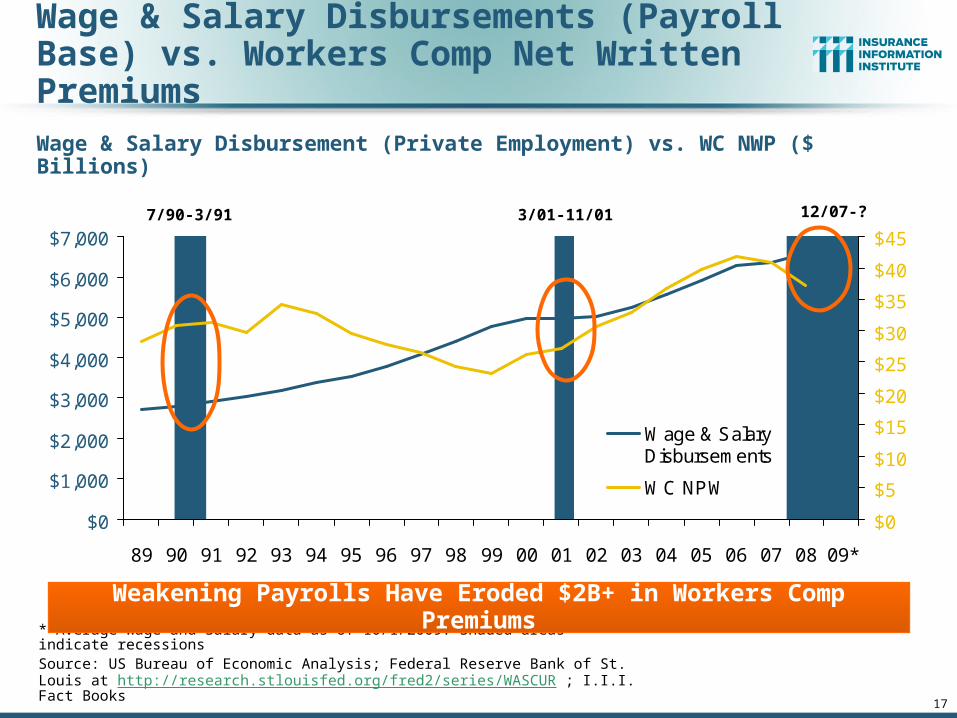

Wage & Salary Disbursement (Private Employment) vs. WC NWP ($ Billions)

Wage & Salary Disbursements (Payroll Base) vs. Workers Comp Net Written Premiums

* Average Wage and Salary data as of 10/1/2009. Shaded areas indicate recessionsSource: US Bureau of Economic Analysis; Federal Reserve Bank of St. Louis at http://research.stlouisfed.org/fred2/series/WASCUR ; I.I.I. Fact Books

Weakening Payrolls Have Eroded $2B+ in Workers Comp Premiums

7/90-3/91 3/01-11/01 12/07-?

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09*

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Wage & SalaryDisbursements

WC NPW

Where Will the Growth in WC Exposure Come From?

18

Industry and Occupation Growth Analysis

19

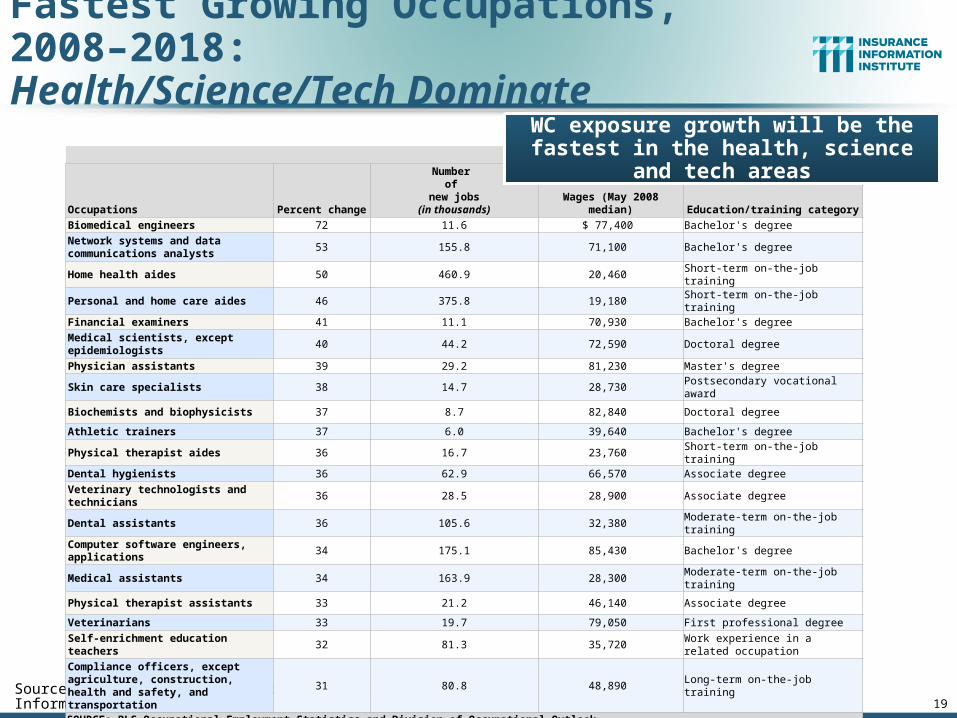

Fastest Growing Occupations, 2008–2018:Health/Science/Tech Dominate

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

OccupationsPercent change

Number of

new jobs(in thousands)

Wages (May 2008 median) Education/training category

Biomedical engineers 72 11.6 $ 77,400 Bachelor's degree

Network systems and data communications analysts

53 155.8 71,100 Bachelor's degree

Home health aides 50 460.9 20,460 Short-term on-the-job training

Personal and home care aides 46 375.8 19,180 Short-term on-the-job training

Financial examiners 41 11.1 70,930 Bachelor's degree

Medical scientists, except epidemiologists

40 44.2 72,590 Doctoral degree

Physician assistants 39 29.2 81,230 Master's degree

Skin care specialists 38 14.7 28,730 Postsecondary vocational award

Biochemists and biophysicists 37 8.7 82,840 Doctoral degree

Athletic trainers 37 6.0 39,640 Bachelor's degree

Physical therapist aides 36 16.7 23,760 Short-term on-the-job training

Dental hygienists 36 62.9 66,570 Associate degree

Veterinary technologists and technicians

36 28.5 28,900 Associate degree

Dental assistants 36 105.6 32,380 Moderate-term on-the-job training

Computer software engineers, applications

34 175.1 85,430 Bachelor's degree

Medical assistants 34 163.9 28,300 Moderate-term on-the-job training

Physical therapist assistants 33 21.2 46,140 Associate degree

Veterinarians 33 19.7 79,050 First professional degree

Self-enrichment education teachers

32 81.3 35,720 Work experience in a related occupation

Compliance officers, except agriculture, construction, health and safety, and transportation

31 80.8 48,890 Long-term on-the-job training

SOURCE: BLS Occupational Employment Statistics and Division of Occupational Outlook

WC exposure growth will be the fastest in the health, science and tech areas

20

Occupations with Largest Numerical Growth, 2008–2018: Health, Services Dominate

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

Dollar growth in WC exposures should grow the most (at current rate levels) in the health and services industries

Occupations

Number of

new jobs(in thousands) Percent change

Wages (May 2008 median) Education/training category

Registered nurses 581.5 22 $ 62,450 Associate degree

Home health aides 460.9 50 20,460 Short-term on-the-job training

Customer service representatives 399.5 18 29,860 Moderate-term on-the-job training

Combined food preparation and serving workers, including fast food

394.3 15 16,430 Short-term on-the-job training

Personal and home care aides 375.8 46 19,180 Short-term on-the-job training

Retail salespersons 374.7 8 20,510 Short-term on-the-job training

Office clerks, general 358.7 12 25,320 Short-term on-the-job training

Accountants and auditors 279.4 22 59,430 Bachelor's degree

Nursing aides, orderlies, and attendants

276.0 19 23,850 Postsecondary vocational award

Postsecondary teachers 256.9 15 58,830 Doctoral degree

Construction laborers 255.9 20 28,520 Moderate-term on-the-job training

Elementary school teachers, except special education

244.2 16 49,330 Bachelor's degree

Truck drivers, heavy and tractor-trailer

232.9 13 37,270 Short-term on-the-job training

Landscaping and groundskeeping workers

217.1 18 23,150 Short-term on-the-job training

Bookkeeping, accounting, and auditing clerks

212.4 10 32,510 Moderate-term on-the-job training

Executive secretaries and administrative assistants

204.4 13 40,030 Work experience in a related occupation

Management analysts 178.3 24 73,570 Bachelor's or higher degree, plus work experience

Computer software engineers, applications

175.1 34 85,430 Bachelor's degree

Receptionists and information clerks

172.9 15 24,550 Short-term on-the-job training

Carpenters 165.4 13 38,940 Long-term on-the-job trainingSOURCE: BLS Occupational Employment Statistics and Division of Occupational Outlook

21

Is Workers Compensation Claim Severity at Risk of Accelerating?

Inflation Trends:Could Rising Deficits, Bailouts &

Stimulus Spark Inflation?

22

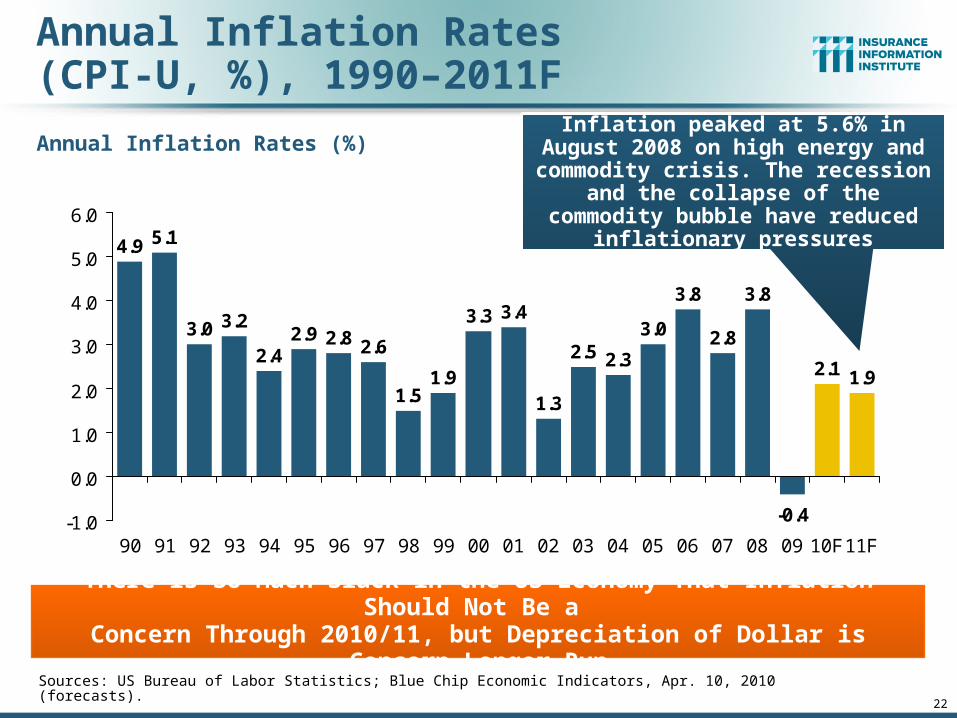

Annual Inflation Rates(CPI-U, %), 1990–2011F

2.8 2.6

1.51.9

3.3 3.4

1.3

2.5 2.3

3.0

3.8

2.8

3.8

-0.4

2.1 1.9

2.92.4

3.23.0

5.14.9

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10F11F

Sources: US Bureau of Labor Statistics; Blue Chip Economic Indicators, Apr. 10, 2010 (forecasts).

There is So Much Slack in the US Economy That Inflation Should Not Be a Concern Through 2010/11, but Depreciation of Dollar is Concern Longer Run

Annual Inflation Rates (%) Inflation peaked at 5.6% in August 2008 on high energy and commodity crisis. The recession and the collapse of the

commodity bubble have reduced inflationary pressures

WC Insurers Experience Inflation More Intensely than 2009 CPI Suggests

Source: Bureau of Labor Statistics; Insurance Information Institute.

2.7%

1.8%

6.9%

3.0% 3.0%3.4%

3.1%3.4%

0%

2%

4%

6%

8%

Overall CPI "Core" CPI HospitalServices

Physicians'Services

DentalServices

PrescriptionDrugs

Medical CareCommodities

Medical CPI

(Percent increase Dec 08 to Dec 09)

Healthcare Costs Are a Major WC Insurance Cost Driver. They AreLikely to Increase Faster than the CPI for the Next Few Years, at Least

23

Excludes Food and Energy

Inpatient Services Rose 6.7%;

Outpatient Services Rose 7.4%

P/C Insurance Financial Performance

24

A Resilient Industry in Challenging Times

P/C Net Income After Taxes1991–2009 ($ Millions)

$14,1

78

$5,8

40

$19,3

16

$10,8

70

$20,5

98

$24,4

04 $36,8

19

$30,7

73

$21,8

65

$3,0

46

$30,0

29

$62,4

96

$3,0

43

$28,3

11

-$6,970

$65,7

77

$44,1

55

$20,5

59

$38,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.3% 2009 ROAS1 = 5.8%

* ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 7.3% ROAS for 2009 and 4.4% for 2008. 2009 net income was $34.5 billion and $20.8 billion in 2008 excluding M&FG.Sources: A.M. Best, ISO, Insurance Information Institute

P-C Industry profits for full-year 2009 were up sharply from 2008, but are still well

below pre-crisis levels

Property/Casualty Insurance Industry Investment Gain: 1994–20091

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.0

$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09

Investment Gains Fell by 50% In 2008 Due to Lower Yields,Poor Equity Market Conditions. In 2009, the Lower Realized Capital Losses

Helped Offset Lower Investment Income

1 Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.* 2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

($ Billions)

A 100 Combined Ratio Isn’t What ItOnce Was: 90-95 is Where It’s At Now

Combined Ratio / ROE

* 2009/2008 figures are return on average statutory surplus. 2008 and 2009 figures exclude mortgage and financial guaranty insurersSource: Insurance Information Institute from A.M. Best and ISO data

97.5

100.6 100.1 100.7

92.6

99.3101.0

7.3%

9.6%

15.9%

14.3%

12.7%

4.4%

8.9%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2008* 2009*0%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s DepressedInvestment Environment to Generate Risk Appropriate ROEs

Combined ratio of about 100 generated a 6% ROE in 2009, 10%

in 2005 and16% in 1979

29

Reduction in Combined Ratio Necessary to Offset 1% Decline in Investment Yield to Maintain Constant ROE, by Line*

*Based on 2008 Invested Assets and Earned Premiums**US domestic reinsurance only.Source: A.M. Best; Insurance Information Institute.

Lower Investment Earnings Place a Greater Burden on Underwriting Performance

-3.1%-3.3%-3.3%-3.7%

-4.3%

-5.2%-5.7%

-7.3%

-1.8%-1.8%-2.0%

-3.6%

-1.9%-2.1%

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

The long-tailed nature of workers comp means that it is more sensitive to changes in

investment yield

30

-10%

-5%

0%

5%

10%

15%

20%

25%

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

10F

Strength of Recent HardMarkets by NWP Growth

(Percent)1975-78 1984-87 2000-03

Shaded areas denote “hard market” periodsSources: A.M. Best (historical and forecast), ISO, Insurance Information Institute

Net Written Premiums Fell 0.7% in 2007 (First Decline Since 1943) by 2.0% in 2008, and 3.7% in 2009, the First 3-Year Decline Since 1930-33

During the Great Depression. Expected decline of 1.6% in 2010.

Good News

P/C insurance industry should

see positive growth in 2011

for the first time since 2006

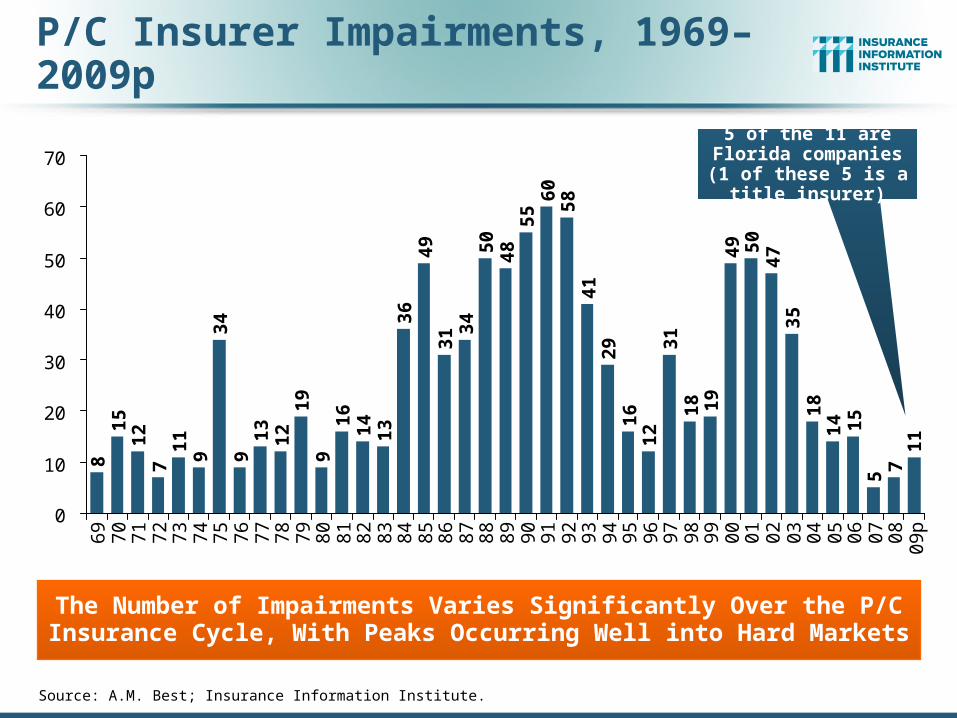

P/C Insurer Impairments, 1969–2009p8

15

12

71

19

34

91

31

21

99

16

14

13

36

49

31 3

45

04

85

56

05

84

12

91

61

23

11

8 19

49 50

47

35

18

14 15

71

1

5

0

10

20

30

40

50

60

70

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

p

Source: A.M. Best; Insurance Information Institute.

The Number of Impairments Varies Significantly Over the P/C Insurance Cycle, With Peaks Occurring Well into Hard Markets

5 of the 11 are Florida companies (1 of these

5 is a title insurer)

Capacity/Capital/PolicyholderSurplus (US)

32

Shrinkage During Crisis, but Not Enough to Trigger Hard Market

Capacity Has Been 100% Restored to Pre-Crisis Levels

33

Policyholder Surplus, 2006:Q4–2009:Q4

Source: ISO, AM Best.

($ Billions)

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$490.8

$511.5$505.0

$515.6$517.9

$380

$400

$420

$440

$460

$480

$500

$520

$540

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4

Capacity Peaked at $521.8 as of 9/30/07

Declines Since 2007:Q3 Peak

08:Q2: -$16.6B (-3.2%) 08:Q3: -$43.3B (-8.3%) 08:Q4: -$66.2B (-12.9%)09:Q1: -$84.7B (-16.2%)

09:Q2: -$58.8B (-11.2%)09:Q3: -$31.8B (-5.9%)09:Q4: -$2.5B (-0.5%)

Capacity as of 12/31/09 was just 2.0% below the 2007 peak and will likely set a new record in 2010

34

U.S. P/C Insurance-RelatedM&A Activity, 1988–2009

$2$5

$19

$1 $0

$20

$0

$9

$35

$14$16

$4

$56

$31

$8$12

$2$3 $3 $5$6

$40

$0

$10

$20

$30

$40

$50

$60

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Tra

ns

ac

tio

n V

alu

e (

$ B

illio

n)

0

20

40

60

80

100

120

140

Nu

mb

er o

f Tra

ns

ac

tion

s

Transaction Values

Number of Transactions

Note: U.S. Company was the acquirer and/or target.

Source: Conning Research & Consulting.

2010: No Mega Deals So Far, Despite Record Capital, Slow Growth and Improved

Financial Market Conditions

$ Value of Deals Down 78% in 2009, Volume Up 7%

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwig

Insurance Information Institute Online: